Embed Size (px)

Citation preview

BPZ5A / BPG5B

COST ACCOUNTING

UNIT I - V

BPZ5A/BPG5B - COST ACCOUNTING

TM

BPZ5A/BPG5B - COST ACCOUNTING

Syllabus

Nature and scope of Cost Accounting

Cost analysis

Concepts and Classifications

Installation of costing systems

Cost centres and Profit centres.

UNIT -1

FUNDAMENTALS OF COST ACCOUNTING

2

TM

MEANING OF COST ACCOUNTING

It is a process of recording, classifying, analyzing, summarizing,

allocating and evaluating various alternative courses of action for the

control of costs

DEFINITION OF COST ACCOUNTING

The Institute of Cost and Management Accountant, England (ICMA)

has defined ―Cost Accounting as – ―the process of accounting for the

costs from the point at which expenditure incurred, to the establishment

of its ultimate relationship with cost centres and cost units‖

For Simple notes click

http://www.newagepublishers.com/samplechapter/002037.pdf

FUNDAMENTAL S OF COST ACCOUNTING

BPZ5A/BPG5B - COST ACCOUNTING 3

TM

Cost Accounting is a branch of knowledge

Cost Accounting is an Art

Cost Accounting is a Science also

Cost Accounting is a profession

BPZ5A/BPG5B - COST ACCOUNTING 4

NATURE OF COST ACCOUNTING

TM

1. Costing

2. Budgeting

3. Cost Audit

4. Cost Control Techniques

BPZ5A/BPG5B - COST ACCOUNTING 5

SCOPE OF COST ACCOUNTING

TM

Cost unit - A cost unit is a unit of product or unit of service

Cost driver - A cost driver is any factor that influences costs.

A change in the cost driver will lead to a change in the total

cost

Cost Control - Cost control is related to achieving the cost

target as its objectives

Cost Reduction - Cost reduction is directed to explore the

possibility of improving the targets themselves

Cost Methods - Job costing, Contract costing, Batch costing,

Process costing, Operation costing, Output costing, Services

costing.

Costing Techniques - Absorption costing, Marginal costing

and Standard costing

BPZ5A/BPG5B - COST ACCOUNTING 6

CONCEPTS

TM

BPZ5A/BPG5B - COST ACCOUNTING 7

CLASSIFICATION OF COST

TM

Determining selling price of a product

Controlling cost

Providing information for decision making

Ascertaining costing profit

Facilitating for financial and other statements

To provide basis for operating policy

BPZ5A/BPG5B - COST ACCOUNTING 8

OBJECTIVES OF COST ACCOUNTING

TM

BPZ5A/BPG5B - COST ACCOUNTING 9

ADVANTAGES OF COST ACCOUNTING

TM

It is expensive system of Accounting

It is unnecessary method

It is system of estimations and probabilities

Lack of trained professionals

Non cooperation from middle and bottom level managers

It is more complex

Not suitable for small scale units

BPZ5A/BPG5B - COST ACCOUNTING 10

LIMITATIONS OF COST ACCOUNTING

TM

Meaning - The common cost accounting system is not suitable for all

business units. It depends upon the nature of business and the type of product

manufactured.

For the successful functioning of the costing system, the following conditions

are essential:

Efficient system of material control.

A sound and well-designed method of wage payment

Sound basis for collection of all indirect expenses

The integration of cost and financial accounts

The use of printed forms so as to facilitate quick compilation of cost reports.

The duties and responsibilities of cost accountant must be made clear.

1BPZ5A/BPG5B - COST ACCOUNTING 11

INSTALLATION OF COSTING SYSTEM

TM

History of business unit:

Nature of the industry

Product range

Technical considerations

Organizational factors

Selling and distribution method

Accounting aspects

Area of control to be exercised

Reporting

Uniformity

Use of electronic data processing

Practical consideration

BPZ5A/BPG5B - COST ACCOUNTING 12

FACTORS TO BE CONSIDERED BEFORE

INSTALLING A COST ACCOUNTING

SYSTEM

TM

DIFFERENCE BETWEEN COST

ACCOUNTING & FINANCIAL ACCOUNTING

Cost Accounting Point of

Difference

Financial Accounting

Internal Reporting Purpose External Reporting mainly to tax

authorities & Government

Optional Obligation Compulsory

Objective Manner Recording Subjective Manner

Marginal Costing

Budgetary Control

Standard Costing

Control No control techniques

The cost data helps in

evaluationEvaluation of

efficiency

Not sufficient for evaluation

Stock is always valued of

cost price

Valuation of

stock

Stock is valued at cost or market

price

BPZ5A/BPG5B - COST ACCOUNTING 13

TM

Syllabus

Cost sheet

Tenders and quotations

Reconciliation of cost and financial accounts.

UNIT -II

COST SHEET

1BPZ5A/BPG5B - COST ACCOUNTING 14

TM

COST SHEET FORMAT

1. Cost Sheet Without Stock Adjustment

2. Cost Sheet With Stock Adjustment

UNIT -II

COST SHEET

To workout simple problems click

http://download.nos.org/srsec320newE/320EL29a.pdf

BPZ5A/BPG5B - COST ACCOUNTING 15

TMCOST SHEET

Particulars Per Unit Total Cost

Raw materials Consumed xxx

direct Labour xxx

Direct Expenses xxx

Prime Cost xxx

Add: Factory overheads

All expenes incurred in manufacturing xxx xxx

works cost xxx

Add: Office Overheads

All expenses incurred in administration xxx xxx

Cost of Production xxx

Add: Selling & Distribution overheads

All expenses incurred in selling distribution xxx xxx

Cost of Sales xxx

Profit xxx

Sales xxx

1BPZ5A/BPG5B - COST ACCOUNTING 16

TM

According to CIMA London

Cost Sheet is ‗A statement which provides for the assembly of the

detailed cost of a centre or a cost unit‘. It is also a periodical

statement.

‗The expenditure which has been incurred upon product for a period

is extracted from the financial books and the store records and set

out in a memorandum statement.

If this statement is confined to the disclosure of the costs of units

produced dividing the period, it is termed as Cost- Sheet, but where

the statement records both total cost, profit and sales, it is usually

known as Statement of Cost or Production Account‘.

COST SHEET -

DEFINITION

BPZ5A/BPG5B - COST ACCOUNTING 17

TM

(1) Direct Materials:

(2) Direct Labour:

(3) Other Direct or Chargeable Expenses:

(4) Prime Cost:

(5) Works Expenses or Overheads:

(6) Scrap or Wastage:

(7) Work in Progress

(8) Office and Administrative Expenses:

(9) Cost of Production or Office Cost:

(10) Cost of Goods Sold:

(11) Selling and Distribution Expenses:

(12) Profit

ELEMENTS OF COST

BPZ5A/BPG5B - COST ACCOUNTING 18

TM

A manufacturing concern may adopt either Integrated Accounting System or

Non- Integral Accounting System. Under Integrated Accounting System,

only one set of books is maintained to record both costing and financial

transaction, therefore, under this system, both financial accounts and cost

accounts give similar results.

But in Non- Integral Accounting System, separate books are maintained for

costing and financial transactions, which may exhibit different results i.e.

profits or losses. In other words, when cost accounts and financial accounts

are maintained independently by a concern, the profit or loss shown by the

cost accounts may not agree with the profit or loss shown by the financial

accounts. In this situation.

It is needed to reconcile the profits or losses shown differently by cost

accounts and financial account by preparing a statement called ' Cost

Reconciliation Statement‘

CONCEPT AND MEANING OF COST

RECONCILIATION STATEMENT

BPZ5A/BPG5B - COST ACCOUNTING 19

TM

1. Reconciliation helps to check the arithmetical accuracy of both sets of

accounts.

2. Management is enable to know the reasons for the difference in

results of both cost and financial accounts.

3. Reconciliation explains reasons for difference which facilitate internal

control.

4. Reconciliation ensures the reliability of cost data.

5. Reconciliation promotes co-ordination between cost and financial

departments.

6. Reconciliation helps in formulation of policies regarding absorption of

overheads and depreciation and stock valuation method.

7. Reconciliation ensures managerial decision-making.

1

NEED FOR RECONCILIATION

BPZ5A/BPG5B - COST ACCOUNTING 20

TM

Problems need to be worked out under

1. Simple cost sheet

2. Cost Sheet with Stock Adjustment

3. Cost sheet with Tender or Quotation

4. Cost Sheet with Estimated cost for future period

5. Cost Sheet with Hidden Information

6. Reconciliation Statement

PROBLEMS

To check more problems click the following

http://download.nos.org/srsec320newE/320EL28a.pdf

BPZ5A/BPG5B - COST ACCOUNTING 21

TM

BPZ5A/BPG5B - COST ACCOUNTING 22

TM

Syllabus

Material purchase control

Levels, aspects, need

Essentials of material control

Stores control

Stores Department

EOQ

Stores Records

ABC analysis

VED analysis

Material costing

Issue of materials – FIFO, LIFO, HIFO, SAM, WAM

Market price

Base Stock method

Standard price method.

UNIT –III

MATERIALS COST

BPZ5A/BPG5B - COST ACCOUNTING 23

TM

Introduction to Materials

Material costs are the costs of acquiring of material resources necessary for

business.

Raw materials and semi-finished products costs. The cost of

acquiring the necessary raw materials and semi-finished products belongs

to this group. This group of material costs is often the largest.

Fuel and energy costs. Acquisition costs of gasoline, machine oil, gas,

solid fuel, electricity, heat belong to this group.

Packaging costs. Acquisition costs of various containers (boxes, bales,

boxes) belong to these costs.

Spare parts costs. Expenses of spare parts used to repair equipment,

machinery or vehicles.

Building materials costs. The cost of building materials arise when the

company is building new facilities or making renovation of existing facilities.

Other material cost. All material costs which are not included in the

above groups related to other expenses. It may be, for example, waste

production or other costs.

MATERIALS COST

BPZ5A/BPG5B - COST ACCOUNTING 24

TM

http://download.nos.org/srsec320newE/320EL28a.pdf

MATERIAL PROCUREMENT SYSTEM

BPZ5A/BPG5B - COST ACCOUNTING 25

TM

ECONOMIC ORDERING QUANTITY

(EOQ)

The Economic Order Quantity (EOQ) is the number of units that a

company should add to inventory with each order to minimize the total

costs of inventory—such as holding costs, order costs, and shortage

costs.

FORMULA FOR EOQ

BPZ5A/BPG5B - COST ACCOUNTING 26

TM

ECONOMIC ORDERING QUANTITY (EOQ)

1BPZ5A/BPG5B - COST ACCOUNTING 27

TM

Stock level refers to the different levels of stock which are required

for an efficient and effective control of materials and to avoid over

and under-stocking of materials. The purpose of materials control is

to maintain the sock of raw materials as low as possible and at the

same time they may be available as and when required. To avoid

over and under-stocking, the storekeeper must fix the inventory

level, which is also known as a demand and supply method of

stock control. In a scientific system of inventory control the

following levels of materials are fixed.

1. Re-order Level

2. Minimum Level Or Safety Level

3. Maximum Level

4. Average stock Level

5.. Danger Level

CONCEPT AND MEANING OF STOCK

LEVEL

BPZ5A/BPG5B - COST ACCOUNTING 28

TM

PURPOSE OF STOCK

LEVEL

BPZ5A/BPG5B - COST ACCOUNTING 29

TM

Maximum Level of Stock = (Reorder Level + Reorder Quantity) –

(Minimum rate of consumption x Minimum

reorder period)

Minimum level of stock = Reorder level – (Average rate of consumption x

Average reorder period)

Reorder level or Ordering level = Maximum rate of consumption ×

Maximum reorder period

Average Stock level = (Maximum stock level + Minimum stock level) /2

or

Minimum Stock level + 14 Reorder Quantity

Danger level = Minimum rate of consumption × Emergency delivery time

BPZ5A/BPG5B - COST ACCOUNTING 30

TM

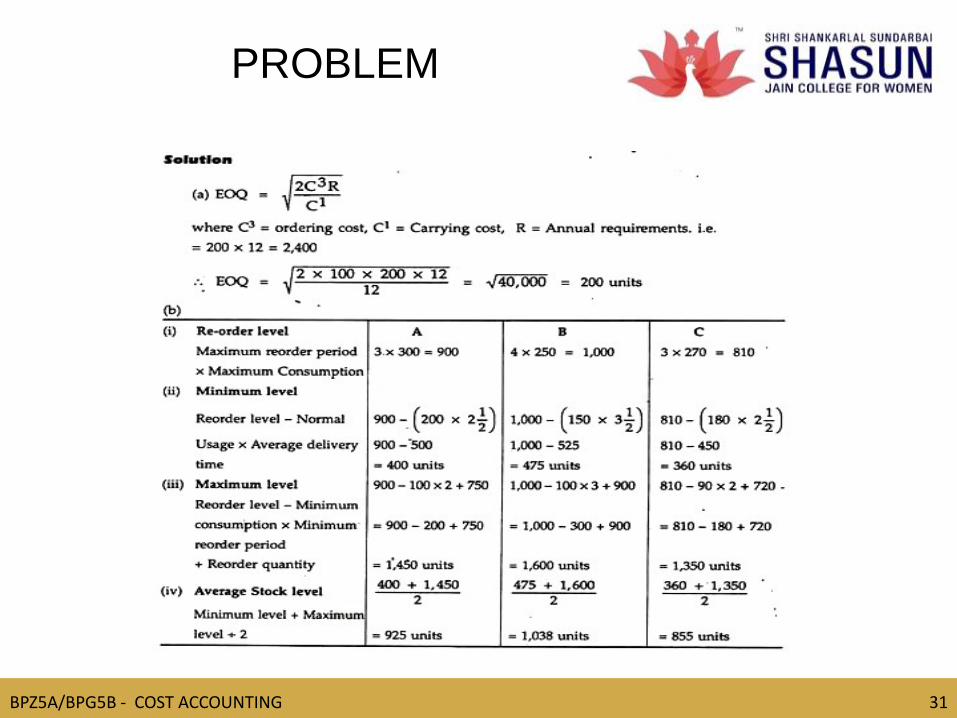

PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 31

TM

To learn more problems click the following link

http://www.zeepedia.com/read.php?control_over_material_order_le

vel_maximum_stock_level_danger_level_cost_and_management_

accounting&b=42&c=8

https://youtu.be/LS68An0PHBQ

https://youtu.be/hawrBU2WVA4

https://youtu.be/1U7H0k1yKes

http://download.nos.org/srsec320newE/320EL30a.pdf

BPZ5A/BPG5B - COST ACCOUNTING 32

TM

FIFO - FIRST IN FIRST OUT

LIFO - LAST IN FIRST OUT

HIFO - HIGHEST IN FIRST OUT

SAM -SIMPLE AVERAGE METHOD

WAM - WEIGHTED AVERAGE METHOD

BASE STOCK

SPECIFIC PRICE METHOD

METHOS OF PRICING OF

MATERIAL ISSUES

BPZ5A/BPG5B - COST ACCOUNTING 33

TM

FIFO Vs LIFO

BPZ5A/BPG5B - COST ACCOUNTING 34

TM

FIFO PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 35

TM

LIFO PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 36

TM

37

WAM PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING

TM

SPECIFIC PRICE METHOD PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 38

TM

SIMPLE AVERAGE PRICE METHOD

PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 39

TM

BASE STOCK METHOD

USING FIFO-PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 40

TM

BASE STOCK METHOD

USING LIFO-PROBLEM

BPZ5A/BPG5B - COST ACCOUNTING 41

TM

WORKOUT PROBLEMS WITH THE HELP OF FOLLOWING LINK

https://youtu.be/3X2PyCLpfFw

https://youtu.be/0YLHjA_OePA

https://youtu.be/slFqL86q3EA

EXTRA PROBLEMS

BPZ5A/BPG5B - COST ACCOUNTING 42

TM

Syllabus

Labour cost

Computation and control

Time keeping

Methods of wage payment

Time rate and Piece rate system

Payroll procedures

Idle time and overtime wage calculation

Labour Turnover.

UNIT -IV

LABOUR COST

BPZ5A/BPG5B - COST ACCOUNTING 43

TM

Labour cost - Meaning

It is classified as direct and indirect. They form the labour cost which in turn

forms a significant percentage of the total cost of production in a

manufacturing or service organization. Minimizing costs does not mean

reducing cost but means getting optimal and efficient productivity from the

employees.

Purposes of Labour Cost

• To calculate the correct gross and net wages for each employee.

• For financial accounting purposes.

• For management accounting purposes (i.e. stock valuation)

• Decision making and control purposes

Elements of Labour Cost.

• Basic Wages.

• Overtime premium

• Bonus payment

• Idle time

• Labour turnover

LABOUR COST

BPZ5A/BPG5B - COST ACCOUNTING 44

TM

CLASSIFICATION OF LABOUR COST

BPZ5A/BPG5B - COST ACCOUNTING 45

TMDIFFERENCE BETWEEN

DIRECT & INDIRECT

LABOUR COST

BPZ5A/BPG5B - COST ACCOUNTING 46

TM

Time Rate System

Wages = No. of hours worked x Rate per hour

Piece Rate System

Wages = Rate per unit x No. of units produced.

Incentive Plans

Straight Piece Rate Method Flat Time Rate Method

Guaranteed Day Work Taylor Differential Piece Rate

Rowan Premium Bonus Plan Halsey Premium Bonus Plan

Group Incentive Schemes Merrick Multiple Piece Rate

Gantt Task Bonus System Bedaux Point System

Emerson Plan Barth Premium System

REMUNERATION METHODS

BPZ5A/BPG5B - COST ACCOUNTING 47

TMMETHODS OF

RENUMERATION

BPZ5A/BPG5B - COST ACCOUNTING 48

TM

LABOUR TURNOVER

MEANING - A measure of the proportion of people leaving relative to the

average number of people employed over a period of time. This rate

should be kept as low as possible. Management might wish to monitor

labour turnover so that control.

Causes of Labour Turnover

Avoidable Unavoidable

i) Poor remuneration. i) Illness, death.

ii) Lack of training opportunities ii) Retirement

iii) Lack of promotion prospects. iii) Relocation, redeployment

iv) Poor working conditions. iv) Family matters.

v) Bullying in work place (Harassment).

LABOUR TURNOVER

BPZ5A/BPG5B - COST ACCOUNTING 49

TM

1. Calculating Labour Turnover by Separation Method

= No. of workers left or separated during a period /

Average number of workers on role during that period x 100

Average No. of. Workers = (No. of workers at the beginning of the

period + No. of workers at the end of the period) / 2

2. Calculating Labour Turnover by Replacement Method

= No. of workers replaced during a period / Average number of

workers on role during that period x 100

3. Calculating Labour Turnover by Flux Method

= (No. of workers separated in a period + No. of workers replaced in

the same period) / Average number of workers on role during that

period x100

METHODS OF CALCULATING

LABOUR TURNOVER

BPZ5A/BPG5B - COST ACCOUNTING 50

TM

To workout problems refer the following link

https://www.slideshare.net/sumitverma48/remuneration-method

https://www.slideshare.net/visavadiya/incentive-11967459

EXTRA PROBLEMS

BPZ5A/BPG5B - COST ACCOUNTING 51

TM

Syllabus

Overheads

Classification

Allocation Apportionment and Absorption.

Accounting and control of overheads

Manufacturing, Administration, Selling and Distribution (Primary

and Secondary Distribution )

Machine Hour Rate.

UNIT –V OVERHEADS

1BPZ5A/BPG5B - COST ACCOUNTING 52

TM

Meaning

Overhead costs, often referred to as

overhead or operating expenses, refer

to those expenses associated with

running a business that can‘t be linked

to creating or producing a product or

service.

Types

Overhead costs can be broken down

into three types:

Fixed

Variable

Semi-variable

UNIT –V

OVERHEADS

BPZ5A/BPG5B - COST ACCOUNTING 53

TM

1.Overhead Collection - Overhead is said to be collected when it is

incurred

2. Overhead Classification - This is the logical grouping of overhead into

the major activities undertaken by a business such as production, selling,

distribution and administration.

3. Overhead Codification - This refers to the use codes for the

identification of overhead costs of different kinds

4. Overhead Allocation - This is charging of whole item of overhead to a

single cost centre

5. Overhead Apportionment - This is the charging of proportions of

overhead to different cost centres using fair and equitable bases.

6. Overhead Absorption - This is the charging of overhead to cost units

using carefully calculated predetermined overhead rates

OVERHEAD ANALYSIS CAN BE

DIVIDED INTO SIX STAGES

BPZ5A/BPG5B - COST ACCOUNTING 54

TM

Over absorption occurs when the overhead absorbed is greater than the

actual overhead incurred. Over absorbed overheads represent gains and

are therefore credited to the profit and loss account.

Under absorption occurs when actual overhead cost incurred is greater

than the overhead absorbed. Under-absorbed overhead represents a

loss and is therefore debited to the profit and loss account.

OVER ABSORPTION AND UNDER

ABSORPTION OF OVERHEAD

BPZ5A/BPG5B - COST ACCOUNTING 55

TM

This is the final stage of the overhead analysis process where the

overhead of the production departments are charged to the final product.

The following is the general formula for calculating overhead absorption

rate. Activity level maybe measured using any of the following

Cost basis

Production hours

Output

Overhead absorption rates are based on budgeted overhead rather than

actual overhead

OVERHEAD ABSORPTION

BPZ5A/BPG5B - COST ACCOUNTING 56

TM

Primary Distribution is the allocation or appointment of different items of

overhead to both production and service departments on suitable basis.

There is no partiality between production and service department in

making primary distribution.

IMPORTANT POINTS SHOULD BE KEPT IN MIND

The basis for allocation and apportionment should be

equitable and practicable.

Charges are to be made to different departments in relation to

benefits received.

The method and basis for allocation and apportionment should

not be time consuming and costly

PRIMARY DISTRIBUTION OF OVERHEAD

BPZ5A/BPG5B - COST ACCOUNTING 57

TMOVERHEADS-BASES OF

APPORTIONMENT

Bases of Apportionment Overhead Cost

1Cost or value of asset

Depreciation, insurance, repairs and

maintenance, etc.

2Floor space occupied

Building depreciation, insurance and

repairs, rent and rates, electricity,

cleaning cost,

3Number of employees

Canteen, personnel administration,

welfare, supervision, etc.

Production or working hours Working hours affect almost all types

5Number of light bulbs Electricity

6.Metre reading Electricity, heating, air conditioning

7.Machine capacity or HP Electrical power

8.Number of requisitions Stores costs

BPZ5A/BPG5B - COST ACCOUNTING 58

TM

OVERHEADS CLASSIFICATION

1BPZ5A/BPG5B - COST ACCOUNTING 59

TM

PRIMARY DISTRIBUTION

OF OVERHEADS

BPZ5A/BPG5B - COST ACCOUNTING 60

TM

SECONDARY DISTRIBUTION

OF OVERHEADS

BPZ5A/BPG5B - COST ACCOUNTING 61

TMSECONDARY

APPORTIONMENT

SECONDARY APPORTIONMENT

It reapportions service department overhead to production

departments. The objective of this stage is to ensure that only

production departments bear all overhead costs, and which will

eventually be charged to products. This is because while there is a

direct link between the product produced and the production

departments, there is no such link between the products and service

departments. The absence of a direct link between service cost centres

and products will make it difficult to charge service cost centre

overheads to products.

SERVICE DEPARTMENTS

The departments such as canteen, administration, stores,

maintenance, etc that do not take direct part in the production process.

They provide support work for the production departments

BPZ5A/BPG5B - COST ACCOUNTING 62

TM

SECONDARY DISTRIBUTION OF

OVERHEADS

BPZ5A/BPG5B - COST ACCOUNTING 63

TM

Machine hour rate is a rational method for absorption of factory

overhead. The factory overhead costs are allocated to a machine or a

group of machines doing the same type of job and the cost per hour of

the machine is ascertained dividing the total allocated overhead costs to

the machine by number of hours the machine worked during the same

period of time for which the costs have been considered.

MACHINE HOUR RATE

BPZ5A/BPG5B - COST ACCOUNTING 64

TM

CALCULATION OF MACHINE HOUR RATE

65BPZ5A/BPG5B - COST ACCOUNTING

TM

To workout more problems click the link

https://youtu.be/i8iFBbWxRBc

https://youtu.be/gvQjzHRRT24

https://youtu.be/TBImiYd1Jv0

https://youtu.be/Lg1wFA8UDSQ

https://www.slideshare.net/yusufswt/machine-hour-rate-

method

EXTRA PROBLEMS

166BPZ5A/BPG5B - COST ACCOUNTING