Embed Size (px)

Citation preview

LIVRO VERDE DO ETANOL

1

LIVRO VERDE DO ETANOL

1

Bio based Chemicals in Brazil

Market achievements and opportunities

Brazilian Development Bank – BNDES

LIVRO VERDE DO ETANOL

2

LIVRO VERDE DO ETANOL Agenda

1. BNDES introduction

2. Recent Programs in Brazil and its results

3. New Finds: Brazilian Chemical Industry Diversification Study

LIVRO VERDE DO ETANOL

3

LIVRO VERDE DO ETANOL BNDES Highlights

Founded on June 20th, 1952.

100% state-owned company under private law.

Key instrument for implementation of Federal Government’s

industrial and infrastructure policies.

Main provider of long-term financing in Brazil.

Emphasis on financing investment projects.

Support to micro, small and medium-sized companies.

Support to Export and Internationalization of Brazilian companies.

LIVRO VERDE DO ETANOL

4

LIVRO VERDE DO ETANOL

Infrastructure

Heavy Industry – Consumer Goods

Technological Development

BNDES Time Line

Imports Substitution

Energy

Agribusiness

Exports

Privatization Program

Urban and Social Development

Social Inclusion

Innovation

Sustainability

Small Business

50’s 60’s 70’s 80’s 90’s 00’s Today

LIVRO VERDE DO ETANOL

5

LIVRO VERDE DO ETANOL

Innovation Investment Financing Infrastructure

Aquisition of Machinery and

Equipment Exports Capital Markets

Aquisition of Capital

goods for Small and

Medium Companies

BNDES Scope of Action

LIVRO VERDE DO ETANOL

6

LIVRO VERDE DO ETANOL BNDES vs. Multilateral Banks

US$ million BNDES IADB World Bank China DB

31/12/2012 30/06/2012 30/06/2012 31/12/2011

Total Assets 350.128 95.522 338.178 993.217

Shareholders´ Equity 25.529 20.194 36.685 70.739

Net Income 4.004 189 783 7.244

Loan Disbursements 78.712 2.046 19.777 N/D

Capitalization (%) 7.3 21.1 10.8 7.1

ROA (%) 18.8 0.2 0.3 0.9

ROE (%) 1.3 0.9 2.1 11.5

IADB = Inter-American Development Bank World Bank China DB = China Development Bank

LIVRO VERDE DO ETANOL

8

LIVRO VERDE DO ETANOL

8

BNDES’ priority: Innovation Policy and instruments to support all companies

NON-REIMBURSABLE

INVESTMENT

EQUITY

FIXED / VARIABLE

INCOME

Closed and Open Mutual Funds

Direct Participation (stake in the company)

Criatec Program (Seed Money)

BNDES INNOVATION Credit Line

FUNTEC

Technological Fund

Projects, including Research,

development and innovation in areas of

national interest

PROSOFT, PROFARMA, PROTVD, PAISS, PRO-Aeronautical, PRO-Engineering, BNDES O&G, INOVA Programs SECTORIAL Programs

PRODUCTS for

SMEs

BNDES Card

BNDES AUTOMATIC

LIVRO VERDE DO ETANOL

9

LIVRO VERDE DO ETANOL Agenda

1. BNDES introduction

2. Recent Programs in Brazil and its results

3. New Finds: Brazilian Chemical Industry Diversification Study

LIVRO VERDE DO ETANOL

10

LIVRO VERDE DO ETANOL Well established sugarcane industry

Brazil has more than 400 sugarcane mills that can crush around 700 million tons per year. Besides that, due to the lack of financial/technological assets, the majority still processing only the

sugarcane juice…

… which represents a great opportunity for those who are able to develop/adapt new technologies to be integrated to these plants, generating synergies and cost reductions for both 1st and 2nd gen ethanol process.

LIVRO VERDE DO ETANOL

11

LIVRO VERDE DO ETANOL Land availability

By improving the low yield of cattle production it will be possible to free large

amount of land for other purposes. Brazilian federal agricultural zoning

considered up to 64 Mha able to produce sugarcane w/o irrigation.

LIVRO VERDE DO ETANOL

12

LIVRO VERDE DO ETANOL Lowest carbon footprint

6.7

9.3

11

2.3

Sugar cane Brazil-bottom

Sugar cane Brazil-average

Sugar cane Brazil-top

Corn USA average

Energy efficiency - BOE output/ BOE input

Source: USDA apud Villela Filho (2011) BOE = barrel of oil equivlent

Sugarcane biomass can provide all primary energy required in its own industrial

process and also generate a surplus that can be added to the power grid.

LIVRO VERDE DO ETANOL

15

LIVRO VERDE DO ETANOL

EUA:

- Renewable Fuel Standard (RFS) – EUA

- Programa de grants do Departamento de Energia (DOE)

Europa:

- European Commission Inniciatives (EU ETS, NER300,

etc.)

Brasil:

- PAISS

Public Policies and the technology run

3

LIVRO VERDE DO ETANOL

22

LIVRO VERDE DO ETANOL

22

PAISS - Results

LIVRO VERDE DO ETANOL

24

LIVRO VERDE DO ETANOL Commercial Projects – Industrial Biotech

BNDES Financing for Investment: > US$ 500 M (2011-2014)

• Braskem - Green PE 200 kt - 2011 - Triunfo/RS US$240M BNDES financing for pilot and commercial scale

• Amyris - Farnesene - 2013 - São Paulo US$ 35M BNDES financing for demo and commercial scale

• Solazyme - Specialty oils - 2014 - São Paulo

US$107M BNDES financing for commercial scale

• GranBio - Cellulosic ethanol - 2014 - Alagoas US$130M BNDES equity and financing

LIVRO VERDE DO ETANOL

25

LIVRO VERDE DO ETANOL Project Perspectives

BNDES Financing Forecast: > US$ 1 bi (2015-2017)

Announced projects:

• Solvay-Rhodia / Granbio - butanol

BNDES financing and grant (Funtec) for research

• DSM – Succinic acid from sugar cane - Grant (Funtec) from BNDES

• Elekeiroz / Coskata – butanol

• PHB – Demo plant

BNDES financing for demo plant

• Biobased chemicals research pipeline

Braskem/Solvay-Rodhia/DSM/Elekeiroz/Oxiteno/CTC – CTBE/Embrapa

BNDES and Finep financing and grants for research

LIVRO VERDE DO ETANOL

26

LIVRO VERDE DO ETANOL Agenda

1. BNDES introduction

2. Recent Programs in Brazil and its results

3. New Finds: Brazilian Chemical Industry Diversification Study

public reports at... www.bndes.gov.br google: “BNDES Química Diversificação”

LIVRO VERDE DO ETANOL

27

LIVRO VERDE DO ETANOL

27

Brazilian Chemical Industry - 2013

Imports Exports US$ billions FOB

Trade balance - Chemicals

Source: MDIC/Secex

LIVRO VERDE DO ETANOL

28

LIVRO VERDE DO ETANOL

28

Atract investments Diversify the industry Reduce trade balance’s shortage Design industrial policies that promote investments Post-study : execution focus Authors:

Study – main objectives

LIVRO VERDE DO ETANOL

29

LIVRO VERDE DO ETANOL

Prioritization and

validation S4

Report 7

(Final)

Drawing of development

policies

The study is at its final stage

Business models drawing

Economics detailing

Initial

Prioritization

of segments

Mapping and

Segmentation

Characterization of selected segments

Mapping and best practices

for development policies

S2

S1

1st July 13

9th Sept 13

May June July Aug Sept Oct Nov Dec Jan Feb Mar Apr May June July Aug Sept

SP

S Seminars SP Specialists Panel

Final

Prioritiz

ation of

Opportu

nities S3

Report 4 Report 3 Report 6 Report 5

16th

Sept

14

LIVRO VERDE DO ETANOL

30

LIVRO VERDE DO ETANOL 64 segments and a business perspective

Tar deriv.

Organics

Acrylic acid and deivati

Metacrylic acid and deriv.

Fatty acids and

deriv. Aromatics

Butadiene, isoprene and deriv.

Cellulose and

deriv.

Waxes and

paraffins

Copoly mers

Cumene and

deriv.

Elasto mers

Ethylene deriv.

Methane

deriv.

Ethylene oxide and

deriv..

Propene deriv.

Vinyl

deriv. Lubricants

Fine chemicals intermediaries

Polymers intermediaries

Special Polymers

Aramids Carbon fibers

Polycar-bonates

Polycetals

Special polyamides

High tenacity polyester

Polyether polyols and polyurethane

Politetra-metileno éter glicol

Resinas epóxidas

Polibutilene terephthalate

Catalysts and additives

Food additives Construction

chemicals Leather

chemicals Mining

chemicals

O&G Chemicals

Polymers additives

Catalysts Flavor and fragrances

Dyes, pigments and coatings

Syntetic dyes

Printing inks

Coating

Soaps, cleaning and cosmetics

Cleaning products

Cosmetics

Other

Explo-sives

Refrigerants

Reagents

Glues and sealants

Glues, adhesives

and sealants

Pesticides

Pesticides

Photo graphics

Photo graphics

Chain

Inorganics

Inorganic acids

Alumi num deriv.

Boron

deriv.

Chlorine and

Alkalis

Cobalt

deriv.

Phospho rus and deriv.

Industrial gases

Iodine and

deriv.

Radio active mat.

Nickel

deriv.

Titanium dioxide and

deriv.

Niobium deriv.

Sulfphates Rare earth

deriv. Uranium

Elemental carbon deriv.

Silicon deriv.

Note: Pharmaceuticals, fertilizers and commodity plastics resines (HDPE, PP, PVC and PET are out of the scope of the study.

Industrial intermediaries

Marke

t

LIVRO VERDE DO ETANOL

31

LIVRO VERDE DO ETANOL Market and production factors guided the selection of segments to deep dive

A multi-criteria analysis tool was used to ensure the robustness of the results

• Imports +Exports (US$)

- Average 08-12

• Production (US$)

- Average 07-11

• CAGR imports + exports (%)

• Unit Price (US$/kg)

-Average 08-12

• Trends in Demand

• Degree, current and future, of availability and cost

competitiveness of raw materials

• Degree of technological dominion and the potential

to develop or purchase it

• Availability of qualified labor

• Quality of available infrastructure

• Regulatory restrictions

• Necessity for investment

Dem

an

d C

ondit

ions

Fac

tors

of

Pro

du

ctio

n

Infra-

structure

CRITERIA

• Size

Capital

Legal

Environ. Labor

• Growth

• Value-added

• Technology

• Raw Materials

INDICATORS SOURCE Qu

antita

tive

Quali

tative

• Trends

• Aliceweb

• Consortium

• Validation from the school of chemistry

• Global Insight

• Macro tendencies

• Aliceweb

• Associations

• PIA

LIVRO VERDE DO ETANOL

32

LIVRO VERDE DO ETANOL

Segment

Market BR

( US$B,

2012)

Brazilian

Share

(%)

Global growth

(12-07)

Brazilian

Growth

(12-07)

Imports

(US$ M)

Exports

(US$ M)

Unit Price

(US$ /kg)

Cosmetics 41.8 9.7% 4.1% 12.4% 830 580 5.4

Defensives 9.7 20.5% 7.6% 16.1% 5,400 500 11.3

Animal feeding additives1 1.10 10.0% 3.7% 10.1% 458 310 2.5

Butadiene, Isoprene 1.95 5.7% 1.1% 3.2% 860 740 2.5

Flavors and fragrances 1.20 5.1% 3.3% 6.5% 295 317 5.2

Oilfield chemicals 0.71 3.6% 11.2% 24.6% 85 9 1.7

Surfactants 1.54 5.7% 3.0% 6.9% 315 185 3.0

Aromatics2 2.52 1.6% 3.8% 5.2% 1,154 0 1.2

Polyurethanes 1.50 3.5% 1.6% 5.8% 944 83 2.7

Cellulose derived products 0.33 1.3% 6.3% 1.1% 190 37 3.5

Lubricants 4.5 3.5% 1.0% 2.6% 1,127 209 2.4

Food additives* 0.65 3.0% 3.8% 4.1% 367 625 2.8

Oleo chemicals 0.66 2.8% 8.1% 23.2% 230 179 1.7

Carbon Fiber 0.10 9.4% 7.9% 107.4% 97 0 24.4

Mining chemicals 0.19 4.1% 2.3% 7.6% 93 8 2.2

Leather chemicals 0.38 8.1% 2.8% 3.7% 111 83 1.7

Silicon Derived Products 0.42 3.0% 3.7% 5.2% 190 536 2.5

Construction chemicals 0.17 1.7% 3.7% 5.0% 30 4 1.1

Polyamides 1.28 1.7% 1.9% -5.2% 509 14 3.4

Com

pet

itiv

en

ess

+

-

19 segments were considered highly attractive and were studied in more detail

LIVRO VERDE DO ETANOL

33

LIVRO VERDE DO ETANOL Main opportunities: relevant and growing local markets or local feedstock availability

33

DEMAND DRIVER

Strong local market

OIL PRODUCTION

CHEMICALS

COSMETICS CROP

PROTECTION

FEEDSTOCKS

Feedstocks available/ emerging technology

RENEWABLE

CHEMICALS

Potentially feedstock availability

OLEOCHEMICALS PETROCHEMICALS

CADEIAS A

JUSANTE

CADEIAS A

JUSANTE

Currently feedstock availability

FLAVORS AND

FRAGRANCES .

CHEMICALS

FROM PULP

FOOD ADDITIVES

LIVRO VERDE DO ETANOL

35

LIVRO VERDE DO ETANOL Sugarcane and maize represent ~60% of 1st generation carbohydrate feedstocks; Brazil owns ~ 30% of this total

* Other includes barley (133MT), sweet potatoes (105MT), sorghum (58MT) and yam (57MT) Source: FAOStat (2014) for 2011/2012 season

CARB. - 1ST GEN.

LIVRO VERDE DO ETANOL

36

LIVRO VERDE DO ETANOL In addition to being the most available culture, sugarcane is one of the most competitive feedstocks

Note: The fermentable weight corresponds to carbohydrates that are consumed in the fermentation Source: Nexant (2013), Next Generaton Biofeedstocks: Resources IS Renawables ; Südzucker (2014); Bayer. Landesanstalt Für Landwirtschaft (2014)

CARB. - 1ST GEN.

LIVRO VERDE DO ETANOL

37

LIVRO VERDE DO ETANOL

Source: FAO (2014), harvest 2011/2012; Nexant (2013), Next Generaton Biofeedstocks: Resources IS Renawables ; Bain / Gas Energy Analysis.

AGROIND. RESIDUE

Brazil is responsible for ~40% of the global production of sugarcane residues

LIVRO VERDE DO ETANOL

38

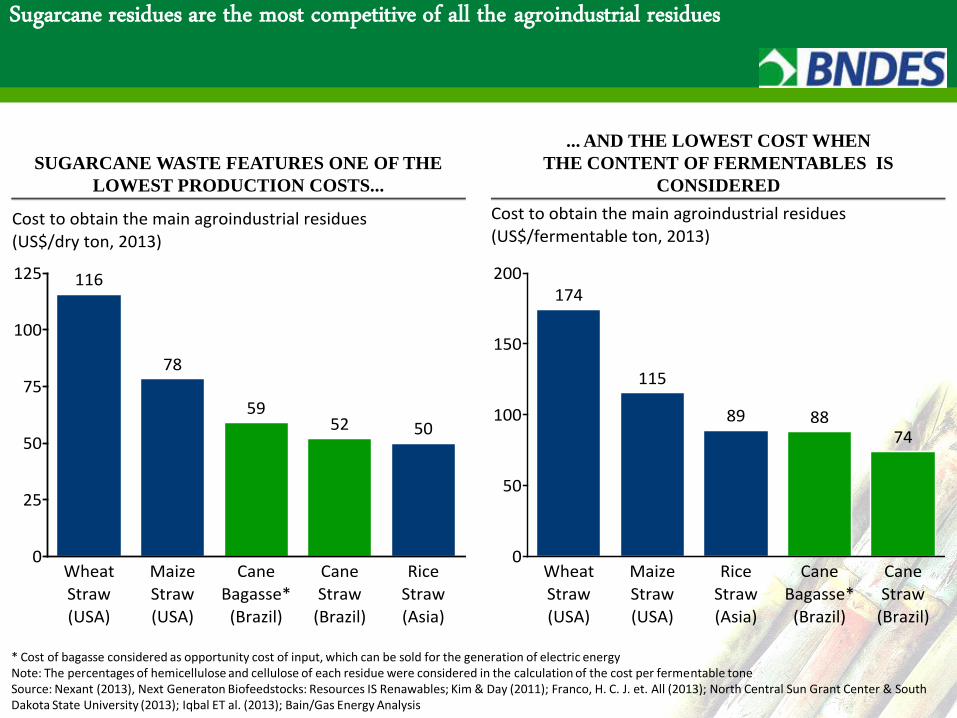

LIVRO VERDE DO ETANOL Sugarcane residues are the most competitive of all the agroindustrial residues

SUGARCANE WASTE FEATURES ONE OF THE

LOWEST PRODUCTION COSTS...

... AND THE LOWEST COST WHEN

THE CONTENT OF FERMENTABLES IS

CONSIDERED

* Cost of bagasse considered as opportunity cost of input, which can be sold for the generation of electric energy Note: The percentages of hemicellulose and cellulose of each residue were considered in the calculation of the cost per fermentable tone Source: Nexant (2013), Next Generaton Biofeedstocks: Resources IS Renawables; Kim & Day (2011); Franco, H. C. J. et. All (2013); North Central Sun Grant Center & South Dakota State University (2013); Iqbal ET al. (2013); Bain/Gas Energy Analysis

LIVRO VERDE DO ETANOL

39

LIVRO VERDE DO ETANOL Biofuels industry will allow evolution of the 2G sugar experience curve

Note: Use of ethanol by Braskem estimated by considering a stoichiometric yield of 54% for the installed capacity of 200 Ktpy Source: CONAB (2013); Braskem (2013); PECEGE/ESALQ (2012 e 2014); CTBE (2013); CTC (2013); Novacana (2014); expert interviews; Bain/Gas Energy analysis

Retrofit of

existing plant

can reduce

Capex

LIVRO VERDE DO ETANOL

40

LIVRO VERDE DO ETANOL 2nd biggest concentration of production capacity of chemicals from biomass is found in Brazil

*Includes projects with undefined location or with location in countries as Italy, India, Canada and others. Note: the data presented on the graph is related to projects that were publicly announced for renewable chemical classes 1 and 2, i.e. the alternative route based on biomass is emerging or in the beginning of business stage. Source: Nexant (2012), Bio-based Chemicals: Going Commercial; Green Chemicals Blog (2012-2014); Biofuels digest (2012-2014); websites of different companies (renewable and conventional chemicals); interviews with experts.

LIVRO VERDE DO ETANOL

41

LIVRO VERDE DO ETANOL Investments are shifting from biofuels to biochemicals

41

In Brazil: information asymmetry and shyness of the local agents (VC and biotech companies)

Source: Cleantech Group