Embed Size (px)

Citation preview

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford

accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code. You will have to write

down only the final verification code on the attestation form, which will be emailed to registered

attendees.

• To earn full credit, you must remain connected for the entire program.

Branch Profits Tax Rules: Calculating and Reporting

Dividend Equivalent Amounts and Identifying Exemptions

WEDNESDAY, MAY 10, 2017, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

May 10, 2017

Branch Profits Tax Rules

John D. Bates, Partner

BakerHostetler, Washington, D.C.

Robert J. Misey, Jr., Shareholder

Reinhart Boerner Van Deuren, Chicago & Milwaukee

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Presenting Attorney

Presented by

Robert Misey

LL.M., J.D., M.B.A., B.A.

Chair, International Department

Reinhart Boerner Van Deuren, s.c.

312-207-5456 or 414-298-8135

The Branch Profits Tax

I. Mechanics

Foreign Corporations

Not incorporated in one of the 50

states 1

2 Treaty Tie-Breakers

©2017 All Rights Reserved

Robert Misey 6

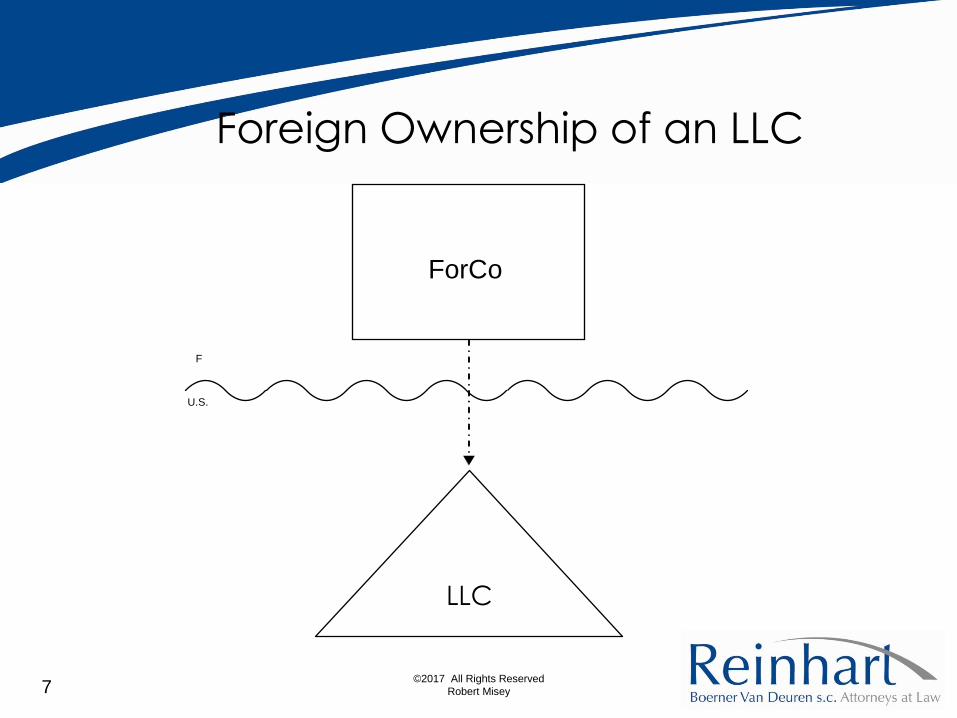

Foreign Ownership of an LLC

ForCo

U.S.

F

LLC

©2017 All Rights Reserved

Robert Misey 7

Taxation of

Foreign Corporations

Code: U.S. will tax a mere trade or

business of a foreign corporation.

The touchstone is considerable,

continuous, and regular.

1

2 Treaty: U.S. will only tax a

permanent establishment of a

foreign corporation

©2017 All Rights Reserved

Robert Misey 8

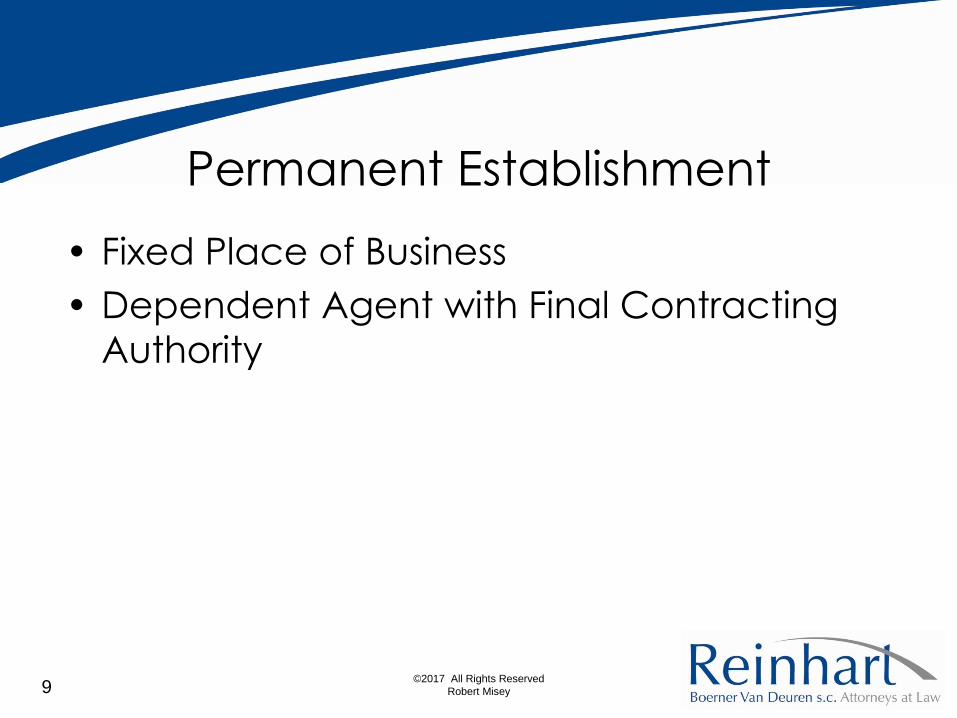

Permanent Establishment

• Fixed Place of Business

• Dependent Agent with Final Contracting

Authority

©2017 All Rights Reserved

Robert Misey 9

Fixed Place of

Business Standard • Plant

• Office

• Excludes preparatory and auxiliary functions

• Excludes projects of a particular length

©2017 All Rights Reserved

Robert Misey 10

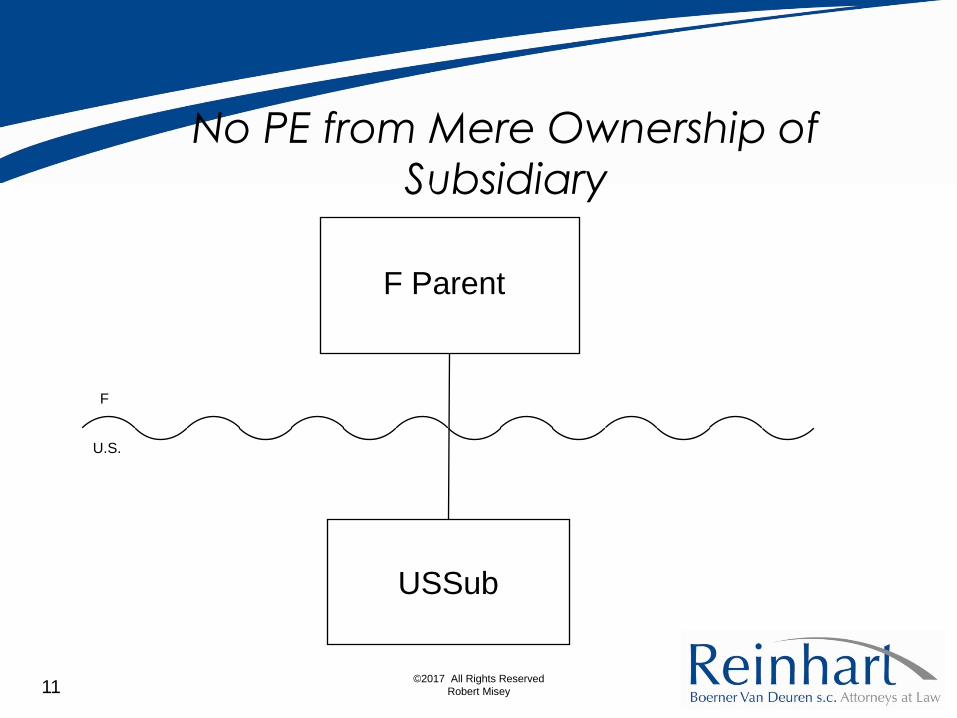

No PE from Mere Ownership of

Subsidiary

F Parent

U.S.

F

USSub

©2017 All Rights Reserved

Robert Misey 11

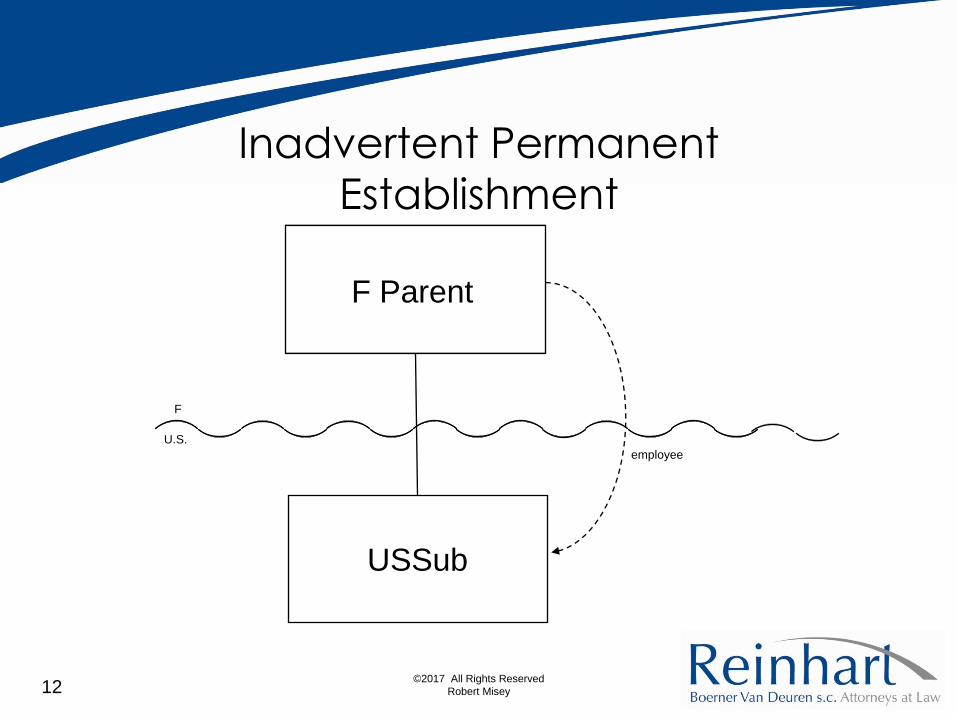

Inadvertent Permanent

Establishment

employee

F Parent

U.S.

F

USSub

©2017 All Rights Reserved

Robert Misey 12

Dependent Agent with Final

Contracting Authority Standard • Independent agents are not a permanent

establishment

– What is independence?

• Dependent agents with final contracting authority

are a permanent establishment

– What is final contracting authority?

©2017 All Rights Reserved

Robert Misey 13

Independent Salesperson?

ForCo

F

U.S.

candy

©2017 All Rights Reserved

Robert Misey 14

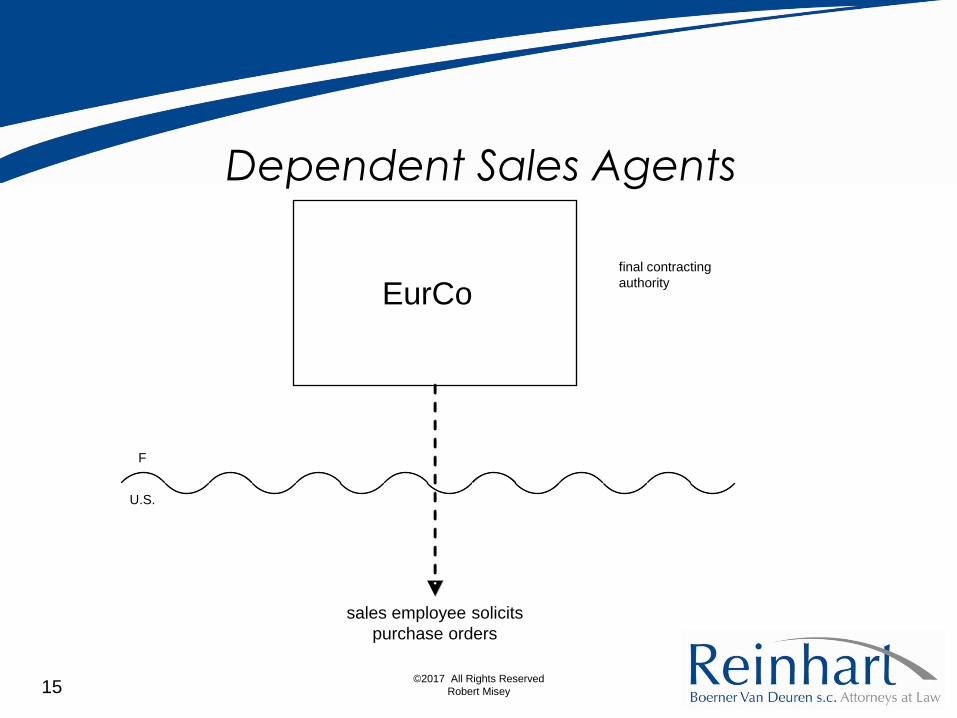

Dependent Sales Agents

EurCo

sales employee solicits

purchase orders

F

final contracting

authority

U.S.

©2017 All Rights Reserved

Robert Misey 15

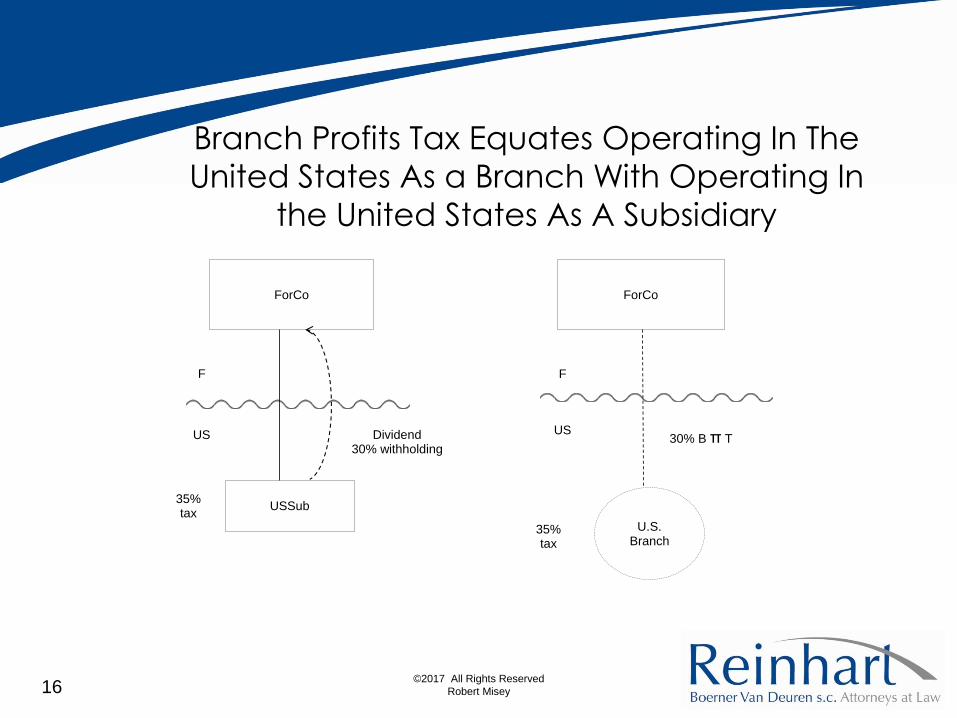

Branch Profits Tax Equates Operating In The

United States As a Branch With Operating In

the United States As A Subsidiary

ForCo ForCo

USSub

U.S. Branch

F

US

F

US

35% tax

35% tax

Dividend 30% withholding

30% B π T

©2017 All Rights Reserved

Robert Misey 16

Profits Attributable to a

Permanent Establishment

• Marginal tax rates

• U.S.—source Income

• Apportionable Expenses

• Transfer Pricing Principles

©2017 All Rights Reserved

Robert Misey 17

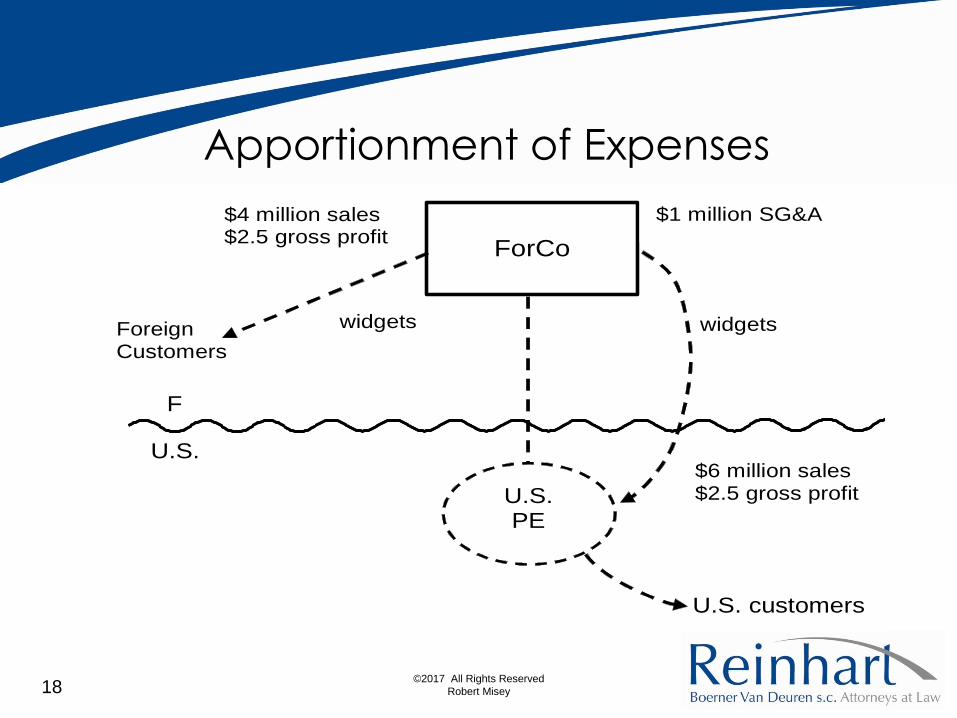

Apportionment of Expenses

ForCo

widgets

F

U.S.

U.S. customers

U.S. PE

$1 million SG&A $4 million sales $2.5 gross profit

$6 million sales $2.5 gross profit

widgets Foreign Customers

©2017 All Rights Reserved

Robert Misey 18

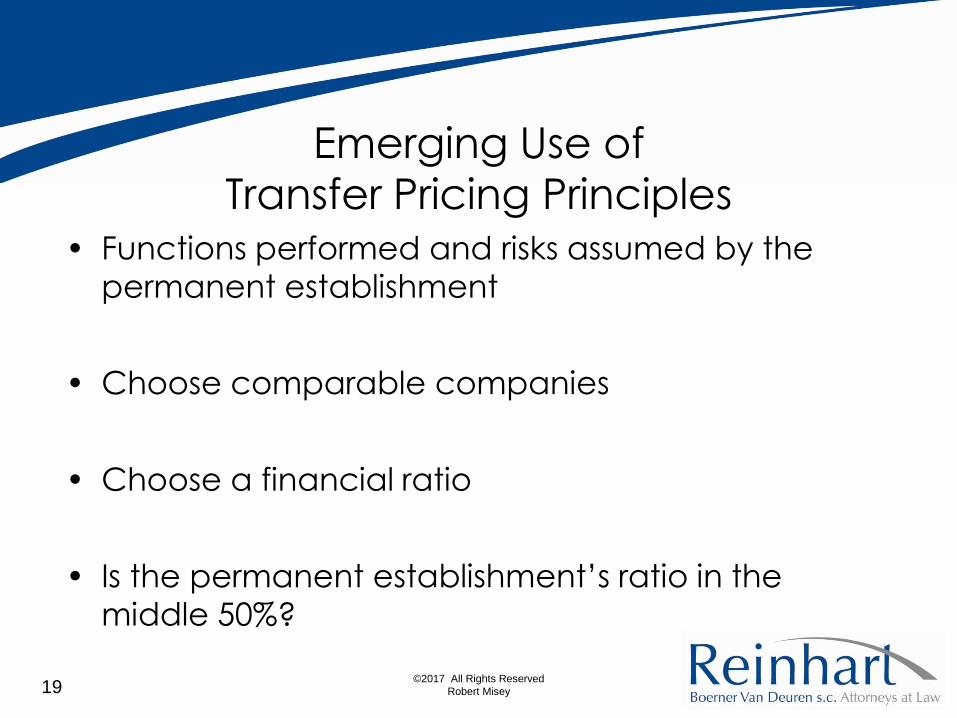

Emerging Use of

Transfer Pricing Principles • Functions performed and risks assumed by the

permanent establishment

• Choose comparable companies

• Choose a financial ratio

• Is the permanent establishment’s ratio in the

middle 50%?

©2017 All Rights Reserved

Robert Misey 19

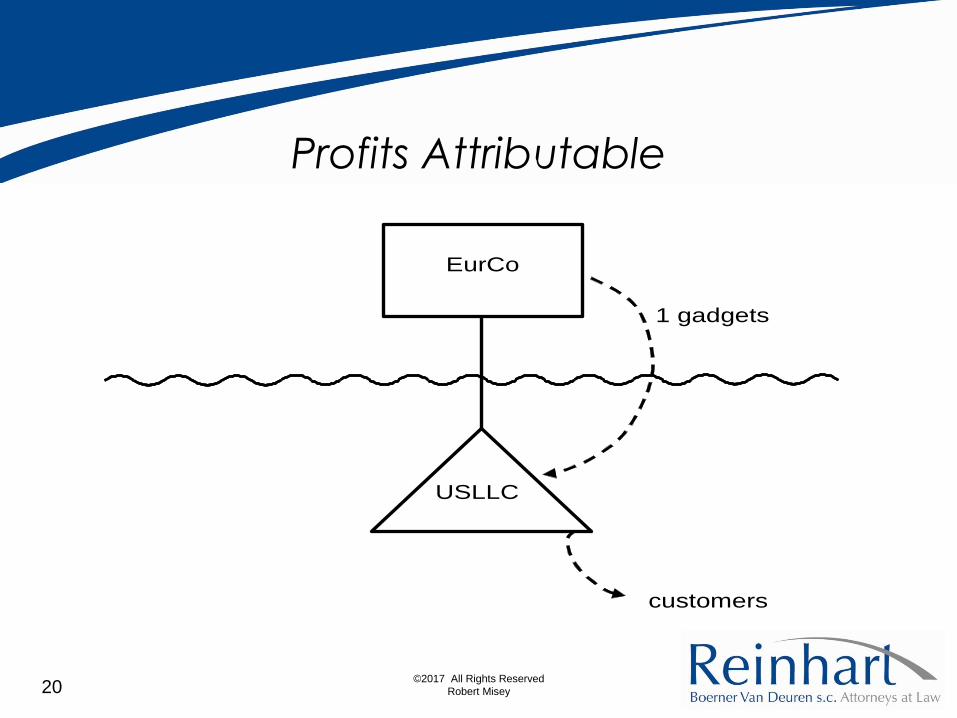

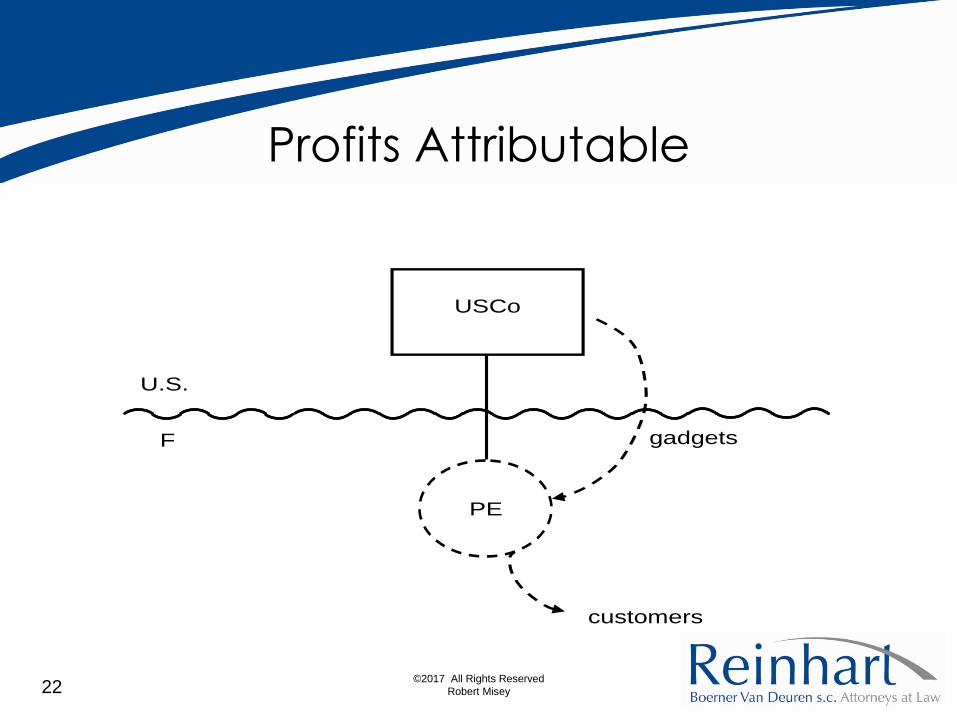

Profits Attributable

1 gadgets

EurCo

customers

USLLC

©2017 All Rights Reserved

Robert Misey 20

The Range

-0.5 8.5 5.5 2.5

©2017 All Rights Reserved

Robert Misey 21

Profits Attributable

gadgets

USCo

customers

U.S.

F

PE

©2017 All Rights Reserved

Robert Misey 22

Branch Profits Tax

• Equates operating in the U.S. via a

permanent establishment with operating in

the U.S. via a subsidiary

• Treaty rate is usually in the dividend article

©2017 All Rights Reserved

Robert Misey 23

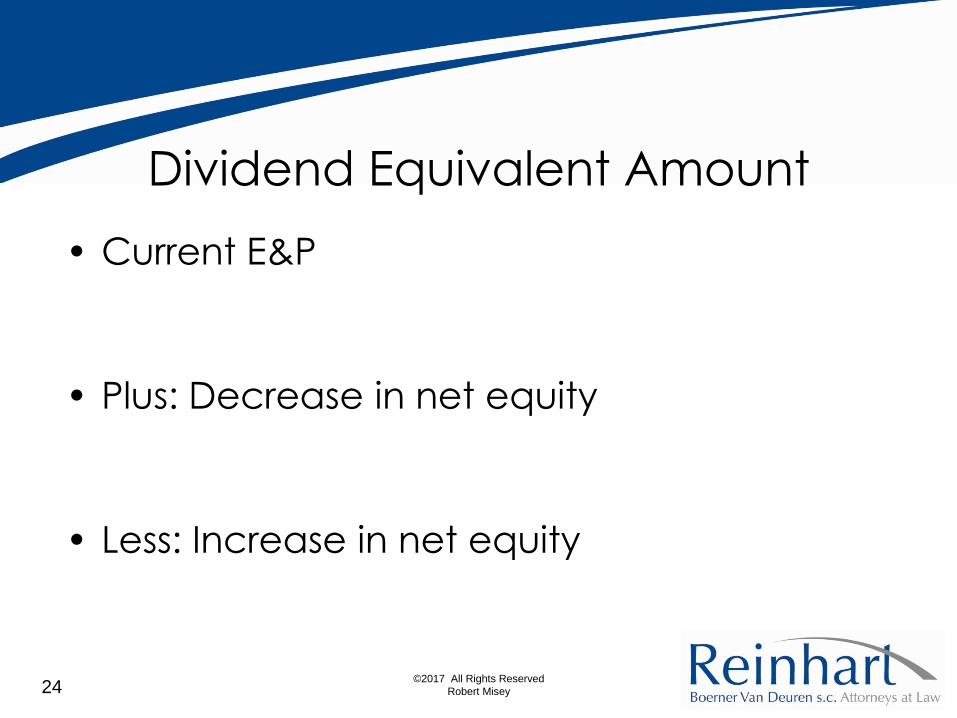

Dividend Equivalent Amount

• Current E&P

• Plus: Decrease in net equity

• Less: Increase in net equity

©2017 All Rights Reserved

Robert Misey 24

Current Earnings & Profits

Effectively Connected Income

Less

Corporate Income Taxes

©2017 All Rights Reserved

Robert Misey 25

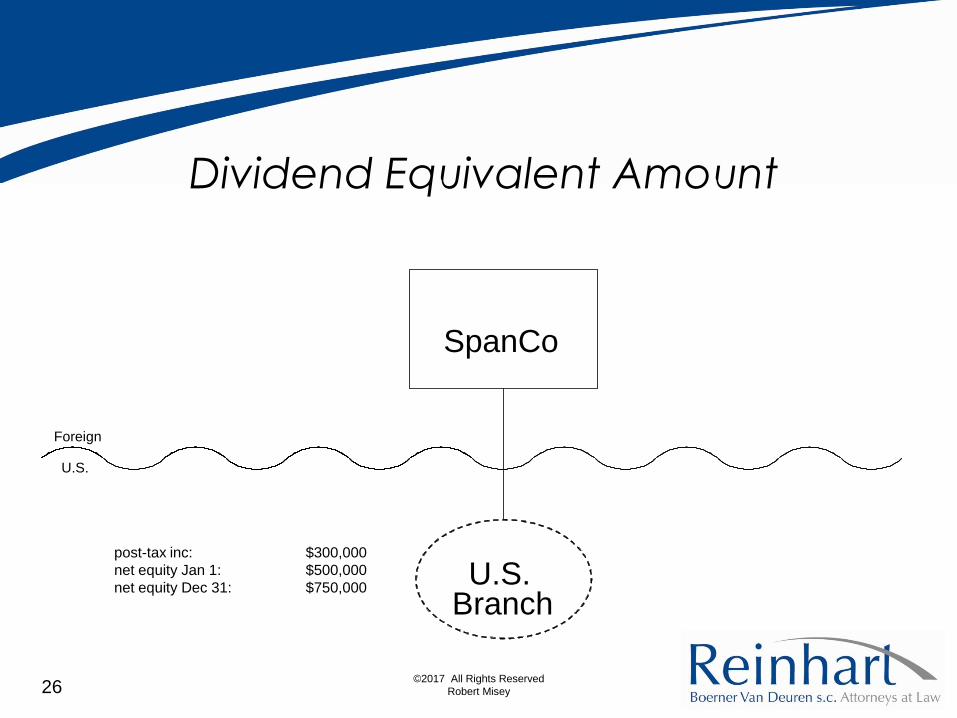

Dividend Equivalent Amount

U.S. Branch

SpanCo

U.S.

Foreign

post-tax inc: $300,000

net equity Jan 1: $500,000

net equity Dec 31: $750,000

©2017 All Rights Reserved

Robert Misey 26

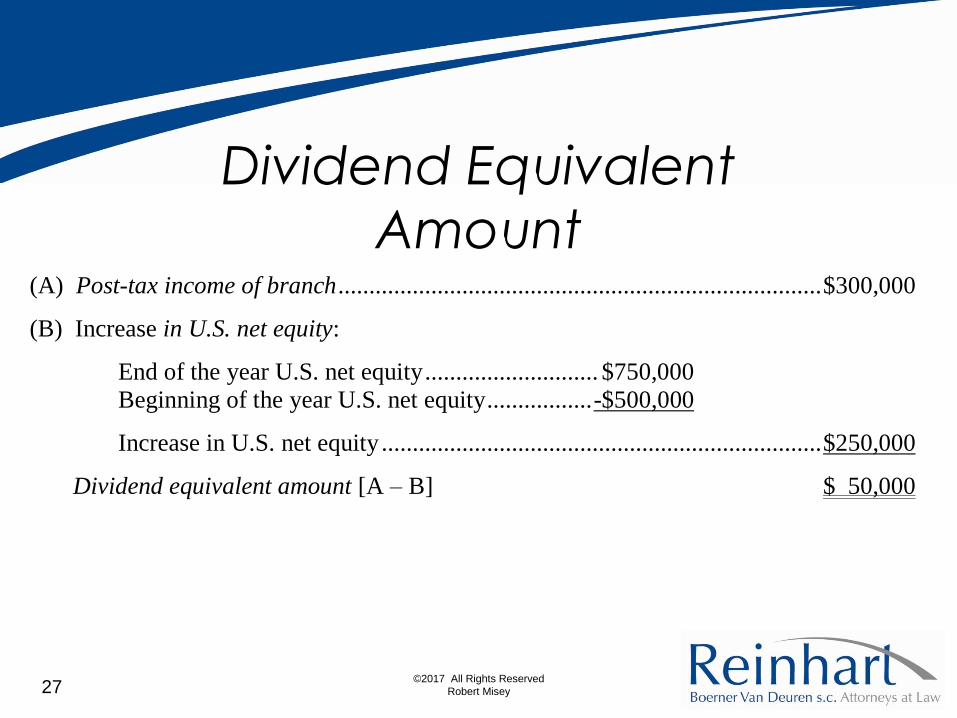

Dividend Equivalent

Amount (A) Post-tax income of branch .............................................................................. $300,000

(B) Increase in U.S. net equity:

End of the year U.S. net equity ............................ $750,000

Beginning of the year U.S. net equity ................. -$500,000

Increase in U.S. net equity ....................................................................... $250,000

Dividend equivalent amount [A – B] $ 50,000

©2017 All Rights Reserved

Robert Misey 27

Dividend Equivalent Amount

SpanCo

U.S.

Foreign

post-tax inc: $300,000

net equity Jan 1: $800,000

net equity Dec 31: $400,000

U.S. Branch

©2017 All Rights Reserved

Robert Misey 28

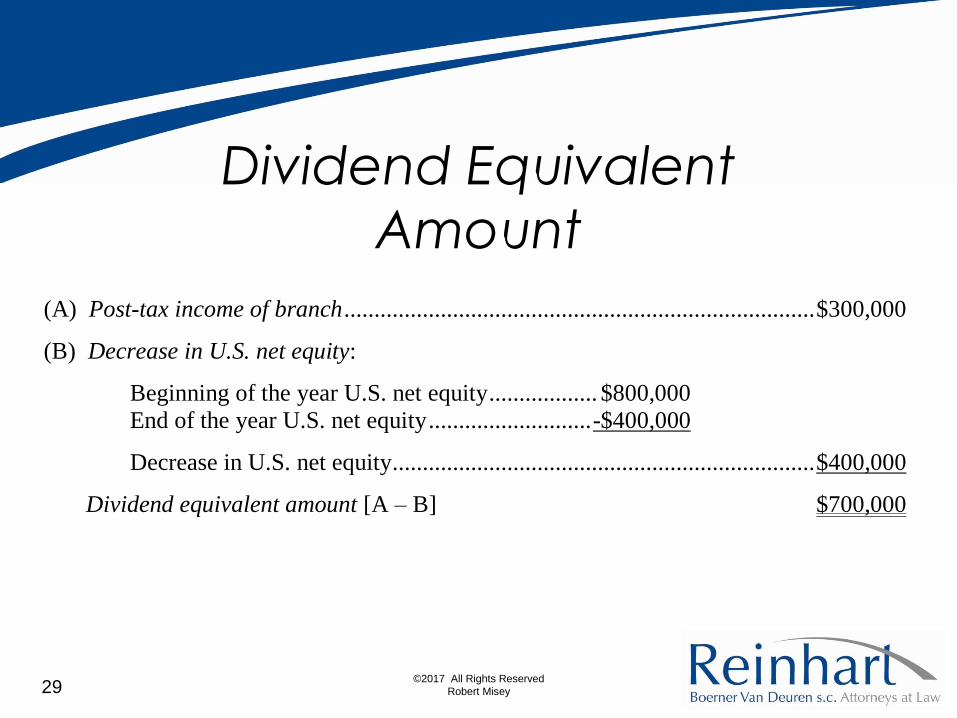

Dividend Equivalent

Amount

(A) Post-tax income of branch .............................................................................. $300,000

(B) Decrease in U.S. net equity:

Beginning of the year U.S. net equity .................. $800,000

End of the year U.S. net equity ........................... -$400,000

Decrease in U.S. net equity...................................................................... $400,000

Dividend equivalent amount [A – B] $700,000

©2017 All Rights Reserved

Robert Misey 29

Robert Misey ROBERT MISEY is Chair of the International Department of the

Midwestern based law firm of Reinhart Boerner Van Deuren s.c. .

Mr. Misey concentrates his practice in the areas of international

business and taxation. Mr. Misey's previous experience includes

nine years as an attorney for the IRS Chief Counsel (International)

in its Washington, D.C. and San Jose, California, offices. He

previously led the International Tax Services group for a region of a

Big Four accounting firm.

Mr. Misey is a frequent speaker and has published numerous

articles. He has authored the treatises U.S. Taxation of

International Transactions and Federal Taxation: Practice and

Procedure.

Mr. Misey received his M.B.A. and J.D. degrees from Vanderbilt

University and his LL.M. degree in Taxation from Georgetown

University. A member of the bar in California, Wisconsin and the

District of Columbia, he can be reached by phone at either

312-207-5456 or 414-298-8135 or by e-mail at

36147011

©2017 All Rights Reserved

Robert Misey 30

II.D – Branch Profits Tax

Exceptions

John D. Bates

Termination Exception

• Termination Exception

– Foreign corporation not subject to BPT in year in which it

terminates all of its US trade or business (Termination

Exception). §1.884-2T(a)(1). Non-previously taxed

accumulated ECEP is eliminated, preventing decrease in US

Net Equity from increasing DEA.

– Policy is that branch termination is analogous to liquidation of

wholly owned domestic subsidiary. Distribution in complete

liquidation by domestic subsidiary is not a dividend subject to

US tax and withholding to foreign shareholder.

– Termination Exception involves stringent substantive and

procedural requirements. Should not assume it necessarily will

be available.

– For application of Termination Exception in FIRPTA context

on disposition of US real property interest, see CCA

200504029.

33

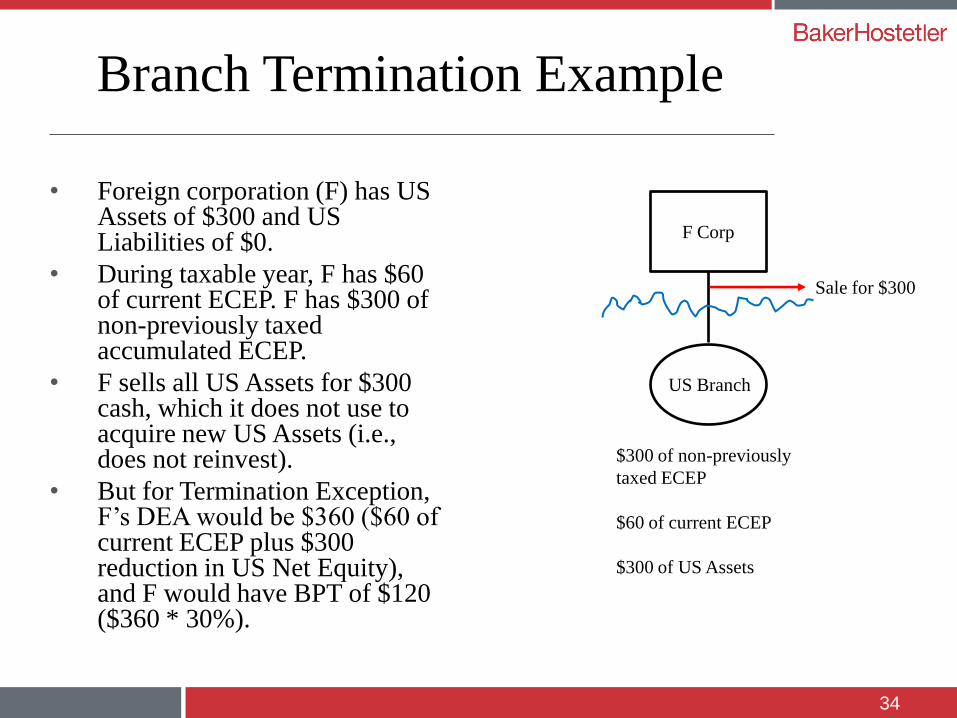

Branch Termination Example

• Foreign corporation (F) has US Assets of $300 and US Liabilities of $0.

• During taxable year, F has $60 of current ECEP. F has $300 of non-previously taxed accumulated ECEP.

• F sells all US Assets for $300 cash, which it does not use to acquire new US Assets (i.e., does not reinvest).

• But for Termination Exception, F’s DEA would be $360 ($60 of current ECEP plus $300 reduction in US Net Equity), and F would have BPT of $120 ($360 * 30%).

34

F Corp

US Branch

$300 of non-previously

taxed ECEP

$60 of current ECEP

$300 of US Assets

Sale for $300

Termination Exception Requirements

• Termination Exception applies only if: – At close of taxable year of termination (Termination Year), either (i) foreign

corporation has no US Assets or (ii) shareholders have adopted irrevocable resolution to completely liquidate foreign corporation and, at close of taxable year following Termination Year, all of foreign corporation’s US Assets are distributed, used to pay off liabilities, or cease to be US Assets. §1.884-2T(a)(2)(i)(A).

– For three taxable years following Termination Year, neither foreign corporation nor related corporation directly or indirectly uses US Assets of terminated US trade or business in another US trade or business (Three-Year Reinvestment Prohibition). §1.884-2T(a)(2)(i)(B).

– Foreign corporation has no ECI (other than certain ECI under §864(c)(6) or §864(c)(7)) during three taxable years following Termination Year. §1.884-2T(a)(2)(i)(C).

– Foreign corporation waives period of limitations for Termination Year. §1.884-2T(a)(2)(i)(D). Must file Form 8848 with tax return for Termination Year. §1.884-2(a)(2)(ii). Extends period of limitations to six taxable years following Termination Year.

• If any of requirements not satisfied, foreign corporation subject to BPT on DEA resulting from termination. §1.884-2T(a)(2)(i).

35

Three-Year Reinvestment Prohibition

• Three-Year Reinvestment Prohibition covers: – All money and property that were US Assets as of close of taxable year

before Termination Year. §1.884-2T(a)(2)(iii)(A).

– All money and property into which US Assets or ECEP are converted at any time during three-year prohibition period through sale, exchange, or other disposition. §1.884-2T(a)(2)(iii)(B).

– All money and property attributable to sale by shareholder of interest in foreign corporation (or successor) at any time after date which is 12 months before close of Termination Year. §1.884-2T(a)(2)(iii)(C).

• Direct or indirect use of assets includes loan of assets to related corporation or use of assets as security in form of pledge, mortgage, or otherwise for indebtedness of related corporation. §1.884-2T(a)(2)(v).

• For purposes of requirement, corporation is related to foreign corporation if either corporation is 10% shareholder of other corporation within meaning of §871(h)(3)(B). §1.884-2T(a)(2)(iv).

36

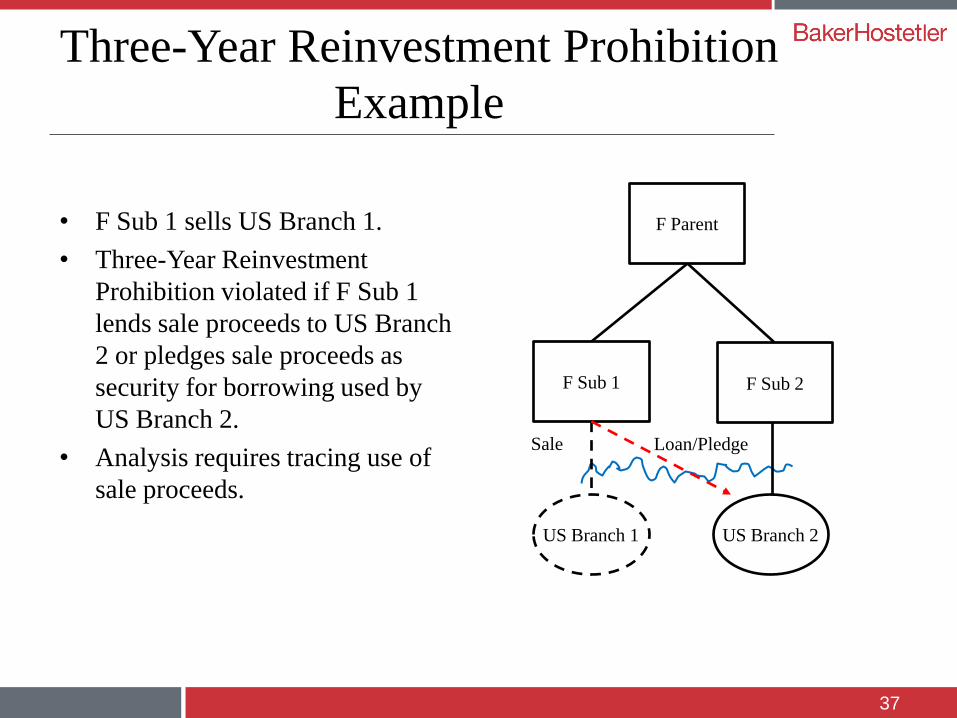

Three-Year Reinvestment Prohibition

Example

• F Sub 1 sells US Branch 1.

• Three-Year Reinvestment

Prohibition violated if F Sub 1

lends sale proceeds to US Branch

2 or pledges sale proceeds as

security for borrowing used by

US Branch 2.

• Analysis requires tracing use of

sale proceeds.

37

F Parent

US Branch 1

Sale

F Sub 1 F Sub 2

US Branch 2

Loan/Pledge

Termination Exception Planning

Considerations

• Separate foreign corporations – To utilize Termination Exception, foreign investors may prefer using separate foreign corporations to operate separate US trades or businesses. This prevents netting of income and losses between US trades or businesses, however.

• §338(g) elections – Termination Exception may apply in context of QSP of foreign corporation with §338(g) election. §1.884-2T(a)(3). Three-Year Reinvestment Prohibition applies to consideration received by shareholders, however.

• Branch reinvestment election – Foreign corporation may elect to be treated as continuing to conduct US trade or business if terminate US trade or business. §1.884-2(b). This may be beneficial if foreign corporation intends to reinvest in new US trade or business, as reinvestment would violate Three-Year Reinvestment Prohibition, so Termination Exception would not be available.

38

§381 Transactions

• Termination Exception does not apply if foreign corporation is

transferor in §381 transaction. §1.884-2T(c).

• BPT generally is deferred. §1.884-2T(c).

– Otherwise, transferor’s US Net Equity would be decreased by transfer of

US Assets and transferee’s US Net Equity would be increased by

acquisition of US Assets.

– Otherwise would result in BPT to transferor and decreased DEA to

transferee, inconsistent with general tax principles of nonrecognition and

carryover of attributes.

• Principles

– Transferor’s US Net Equity determined without regard to transfers of US

Assets or US Liabilities to transferee. §1.884-2T(c)(2)(i).

– Transferor’s ECEP determined without regard to carryover to transferee.

§1.884-2T(c)(2)(ii).

– Transferee inherits ECEP, which retain character. §1.884-2T(c)(4).

– Transferee increases US Net Equity as of close of prior taxable year by

amount of inherited US Net Equity. §1.884-2T(c)(5).

39

Inbound §381 Transactions

• Special rules apply in inbound §381 transactions.

– Foreign shareholders of transferee domestic corporation eligible

for reduced US tax and withholding under treaties on dividends

of inherited non-previously taxed ECEP only to extent that

transferor would have been eligible for reduced BPT under treaty

in taxable year of §381 transaction. §1.884-2T(c)(4)(iii).

– Must file Form 2045 transferee agreement and Form 8848

waiver of period of limitations for six years regarding transfer of

branch assets. §1.884-2(c)(2)(iii).

– Limitations on reinvestment of proceeds from dispositions by

certain significant shareholders of stock of transferee or

transferor during following three taxable years. §1.884-2(c)(6)(i).

If limitations violated, exception not applicable, so transferee

potentially incurs BPT.

40

§351 Transactions

• Foreign corporation also may defer BPT if it transfers part or

all of its branch to domestic corporation in §351 transaction.

§1.884-2T(d). Deferral not available if transferee is foreign

corporation.

– Transferor must “control” (within meaning of §368(c)) transferee

domestic corporation. §1.884-2T(d)(1).

– Transferee domestic corporation inherits ECEP. §1.884-2T(d)(4).

Similar limitation on ability of shareholders of transferee

domestic corporation to reduce US tax and withholding on

dividends of ECEP.

– Transferor generally recognizes DEA if it disposes of stock of

transferee domestic corporation. §1.884-2T(d)(5).

– Deferral is elective. §1.884-2T(d)(3).

– Filing requirements must be satisfied.

41

III – Branch-Level Interest

Tax

42

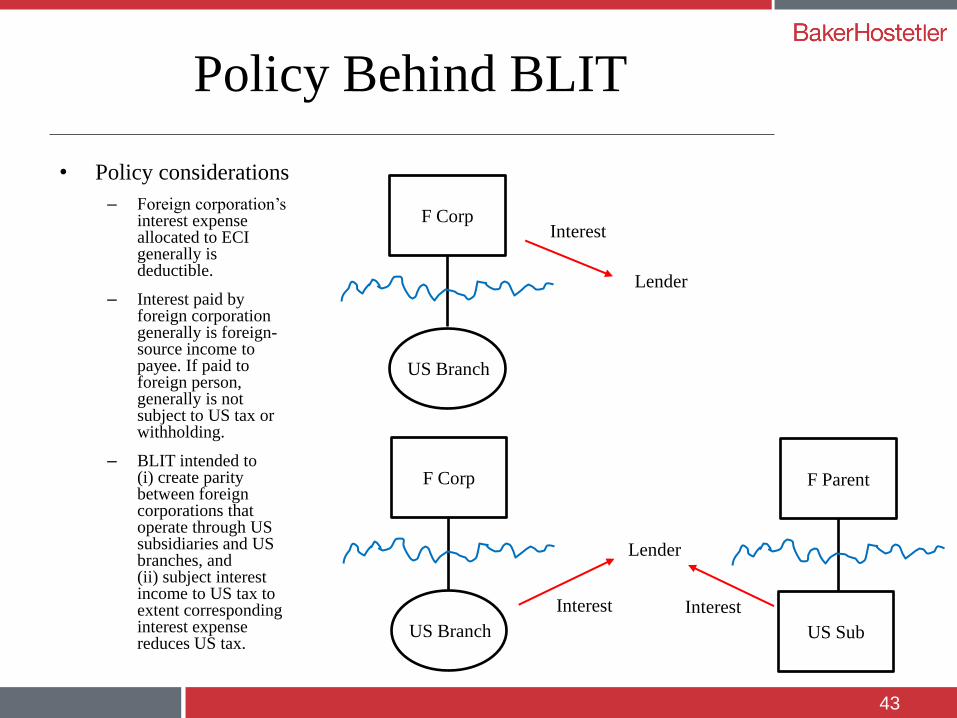

Policy Behind BLIT

• Policy considerations

– Foreign corporation’s interest expense allocated to ECI generally is deductible.

– Interest paid by foreign corporation generally is foreign-source income to payee. If paid to foreign person, generally is not subject to US tax or withholding.

– BLIT intended to (i) create parity between foreign corporations that operate through US subsidiaries and US branches, and (ii) subject interest income to US tax to extent corresponding interest expense reduces US tax.

43

F Corp

Lender

US Branch

Interest

F Corp

Lender

US Branch

Interest

F Parent

Interest

US Sub

BLIT

• Branch interest tax

– Interest “paid by” USTB of foreign corporation (Branch Interest) treated

as paid by domestic corporation. §884(f)(1)(A); §1.884-4(a)(1).

– Because Branch Interest treated as paid by domestic corporation, treated

as US-source. Branch Interest paid to foreign person generally subject to

US tax and withholding. Also, branch interest paid to domestic

corporation is U.S.-source for purposes of FTC. §1.884-4(a)(1).

• Excess interest tax

– Excess of interest expense “allocable” to USTB (Allocated Interest) over

Branch Interest (Excess Interest) treated as received by foreign

corporation from domestic subsidiary. §884(f)(1)(B); §1.884-4(a)(2)(ii).

– Foreign corporation generally liable for US tax on Excess Interest under

§881(a). §1.884-4(a)(2)(ii). Tax thus imposed on notional interest

payment.

– Tax on Excess Interest reported by foreign corporation and is not subject

to US withholding. §1.884-4(a)(2)(iv).

44

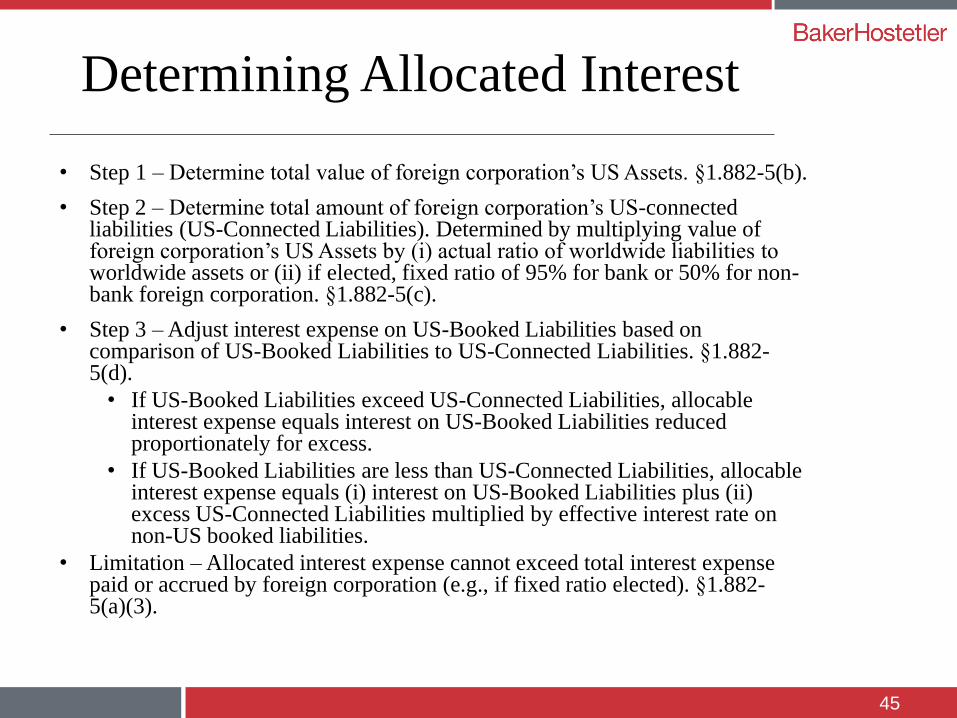

Determining Allocated Interest

• Step 1 – Determine total value of foreign corporation’s US Assets. §1.882-5(b).

• Step 2 – Determine total amount of foreign corporation’s US-connected liabilities (US-Connected Liabilities). Determined by multiplying value of foreign corporation’s US Assets by (i) actual ratio of worldwide liabilities to worldwide assets or (ii) if elected, fixed ratio of 95% for bank or 50% for non-bank foreign corporation. §1.882-5(c).

• Step 3 – Adjust interest expense on US-Booked Liabilities based on comparison of US-Booked Liabilities to US-Connected Liabilities. §1.882-5(d).

• If US-Booked Liabilities exceed US-Connected Liabilities, allocable interest expense equals interest on US-Booked Liabilities reduced proportionately for excess.

• If US-Booked Liabilities are less than US-Connected Liabilities, allocable interest expense equals (i) interest on US-Booked Liabilities plus (ii) excess US-Connected Liabilities multiplied by effective interest rate on non-US booked liabilities.

• Limitation – Allocated interest expense cannot exceed total interest expense paid or accrued by foreign corporation (e.g., if fixed ratio elected). §1.882-5(a)(3).

45

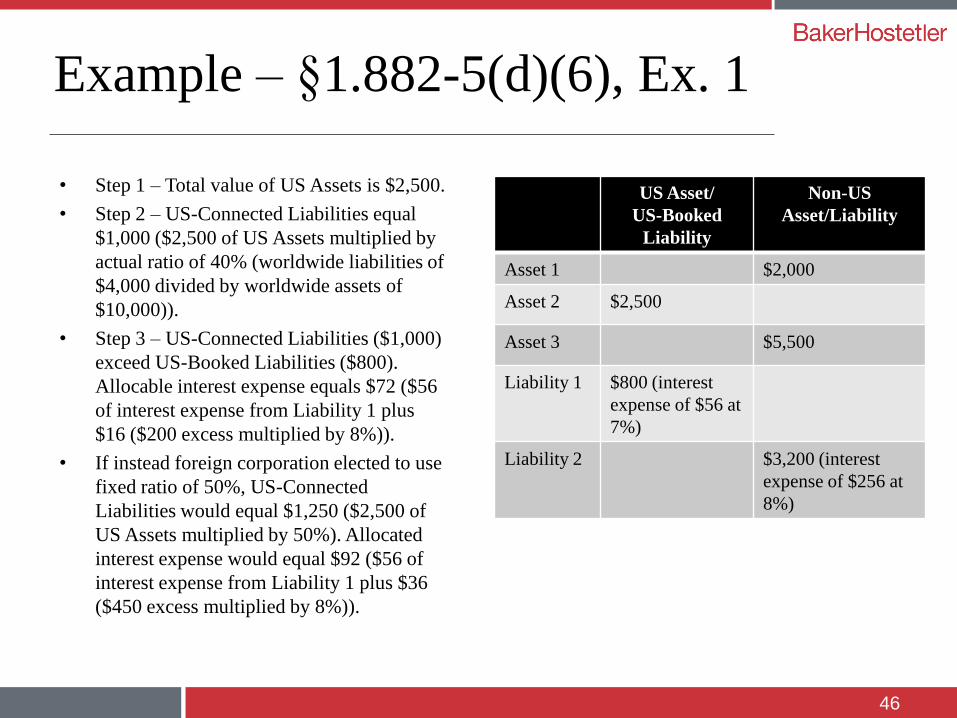

Example – §1.882-5(d)(6), Ex. 1

• Step 1 – Total value of US Assets is $2,500.

• Step 2 – US-Connected Liabilities equal

$1,000 ($2,500 of US Assets multiplied by

actual ratio of 40% (worldwide liabilities of

$4,000 divided by worldwide assets of

$10,000)).

• Step 3 – US-Connected Liabilities ($1,000)

exceed US-Booked Liabilities ($800).

Allocable interest expense equals $72 ($56

of interest expense from Liability 1 plus

$16 ($200 excess multiplied by 8%)).

• If instead foreign corporation elected to use

fixed ratio of 50%, US-Connected

Liabilities would equal $1,250 ($2,500 of

US Assets multiplied by 50%). Allocated

interest expense would equal $92 ($56 of

interest expense from Liability 1 plus $36

($450 excess multiplied by 8%)).

46

US Asset/

US-Booked

Liability

Non-US

Asset/Liability

Asset 1 $2,000

Asset 2 $2,500

Asset 3 $5,500

Liability 1 $800 (interest

expense of $56 at

7%)

Liability 2 $3,200 (interest

expense of $256 at

8%)

Branch Interest

• Branch Interest includes interest paid with respect to:

– US booked liability (US Booked Liability). §1.884-4(b)(i)(A).

– Insurance liability on US business. §1.884-4(b)(i)(B).

– Liability giving rise to interest expense that is directly allocated

to income from US Asset. §1.884-4(b)(i)(B).

– Generally, liability that is specifically identified as liability of

USTB of foreign corporation on or before earlier of (i) date first

payment of interest made or (ii) due date for tax return (including

extensions) and that satisfies certain requirements (Specifically

Identified Liability). §1.884-4(b)(ii).

47

Liabilities Giving Rise to Branch Interest

• US Booked Liability – Liability properly reflected on books of USTB: – Liability secured predominantly by US Assets of foreign corporation. §1.882-

5(d)(2)(ii)(A)(1).

– Foreign corporation enters liability on books at time reasonably contemporaneous with time liability incurred and liability relates to activity that generates ECI. §1.882-5(d)(2)(ii)(A)(2).

– Foreign corporation maintains books relating to activity that generates ECI and IRS determines that there is direct connection between liability and activity. §1.882-5(d)(2)(ii)(A)(3).

• Specifically Identified Liability requirements – Amount of interest does not exceed 85% of interest of foreign corporation that

would be Excess Interest before taking into account interest treated as Branch Interest under Specifically Identified Liability rule. §1.884-4(b)(1)(ii)(A).

– Liability identified as required in §1.884-4(b)(3)(i).

– Recipient of interest notified as required in §1.884-4(b)(3)(ii). §1.884-4(b)(1)(ii)(B).

– Liability not (i) directly related to foreign trade or business or (ii) secured by foreign assets. §1.884-4(b)(1)(ii)(C).

48

Special Rules for Branch Interest

• 80% gross-up – Generally, foreign corporation must treat 100% of

interest expense as Branch Interest if US Assets for year are at least

80% of sum of money and E&P bases of all properties, unless

liability giving rise to interest is (i) directly related to foreign trade

or business or (ii) secured by foreign assets. §1.884-4(b)(5)(i).

• Scale-back Rule – If Branch Interest exceeds interest expense

allocated to ECI under §1.882-5 (Allocated Interest), excess is

treated as not being Branch Interest. §1.884-4(b)(6).

– Scale-back rule can override the 80% gross-up rule. §1.884-4(b)(5)(i).

– If interest is treated as not being Branch Interest, it is not treated as paid by a

domestic corporation.

– Default order of reductions of interest on last-incurred basis: (i) Specifically

Identified Liabilities and (ii) US Booked Liabilities. Alternatively, may specify

liabilities treated as not giving rise to Branch Interest.

49

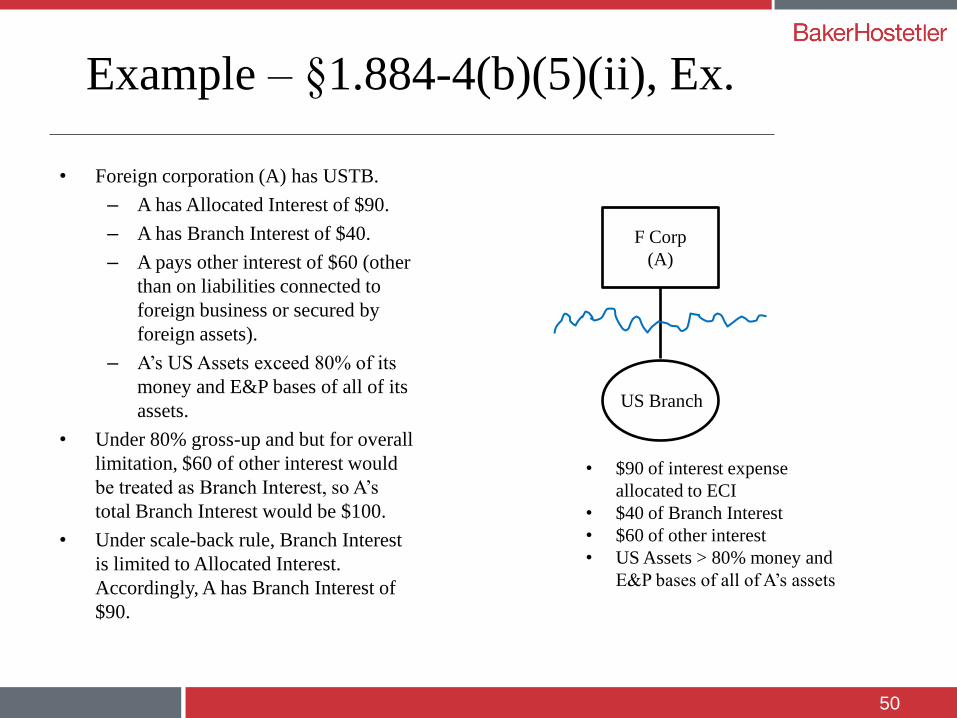

Example – §1.884-4(b)(5)(ii), Ex.

• Foreign corporation (A) has USTB.

– A has Allocated Interest of $90.

– A has Branch Interest of $40.

– A pays other interest of $60 (other

than on liabilities connected to

foreign business or secured by

foreign assets).

– A’s US Assets exceed 80% of its

money and E&P bases of all of its

assets.

• Under 80% gross-up and but for overall

limitation, $60 of other interest would

be treated as Branch Interest, so A’s

total Branch Interest would be $100.

• Under scale-back rule, Branch Interest

is limited to Allocated Interest.

Accordingly, A has Branch Interest of

$90.

50

F Corp

(A)

US Branch

• $90 of interest expense

allocated to ECI

• $40 of Branch Interest

• $60 of other interest

• US Assets > 80% money and

E&P bases of all of A’s assets

Taxation of Branch Interest

• Exceptions to US tax or withholding on Branch Interest paid to

foreign person (§1.884-4(a)(1)):

– Interest is ECI (US tax but no US withholding)

– Portfolio interest exemption

– US bank deposit interest exception

– Reduced tax rate or exemption under treaty

• Policy is that these exceptions to US tax or withholding would apply

to interest paid by wholly owned domestic subsidiary of foreign

corporation

• Other rules potentially applicable to Branch Interest:

– §1.881-3 anti-conduit financing regulations

– §894(c) if Branch Interest paid to hybrid entity

– Proposed regulations would apply §163(j) anti-earnings stripping rules to defer

deductions for Branch Interest paid to a related person and Excess Interest, in

certain circumstances. Prop. §1.163(j)-8.

51

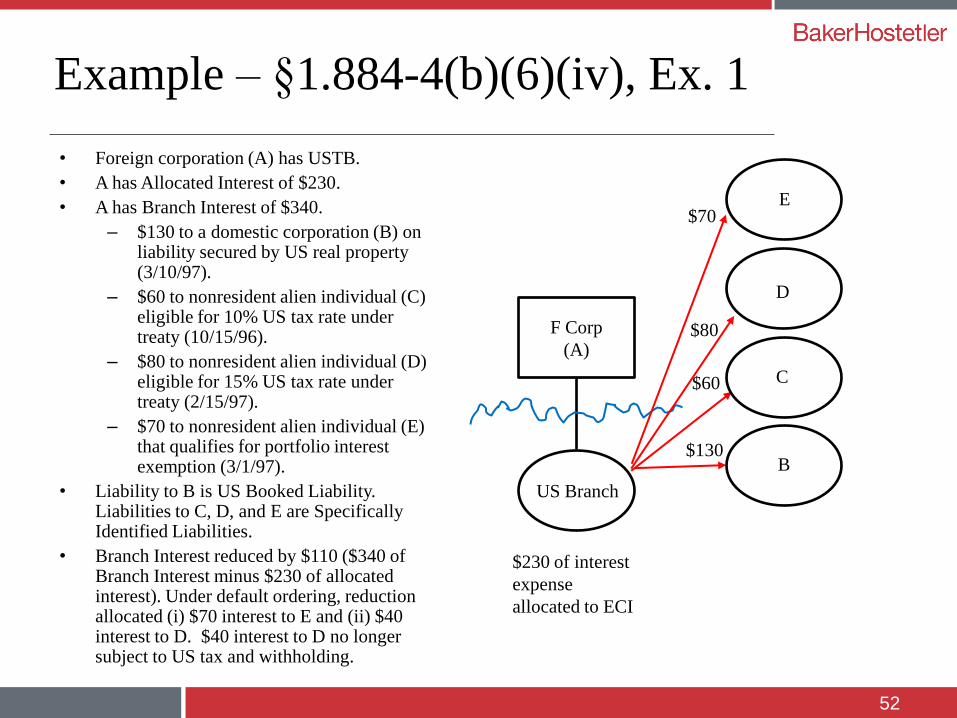

Example – §1.884-4(b)(6)(iv), Ex. 1

• Foreign corporation (A) has USTB.

• A has Allocated Interest of $230.

• A has Branch Interest of $340.

– $130 to a domestic corporation (B) on liability secured by US real property (3/10/97).

– $60 to nonresident alien individual (C) eligible for 10% US tax rate under treaty (10/15/96).

– $80 to nonresident alien individual (D) eligible for 15% US tax rate under treaty (2/15/97).

– $70 to nonresident alien individual (E) that qualifies for portfolio interest exemption (3/1/97).

• Liability to B is US Booked Liability. Liabilities to C, D, and E are Specifically Identified Liabilities.

• Branch Interest reduced by $110 ($340 of Branch Interest minus $230 of allocated interest). Under default ordering, reduction allocated (i) $70 interest to E and (ii) $40 interest to D. $40 interest to D no longer subject to US tax and withholding.

52

F Corp

(A)

D

US Branch

$80

C

B

$60

$130

$230 of interest

expense

allocated to ECI

E $70

Taxation of Excess Interest

• Excess Interest generally equals (i) Allocated Interest minus (ii) Branch Interest. §1.884-4(a)(2)(i).

• Excess Interest treated as paid to foreign corporation by wholly owned subsidiary domestic corporation. – US tax on Excess Interest reported on foreign corporation’s Form 1120F. Not

subject to withholding. §1.884-4(a)(2)(iv).

– Only potentially available exceptions to US tax are (i) US bank deposit interest exception, and (iv) reduced tax rate or exemption under treaty. §1.884-4(a)(2)(ii). Portfolio interest exemption not available because Excess Interest deemed paid by wholly owned domestic corporation to foreign corporation.

• Foreign corporation may elect to treat Branch Interest as if paid in year in which it accrues. §1.884-4(c)(1). – Effect is to reduce Excess Interest in year Branch Interest accrues, rather than year

paid.

– Prevents mismatch that would result because Excess Interest determined based on interest expense paid or accrued whereas, but for election, Branch Interest determined based on interest paid.

– If no election made, interest could be taxed twice: first as Excess Interest in year accrued and second as Branch Interest in year paid.

53

Example – §1.884-4(a)(4), Ex. 1

• Foreign corporation (A) has US trade or business.

• A has Allocated Interest of $120.

• A has Branch Interest of $100.

– $55 to a nonresident alien (B), which qualifies for portfolio interest exemption

– $25 to foreign corporation (C) that owns 15% of voting power of A, which is subject to $7.50 of US tax and withholding ($25 of Branch Interest x 30%)

– $20 to domestic corporation (D), which is not subject to US withholding

• Excess Interest = $20 ($120 of Allocated Interest minus $100 of Branch Interest). Excess Interest subject to $6 of US tax ($20 of Excess Interest x 30%).

54

F Corp

(A)

B

US Branch

$55

C

D

$25

$20

$120 of interest

expense

allocated to ECI

BLIT Planning Considerations

• Several reasons Excess Interest may be less favorable than Branch

Interest:

– Tax on Excess Interest imposed directly on foreign corporation, whereas tax on

Branch Interest imposed on payee.

– Exemptions under US domestic tax law potentially available for tax on Branch

Interest (e.g., portfolio interest exemption) but not tax on Excess Interest.

– Tax treaties may be less likely to reduce tax on Excess Interest.

• As planning matter, can avoid Excess Interest by over-booking

liabilities as US-Booked Liabilities and relying on scale-back rule to

reduce Branch Interest. Can identify which interest not treated as

Branch Interest under scale-back rule tax-efficiently.

• 80% gross-up can be favorable in that it converts Excess Interest to

Branch Interest, but can raise withholding issues.

55

III – Branch Tax Compliance

56

General Reporting Considerations

• If foreign corporation conducts US trade or business, must file Form

1120-F, regardless of whether:

– Foreign corporation has ECI,

– Foreign corporation has US-source income, or

– Foreign corporation’s income is exempt from US tax under treaty. §1.6012-

2(g)(1)(i).

• Consequences of failure to file Form 1120-F:

– Penalties. §§6651, 6662-6663, and 7203.

– Denial of deductions and credits. §1.882-4(a)(2).

• Rule has been upheld as valid. See Swallows Holding Ltd. v. Commissioner,

515 F.3d 162 (3d Cir).

• Unclear whether rule applies if foreign corporation claims benefits under US

tax treaty.

– Period of limitations remains open. §6501(c)(3).

• Foreign corporation that claims benefits under treaty must file Form

8833. §301.6114-1(a)(1).

57

Reporting BPT

• BPT reported on Form 1120-F,

Section III.

• Foreign corporation need not

withhold or report DEAs on

Form 1042 and Form 1042-S.

• BPT not collected through

estimated tax payments.

• To claim reduced US tax rate

under treaty, foreign

corporation files Form 8833.

58

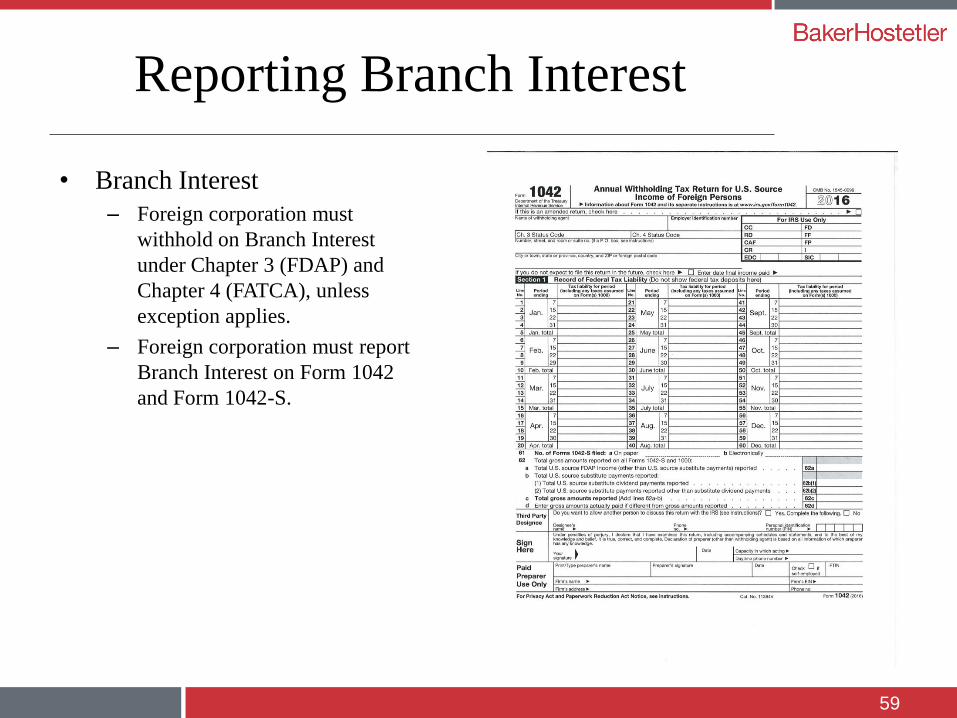

Reporting Branch Interest

• Branch Interest

– Foreign corporation must

withhold on Branch Interest

under Chapter 3 (FDAP) and

Chapter 4 (FATCA), unless

exception applies.

– Foreign corporation must report

Branch Interest on Form 1042

and Form 1042-S.

59

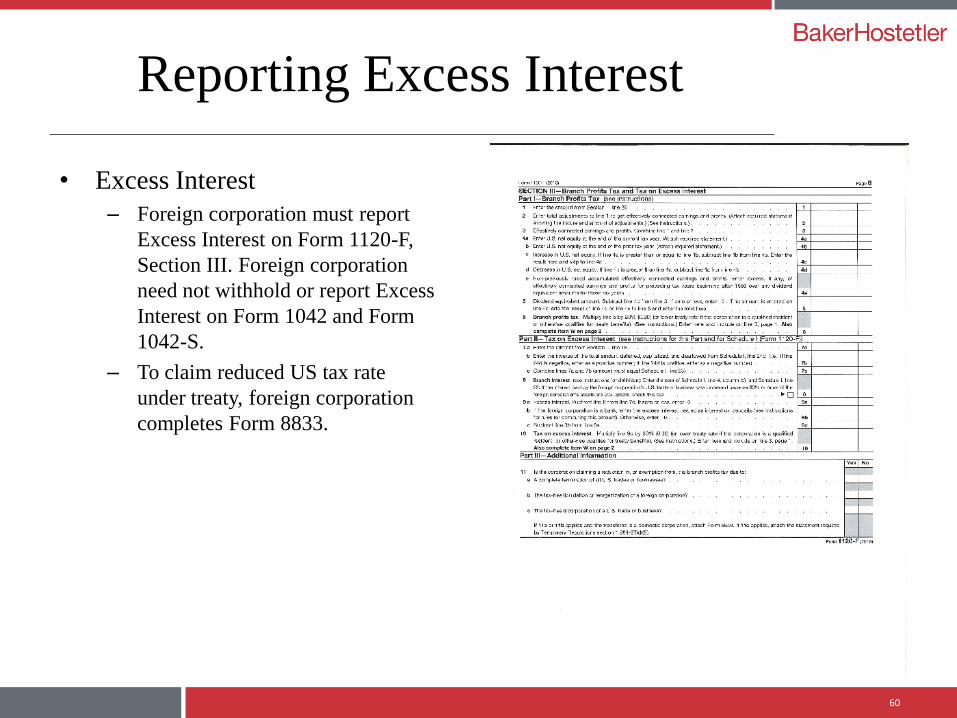

Reporting Excess Interest

• Excess Interest

– Foreign corporation must report

Excess Interest on Form 1120-F,

Section III. Foreign corporation

need not withhold or report Excess

Interest on Form 1042 and Form

1042-S.

– To claim reduced US tax rate

under treaty, foreign corporation

completes Form 8833.

60

60

IV – Branch Profits Tax and

FIRPTA

62

FIRPTA

• Under FIRPTA, gain on disposition of US real property

interest (USRPI) treated as ECI. §897(a)(1).

• USRPIs generally include:

– Interest in real property in United States. §897(c)(1)(A)(i).

– Interest other than solely as creditor in domestic corporation

unless taxpayer establishes that domestic corporation was not

US real property holding corporation (USRPHC) at any time in

five years preceding disposition. §897(c)(1)(A)(ii).

• Corporation is a USRPHC if value of its USRPIs is 50% or more of value

of its (i) USRPIs, (ii) foreign real property interests, and (iii) assets used

in a trade or business. §897(c)(2). Look-through rule applies if

corporation owns 50% or more of stock of subsidiary corporation, by

value. §897(c)(5).

• Foreign corporation may be treated as USRPHC for limited purpose of

testing whether domestic corporation is USRPHC. §897(c)(4)(A).

FIRPTA does not apply to gain on stock of foreign corporation, however.

63

Interaction of FIRPTA and BPT

• US Asset

– If income from USRPI is ECI, USRPI is a US Asset. §1.884-1(d)(3)(i), Ex. 2.

This includes if foreign corporation makes §882(d) election to treat income

derived from real property as ECI.

– If income from USRPI is not ECI, USRPI is not a US Asset. §1.884-1(d)(3)(i),

Ex. 3. Gain from sale of USRPI nonetheless may give rise to ECEP subject to

BPT.

• ECEP

– Gain on USRPI generally is ECI and thus gives rise to ECEP. §884(d)(1).

– Exception

• Gain on interest other than as creditor in domestic corporation that was

USRPHC within preceding five years does not give rise to ECEP even

though it is treated as ECI. §884(d)(2)(C).

• Policy is to avoid triple taxation. First level of tax at domestic corporation,

and second level of tax at interest holder. BPT would be third level of tax.

64

Interaction of FIRPTA and BPT

• Scenario 1

– Gain gives rise to ECEP

– Consider application of

Termination Exception. See

CCA 200504029.

• Scenario 2 – Gain does not give

rise to ECEP even though it

constitutes ECI under FIRPTA.

65

F

Purchaser

USRPI

F

Purchaser

USRPHC

V – Branch Taxes and Tax Treaties

66

Tax Treaties

• Benefits under US tax treaties generally include: – Reduced US tax rates on US-source dividends and interest income.

– Business profits taxable in United States only to extent they are attributable to US permanent establishment.

• Requirements for qualifying for benefits under US tax treaties: – Residence – Foreign corporation typically resident of treaty country if liable to tax by

reason of place of incorporation, place of management, or similar nature.

– Limitation on benefits – Limitation on benefits tests applicable to foreign corporations in modern US tax treaties include:

• Publicly traded test

• Subsidiary of publicly traded company test

• Ownership/base erosion test

• Active trade or business test (only with respect to income connected to trade or business in treaty country)

• Derivative benefits test

• Discretionary test

– Operative treaty provisions (e.g., dividends article in treaty)

– US domestic tax law overrides (e.g., §894(c), §1.881-3)

67

BPT and Treaties

• Relief from BPT varies by US tax treaty. US tax treaties generally may:

– Reduce BPT rate (including to 0% under certain treaties).

– Limit BPT to business profits attributable to US permanent establishment (rather

than ECEP).

– Eliminate BPT under nondiscrimination provision (older treaties).

• US model treaty would reduce BPT rate in dividends article to lowest tax rate

applicable to dividends. BPT rate of 5% in 2016 US Model, Art. 10(10).

• Policy is that BPT is substitute for US tax on dividends paid by wholly owned

domestic subsidiary, and US tax treaties generally reduce US tax rates on

dividends. Recent US tax treaties reduce BPT rate to 5% or 0%, generally.

• Consistency principle

– Foreign corporation that applies business profits/permanent establishment articles

of US tax treaty to determine taxable income, must apply same rules to determine

Dividend Equivalent Amount.

– Foreign corporation that applies US domestic tax law to determine taxable income,

must use US domestic tax law to determine Dividend Equivalent Amount.

68

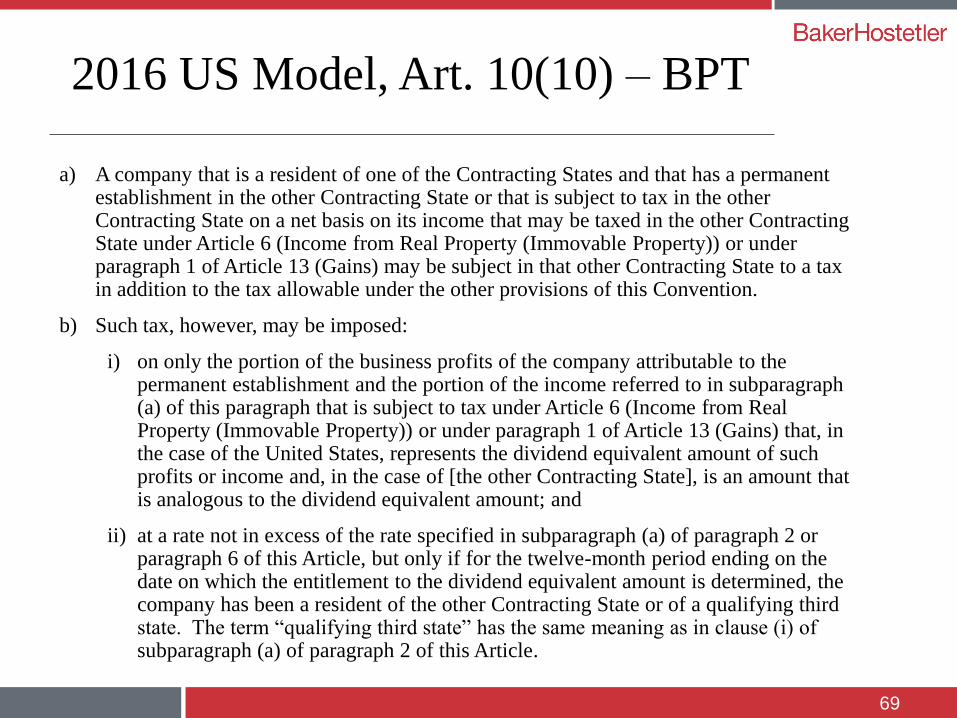

2016 US Model, Art. 10(10) – BPT

a) A company that is a resident of one of the Contracting States and that has a permanent establishment in the other Contracting State or that is subject to tax in the other Contracting State on a net basis on its income that may be taxed in the other Contracting State under Article 6 (Income from Real Property (Immovable Property)) or under paragraph 1 of Article 13 (Gains) may be subject in that other Contracting State to a tax in addition to the tax allowable under the other provisions of this Convention.

b) Such tax, however, may be imposed:

i) on only the portion of the business profits of the company attributable to the permanent establishment and the portion of the income referred to in subparagraph (a) of this paragraph that is subject to tax under Article 6 (Income from Real Property (Immovable Property)) or under paragraph 1 of Article 13 (Gains) that, in the case of the United States, represents the dividend equivalent amount of such profits or income and, in the case of [the other Contracting State], is an amount that is analogous to the dividend equivalent amount; and

ii) at a rate not in excess of the rate specified in subparagraph (a) of paragraph 2 or paragraph 6 of this Article, but only if for the twelve-month period ending on the date on which the entitlement to the dividend equivalent amount is determined, the company has been a resident of the other Contracting State or of a qualifying third state. The term “qualifying third state” has the same meaning as in clause (i) of subparagraph (a) of paragraph 2 of this Article.

69

2016 US Model, Art. 24(6) – Exception to

Nondiscrimination

1. Nationals of a Contracting State shall not be subjected in the other Contracting state to any

taxation or any requirement connected therewith that is more burdensome than the taxation

and connected requirements to which nationals of that other Contracting State in the same

circumstances, in particular with respect to residence, are or may be subjected. This provision

shall also apply to persons who are not residents of one or both of the Contracting States.

However, for the purposes of United States taxation, United States nationals who are subject

to tax on a worldwide basis are not in the same circumstances as nationals of [the other

Contracting State] who are not residents of the United States.

…

6. Nothing in this Article shall be construed as preventing either Contracting State from

imposing a tax as described in paragraph 10 of Article 10 (Dividends) or paragraph 7 of

Article 11 (Interest).

70

Treaties that Eliminate BPT

• China (1984)

• Cyprus (1984)

• Egypt (1980)

• Hungary (1979; new treaty that has been signed but not ratified would

permit BPT)

• Jamaica (1980)

• Korea (1976)

• Morocco (1977)

• Norway (1971)

• Pakistan (1957)

• Philippines (1976)

71

Qualified Resident Requirement

• Foreign corporation eligible

for reduction or elimination of

BPT under US tax treaty only

if:

– foreign corporation is qualified

resident (Qualified Resident), or

– US tax treaty has limitation on

benefits article that entered into

force after 12/31/86. §1.884-1(g).

• Qualified Resident –

Alternative tests in §1.884-5:

– ownership/base erosion test

– publicly traded company test

– active trade or business test

– discretionary IRS ruling

72

F

(Treaty

Country)

US Branch

ECEP Compared to Attributable Profits

• ECEP – Determined using rules for determining ECI (e.g., limited force of attraction)

– Inter-branch transactions (i.e., transactions between branch and foreign corporation or between branches of foreign corporation) not taken into account.

• Business profits attributable to US permanent establishment – Profits that US permanent establishment would be expected to earn if it were a

separate enterprise. Encompasses separate entity principle and “arm’s length” transfer pricing principles.

– Authorized OECD Approach (AOA) takes into account assets used, risks assumed, and activities performed by permanent establishment, and apply OECD Transfer Pricing Guidelines. Inter-branch transactions are taken into account.

• Step 1 – Treat PE as separate enterprise, attributing functions, assets, and risks.

• Step 2 – Apply OECD transfer pricing guidelines to inter-branch transactions.

• Consistency principle applies to election to apply treaty rules or US domestic tax law rules.

73

Branch Interest and Treaties

• US tax treaties generally may reduce or

eliminate BLIT rate. Different rules apply to

Branch Interest and Excess Interest.

• Tax rate applicable to Branch Interest may be

reduced under interest article of US tax treaty

of either (i) foreign corporation (payer) or (ii)

foreign payee. §1.884-4(b)(8).

• Foreign corporation (payer) or foreign payee

generally may claim reduced tax rate on

Branch Interest if it is:

– Qualified Resident, or

– US tax treaty has limitation on benefits

article that entered into force after

12/31/86. §1.884-4(b)(8)(i)-(ii).

• If F satisfies requirements, reduced or zero tax

rate applies to Branch Interest under US-

Country X treaty, even if there is no US

Country Y treaty. §1.884-4(b)(8)(vi), Ex. 1.

74

F

(Country X) Lender

(Country Y)

US

Interest

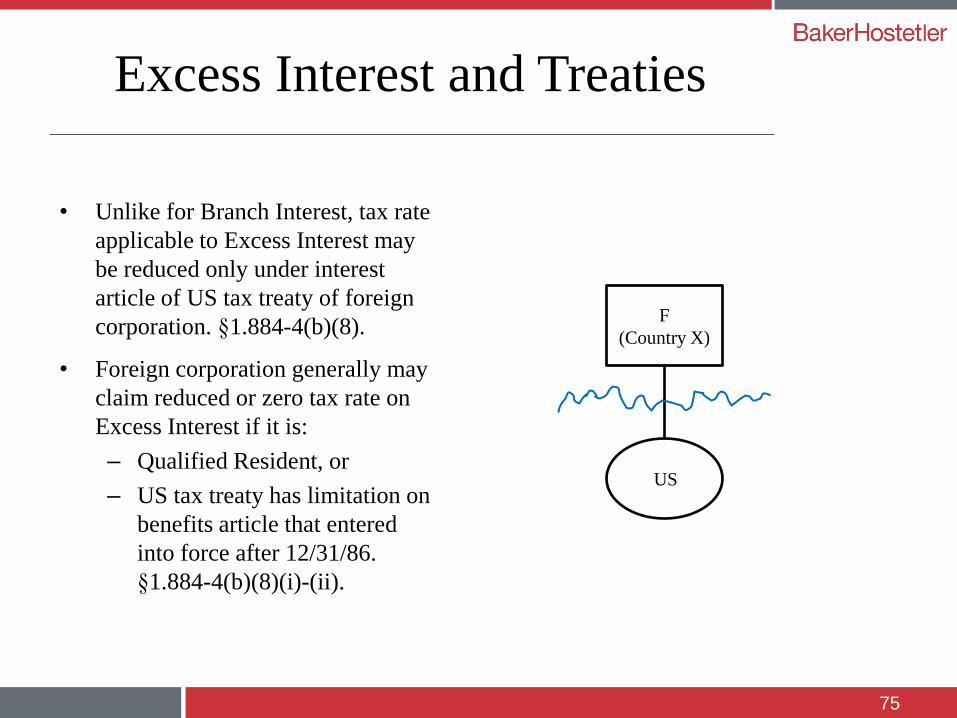

Excess Interest and Treaties

• Unlike for Branch Interest, tax rate

applicable to Excess Interest may

be reduced only under interest

article of US tax treaty of foreign

corporation. §1.884-4(b)(8).

• Foreign corporation generally may

claim reduced or zero tax rate on

Excess Interest if it is:

– Qualified Resident, or

– US tax treaty has limitation on

benefits article that entered

into force after 12/31/86.

§1.884-4(b)(8)(i)-(ii).

75

F

(Country X)

US

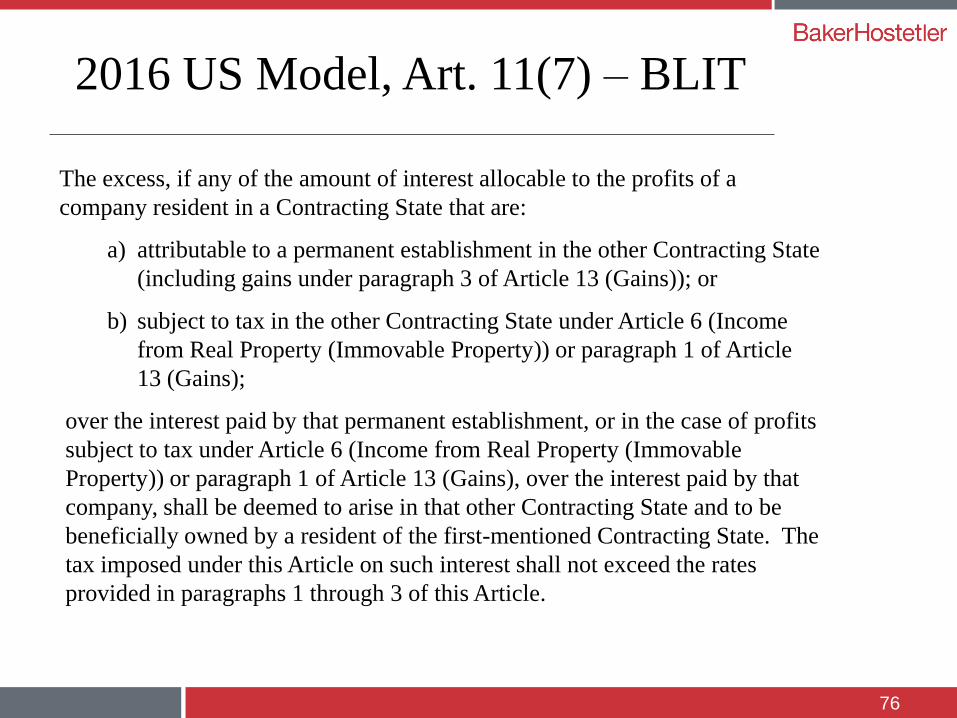

2016 US Model, Art. 11(7) – BLIT

The excess, if any of the amount of interest allocable to the profits of a

company resident in a Contracting State that are:

a) attributable to a permanent establishment in the other Contracting State

(including gains under paragraph 3 of Article 13 (Gains)); or

b) subject to tax in the other Contracting State under Article 6 (Income

from Real Property (Immovable Property)) or paragraph 1 of Article

13 (Gains);

over the interest paid by that permanent establishment, or in the case of profits

subject to tax under Article 6 (Income from Real Property (Immovable

Property)) or paragraph 1 of Article 13 (Gains), over the interest paid by that

company, shall be deemed to arise in that other Contracting State and to be

beneficially owned by a resident of the first-mentioned Contracting State. The

tax imposed under this Article on such interest shall not exceed the rates

provided in paragraphs 1 through 3 of this Article.

76

VI – Structures

77

US “Blocker”

• Many foreign corporations

conduct business in United States

through domestic subsidiaries to

avoid filing Form 1120-Fs. Also

avoids BPT and BLIT.

• Non-tax considerations:

– Administrative costs of subsidiaries

– Limited liability

• Dividends and interest paid by

domestic subsidiary subject to US

tax at 30% rate unless reduced rate

applies under US tax treaty.

• Must consider §163(j) and §385

regulations, among other

provisions.

78

Foreign

Corp

US Corp

Loan

Foreign Hybrid Entity

• Foreign corporation owns foreign entity,

which conducts a US trade or business.

• Foreign entity treated as disregarded entity

for US tax purposes but is fiscally

regarded for foreign tax purposes.

• May foreign disregarded entity claim

reduced BPT rate under US tax treaty?

• Under 2016 US Model, Art. 1(6), hybrid

entity generally may be resident of treaty

country and treated as deriving income.

• For a discussion, see Penn, Nauheim, and

Conklin, Applying Branch Profits Tax

Treaty Limits to Hybrid Entities, Tax

Notes (Nov. 21, 2011).

79

F Corp

(No Treaty)

F DRE

(Treaty)

US Branch

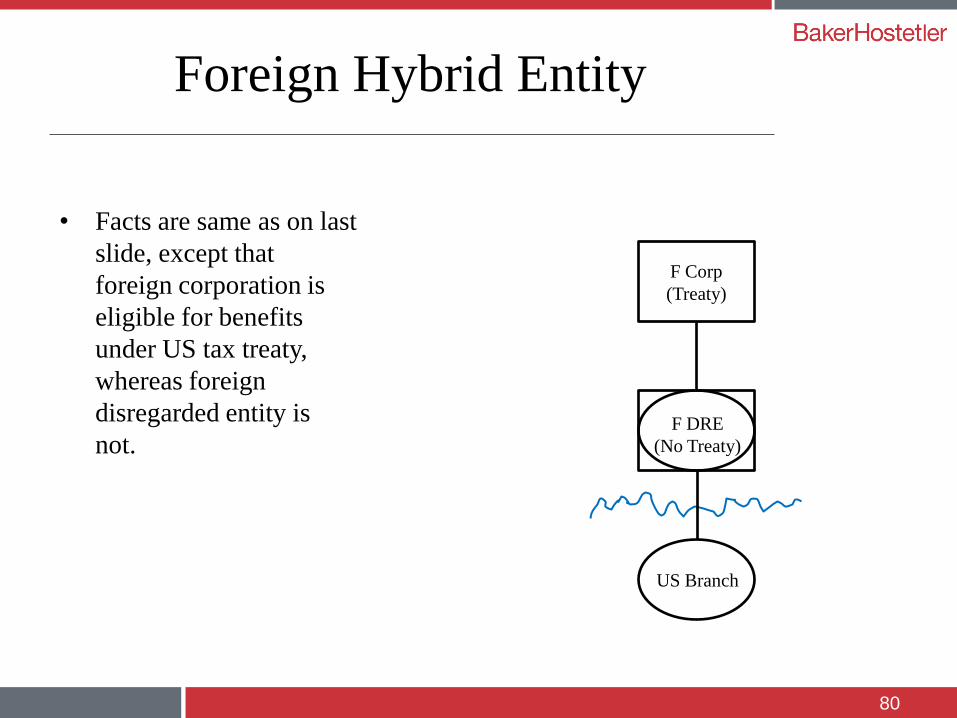

Foreign Hybrid Entity

• Facts are same as on last

slide, except that

foreign corporation is

eligible for benefits

under US tax treaty,

whereas foreign

disregarded entity is

not.

80

F Corp

(Treaty)

F DRE

(No Treaty)

US Branch

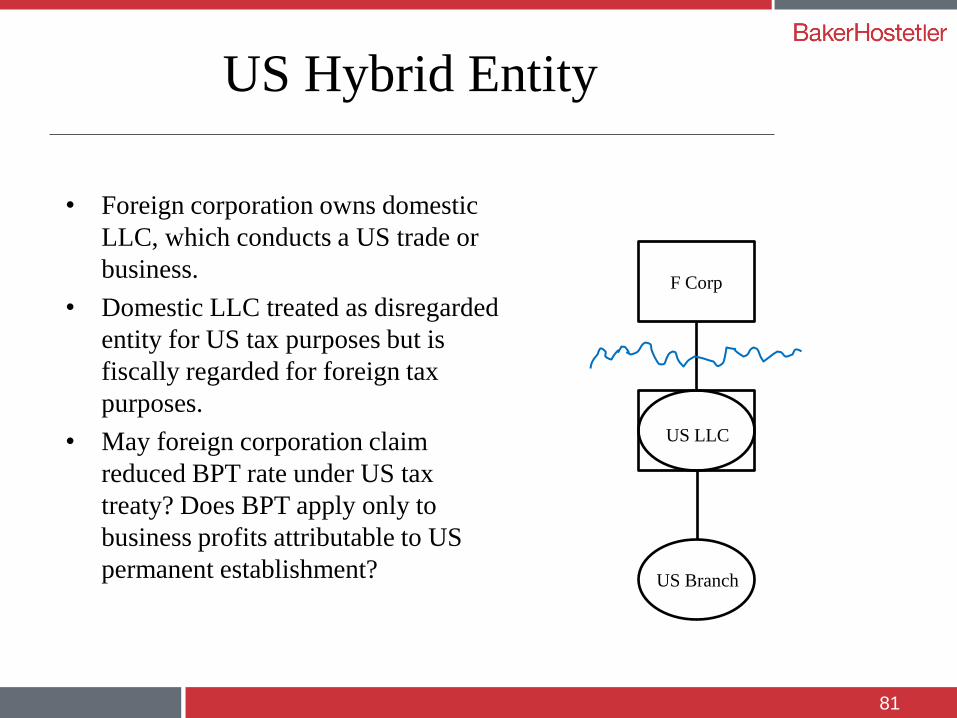

US Hybrid Entity

• Foreign corporation owns domestic

LLC, which conducts a US trade or

business.

• Domestic LLC treated as disregarded

entity for US tax purposes but is

fiscally regarded for foreign tax

purposes.

• May foreign corporation claim

reduced BPT rate under US tax

treaty? Does BPT apply only to

business profits attributable to US

permanent establishment?

81

F Corp

US LLC

US Branch

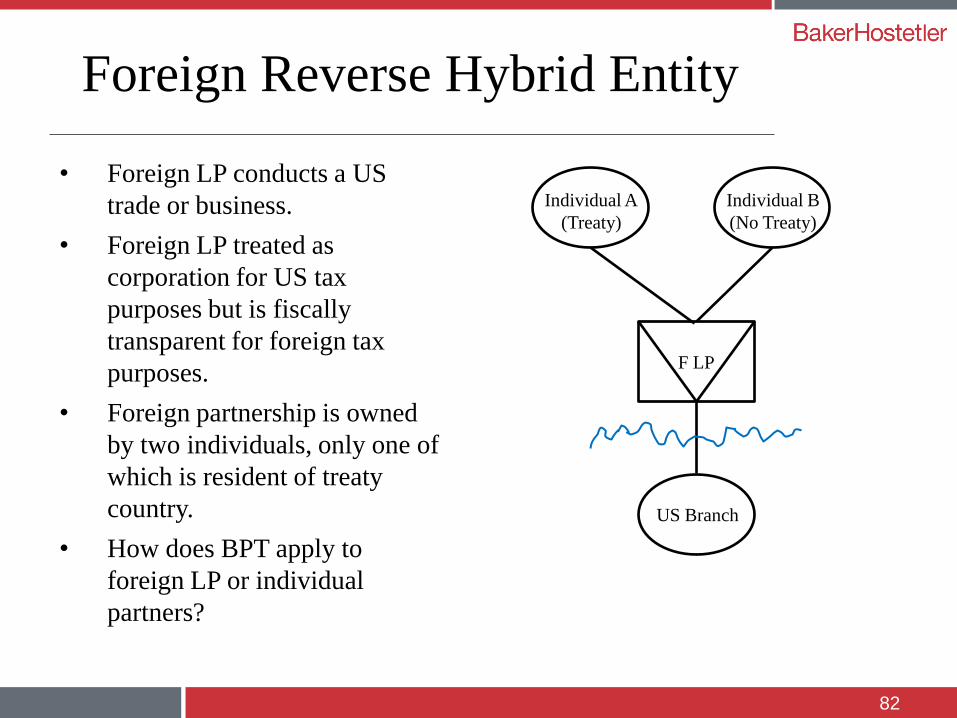

Foreign Reverse Hybrid Entity

• Foreign LP conducts a US

trade or business.

• Foreign LP treated as

corporation for US tax

purposes but is fiscally

transparent for foreign tax

purposes.

• Foreign partnership is owned

by two individuals, only one of

which is resident of treaty

country.

• How does BPT apply to

foreign LP or individual

partners?

82

F LP

US Branch

Individual A

(Treaty)

Individual B

(No Treaty)