Embed Size (px)

Citation preview

© PYRAMID RESEARCH 2011 ID# 1010

HIGHLIGHTS Brazil is undergoing a cultural and economic transformation that is making it possible for many to have access to telecom services, including broadband, pay-TV and advanced mobile services. In order to address the many segments now existing in Brazil, operators are being pushed to segment their offers and complement their portfolio with services that appeal to the many existing income levels. In the past year, the mobile and pay-TV offers that succeeded the most were those that had a segmentation logic built into their strategies, addressing a portion of the population that before couldn’t afford these services. The government is also taking several actions to facilitate the telecom market development in Brazil. Among these actions, we find a national broadband plan, faster action on spectrum licensing, and tax incentives for national manufacturing of smartphones and tablets.

Vol. 3, No. 8, December 2011

Brazilian Operators Target Diverse and Growing Telecom Market with Creative Offers

TABLE OF CONTENTS

INTRODUCTION 2

TELECOM IN BRAZIL 3 A. Data services will drive strong growth in mobile revenues 3 B. DTH services will dominate the pay-TV market 5 C. Government incentives are promoting additional investment in the sector 6

MARKET DETAIL 8 CASE STUDY: TIM Brazil regains the second position in mobile services in Brazil through segmentation of its services 8 CASE STUDY 2: Telefônica launches different pay-TV services to address different types of customers 10

KEY FINDINGS 12

RELATED RESOURCES 13

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 2

Introduction The perception of Brazil around the world has changed greatly in the past decade. While some may consider it a poor market due to its historically low GDP per capita and relatively low scores on the UN Human Development Index, the economic situation in the country is certainly changing and improving. Brazil’s size and market potential place the country in a unique position, especially considering the increasing demand and purchasing power of traditionally disadvantaged or middle- to lower-income socioeconomic classes. When it comes to telecommunications services, extreme price sensitivity and low service penetration may not be the norm any longer. Despite the country’s reputation for sharp income disparities and poverty levels, Brazil has gained a reputation for having the highest iPhone and iPad prices in the world. And as in any other country, these gadgets attract a crowd of technology fans that line up for hours and empty out any stock that stores and operators might have. There are many studies remarking how expensive broadband is in Brazil, and how Brazilians pay more for lower-quality services. Some studies blame it on taxes, some blame it on the operators’ profit margins. But the bottom line is that telecom services are indeed more expensive, and Brazilians are using those services more than ever before. How can such an underdeveloped country with so many socioeconomic problems have millions demanding these expensive telecom products and services? And where is this demand coming from? Today Brazil is undergoing a cultural and economic transformation that is making it possible for more and more people to have access to basic services. What many didn’t expect, however, is that services before considered a privilege of the richest social strata ― including telecom services such as mobile telephony, the Internet and pay-TV ― are rapidly joining the “basic” category and becoming a part of basic consumption for most in the country. Infrastructure was also an issue preventing many Brazilians from having access to telecom services. However, the government is giving clear signs that it is extremely committed to changing this situation. This commitment, which many Brazilians found hard to believe due to decades of unkept promises, is now visible. Despite being late, the 3G licenses auction in 2009 was a success, resulting in a very positive deployment of 3G networks that are now being used by 61m subscribers. The same is expected to happen with 4G/LTE. The frequencies auction scheduled for 2011 was delayed, but the government is pushing it to happen soon so that the all cities that will host FIFA World Cup in 2014 to have LTE coverage. While the push for LTE has been aimed at meeting the needs of those coming to the country especially for the World Cup, the benefits of these deployments will last well after the event is over. Laws regarding pay-TV services were also changed in order to spur service penetration. The ban on incumbents offering IPTV in their incumbency area was lifted, so these operators can now compete against traditional pay-TV players that dominate the market. Unlike in previous years, telecom providers in the country are also aware of the market changes and are doing what it takes to meet market expectations. Even before the bidding for 4G licenses begins, we can already see 4G deployments in alternative frequencies. For these reasons, Pyramid Research believes that Brazil will remain the largest market for telecommunications in Latin America. With the expansion of the services to additional areas and lower-income segments, ARPS can go down, although revenues will significantly increase.

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 3

Telecom in Brazil The telecom services market in Brazil has been experiencing an exciting growth pattern in past years, and the future outlook for the country remains very positive. The country has been experiencing a significant enrichment of the middle and lower classes, and more and more services are being customized to address that demand. It is interesting that the telecom services catering to these newly empowered segments are not only low-cost/low-quality in nature. We often see offers that actually are lower in price, but many of them also include value-added service (VAS) components that before were limited to the nation’s rich. Among these new services, we can highlight mobile plans that include limited or prepaid mobile broadband, and pay-TV, which is now available in digital format to most of the country through DTH, even with limited premium channels. The effort from operators to address that new segment is also forcing them to offer better and faster services that appeal to higher-income segments. Among these services we find IPTV and 4G. Some of these new services have had to overcome regulatory or spectrum availability impediments in the past, but the market is pushing for these to be quickly deployed. In this Insider we will discuss the reasons behind the development of many of the telecom services Brazilians now enjoy. The focus will be on mobile and pay-TV services, as well as on government initiatives to modernize and liberalize the nation’s telecom networks. The report closes with a series of case studies on TIM Brazil and Telefônica, two operators at the center of the telecom transformation in Brazil.

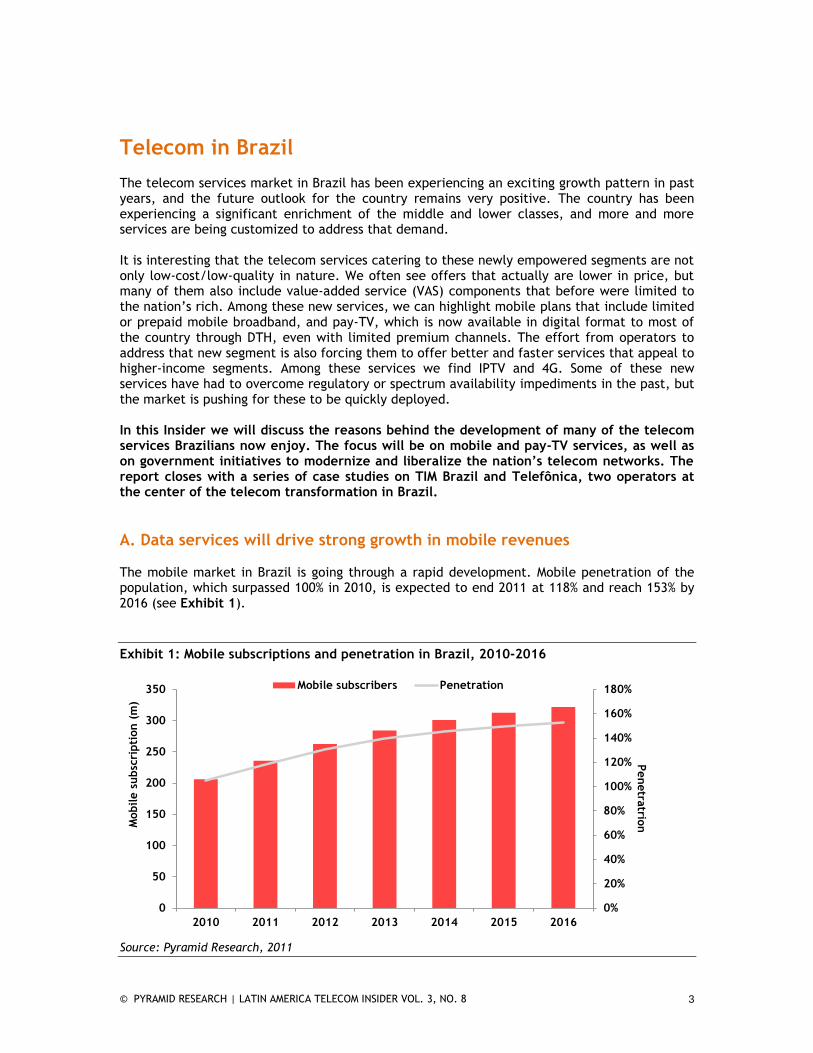

A. Data services will drive strong growth in mobile revenues The mobile market in Brazil is going through a rapid development. Mobile penetration of the population, which surpassed 100% in 2010, is expected to end 2011 at 118% and reach 153% by 2016 (see Exhibit 1).

Exhibit 1: Mobile subscriptions and penetration in Brazil, 2010-2016

Source: Pyramid Research, 2011

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016

Penetra

trionM

obile s

ubsc

ripti

on (

m)

Mobile subscribers Penetration

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 4

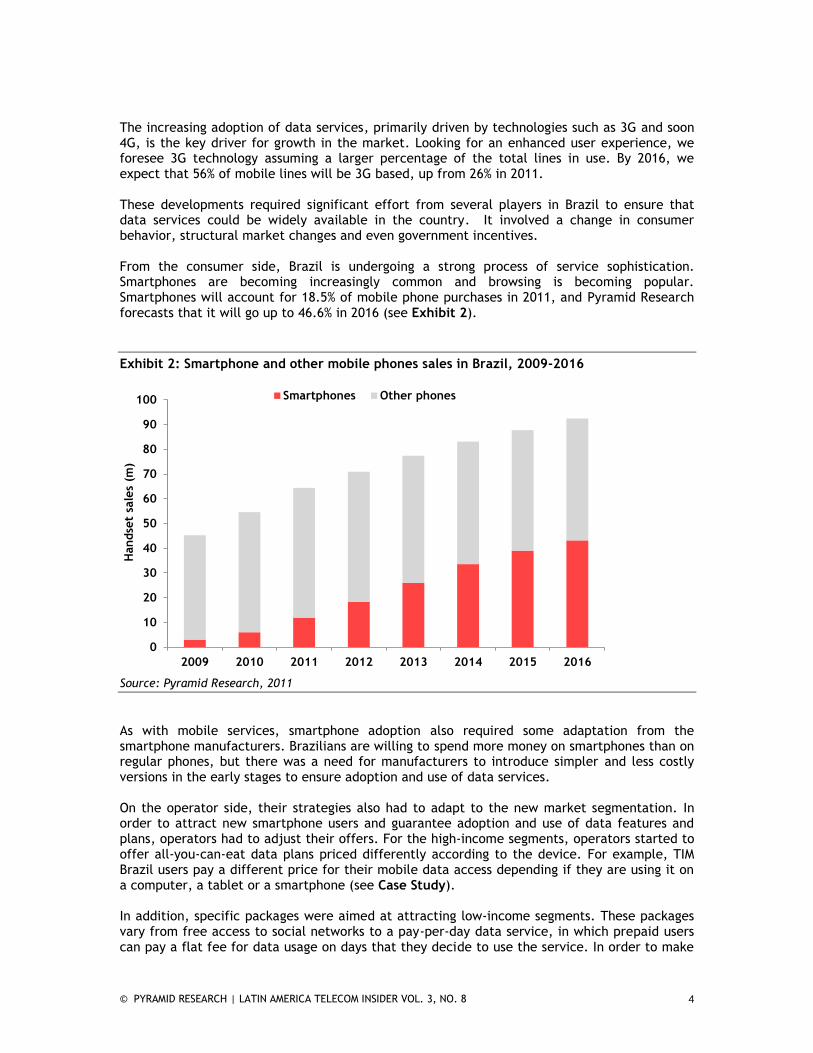

The increasing adoption of data services, primarily driven by technologies such as 3G and soon 4G, is the key driver for growth in the market. Looking for an enhanced user experience, we foresee 3G technology assuming a larger percentage of the total lines in use. By 2016, we expect that 56% of mobile lines will be 3G based, up from 26% in 2011. These developments required significant effort from several players in Brazil to ensure that data services could be widely available in the country. It involved a change in consumer behavior, structural market changes and even government incentives. From the consumer side, Brazil is undergoing a strong process of service sophistication. Smartphones are becoming increasingly common and browsing is becoming popular. Smartphones will account for 18.5% of mobile phone purchases in 2011, and Pyramid Research forecasts that it will go up to 46.6% in 2016 (see Exhibit 2).

Exhibit 2: Smartphone and other mobile phones sales in Brazil, 2009-2016

Source: Pyramid Research, 2011

As with mobile services, smartphone adoption also required some adaptation from the smartphone manufacturers. Brazilians are willing to spend more money on smartphones than on regular phones, but there was a need for manufacturers to introduce simpler and less costly versions in the early stages to ensure adoption and use of data services. On the operator side, their strategies also had to adapt to the new market segmentation. In order to attract new smartphone users and guarantee adoption and use of data features and plans, operators had to adjust their offers. For the high-income segments, operators started to offer all-you-can-eat data plans priced differently according to the device. For example, TIM Brazil users pay a different price for their mobile data access depending if they are using it on a computer, a tablet or a smartphone (see Case Study). In addition, specific packages were aimed at attracting low-income segments. These packages vary from free access to social networks to a pay-per-day data service, in which prepaid users can pay a flat fee for data usage on days that they decide to use the service. In order to make

0

10

20

30

40

50

60

70

80

90

100

2009 2010 2011 2012 2013 2014 2015 2016

Handse

t sa

les

(m)

Smartphones Other phones

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 5

this service as easy as possible, there is no need for activation; customers just pay around US$0.27 on days that they use it. While we expect fixed telecom service revenue to grow 2.3% from 2011 to 2016, reaching $32.4bn, mobile service revenue will grow 24% in the same period, reachingS$46.4bn. Much of this revenue growth will come from data, which will jump from $8.9bn in 2011 to $17.3bn in 2016, driven by the increasing number of subscribers that will join the service as device prices go down and more mobile applications become available.

Exhibit 3: Mobile services revenues in Brazil, 2010-2016

Source: Pyramid Research, 2011

B. DTH services will dominate the pay-TV market After years of low penetration, pay-TV is becoming a popular service in Brazil. This service, which spent more than a decade divided among high-end cable options and expensive DTH services, is now adapting to cater to a larger section of the population. Until recently, fixed telecom incumbents were prohibited from offering pay-TV in their areas, unless they did it through DTH. That rule scared away fixed operators that would have needed to deploy a new network outside of their original coverage or set up a DTH infrastructure, with no synergy with their existing network. For years that restriction kept the pay-TV market restricted to pay-TV operators, which can operate on the fixed telephony and broadband market. This restriction played an important role on the popularization of broadband in Brazil, which is why it was kept in place. On the other hand, it held the pay-TV market hostage to a few companies. The broadband market benefitted from competition between the fixed and pay-TV operators. In fact, pay-TV operators set some important standards in the Brazilian telecom services market, such as megabit speeds for broadband and unlimited intra-network calls among fixed phones.

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2016

Serv

ice r

evenues

(US$bn)

Mobile voice Mobile data

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 6

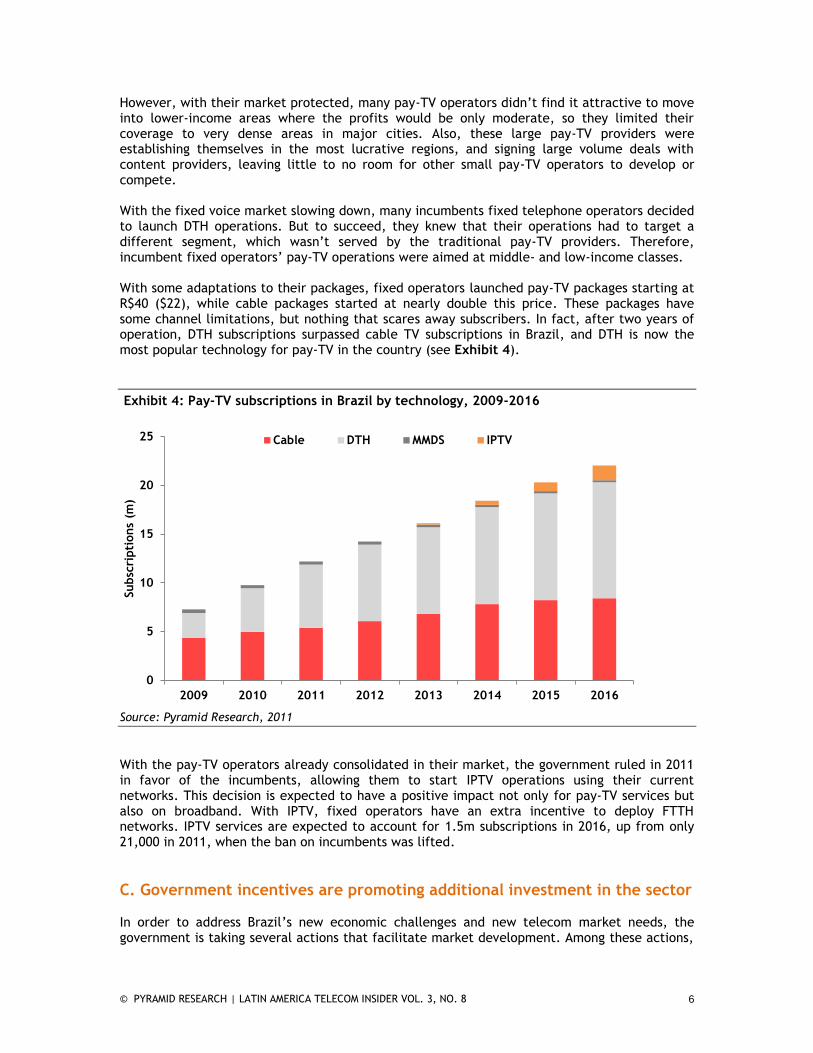

However, with their market protected, many pay-TV operators didn’t find it attractive to move into lower-income areas where the profits would be only moderate, so they limited their coverage to very dense areas in major cities. Also, these large pay-TV providers were establishing themselves in the most lucrative regions, and signing large volume deals with content providers, leaving little to no room for other small pay-TV operators to develop or compete. With the fixed voice market slowing down, many incumbents fixed telephone operators decided to launch DTH operations. But to succeed, they knew that their operations had to target a different segment, which wasn’t served by the traditional pay-TV providers. Therefore, incumbent fixed operators’ pay-TV operations were aimed at middle- and low-income classes. With some adaptations to their packages, fixed operators launched pay-TV packages starting at R$40 ($22), while cable packages started at nearly double this price. These packages have some channel limitations, but nothing that scares away subscribers. In fact, after two years of operation, DTH subscriptions surpassed cable TV subscriptions in Brazil, and DTH is now the most popular technology for pay-TV in the country (see Exhibit 4).

Exhibit 4: Pay-TV subscriptions in Brazil by technology, 2009-2016

Source: Pyramid Research, 2011

With the pay-TV operators already consolidated in their market, the government ruled in 2011 in favor of the incumbents, allowing them to start IPTV operations using their current networks. This decision is expected to have a positive impact not only for pay-TV services but also on broadband. With IPTV, fixed operators have an extra incentive to deploy FTTH networks. IPTV services are expected to account for 1.5m subscriptions in 2016, up from only 21,000 in 2011, when the ban on incumbents was lifted.

C. Government incentives are promoting additional investment in the sector In order to address Brazil’s new economic challenges and new telecom market needs, the government is taking several actions that facilitate market development. Among these actions,

0

5

10

15

20

25

2009 2010 2011 2012 2013 2014 2015 2016

Subsc

ripti

ons

(m)

Cable DTH MMDS IPTV

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 7

we find a coherent national broadband plan, faster regulatory action on spectrum licensing and tax incentives for national manufacturing of smartphones and tablets. The Brazilian mobile market is becoming so attractive that many traditional smartphone manufacturers, which had no interest to develop a local presence in Brazil, are now present or considering a having assembly lines in the country. To attract such investment, the government is offering tax incentives, which generate a significant price reduction for these devices in Brazil. This reduction is already in place for tablets and is expected to be implemented in the first half of 2012 for smartphones. Among manufacturers that are benefiting from the opportunities to manufacture and produce in Brazil, we find Apple, which will start manufacturing its iPhone in Brazil in 2012, and RIM, which already manufactures many of its phones in the country in order to avoid import taxes and consequently lower the cost and price of its devices in the country. Government incentives for the mobile segment don’t stop with smartphone and tablet manufacturing incentives. The government is also moving quickly with a 4G spectrum auction. It is working on a tight schedule and pushing operators to have all 10 cities that will host the FIFA World Cup in 2014 covered with LTE by at least one year before the event. For that to take place, the licenses that were thought to be auctioned in 2011 will definitely be auctioned no later than early 2012, and many of the current field tests will become actual operations. In order to further spur broadband penetration and meet its national plan’s goals, the government is giving tax incentives for operators that offer 1MB broadband connections for under R$30 (roughly $17), including mobile operators. Such incentive is providing an opportunity for many operators to address new markets and to contribute to the inclusion of many in the digital world of possibilities. In the pay-TV market, the government also acted fast to spur service penetration. As discussed above, and after a few years prohibiting incumbents from providing IPTV in their designated areas, this decision was overturned after the regulator said that pay-TV providers didn’t need the market protection any longer. In 2011, Anatel changed its regulation to allow fixed operators to offer IPTV on their own fixed networks, which is expected not only to benefit pay-TV services but most importantly to promote FTTx investments and services, since fiber technology is often required to deliver high-end pay-TV services through IP.

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 8

Market detail

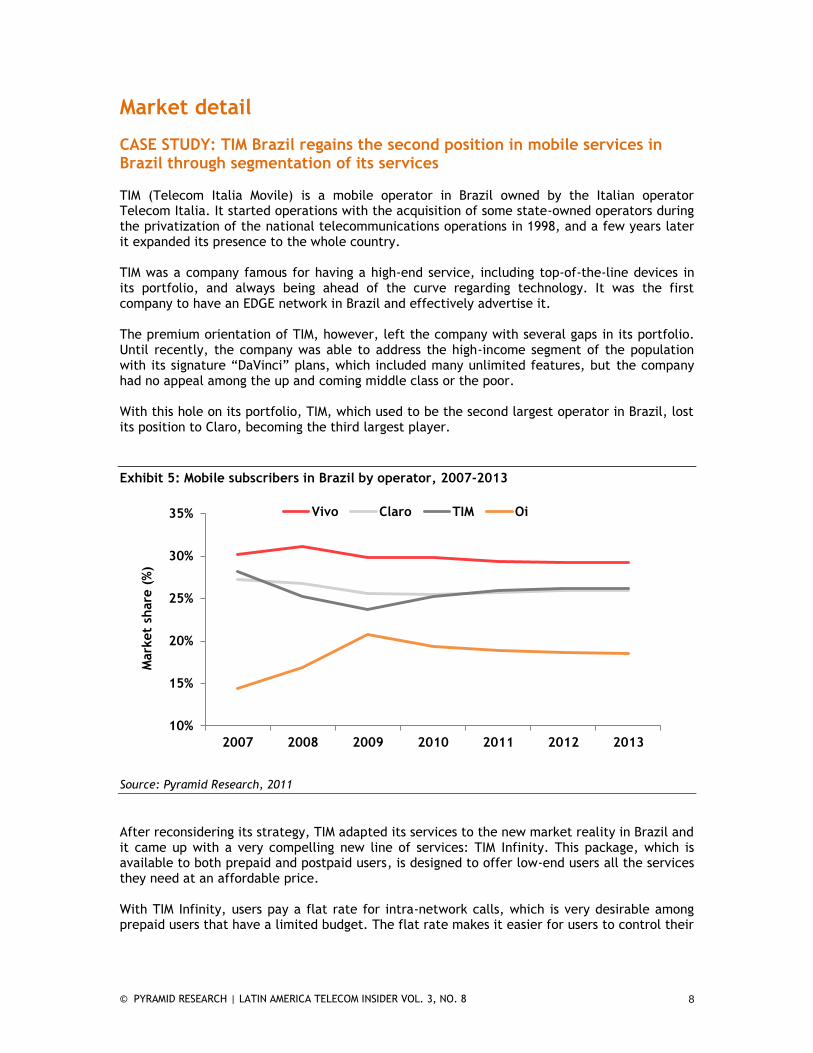

CASE STUDY: TIM Brazil regains the second position in mobile services in Brazil through segmentation of its services TIM (Telecom Italia Movile) is a mobile operator in Brazil owned by the Italian operator Telecom Italia. It started operations with the acquisition of some state-owned operators during the privatization of the national telecommunications operations in 1998, and a few years later it expanded its presence to the whole country. TIM was a company famous for having a high-end service, including top-of-the-line devices in its portfolio, and always being ahead of the curve regarding technology. It was the first company to have an EDGE network in Brazil and effectively advertise it. The premium orientation of TIM, however, left the company with several gaps in its portfolio. Until recently, the company was able to address the high-income segment of the population with its signature “DaVinci” plans, which included many unlimited features, but the company had no appeal among the up and coming middle class or the poor. With this hole on its portfolio, TIM, which used to be the second largest operator in Brazil, lost its position to Claro, becoming the third largest player.

Exhibit 5: Mobile subscribers in Brazil by operator, 2007-2013

Source: Pyramid Research, 2011

After reconsidering its strategy, TIM adapted its services to the new market reality in Brazil and it came up with a very compelling new line of services: TIM Infinity. This package, which is available to both prepaid and postpaid users, is designed to offer low-end users all the services they need at an affordable price. With TIM Infinity, users pay a flat rate for intra-network calls, which is very desirable among prepaid users that have a limited budget. The flat rate makes it easier for users to control their

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011 2012 2013

Mark

et

share

(%

)

Vivo Claro TIM Oi

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 9

balances while also giving them the confidence to make more calls since they know how much they’re spending. Another great benefit of the Infinity plan is the Web and SMS feature. For prepaid users, unlimited SMS and browsing can be used every day for a flat daily fee of R$0.50 ($0.27) for each service. Users only pay this fee on days when they use the service, which again gives them the confidence to use it without fear of surprises on their statements.

Exhibit 6: TIM Infinity plan advertisement

Source: TIM

To address the high-income segment, TIM also designed new services. Besides the unlimited plans, TIM created offers that make it easier for the average users to buy data packages based on the actual device they are going to use. On this plan, Internet prices vary from R$80 ($42) for unlimited mobile broadband for laptop use to R$30 ($16) for smartphone use. The difference in price refers to the speed of each service and the maximum download limit before this speed is reduced.

Exhibit 7: TIM Liberty plan advertisement

Source: TIM

By adding these plans to its portfolio and adapting to the new reality in Brazil, and focusing also on value-added services such as data, TIM was able to regain the runner-up position, and it is expected to remain there for years to come. It did decrease its overall ARPU, but after a bad

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 10

2010, TIM’s revenues should grow 20.5% in 2011, when the total mobile market is expected to grow 12.5%.

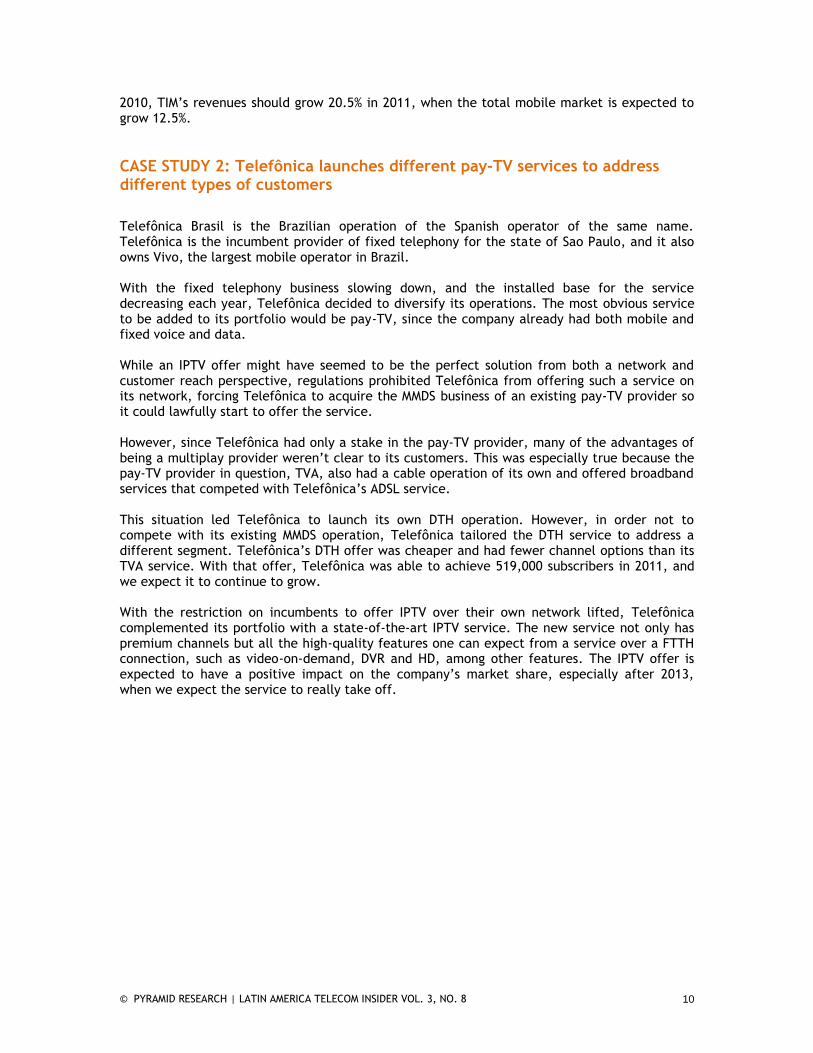

CASE STUDY 2: Telefônica launches different pay-TV services to address different types of customers

Telefônica Brasil is the Brazilian operation of the Spanish operator of the same name. Telefônica is the incumbent provider of fixed telephony for the state of Sao Paulo, and it also owns Vivo, the largest mobile operator in Brazil. With the fixed telephony business slowing down, and the installed base for the service decreasing each year, Telefônica decided to diversify its operations. The most obvious service to be added to its portfolio would be pay-TV, since the company already had both mobile and fixed voice and data. While an IPTV offer might have seemed to be the perfect solution from both a network and customer reach perspective, regulations prohibited Telefônica from offering such a service on its network, forcing Telefônica to acquire the MMDS business of an existing pay-TV provider so it could lawfully start to offer the service. However, since Telefônica had only a stake in the pay-TV provider, many of the advantages of being a multiplay provider weren’t clear to its customers. This was especially true because the pay-TV provider in question, TVA, also had a cable operation of its own and offered broadband services that competed with Telefônica’s ADSL service. This situation led Telefônica to launch its own DTH operation. However, in order not to compete with its existing MMDS operation, Telefônica tailored the DTH service to address a different segment. Telefônica’s DTH offer was cheaper and had fewer channel options than its TVA service. With that offer, Telefônica was able to achieve 519,000 subscribers in 2011, and we expect it to continue to grow. With the restriction on incumbents to offer IPTV over their own network lifted, Telefônica complemented its portfolio with a state-of-the-art IPTV service. The new service not only has premium channels but all the high-quality features one can expect from a service over a FTTH connection, such as video-on-demand, DVR and HD, among other features. The IPTV offer is expected to have a positive impact on the company’s market share, especially after 2013, when we expect the service to really take off.

© PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8 11

Exhibit 8: Telefônica’s pay-TV subscriptions and penetration in Brazil, 2010-2016

Source: Pyramid Research, 2011

By segmenting its market and offering different services to customers from different socioeconomic backgrounds, Telefônica has been able to attract an estimated 721,000 users by the end of 2011. By 2016, the company is expected to reach 1.94m pay-TV subscribers.

0%

2%

4%

6%

8%

10%

0

0.5

1

1.5

2

2.5

2010 2011 2012 2013 2014 2015 2016

Mark

et sh

are

Mobile s

ubsc

ripti

on (

m)

Telefonica pay-TV subscribers Market share

Author: Vinicius Caetano, Senior Analyst ([email protected]) Editor: Matt Donnelly, Managing Editor ([email protected]) Support: www.pyramidresearch.com/insiders.htm ([email protected]) © PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8

12

Key findings

The reality of Brazil has changed, and operators need to segment their strategies and adapt to the new characteristics of the demand. With increasing user sophistication, there is no more room for one-size-fits-all strategies.

The growing middle class and low-income segments are demanding more services. They

are willing to spend money for value-added services, as long as they are priced and positioned correctly to address their needs.

On the other end of the curve, there is a rich strata savvy about state-of-the-art new

technologies and better and faster services. Operators need to understand how to balance their portfolios in order to address this segment, as well.

Recommendations

Operators ― Fixed operators should segment their offers. They can secure their most relevant markets through value-added services such as high-speed Internet and pay-TV, as well as by offering mid-range services to attract new clients. Revenue will soon become a much more important metric than ARPU. It is important to manage the profitability of each service; however, the fear of a lower ARPU shouldn’t scare operators away from offering low- to middle-end services.

Regulators ― Continue promoting competition (as with network unbundling, for example) and acting swiftly to allow operators to address the needs of this fast-paced market.

Equipment vendors ― With the increasing amount of mobile Internet coverage, mobile equipment vendors must work closely with mobile operators and be prepared to act fast, since time to market is important for a successful mobile strategy. On the fixed side, vendors can also expect increased demand for high-speed Internet, including FTTH, and for pay-TV lines of business.

Author: Vinicius Caetano, Senior Analyst ([email protected]) Editor: Matt Donnelly, Managing Editor ([email protected]) Support: www.pyramidresearch.com/insiders.htm ([email protected]) © PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8

13

Related resources Why Cloud Computing Services Are Good for Operators and SMEs in Latin America Telecom Insider published July 2011 Cloud computing can help operators in Latin America reduce their internal costs and develop competencies that can help them sell these same services to small and midsize clients needing to become leaner and more agile in a global marketplace. And since cloud computing rides on top of the broadband networks being built out by operators today, it provides another important way for operators to achieve a greater return on their investment. This report examines what cloud computing is, the framework behind this model and identifies the main drivers behind its adoption in Latin America. Three case studies look at fixed operators in Mexico that offer cloud services with an eye to what they understand to be cloud computing, the main reasons they adopted cloud computing, and the different services they offer.

Latin America Fixed Communications Forecasts Forecasts published quarterly Our Fixed Communications Forecast products provide a complete picture of wireline voice and data communications in each of 19 Latin American markets. The Excel output includes five years of historical data and five years of market projections for metrics such as demographics and economic trends, penetration of broadband and narrowband lines, Internet users, business users, voice telephony lines, VoIP, PCs, IPTV and revenue. We believe our Fixed Communications Forecasts are superior because they capture granular data gathered through extensive field research and use a thorough methodology consistently applied to all markets. Data from these Forecasts is available online for subscribers to our DataTracker service.

Mobile Social Networks Set to Experience Rapid Growth as Mobile Penetration Rates Rise Telecom Insider published October 2011 Pyramid Research believes mobile devices will become the platform of choice for accessing social networking sites in LA. To catch up with the developed world, where mobile social networking is increasing business opportunities, there are some changes that Latin American operators and device manufacturer need to make. This report discusses those changes and how much progress LA operators have made thus far.

Brazil: Mobile Data and Prepaid Mobile Drive Unprecedented Telecom Revenue Growth by 2015 Country Intelligence Report published March 2011 Pyramid Research estimates that total telecom revenue in Brazil reached $67.4bn by year-end 2010, up $13.4bn from 2009, and will total $88.7bn in 2015, with a CAGR of 5.6%, fueled by expansion in mobile data services and broadband Internet access.

For more information or to purchase, contact Pyramid Research at:

+1.617.871.1900 or [email protected] or www.pyramidresearch.com

Author: Vinicius Caetano, Senior Analyst ([email protected]) Editor: Matt Donnelly, Managing Editor ([email protected]) Support: www.pyramidresearch.com/insiders.htm ([email protected]) © PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8

14

SUBSCRIBER LICENSE AGREEMENT Any Pyramid Research Insider report ("Report") and the information therein are the property of or licensed to Pyramid Research and permission to use the same is granted to annual or single-report subscribers ("Subscribers") under the terms of this Subscriber License Agreement ("Agreement") which may be amended from time to time without notice. When requesting a Report, Subscriber acknowledges that it is bound by the terms and conditions of this Agreement and any amendments thereto. Pyramid Research therefore recommends that you review this page for amendments to this Agreement prior to requesting any additional Reports. OWNERSHIP RIGHTS All Reports are owned by Pyramid Research and protected by United States Copyright and international copyright/intellectual property laws under applicable treaties and/or conventions. Subscriber agrees not to export any Report into a country that does not have copyright/intellectual property laws that will protect Pyramid Research’s rights therein. GRANT OF LICENSE RIGHTS Pyramid Research hereby grants Subscriber a personal, non-exclusive, non-refundable, non-transferable license to use the Report for research purposes only pursuant to the terms and conditions of this Agreement. Pyramid Research retains exclusive and sole ownership of each Report disseminated under this Agreement. Subscriber agrees not to permit any unauthorized use, reproduction, distribution, publication or electronic transmission of any Report or the information/forecasts therein without the express written permission of Pyramid Research. Subscribers purchasing site licenses may make a Report available to other persons from their organization at the specific physical site covered by the agreement, but are prohibited from distributing the report to people outside the organization, or to other sites within the organization. Enterprise-level Subscribers, however, may make a Report available for access on intranets or closed computer systems for internal use under their service agreements with Pyramid Research. DISCLAIMER OF WARRANTY AND LIABILITY Pyramid Research has used its best efforts in collecting and preparing each Report. Pyramid Research, its employees, affiliates, agents and licensors do not warrant the accuracy, completeness, currentness, noninfringement, merchantability or fitness for a particular purpose of any reports covered by this agreement. Pyramid Research, its employees, affiliates, agents or licensors shall not be liable to subscriber or any third party for losses or injury caused in whole or part by our negligence or contingencies beyond Pyramid Research’s control in compiling, preparing or disseminating any report or for any decision made or action taken by subscriber or any third party in reliance on such information or for any consequential, special, indirect or similar damages, even if Pyramid Research was advised of the possibility of the same. Subscriber agrees that the liability of Pyramid Research, its employees, affiliates, agents and licensors, if any, arising out of any kind of legal claim (whether in contract, tort or otherwise) in connection with its goods/services under this agreement shall not exceed the amount paid to Pyramid Research for use of the report in question. About Pyramid Research Pyramid Research (http://www.pyr.com) offers practical solutions to the complex demands our clients face in the global telecommunications, media and technology industries. Our analysis is uniquely positioned at the intersection of emerging markets, emerging technologies and emerging business models, powered by the bottom-up methodology of our market forecasts for more than 100 countries–a distinction that has remained unmatched for nearly 25 years. As the telecom research arm of the Light Reading Communications Network, Pyramid Research works

Author: Vinicius Caetano, Senior Analyst ([email protected]) Editor: Matt Donnelly, Managing Editor ([email protected]) Support: www.pyramidresearch.com/insiders.htm ([email protected]) © PYRAMID RESEARCH | LATIN AMERICA TELECOM INSIDER VOL. 3, NO. 8

15

with Heavy Reading, providing the communications industry’s most comprehensive market data, trusted research and insightful technology analysis.