Embed Size (px)

Citation preview

3

proceedings

As a result of 40 years of little investment, Brazil still lags its Bric counterparts Russia, India and China in the quality

and scale of its infrastructure, which in turn has restricted growth. However, Brazil is now undergoing the greatest

building programme in the history of Latin America, with government investment in infrastructure targeting urban

development and housing, roads and railways, ports and airports, and energy. The programme and the country

itself offer attractive opportunities to civil engineers – and the nature of many of the projects calls for innovative

engineering solutions. However, doing business in Brazil is not straightforward and interested parties must be

prepared for differences in culture and ways of working. This paper identifies the key developments under way in

major infrastructure areas. It then offers a pragmatic perspective on what engineers need to take into account to

pursue the opportunities that the massive construction programme has to offer.

Len Pannett MBA, CEng, MIEE Freelance operational strategy consultant, Wallingford, UK

Proceedings of the Institution of Civil Engineers Civil Engineering Special Issue 166 November 2013 Issue CE6 Pages 3–12 http://dx.doi.org/10.1680/cien.13.00026 Paper 1300026

Received 09/04/2013 Accepted 09/07/2013

Keywords: developing countries/infrastructure planning

ICE Publishing: All rights reserved

Brazil – building the country of tomorrow

Civil Engineering Special Issue Volume 166 Issue CE6

Brazil – building the country of tomorrow Pannett

1. Introduction

The past 10 years have seen Brazil transform from being ‘the country of tomorrow that always will be’ (as it has often been described), to one of the top six economies in the world. Over the past three decades, the country has emerged from military dictatorship to become the third biggest democracy, from dark days of hyperinflation to being so economically and politically sound that it has been one of the darlings of investors over the past few years.

It has moved itself to become a significant player on the world stage, such as leading the United Nations (UN) mission in Haiti and seeking admittance to the UN permanent security council, making oil and gas finds off the coast that are propelling it to the top of the list of oil-producing nations, and hosting the most significant future sports events on the planet, namely the 2014 FIFA World Cup Brazil and the Rio 2016 Olympic and Paralympic Games.

In growing, Brazil has continued to advance in those areas where it was already the leader, such as in the sugar-cane-based production of ethanol, agriculture and commodities, and it has also been seeking to remedy the major sectors that have held it back in the past, particularly wealth distribution and education. It is now turning its attention to the third big area for improvement for growth: infrastructure. This latter sector in particular presents some of the world’s most significant opportunities and challenges for investors, suppliers and operators, particularly in the areas of civil engineering.

This paper describes what is happening in the country in terms of the major infrastructure areas for growth and development that have been mapped already, and what particular nuances need to be taken into consideration by organisations which wish to pursue them. Much of the data presented to quantify the forthcoming projects comes from the Brazilian government, and it has been presented variously at

several conferences and forums over the past 12 months, particularly at a series of investment forums which took place in March 2013 in London and New York.

2. Brazil: a changing nation

Brazil is a country of continental proportions: a population of over 190 million people live across its 8·5 million km2, making it the fifth largest by landmass and population. It has 7500 km of coastline, 3·3 million km2 of Amazon rainforest and the biggest river system in the world, providing the biggest national volume of fresh water.

Historically, Brazil was the first major exporter of gold, diamonds and other precious stones, as well as coffee and rubber. It is a leading exporter of iron ore and other metals, metallurgical products, chemicals, soybeans, sugar and sugar-based ethanol, and other foodstuffs such as beef and oranges (The Economist, 2007). It now has a thriving industry, which includes the world’s second biggest mining conglomerate, the third biggest aircraft manufacturer, the tenth largest oil and gas company, and a technology base that designs hardware, creates software and puts satellites into orbit.

Its electorate of 100 million voters is the democratic basis for a US$2·5 trillion economy (2011 figures), which has achieved annual growth rates of up to 7·5% over the past 10 years. It emerged from the economic crisis of 2008 relatively well, although indications are that the growth rate will slow to a more modest 2–3% in 2013 (Goodman, 2013). The country has moved further into the forefront of the global stage, most noticeably when it overtook the UK in terms of gross domestic product (GDP) in late 2012, a position which, although lost earlier this year, it will no doubt return to and better in the coming years. ‘Brazil has always been big; perhaps, though, it hasn’t been as visible as it is today’, Roberto Jaguaribe, Brazilian ambassador to

4

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

the UK, told the audience of the Brazilian Infrastructure Forum in London in March 2013.

The country’s economic success has been achieved, largely, by the global commodities boom of 2002–2010, which saw China transform itself through an intensive building and industrial expansion programme, with Brazil as its leading supplier of materials for that transformation, particularly iron ore, oil and other commodities. In parallel with this increase in exports, Brazil enjoys political stability and a drive to lower national interest rates, stabilise the exchange rate and control inflation, all within defined, narrow bands – something altogether more remarkable given the multi-party coalition that now forms the Brazilian government.

The recent uncertainty and upheaval in the traditionally more economically stable regions of Europe and the USA have presented Brazil with an opportunity to improve its internal situation, from redistributing wealth and raising living standards of the poorest parts of society to long-overdue investment in its infrastructure, urban and rural. This improvement has been catalysed by the country’s hosting of a series of world-scale events, from the 2007 Pan-American Games in Rio de Janeiro, the CISM Military World Games in Rio in 2011 and the 2012 UN-sponsored Rio+20 sustainable development conference to the coming 2014 FIFA World Cup Brazil and Rio 2016 Olympic and Paralympic Games. Indeed, the business cases for the latter two were predicated on legacy improvements to transport infrastructure as well as the building of sporting venues, assurances that have so far been very slow to materialise.

To lead and administer the required infrastructure investment, the government has recently created public companies such as the national-level planning and logistics company Empresa de Planejamento e Logística (EPL) and the state-level Olympic municipal company Empresa Olímpica Municipal (EOM). These vehicles will work with both public and private bodies to drive and implement infrastructure strategy at federal, state and municipal levels.

The renewed investment has arisen from the increased demand of an increasingly wealthy and vocal population, a larger and more active industry, and the recognition that the lack of investment over the past 40 years has for too long held the country’s growth rates back. ‘Brazilian growth will be led by infrastructure investments’, the head of the Brazilian National Development Bank, Luciano

Coutinho, told audiences in New York and London earlier this year. There is, however, a long way to go: according to the World

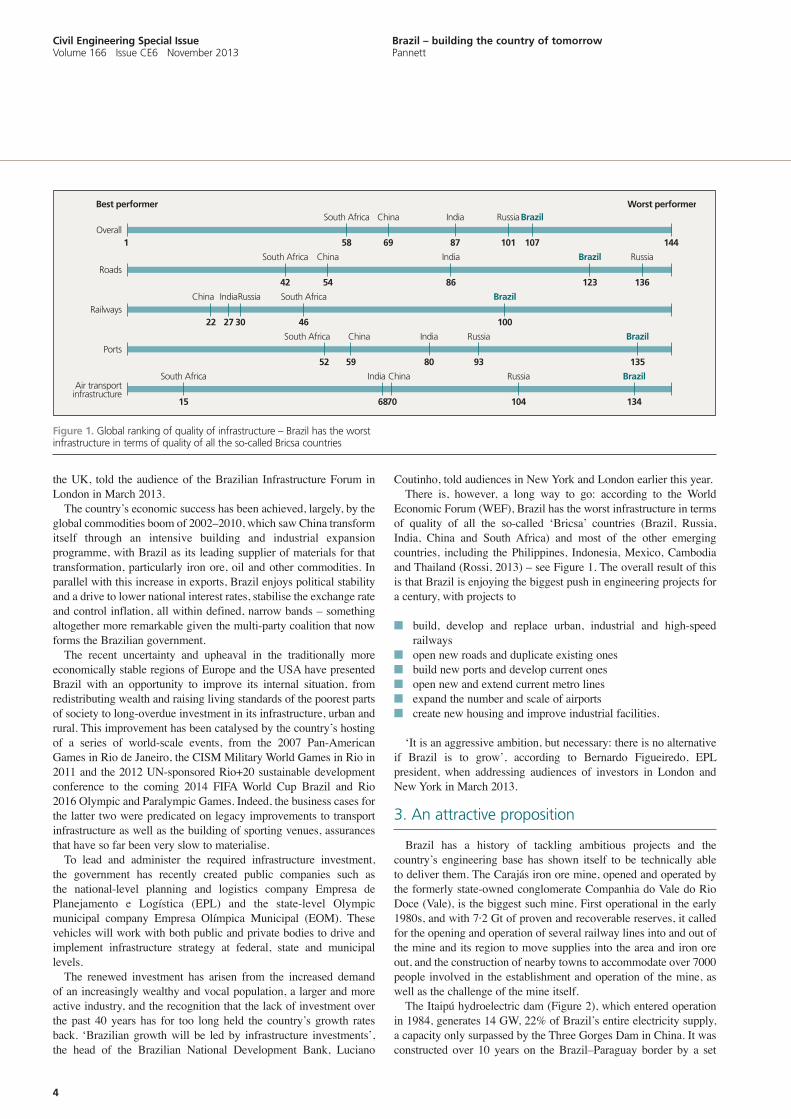

Economic Forum (WEF), Brazil has the worst infrastructure in terms of quality of all the so-called ‘Bricsa’ countries (Brazil, Russia, India, China and South Africa) and most of the other emerging countries, including the Philippines, Indonesia, Mexico, Cambodia and Thailand (Rossi, 2013) – see Figure 1. The overall result of this is that Brazil is enjoying the biggest push in engineering projects for a century, with projects to

n build, develop and replace urban, industrial and high-speed railways

n open new roads and duplicate existing onesn build new ports and develop current onesn open new and extend current metro linesn expand the number and scale of airports n create new housing and improve industrial facilities.

‘It is an aggressive ambition, but necessary: there is no alternative if Brazil is to grow’, according to Bernardo Figueiredo, EPL president, when addressing audiences of investors in London and New York in March 2013.

3. An attractive proposition

Brazil has a history of tackling ambitious projects and the country’s engineering base has shown itself to be technically able to deliver them. The Carajás iron ore mine, opened and operated by the formerly state-owned conglomerate Companhia do Vale do Rio Doce (Vale), is the biggest such mine. First operational in the early 1980s, and with 7·2 Gt of proven and recoverable reserves, it called for the opening and operation of several railway lines into and out of the mine and its region to move supplies into the area and iron ore out, and the construction of nearby towns to accommodate over 7000 people involved in the establishment and operation of the mine, as well as the challenge of the mine itself.

The Itaipú hydroelectric dam (Figure 2), which entered operation in 1984, generates 14 GW, 22% of Brazil’s entire electricity supply, a capacity only surpassed by the Three Gorges Dam in China. It was constructed over 10 years on the Brazil–Paraguay border by a set

South AfricaOverall

581 14469 87 101 107

China India RussiaBrazil

South AfricaRoads

42 54 86 136123

China India RussiaBrazil

South AfricaRailways

4622 27 30 100

China IndiaRussia Brazil

South AfricaPorts

52 59 80 93 135

China India Russia Brazil

South AfricaAir transport

infrastructure15

Best performer Worst performer

7068 104 134

ChinaIndia Russia Brazil

Figure 1. Global ranking of quality of infrastructure – Brazil has the worst infrastructure in terms of quality of all the so-called Bricsa countries

5

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

of largely Brazilian consortia, employing 40 000 people, and using sufficient concrete to build 210 Maracanã stadia, enough iron and steel for 380 Eiffel Towers, and the excavation of earth and rock with a volume equivalent to 8·5 times that of the Channel Tunnel.

However, following those two megaprojects in the early 1980s, there was little investment in infrastructure in the country until 2007, a fact that held back the country during the turbulent economic times of the 1990s. That was to begin to change in 2007 with the establishment of the federal government’s programme for accelerated growth, Plano de Aceleração de Crescimento (PAC), a R$503 billion (£157 billion) programme of economic policies and investment projects to transform infrastructure, covering ports, roads, airports, sanitation, energy, waterways, railways and metros, as well as other sectors, with investment during the period 2007–2010 coming from federal, state and private bodies (Figure 3).

The funds were expanded by a further R$142 billion (£44 billion) in 2009, and followed by a successor PAC2, which for the period 2010–2014 is directing a further R$1·59 trillion (£497 billion) at urban redevelopment, the provision of basic services to local communities, provision of housing, clean water and electricity for all, improving the logistics network (rail, road and riverine) across the country, and ensuring security of energy generation using clean and renewable sources, as well as developing the recently discovered ‘pre-salt’ offshore oil fields to increase national oil and gas production.

25

20

15

10

5

0PAC

inve

stm

ent

dis

bu

rsem

ents

: £ b

illio

n

2007

2.4

2008 2009 2010 2011 2012 2013*

* Projections

2014*

3.7

6.07.3

9.3

13.1

17.9

22.7

Figure 3. Growth of financing from the Brazilian government through the PAC growth acceleration plans – the majority is being spent on infrastructure

Figure 2. The 1984 Itaipú hydroelectric dam generates 14 GW, 22% of Brazil’s entire electricity supply, a capacity only surpassed by the Three Gorges dam in China (courtesy Gilmar Antonio Piolla, Acervo Itaipu Binacional)

6

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

Recent non-conventional oil and gas finds, including shale, have also been considered for investment in this package. Following the widespread unrest earlier in 2013, president Dilma Rouseff also announced a further R$50 billion (£15 billion) destined to urban transport, although there has been no further declaration of the source of this funding nor details of what it will be spent on.

As well as government-funded programmes, the country is embarking on a course of seeking private companies to develop, build and operate much of its infrastructure, such as airports, ports, roads and railways. For example, in 2012, the president announced a R$133 billion (£42 billion) programme to transform the country’s largely decrepit highway and railway system. Through this scheme, businesses will be responsible for much of the building and amelioration of some 7500 km of roads and over 10 000 km of railways.

The mechanisms will largely be a variety of private–public partnerships (PPPs), using lessons learnt from other countries’ experiences in this area as well as past attempts at leveraging PPPs in Brazil itself. Part of the motivation for this is the perception that the private sector is more effective at completing these types of project on time and within budget. Richard Dubois, infrastructure partner at PwC in São Paulo, observed that, ‘Private companies usually build construction projects in Brazil in half the time and at 60% of the cost of the public sector’ (Winter and Goy, 2012).

The PPPs will finance concessions for construction and operation of the infrastructure, with durations of 25 and 35 years, depending on their nature and sector. However, the commitment to PPPs may be eroding, as evidenced by the changes to the financing of the high-speed train between Rio and São Paulo. Politically, it is easy to see the attraction of this investment. ‘Brazil is a big country and, being big, our problems also are’, Gleisi Hoffmann, the president’s chief of staff, told an audience of investors earlier this year, continuing, ‘Our solution is investment, investment, investment.’

Figures from the Brazilian economic and social development bank, Banco Nacional de Desenvolvimento Econômico e Social (BNDES), indicate that every increase of 1% in the supply of infrastructure can equate to a rise of 0·5% in GDP. Overall, these investment packages will see government-backed investment in infrastructure rise from 1·62% in 2006 (Brazilian Planning Ministry, 2010) to a forecasted 4·5% of GDP in 2013 (Veja, 2012), with a view to reaching 5% of GDP over the coming 4 years. This compares to the UK’s figures of 2·6% of GDP in 2006 (HM Treasury, 2011) rising to 2·9% in 2008.

4. Urban and housing redevelopment

The growth of urban centres in Brazil over the past 40 years has left most with a straining infrastructure, overburdened transport systems and the ills that come from a lack of urban planning. For example, some parts of Diadema, a poorer area of the capital city São Paulo, saw growth with an average rate of 16% per year between 1950 and 1980. São Paulo itself has nearly doubled in size from 1970, from a population of 5·9 million to over 11·3 million today.

Spurred by a combination of hosting world events and the receipt of revenues from the commodities boom, many cities are now transforming themselves. For example, the former capital city of Rio de Janeiro is presently redeveloping its port area, much as has been carried out in London, San Francisco, Barcelona and Buenos Aires. The aim is to provide a mix of residential and commercial space, threaded with efficient and open transport links to the rest of the city,

while opening up many of the older, heritage buildings, including former royal palaces and portside warehouses. This development is driven by the need to support the expanding oil and gas industry, whose resources struggle to find accommodation in the full city and its clogged transport arteries.

The Porto Maravilha development (Figure 4) includes the removal of one of the main road traffic viaducts in Rio and re-routing it into two subterranean, coastal tunnels, with a combined extension of 3·5 km. Planned to be operational by the start of the Rio 2016 games, and at depths of up to 38 m, part of the tunnel system will comprise twin galleries, each containing three lanes, forming an underground dual carriageway. A further three tunnels are being bored in the area to improve the circulation of traffic and a new light bus rapid transit system, with the adaptation and inclusion of 200-year-old, slave-built stretches that had previously been sealed. This £2·5 billion programme will result in over 5 million m2 of usable real estate for commercial, residential, cultural, tourist and educational purposes.

More widely, the PAC is funding the construction of over 2 million new houses in a project termed ‘minha casa, minha vida’ (‘my home, my life’), aimed at providing social housing for low-income families. This £24 billion project has seen further subsidies from local governments to accelerate construction and remove local housing bottlenecks, and many of the new houses will accommodate families who will be moved as part of the preparations for the forthcoming sports events.

5. Rail and metro

The transportation of goods across the country has been a major issue for Brazilian industry since its earliest days. The arrival of the UK as a major trading partner in the nineteenth century brought with it the newly developed railway, and British engineers and companies were instrumental in opening up the country, laying new lines and designing and building rail stations across the land. For example Rio’s two main termini, Central do Brasil and Estação Leopoldina, were designed by Scottish architect Robert Prentice and some of the first lines, such as the 1867 project linking the port of Santos to São Paulo, were built by British firms.

However, during the 1930s and 1940s and under pressure from the growing automotive industry, the government sought to move transportation away from rail onto roads and investment in the rail network largely stagnated. From then on much of the investment in overland rail has come from mining companies seeking to move their ores to coastal and riverine ports. Vale, for example, now owns and operates over 10 000 km of railways across the country. This situation has resulted in a divided network, often with separate lines (and thus separate operators) for passenger and cargo, between and within cities. Of the current 29 000 km only 4% is electrified, with consequences on the cost of running the network as well as on carbon dioxide emissions.

During the 1970s many of the larger cities, particularly São Paulo and Rio de Janeiro, began to invest in metro-based solutions to questions of mass transit. In the former, the scale of the conurbation meant that the network grew rapidly and today it comprises nine lines. In Rio restrictions due to the geography of the city have kept the network to a more conservative two subterranean lines with a total of 36 stations. Other cities have small but similar networks.

The lack of scale of rail operations, both over- and underground, has now been recognised internally. The Brazilian government

7

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

at federal, state and city levels is aiming to improve integration, to expand existing lines and to open new ones. By 2020 the EPL is aiming to oversee the construction of over 10 000 km of new railways, resulting in an overland network of over 40 000 km (which compares to China’s 90 000 km today). ‘We are virtually building the country’s entire network’ says Bernardo Figueiredo. To achieve that, over R$91 billion (£28 billion) has been earmarked to be spent over the coming 5 years.

Key projects include construction of the country’s first high-speed line, a 511 km link between the cities of Campinas, São Paulo and Rio. This has an expected initial demand of 7·1 million passengers in the first year of operation, rising to 11·3 million over 10 years and to 27·8 million over 30 years (Halcrow-Sinergia Consortium, 2009), although those figures are based on a highly optimistic start of operations in 2014. The aim of this line is to transfer passenger traffic from the Rio–São Paulo ‘air bridge’ and provide a more competitive but time-neutral solution for travel between the cities.

The project is not without technical challenges as its route will take it through mountainous and highly urbanised terrains, with some 40% of the route consisting of tunnels, viaducts and bridges. Financing of the project was to be through a series of PPPs but this has now been changed to being a public project to be tendered as a set of ten parts. The total investment for the project, including construction and resolution of land issues, is estimated at over R$35 billion (£11 billion). It should be pointed out that issues of demand forecast, planning permission and land management are yet to be resolved.

Other projects include more than 12 city-to-city lines, which will not only open up rail as a realistic option for intercity passenger travel

Figure 4. Museum of Tomorrow at the £2·5 billion Porto Maravilha development in Rio de Janeiro which is due for completion in 2016. The project includes removal of a major urban road viaduct and re-routing it into 3·5 km of coastal tunnels (courtesy Prefeitura do Rio de Janeiro)

As well as government-funded programmes, the country is embarking on a course of seeking private companies to develop, build and operate much of its infrastructure, such as airports, ports, roads and railways

8

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

but also open up the country for internal and international movement of cargo, such as the 4200 km North–South line (Figure 5) linking Belém in the north to Porto Murtinho in the south.

Expansion of the metro networks is also planned in 24 towns, including an investment of R$7·7 billion (£2·4 billion) in São Paulo alone to double the annual number of passengers, modernise the stock and upgrade the signalling system. A high-capacity urban monorail line in São Paulo will be built, rivalling Tokyo’s 300 000 annual passengers line.

6. Roads

As with rail, the road network in Brazil has suffered considerably through lack of a joined-up, strategic vision for its development, as well as low levels of investment. While some major projects have been attempted in the past, such as the ill-fated Trans-Amazon Highway in the 1980s, it is only in the past few years that investment has been earmarked for the construction and operation of new highways.

As part of the PAC2 tranche of funding, R$42 billion (£13 billion) will be spent on increasing the highways network by over 7500 km. Of those, nine major projects, mostly across the central belt of the country, will be contracted over 2013/2014, using PPP-like funding as with other areas.

Improvement, maintenance and operation of many of the existing routes will be passed to the private sector, and both new and existing operators will be encouraged to use road tolls to finance their ongoing costs.

7. Ports

Given Brazil’s nearly 7500 km of coast and its historical position as a major exporting nation, it is surprising that the scale and quality of its port infrastructure is far below that which would be expected. As well as being managed locally and publically, with little national-level planning, the number and scale of ports in the major trade points along the coast, as well as their internal sophistication, are logistics bottlenecks. For example, most of the ports lack efficient container management on the dockside, leading to extremely long lead times for their clearance coming into and exiting the country.

Over the past 15 years, many large-scale planning permissions have been granted to new extraction and processing plants in mining and agriculture when the bidder has agreed to construct new terminals and facilities. For example, the giant food commodities firm, Cargill, built a new terminal in Santarém, on the Amazon River. Other firms have taken a more strategic view, such as the EBX Group, which is building the so-called Super Port of Açu. Porto Central, in the state of Espírito Santo, is currently developing a 6800 ha deep-water facility that is intended to rival Rotterdam in scale and volume of handled cargo.

Initially part of the earmarked PAC funding, Brazil is also planning to transform the management and development of port facilities. The state of Rio alone will gain four new ports with an investment of R$9 billion (£3 billion). With the first to be opened by 2016, these ports will support the exploration operations, and eventual production, in the pre-salt offshore oil and gas fields. They will comprise a mix of onshore and offshore facilities, enabling unloading of oil and gas, as well as refuelling of tenders and carriers (Batista, 2013). This trend is expected to continue, with the federal government changing legislation to encourage the opening up of the construction and operation of port terminals by private entities, and the implementation of a ‘port lease’ approach.

8. Airports

In December 2012, the Brazilian government announced an ambitious target: to build 800 private and public, regional and local airports across the country over the coming years (Franco, 2012), with the aim of connecting medium and larger towns to the air network. Although not disclosing what level of investment is expected to fund this vast expansion, the president said, ‘We want cities of up to 100 000 inhabitants to have airports within 60 km: we intend to have a very strong regional air programme’ (Franco, 2012).

With a country of continental dimensions, air travel is a necessity for many, and improvements to the main air hubs, such as São Paulo, Brasília, Belo Horizonte and Rio, as well as additional, regional airports are often cited by travellers as a top requirement for meeting the growing demand. For instance, in March 2013, Rio’s state government announced an ambitious aim of increasing passenger capacity at the city’s main airport from its current level of 15 million

Figure 5. The 4200 km North–South railway line provides a vital cargo route between Belém in the north and Porto Murtinho in the south – over 12 other city-to-city lines are planned (courtesy Edsom Leite)

Porto Central, in the state of Espírito Santo, is currently developing a 6800 ha deep-water facility that is intended to rival Rotterdam in scale and volume of handled cargo

9

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

to 70 million per annum by 2042, a target which will require it to become the first three-runway airport in the country. Investment in this expansion is expected to assign R$11·8 billion (£3·7 billion) for São Paulo and Rio alone, and there has been a significant interest from several consortia worldwide for the concessions in Rio and Belo Horizonte alone (Valor, 2013).

9. Energy

Of all the infrastructure sectors, oil and gas has been the most transformative in Brazil over the past 25 years. The recent ultra-deep-water finds in the so-called pre-salt basin off the coast of Rio and Santos have propelled the country from being a net importer of oil to being an exporter, eligible for membership of the Organisation of Petroleum Exporting Countries.

Present estimates of the area’s reserves alone would more than double the country’s reserves, with up to 35 billion barrels of oil equivalent found in the past 10 years (Gaier and Bonato, 2013). These finds have spurred the sector (Figure 6), not just the upstream producers but also the downstream, an area where Brazil has traditionally fallen behind. This has had a consequential impact on the associated supply chain, from marine construction of rigs and tenders, to shore-side pipelines, storage and refinery facilities.

Natural gas is also beginning to emerge as a major power source

in the country, driven by conventional, on- and off-shore finds as well as early prospects for non-conventional sources. The challenges of extracting both oil and gas from these deep-water and non-conventional sources will require innovative approaches, both in the design and the construction of facilities.

Headlined by the mega-project at Itaipú, Brazil has a long history of using hydroelectric power to feed its energy consumption. Indeed, today Brazil can be said to have the most sustainable energy generation, with some 68% of its power generated by that means (ANEEL, 2013). Despite environmental and land use concerns, this trend is continuing and presently there are 23 projects to be auctioned by 2017, with a combined generation capacity of 21·4 GW and a budget of US$40 billion (£27 billion).

In addition, two ongoing projects are noteworthy because of their scale. Belo Monte, although long-awaiting final planning permission, will channel the waters of the Xingu River to generate up to 11·2 GW of power, making it the third largest such facility in the world, at an estimated cost of US$16 billion (£10·7 billion). The Jirau dam will have a span of 8 km over the Madeira River in the state of Rondônia and feature fifty 75 MW turbines, more than any other dam in the world, resulting in an installed capacity of 3·7 GW. Presently this project is estimated to cost US$15·6 billion (£10·4 billion).

This desire for sustainable generation is also reflected in other areas. Wind power is set for a fast expansion, and by 2017 it is

Figure 6. The first combined oil and gas production platform entirely constructed in Brazil started operation in the pre-salt offshore fields in 2009 (courtesy Agência Petrobras)

10

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

estimated that 8·5 GW will be generated from offshore and onshore wind farms. As with other infrastructure projects, this will be achieved through a series of PPP-like structures, with 5·7 GW being auctioned by 2017, with a value of US$11·9 billion (£7·9 billion). The set of licence auctions in late December 2012 saw a high number of bids, indicating that there is a real appetite for these types of project in the country.

Several projects are also under way to transform the electricity distribution network. Spurred by several large-scale blackouts over the past decade, this network has been identified as being unreliable and prone to failure. With World Bank and other international bodies joining the private and public organisations to invest in this transformation, it is as urgent to improve the supply to customers as connection of many of the new-generation projects to the grid.

Brazil has also long had a global lead on alternative fuels, particularly sugar-cane-derived ethanol. Propelled by a government-subsidised programme in the 1970s to move away from petroleum-based fuels, ethanol is now a major constituent of the road fuel market, with 87% of vehicles sold in 2012 (ANFAVEA, 2013) being ‘flex fuel’, able of coping with all levels of ethanol–petroleum mixes. This demand has had to endure a maturing supply, with the ethanol industry only recently emerging from an agricultural-based model to an industrial one. Central to this transformation is the need for improved distribution and storage, as well as production facilities that can operate with greater efficiency.

With a sector-wide acceleration in production capacity over the past 10 years, Brazilian mills already achieve production volumes higher than anywhere else and this is being expanded through the use of sugar bagasse (the fibrous remains of crushed sugar cane). However, with bigger harvests, themselves motivated by higher demands for ethanol, the frequently antiquated production plants are running out of capacity. Further investment levels will be tied to commodity prices for sugar and ethanol, and these have suffered in the past few years.

10. Working in Brazil

With so many opportunities across the infrastructure spectrum, Brazil naturally is an attractive proposition for firms involved in the design, construction and servicing industries, as well as those involved in the supply chain of those sectors. But to make use of such opportunities firms must be cognisant of what working in Brazil entails.

Working in a new country always brings with it the need to understand and adapt to the particular nuances of the country’s culture and situation, and Brazil is no exception (Figure 7). If foreign organisations are going to pursue the many opportunities that the boom in infrastructure investment presents, they must first have an appreciation for the culture and ways of working. This section will detail some of the more subtle aspects other than the purely fiscal and legal differences.

10.1 CultureAn often-commented aspect of Brazilian culture is that, because

of its historical roots, it has a more European feel than American. Business is highly relationship based, with negotiations made face to face, and the increased use of technology such as Skype and web-based video is beginning to enhance that.

Notably a friendly culture, attempts at developing business remotely or only occasionally visiting the country tend to be

dismissed as coming from parties that are not truly interested. This means that if an organisation has ambitions to expand in the country, to bid and win tenders and be part of the growth of infrastructure there, it needs to be based in the country.

It can be achieved physically, such as opening an office in the country or acquiring a local firm, or by developing local representation through the establishment of local partnerships or joint ventures. There are financial benefits of this, as fiscal rules regarding the transfer of funds from Brazil are notoriously strict, costly and complicated.

Presence in the country also proves commitment as there is often a view that foreign firms and workers, especially from the USA and Europe, will leave if and when economic conditions ‘at home’ improve.

10.2 LanguageAs a whole, engineering business is largely transacted in Portuguese,

especially at the middle management and factory-floor level and outside the major conurbations, although the senior management levels will usually have a level of competency in English.

According to the British Council, only 5% of Brazilians speak English, and only 36% of those who claim to have fluency actually do (Amorim, 2012a). Therefore, employing Portuguese-speaking resources will become a higher priority as foreign companies become more deeply involved in a project, especially if these are to be realised in rural and remote areas.

10.3 ResourcesBrazil is presently enjoying historically low unemployment levels

of around 5·8% (IBGE, 2013), especially when compared to the USA and European countries. However, the biggest challenge facing organisations is the availability of suitable resources: according to the Brazilian Institute of Engineers, there is a national shortage of some 800 000 suitably qualified and experienced engineers in the country (Nogueira, 2013). Another survey of 721 engineering firms by the Brazilian Economic Institute identified the shortage of qualified personnel as presenting serious difficulties to over 41% of them (Amorim, 2012b). They identified the very high level of competition in the sector and a consequential rise in the cost of labour as being symptomatic of this situation. However, the shortage is slowly ameliorating.

For example, the rail sector was estimated to employ some 16 600 in 1997, rising to 44 000 at the end of 2012, with a parallel increase in the number of places at universities and technical colleges to qualify new rail-related engineers and technicians. In some cases, this has meant the restarting of courses that had previously been withdrawn nationally. In the oil sector, concession agreements for the development of the pre-salt basin call for 1% of revenues to be directed to research and development, particularly through sponsorships, grants and scholarships at universities (ANP, 2005), and 75% of royalties from the oil finds will be destined to education.

Even with the various initiatives, there will be significant, short-term shortfall in trained, experienced and qualified staff, including engineering, technical and managerial sectors, which will impact the pace at which many projects can progress. Many companies, such as Vale and Supervia, have accelerated in-house training courses to help plug the gap. Seeing this gap as an opportunity, many Brazilian expats have returned to their home country, driven by the comparatively favourable economic and work conditions.

11

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

Firms trying to make up the difference by importing non-Brazilian, foreign-based resources have been faced with a lengthy bureaucracy and very highly priced work visas, with the result that many opt to invest more time, effort and money in other, more open and easier to enter countries. To help that situation, the Brazilian government has sought to ease the ‘red tape’ and cost of visas, and this approach is expected to gain momentum over the coming months.

10.4 The ‘Brazil cost’The World Bank’s 2012 annual global report Doing Business,

which evaluates the ease of starting a business, dealing with construction permits, registering property, and paying taxes, ranks Brazil at 130th out of 185 countries, below Vietnam, Paraguay and Argentina (World Bank, 2012).

Furthermore, the WEF ranks Brazil last out of 144 countries in terms of the burden of government regulation (WEF, 2013). This bureaucracy is exacerbated by an impenetrable, often changing, fiscal and regulatory environment at federal, state and city level. Often these tiers contradict each other, adding costs and delays to civil projects before, during and after construction. This is the ‘custo Brasil’, the Brazil cost: the increased operational costs of doing business in Brazil.

The cost includes high rates of taxation, both corporate and personal, a legal code which mixes twenty-first century technology, such as the use of web resources for submitting tax declarations, with nineteenth century practices, such as the need to register one’s signature with a notary’s office in order to sign documents.

For instance, on average, it takes 13 procedures and 119 days of work to start a business in Brazil, and construction permits demand an average 17 procedures and 469 days to get finally authorised (Gomes, 2012). Before signing engineering documents, including drawings, quality controls and engineering specifications, engineers must be registered with the state’s regional engineering and agronomic council (CREA), which requires the recognition of the individual’s academic and professional qualifications and experience.

Although there have been some political moves to reduce the Brazil cost, legislative changes have hindered such efforts. The past few years have seen a greater emphasis on the protection of the environment and national heritage, and this has been reflected in stricter laws in the area which require more permits from federal and state governments. Whereas in the past these areas were approached with an almost cavalier attitude, this can no longer be the case.

For example, Anglo American, the global mining company, has been hindered in the construction of its US$8·8 billion (£5·8 billion) Minas Rio iron ore project largely because of delays in obtaining environmental licences and archaeological approvals, many newly introduced and with changing criteria. This situation has been recognised and the EPL is positioning itself between the private sector, which will build and operate projects, and the government bodies and agencies that will issue licences. This, it is hoped, will facilitate and accelerate licensing issues.

If firms and individuals are to consider participating in projects in the country, this Brazil cost must be taken into account and prepared for, through the use of local agents, qualified accountants and recognised lawyers.

10.5 TimeAs with all countries, the nuances of Brazilian culture bring

challenges to those operating in the country. One aspect that is

readily noticeable is that time keeping is not as rigorously followed as in the USA and European countries. Meetings will start late and go over their allotted time; deadlines will be missed. Together with the need for relationships to be established before business is transacted, this requires those working in the country to have patience and perseverance, and to make allowances for such delays in plans and schedules.

Frequently lack of timeliness spills over into the management of projects, with many observers noting that projects tend to run behind schedule for much of their life, only to have an increase of resources (and therefore funding) in the latter stages to recover as far as possible. For example, in contrast to the London 2012 venues, most of which were completed long before the games were opened to allow for testing and proving, most of the venues for the 2014 FIFA World Cup, including the Maracanã Stadium itself, have been and will be completed only days before the first matches to be played in them are scheduled, such as this year’s Confederations Cup.

Already commentators have noted similar trends emerging for other large-scale projects and forthcoming events.

10.6 CorruptionWith a multi-party coalition-based government, a very uneven

income distribution and the lack of large-scale land reform, corruption has been an ever-present problem in Brazil. ‘Corruption appears much more staggering in Brazil than in other countries in Latin America and the rest of the world’, according to Michael Pedersen, head of the WEF Partnering Against Corruption Initiative (PACI) (Pedersen, 2010).

According to the WEF’s Executive Opinion Survey (WEF, 2013), the country ranks 65th out of 144 in terms of irregular payments and bribes, 121st in terms of public trust of politicians, 122nd on the business costs of crime and violence, 84th on ethical behaviour of firms and 71st on judicial independence. This image has been exacerbated by recent high-profile cases at the highest levels of federal and state government, such as the so-called Mensalão case, which found senior members of the ruling Workers Party and its government allies guilty of accepting bribes for votes. This is very much a recognised problem, and the issue is beginning to be tackled. For example, the president removed seven of her ministers from power in the first 2 years after taking office, although little has been

Figure 7. Carnival in Rio de Janeiro: organisations wishing to work in Brazil need to understand and appreciate its unique culture

12

Civil Engineering Special Issue Volume 166 Issue CE6 November 2013

Brazil – building the country of tomorrow Pannett

done to prosecute those individuals. Commercially, therefore, companies must put in place preventative

measures to counter corruption and to deal with instances where they may and do occur. Companies with anti-corruption programmes and ethical guidelines, such as those called for by UK anti-bribery legislation, report up to 50% fewer incidents of potential and actual corruption.

11. Conclusion – changing economics?

Roberto Jaguaribe told audiences in early 2013, ‘We are a rich country, but still a developing country with many, many problems.’ After the success of the past 10 years, those problems are now affecting the main economic statistics, and regaining the previous levels of growth requires a step-change transformation in the quality, availability and extent of infrastructure. Although this was broadly recognised by the Brazilian government, whose desire to transform

that infrastructure is supported with very ambitious funding and announcements of further future funding, it has been energised by the widespread popular demonstrations over June and July 2013.

As the country deals with the bottlenecks that are holding it back, it is clear that resolving them will require support and participation of individuals, organisations and companies, particularly in the engineering sectors where resources are scarce. While this undoubtedly creates significant opportunities, if those entities are to succeed then they must plan for the nuances and challenges of working in Brazil, as their resolution will require investment of time and money.

This paper opened with the statement that Brazil is often said to be ‘the country of tomorrow that always will be’. Provided all the pieces come together, if Brazil follows through with its promise of funding and gets the expertise and support it needs to realise its infrastructure ambitions, then, as Brazilian society changes for the better, ‘tomorrow’ can truly become ‘today’.

References

Amorim M (2012a) Brasileiros não sabem falar inglês: apenas 5% dominam o idioma. O Globo, 30 September, see http://oglobo.globo.com/emprego/brasileiros-nao-sabem-falar-ingles-apenas-5-dominam-idioma-6239142 (accessed 14/05/2013).

Amorim M (2012b) Ferrovias abrem 7 mil vagas até 2014 e ressuscitam graduação no setor. O Globo, 26 August, see http://oglobo.globo.com/emprego/ferrovias-abrem-7-mil-vagas-ate-2014-ressuscitam-graduacao-no-setor-5899705 (accessed 14/05/2013).

ANEEL (2013) Capacidade de Geração do Brasil, Brazilian Electricity Regulator Agency’s Real-time Generation Capacity Database. See http://www.aneel.gov.br/aplicacoes/capacidadebrasil/capacidadebrasil.cfm (accessed 14/05/2013).

ANFAVEA (2013) Carta da ANFAVEA, May 2013. See http://www.anfavea.com.br/cartas/Carta324.pdf (accessed 05/06/2013).

ANP (2005) ANP Rules Number 5/2005, Revision 01, 24 November 2005. See http://www.petrobras.com.br/minisite/comunidade_cienciatecnologia/portugues/docs/Regulamento.pdf (accessed 05/06/2013).

Batista HG (2013) Novos portos focados no pré-sal investirão R$9 bilhões no Rio. O Globo, 18 February, see http://extra.globo.com/noticias/economia/novos-portos-focados-no-pre-sal-investirao-9-bilhoes-no-rio-7596749.html (accessed 14/05/2013).

Brazilian Planning Ministry (2010) Balanço 4 Anos, 2007–2010. Brazilian Government, see http://www.planejamento.gov.br/secretarias/upload/Arquivos/noticias/pac/Pac_1_4.pdf (accessed 14/05/2013).

Franco BM (2012) Dilma quer ligar todas cidades médias ou grandes com aeroportos regionais. Folha de São Paulo, 13 December, see http://www1.folha.uol.com.br/mercado/1200053-dilma-quer-ligar-todas-cidades-medias-ou-grandes-com-aeroportos-regionais.shtml (accessed 14/05/2013).

Gaier RV and Bonato G (2013) Reservas do pré-sal podem chegar a 35 bi boe. Reuters Brasil, 12 March, see http://br.reuters.com/article/topNews/idBRSPE92B02P20130312 (accessed 14/05/2013).

Goodman J (2013) IMF cuts Brazil GDP forecast as supply constraints accumulate. Bloomberg Businessweek, 16 April, see http://www.businessweek.com/news/2013-04-16/imf-cuts-brazil-gdp-forecast-as-supply-constraints-accumulate.

Gomes L (2012) Brazil’s Business Labyrinth of Bureaucracy. BBC News website, 17 May, see http://www.bbc.co.uk/news/business-18020623 (accessed 14/05/2013).

Halcrow-Singeria Consortium (2009) Demand and Revenue Forecast. Brazil TAV Project Documentation, vol. 1, June 2009, see http://www.epl.gov.br/html/objects/_downloadblob.php?cod_blob=909 (accessed 14/05/2013).

HM Treasury (2011) National Infrastructure Plan 2011. HM Treasury, UK, see http://www.hm-treasury.gov.uk/national_infrastructure_plan2011.htm (accessed 14/05/2013).

IBGE (2013) Brazilian Geography and Statistics Institute Statistics. See http://www.ibge.gov.br/home/.

Nogueira LA (2013) Fábrica de engenheiros. Isto é Dinheiro, 1 March, see http://www.istoedinheiro.com.br/noticias/113520_FABRICA+DE+ENGENHEIROS (accessed 05/06/2013).

Pedersen M (2010) Kicking Corruption Out of Brazil – Good for Business. World Economic Forum, see http://www3.weforum.org/docs/WEF_PACI_KickingCorruptionBrazil_Article_2010.pdf (accessed 14/05/2013).

Rossi V (2013) Brazil bottlenecks. Financial Times, 1 April, see http://blogs.ft.com/beyond-brics/2013/04/01/chart-of-the-week-brazils-bottlenecks/#axzz2TBteRdsu (accessed 14/05/2013).

The Economist (2007) The economy of heat. The Economist 402 (8780).Valor (2013) Aeroportos em Leilão Atraem 20 Grupos. Valor, 16 May, see http://

www.valor.com.br/empresas/3126058/aeroportos-em-leilao-atraem-20-grupos (accessed 25/07/2013).

Veja (2012) Planejamento Prevê Crescimento de 4,5% do PIB em 2013. Veja, Economia, 30 August, see http://veja.abril.com.br/noticia/economia/planejamento-preve-pib-de-4-5-no-ano-que-vem (accessed 14/05/2013).

WEF (World Economic Forum) (2013) The Global Competitiveness Report 2012–13. WEF, Geneva, Switzerland, p. 117, see http://www3.weforum.org/docs/WEF_GlobalCompetitivenessReport_2012-13.pdf (accessed 05/06/2013).

Winter B and Goy L (2012), Analysis: Next hurdles for Brazil: sticky fingers, red tape. Reuters, 17 August, see http://www.reuters.com/article/2012/08/17/us-brazil-infrastructure-idUSBRE87G0KC20120817 (accessed 14/05/2013).

World Bank (2012) Doing Business. World Bank, Washington DC, USA, see http://data.worldbank.org/indicator/IC.BUS.EASE.XQ (accessed 14/05/2013).

What do you think?

If you would like to comment on this paper, please email up to 200 words to the editor at [email protected].

If you would like to write a paper of 2000 to 3500 words about your own experience in this or any related area of civil engineering, the editor will be happy to provide any help or advice you need.

![Brazil country analysis report [team 2]](https://img.dokumen.tips/doc/110x75/554c1de7b4c905ec518b5439/brazil-country-analysis-report-team-2.jpg)