Embed Size (px)

Citation preview

Mater Engineering, Ltd/ Pinchot Institute

1Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Public Timber Sales and Sustainability

Who Buys; Who Benefits; and Why CROP is a Vital Key

Presented byCatherine M. Mater

President—Mater EngineeringSenior Fellow – The Pinchot Institute for Conservation

Corvallis, Oregon; Washington, DCTel: 541-753-7335 Fx: 541-752-2952

E-mail: [email protected]

Mater Engineering, Ltd/ Pinchot Institute

2Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Since we’re in Denver …

Let’s meditate on new protocol to relieve stress regarding supply issues.

Mater Engineering, Ltd/ Pinchot Institute

3Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

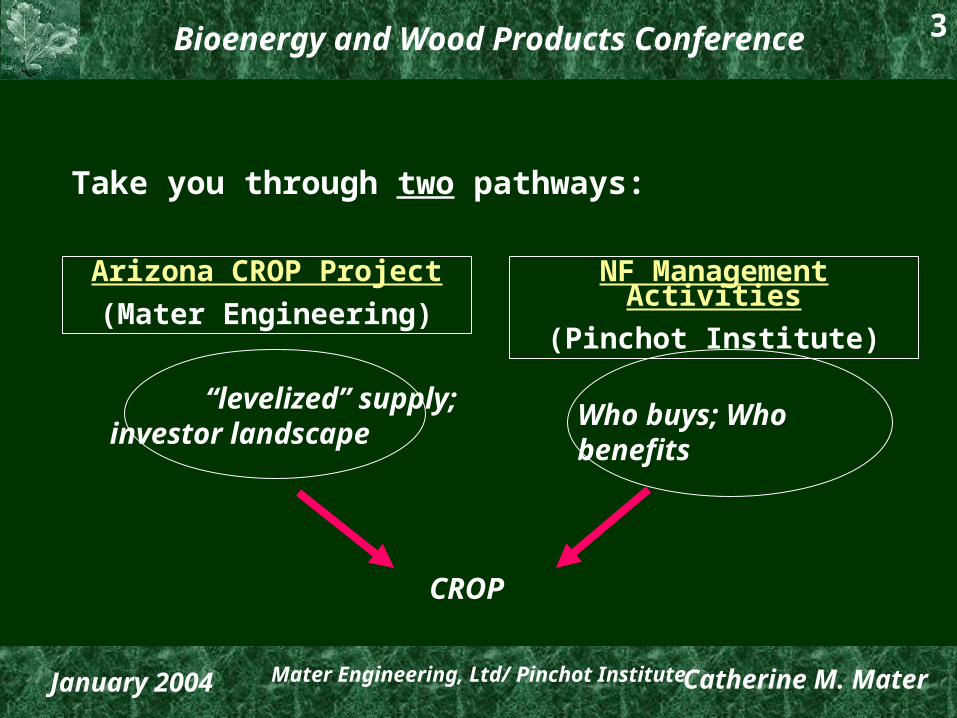

Take you through two pathways:

Arizona CROP Project

(Mater Engineering)

“levelized” supply; investor landscape

NF Management Activities

(Pinchot Institute)

Who buys; Who benefits

CROP

Mater Engineering, Ltd/ Pinchot Institute

4Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

. . . where and why it all began

To explain “investor landscape”, “levelized” and “CROP”, you have to know . . .

Mater Engineering, Ltd/ Pinchot Institute

5Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Grand Canyon Trust

Greater Forests Flagstaff Partnership

Arizona

Mater Engineering, Ltd/ Pinchot Institute

6Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Foundations of the Partnership

Restore natural ecosystem functions within Flagstaff Urban Interface.

Reduce catastrophic wildfire risk.

Research, test, and demonstrate key ecological, economical (ie wood utilization), and social dimensions of restoration.

Mater Engineering, Ltd/ Pinchot Institute

7Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

For economics –

•Technology should not drive the wood flow.

•Restoration/stewardship practices should define the technology choices for investment

reverse the formula!!

Mater Engineering, Ltd/ Pinchot Institute

8Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Timber Volume Sold by Diameter and YearA-S, Coconino, Kaibab (Williams RD)

Small logs sold

Large logs sold

19891990

19911992

19931994

020406080

100120140160180

Small logs sold

020406080

100120140160180

mm

bf

Mater Engineering, Ltd/ Pinchot Institute

9Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

1995 1996 1997 1998 1999 2000 2001 2002

Harvested

Off ered

0

0

10

20

30

40

50

60

70

80

90

100

mm

bf

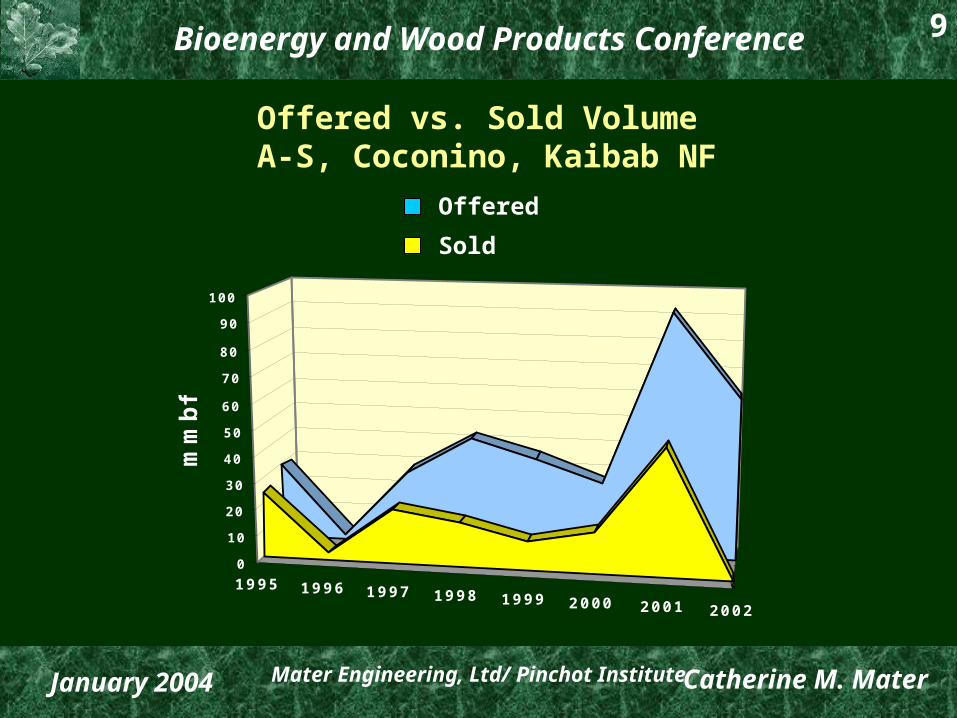

Offered vs. Sold Volume A-S, Coconino, Kaibab NF

Offered

Sold

Mater Engineering, Ltd/ Pinchot Institute

10Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Flagstaff

~200 miles

Investor Landscape

Mater Engineering, Ltd/ Pinchot Institute

11Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

0

2

4

6

8

10

12

14

16

18

20

95 96 97 98 99 00 01 02

Mormon Lake

Offered

Sold

0

2

4

6

8

10

12

95 96 97 98 99 00 01 02

Blue Ridge

0

2

4

6

8

10

12

95 96 97 98 99 00 01 02

Williams

0

2

4

6

8

10

12

14

16

18

20

95 96 97 98 99 00 01 02

Peaks

0

2

4

6

8

10

12

95 96 97 98 99 00 01 02

Long Valley

Coconino and Kaibab Timber Offering by Ranger District 1995 - 2002

Stable

Unstable

Mater Engineering, Ltd/ Pinchot Institute

12Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

0 2 4 6 8 10

12 14 16 18

Unstable

Mater Engineering, Ltd/ Pinchot Institute

13Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

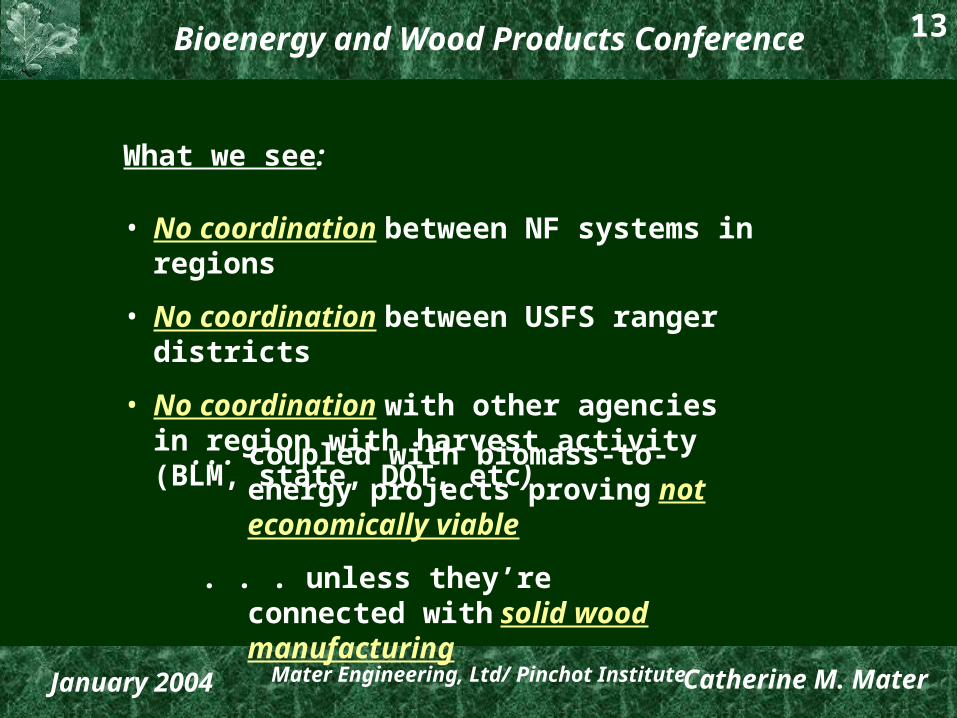

What we see:

• No coordination between NF systems in regions

• No coordination between USFS ranger districts

• No coordination with other agencies in region with harvest activity (BLM, state, DOT, etc)

. . . coupled with biomass-to-energy projects proving not economically viable

. . . unless they’re connected with solid wood manufacturing

Mater Engineering, Ltd/ Pinchot Institute

14Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

What investors see:

Erratic supply at best; no level playing field

Uncertainty where or when supply will come from in an investment landscape (~200 mile radius)

Little information on resource characteristics to be supplied

No investor risk mitigation efforts within the investor landscape (agency coordination targeting risk factors)

Mater Engineering, Ltd/ Pinchot Institute

15Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

What to do with small logs (5”-12”) and biomass (< 5”) material.

How to invite new investment into the region.

Key Questions:

Mater Engineering, Ltd/ Pinchot Institute

16Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

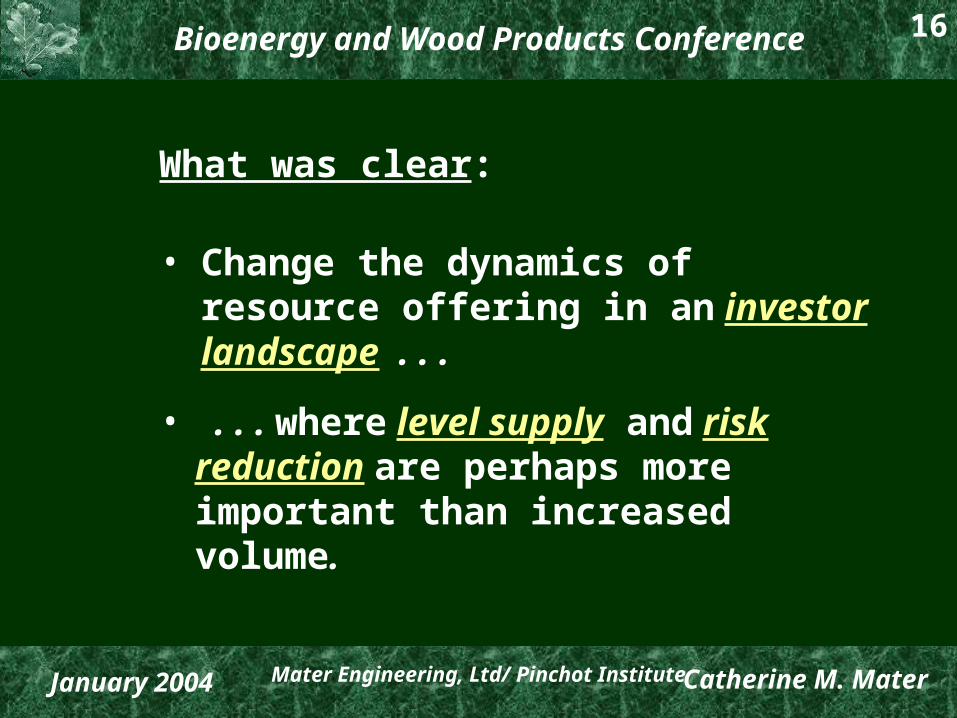

What was clear:

• Change the dynamics of resource offering in an investor landscape . . .

• . . . where level supply and risk reduction are perhaps more important than increased volume.

Mater Engineering, Ltd/ Pinchot Institute

17Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Solution . . . Seed the CROP

(Coordinated Resource Offering Protocol)

Mater Engineering, Ltd/ Pinchot Institute

18Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

CROP (coordinated resource offering protocol)

Nation’s first benchmark project in investor landscape coordination of projected resource offering:

Within agencies (ie RD’s within NF system)

Between agencies (USFS, BLM, state, Counties, Indian nations, etc.)

Mater Engineering, Ltd/ Pinchot Institute

19Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

CROP

Premise: • Focus is on “levelized” supply between key players, not necessarily adding more supply.

• “Levelized” effort must apply to volume, diameter, and species in locational context.

Mater Engineering, Ltd/ Pinchot Institute

20Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Why levelized?

Mater Engineering, Ltd/ Pinchot Institute

21Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

USDA FS Southern Research StationMater Engineering, Ltd

University of Oregon Ecosystem Workforce ProgramPinchot Institute for Conservation

Assessing Community Benefits from Land Management Activities on the National Forests

New research results soon to be released:

Mater Engineering, Ltd/ Pinchot Institute

22Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

1. Who buys Forest Service timber sales?

2. Who performs service contracts for the Forest Service?

Demographics, Consistency, Impacts

Three simple questions?

3. Who benefits?

Mater Engineering, Ltd/ Pinchot Institute

23Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Six National Forests Selected:

Willamette, Deschutes

Coconino

Arapaho-Roosevelt

Nantahala

Bitterroot

Mater Engineering, Ltd/ Pinchot Institute

24Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Methodology:

• 1998 – 2002 FY timber sale and service contract data analyzed.

• 71 timber sale purchasers interviewed 71; at least 50% response for each forest.

• 131 service contractors interviewed; 74% average response rate .

Mater Engineering, Ltd/ Pinchot Institute

25Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Contracts typically undertaken with local employees.

60-70% subcontract work; 65-70% goes to local companies.

70-74% primarily purchase supplies from local businesses.

Most work done by distant contractors.

90% “rarely” or “never” hire locals for contracts.

61% pay food and lodging; but lodging mostly described as camping.

Timber Service

Mater Engineering, Ltd/ Pinchot Institute

26Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

How do timber purchasers perceive FS programs? Do perceptions match performance?

Mater Engineering, Ltd/ Pinchot Institute

27Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Supply: total volume

78% of timber purchasers noted a decrease in total volume of timber sales offered by the forest service over the last five years.

Performance:

Only the Bitterroot & the Nantahala exhibited continuous declines in sales volume offered between 1998 - 2002. The Arapaho-Roosevelt, Willamette, Deschutes, and Coconino offered sales volumes in 2000 – 2002 which were close to or exceeded sales volumes offered in 1998 – 1999.

Mater Engineering, Ltd/ Pinchot Institute

28Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Lack of levelized, steady offerings may foster perceptions of diminishing sales volumes and may reduce ability to respond to timber sales offerings in absence of long-term harvest planning protocol.

Willamette Sales by Log S ize

0

20000

40000

60000

80000

100000

FY98 FY99 FY00 FY01 FY02

MB

F

Small logs, pulp

Sawlogs

Coconino Sales by Log Size

0

2000

4000

6000

8000

10000

12000

14000

FY98 FY99 FY00 FY01 FY02

Small logs, pulp

Sawlogs

Mater Engineering, Ltd/ Pinchot Institute

29Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Timber purchasers:

• 32% reduced wages or employee benefits

• 54% laid off employees

• 14% reduced work hours or shifts

• 23% reduced hiring of outside contractors

Mater Engineering, Ltd/ Pinchot Institute

30Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Meanwhile, back in Arizona, we began to examine how to . . .

Invite investment to the regions focused on small log processing.

Increase the value of resource sales.

Reduce the disparity between offered and sold.

Increase environmental support for long term removal activity.

Mater Engineering, Ltd/ Pinchot Institute

31Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

. . . but examine through a CROP lens

How much is proposed for removal (5-year period)?

How levelized is the removal flow over time?

Where and who will the volume come from?

Mater Engineering, Ltd/ Pinchot Institute

32Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

5 National Forests

AZ Trust Lands

ADOT

Department of Defense (Camp Navajo)

Indian Nations

Key players in Arizona investor landscape:

Mater Engineering, Ltd/ Pinchot Institute

33Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

11% Williams RD

6%

7% Morman Lake RD

11% Mogollon RD

20% Black Mesa RD

14% Lakeside RD

6% Alpine RD

18% Springerville RD

2% Pleasant Valley RD

2% Payson RD

2% Bradshaw RD

Williams RD - Kaibab NFAnnual Volume by DBH

0100020003000400050006000700080009000

2003 2004 2005 2006 2007

CC

F

vol 5-9"vol 9-12"vol 12+"

ROM #1: 2003-2007: 5” - 12+”

39% unstable supply

54% stable supply

11%

2%

7%

11%

20%

14%

20%

14%

18%

6%2%

2%

Mater Engineering, Ltd/ Pinchot Institute

34Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

5” – 9”: Where 60% or more of the NF volume will come from5-year (total: 340,677 ccf)

= 2003 (5%)

= 2004 (23%)

= 2005 (19%)

= 2006 (23%)

= 2007 (29%)

ROM #2

Mater Engineering, Ltd/ Pinchot Institute

35Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

9” – 12”: Where 60% or more of the NF volume will come from5-year (total: 188,207 ccf)

= 2003 (9%)

= 2004 (24%)

= 2005 (20%)

= 2006 (22%)

= 2007 (26%)

ROM #3

Mater Engineering, Ltd/ Pinchot Institute

36Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

12+”: Where 60% or more of the NF volume will come from5-year (total: 213,020 ccf)

= 2003 (28%)

= 2004 (19%)

= 2005 (17%)

= 2006 (17%)

= 2007 (20%)

ROM #4

Mater Engineering, Ltd/ Pinchot Institute

37Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Where 60% or more of the NF volume will come from over 5 years

= 5” – 9” (340,677 ccf total)

= 9” – 12” (188,207 ccf total)

= >12” (213,020 ccf total)

X

X

X

X

X

ROM #5

Mater Engineering, Ltd/ Pinchot Institute

38Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

<5" Projected 5-Year Biomass Removal Peaks RD (CCF)

00.10.20.30.40.50.60.70.80.9

1

2003 2004 2005 2006 2007

CC

F

None Projected

<5" Projected 5-Year Biomass Removal Pleasant Valley RD (CCF)

00.10.20.30.40.50.60.70.80.9

1

2003 2004 2005 2006 2007

CC

F

None Projected

<5" Projected 5-Year Biomass Removal Alpine RD (5,659.2 ccf)

0

500

1000

1500

20002500

3000

3500

4000

4500

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Bradshaw RD (300 ccf)

0

20

40

60

80

100

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Lakeside RD (10,010.4 ccf)

0

500

1000

1500

2000

2500

3000

3500

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Williams RD (1,500 ccf)

0100200300400500600700800

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Springerville RD (16,357.8 ccf)

0

1000

2000

3000

4000

5000

6000

2003 2004 2005 2006 2007

CC

F

<5" Projected Biomass Removal Black Mesa RD (14,211.6 ccf)

01000200030004000

5000600070008000

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Payson RD (800 ccf)

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Mogollon RD (11,600 ccf)

0

100

200

300

400

500

2003 2004 2005 2006 2007

CC

F

<5" Projected 5-Year Biomass Removal Morman Lake RD (14,211.6 ccf)

0

50

100

150

200

250

2003 2004 2005 2006 2007

CC

F

2003-2007: < 5” biomass 3% Williams RD 2% Morman Lake RD

3% Mogollon RD

28% Black Mesa

19% Lakeside RD

11% Alpine RD

32% Springerville RD 2% Payson RD

< 1% Bradshaw RD

None Projected

None Projected

51% stable supply39% unstable supply

ROM # 6

Mater Engineering, Ltd/ Pinchot Institute

39Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Biomass (<5): Where 60% or more of the NF volume will come from5-year (total: 51,440 ccf)

= 2003 (2%)

= 2004 (26%)

= 2005 (18%)

= 2006 (24%)

= 2007 (30%)

ROM #7

Mater Engineering, Ltd/ Pinchot Institute

40Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Meanwhile, because of NFP mandates and the N. AZ project, similar efforts unfolding in Oregon:

Central Oregon (Bend -Redmond

South Central (Hines)

Oregon

Mater Engineering, Ltd/ Pinchot Institute

41Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Oregon investor landscapes include:

Central Oregon:

• 7 National forests

• State lands

• ODOT

• BLM

• Indian nations

• Counties

South-Central Oregon:

• 5 National forests

• ODOT

• BLM

• Counties

Mater Engineering, Ltd/ Pinchot Institute

42Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

O c h o c o N a t i o n a l F o r e s t

Ochoco - Paulina Ranger District

0200400600800

1,0001,2001,4001,600

Offered Sold Offered Sold Offered Sold

12" & Greater 4" - 11" <4"

mbf

2000

2001

2002

Ochoco NF:

Offered vs sold for ’00-’02

Same picture as Arizona

Unstable

Mater Engineering, Ltd/ Pinchot Institute

43Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

OR CROP working circle:100-mile radius

95%

03-07 : Lodgepole Pine

• Deschutes NF: L. Pine

39%

52%

03-07 : Juniper • BLM: Juniper

Mater Engineering, Ltd/ Pinchot Institute

44Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Marketing plan for new restoration-based high value-add technologies

CROP it . . . And they will come!

Mater Engineering, Ltd/ Pinchot Institute

45Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Mater Engineering, Ltd/ Pinchot Institute

46Bioenergy and Wood Products Conference

Catherine M. MaterJanuary 2004

Potential for CROP as a new supply/investment tool?

We think excellent potential . . .

. . . Just may have to view things from a different

angle!

![Solennità ta' l-l '1@lf!iS[]l)santamarija.com/.../05/Solennitta-ta-l...sema-Patruna-ta-l-Imqabba.pdf · Mater castissima Mater inviolata Mater intemerata Mater amabi/is Mater admirabi/is](https://img.dokumen.tips/doc/110x75/5ac828de7f8b9a40728c7e15/solennit-ta-l-l-1lfisl-castissima-mater-inviolata-mater-intemerata-mater.jpg)

![The Indianapolis times. (Indianapolis [Ind.]) 1933-05-05 [p ] · 2019. 12. 3. · $2 a week. Mrs. CorneliaBryce Pinchot, wife of Governor Pinchot, inher private investigation of young](https://img.dokumen.tips/doc/110x75/5febfc44c8d3eb365c1c5e37/the-indianapolis-times-indianapolis-ind-1933-05-05-p-2019-12-3-2.jpg)