Embed Size (px)

DESCRIPTION

Eric Böss, Christoph Mast and Kent Rossiter Allianz Global Investors | GlobalTrading 2016 Quarter 1

Citation preview

GLOBALTRADINGFIXGLOBAL.COM

Global Edition

Subscribe at www.fixglobal.com

EMEA Edition

In support of

Q1 • 2016 • Issue #57

ALSO INSIDE: AXA IM, BARINGS, IIROC, ACORN CAPITAL, SEQUOIA CAPITAL FUND MANAGEMENT, VANGUARD, IOSCO, CAPITAL GROUP

Building A Global FirmEric Böss, Christoph Mast and Kent Rossiter

Allianz Global Investors

Emma QuinnAB

Carlos OliveiraBrandes Investment Partners

Greg LeeBarclays

Dear Readers,As we know, the traditional institutional trading paradigm is supported by multiple business, operational, technology and regulatory components, functions and people. But from a critical path perspective this paradigm involves the communication between portfolio managers, buy- and sell-side traders and markets / sources of liquidity. Over several years, and as technology, FIX and other factors have evolved how these parties interact, they still remain the primary entities in the equation. Nevertheless, a snapshot of global electronic trading and the electronic products as used in the trading process today would likely inspire a “future shock” reaction from someone involved at the time FIX was first launched. Liquidity access is no longer limited just to exchanges, brokers are becoming more innovative in how they service their buy-side clients, and the buy-side is focusing on how both its portfolio managers and traders can make better, more informed investment and trading decisions.

In parallel to the ongoing developments in institutional trading, the regulatory powers in many regions are considerably refocusing on how they define their roles and activities in an effort to both service the industry and fulfill their obligations to the public.

In this edition of GlobalTrading we have several contributions relating to the above. Allianz Global Investors has kindly provided views on building a global firm in today’s environment including trading desks, trading systems, regulations, asset classes, TCA and working with brokers. We also have perspectives on the roles of regulators, cross border regulations and the prospect of international reporting standards from some noted regional and global authorities. Additionally, we are grateful for articles addressing trading in small caps, the impact of mutual funds on bond trading and analyzing the cost of FX trades.

Please enjoy this edition of GlobalTrading. As always we appreciate your interest, support and contributions to GlobalTrading and the FIX Trading Community.

Best Regards,

Bill HebertAlpha Omega Financial Systems, Inc.Co-Chair, Global Member Services Committee, FIX Trading Community

GlobalTrading’s Editorial Think Tank

Bill HebertAlpha Omega Financial Systems, Inc.Co-Chair, FIX Trading Community Global Membership Services Committee

GlobalTrading PublisherEdward Mangles

General ManagerRebecca Trant

Managing EditorPeter Waters

Sales and MarketingYulia KuksinaRavi GangwaniJane Lenny

PhotographerRosemarie Conway

Publishers’ NoteGlobalTrading is proudly published by HM Publishing in support of the FIX Protocol and the FIX Trading Community. GlobalTrading is the official quarterly publication of the the FIX Trading Community, however, the content does not necessarily represent the opinions of the FIX Trading Community.

The opinions expressed in this publication are not necessarily those of the publishers or of the institutions of the contributing author. Although care has been taken to ensure the accuracy of the information contained within the publication, neither the publishers, authors nor their employers can be held liable for any inaccuracies, errors or omissions; nor held liable for any actions taken on the basis of the views expressed, or information provided within this publication. No part of this publication covered by the publisher’s copyright may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, be they graphic, electronic or mechanical, including photocopying, without the written permission of the publisher. Any unauthorised use of this publication will result in immediate legal proceedings.

All Rights Reserved © 2016

Design & LayoutGoldie Lee

General [email protected]

AdvertisingCompanies interested in discussing sponsorship and/or advertising opportunities please contact your regional editorial representative or [email protected].

PublisherHM Publishing2802, 28/F Lippo Centre Tower Two89 Queensway, Admiralty, Hong KongTel: 852 2121 1566 Fax: 852 3007 3821

We Put the Dash in Dashboard.Buy-side Optimized Workflow on Eikon streamlines your workflow of directing trades into the market, all in a single view.Enter any security and see all this on the dashboard:

• Who you’ve traded it with over the past 30 days

• Which brokers are most active in it

• Which firms cover it and their StarMine® rankings

See how Buy-side Optimized Workflow helps you target the best way to move and manage your trades.

To access, type BOW in your Eikon toolbar.

Visit financial.thomsonreuters.com/eikon

© 2015 Thomson Reuters. S025012/11-15 Thomson Reuters and the Kinesis logo are trademarks of Thomson Reuters.

PERSONALIZED 30 DAY TRADE

HISTORY

STARMINE ANALYSTS RANKINGS

TODAY’S BROKER RANKING

20 DAY BROKER

RANKING

TRADE HISTORY

CHART TODAY’S ACTIVE IOIs

S025012_v10.indd 1 03/11/2015 12:48

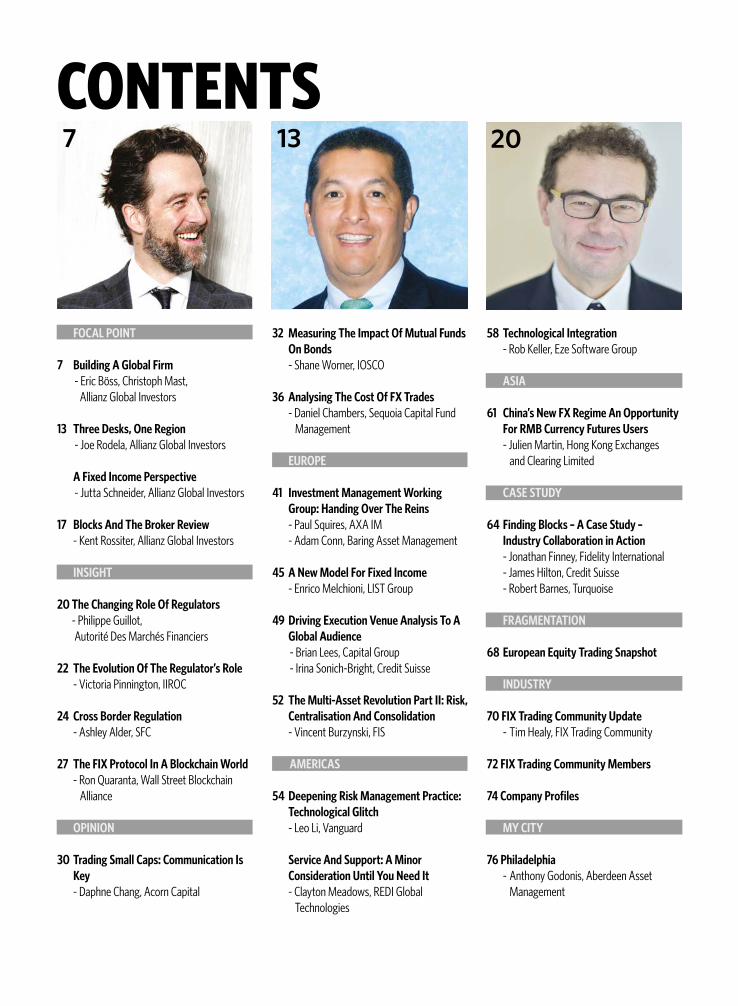

CONTENTS7 13 20

FOCAL POINT

7 Building A Global Firm - Eric Böss, Christoph Mast, Allianz Global Investors

13 Three Desks, One Region - Joe Rodela, Allianz Global Investors

A Fixed Income Perspective - Jutta Schneider, Allianz Global Investors

17 Blocks And The Broker Review - Kent Rossiter, Allianz Global Investors

INSIGHT

20 The Changing Role Of Regulators - Philippe Guillot,

Autorité Des Marchés Financiers

22 The Evolution Of The Regulator’s Role - Victoria Pinnington, IIROC

24 Cross Border Regulation - Ashley Alder, SFC

27 The FIX Protocol In A Blockchain World - Ron Quaranta, Wall Street Blockchain

Alliance

OPINION

30 Trading Small Caps: Communication Is Key

- Daphne Chang, Acorn Capital

32 Measuring The Impact Of Mutual Funds On Bonds

- Shane Worner, IOSCO

36 Analysing The Cost Of FX Trades - Daniel Chambers, Sequoia Capital Fund Management

EUROPE

41 Investment Management Working Group: Handing Over The Reins

- Paul Squires, AXA IM - Adam Conn, Baring Asset Management

45 A New Model For Fixed Income - Enrico Melchioni, LIST Group

49 Driving Execution Venue Analysis To A Global Audience

- Brian Lees, Capital Group - Irina Sonich-Bright, Credit Suisse

52 The Multi-Asset Revolution Part II: Risk, Centralisation And Consolidation

- Vincent Burzynski, FIS

AMERICAS

54 Deepening Risk Management Practice: Technological Glitch

- Leo Li, Vanguard

Service And Support: A Minor Consideration Until You Need It

- Clayton Meadows, REDI Global Technologies

58 Technological Integration - Rob Keller, Eze Software Group

ASIA

61 China’s New FX Regime An Opportunity For RMB Currency Futures Users - Julien Martin, Hong Kong Exchanges

and Clearing Limited

CASE STUDY

64 Finding Blocks – A Case Study – Industry Collaboration in Action

- Jonathan Finney, Fidelity International - James Hilton, Credit Suisse - Robert Barnes, Turquoise

FRAGMENTATION

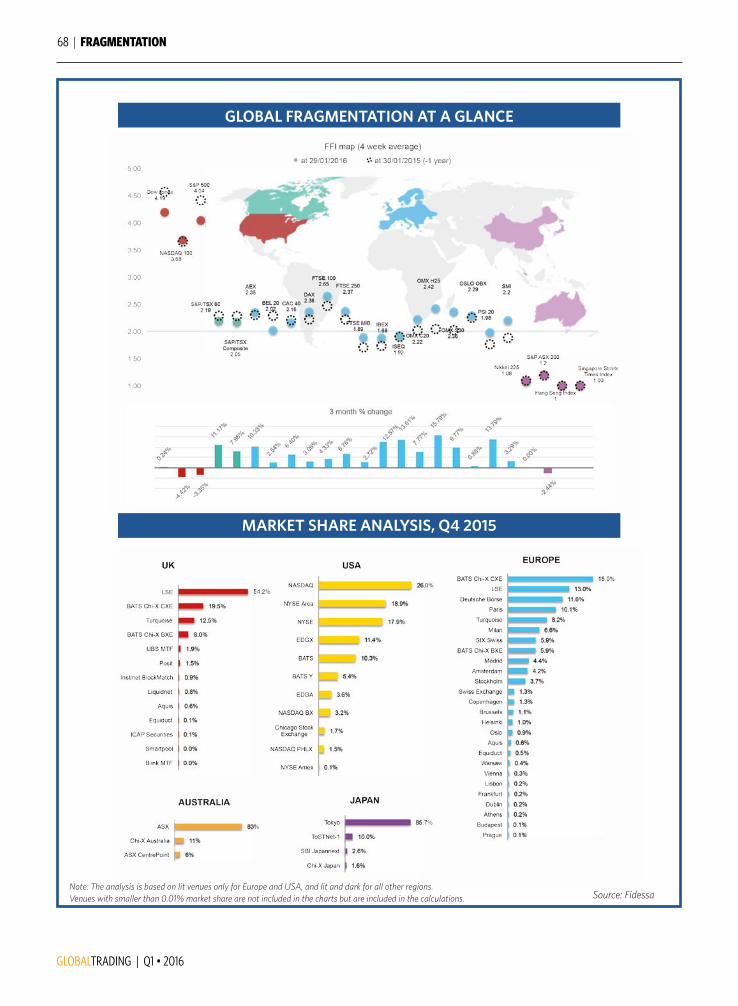

68 European Equity Trading Snapshot

INDUSTRY 70 FIX Trading Community Update - Tim Healy, FIX Trading Community

72 FIX Trading Community Members

74 Company Profiles

MY CITY 76 Philadelphia - Anthony Godonis, Aberdeen Asset Management

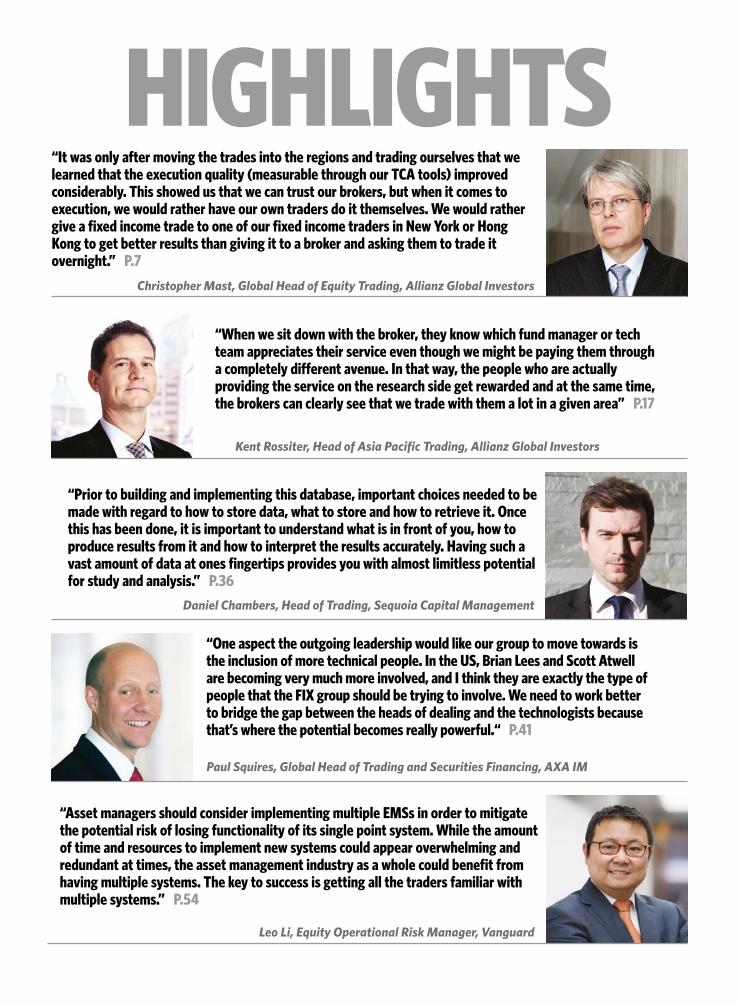

HIGHLIGHTS“It was only after moving the trades into the regions and trading ourselves that we learned that the execution quality (measurable through our TCA tools) improved considerably. This showed us that we can trust our brokers, but when it comes to execution, we would rather have our own traders do it themselves. We would rather give a fixed income trade to one of our fixed income traders in New York or Hong Kong to get better results than giving it to a broker and asking them to trade it overnight.” P.7

“When we sit down with the broker, they know which fund manager or tech team appreciates their service even though we might be paying them through a completely different avenue. In that way, the people who are actually providing the service on the research side get rewarded and at the same time, the brokers can clearly see that we trade with them a lot in a given area” P.17

Christopher Mast, Global Head of Equity Trading, Allianz Global Investors

Kent Rossiter, Head of Asia Pacific Trading, Allianz Global Investors

“Prior to building and implementing this database, important choices needed to be made with regard to how to store data, what to store and how to retrieve it. Once this has been done, it is important to understand what is in front of you, how to produce results from it and how to interpret the results accurately. Having such a vast amount of data at ones fingertips provides you with almost limitless potential for study and analysis.” P.36

“Asset managers should consider implementing multiple EMSs in order to mitigate the potential risk of losing functionality of its single point system. While the amount of time and resources to implement new systems could appear overwhelming and redundant at times, the asset management industry as a whole could benefit from having multiple systems. The key to success is getting all the traders familiar with multiple systems.” P.54

Daniel Chambers, Head of Trading, Sequoia Capital Management

Paul Squires, Global Head of Trading and Securities Financing, AXA IM

“One aspect the outgoing leadership would like our group to move towards is the inclusion of more technical people. In the US, Brian Lees and Scott Atwell are becoming very much more involved, and I think they are exactly the type of people that the FIX group should be trying to involve. We need to work better to bridge the gap between the heads of dealing and the technologists because that’s where the potential becomes really powerful.“ P.41

Leo Li, Equity Operational Risk Manager, Vanguard

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 7

By Eric Böss, Global Head of Trading and Christoph Mast,

Global Head of Equity Trading, Allianz Global Investors.

Building A Global Firm

More Buy-side Interviews

Christoph: Allianz Global Investors historically had a trading setup focussed on equities organised in silos and by regions. Over the last 15 years the system has evolved so that regions are responsible not only for the trading of the portfolio managers in their region, but they are focusing on the time zone trades, regardless of where the portfolio manager sits. For Asian and US portfolio managers, the advantage is that they have a trading desk in the time zone in their respective region. This means they have an increased concentration of specialist traders in a particular stock for their fund, within their region and globally.

The process has been challenging because we had to get both the trading software in place and also ensure that all the rules and regulations of the different regions and countries were fulfilled.

Next we started to broaden the scope of trading to cover all asset classes. Currently we are as involved in trading on the equities side as we are on the fixed income side. There is also a

GLOBALTRADING | Q1 • 2016

8 | FOCAL POINT

global products where the location of the trader is less relevant. However, other segments like covered bonds, corporates, emerging markets or high yield can be fairly local.

We are currently building on the successful model implemented in equities in terms of our fixed income trading expertise. That is building regional expertise, connecting it in one trading system and at the same time ensuring that we are not getting too granular – avoiding the risk of not being scalable anymore . This is occasionally a difficult balance to strike.

Beyond equities and fixed income there are two more asset classes we trade – FX and derivatives. Derivatives are by definition a group of instruments of their own, so we decided that having derivative specialists within the firm is a valid way to go, especially in an environment where derivatives are used widely.

It is extremely helpful to have people with expertise on the instrument side as well as on the related underlying market side. Derivatives, while many of them trade like equities, are settled completely differently. There are margins involved, different exchange rules, and they fall under different regulations. These are the main reasons why we decided to have specialist derivatives teams trading at least in those regions where there is sufficient trading volume to make that a valid decision. Currently those are the US and Europe.

We also have a FX team in Europe, which is partly due to the fact that Europe is the most multifaceted market in terms of number and complexity of funds. FX is the least regionally specific market, so trading can be located pretty much anywhere which is why we decided to leave it in Europe where most of the client base active in currencies is located.

Going multi-assetEric: While building our global multi-asset trading capabilities we looked at our existing equities structure, took what we liked about it and translated that into what we wanted to achieve. But extrapolating that to, for example, the rates market is not a simple ‘copy and paste’ operation. There are areas within fixed income which can be handled like stock trading (primarily the super liquid government markets), but for anything that is not primarily

huge trading business on the derivatives side and an FX trading desk focusing on the FX trades of the portfolio managers. Currently, we are in the process of extrapolating the long-established equity global dealing structure for fixed income to the regional trading desks. We have already moved on a global basis with emerging market fixed income trades over the last couple years but we are now working on a structure which will allow us to trade fixed income and derivatives wherever it needs to be traded and for any of our global accounts.

A global setupChristoph: Allianz Global Investors has 24 traders in Europe, seven traders in the US and 18 in Asia-Pacific trading all asset classes. So there is a strong centralised trading desk in each region. This structure raises many questions, including: how much do each of the desks trade for their own region? How much do they trade for other regions? How big a market participant are we in a particular region? What’s happening as far as flows are concerned? What is the impact on execution quality and the feedback of the portfolio managers? How much is our business focusing on portfolio management centricity? What developments are not only measuring the performance of the traders but also the input of the portfolio managers as far as information flow goes?

Eric: Allianz Global Investors now is a truly global asset manager with operations in all three major time zones, active in most asset classes and running a global trading setup that acts as one platform serving all portfolio managers.

Despite our global reach we firmly believe in regional presence and think there is value in regional trading expertise. Taking for example market micro structure and liquidity, these are very different in for example France and the US. So having a US-based trader for the US and Europe-focused traders in Europe and the same for Asia is something that we still consider is the best way forward for equity markets.

While on the one hand we want to be regional, we do still have to make sure that we are scalable on a global level. The approach we are taking with fixed income trading is very similar, because fixed income markets are regional as well to some extent. But there are parts of it, like the Treasury market and the related derivatives markets which are very much

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 9

This is precisely the task ahead of us in fixed income because this whole market is still very much a phone and text-driven, bilateral market.

Electronic execution and trade supporting tools are moving ahead fast but it is surprising how focussed on bilateral trading the fixed income market still is. We strongly believe in technology and especially in the transparency and scalability benefits of electronic trading. It is certain that going forward, fixed income will be traded on more than one venue and on several platforms so without good technology on the trading floor you will fall behind.

Christoph: Before the introduction of global dealing across our equities business we were happy having our executions done through brokers when we were outside our time zone. We had trusted brokers and gave them instructions on how to execute the trades.

It was only after moving the trades into the regions and trading ourselves that we learned that the execution quality (measurable through our TCA tools) improved considerably. This showed us that we can trust our brokers, but when it comes to execution, we

Eric Böss,Global Head of Trading, Allianz Global Investors

traded electronically, the blueprint doesn’t fit well enough.

In Europe we already trade 85-90% of our fixed income flow electronically. The plan is to do more than that as a result of all that we have learned in equities. In order to be scalable, we must be technologically savvy – we need to have all the systems we need, but not too many to support.We can already extrapolate some market infrastructure information: questions around best execution and TCA policies, order aggregation and separation which we know from our equity history. But the market infrastructure within fixed income is so different to equities that it requires considerably more thought.

One lesson learned in our equities operation following the fall of the exchange monopolies and arrival of competition in the form of alternative execution venues, was the need to re-aggregate the liquidity.

“While building our global multi-asset trading capabilities we looked at our existing equities structure, took what we liked about it and translated that into what we wanted to achieve. But extrapolating that to, for example, the rates market is not a simple ‘copy and paste’ operation.”

Multi-asset trading and investment management solutions for the world’s financial community.

fidessa.com

Fidessa_Generic Corporate Advert_03.indd 1 07/08/2015 11:27

GLOBALTRADING | Q1 • 2016

10 | FOCAL POINT

would rather have our own traders do it themselves. We would rather give a fixed income trade to one of our fixed income traders in New York or Hong Kong to get better results than giving it to a broker and asking them to trade it overnight. This was one of the main drivers for our decision to go global outside of equities.

In addition, MiFID II has put much more emphasis on traders and on the execution for clients. This means that areas which historically we were able to leave to brokers, we now have to monitor much more directly. MiFID II will require buy-side traders to take far more ownership of all parts of the value chain of the execution services than previously. This will require additional resources on the buy-side.

Integration of the portfolio managersChristoph: Twenty years ago, portfolio managers were frequently making trades themselves. When centralised trading desks were installed, the portfolio managers were encouraged to leave those trades to our discretion. Trading has come a long way since then, but our main focus, along with best execution is how we better communicate with the portfolio managers. Our aim is that a portfolio manager receives information from the market but also that traders are in a position to advise the portfolio managers on what to make of that information. This process is still evolving but the feedback from our portfolio managers is that it is highly appreciated.

Eric: Fixed income traders, almost by definition and by the nature of their asset class, have to be a little

bit more embedded into portfolio management compared to equity traders.

Looking at fixed income trading in our firm 15 years ago, traders ran portfolios and did execution trading, so the model was much more hybrid. Fixed income portfolio managers now require a different level of expertise from their traders; they need more communication, colour and consultancy so traders have to be more embedded.

Christoph: In fixed income we have to appreciate that the asset class as a whole is more complex than equities. Trading US treasuries could be run from virtually anywhere. The requirements of emerging market bond trading, for example, which trade across time zones, include FX in various forms and potentially derivatives are inherently more complex. Then there are areas like credit where knowledge of the market itself is already valid and important for portfolio managers and traders

“We would rather give a fixed income trade to one of our fixed income traders in New York or Hong Kong to get better results than giving it to a broker and asking them to trade it overnight.”

Christoph Mast,Global Head of Equity Trading, Allianz Global Investors

Not just any network, but a global, financial community network.

Rely on IPC for data and voice connectivity to the Global Capital Markets

Connect. Collaborate. Communicate.

© 2016 IPC Systems, Inc. All rights reserved. IPC, the IPC logo, Connexus and Unigy are trademarks of IPC Systems, Inc.

To learn how to gain access to a ready-made ecosystem of diverse market participants, visit www.ipc.com/fmn

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 11

in their communication because it is not cross regional.

The question is how to slice up that big fixed income execution pie. We are still in the process of finding out what the best execution set-up for certain parts of our businesses is.

Client demandEric: Our traders, if they still want to be a relevant part of the investment process, have to be able to prove their added value. We have always been very keen on monitoring and documenting the quality of our trading, using internal as well as external work and systems.

Christoph: When we rolled out full global equity trading in 2004, our global trading policy was expedited. We had to revisit the policy with the advent of MiFID I and now are re-examining it every two years because of ongoing changes to our processes. Our trading policy not only describes our goals but also our processes – we are actually describing the way we want our traders to deal and how we monitor that.

Our clients are also stipulating how they want their orders to be monitored and analysed. The same is true for consultants and regulators. In order to stay ahead we must introduce new products and concepts as soon as they are on the market. We were amongst the first to test fixed income TCA from various vendors (and so found out that they were not yet delivering what we require).

Eric: We were one of the first firms in Europe to implement electronic RFQ trading for equity derivatives. This was simply because we thought it would make our lives easier and we were able to remove a number of best execution requirements by having RFQ trading instead of the old style mail and phone check systems. The data we can analyse now helps us a lot in improving our broker selection and trade analytics.

Currently our fixed income staff are analysing the potential execution platforms coming onto the market in Europe. They are exploring which ones might work and trying to get ahead of the game in terms of technology. Unfortunately, because of the sheer number of new platforms coming to market, their

job has become more difficult and as a result the pre-screening takes more time than a regular trading group can actually afford. At the end of the day, we are traders, not IT project managers.

Developing true TCAChristoph: We are currently very much engaged in implementing MiFID II’s proposals. We know the direction it’s headed. The requirements will be refined but they are pretty much fixed from an asset class perspective. As a result, we will re-visit our best execution policy. We have to consider how we want to handle full unbundling and we have to make sure that TCA is operable outside the equity world as well; the need exists but the solution may not be that easy.

In the last decade we have been through several providers and various ways of looking at TCA; in fixed income and derivatives, we still need more. If we were to try to find a TCA provider for our whole multi-asset business. No matter what some vendors claim, there is still no one out there who can meet our expectations.

This leaves us with the question of how to do TCA until the market has developed sufficient providers to satisfy our own and our clients’ high end needs. This is an area into which we are putting considerable effort.

Eric: We need to work on translating or adjusting that to fixed income, derivatives and FX. With FX, once we have more transaction data available, it will be possible to run the same or similar mechanisms used in equities. In fixed income I think the approach will be more holistic and less number crunching. Some parts of derivatives, primarily futures, are close enough to equities in the way they trade, hence we can use the same, proven analytics.Options and swap markets pose more of a challenge.

In some asset classes we will have to come up with new ideas on how to define TCA. This is where we will be focussing our efforts over the next six months because it is an important part of improving trading and our client base is already asking for more.

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 13

US Trading at Allianz Global Investors operates within a global trading platform – but with a regional approach. We now work out of three locations in the US. Our trading used to be solely San Francisco based but when we merged a number of boutique firms owned by Allianz, we integrated them into our global trading platform. It is still one US trading platform but it now operates out of San Diego, San Francisco and New York City.

Most equity-related trading takes place on the San Diego and San Francisco desks. Most derivatives, futures and some emerging market debt trading takes place out of New York, where we have two very highly experienced options/derivatives traders. We used to trade some derivatives out of San Francisco but two years ago transitioned that flow to New York.

The reason for having trading activities in the different locations is because we have portfolio management activities there and our experience is that there is added value in having traders operate in the same location as portfolio managers.

But I must emphasise that even though we are located in three different places, we really do function as one desk. We all use the same trade blotter so whenever a portfolio manager enters a trade, we can all see it. Similarly, we use the same turret system to our brokers, so if a broker calls the desk, the call comes into the three different locations simultaneously; any one of us can pick it up and service that call for any other trader.

With Joe Rodela, Head of US Equity Trading, Allianz Global Investors

Three Desks, One Region

We follow all the same policies and procedures and our commission management and broker voting systems are identical. Our view is that we are ‘one desk, one team’. It just happens that we are sitting in three different locations.

In order for it to work, I rotate through our San Diego office once a month, and I go to the New York office every quarter. At least once a quarter our other traders will play musical chairs as well and work from the other locations. In that way we enhance the ‘one desk, one team’ culture.

There are often times when I will be sitting on the New York desk but I’ll still be trading for the portfolio management teams in San Francisco, or I could be in San Diego doing the same thing. The way our telephone systems and trade blotters are set up means that it is unlikely that the portfolio manager will actually know which office I’m in. They can reach me just as they would any other time, – regardless of where I am sitting, they will know how to contact me. They will only know where I actually am if they physically try to come and find me. Technology has helped make this transition relatively seamless.In addition, there is an intercom system set up between the desks. We just have to hit a button and we connect between the traders in San Diego or New York instantly, and they can do the same thing back to us.

We have carefully examined the risks and rewards of this type of set up. We need to keep

GLOBALTRADING | Q1 • 2016

14 | FOCAL POINT

For portfolio managers, analysts, and traders, the process is pretty seamless regardless of where they are sitting.

StrategyIf a firm is to set up a global trading platform to trade anywhere in the world there are three ways of approaching it: • The firm could operate out of one location

which would mean the desk would require 24-hour cover, so there would be shifts of traders coming in around the clock.

• A firm could have one location but base the hours on whichever region the desk is in. So in the US, they would have US hours and when the traders go home, they would simply hand off orders to the brokers who would hand them off to the regions. The traders would need to be on call 24 hours a day in case anything happened with the order that needed attention, regardless of the time of day or night.

• The third option is the way we operate: having specialised trading desks in the regions so as to have experts in each market. It allows for the promotion of best practice within each specific region. We adopt the same policies and procedures on a global level, but there are also regional sub-sets of policy for each specific region.

united as one team given that we are physically in different locations. The technology available to us and the fact that the traders are willing to rotate around the offices means it works well.Another advantage of having three desks is for business continuity and disaster recovery purposes. For example, there could be an emergency in San Francisco which might prevent us from getting into our offices. All we would need to do is put a call through to San Diego or New York in order to have them pick up trading activities for the day.

Global positioningThe way our global trading platform is set up gives us centres of expertise. It works in a similar way for the portfolio manager team regardless from where they operate. If a US-based portfolio manager wants to enter a trade in Taiwan, they put the order in the system as normal. The only thing that is different is the desk to which they route the order. For example, for Taiwan they would just highlight our Hong Kong desk which takes care of pan-Asian trading. They hit the enter button and the order will appear on our Hong Kong desk; so when the Hong Kong traders come in the next morning, they will see the order on their blotter just as we would see it here and they work it just as they do for the local Asian-based portfolio management teams in Asia.

“The way our global trading platform is set up gives uscentres of expertise. It works in a similar way for theportfolio manager team regardless from where theyoperate.”

Joe Rodela, Head of US Equity Trading, Allianz Global Investors

Global Trading adv_FINAL-outlined.indd 1 17/02/2016 6:21:10 PM

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 15

We currently trade 80-90% of our fixed income electronically, so we are ahead of the curve compared to many other involved counterparties. Over the last two years an increasing number of new trading platforms has been introduced to the market to meet the new requirements and provide trading possibilities despite low liquidity. We took this opportunity to continuously test and evaluated those different trading systems in order to stay well informed and ensure best liquidity for our trading.

Obviously, we cannot test all of them, as there are over 40 new initiatives by now. Nevertheless we have met with a representative sample (new trading platforms as well as new information systems) which for instance also opened up buy-side to buy-side access in addition to the usual buy-side to sell-side trading we usually do.

A mandatory requirement for onboarding a new system is the direct connection to our OMS. This is true even for those systems that allow us to only monitor liquidity as opposed to a trading system.

We have witnessed that the markets are becoming increasingly illiquid and sophisticated due to new regulations and capital control measures. This implies that the requirements for trading overall is becoming more complex. In this demanding environment the question whether the buy-side will become a major provider for liquidity arises more and more. As far as I can estimate neither the buy-side desks nor the numerous new trading platforms will become the new major liquidity sources. This will continue to be the task of the sell-side. However establishing new possibilities for the buy-side counterparties to match interest directly on an anonymous platform is opening up new opportunities and increasing transparency.

Taking all this into account it remains essential to maintain close relationships with the sell-side for

A Fixed Income Perspective

sourcing liquidity and being able to trade efficiently in the market.

Another key area for us is the internal relationships between traders and portfolio managers. At Allianz Global Investors we have established an intensive communication and interdepartmental cooperation which has been running a long time now. This means we are not only focused on the pure execution but providing an extended function by supporting the portfolio managers in various ways. We provide feedback on liquidity, present trading ideas and show them relevant axes.

Yet we are not only involved in secondary business but also for the setup of new portfolios and new trading instruments. Usually the PMs ask us for our opinion on any planned bond purchase and schedule to carry out the planned set up.

With Jutta Schneider, European Head of Fixed Income Trading, Allianz Global Investors

Jutta Schneider, European Head of Fixed Income Trading, Allianz Global Investors

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 17

There are risks around everything we do, and every decision our traders take impacts the final results of our executions. We need to understand the signals and act to the best of our abilities. Risk is central to what traders do, day-in, and day-out: we need to look at the benefits of risk instead of fearing it. Too often a trader’s natural instinct is to hedge themselves by dragging trades out through the whole day even when they’ve got strong conviction that they’d be better off taking another course of action. This is the type of behaviour we monitor on the desk and look to change.We have to be open to new technology; some new vendors are very innovative, while others appear to have little differentiation from established products and don’t appear to add any real value.

Broker reviewFor equity TCA we constantly review our brokers on a global basis. We feel it’s important to view our results as best we can against our peers, and our TCA vendor arguably has the largest peer data-set with which to work. Monitoring our executions is an ever-improving process but we are very pleased with our long-term TCA results and peer rankings.

By Kent Rossiter, Head of Asia Pacific Trading, Allianz Global Investors

Blocks And The Broker Review

We work with brokers every day and we’ve known a lot of our counterparts for decades. Over this long time we’ve come to know who’s likely to be the most helpful or knowledgeable about different trading situations and markets. Naturally we want them to be there to help us in the future, so we need to pay the people who can benefit our clients trading activities. Those brokers most successful in matching up IOIs are likely to be the brokers getting our highest votes as well. However, the voting is not just restricted to that one important service. It also rewards them for good trading calls, execution skills, being able to watch our orders carefully, responsiveness to our IB chats, and so on. And so it’s not just focused on blocks but the end-result of the whole execution process.

Globally AllianzGI has three main regional voting groups which are the European-based investment teams, the investment teams based in America and the investment teams based in Asia. Each of the different regional team members will vote for the brokers they feel provide the best service. But for example, if the US team votes a certain amount of money to go to one broker, and we don’t end up trading with them in Asia,

GLOBALTRADING | Q1 • 2016

18 | FOCAL POINT

they’re getting the votes from. Every half year, our main brokers come in and we all sit down and go over with them who from our regions are voting for them. When we sit down with the broker, they know which fund manager or tech team appreciates their service even though we might be paying them through a completely different avenue. In that way, the people who are actually providing the service on the research side get rewarded and at the same time, the brokers can clearly see that we trade with them a lot in a given area, and because of that, the broker can assume that they have a good franchise servicing that need.

Generally as an outcome of the vote we have 75 or 80 different brokers or research outfits tagged. The latter research outfits don’t have execution capabilities so we end up trading with one of our top brokers who we have the aforementioned CSA program set up with. And then every half year we’ll figure out how much from the CSA program we need to pay these external research providers and organize the payments so they still get rewarded.

BlocksActual market liquidity in a stock we want to buy or sell doesn’t necessarily exist when we need to be doing that buying or selling. When orders are of block size it often doesn’t make sense to test the waters getting small executions because we might not make much progress before we find ourselves pushing the stock price. By putting out some feelers in the right places we often get a look at contra-liquidity before an order goes into the market. Patience doesn’t always pan out

then that broker can be paid by the US and European trading desks. Or if we are getting exceptional service from a particular broker we may trade a lot with them here in Asia, in which case the US and Europe may trade with them far less. Another situation is where the PM might be voting for that broker because they like the US consumer research analyst, but from a trading standpoint, we find that broker to be excellent in Korea, Taiwan and Japan tech names so instead trade a lot with them out here in Asia to pay them. And there are situations where some brokers just are poor at executions or technology everywhere and we don’t feel comfortable paying them through trading activities. In this case we have Commission Sharing Agreements (CSA’s) in place and can pay them from that pool.

As a consequence it is very important that we sit down with the brokers and be transparent as to where

“When we sit down with the broker, they know which fund manager or tech team appreciates their serviceeven though we might be paying them through acompletely different avenue.”

Kent Rossiter, Head of Asia Pacific Trading, Allianz Global Investors

© 2016 Eze Software Group LLC. All Rights Reserved. Unless otherwise noted, product names, trade names, designs, logos and all other trademarks or service marks used herein are the property of Eze Software Group LLC or its affiliates.

A TOP PERFORMER, FOR TOP PERFORMERS

Top-performing investment firms need top-performing technology. More than 2,000 firms worldwide rely on Eze Software Group to manage their investment process.

EZESOFT INVESTMENT SUITE

@EZE_SOFT EZE SOFTWARE GROUPEZESOFT.COM

Q1 • 2016 | GLOBALTRADING

FOCAL POINT | 19

get to execute size that wouldn’t have ever been there in the market if it weren’t for that initial call.

And sometimes a broker comes to us. They know that we’re a big holder, either because we’ve traded the stock with them before in size, or they can see us as a significant shareholder on the Bloomberg HDS page or another reporting system. The broker will come and tell us that they have a chunky size in case we’re interested. Even though I might not have an order on my desk, it provides the perfect opportunity to go to the PM and see if they want to take advantage of the unexpected liquidity.

The great thing about doing this is that there was only one side of the trade to start with. The other side didn’t exist and yet because we work with the broker and PM together, we are able to create something. Accomplishing this requires communication with our PM’s, and skill and trust between the brokers and the buy-side, something that won’t likely be automated anytime soon.

DISCLAIMER

§ The views and opinions expressed in this document, which are subject to

change without notice, are those of Allianz Global Investors Asia Pacific

Limited and/ or its affiliated companies at the time of publication.

§ Some of the information contained herein including any

expression of opinion or forecast has been obtained from or

is based on sources believed by us to be reliable, but is not

guaranteed and we do not warrant nor do we accept liability

as to adequacy, accuracy, reliability or completeness of such

information obtained from or based on external sources.

§ The information contained herein including any expression of opinion

is for information purposes only without consideration given to

specific investment objectives, financial status or particular needs

of any person, and is given on the understanding that it is not a

recommendation nor investment advice and any person who acts

upon it or otherwise changes his or her position in reliance thereon

does so entirely at his or her own risk without liability on our part.

§ This is not a recommendation or offer to buy or sell or a

solicitation or incitement of offer to buy or sell any particular

security, strategy, investment product or services.

Issuer of this material: Allianz Global Investors Asia Pacific Limited.

however. Finding and trading blocks is therefore often a timing decision, with a bit of good luck thrown in. It is not worth immediately going to the market just because we happen to get the order at 10:08am. If the liquidity is not there, we might want to wait and be a bit more patient to try to line up blocks by talking with our contacts or using the technology which is out there.

We’re able to do the searching ourselves but the fact is we still find most of the flow through our large panel of brokers. Without the information from these brokers, we would have far fewer matches and fewer trading opportunities.

Many crossing platforms are very innovative and they’re moving in the right direction. Often we’ll see five IOIs in a name from brokers so we decide whether we want to negotiate with the broker or try our luck in the anonymous electronic matching systems.

One of the most satisfying results, which only happens rarely, is trying to match up flow and let PM’s know of outsized block flow we may see on the Street, even when we don’t have live orders. When our PM’s hear about such opportunities they can be quite responsive and generate an order on the back of it. That’s a win-win for both sides; we each

“By putting out some feelers in the right places we often get a look at contra-liquidity before an order goes into the market. Patience doesn’t always pan out however. Finding and trading blocks is therefore often a timing decision, with a bit of good luck thrown in.”

GLOBALTRADING | Q1 • 2016

20 | INSIGHT

With Philippe Guillot, Executive Director, Markets Directorate, Autorité des marchés financiers

The Changing Role Of Regulators

The entire regulatory process incorporating how the regulators enact incoming rules, and how we interact with the industry is changing. MiFID I was voted on in 2004 and implemented in 2007, then there was the financial crisis of 2008 which led to further talks resulting in MiFID II, which was voted on in 2014 and is due for implementation in either 2017 or 2018.

From these timescales it is clear that ‘legislator time’ is completely different from ‘market time’. The legislator makes regulatory changes every ten years or so whereas markets move every microsecond. Between the two, there is a need for constant vigilance in the function of markets. This has created a new role for the regulators, which we call ‘dynamic regulation’. Even a few years ago, this extension was not really possible because regulators were only enforcers. The evolution has come about due to the increased electronification of the industry, linked to the fact that there is now more data available, an increased capacity to store that data and new methods of comparing data. This is the big ‘data evolution’ experienced by every industry, but in particular the financial services industry.

The amount and quality of information available over the last 20 years has completely changed the processes undertaken by proprietary traders, execution brokers and financial analysts. That same information is also

used by asset managers who themselves have a variety of new strategies which changes the trading and regulatory environment. Today’s market microstructure is different from tomorrow’s market microstructure and from yesterday’s. Into that mix, we need to be able to adjust the regulation accordingly. Regulation exists in order to define a floor and a ceiling on what firms can do, must do, and could do. We look at a firm’s actions from every aspect and we see that, in the context of regulation, they can either be doing too much or too little, and what we want is a regulatory environment where everybody can work and trade together in a balanced ecosystem.

Added to that, a dynamic regulator has to base its judgements on the data it receives, which largely comes from within the industry itself. As we base our judgements on that data, it is in everyone’s interest to ensure that the data is comprehensive, clean and understandable. We have to look at every link of the data chain because everyone who is producing, cleaning and using that data has to share responsibility for its quality.

This puts us all into an environment where we have been benefitting each time there was a new layer of regulation. We all gained from MiFID I because we started to receive data from MiFID I that we were not

Q1 • 2016 | GLOBALTRADING

INSIGHT | 21

getting before. EMIR regulation into derivatives resulted in our receiving new data on derivatives that had not been available before. And we expect that we will benefit from MiFID II in the same way because there will be new data available as a result. It’s an ongoing process of learning and adjusting which must be done by each link in the chain. This means we need to collaborate as an industry to ensure that the decisions we make have been empowered by the sets of regulations and are based on proper data. It’s critical that the data received is reliable as this allows us to help prevent problems in the industry rather than merely enforce the rules. Prevention only works through collaboration.

For instance, the simple fact that firms need to report new areas, such as derivative positions, puts the industry into a virtuous circle. Companies have come to us saying that new regulatory obligations had forced them to look at what was happening inside their own services, making them aware of operating inefficiencies and areas where unnecessary risks were being taken.

Role of global regulationAll markets are interconnected and activity in one market will impact on everything else. Regulation is not homogenous, there is local regulation, but it could be national or continental. However, in order for regulation to be efficient there needs to be a global approach. The role of organisations like the International Organization of Securities Commissions (IOSCO) is critical because they are the best link between all the various agencies irrespective of their location.

“We have to be able to listen to what the industry has to say, but equally be detached enough in order to properly enforce the regulation.”

IOSCO produces a broad set of principles, but if all regulations are taken locally and adhere to IOSCO principles then there will be regulatory convergence. Obviously because IOSCO is global, it cannot go into as much detail as local regulations. However, if we refer back to the earlier point about regulation defining a floor and a ceiling, then IOSCO can describe both of these very easily and from that we can build different layers at a national or international level.

Limit to collaborationIt is important that we remain close to the industry as when new regulations are implemented, we need to hear what the industry is saying in response to those new regulations. We have to be able to listen to what the industry has to say, but equally be detached enough in order to properly enforce the regulation.

During that listening process, it is good to remember (from the regulator’s standpoint) that the industry may have a vested interest in what it is saying, which is why it is important for the regulator to listen to everybody in the industry so as to distinguish what is vested interest and what is genuine concern. The industry can help here too, as the more objective they are, the easier it is to have a constructive dialogue.

We cannot say that we must not talk to the industry because that doesn’t help produce proper regulation. But at the same time we cannot say we will do whatever the industry wants because that leads to other problems. We have to meet somewhere in the middle. There has to be a balanced approach.

Philippe Guillot,Executive Director, Markets Directorate, Autorité des marchés financiers

GLOBALTRADING | Q1 • 2016

22 | INSIGHT

With Victoria Pinnington, Senior Vice-President, Market Regulation & Policy, Investment Industry Regulatory Organization of Canada (IIROC)

The Evolution Of The Regulator’s Role

Capital markets have undergone significant and unprecedented change in recent years. As a result, regulators and market participants alike have been grappling with challenges and opportunities associated with a proliferation of new products and players, segmentation and fragmentation of markets and the sheer speed of trading across all asset classes.

This pace of change in our markets has made it imperative that IIROC, as the national self-regulator responsible for the oversight of all investment dealers and their trading activity in Canadian debt and equity securities, continues to evolve in its role and keep pace to ensure surveillance of the markets remains current and effective.

Analysis and consultationIIROC plays a unique and central role in the Canadian regulatory framework based on our mandate to conduct surveillance of all Canadian equity markets, including exchanges and Alternative Trading Systems, both lit or dark, and all Canadian debt trading. We continually invest in and leverage technology to effectively monitor this fast-paced and quickly changing environment.

An important way to keep current about the markets we regulate is to study the regulatory data we receive to understand markets’ changing dynamics, emerging

trends, participants and

their activity. 水Another important

way is encouraging discussion with the

industry which gives us the opportunity to step

back and examine the wider question of how our markets

are evolving and consider the views and needs of diverse

stakeholders.

An example is IIROC’s approach to addressing issues related to the growth

of High Frequency Trading (HFT). IIROC commissioned and published five academic

papers on HFT and its effect on Canadian markets, examining:

• High frequency market making to large institutional trades

• Role of HFT in market integration/market fragmentation• HFT within the context of both the impact of change

to short selling rules and dark trading rules introduced in 2012

• Liquidity provision and market making by HFT

To gain industry insights on our comprehensive study, IIROC co-hosted a public forum at which the academics discussed their findings and engaged in a robust dialogue with interested stakeholders.

While the results showed that there were no concerns that warranted regulatory action at this time beyond measures already implemented by IIROC, (the implementation of the Electronic Trading Rules,

Q1 • 2016 | GLOBALTRADING

INSIGHT | 23

requirements for third-party electronic access to marketplaces and guidance on manipulative and deceptive practices), it demonstrates the importance of IIROC taking a data-driven and consultative approach.

Recognising the value of the data to a broader constituency, we are working to implement a data sharing strategy, so that data gathered and maintained as a public good is shared, with appropriate controls, with regulators and other industry stakeholders.

The importance of regulatory partnershipAnother element to managing the challenges is collaborating with our regulatory partners. The more effective our partnership and coordination, the better we can carry out our shared responsibilities to protect markets and protect investors.

An example of this is our recent work with the Bank of Canada and the Canadian Securities Administrators (CSA) to improve the timeliness and comprehensiveness of regulatory oversight of Canada’s debt markets.

Trading in debt now dwarfs trading in equity, but although greatly important to Canada’s economic growth and financial stability, the debt market has been relatively opaque to regulators and investors.

We and our partners at the Bank of Canada and the CSA recognised that robust regulatory supervision and oversight of the debt markets are critical to enhancing market integrity and investor confidence. Last November, we began collecting information on all the debt security trades done by the dealers we regulate. As a result, IIROC is better positioned to monitor and enforce compliance with investor protection and market

“The more effective our partnership and coordination, the better we can carry out our shared responsibilities to protect markets and protect investors.”

integrity rules in a cost-effective way, consistent with the equity market surveillance we already conduct across Canada.

The CSA is also working with IIROC to enhance dark market oversight and provide greater transparency to this growing and significant asset class. Under the CSA proposal currently out for comment, IIROC will become the transparency agent or “information processor” for the Canadian corporate debt market. In this role, IIROC will publicly disseminate trade information providing transparency that will facilitate more informed decision-making by all market participants.

ConclusionThe knowledge gained through our investments in IIROC’s surveillance, oversight and analytical work is especially important at a time when the environment is increasingly challenging securities regulators, the investment industry and all market participants.

Going forward, we’ll continue to use and share valuable data, count on insights from our stakeholders and collaborate with our regulatory partners as we manage the challenges and explore the opportunities that come with an evolving market structure.

Victoria Pinnington,Senior Vice-President, Market Regulation & Policy, Investment Industry Regulatory Organization of Canada (IIROC)

GLOBALTRADING | Q1 • 2016

24 | INSIGHT

Edited excerpts from a speech by Ashley Alder Chief Executive Officer, SFC

24 | INSIGHT

Cross Border Regulation

Cross-border regulation IOSCO has been considering how it can address these issues at a global level. First, the basic problem is fairly straightforward. This is that the application of local rules to cross-border financial business which affects national interests can lead to conflicts where one internationally active firm is subject to different conflicting rules. This can ‘Balkanise’ markets and lead to a broader drag on cost-effective financing for growth. And of course the most discussed example is derivatives, where talks are still eating up a large amount of time in the EU, the US and elsewhere. Now the G20 in its 2013 Moscow and St Petersburg communiques introduced a new idea called “deference”. This was meant to solve cross-border conflicts in the derivatives world. This formula was repeated in April of this year in another G20 communique from Washington. The idea is basically a reference to substituted compliance or EU style recognition. But in reality the G20 formula begs a lot of tricky questions. It provides that jurisdictions can defer to another “when justified by the quality of respective regulations and enforcement regimes”, but only if these lead to “essentially identical outcomes” and so long as the rules are “non-discriminatory”. It also says that we all must also have “due respect to home country regulation”. This is asking a lot. And these questions are largely the same as those which IOSCO’s Task Force on Cross-Border Regulation wrestled with for over two years. Now the end result of our Task Force’s work is

that we have a very detailed toolkit for regulators to refer to when looking at cross-border financial activity and the specific factors to take into account when using it. And we also decided to hardwire cross-border considerations such as timing mismatches into all of IOSCO’s standard-setting work.

But the Task Force also concluded that “IOSCO should engage more with the G20 and FSB to raise greater awareness of the key issues and challenges faced by IOSCO members on cross-border regulation, including the need for more refined thinking on the concept of deference”. Now what are these issues and challenges? First, we need to understand that national securities regulators are firmly bound by their domestic laws, national interests and national policy objectives when acting on a cross-border basis.

Second, the real authority of international standard setters such as IOSCO is inevitably weak because it isn’t based on binding treaty obligations, and as a result, global standards do not trump local law. In fact, global standards are rarely even referred to directly in securities legislation. And if they aren’t, it’s hard for national regulators to take them into account if local law already deals with an issue.

Third, peer pressure to apply international standards on a uniform basis can be effective, but this is far harder in securities markets compared to other regulatory

Q1 • 2016 | GLOBALTRADING

INSIGHT | 25

“......we are a long way from the ambition expressed by global firms that any proposed markets regulation that could have a significant cross-border effect must first be decided on as an international standard,......”

regimes as there is far more diversity and complexity of firms, investors, products, infrastructure and exchange platforms.

Fourth, regulators sometimes act protectively if they think that recognition of a foreign regime could cause domestic business to move overseas. In other words, even if differences in rules don’t increase systemic risk or compromise investor protection, if they still imply a difference in the cost of doing business, regulators will react in their national interests.

Fifth, recognition or deference becomes harder when the countries involved are at different stages of development, as is the case in Asia. And finally, there is often a basic reluctance to outsource regulation when a failure could end up with blame heaped at the door of the domestic regulator.

So we are a long way from the ambition expressed by global firms that any proposed markets regulation that could have a significant cross-border effect must first be decided on as an international standard, before being transplanted uniformly into local law. However, there is light at the end of the tunnel. Our IOSCO report recognises that in reality, regulators have put in an enormous effort trying to overcome hurdles where it matters, normally through bilateral negotiations of different types of recognition or deference agreements supported by MOUs. We have seen how the CFTC and the Securities and Exchange Commission have both progressed their approach to recognition through

substituted compliance – a big change when compared to the hard line taken a while ago. And it seems that international standards are referred to as a measure of equivalence in new EU legislation about benchmarks. And occasionally, discussions have been multilateral, a good example being an ad hoc group of regulators from major markets that meet to discuss derivatives – called the OTC Derivatives Regulators Group (ODRG). Our IOSCO Task Force therefore concluded that the general direction of travel is fairly clear. “The emphasis is towards more engagement via recognition to solve cross-border overlaps, gaps and inconsistencies through a combination of more granular international standards implemented at a jurisdictional level, and an increasing emphasis on determining when it may be appropriate to recognise foreign laws and regulations as a sufficient substitute or equivalent for domestic laws and regulations”.

To conclude, we are still dealing with the fact that participants in global markets are regulated by national regulators, and perfect harmonisation and total convergence of regulatory standards are unlikely. And a global rulebook is an unattainable ideal. But the outlook is far brighter than a few months ago, and I am hopeful that further progress will be made as we start to deal with Europe on the international reach of its benchmark legislation.

Ashley Alder,Chief Executive Officer, SFC

Q1 • 2016 | GLOBALTRADING

INSIGHT | 27

Ron Quaranta, Chairman of the Wall Street Blockchain Alliance, and Co-Chair of the FIX Trading Community’s Digital Currency/Blockchain Working Group.

The FIX Protocol in a Blockchain WorldFor those of us in financial services who have been involved in the world of digital currencies and distributed ledgers (also known as a blockchain), 2015 was the year that this innovative technology finally appeared on the radar of every major bank, broker-dealer, exchange and institutional investor. On a global scale, entire teams within these organisations have been created to research and analyse how blockchain technology might integrate with existing financial markets workflows. Innovation labs have been set up to spearhead the development of this disruptive capability, and hardly a day had gone by that we did not read an article in business and trade publications touting distributed ledger technology and the coming disruption to financial markets. As we enter 2016, we

will likely begin to see the implementation of many of these solutions on a wider scale. Thus, the purpose of this article is to briefly define what a blockchain is, discuss its history to date, and understand how the FIX Protocol may play an integral part in blockchain technology use in global financial markets.

What is the Blockchain?The Blockchain is essentially the underlying technology associated with the digital crypto currency known as Bitcoin. As many readers already know, Bitcoin was launched as open-source software in early 2009, by the still anonymous Satoshi Nakamoto, based upon Nakamoto’s published 2008 whitepaper “Bitcoin: A Peer-to-Peer Electronic Cash System”. The system is

GLOBALTRADING | Q1 • 2016

28 | INSIGHT

designed as a peer-to-peer online payments system, allowing participants to transact directly without needing an intermediary, with transactions verified by nodes on the Bitcoin network. Without diving too deeply into the more technical aspects of its operation, all transactions in the network are cryptographically recorded in a sequential chain of blocks (hence, “blockchain”), and each transaction references the block before it, thereby making illicit changes to the data extremely difficult. All nodes on the network hold a full copy of this public distributed ledger. Within this ecosystem, the blockchain unit of account is bitcoin itself. So with no central repository and no single administrator, all nodes on the network are incentivised to verify transactions, with their reward being the “mining” or creation of new bitcoin.

Bitcoin is the oldest and most widespread of the digital currencies, with a global market capitalisation of over USD6 billion as of late December 2015. However, it is not the only game in town. As of the time of this writing, there were over 650 publicly known digital currencies, many with little value, but most leveraging some form of blockchain technology.

“• Blockchains are meant to be data stores for sequential or chronologically ordered data.

• Blockchains are designed to be immutable, or tamper resistant. The ability to rewrite or alter data would be so costly across a wide enough network as to be prohibitively expensive.”

So why is this important? Why is the concept of a blockchain relevant to financial services? To answer these questions, it is helpful to put the main characteristics of blockchain technology in focus:

• Blockchains are meant to be data stores for sequential or chronologically ordered data.

• Blockchains are designed to be immutable, or tamper resistant. The ability to rewrite or alter data would be so costly across a wide enough network as to be prohibitively expensive.

• Cryptography and its associated digital signatures, prove identity of, and enforce access by, participants within the network. This also prevents the problem of “double-spending”.

• Public blockchains are designed to be transparent and anonymous.

The Public versus Private debateAt this point, it is important to touch on a topic of significant industry debate, namely the growing discussion about public versus private blockchains. The Bitcoin Blockchain is an example of a public, fully decentralised, permission-less data store that is open

Ron Quaranta,Chairman of the Wall Street Blockchain Alliance, and Co-Chair of the FIX Trading Community’s Digital Currency/Blockchain Working Group

Q1 • 2016 | GLOBALTRADING

INSIGHT | 29

Trading Community are working to define not only integration points, but also potential use cases and best practices for a future blockchain world. In 2015, FIX formed the Digital Currency/Blockchain Working Group, with the mission to “…identify, analyse and define use cases and integration points for digital currency and distributed ledger technologies across the spectrum of capital markets requirements, and recommend best practices for FIX implementation and usage of this emerging technology in financial markets”.

The group has a broad membership, with participants from banks, broker dealers, blockchain start ups and more, and all with a wealth of industry experience. Within this group, members have embarked on a series of activities, including: • Educational seminars for Working Group members,

to deepen our group understanding of blockchain technology and its implications.

• Preliminary review and recommendations of FIX implementation for digital currency trading (with much of the FIX Protocol already quite useful for digital currency trading in the context of FX).

• Initiated review of FIX and wider industry standards of digital currency and digital asset identifiers, as well as global marketplace identifiers.

• Structured an initial review of securities clearing and settlement via blockchain, with a goal towards understanding impact to FIX related messages.

• Created framework for FIX integration in broader distributed ledger initiatives, including smart contracts and alternative digital assets.

• Initiated discussion about alternative FIX uses i.e. – embedding FIX messages within a data block, etc.

ConclusionThis article is meant to be a very basic introduction to the world of blockchain and FIX, and merely scratches the surface of this growing field and its implications for financial markets and beyond. In future articles, we will address specific use cases and well as dive into the capability at a technical and product level. FIX Members are also encouraged to join the dialogue by participating in the Community’s Digital Currency/Blockchain Working Group.

to anyone wishing to participate in the network, and willing to adhere to the consensus mechanisms that enable its functionality. In addition to Bitcoin, Ethereum and Factom are well known examples of public blockchains. A private blockchain is often designed to utilise the most interesting aspects of blockchain technology, while maintaining the closed network aspects of many data systems in financial markets. As opposed to the decentralised model, the owner or administrator of a private blockchain maintains the authority to implement changes and define membership in that blockchain.

As we give thought to the many functions within the world of financial services, we start to envision how this capability might make workflows and data processing more efficient and cost effective. For example, how economically beneficial would it be for multiple banks to be leveraging a common, shared data store for a relevant business line? In a world where global financial organisations have literally hundreds of different databases, and every one of these firms has some form of “reconciliation” department, one can imagine the cost savings and growing transactional volume in a world of more efficient data processing. Currently, several firms are working on blockchain based solutions that would re-invent specific segments of financial markets processing, including syndicated loans, securities clearing and settlement and international trade finance.

None of the above as yet addresses the concerns that are being encountered within the industry about blockchain technology. How do competing firms leverage this technology while still protecting their own and their client’s data? How will regulators view industry participation? Can transparency make the burden of compliance easier? Are private blockchains simply different databases, and how can the full benefits of a distributed ledger be realised if participation is centralised? These and many other questions are already under serious consideration in the industry, and the landscape will invariably continue to develop over the coming year.

What is the role of FIX in all of this?Up to this point, we have not really addressed the role of the FIX Protocol in the world of blockchain technology. The reason is simple. Given the dynamic state of this technology and its evolution over the past few years, the financial markets and members of FIX

Itiviti. A new force.Technology solutions and services for a sustainable competitive edge in capital markets. Visit itiviti.com

GLOBALTRADING | Q1 • 2016

30 | OPINION

Trading Small Caps: Communication Is Key With Daphne Chang, Dealer, Acorn Capital

While liquidity is important for all traders, it is crucial for small cap traders. Portfolio managers regularly demand positions of at least 5% of a company’s holdings, so finding and executing block trades is always the priority.

Clear communications and close coordination with our PMs is critical to understanding stock valuations and how target weights for the fund are to be established. To have efficient communication, we have regular research meetings with our portfolio managers and analysts to discuss about our portfolio. Apart from the research meetings, we have developed our internal research system for the portfolio managers to upload their research reports or notes at anywhere and anytime. Once their reports or notes are uploaded in the system, the trading desk will receive the notification emails and can quickly pick up the revaluation from the PMs in order to take proper action in the market.

In this space, the trading desk’s activities cannot simply be limited to mechanically executing trades. We need to be up to speed in all aspects of the market, whether

monitoring the actions and movements of brokers, IOI, turnover changes, and changes in substantial holders.

Armed with this knowledge, our desk has far better opportunities to secure blocks at preferred prices at the right time.

Managing relationshipsDeveloping sound relationships with local brokers is important, particularly those who specialise in small caps. Well maintained broker relationships keep the trading desk abreast of underlying trading activity, potential placements and other corporate opportunities. We give high rankings for the brokers who can provide good small cap flow, deep knowledge about the small cap market, and good effort on delivering the block trades.

In situations where there is high liquidity, our adoption of algo trading strategies has helped us optimize our execution of trades enabling a lower profile in executing larger positions which might create undesired uncertainty in the market.Empowering dealers to act independently is

Q1 • 2016 | GLOBALTRADING

OPINION | 31

important in the small cap space because market conditions often require nimble and effective responses. Naturally, PM’s will make the buy-sell decision but how the order is executed must be the province of the trading desk. This is where traders must be au fait with how PM’s have arrived at their valuations and the underlying investment case with catalyst expectations. These provide the desk with guidance for an acceptable price when seeking liquidity. In addition, our dealers can see each

other’s trades at our own trading screen and are all aware of the valuation/target weights of each single trade. By sharing all the information together and working as a team, the trading desk can maximise the performance.

By the same token, the communication must go both ways with the PM. For example, unusual price movements and flows must be fed back to the PMs regardless of their buy-sell decision or the progress of the execution.

TechnologyTechnology can often have a limited application in small cap dealing. Transaction cost analysis can be of limited use in providing information to analyse trades. The methodology for valuing a trader’s performance is generally not a matter of whether the trader can secure a block above the VWAP price or below the VWAP with 60 days to complete the target position, for example. Performance is generally a function of how efficiently the trader can execute the PM’s decision and achieve the desired portfolio position.

Adopting our algo strategy has allowed us to better exploit liquid conditions, but traditional knowledge and relationships are still far and away the most important resources for traders in small caps.

“Traders who have relied mainly on technology for executing their trades may find adjusting to the small cap space challenging initially......”

What sets us apart, I believe, is the strength of our Portfolio Managers in research and analysis. The fact is, market research for small cap stocks is often very limited and the brokers covering these companies can be very thin on the ground. There are often no research reports from external sources available, which means the quality of our own research needs to be world class.

So, the performance of a trader is directly related to the performance of the PMs and the quality of their communications. In this way, our trading desk’s knowledge has been bolstered by regular research meetings where we discuss all manner of topics ranging from broker movements to market flows.

Traders who have relied mainly on technology for executing their trades may find adjusting to the small cap space challenging initially if lacking the fundamental experience and knowledge derived from such close relationships.

Daphne Chang, Dealer, Acorn Capital

GLOBALTRADING | Q1 • 2016

32 | OPINION

liquidity declining (See Figure 3). However, the BTR is biased by a skewed denominator effect. The BTR captures secondary market turnover as a proportion of primary issuances. With record primary issuances, the data highlights that in fact it’s not a question of “less secondary market activity”, but rather of higher primary issuances that have outpaced trading.

Measuring The Impact Of Mutual Funds On BondsShane Worner, Senior Economist, IOSCO examines the impact of asset management flows on bond market liquidity.

In the wake of the crisis of 2008, many economies implemented accommodative monetary policies to help alleviate some of the worst effects of the fallout. These accommodative monetary policies have increased the liquidity of primary market corporate bond issuances, driving down interest rates and ultimately lowering the cost of borrowing associated with corporate bonds.

However, with the US Federal Reserve signalling the normalisation of interest rates, there is continuing concern that the secondary market liquidity has failed to keep up with primary market liquidity and is prone to evaporation. Also in doubt is whether the changing structure of the secondary market will stand up in a stressed scenario. Given their importance to corporate bond markets, the driving factors behind these concerns deserve a closer look.