Embed Size (px)

Citation preview

Borrowing Basics 1

Borrowing Basics 2

Purpose

Borrowing Basics:

• Describes how credit works and the types of credit available.

• Helps you determine if you are ready to apply for credit.

Borrowing Basics 3

Objectives

By the end of this course, you will be able to:

• Define credit.

• Explain why credit is important.

• Distinguish between secured and unsecured loans.

• Identify three types of loans.

Borrowing Basics 4

Objectives (Continued)

• Identify the costs associated with getting a loan.

• Explain why it is important to be wary of rent-to-own, pay-day loan, and refund anticipation services.

• Determine if you are ready to apply for credit.

Borrowing Basics 5

Credit

• Credit is money you borrow to pay for things.

• It is also called a loan.

• “Good” credit means making payments on time.

• “Bad” credit means it will be harder to borrow in the future.

Borrowing Basics 6

Why Credit Is Important

• It can be useful in emergencies.

• It’s more convenient than carrying cash.

• It lets you make large purchases.

• It can affect your ability to get employment, housing, and insurance.

Borrowing Basics 7

Collateral

Property or another asset you promise to give to the bank if you can’t repay your loan.

Borrowing Basics 8

Collateral Items

Car Property

Borrowing Basics 9

Types of Loans

• Consumer installment loans

• Credit cards

• Home loans

Borrowing Basics 10

Consumer Installment Loan

A loan used to pay for personal expenses:

• Automobile

• Computer

• Furniture

• College tuition

Borrowing Basics 11

Credit Cards

Give you the ongoing ability to borrow money for:

• Household,

• Family, and

• Personal needs.

Borrowing Basics 12

Home Loans

• Home purchase loans

• Home refinance loans

• Home equity loans

Borrowing Basics 13

Borrowing Money Responsibly

• Would you use credit to pay overdue bills?

• Would you use credit to make a purchase even if you could pay cash?

• Would you use credit if you really wanted something but could not afford the monthly payment?

Borrowing Basics 14

The Cost of Credit

• Fees

• Interest

Borrowing Basics 15

Fees

• Annual maintenance fees

• Service charges

• Late fees

Borrowing Basics 16

Interest

The money financial institutions charge for letting you use their money.

The rate of interest is either:

• Fixed

• Variable

Borrowing Basics 17

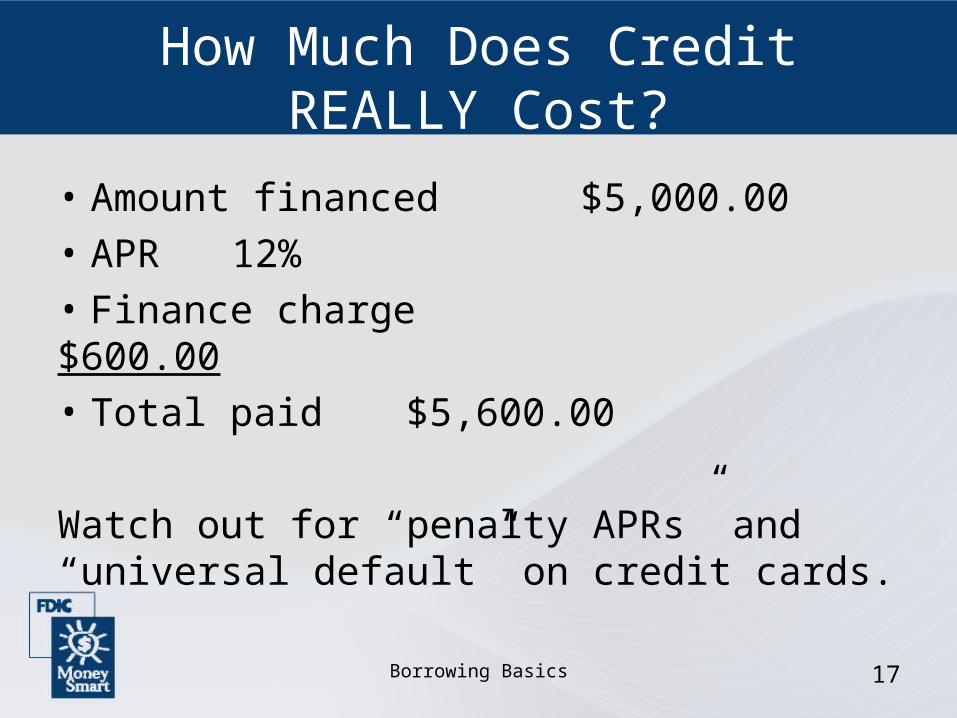

How Much Does Credit REALLY Cost?

• Amount financed $5,000.00

• APR 12%

• Finance charge $600.00

• Total paid $5,600.00

Watch out for “penalty APRs” and “universal default” on credit cards.

Borrowing Basics 18

The True Cost of Alternative Financial Services

• Rent-to-own services

• Pay-day loan services

• Refund anticipation services

Borrowing Basics 19

Rent-to-Own Services

• You use the item by making monthly or weekly payments.

• The store owns the item until you make your final payment.

• Using rent-to-own services is more expensive than getting a consumer installment loan.

Borrowing Basics 20

Pay-Day Loans

Loans that:• Are made for a fee to people who need

money right away.• Are paid back with the borrower’s next

paycheck.• Are renewed for an additional fee if not

paid off in the agreed-on time period.• Should be used only for emergencies.

Borrowing Basics 21

Refund Anticipation Loans

• These short-term loans are secured by your income tax refund.

• The money for the loans comes from a bank or finance company.

• They are more costly than you might think.

Borrowing Basics 22

The “Four Cs” of Credit Decision Making

• Capacity

• Capital

• Character

• Collateral