Embed Size (px)

Citation preview

<Right Click> Minor Committee Name Agenda 9 December 2020

Agenda

BUDGET REVIEW AND EXPENDITURE COMMITTEE MEETING

9 December 2020

Notice of Meeting The next meeting of the Budget Review and Expenditure Committee will take place in the Embleton Room, City of Bayswater Civic Centre, 61 Broun Avenue, Morley, on Wednesday 9 December 2020 commencing at 6:00pm. Yours sincerely

ANDREW BRIEN CHIEF EXECUTIVE OFFICER 3 December 2020

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 2

TABLE OF CONTENTS

ITEM SUBJECT PAGE NO

1. OFFICIAL OPENING 3

2. ACKNOWLEDGEMENT OF COUNTRY 3

3. ATTENDANCE 3

3.1 Apologies 3

3.2 Approved Leave of Absence 3

4. DISCLOSURE OF INTEREST SUMMARY 4

5. DELEGATED AUTHORITY BY COUNCIL 4

6. TERMS OF REFERENCE 4

7. CONFIRMATION OF MINUTES 6

8. REPORTS 7

8.1 Rating Strategy - Rating Method 7

8.2 Capital Works Update 15

8.3 Borrowings 27

8.4 Long-Term Financial Plan Review - Progress Report 34

9. PREVIOUS MATTERS DEALT WITH NOT ON THE AGENDA 41

10. GENERAL BUSINESS 41

11. CONFIDENTIAL ITEMS 41

12. NEXT MEETING 41

13. CLOSURE 41

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 3

AGENDA

1. OFFICIAL OPENING

2. ACKNOWLEDGEMENT OF COUNTRY

In accordance with the City of Bayswater's Reflect Reconciliation Action Plan November 2019- November 2020, the Presiding Member will deliver the Acknowledgement of Country.

Noongar Language

Ngalla City of Bayswater kaatanginy baalapa Noongar Boodja baaranginy, Whadjuk moort Noongar moort, boordiar's koora koora, boordiar's ye yay ba boordiar's boordawyn wah. English Language Interpretation

We acknowledge the Traditional Custodians of the Land, the Wadjuk people of the Noongar Nation, and pay our respects to Elders past, present and emerging.

3. ATTENDANCE

Members

Cr Lorna Clarke Chairperson Cr Dan Bull, Mayor Cr Filomena Piffaretti, Deputy Mayor Cr Stephanie Gray Cr Barry McKenna Cr Steven Ostaszewskyj Officers

Mr Andrew Brien Chief Executive Officer Mr Des Abel A/Director Corporate and Strategy Mrs Linnet Solomon Manager Financial Services Mr Gareth Rozario Management Accountant Ms Cassandra Flanigan Executive Support/Research Officer Ms Carol Newport Personal Assistant Director Corporate and Strategy

3.1 Apologies

3.2 Approved Leave of Absence

Nil.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 4

4. DISCLOSURE OF INTEREST SUMMARY

In accordance with section 5.65 of the Local Government Act 1995: A member who has an interest in any matter to be discussed at a Council or Committee meeting that will be attended by the member must disclose the nature of the interest -

(a) in a written notice given to the CEO before the meeting; or (b) at the meeting immediately before the matter is discussed.

5. DELEGATED AUTHORITY BY COUNCIL

There are no items appearing in this agenda for which the Budget Review and Expenditure Committee has been granted delegated authority by Council in accordance with section 5.23(1)(b) of the Local Government Act 1995; this meeting is closed to the Public.

6. TERMS OF REFERENCE

BUDGET REVIEW AND EXPENDITURE COMMITTEE

1. Objectives The primary objective of the Committee is to provide guidance and oversight as part of the budget process and workshops, as well as review and monitor monthly expenditure and delivery of significant or strategic financial commitments and financial and/or economic impacts on or by the City, of major capital projects.

2. Powers The Committee does not have executive powers or authority to implement actions in areas over which the Chief Executive Officer has legislative responsibility and does not have any delegated responsibility. The Committee does not have any management functions and cannot involve itself in management processes or functions.

3. Membership The Committee will consist of no less than five* Councillors (including the Chair) as sitting members of the Committee at all times, with all Councillors entitled to observe all meetings and access all information provided to the Committee.

All members (other than observers) shall have full voting rights. Tenure of each member of the Committee is in accordance with s5.11 of the Local Government Act 1995 (the Act), and other Councillors are appointed as Deputy Members in accordance with s5.11A of the Act. The Chief Executive Officer and other officers are not members of the Committee. The Chief Executive Officer or their nominee is to be available together with the Director Corporate and Strategy or their nominee to provide advice and guidance to the Committee. Other officers may attend as and when required. The City shall provide such administrative advice as may be required from time to time.

*minimum three required under the legislation.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 5

4. Meetings The Committee will meet no less than six times a year.

5. Order of business The order of business for Committee meetings shall be, or as near thereto as practicable:

Official Opening

Acknowledgement of Country

Attendance

- Apologies

- Approved Leave of Absence

Disclosure of Interest

Terms of Reference

Confirmation of Minutes

Presentations

Deputations

Officer Reports

Confidential Items

Next meeting date and closure

6. Roles and functions

The roles and functions of the Committee in relation to the Budget are to:

(1.)(a) Guide and assist the City in determining the funding requirements for maintaining assets and meeting normal operational requirements;

(1.)(b) Consider funding requirements for capital works projects, including major projects that are at risk of going over budget, and any adjustments required to the scope of major projects to meet budgetary limits;

(1.)(c) Identify any cost offsets, or grant funding opportunities to reduce the financial impact of major projects on the budget and Long Term Financial Plan;

(1.)(d) Review expenditure reprioritisation opportunities to maintain alignment between the Long-Term Financial Plan, Strategic Community Plan, Asset Management Plan, Workforce Plan, Information Communications and Technology Plan and other key planning documents;

(1.)(e) Support the principles of long-term financial sustainability

in the development of the annual budget and rate setting

statement;

(2.) Provide support and direction for the development of

policies relating to the City’s financial sustainability, rating

strategies, grant funding and investments; and

(3.) Review and monitor expenditure reports.

7. Location City of Bayswater Civic Centre

8. Liaison Officer Director Corporate and Strategy

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 6

7. CONFIRMATION OF MINUTES

The Minutes of the meeting of the Budget Review and Expenditure Committee Meeting held on Tuesday, 6 October 2020 which have been distributed, be confirmed as a true and correct record. Moved: Seconded:

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 7

8. REPORTS

8.1 Rating Strategy - Rating Method

Responsible Branch: Financial Services

Responsible Directorate: Corporate and Strategy

Authority/Discretion: ☐ Advocacy

☒ Executive/Strategic

☐ Legislative

☐ Review

☐ Quasi-Judicial

☐ Information Purposes

Voting Requirement: Simple Majority Required

Attachments: Nil.

Refer: Item 8.1: SCM 07.06.2006 – Confidential Report Item 9.5: SCM 04.07.2006 Item 10.6.3.6: OCM 27.10.2020

SUMMARY

A draft 2021-2031 rating strategy is being developed with the aim of equitably, transparently and consistently sharing the cost of rates and charges across the City's ratepayers. To develop the strategy, additional direction from Council is required to determine if it will be based on differential rating or uniform rating. This strategy will help guide future budget and Long-Term Financial Plan preparations. OFFICER'S RECOMMENDATION

That Council requests the Chief Executive Officer to prepare the rating strategy based on a uniform general rate, with consideration given to the phasing out of the COVID-19 concession.

BACKGROUND

The purpose of levying rates is to meet Council's budgetary requirements in each financial year in order to deliver services, facilities and community infrastructure. Property valuations provided by the Valuer General are used as the basis for the calculation of rates each year. The Local Government Act 1995 (the Act) section 6.32 allows local governments to impose a general rate on rateable land within its district which may be uniform or differential. Uniformed rating applies the same rate in the dollar and minimum payment set across the City regardless of the property type/category, while differential rating applies a different rate in the dollar and minimum payment for each category. For example, commercial properties could have a higher rate in the dollar and minimum payment than residential, or vice versa. The differential rating categories must be according to the characteristics stated in the Act, section 6.33. Section 6.36 of the Act requires a minimum notice period of 21 days of the intention to apply differential rates and minimum payments, and must consider any submissions received. The purpose of advertising is to provide ratepayers with the ability to comment and make a submission prior to the rates being formally imposed. On 7 June 2006, Council resolved to change from differential rating to uniform rating. The Council report at that time did not specify the reasons. Prior to the 2006/07 Budget, the differential rating categories were:

Residential - Light Industry

Hotel - General Industry

Business - Special Purpose

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 8

Office - Access Highway

Showroom/Warehouse - Maylands Residential

Public Purpose - Maylands Commercial

Service Station - Maylands Industrial

Council adopted the 2020/21 uniform general rate of 8.311 cents in the dollar on all rateable properties within the district, with the minimum rate being $1,105. A COVID-19 concession applied to ensure that no ratepayer had an annual levy greater than their respective 2019/20 levy, unless there were changes to their property. EXTERNAL CONSULTATION

No consultation has occurred with the public or other agencies on this matter in the development of this report. This matter was discussed at the 6 October 2020 meeting of the Budget Review and Expenditure Committee, and the following was recommended and adopted by Council at its Ordinary Meeting on 27 October 2020: "That Council request the Chief Executive Officer to develop a rating strategy to be presented to

Council by March 2021, which addresses the following

a) Uniform Rating;

b) Differential Rating; and

c) Waste Avoidance and Resources Recovery Levy." If differential rating is the recommended method, the approval from the Minister is required if the imposed differential rate in the dollar is more than twice the lowest differential rate in the dollar as per the Act, section 6.33. Differential rating is required to be advertised for a minimum 21 days, with a public notice published in the local newspaper, and any submissions submitted to Council for consideration. OFFICER'S COMMENTS

The City has a high proportion of residential properties making up 92.31% and a further 2.37% being residential vacant properties. The City has an established rate base and there are limited opportunities available for further developments. The following are statistics in each property type category:

2020/21 Levy

Property Category No. of

Properties

Properties

% $

Revenue

%

Commercial 656 2.03 7,880,020 13.51

Industrial 984 3.05 5,354,644 8.99

Residential 29,829 92.31 41,217,113 75.08

Commercial Vacant Land 10 0.03 65,748 0.11

Industrial Vacant Land 69 0.21 403,362 0.68

Residential Vacant Land 766 2.37 936,326 1.63

COVID-19 Concession - - -6,865,171 -

Total 32,314 100.00 48,992,042 100.00

The rating model is approved by Council as part of the annual budget adoption. The adoption of a rating strategy will assist in providing transparency of the rating model. The rating strategy will

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 9

outline if the City will levy using a uniform rate or differential rating model. The impacts of the two different model types are outlined below. Uniform Rating Model

The benefits of uniformed rating are:

Streamlining the rating process;

Transparency;

Consistency; and

More simple method. The disadvantage of uniformed rating is that every property rate calculation is based on the same rate in the dollar (RID) which does not consider the categories and levels of amenities delivered. Differential Rating Model

The benefit of differential rating is that every ratepayer makes a reasonable contribution to the rate burden. It takes into consideration the levels of service provided to different categories of properties to reflect the cost of provision of services to those categories of properties as well as the need to encourage the specific types of activities within the City. A differential rating model is less advantageous at the current time due to the following:

Majority of the rating database sits within the Residential category;

Limited ability for development within the City; and

More complex method. Scenarios

The following scenarios are based on the 2020/21 Annual Rates levied for illustrative purposes. These scenarios were created to develop an understanding of how categories would be impacted. The total rates income has not been considered in context of the Long-Term Financial Plan as the plan is currently under review. Uniform Rating Model

Scenario One: Uniform general rate, no COVID-19 concession.

Category Type No. of

Properties Properties

% Rate

$'s/RID

Total Levied

$

Levied %

Commercial Minimum Rate 56 0.17 906 50,736 0.10

Commercial Levy 600 1.86 7.390 6,951,716 14.19

Industrial Minimum Rate 34 0.11 906 30,804 0.06

Industrial Levy 948 2.93 7.390 4,698,132 9.59

Residential Minimum Rate 6,195 19.18 906 5,612,670 11.46

Residential Levy 23,631 73.14 7.390 30,447,517 62.14 Commercial Vacant Land Levy 10 0.03 7.390 58,462 0.12

Industrial Vacant Land Levy 69 0.21 7.390 358,662 0.73 Residential Vacant Land Minimum Rate 557 1.72 906 504,642 1.03 Residential Vacant land Levy 209 0.65 7.360 283,754 0.58

32,309 100.00 - 48,997,095 100.00

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 10

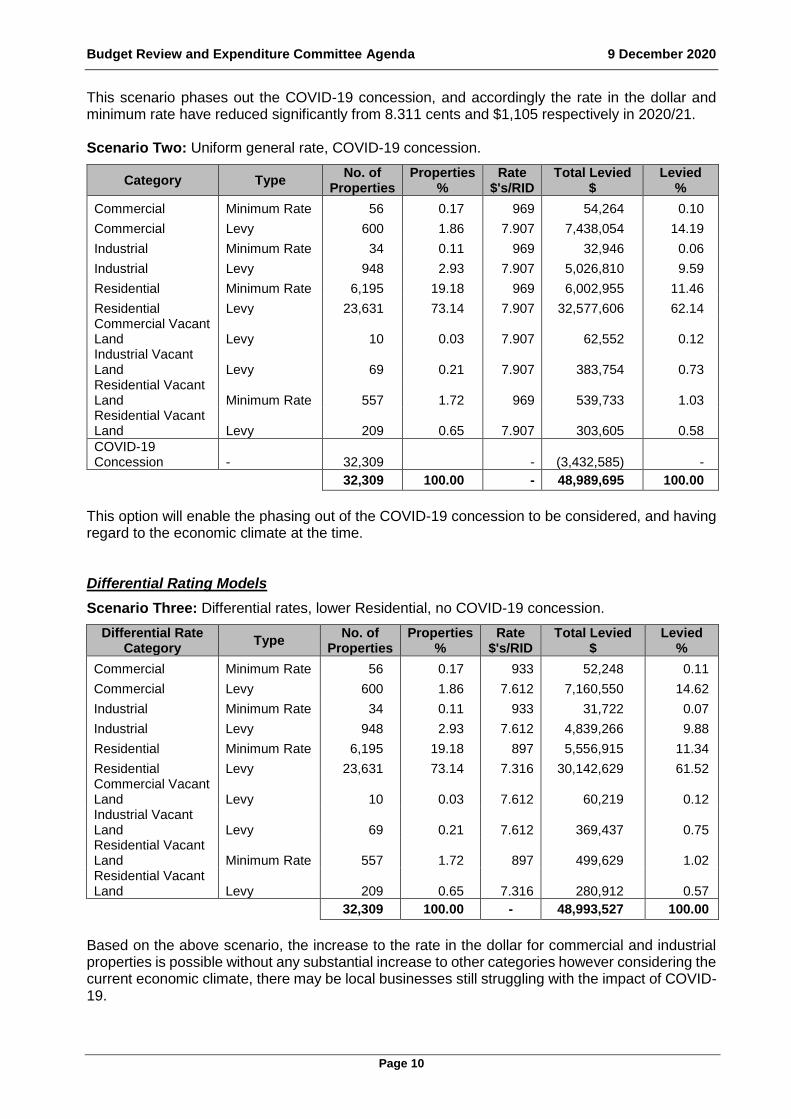

This scenario phases out the COVID-19 concession, and accordingly the rate in the dollar and minimum rate have reduced significantly from 8.311 cents and $1,105 respectively in 2020/21. Scenario Two: Uniform general rate, COVID-19 concession.

Category Type No. of

Properties Properties

% Rate

$'s/RID Total Levied

$ Levied

%

Commercial Minimum Rate 56 0.17 969 54,264 0.10

Commercial Levy 600 1.86 7.907 7,438,054 14.19

Industrial Minimum Rate 34 0.11 969 32,946 0.06

Industrial Levy 948 2.93 7.907 5,026,810 9.59

Residential Minimum Rate 6,195 19.18 969 6,002,955 11.46

Residential Levy 23,631 73.14 7.907 32,577,606 62.14 Commercial Vacant Land Levy 10 0.03 7.907 62,552 0.12 Industrial Vacant Land Levy 69 0.21 7.907 383,754 0.73 Residential Vacant Land Minimum Rate 557 1.72 969 539,733 1.03 Residential Vacant Land Levy 209 0.65 7.907 303,605 0.58

COVID-19 Concession - 32,309

- (3,432,585) -

32,309 100.00 - 48,989,695 100.00

This option will enable the phasing out of the COVID-19 concession to be considered, and having regard to the economic climate at the time. Differential Rating Models

Scenario Three: Differential rates, lower Residential, no COVID-19 concession.

Differential Rate Category

Type No. of

Properties Properties

% Rate

$'s/RID Total Levied

$ Levied

%

Commercial Minimum Rate 56 0.17 933 52,248 0.11

Commercial Levy 600 1.86 7.612 7,160,550 14.62

Industrial Minimum Rate 34 0.11 933 31,722 0.07

Industrial Levy 948 2.93 7.612 4,839,266 9.88

Residential Minimum Rate 6,195 19.18 897 5,556,915 11.34

Residential Levy 23,631 73.14 7.316 30,142,629 61.52 Commercial Vacant Land Levy 10 0.03 7.612 60,219 0.12 Industrial Vacant Land Levy 69 0.21 7.612 369,437 0.75 Residential Vacant Land Minimum Rate 557 1.72 897 499,629 1.02 Residential Vacant Land Levy 209 0.65 7.316 280,912 0.57

32,309 100.00 - 48,993,527 100.00

Based on the above scenario, the increase to the rate in the dollar for commercial and industrial properties is possible without any substantial increase to other categories however considering the current economic climate, there may be local businesses still struggling with the impact of COVID-19.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 11

Scenario Four: Differential rates, lower Residential with COVID-19 concession.

Differential Rate Category

Type No. of

Properties Properties

% Rate

$'s/RID Total Levied

$ Levied

%

Commercial Minimum Rate 56 0.17 998 55,888 0.11

Commercial Levy 600 1.86 8.145 7,661,939 14.62

Industrial Minimum Rate 34 0.11 998 33,932 0.07

Industrial Levy 948 2.93 8.145 5,178,117 9.88

Residential Minimum Rate 6,195 19.18 960 5,947,200 11.34

Residential Levy 23,631 73.14 7.828 32,252,119 61.52 Commercial Vacant Land Levy 10 0.03 8.145 64,435 0.12 Industrial Vacant Land Levy 69 0.21 8.145 395,305 0.75 Residential Vacant Land Minimum Rate 557 1.72 960 534,720 1.02 Residential Vacant Land Levy 209 0.65 7.828 300,572 0.57

COVID-19 Concession - 32,309 - (3,432,585) -

32,309 100.00 - 48,991,642 100.00

The above scenarios affect properties in different ways, however the below table provides examples of properties in different suburbs and different category types, and the impact each model would have on the rates payable.

Suburb & Type 2020/21 Levy

$ Scenario 1

$ Scenario 2

$ Scenario 3

$ Scenario 4

$

Commercial

Dianella 1,941 1,907 1,939 1,964 2,000

Noranda 8,790 9,053 9,686 9,325 9,978

Morley –Minimum 906 906 969 933 998

Bedford –Vacant 3,260 3,584 3,450 3,692 3,565

Industrial

Morley – 5,692 6,096 5,941 6,280 6,137

Bayswater - Minimum 906 906 969 933 998

Maylands – Vacant 1,215 1,367 1,301 1,408 1,345

Residential

Embleton 1,414 1,518 1,477 1,503 1,461

Morley 1,596 1,556 1,588 1,541 1,571

Mount Lawley 1,105 980 1,048 970 1,038

Noranda 1,330 1,287 1,318 1,274 1,305

Morley – vacant 1,074 1,031 1,060 1,021 1,048

Mount Lawley –Vacant 4,526 4,323 4,458 4,280 4,412

Average Increase 2.25% 2.24% 2% 4.78%

Differential general rating on vacant land will not meet section 6.35 of the Act legislation, as it exceeds the 50% threshold and therefore would not be a viable option. Not having a COVID-19 concession for the 2021/22 Budget will be administratively simpler, however the economic impact of the COVID-19 pandemic on the community should be considered. Therefore scenarios 1 and 3 are not recommended.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 12

As a result, the two remaining scenarios are 2 and 4. Both these options recommend phasing out the COVID-19 concession, however scenario 2 is based on uniform rating and scenario 4 is based on differential rating. When comparing the two methods, differential rating is considered more complex and requires additional administration to meet legislations. Although differential rating will enable some categories to have lower rates, it would be at the greater expense of other categories. Given the current economic climate, this would not be a preferred option. In addition, it is considered that the high percentage of residential properties does not provide an adequate mix of properties to fully achieve the benefits of a differential rating model. As a result, scenario 2 is recommended as the most suitable option given all the information outlined in this report. When the economic climate improves, or if legislation changes are implemented, it would be worth re-assessing the City’s rating strategy at that time. LEGISLATIVE COMPLIANCE

"Section 6.33 of the Local Government Act 1995 - Differential general rates

(1) A local government may impose differential general rates according to any, or a combination, of the following characteristics -

a) the purpose for which the land is zoned, whether or not under a local planning scheme or improvement scheme in force under the Planning and Development Act 2005; or

b) a purpose for which the land is held or used as determined by the local government; or

c) whether or not the land is vacant land; or

d) any other characteristic or combination of characteristics prescribed.

….

(3) In imposing a differential general rate a local government is not to, without the approval of the Minister, impose a differential general rate which is more than twice the lowest differential general rate imposed by it."

"Section 6.35 of the Local Government Act 1995 – Minimum payment

…

(3) In applying subsection (2) the local government is to ensure the general minimum is imposed on not less than –

(a) 50% of the total number separately rated properties in the district; or (b) 50% of the number of properties in each category referred to in subsection (6),

on which a minimum payment is imposed." "Section 6.36 of the Local Government Act 1995 - Local government to give notice of certain rates

(1) Before imposing any differential general rates or a minimum payment applying to a differential rate category under section 6.35(6)(c ), a local government is to give local public notice of its intention to do so."

OPTIONS

In accordance with the City’s Risk Management Framework, the following options have been assessed against the City’s adopted risk tolerance. Comments are provided against each of the risk categories.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 13

Option 1 That Council requests the Chief Executive Officer to prepare the rating strategy based on a uniform general rate, with consideration given to the phasing out of the COVID-19 concession.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate Low

Reputation Low Low

Governance Low Low

Community and Stakeholder Moderate Moderate

Financial Management Low Low

Environmental Responsibility Low Low

Service Delivery Low Low

Organisational Health and Safety Low Low

Conclusion The option is considered the simplest, and provides a uniform rate across all properties in the district. This option will enable the phasing out of the COVID-19 concession to be considered, and having regard to the economic climate at the time.

Option 2 That Council requests the Chief Executive Officer to prepare the rating strategy based on differential rating, with the phasing out of the COVID-19 concession.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate Low

Reputation Low Moderate

Governance Low Moderate

Community and Stakeholder Moderate Moderate

Financial Management Low Low

Environmental Responsibility Low Low

Service Delivery Low Low

Organisational Health and Safety Low Low

Conclusion Differential rating is a more complex process, and will require additional administration time to implement. This model may result in some categories paying lower rates at the general expense of other categories. Due to the increased legislative requirements, there is more risk that the rating model will not comply with the Act.

Option 3 That Council requests the Chief Executive Officer to prepare the rating strategy based on an alternative rating model.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate

Risk dependent on alternative model adopted by Council.

Reputation Low

Governance Low

Community and Stakeholder Moderate

Financial Management Low

Environmental Responsibility Low

Service Delivery Low

Organisational Health and Safety Low

Conclusion The overall risk assessment will depend on the alternative rating model adopted by Council.

FINANCIAL IMPLICATIONS

System changes would be required to convert from a uniform rating model to a differential rating model. The cost is estimated to be $15,000. In addition, advertising costs of approximately $800 will be incurred to meet legislative requirements. There is also likely to be an increase in officer time in administering a differential rating model. The uniform rating model is not expected to have any additional financial implications.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 14

STRATEGIC IMPLICATIONS

In accordance with the City of Bayswater Strategic Community Plan 2017-2027 (as amended), the following applies:

Theme: Leadership and Governance Aspiration: Open, accountable and responsive service Outcome L1: Accountable and good governance CONCLUSION

It is considered that the benefits of uniformed rating outweigh those of differential rating. With the property number percentage mainly comprising residential properties, the diversity required for differential rating is not considered adequate and therefore the impact to the rate levy would be insignificant. In addition, phasing out the COVID-19 concession will consider the economic climate.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 15

8.2 Capital Works Update

Responsible Branch: Financial Services

Responsible Directorate: Corporate and Strategy

Authority/Discretion: ☐ Advocacy

☐ Executive/Strategic

☐ Legislative

☐ Review

☐ Quasi-Judicial

☒ Information Purposes

Voting Requirement: Simple Majority Required

Attachments: 1. Capital Expenditure Report as at 11 November 2020

SUMMARY

For the Budget Review and Expenditure Committee and Council to note the Capital Works Update report as at 11 November 2020. OFFICER'S RECOMMENDATION

That Council notes the Capital Works Update report as at 11 November 2020, as contained in this report.

BACKGROUND

Council adopted the 2020/21 Budget at the Special Council Meeting on 30 June 2020, however this was subsequently amended at the Ordinary Council Meeting on 27 October 2020. This report is to update the Committee and Council on the progress of the capital works projects. EXTERNAL CONSULTATION

Nil. OFFICER'S COMMENTS

The progress of capital works against the 2020/21 Budget is detailed in Attachment 1. This report outlines the changing timeframes for the projects. Where there have been changes to the timeframes, the report notes the reasons and provides transparency as to when major spending against the project is estimated to occur. Major concerns, potential carry forwards, changing situations and potential cost savings are noted in the comment section of the report. As the year progresses and more information becomes available, the information will be analysed and reported to the Committee. As part of the City's commitment to continuous improvement, but also to enhance accountability, governance and financial management, the report will continue to be refined to assist the Committee in understanding the progress of the projects. Graph 1 below illustrates the capital works spend by month for the 2020/21 financial year.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 16

Graph 1: Capital Works Budget Spend

Graph 2 illustrates the projects that have commenced. Graph 2: Project Commenced

Analysis of the Capital Works Report as at 11 November 2020 is as follows: Local Stimulus Package

The updates of three major projects that were adopted at part of the Local Stimulus Package at a Special Council Meeting on 5 May 2020, have been listed below.

Maylands Waterland - Redevelopment (Project 80364) - The budget of $2,500,000 is expected to be spent this financial year with $39,744 spent to date (preliminary concept planning is completed with a further $16,786 committed). Statutory approvals are progressing and the Project Manager/Superintendent was appointed at the 27 October 2020 Ordinary Council Meeting. Demolition is anticipated for late December/early 2021, with site works anticipated in January 2021. The project is on track and is scheduled to be completed by October 2021, following construction handover and testing.

Morley Sport and Recreation Centre – Basketball Court Extension (Project 80613) - Architect designs and site surveys are completed with the Project Manager appointed. The construction tender was advertised, and at its Ordinary Meeting held 24 November 2020, Council appointed the building contract to Byte Construction Pty Ltd and approved the

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 17

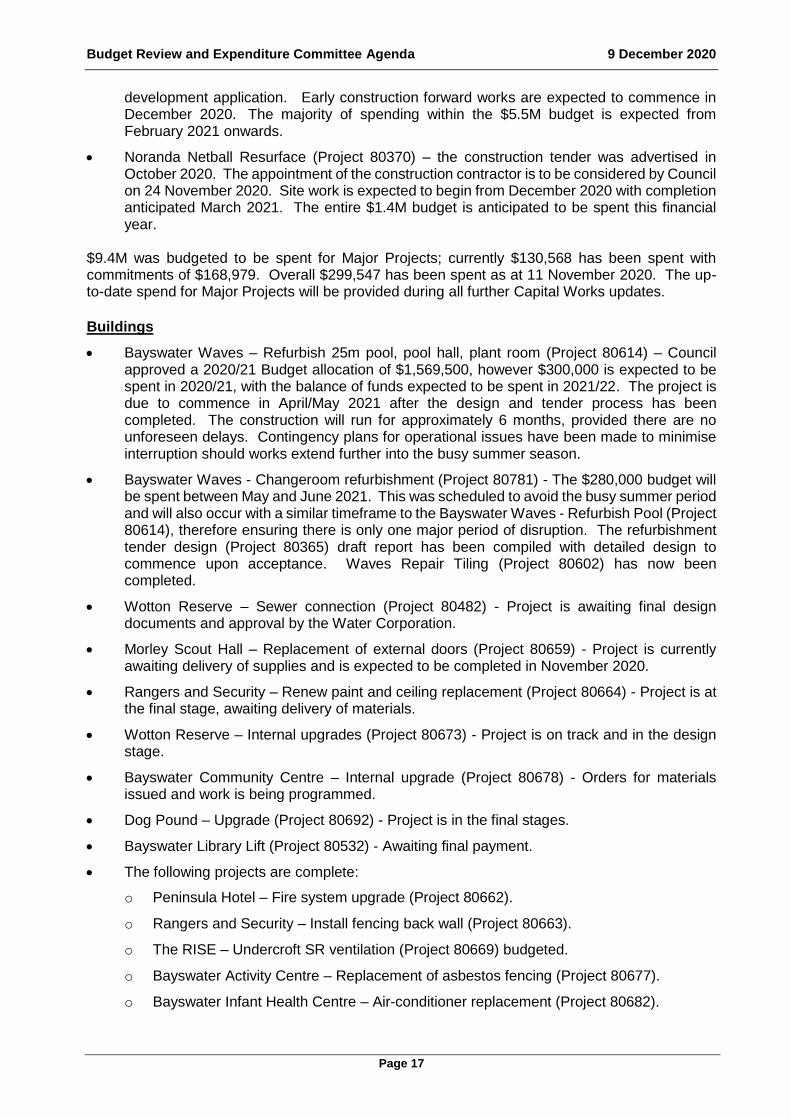

development application. Early construction forward works are expected to commence in December 2020. The majority of spending within the $5.5M budget is expected from February 2021 onwards.

Noranda Netball Resurface (Project 80370) – the construction tender was advertised in October 2020. The appointment of the construction contractor is to be considered by Council on 24 November 2020. Site work is expected to begin from December 2020 with completion anticipated March 2021. The entire $1.4M budget is anticipated to be spent this financial year.

$9.4M was budgeted to be spent for Major Projects; currently $130,568 has been spent with commitments of $168,979. Overall $299,547 has been spent as at 11 November 2020. The up-to-date spend for Major Projects will be provided during all further Capital Works updates.

Buildings

Bayswater Waves – Refurbish 25m pool, pool hall, plant room (Project 80614) – Council approved a 2020/21 Budget allocation of $1,569,500, however $300,000 is expected to be spent in 2020/21, with the balance of funds expected to be spent in 2021/22. The project is due to commence in April/May 2021 after the design and tender process has been completed. The construction will run for approximately 6 months, provided there are no unforeseen delays. Contingency plans for operational issues have been made to minimise interruption should works extend further into the busy summer season.

Bayswater Waves - Changeroom refurbishment (Project 80781) - The $280,000 budget will be spent between May and June 2021. This was scheduled to avoid the busy summer period and will also occur with a similar timeframe to the Bayswater Waves - Refurbish Pool (Project 80614), therefore ensuring there is only one major period of disruption. The refurbishment tender design (Project 80365) draft report has been compiled with detailed design to commence upon acceptance. Waves Repair Tiling (Project 80602) has now been completed.

Wotton Reserve – Sewer connection (Project 80482) - Project is awaiting final design documents and approval by the Water Corporation.

Morley Scout Hall – Replacement of external doors (Project 80659) - Project is currently awaiting delivery of supplies and is expected to be completed in November 2020.

Rangers and Security – Renew paint and ceiling replacement (Project 80664) - Project is at the final stage, awaiting delivery of materials.

Wotton Reserve – Internal upgrades (Project 80673) - Project is on track and in the design stage.

Bayswater Community Centre – Internal upgrade (Project 80678) - Orders for materials issued and work is being programmed.

Dog Pound – Upgrade (Project 80692) - Project is in the final stages.

Bayswater Library Lift (Project 80532) - Awaiting final payment.

The following projects are complete:

o Peninsula Hotel – Fire system upgrade (Project 80662).

o Rangers and Security – Install fencing back wall (Project 80663).

o The RISE – Undercroft SR ventilation (Project 80669) budgeted.

o Bayswater Activity Centre – Replacement of asbestos fencing (Project 80677).

o Bayswater Infant Health Centre – Air-conditioner replacement (Project 80682).

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 18

Upper Hillcrest Reserve – Storage shed (Project 80570) - Awaiting design and final approval.

Depot Offices Renovation (Project 80596) - The renovation of the meeting room, lunch room and open office workroom has been completed. Renovation of the main kitchen and small tearoom areas is programmed to be completed in the coming months.

Energy Efficiency Projects (Project 80619) - The installation has finished at Morley Windmills Soccer Club. Works at the Morley District Cricket Club (Lower Hillcrest Reserve) and Morley Noranda Recreation Club are scheduled to be completed at the end of November to early December 2020.

Bayswater Library Lift (Project 80532), Maylands Tennis Club - toilet renewal (Project 80628), Morley Sport & Recreation Centre - emergency exit door (Project 80609) and Maylands Library - Workroom modification (Project 80606), are showing as overspent. This is mainly due to the distribution of overheads. The overheads budgets will be reviewed as part of the mid-year budget review.

Furniture and Equipment

The four-year replacement program for workstations (Project 80091) is expected to be completed within budget. Virtual Infrastructure Storage (Project 80090) is also progressing well, with equipment being purchased.

Plant and Equipment

In accordance with the plant replacement program, the below items have been purchased year to date:

Description Amount

Hino Truck $71,064

Izuzu Tip Truck $66,093

Golf Course Machinery $46,800

Hyundai Sedan (electric) $43,301

Holden Colorado $39,052

Trailer $22,140

Ford Ranger $35,134

Verti-Drain refurbish $13,637

Toro Mowers $68,370

Sprayrig Fit out $21,361

Small Tools and Accessories $25,357

Total $452,312

Roads, Footpaths and Drainage

Road resurfacing works peak around October to December 2020 as spring is the preferred work period.

Design of a slip lane at 60 Russell Street, corner Walter Road (Project 80426) - The proceedings are ongoing with regard to the developer's obligations and commitments.

Citywide Traffic Program (Project 80291) - The project is ongoing and is being completed within a planned program.

Resurface on McGilvray and Benara (Project 80516) and McGilvray Avenue Stage 2 upgrade (Project 80699) - Progressing well; expected to be completed in December 2020.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 19

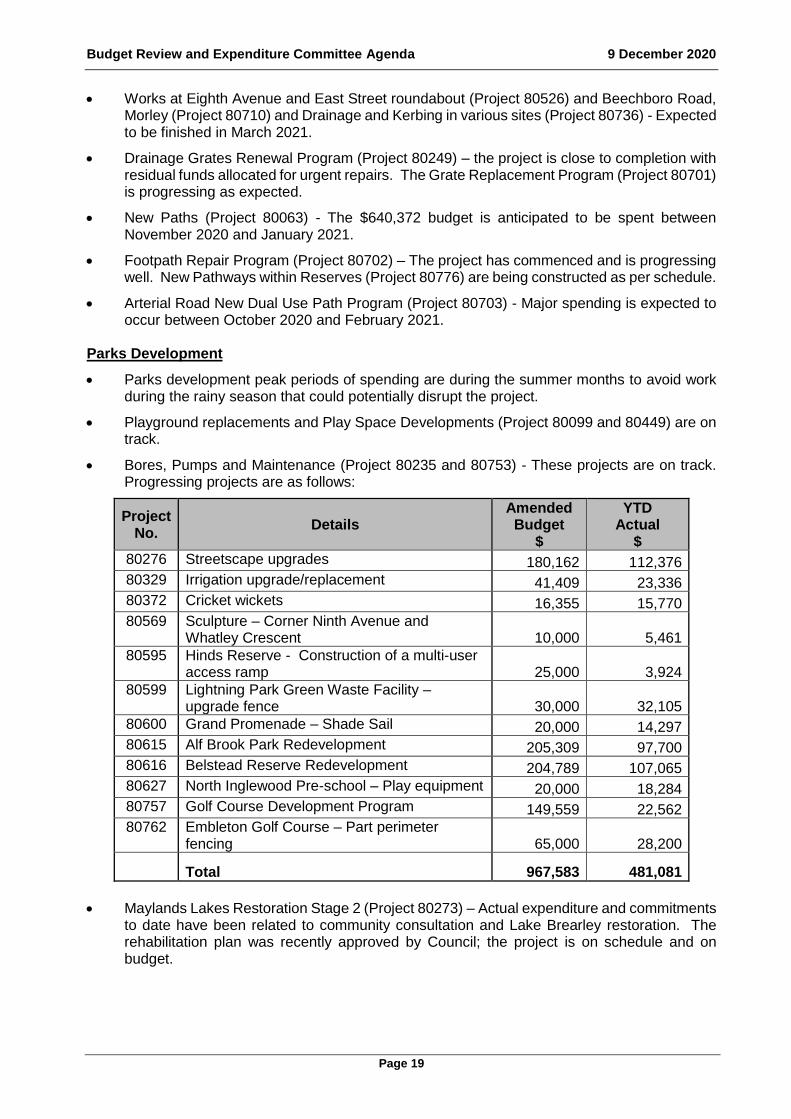

Works at Eighth Avenue and East Street roundabout (Project 80526) and Beechboro Road, Morley (Project 80710) and Drainage and Kerbing in various sites (Project 80736) - Expected to be finished in March 2021.

Drainage Grates Renewal Program (Project 80249) – the project is close to completion with residual funds allocated for urgent repairs. The Grate Replacement Program (Project 80701) is progressing as expected.

New Paths (Project 80063) - The $640,372 budget is anticipated to be spent between November 2020 and January 2021.

Footpath Repair Program (Project 80702) – The project has commenced and is progressing well. New Pathways within Reserves (Project 80776) are being constructed as per schedule.

Arterial Road New Dual Use Path Program (Project 80703) - Major spending is expected to occur between October 2020 and February 2021.

Parks Development

Parks development peak periods of spending are during the summer months to avoid work during the rainy season that could potentially disrupt the project.

Playground replacements and Play Space Developments (Project 80099 and 80449) are on track.

Bores, Pumps and Maintenance (Project 80235 and 80753) - These projects are on track. Progressing projects are as follows:

Project No.

Details Amended Budget

$

YTD Actual

$

80276 Streetscape upgrades 180,162 112,376

80329 Irrigation upgrade/replacement 41,409 23,336

80372 Cricket wickets 16,355 15,770

80569 Sculpture – Corner Ninth Avenue and Whatley Crescent 10,000 5,461

80595 Hinds Reserve - Construction of a multi-user access ramp 25,000 3,924

80599 Lightning Park Green Waste Facility – upgrade fence 30,000 32,105

80600 Grand Promenade – Shade Sail 20,000 14,297

80615 Alf Brook Park Redevelopment 205,309 97,700

80616 Belstead Reserve Redevelopment 204,789 107,065

80627 North Inglewood Pre-school – Play equipment 20,000 18,284

80757 Golf Course Development Program 149,559 22,562

80762 Embleton Golf Course – Part perimeter fencing 65,000 28,200

Total 967,583 481,081

Maylands Lakes Restoration Stage 2 (Project 80273) – Actual expenditure and commitments to date have been related to community consultation and Lake Brearley restoration. The rehabilitation plan was recently approved by Council; the project is on schedule and on budget.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 20

Other Infrastructure

Bayswater Croquet 2 - renew floodlights (Project 80444) - Project completed, with a small overspend. This project was carried forward from last year as the lamps were imported from China; due to COVID-19 they took longer to arrive.

Bayswater Bowling Club - renew floodlights (Project 80443) - Project to be completed in November. This project was carried forward from last year as the lamps were imported from China; due to COVID-19 they were exported late.

Street Light Upgrade/Renewal (Project 80250) - Project is progressing well, however Western Power is increasing the price of their materials. Currently $110,207 has been spent and, at this stage, is expected to be completed within budget.

PAW gates and reserve lighting (Project 80251) and Passive Light Replacement Program (Project 80617) is on track. However, due to the price rise, requests from residents are undertaken on an "as required" basis. It may be beneficial to review funding to provide more street lighting and to upgrade the Morley townsite to LED to reduce carbon emissions as part of the mid-year budget review.

Bedford Bowling Club - path replacement (Project 80610) - Is showing as overspent. This is mainly due to the distribution of overheads. The overheads budgets will be reviewed as part of the mid-year budget review.

Intangible Assets

Library’s Knowledge Management system is at the finalisation stage.

Finance Branch’s Rating system improvement – Stage 1 is progressing as per schedule.

Corporate Performance System (Project 80789) - Evaluation of the project is anticipated between October and November 2020. Appointment of the contractor is expected in December 2020/January 2021, with the project beginning in February 2021.

LEGISLATIVE COMPLIANCE

Nil OPTION

In accordance with the City’s Risk Management Framework, the following option has been assessed against the City’s adopted risk tolerance. Comments are provided against each of the risk categories.

Option 1 That Council notes the Capital Works Report as at 11 November 2020, as contained in this report.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate Low

Reputation Low Low Governance Low Low Community and Stakeholder Moderate Low Financial Management Low Low Environmental Responsibility Low Low Service Delivery Low Low Organisational Health and Safety Low Low Conclusion The Capital Works Report provides an update to Council on the financial position of

each project. The overall assessment is considered low as the report is for noting.

FINANCIAL IMPLICATIONS

The Financial Implications are outlined in Officer's Comments above.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 21

STRATEGIC IMPLICATIONS

In accordance with the City of Bayswater Strategic Community Plan 2017-2027 (as amended), the following applies:

Theme: Leadership and Governance Aspiration: Open, accountable and responsive service Outcome L1: Accountable and good governance CONCLUSION

The Capital Works Report as at 11 November 2020 is presented to the Budget Review and Expenditure Committee and Council for noting.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 22

Attachment 1

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 23

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 24

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 25

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 26

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 27

8.3 Borrowings

Responsible Branch: Financial Services

Responsible Directorate: Corporate and Strategy

Authority/Discretion: ☐ Advocacy

☒ Executive/Strategic

☐ Legislative

☐ Review

☐ Quasi-Judicial

☐ Information Purposes

Voting Requirement: Simple Majority Required

Attachments: Nil

Refer: N/A

SUMMARY

The City is currently undertaking a major review of the Long-Term Financial Plan (LTFP). The review will consider if borrowings should be included in the LTFP. Accordingly Council’s feedback is being sought in relation to including loan funding in the LTFP. OFFICER'S RECOMMENDATION

That Council adopts the utilisation of borrowings as part of the Long-Term Financial Plan for 2021/22 - 2030/31 to:

1. Fund major capital works; and

2. Maintain the Debt Service Cover Ratio and Current Ratio within the recommended benchmark of 2.00 and 1.00 respectively.

BACKGROUND

The City currently has one interest bearing self-supporting loan with the Western Australian Treasury Corporation, which is for Football West. Table 1 below highlights the City's position in respect of the self-supporting loan. Table 1: Current Self-Supporting Loans

Predicted Borrowing Capacity, Forecast Interest Rate and Repayments Amounts

The City's forecast borrowing capacity, based on the prudential limits for the next 10 years, is $30m. For any funds borrowed from the Western Australian Treasury Corporation (WATC), a Guarantee Fee of 0.7% is payable in addition to the interest expense. Table 2 outlines the 10-year forecast borrowing rates provided by the WATC with 0.7% Guarantee Fee and 1-2% tolerance level for rate variance.

Balance Balance Balance

30/06/2020 30/06/2021 30/06/2022

Interest bearing self-supporting loan 6,435$ 1,329$ -$

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 28

Table 2: 10-Year Borrowing Forecast Interest Rates

Tables 3 and 4 outline the total interest and yearly repayment component for a medium-term loan up to 5 years with an interest rate lower than 2%. These figures are indicative only. Table 3: 3-Year Loan Forecast

Table 4: 5-Year Loan Forecast

Financial Year

3 Years

Loan

5 Years

Loan

10 Years

Loan

15 Years

Loan

20 Years

Loan

2020/21 1.44% 1.72% 2.41% 2.98% 3.31%

2021/22 1.45% 1.76% 2.55% 3.12% 3.45%

2022/23 1.58% 1.89% 2.67% 3.22% 3.55%

2023/24 2.27% 2.57% 3.33% 3.87% 4.18%

2024/25 2.46% 2.76% 3.49% 4.01% 4.31%

2025/26 2.65% 2.94% 3.66% 4.15% 4.45%

2026/27 2.84% 3.12% 3.82% 4.29% 4.58%

2027/28 3.52% 3.80% 4.49% 4.93% 5.21%

2028/29 3.71% 3.99% 4.65% 5.08% 5.35%

2029/30 3.90% 4.17% 4.81% 5.22% 5.48%

Interest Rate

Forecast for 3-Years Loan Term

Loan

Threshold

Yearly

Interest

(1.44%)

Yearly

Repayment

(Interest+Prin

ciple)

Yearly

Interest

(1.45%)

Yearly

Repayment

(Interest +

Principle)

Yearly

Interest

(1.58%)

Yearly

Repayment

(Interest +

Principle)

$ $ $ $ $ $ $

1,000,000 28,937 342,979 29,038 343,013 31,765 343,922

2,000,000 57,874 685,958 58,076 686,025 63,530 687,843

3,000,000 86,812 1,028,937 87,115 1,029,038 95,295 1,031,765

4,000,000 115,749 1,371,916 116,153 1,372,051 127,060 1,375,687

5,000,000 144,686 1,714,895 145,191 1,715,064 158,826 1,719,609

6,000,000 173,623 2,057,874 174,229 2,058,076 190,591 2,063,530

7,000,000 202,561 2,400,854 203,267 2,401,089 222,356 2,407,452

8,000,000 231,498 2,743,833 232,306 2,744,102 254,121 2,751,374

9,000,000 260,435 3,086,812 261,344 3,087,115 285,886 3,095,295

10,000,000 289,372 3,429,791 290,382 3,430,127 317,651 3,439,217

Initiated in 2020/21 Initiated in 2021/22 Initiated in 2022/23

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 29

Borrowing Policy

Council, at its Ordinary Council Meeting held on 23 June 2020, resolved to amend the Loan Borrowing Policy to reflect that consideration could only be given to borrowings which are to fund new or major upgrades to City assets or strategic land acquisitions where the City has the capacity to repay the interest on the debt and accumulated cash reserves to ensure full principal repayment upon loan maturity. The Loan Borrowing Policy has broadened the City's ability to borrow, giving the City an additional scope for resourcing. The City can now take advantage of the low cost of finance with current loan rates being competitive with the Western Australian Treasury Corporation (WATC) rates, and using debt as a temporary measure for enhancing its future funding capability given the City's preferred position is to minimise debt. EXTERNAL CONSULTATION

The WATC has been contacted for forecast rate consultation. A comparison of other metropolitan local governments (LGs) was undertaken. Many Western Australian LGs are debt-averse and view the achievement of a low level of debt or even becoming debt-free as a primary goal. Others see the use of loan funding as being a critical component of the funding mix to deliver much-needed infrastructure to the community. The City is considered to be debt-averse based on the historical trend of its debt-free position over the years. Graph 1 highlights the pure dollar value of debt of other metropolitan local governments, which indicates the acceptable median range of debt threshold. Graph 1: Comparisons of Debt for Local Governments

As presented in the above graph, the median range of debt for a local government with an average turnover up to $75 million (similar size) is $11.7 million.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 30

OFFICER'S COMMENTS

The City’s service provision is asset-intensive, and the City's infrastructure assets have average long (but not infinite) useful lives. The financing of the required capital works and new initiatives are municipal funds, grants and contributions, sale of assets and reserve funds (cash-backed). However, the challenge of meeting the yearly funding requirements is growing as a result of the reduction of revenue growth opportunities (e.g. mature rate base) and the resultant limited revenue growth. Borrowings can be used as a viable and equitable mechanism of meeting the funding shortfall gaps for enhancing the long-term financial sustainability of the City without increasing the financial burden of the residents. The City's Loan Borrowing Policy helps to recognise the degree to which borrowing is acceptable, and assists in determining in which circumstances borrowing should be utilised. The City has been adopting a year-on-year approach to budgeting with sufficient cash available to meet the yearly funding for both capital works and initiatives. However, the dwindling balance of the City's cash as a result of the financial implications of year-on-year budgeting, the COVID-19 pandemic, and the limited revenue growth, has negatively impacted on the long-term financial sustainability of the City. The City has limited internal capacity to maintain community infrastructure, therefore leading to substantial renewal gaps, with some assets reaching or going beyond their economic life. The renewal gap is the difference between what the City is currently spending on asset renewal and what is ideally needed to spend given the portfolio of assets. The draft Asset Management Plan indicates an estimated renewal gap for all asset classes, being approximately $4 million in 2020/21. The cumulative renewal gap from 2020/21 to 2029/30 is expected to be approximately $38,015,056 as outlined in the draft Asset Management Plan. However the gap is expected to be higher once a detailed review of the building asset database is completed. The asset expenditure is currently driven by:

The transfer of new assets to the City by State Government and the provision of limited funding, if provided, to only cover short-term operational expenditure;

Council's adoption of projects which will result in new or upgraded assets, both of which will add to future operational costs; and

Operational expenditure driven by the current asset base in the City. City's Philosophy of Debt

The City's Loan Borrowing Policy states that borrowing would only be considered for funding new or major upgrades of City assets or strategic land acquisitions. The key consideration for the City in the utilisation of the borrowed funds is to drive economic growth that will create commercial, residential, employment, community and cultural opportunities. Economic growth can be achieved through major upgrades of the City's assets that will transform a strategic location to become a centre of attraction for both commercial and social activities. On the other hand, strategic land acquisition will require a longer time and higher level of funding for development purposes before a return can be materialised. The use of borrowing to fund capital expenditure can be an effective mechanism of linking the payment for the asset to the successive City populations who receive benefits over the life of the asset. This matching concept is frequently referred to as 'inter-generational equity'. One of the key considerations for the City in the application of future loan borrowings is the premise that its long-term financial strategies should strive for a financial structure where its annual operational and asset renewal needs can be met from annual funding sources. That is, the City

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 31

does not have to access funding from non-renewable sources, such as loans, asset sales or reserves to meet its annual expenditure needs. Appropriate Level of Debt

The City should consider the prudential limits for establishing the maximum levels of debt. It will provide a blanket of comfort for being debt-averse and also mitigating the future risk of using debt as a source for excessive spending on projects and services that are unaffordable or sub-optimal. The prudential principle limits set for Victorian local governments are:

Debt servicing (interest repayments) as a percentage of total revenue should not exceed 5%.

Total debt as a percentage of rate revenue should not exceed 60%.

Current Ratio, also known as the Working Capital Ratio (current assets/current liabilities), to remain in excess of 1.1.

That the City spreads the liability equitably over both current and future years. In Western Australia, the Debt Service Cover Ratio and the Current Ratio are predominately used by local governments. The Department of Local Government and Communities' Long-Term Financial Plan Guidelines recommends the benchmark as:

Debt Service Cover Ratio – 2.00

Current Ratio – 1.00 The City should maintain minimum loan thresholds to ensure that a loan facility is used for major capital expenditure. For consideration of loan funds on capital projects based on funding new/upgrade of major assets that provide a broad community benefit, a minimum loan threshold should be considered. Optimisation of Borrowings

A borrowing rate of lower than 2% is considered to be historically low and is an economically feasible option for the City to optimise borrowings as an opportunity for investment into the future growth of the City. The forecast borrowing rate Table 2 above, indicates that a medium-term loan of 3 to 5 years will achieve a borrowing interest rate below 2 %. The loan entry point is the driver of interest cost with the earliest entry point deriving the highest interest savings.

LEGISLATIVE COMPLIANCE

The Local Government Act 1995 provides as follows:

A local government is empowered to borrow money, obtain credit and arrange for other forms of financial accommodation, to enable it to perform is functions - sec 6.20(1).

The power to borrow cannot be delegated - sec 5.43(f).

The annual budget is to incorporate any proposed borrowing by the local government sec 6.2(4)(d).

Security for any borrowing can only be given over the general funds of the local government - sec 6.21(2).

An absolute majority decision and one month public notice are required for any proposed borrowing that has not been included in the annual budget - sec 6.20(2).

An absolute majority decision and one month public notice are required to change the purpose for which any money, or part thereof, was borrowed - sec 6.20(3), unless the change of purpose has been disclosed in the annual budget - sec 6.20(4).

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 32

In addition, the Local Government (Financial Management) Regulations 1996 require any material variation between actual interest and principal repayment and what is included in budget estimate, to be reported to Council in the Monthly Financial Report. OPTIONS

In accordance with the City’s Risk Management Framework, the following options have been assessed against the City’s adopted risk tolerance. Comments are provided against each of the risk categories.

Option 1 That Council adopts the utilisation of borrowings as part of the Long-Term Financial Plan for 2021/22 - 2030/31 to:

1. Fund major capital works; and

2. Maintain the Debt Service Cover Ratio and Current Ratio within the recommended benchmark of 2.00 and 1.00 respectively.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate Moderate

Reputation Low Low

Governance Low Low

Community and Stakeholder Moderate Low

Financial Management Low Low

Environmental Responsibility Low Low

Service Delivery Low Low

Organisational Health and Safety Low Low

Conclusion The City should take advantage of the low borrowing rates to use borrowings as an alternative funding mechanism to support the strategic growth of the City for long-term financial sustainability. The overall risk rating is considered to be low as considering borrowings as part of the LTFP is the recommended option for the City’s strategic direction and financial management.

Option 2 That Council maintains the current debt-free position in the 2021/22 to 2030/31 Long-Term Financial Plan.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate Moderate

Reputation Low Low

Governance Low Low

Community and Stakeholder Moderate Moderate

Financial Management Low Low

Environmental Responsibility Low Low

Service Delivery Low Moderate

Organisational Health and Safety Low Low

Conclusion This option limits the funding sources to be considered in the LTFP and, as a result, could impact the number of projects which can be funded. In addition the principle of 'inter-generational equity' would not be met.

FINANCIAL IMPLICATIONS

The financial implications are outlined in the report. STRATEGIC IMPLICATIONS

In accordance with the City of Bayswater Strategic Community Plan 2017-2027 (as amended), the following applies:

Theme: Leadership and Governance Aspiration: Open, accountable and responsive service Outcome L1: Accountable and good governance

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 33

The use of borrowings to fund new/significantly upgraded major assets of the City that drive economic growth will indirectly enhance the delivery of the City's Strategic Community Plan. CONCLUSION

The decline in borrowing rates in recent years gives rise to debt as a viable and equitable mechanism of funding major capital projects for local government. The borrowing rates (exclusive of guarantee fee) have fallen to a record-breaking low. It is anticipated that the economic benefits generated from the borrowings will outweigh the costs in most instances, if the LGs adopt effective debt management. As outlined above, a certain level of debt can be viewed as a positive mechanism in financing infrastructure within the City. It is recommended that the City now consider borrowings to support the strategic growth of the City and enhance the long-term financial sustainability of the City.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 34

8.4 Long-Term Financial Plan Review - Progress Report

Responsible Branch: Corporate & Strategy

Responsible Directorate: Financial Services

Authority/Discretion: ☐ Advocacy

☒ Executive/Strategic

☐ Legislative

☐ Review

☐ Quasi-Judicial

☒ Information Purposes

Voting Requirement: Simple Majority Required

Attachments: Nil

Refer Item 8.5 : ARMC 10.11.2020

SUMMARY

The City has commenced a review of the Long-Term Financial Plan. This report is to provide Council an update on the progress of the project and the challenges. OFFICER'S RECOMMENDATION

That Council notes the progress on the review of the Long-Term Financial Plan as contained in this report.

BACKGROUND

The Integrated Planning and Reporting (IPR) Framework, is a framework developed by the State Government that came into effect in July 2013. The IPR is to ensure all local governments plan responsibly for the future and equip their organisations to respond to short, medium and long-term community needs. The Long-Term Financial Plan (LTFP) is an indicator of a local government's long-term financial sustainability as well as a dynamic tool for setting priorities. Therefore, the LTFP is an integral part of the local government's strategic planning process and aligns to other core planning documents as set out in the IPR framework. The City has commenced a review of the 2017/18 to 2026/27 LTFP. A revised plan will be required to be developed based on the methodology and format set within the IPR framework. The LTFP will include the proposed plans, and the financial analysis of all strategic objectives and goals set out in the integrated framework documents over ten years. The plan will align with the core planning documents, including the Strategic Community Plan and the Corporate Business Plan. Information contained in other strategic plans, including the Asset Management Plan and Workforce Plan will inform the LTFP, which is the basis for the preparation of the City’s Annual Budgets. The City's LTFP was developed in 2017 and has not been updated. As a result, the plan is now disintegrated from the City's core planning documents (e.g. Strategic Community Plan, Corporate Business Plan). The City has been relying on the 'annual budget' to 'annual budget' for setting priorities which are based on a short-term financial approach. It is considered that the short-term financial approach and the disintegration of the core planning documents to the LTFP has had a significant influence on the long-term financial sustainability of the City. In March 2020, Paxon Group was engaged to undertake a review of the financial sustainability of the City. The report presented to the 10 November 2020 Audit and Risk Management Committee recommended that an up-to-date LTFP with integration to all core planning documents should be in place. The LTFP will assist the City to have a long-term focus on the financial sustainability to support the community's needs of today and into the future. A fixed-term contractor has been engaged to assist in the review and development of the LTFP. The first draft of the plan will be submitted for Council review by mid-February 2021.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 35

EXTERNAL CONSULTATION

No consultation has occurred with the public or other agencies on this matter. OFFICER'S COMMENTS

The development of a comprehensive and integrated LTFP represents an opportunity for the City to enter into a more structured and rigorous planning and delivery cycle. The LTFP will help the City to align its financial capacity with long-term service objectives instead of short-term. It will be used as a tool to address financial challenges, stimulate long-term and strategic thinking and also give consensus on long-term financial direction. Forecasts are used to provide insight into future financial capacity so that strategies can be developed to achieve long-term sustainability. The forecasts are developed based on a set of fundamental assumptions and objectives linking to the City's core planning documents. The plan predicts the operational and capital needs placed on the City from period 2021/22 to 2030/31. The predictions are driven by the economic and social environment indicators, including the WALGA Local Government Cost Index, Consumer Price Index, interest rates, employment levels, population growth and demographic change. The preparation of the LTFP is underpinned by the City Strategic Budget policy adopted on 28 January 2020. The LTFP highlights linkages between specific plans and strategies and enhances the transparency and accountability of the City to the community, and works towards achieving the following objectives:

The achievement of a prudent balance between meeting the service needs of our community

(both now and future) and remaining financially sustainable for future generations.

An increased ability to fund both capital works in general and meet the asset renewal

requirements as outlined in asset management planning.

Endeavouring to maintain a sustainable City in an environment where Council must either

constrain its net operational costs or reduce funds available to capital expenditure due to the

expectations of maintaining a low level of rate increases combined with reducing levels in

government grant funding.

The following financial principles adopted in the City’s Strategic Budget Policy are embedded in the LTFP: Principle 1: Recurring income must exceed recurring expenditure. Principle 2: Each of the City's service delivery activities is to be cost and quality competitive whilst controlling City Operating costs. Principle 3: Asset renewal must have higher priority than the creation of new assets. Principle 4: Reserves are to be accumulated and allocated in accordance with Council resolution (OCM August 2017). Principle 5: New income - producing opportunities are to be identified and returns on City commercial property holdings are to be optimised. Principle 6: The uses of debt, internal borrowing and private financing are to be considered where appropriate. Principle 7: The Department of Local Government, Sport and Cultural Industries' key performance indicators are to be met (refer mycouncil.wa.gov.u).

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 36

From the review of the long-term financial sustainability of the City, based on the current financial position, the following financial strategies are proposed to be adopted in the LTFP for working towards the targeted goals:

Diversification of the revenue source of the City to increase growth opportunities.

Optimising returns for cash investments whilst complying with the objectives to:

o Safeguard the City's cash and investment portfolio; and

o Ensure liquidity for the City's business objectives over the long, medium and short term.

An effective operating model with an emphasis on cost recovery and cost savings.

Loan borrowing as part of the strategy planning for:

o Major capital works including infrastructure renewal gaps; and

o Investments to assist diversification of its revenue base.

Ultimately, the LTFP will drive the following outcomes for the City:

establish a prudent and sound financial framework, combining and integrating financial

strategies to achieve a planned outcome;

establish a financial framework against which the City’s strategies, policies and financial

performance can be measured against;

ensure that the City complies with sound financial management principles, as required by the

Local Government Act 1995 and plan for the long-term financial sustainability of Council; and

allow Council to meet the objectives of the Local Government Act 1995 to promote the social,

economic and environmental viability of the district.

Overall, the review of the LTFP will include a number of challenges as outlined below. Rate Revenue

Rates revenue is the City’s predominate revenue source, therefore rate setting is considered the single highest risk to revenue growth. The identified limitations in rate growth are as follows:

Mature rate base and limited opportunities exist for further developments which may increase

the rate base; and

Rate setting takes place in a rigid environment, including legal constraints, the financial

capacity of ratepayers to accept rate increase and the political environment.

Fees and Charges

Fee and charges is another main driver and contributed 23% to the revenue. However, services were provided exclusively for the benefit of the community or other government tiers without taking into consideration the cost of recovery. The Paxon internal audit report recommended the City complete a review of the Fees and Charges schedule, and service of a private nature be reviewed. The review will commence in early 2021, however will not be completed for the review 2021/22 to 2030/31 LTFP. However, the underlying principles of cost recovery for a number of fees needs to be incorporated into the LTFP. Interest Earning

In recent times, the Reserve Bank of Australia has had historically record low interest rates. As a result, the interest earning for the City is expected to be low for some time, therefore impacting on the City’s overall income.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 37

Asset Management and Renewal Gaps

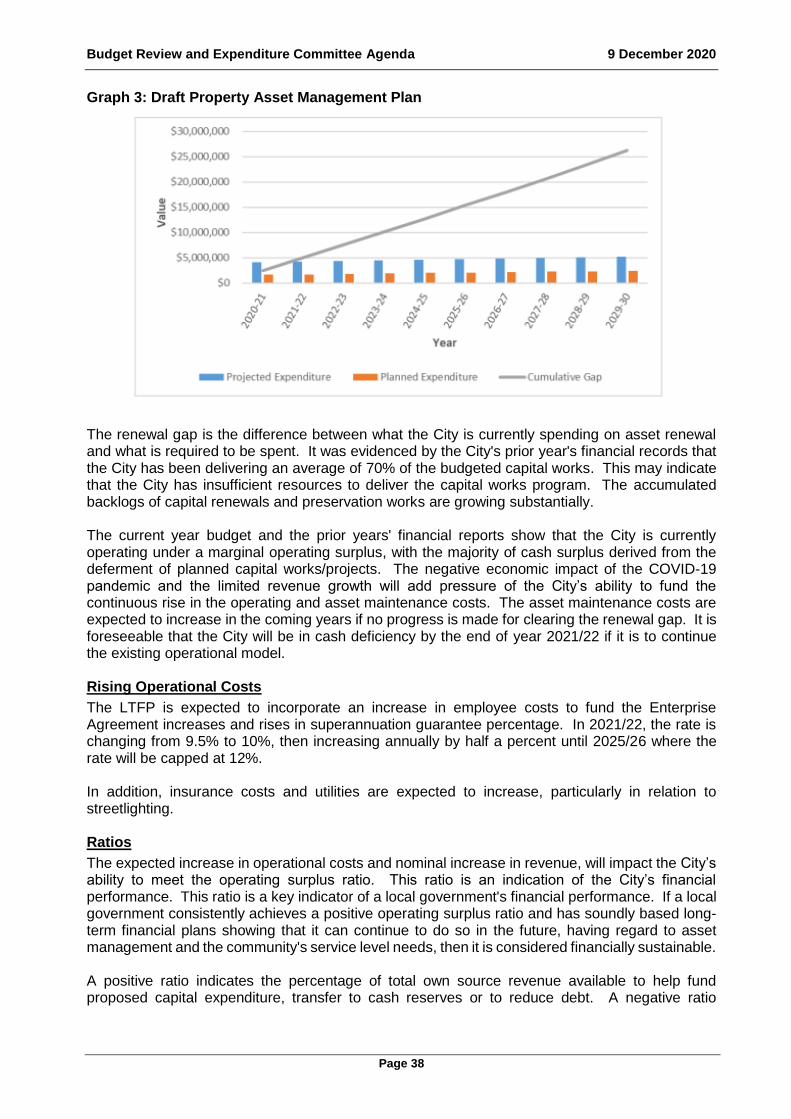

The City is working on limited resources for maintaining a sizeable community infrastructure with some reaching or going beyond their economic life. The latest version of the draft Asset Management Plans shows an estimated renewal gap for all classes of assets of up to $4 million in FY 2020/21. Overall the estimated renewal gaps as outlined in the draft Asset Management Plans are outlined in the Graphs 1 to 3. Graph 1: Draft Transport Asset Management Plan

Graph 2: Draft Recreation Asset Management Plan

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 38

Graph 3: Draft Property Asset Management Plan

The renewal gap is the difference between what the City is currently spending on asset renewal and what is required to be spent. It was evidenced by the City's prior year's financial records that the City has been delivering an average of 70% of the budgeted capital works. This may indicate that the City has insufficient resources to deliver the capital works program. The accumulated backlogs of capital renewals and preservation works are growing substantially. The current year budget and the prior years' financial reports show that the City is currently operating under a marginal operating surplus, with the majority of cash surplus derived from the deferment of planned capital works/projects. The negative economic impact of the COVID-19 pandemic and the limited revenue growth will add pressure of the City’s ability to fund the continuous rise in the operating and asset maintenance costs. The asset maintenance costs are expected to increase in the coming years if no progress is made for clearing the renewal gap. It is foreseeable that the City will be in cash deficiency by the end of year 2021/22 if it is to continue the existing operational model. Rising Operational Costs

The LTFP is expected to incorporate an increase in employee costs to fund the Enterprise Agreement increases and rises in superannuation guarantee percentage. In 2021/22, the rate is changing from 9.5% to 10%, then increasing annually by half a percent until 2025/26 where the rate will be capped at 12%. In addition, insurance costs and utilities are expected to increase, particularly in relation to streetlighting. Ratios

The expected increase in operational costs and nominal increase in revenue, will impact the City’s ability to meet the operating surplus ratio. This ratio is an indication of the City’s financial performance. This ratio is a key indicator of a local government's financial performance. If a local government consistently achieves a positive operating surplus ratio and has soundly based long-term financial plans showing that it can continue to do so in the future, having regard to asset management and the community's service level needs, then it is considered financially sustainable. A positive ratio indicates the percentage of total own source revenue available to help fund proposed capital expenditure, transfer to cash reserves or to reduce debt. A negative ratio

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 39

indicates the percentage increase in total own source revenue (principally rates) that would have been required to achieve a break-even operating result. The benchmark set by the Department of Local Government, Sport and Cultural Industries is between 1% and 15% (0.01 and 0.15) basic standard, and greater than 15% (>0.15) for advanced Standard. In addition, the assets ratios need to be strongly considered as part of the LTFP. With the expected increase in the City’s renewal gap, the City’s ability to meet the asset ratios will be challenged. The three asset ratios are:

1. Asset Renewal Funding Ratio

This ratio indicates whether the local government has the financial capacity to fund asset renewal as required, and can continue to provide existing levels of services in future, without additional operating income; or reductions in operating expenses.

2. Asset Consumption Ratio

This ratio seeks to highlight the aged condition of a local government's assets. If a local

government is responsibly maintaining and renewing/replacing its assets in accordance with

a well-prepared asset management plan, then the fact that its Asset Consumption Ratio may

be relatively low and/or declining should not be cause for concern – providing it is operating

sustainably.

3. Asset Sustainability Ratio

This ratio indicates whether a local government is replacing or renewing existing assets at the same rate that its overall assets are wearing out.

Diversification of Revenue

The Paxon internal audit report recommended the City consider loan borrowings. This would assist in the diversification of revenue sources and ensure financial sustainability. In addition, the internal audit report also recommended that the City examine opportunity for partnerships and commercial activities. As opportunities are identified, the LTFP will be updated. LEGISLATIVE COMPLIANCE

All local governments are required to have to plan for the future of their district under section 5.56 (1) of the Local Government Act 1995. Regulations under section 5.56(2) of the Act outline the minimum requirements to achieve this. Although the minimum requirement of the plan for the future is the development of a Strategic Community Plan and a Corporate Business Plan, a LTFP is recommended as part of the IRR Framework. OPTIONS

In accordance with the City’s Risk Management Framework, the following option has been assessed against the City’s adopted risk tolerance. Comments are provided against each of the risk categories.

Option 1 That Council notes the progress on the review of the Long-Term Financial Plan as contained in this report.

Risk Category Adopted Risk Appetite Risk Assessment Outcome

Strategic Direction Moderate Low

Reputation Low Low

Governance Low Low

Community and Stakeholder Moderate Low

Financial Management Low Low

Environmental Responsibility Low Low

Service Delivery Low Low

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 40

Organisational Health and Safety Low Low

Conclusion That Council notes the update on the LTFP and the challenges expected in developing a balanced and sustainable plan. The overall assessment is considered low as the report is to update Council on the review of the LTFP. The report outlines the internal audit recommendation from Paxon which will be addressed as part of the review.

FINANCIAL IMPLICATIONS

The Long-Term Financial Plan will help to improve the financial position of the City if a thorough process is followed through consistently. STRATEGIC IMPLICATIONS

The Long-Term Financial Plan will stimulate long-term and strategic thinking and also give consensus on long-term financial direction. In accordance with the City of Bayswater Strategic Community Plan 2017-2027 (as amended), the following applies:

Theme: Leadership and Governance Aspiration: Open, accountable and responsive service Outcome L1: Accountable and good governance CONCLUSION

The City has progressed the LTFP major review, however, as outlined in the report a number of challenges are expected.

Budget Review and Expenditure Committee Agenda 9 December 2020

Page 41

9. PREVIOUS MATTERS DEALT WITH NOT ON THE AGENDA

Reconciliation of matters arising from past meetings: Nil.

10. GENERAL BUSINESS

Nil.

11. CONFIDENTIAL ITEMS

Nil.

12. NEXT MEETING

The next meeting of the Budget Review and Expenditure Committee will be held at a time and on a date to be determined.

13. CLOSURE