Embed Size (px)

Citation preview

Bilfinger SE Company Presentation

October 2016

1. Bilfinger at a glance

2. Sale of Building and Facility

3. Industrial at a glance

4. Update on Power

5. Facts and Figures Q2 2016

6. Financial backup

Agenda

Bilfinger SE | Company Presentation | October 2016 page 2

▪ Multinational player with leading positions in attractive markets

▪ High-quality services provider and partner to our customers

▪ Strong customer base with long-term relationships

▪ Approx. 60% recurring business

▪ 2015: Output volume of € 5.0 billion, adjusted EBITA of € -23m

Bilfinger at a glance

Bilfinger SE | Company Presentation | October 2016 page 3

€ 5.0bn output volume

employees

recurring business thereof ~60%

40,000 Approx.

Leading European engineering and services group

Segment Industrial Power

Service Focus

Output volume 2015

Services for Process Industry

€ 3.7bn (76%)

Utilities

€ 1.3bn (24%)

Adj. EBITA 2015 / margin € 128m / 3.5% € -69m / -5.4%

Divisions Industrial Maintenance

Engineering Solutions

Insulation, Scaffolding and Painting

Oil and Gas

Power

Outlook 2016

Output volume

Adj. EBITA

Significant decrease to about € 3.1

billion

At prior-year level

Significant decrease to about € 1.0

billion

Significant improvement, but still

negative

Bilfinger SE | Company Presentation | October 2016 page 4

Germany

23%

Rest of

Europe

52%

America

17%

Asia

5%

Output volume

2016e

Africa

3%

Restructuring of administration raises transparency and strength

and improves our competitiveness

Restructuring of administration raises transparency and strength and

improves our competitiveness

page 5

Standardization of processes,

harmonization of IT systems

One-time expenses in the high

double digit million euro range

(over €50 million in investments

in IT)

Streamlining of Group

headquarters

Commitment to Mannheim

location

GROUP HEAD-

QUARTERS

SAVINGS

EFFECTS

INDUSTRIAL

Reduction in the number of divisions and

companies

Bundling of administrative tasks / expansion

of shared service centers to Europe

Establishment of lead companies in

selected countries

Annual savings of roughly €100

million from 2018 (initial effects

from 2017)

Discussions with social partners

already begun

Bilfinger SE | Company Presentation | October 2016

Program to enhance efficiency in administration

Optimize administrative processes, reduce costs

INVESTMENTS

IN THE FUTURE

1. Bilfinger at a glance

2. Sale of Building and Facility

3. Industrial at a glance

4. Update on Power

5. Facts and Figures Q2 2016

6. Financial backup

Agenda

Bilfinger SE | Company Presentation | October 2016 page 6

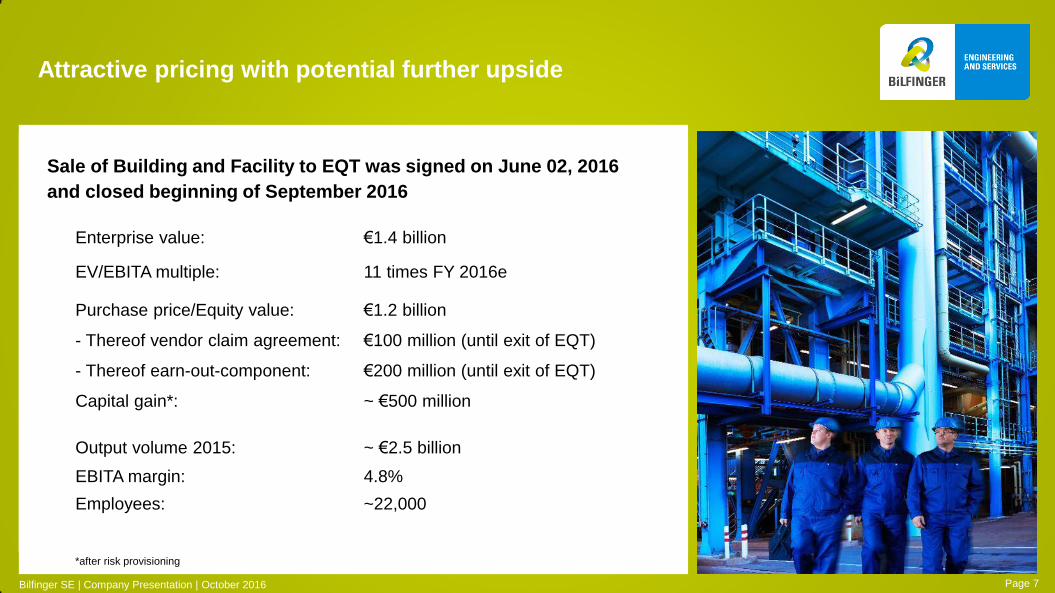

Attractive pricing with potential further upside

Bilfinger SE | Company Presentation | October 2016 Page 7

Sale of Building and Facility to EQT was signed on June 02, 2016

and closed beginning of September 2016

Enterprise value: €1.4 billion

EV/EBITA multiple: 11 times FY 2016e

Purchase price/Equity value: €1.2 billion

- Thereof vendor claim agreement: €100 million (until exit of EQT)

- Thereof earn-out-component: €200 million (until exit of EQT)

Capital gain*: ~ €500 million

Output volume 2015: ~ €2.5 billion

EBITA margin: 4.8%

Employees: ~22,000

*after risk provisioning

Considerations regarding allocation of funds

Strategic investments and acquisitions in Industrial business

Further strengthen the company’s capital structure

Sale of Building and Facility provides Bilfinger

with significant amount of funds

Bilfinger SE | Company Presentation | October 2016 Page 8

Growth

Additional resources to actively participate in ongoing market

consolidation and to invest in growth areas

Markets

Distinct customer base with stronger management focus

No restraints from ‘the other business‘

Perception

Clear identity and focused market approach strengthen Bilfinger brand

Management

Far-reaching harmonization of internal structures, e.g. IT

Faster decision making processes

Capital markets

Reduced complexity and increased comparability for investors

concentrating on specific businesses/market cycles

Pure play Industrial

opens attractive strategic opportunities

Bilfinger SE | Company Presentation | October 2016 Page 9

1. Bilfinger at a glance

2. Sale of Building and Facility

3. Industrial at a glance

4. Update on Power

5. Facts and Figures Q2 2016

6. Financial backup

Agenda

Bilfinger SE | Company Presentation | October 2016 page 10

2015: Output volume of € 3.65 billion, adjusted EBITA of € 128 million

Approx. 30,000 employees

Customer focus: Process Industry

i.e. chemicals, pharma, oil and gas, energy

Approx. 70% recurring business

Four divisions:

Industrial Maintenance

Engineering Solutions

Insulation, Scaffolding and Painting

Oil and Gas

Industrial at a glance

Bilfinger SE | Company Presentation | October 2016 Page 11

€ 3.65bn output volume

EBITA adjusted

employees

recurring business thereof ~70%

€128m

30,000 Approx.

Strong market position in Europe and strong potential

to expand in faster growing regions outside Europe

Number 1 industrial services provider in various markets in Europe

(German-speaking countries, Nordics, UK, Offshore North-Sea, BeNe, Central-Eastern

Europe)

Combination of engineering, construction and asset performance management

(comprises services striving to increase plant availability, extension of plant life time,

reducing maintenance costs) realized as project and recurring business

Robust business model proven by comparably stable margins in sometimes tough

environment (e.g. turmoil in oil markets)

Well-established broad customer base covering the entire process industry including

oil and gas, chemical, petrochemical, agrochemical, gas processing, biotech pharma,

pharmaceutical, food processing, pulp and paper, steel and aluminum production

Highly recognized safety and quality performance

Page 12 Bilfinger SE | Company Presentation | October 2016

Bilfinger helps its customers to optimize their asset performance

Plant Optimizatio

Installation /

Commissioning

Decommissioning

Design

DISMANTLING/

REMOVAL

CONSTRUCTION

CONSULTING &

ENGINEERING

INVEST PHASE

Engineering and Construction Services for new

assets

OPERATING PHASE

Industrial Services for existing assets

DIVESTMENT PHASE

MAINTENANCE SERVICES / TRADES

CONVERSION / MODERNIZATION /

EXTENSION

OPERATIONS

SERVICES

Asset Life

Cycle and

Service

Portfolio

Page 13 Bilfinger SE | Company Presentation | October 2016

Customers Medium term Long term

Imbalance between supply and demand on the raw

materials markets

Over-capacity among our customers

Regulation of the supply and demand situation

Reduction of over-capacities

Increasing demand with limited supply

(+ high break-even costs)

Industrial countries: slump in demand

Developing countries: growth in demand

Germany: continued uncertainty due to

transformation of the energy market

Developing countries: continued high demand

Germany and industrial countries: market opportunities in

renewable energies

Concentration/specialization through mergers and

subsequent separation

Basis chemicals stable, specialty chemicals growing

Middle East, USA: basis and specialty chemicals growing

Europe: basis chemicals declining

Industrial countries: growth through demographic

development among other things

Developing countries: growth through population

increases and expanding wealth

Industrial and developing countries: growth trends continue

Good long-term perspectives in our markets

Sources: OECD; ExxonMobil; EvaluatePharma; Roland Berger; Lünendonk

Bilfinger SE | Company Presentation | October 2016 Page 14

Energy

Oil and Gas

Chemicals

Pharma

Four strategic goals will solidify and enhance

Bilfinger’s market position

Bilfinger SE | Company Presentation | October 2016

Enhance strong

market position /

market leadership in

Europe

Strengthen service

portfolio in

engineering and

advanced asset

performance

management

Establish local

presence in selected

international growth

markets

Increase

digitization-based

services offering

Markets Where do we participate in growth markets?

Services / Innovation How do we differentiate from competitors?

Page 15

Digitization / Industry 4.0

Bilfinger with a good starting position

Digitization trend will sustainably change the processes and assets of our customers

Market expects significant efficiency increase in the process industry through Industry 4.0

Maintenance processes considered to have one of the biggest optimization potentials

Competitive landscape will change, new business models will be developed

Being market leader and provider of services along the entire value chain of assets provides many starting points

for the creation of digital innovation

Bilfinger SE | Company Presentation | October 2016 Page 16

Digitization is both, challenge and opportunity for Bilfinger

New

products

and services

Digitization / Industry 4.0

From internal process optimization to the development of

new products and services

Bilfinger SE | Company Presentation | October 2016

Digitization of processes

(vertical integration)

Integration and

collaboration

(horizontal integration)

Remote monitoring

Smart metering

Remote Maintenance

Predictive Maintenance

Mobile Maintenance

Digital documentation of maintenance work

Augmented Reality

Time recording via fingerprint

Client service portals

Supplier portals

Integrated work order management

Page 17

Examples:

Digitization / Industry 4.0

Various digital products and services already in use

Bilfinger SE | Company Presentation | October 2016

Condition Monitoring: VibraCheck

Autonomous condition monitoring

system for vibration measurement

Features (selection):

mobile signal transmission,

remote control, automatic alerts,

data evaluation

(e.g. of the amplitude spectrum)

iMaintenance: intelligent maintenance

Mobile application for optimization of

inspection and maintenance intervals

Features (selection): collection and

evaluation of process- and experience-

based data about inspection and

maintenance, deduction of recommended

optimization measures regarding

inspection and maintenance intervals

Mobile Maintenance

Optimized Work-Order-Management

System sends orders directly to the

respective employee

Features (selection):

time recording, material consumption,

barcode-identification, documentation

including pictures (as basis for quick

service acceptance and settlement)

Time recording using fingerprint scan

Fingerprint scan to document start

and end of presence at construction

site

Features (selection): work time

documentation, validity checks,

transmission to ERP-system

Page 18

Further change from “provider of single services relationship”

to a “knowledge-based partnership“

Bilfinger SE | Company Presentation | October 2016

Strategic Partnership

Value generation Cost minimization

Individual Services

Simple Supply and Service

Relationship

Rotating Equipment

Static Equipment

Electrical

Instrumentation and Control Technology

Valves Services

Insulation, Scaffolding, Corrosion Protection

Industrial Cleaning etc.

Bundling of Services

Segment Mechanical Services

Segment E/I&C Services

Modification and Extension

Turnaround

System Service Provider

Integrated Asset Service

Main Contract Value

Performance Contract

(Outsourcing)

Page 19

Optimized maintenance cycles, win-win for service provider and customer

Summary

▪ Strong position as market leader in Europe

▪ Faster growing markets outside Europe

▪ Increasing demand for advanced asset performance services

▪ Significant resources available to exploit growth potentials

Page 20

Divestment of Building and Facility supports the funding

Bilfinger SE | Company Presentation | October 2016

1. Bilfinger at a glance

2. Sale of Building and Facility

3. Industrial at a glance

4. Update on Power

5. Facts and Figures Q2 2016

6. Financial backup

Agenda

page 21 Bilfinger SE | Company Presentation | October 2016

2015: Output volume of € 1.3 billion, adjusted EBITA of € -69 million

Approx. 10,000 employees

Customer focus: Energy sector

Approx. 80% project business

Power at a glance

Page 22

€ 1.3bn output volume

employees

project business thereof ~80%

10,000 Approx.

Bilfinger SE | Company Presentation | October 2016

Update on Power:

Process is now geared towards sale of single units

Result of the selling process until June 2016:

None of the bids for the entire business reflect the true value

A number of attractive indicative bids for single units have been received

even without targeted marketing approach

Sale of single units allows for a more targeted approach, potential buyers

vary from business to business

Own restructuring and repositioning as alternative way to increase value

Bilfinger SE | Company Presentation | October 2016 Page 23

Driving value-enhancing development, including sale of single units

1. Bilfinger at a glance

2. Sale of Building and Facility

3. Industrial at a glance

4. Update on Power

5. Facts and Figures Q2 2016

6. Financial backup

Agenda

page 24 Bilfinger SE | Company Presentation | October 2016

▪ Adjusted EBITA: substantial improvement compared to

weak prior year

▪ Industrial: book to bill at 1, earnings at prior-year level, efficiency

measures taking effect

▪ Power: orders received and output volume decline further;

earnings still negative but improved

▪ Cash flow from operating activities below prior year

▪ Outlook for 2016 confirmed and specified

January to June 2016: Business Highlights

Business development in line with expectations

Bilfinger SE | Company Presentation | October 2016 page 25

▪ Pure play Industrial opens new perspectives

▪ Cash inflow allows for strategic investments in growth fields

▪ Power business will be further developed to optimize value

▪ Realignment of administration will reduce costs, simplify

structures and increase performance

▪ Investment program established for Group-wide harmonization of

IT infrastructure

January to June 2016: Strategic Highlights

Sale of Building and Facility to EQT for EV of € 1.4 bn

Bilfinger SE | Company Presentation | October 2016 page 26

3,537

2,677

Q1-Q2 2015 Q1-Q2 2016

2,297

2,039

Q1-Q2 2015 Q1-Q2 2016

January to June 2016:

Decrease in output volume and orders received as expected

Bilfinger SE | Company Presentation | October 2016 page 27

Order backlog

-24%

organic -20%

Orders received

-11%

organic -8%

Output volume

-11%

organic -8%

2,412

2,141

Q1-Q2 2015 Q1-Q2 2016

in € million in € million in € million

All figures refer to continuing operations unless stated otherwise

January to June 2016:

Substantial improvement in earnings compared to weak prior year

Bilfinger SE | Company Presentation | October 2016 page 28

Net profit*

-439

-134

Q1-Q2 2015 Q1-Q2 2016

in € million

All figures refer to continuing operations unless stated otherwise * includes continuing and discontinued operations

-59

-13

Q1-Q2 2015 Q1-Q2 2016

-48

-15

Q1-Q2 2015 Q1-Q2 2016

Adjusted net profit

Adjusted EBITA

in € million in € million

-139

-285

Q1-Q2 2015 Q1-Q2 2016

-22

-124

Q1-Q2 2015 Q1-Q2 2016

Free cash flow

January to June 2016:

Operating cash flow below prior-year level due to restructuring payments as

well as increase in working capital

Bilfinger SE | Company Presentation | October 2016 page 29

in € million in € million

All figures refer to continuing operations unless stated otherwise

Operating cash flow

January to June 2016:

Business development in both segments as expected

Bilfinger SE | Company Presentation | October 2016 page 30

Industrial

76%

Power

24%

45

-17

Industrial Power

Output volume*

EBITA adjusted

* Before consolidation/others

in € million Q1-Q2 2016 Q1-Q2 2015 Year-on-year

Industrial 1,622 1,781 -9%

Power 505 607 -17%

Consolidation/other 14 24

Group 2,141 2,412 -11%

in € million Q1-Q2 2016 Q1-Q2 2015 Year-on-year

Industrial 45 48 -6%

Power -17 -71 +76%

Consolidation/other -41 -36

Group -13 -59 +78%

in € million Q2 2016 Q2 2015 Change FY 2015

Output volume 834 946 -12% 3,650

Orders received 825 876 -6% 3,302

Order backlog 2,001 2,416 -17% 2,101

Capital expenditure 14 10 40% 47

Depreciation of P, P & E 15 24 -38% 70

EBITA adjusted 31 39 -21% 128

EBITA margin adjusted 3.7% 4.1% 3.5%

Market situation

▪ Europe:

Good demand for turnarounds

Industrial scaffolding solid; highly-competitive environment for plant insulation in GER

Business development in British and Scandinavian oil and gas sector remains restrained

Generally limited willingness to invest in projects except for biotech pharma industry

▪ United States:

Project business negatively impacted after the end of the shale gas boom

Demand for maintenance in process industry more stable

Industrial:

Stable demand for maintenance services in chemical and

pharmaceutical industries

Bilfinger SE | Company Presentation | October 2016 page 31

24% Germany

57% Rest of Europe

17% America

FY 2016e

2% Asia

Output volume by region

*In Q2 2015: thereof €7m exceptional depreciation (restructuring Industrial)

*

Quarterly development

▪ Organic development in orders

received almost stable

▪ Lower EBITA due to lower output

volume, mainly in European oil

and gas sector, as well as weak

environment for US project

business

▪ Efficiency enhancement measures

start to take effect – will show

even higher impact in second half

Industrial:

Book-to-bill at 1

Bilfinger SE | Company Presentation | October 2016 page 32

in € million Q2 2016

reported Year-on-year Organic

Output volume 834 -12% -8%

Orders received 825 -6% -2%

EBITA adjusted 31 -21% -17%

0

200

400

600

800

1,000

0%

2%

4%

6%

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

Output volume

EBITA margin adjusted

Market situation

▪ Fossil fuel power plants:

Germany and other European countries: Substantial price pressure due to market

over-capacities, demand for services declining as a result of insufficient capacity

utilization and profitability of the power plants

South Africa and Middle East: Stable demand in services business

▪ Nuclear Power:

Individual projects in Germany and abroad offer medium term prospects

Power:

Demand in project business remains low

Bilfinger SE | Company Presentation | October 2016 page 33

Output volume by region

FY 2016e

41% Rest of Europe

27% Germany

2% America

14% Africa

16% Asia

*In Q2 2016: thereof €14m (in FY 2015: thereof €14m) exceptional depreciation (restructuring Power)

*

in € million Q2 2016 Q2 2015 Change FY 2015

Output volume 258 320 -19% 1,284

Orders received 189 262 -28% 986

Order backlog 650 1,050 -38% 762

Capital expenditure 2 2 0% 9

Depreciation of P, P & E 18 6 200% 37

EBITA adjusted -11 -53 79% -69

EBITA margin adjusted -4.3% -16.6% -5.4%

*

Quarterly development

▪ Orders received on low level due

to substantially fewer projects in

the market for fossil fuel power

plants

▪ Still negative, but significantly

improved EBITA adjusted through

positive effects from capacity

adjustments and reduced project

losses based on better risk

management

Power:

Reduction in output volume due to sustained market weakness

Bilfinger SE | Company Presentation | October 2016 page 34

in € million Q2 2016

reported Year-on-year Organic

Output volume 258 -19% -13%

Orders received 189 -28% -20%

EBITA adjusted -11 +79% +77%

0

200

400

-20%

-15%

-10%

-5%

0%

5%

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

Output volume EBITA margin adjusted

Outlook FY 2016

Outlook confirmed despite weak environment for US project business

Efficiency enhancement measures with higher impact in second half

Output volume Adjusted EBITA

in € million 2015 expected 2016 2015 expected 2016

Industrial 3,650 significant decrease to

about €3.1 billion 128 at prior-year level

Power 1,284 significant decrease

to about €1.0 billion -69

significant improvement,

but still negative

HQ/Others* 68 - -82 -

Group 5,002 significant decrease

to about €4.1 billion -23 significant improvement

* Including Government Services

Definition for the qualified comparative forecast:

at prior-year level: + / -0%; slight: 1-5%; significant: > 5%

Bilfinger SE | Company Presentation | October 2016 page 35

Outlook FY 2016

Special items

In 2016, from today’s perspective, we expect the following significant special items:

Capital gain from the sale of the Building and Facility segment of ~ €500 million

One-time expenses for the program to reduce administrative expenses in the high double-digit million euro range.

This includes investments of over €50 million for the harmonization of our IT systems, of which a small portion will

be incurred in 2016. Restructuring costs are also included, of which the majority will be recognized in profit or loss

in the current year.

In the Power business segment, additional restructuring expenses in the mid double-digit million euro range as

well as extraordinary non-cash impairments on tangible assets in the amount of €14 million.

A substantial portion of the one-time expenses in connection with the further development of our compliance

system and the conclusion of older cases in the total amount of approximately €50 million.

Reported net profit will also be burdened by the non-capitalization of deferred tax assets on the negative result

of the holding.

Bilfinger SE | Company Presentation | October 2016 page 36

Backup

1. Bilfinger at a glance

2. Sale of Building and Facility

3. Industrial at a glance

4. Update on Power

5. Facts and Figures Q2 2016

6. Financial backup

Agenda

Bilfinger SE | Company Presentation | October 2016 page 37

Q2 2016

Volume and contract overview

Bilfinger SE | Company Presentation | October 2016 page 38

Backup

in € million Q2 2016 Q2 2015 Change Q2 2016 Q2 2015 Change Q2 2016 Q2 2015 Change

Industrial 834 946 -12% 825 876 -6% 2,001 2,416 -17%

Power 258 320 -19% 189 262 -28% 650 1,050 -38%

Consolidation/ Other 5 15 12 46 26 71

Continuing

Operations1,097 1,281 -14% 1,026 1,184 -13% 2,677 3,537 -24%

Output volume Orders received Order backlog

in € million H1 2016 H1 2015 Change H1 2016 H1 2015 Change H1 2016 H1 2015 Change

Industrial 1,622 1,781 -9% 1,607 1,716 -6% 2,001 2,416 -17%

Power 505 607 -17% 419 586 -28% 650 1,050 -38%

Consolidation/ Other 14 24 13 -5 26 71

Continuing

Operations2,141 2,412 -11% 2,039 2,297 -11% 2,677 3,537 -24%

Output volume Orders received Order backlog

Q1-Q2 2016

Volume and contract overview

Bilfinger SE | Company Presentation | October 2016 page 39

Backup

FY 2015

Volume and contract overview (new structure)

Bilfinger SE | Company Presentation | October 2016 page 40

Backup

Output Volume Orders received Order backlog

in € million FY 2015 FY 2015 FY 2015

Industrial 3,650 3,302 2,101

Power 1,284 986 762

Consolidation/ Other 68 13 39

Continuing Operations 5,002 4,301 2,902

Organic development output volume

Bilfinger SE | Company Presentation | October 2016 page 41

Backup

in € million H1 2015 Δ Net acquisitions Δ F/X Δ Organic H1 2016

Industrial 1,781 -12 -1% -29 -1% -118 -7% 1,622 -9%

Power 607 -12 -2% -20 -4% -70 -11% 505 -17%

Continuing Operations 2,412 -25 -1% -49 -2% -197 -8% 2,141 -11%

in € million Q2 2015 Δ Net acquisitions Δ F/X Δ Organic Q2 2016

Industrial 946 -12 -1% -21 -3% -79 -8% 834 -12%

Power 320 -12 -3% -9 -3% -41 -13% 258 -19%

Continuing Operations 1,281 -25 -2% -30 -2% -129 -10% 1,097 -14%

Organic development orders received

Bilfinger SE | Company Presentation | October 2016 page 42

Backup

in € million Q2 2015 Δ Net acquisitions Δ F/X Δ Organic Q2 2016

Industrial 876 -14 -2% -17 -2% -20 -2% 825 -6%

Power 262 -12 -5% -8 -3% -53 -20% 189 -28%

Continuing Operations 1,184 -26 -2% -25 -2% -107 -9% 1,026 -13%

in € million H1 2015 Δ Net acquisitions Δ F/X Δ Organic H1 2016

Industrial 1,716 -14 -1% -28 -1% -67 -4% 1,607 -6%

Power 586 -12 -2% -15 -2% -140 -24% 419 -28%

Continuing Operations 2,297 -26 -1% -43 -2% -189 -8% 2,039 -11%

Organic development EBITA adjusted

Bilfinger SE | Company Presentation | October 2016 page 43

Backup

in € million Q2 2015 Δ Net acquisitions Δ F/X Δ Organic Q2 2016

Industrial 39 -1 -2% -1 -2% -6 -17% 31 -21%

Power -53 0 -1% 2 +3% 40 +77% -11 +79%

Continuing Operations -34 -1 -2% 1 +3% 36 +105% 2 +106%

in € million H1 2015 Δ Net acquisitions Δ F/X Δ Organic H1 2016

Industrial 48 -1 -2% -1 -2% -1 -2% 45 -6%

Power -71 0 0% 1 2% 53 +74% -17 +76%

Continuing Operations -59 -1 -1% -1 -1% 48 +80% -13 +78%

Income statement

Bilfinger SE | Company Presentation | October 2016 page 44

Backup

in € million Q1-Q2 2016 Q1-Q2 2015 FY 2015 Comments Q1-Q2 2016

Output volume 2,141 2,412 5,002

EBITA -118 -44 -157

EBITA adjusted -13 -59 -23 See separate slide „Overview of earnings adjustments“

EBITA margin adjusted -0.6% -2.4% -0.5%

Amortization 6 338 344 FY 2016e: ~€10m

EBIT -124 -382 -501 Depreciation of P, P&E: €54m

Net interest result -11 -17 -30 In Q1-Q2 2015 higher interest expenses due to a project financing in Power

EBT -135 -399 -531

Income taxes -11 -68 -60 Nearly no deferred taxes were capitalized for tax losses

Earnings after taxes from continuing

operations -146 -467 -591

Earnings after taxes from discontinued

operations 10 23 64

Operating result of divisions sold to EQT €26m, Concessions €0m, result

from the sale of Water division -€16m, operating result Water division -€3m,

operating result Offshore and the former Construction activities €2m

Minority interest 2 5 17

Net profit -134 -439 -510

Net profit adjusted (continuing operations) -15 -48 -30

Overview of earnings adjustments

Bilfinger SE | Company Presentation | October 2016 page 45

Backup

in € million Q1-Q2 2016 Q1-Q2 2015 FY 2015 Comments Q1-Q2 2016

EBITA -118 -44 -157

Adjustments special items (pre-tax) 105 -15 134

In Q1-Q2 2016: restructuring (particularly Power) €43m

Sale of Engineering Services Asian Pacific and MCE Stahlbau, reversal of the

acquisition of Mauell as well as sales related expenses €28m

Impairments on tangible assets Power €14m

Efficiency enhancements headquarters €12m

Further development compliance system €8m

In Q1-Q2 2015: capital gain from the sale and re-evaluation of Nigerian activities and

sale of remaining concessions activities -€58m

Restructuring (particularly Industrial) €24m

Impairments on tangible assets Industrial €7m

Sales related expenses €4m

Efficiency enhancements headquarters €4m

Further development compliance system €4m

EBITA adjusted -13 -59 -23

Net interest -11 -17 -30

Normalized/ Underlying tax rate 7 24 16 Normalized tax rate of 31%

Minorities 2 4 7

Net Profit adjusted continuing operations -15 -48 -30

EPS adjusted continuing operations -0.34 -1.09 -0.68

Bilfinger SE | Company Presentation | October 2016 page 46

1,378

196

June 30, 2016

Equity and Liabilities

4,596

1,167

144

523

June 30, 2016

296

96

Assets

4,596

855

1,322

1,048

421

162

1,584 -269

-231

-2

+3

-50

-40

-589 -589

-98

-232

-9 +3

+1

-3

-251

Assets held for sale

Cash and cash equivalents

Receivables and other current assets

Other non-current assets

Property, plant and equipment

Intangible assets1)

Compared to pro-forma balance sheet as of Dec. 31, 2015

1) Thereof goodwill €844 million (including intangibles

from acquisitions)

Liabilities held for sale

Other current liabilities

Prepayments received

Other non-current liabilities

Pension provisions

Financial debt

Shareholders’ equity

in € million

Balance sheet

Backup

Valuation net debt

Bilfinger SE | Company Presentation | October 2016 page 47

Backup

* Pro-forma balance sheet as of Dec. 31, 2015

in € million Jun. 30, 2016 Dec. 31, 2015* Comments Jun. 30, 2016

Cash and cash equivalents 196 427 See cash flow statement for details of change

Financial debt -523 -526 Including €500 million corporate bond (due Dec. 2019)

Net cash (+) / net debt (-) -327 -99

Pension provisions -296 -295

Increase due to lower discount rate (from 2.25% to 1.30% in Euro-

Zone), offset by deconsolidation of Mauell (€36m)

Expected cash-in disposals Approx. 935 Approx. 1,125 Expected sale of Building and Facility divisions €900 million

Expected sale Nigerian activities €35m

Inter-company loan Building and Facility divisions sold to EQT -77 -180

Financial assets (disposal Building and Facility divisions) 300 300 Approx. €200 million earn-out agreement and approx. €100 million

vendor’s claim

Future cash-out restructuring and risk provisions Approx. -180 Approx. -223

Including future cash-out restructuring Industrial and Power, SG&A

efficiency program (approx. €160m)

and legacy (Tubin, approx. €20m)

Future cash-out Compliance -40 -50

Further intra-year working capital need (seasonal shift) - -150 to -200

Valuation cash (+) / net debt (-) Approx. 300 Approx. 400

Cashflow statement

page 48 Bilfinger SE | Company Presentation | October 2016

Backup

in € million Q1-Q2 2016 Q1-Q2 2015 FY 2015 Comments Q1-Q2 2016

Cash earnings from continuing operations -81 -49 -122

Change in working capital -218 -51 203 Typical intra-year increase in working capital, though more pronounced

as in previous year. Power in previous year with extraordinary lower working capital.

Gains on disposals of non-current assets 14 -39 -42 Contains expenses from disposals

Cash flow from operating activities of continuing operations -285 -139 39

Net capital expenditure on property, plant and equipment /

intangibles -17 -19 -36 Gross Capex FY 2016e: up to 100m EUR

Proceeds from the disposal of financial assets 178 136 214 Esp. cash inflow from the sale of Water division

Free cash flow (continuing operations) -124 -22 217

Investments in financial assets of continuing operations -2 -1 -4

Cash flow from financing activities of continuing operations -4 -3 -105

Change in cash and cash equivalents of continuing

operations -130 -26 108

Change in cash and cash equivalents of discontinued

operations -110 -93 -45 Thereof divisions sold to EQT: -€61m, Construction: -€27m, Offshore: -€30m

F/X effects -1 4 2

Cash and cash equivalents at Jan. 1 475 403 403 Change in cash and cash equivalents classified as assets held for

sale -38 -51 7

Cash and cash equivalents at Jun. 30 196 237 475

▪ The Building, Facility Services and Real Estate divisions

were sold in June 2016 to financial investor EQT, the

transaction is expected to be completed in the third

quarter of 2016.

▪ Output volume: In the magnitude of the prior year.

▪ Orders received: Below unusually high prior-year figure,

typical volatility in this business.

▪ Adjusted EBITA: At prior-year level.

Discontinued operations: Building and Facility

Bilfinger SE | Company Presentation | October 2016 page 49

Backup

in € million H1 2016 H1 2015 Change FY 2015

Output volume 1,165 1,183 -2% 2,501

Orders received 1,207 1,774 -32% 3,286

Order backlog 2,625 2,410 9% 2,581

Capital expenditure 6 10 -40% 16

Depreciation of P, P & E 4 4 0% 17

EBITA adjusted 45 47 -4% 126

EBITA margin adjusted 3.9% 4.0% 5.0%

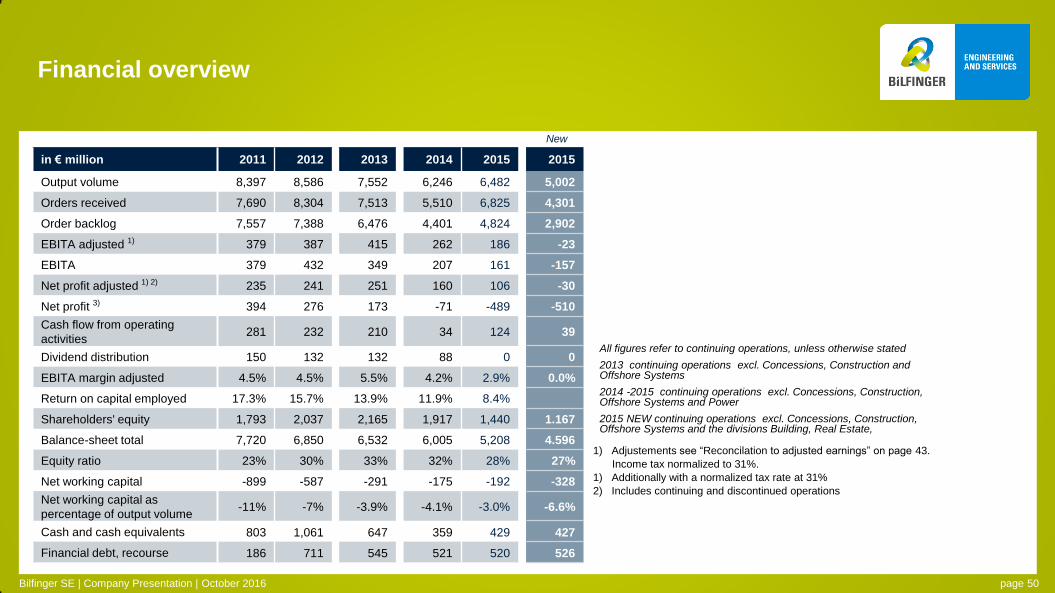

in € million 2011 2012 2013 2014 2015 2015

Output volume 8,397 8,586 7,552 6,246 6,482 5,002

Orders received 7,690 8,304 7,513 5,510 6,825 4,301

Order backlog 7,557 7,388 6,476 4,401 4,824 2,902

EBITA adjusted 1) 379 387 415 262 186 -23

EBITA 379 432 349 207 161 -157

Net profit adjusted 1) 2) 235 241 251 160 106 -30

Net profit 3) 394 276 173 -71 -489 -510

Cash flow from operating

activities 281 232 210 34 124 39

Dividend distribution 150 132 132 88 0 0

EBITA margin adjusted 4.5% 4.5% 5.5% 4.2% 2.9% 0.0%

Return on capital employed 17.3% 15.7% 13.9% 11.9% 8.4%

Shareholders' equity 1,793 2,037 2,165 1,917 1,440 1.167

Balance-sheet total 7,720 6,850 6,532 6,005 5,208 4.596

Equity ratio 23% 30% 33% 32% 28% 27%

Net working capital -899 -587 -291 -175 -192 -328

Net working capital as

percentage of output volume -11% -7% -3.9% -4.1% -3.0% -6.6%

Cash and cash equivalents 803 1,061 647 359 429 427

Financial debt, recourse 186 711 545 521 520 526

Financial overview

1) Adjustements see “Reconcilation to adjusted earnings” on page 43.

Income tax normalized to 31%.

1) Additionally with a normalized tax rate at 31%

2) Includes continuing and discontinued operations

Bilfinger SE | Company Presentation | October 2016

All figures refer to continuing operations, unless otherwise stated

2013 continuing operations excl. Concessions, Construction and Offshore Systems

2014 -2015 continuing operations excl. Concessions, Construction, Offshore Systems and Power

2015 NEW continuing operations excl. Concessions, Construction, Offshore Systems and the divisions Building, Real Estate,

page 50

New

Shareholder structure

▪ High proportion of institutional investors

▪ International shareholder base

▪ Free float according to Deutsche Boerse: 70.39%

Treasury Stock

▪ 1,815,085 shares

▪ No cancellation planned

Shareholder structure

Bilfinger SE | Company Presentation | October 2016

Jun. 30, 2016

Treasury Stock 4%

Undisclosed/ Retail

Investors 35%

Institutional Investors: 61%

Cevian Capital 26%

Germany 9%

Switzerland 8%

UK 6%

USA 6%

Scandinavia 4%

France 1%

Other 1%

page 51

November 10, 2016

Interim Report Q3 2016

February 14, 2017

Preliminary Report FY 2016

March 15, 2017

Press conference on financial statements

May 15, 2017

Interim Report Q1 2017

May 24, 2017

Annual General Meeting

August 14, 2017

Interim Report Q2 2017

November 14, 2017

Interim Report Q3 2017

Financial calendar and share facts

1) Including 1,815,085 shares held as treasury stock

52 week high / low: € 45.35 / € 25.05 (as of October 27, 2016)

Closing price € 32.17 (as of October 27, 2016)

Market cap: 1) € 1.5 bn (as of October 27, 2016)

Shares outstanding: 1) 46,024,127

ISIN / Ticker abbreviation: DE0005909006 / GBF

Main stock markets: XETRA / Frankfurt

Segments Deutsche Boerse / Indices:

Prime Standard

MDAX,

DAXsubsector Industrial Products & Services Idx.,

Euro STOXX Low Carbon, STOXX Europe 600, Euro

STOXX, STOXX EUROPE TMI Support Services

Bilfinger SE | Company Presentation | October 2016 page 52

Bilfinger bond and rating

Bilfinger SE | Company Presentation | October 2016

ISIN / Stock exchange

abbreviation DE000A1R0TU2

WKN A1R0TU

Listing Luxembourg (official trading)

Emission volume € 500 million

Interest coupon 2.375%

Maturity December 07, 2019

Closing 103.84% (as of October 27, 2016)

Rating Agency Standard & Poors

Current Corporate

Credit Rating BB+ / Stable Outlook / B

page 53

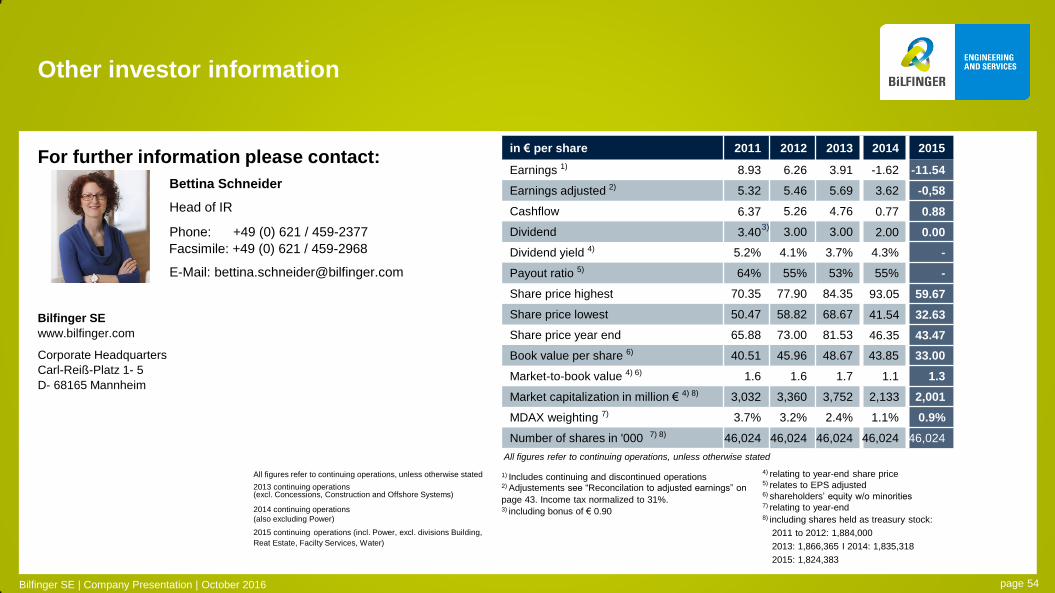

For further information please contact:

Bettina Schneider

Head of IR

Phone: +49 (0) 621 / 459-2377

Facsimile: +49 (0) 621 / 459-2968

E-Mail: [email protected]

Bilfinger SE

www.bilfinger.com

Corporate Headquarters

Carl-Reiß-Platz 1- 5

D- 68165 Mannheim

Other investor information

1) Includes continuing and discontinued operations

2) Adjustements see “Reconcilation to adjusted earnings” on

page 43. Income tax normalized to 31%. 3) including bonus of € 0.90

in € per share 2011 2012 2013 2014 2015

Earnings 1) 8.93 6.26 3.91 -1.62 -11.54

Earnings adjusted 2) 5.32 5.46 5.69 3.62 -0,58

Cashflow 6.37 5.26 4.76 0.77 0.88

Dividend 3.40 3.00 3.00 2.00 0.00

Dividend yield 4) 5.2% 4.1% 3.7% 4.3% -

Payout ratio 5) 64% 55% 53% 55% -

Share price highest 70.35 77.90 84.35 93.05 59.67

Share price lowest 50.47 58.82 68.67 41.54 32.63

Share price year end 65.88 73.00 81.53 46.35 43.47

Book value per share 6) 40.51 45.96 48.67 43.85 33.00

Market-to-book value 4) 6) 1.6 1.6 1.7 1.1 1.3

Market capitalization in million € 4) 8) 3,032 3,360 3,752 2,133 2,001

MDAX weighting 7) 3.7% 3.2% 2.4% 1.1% 0.9%

Number of shares in '000 7) 8) 46,024 46,024 46,024 46,024 46,024

3)

Bilfinger SE | Company Presentation | October 2016

4) relating to year-end share price

5) relates to EPS adjusted 6) shareholders’ equity w/o minorities 7) relating to year-end 8) including shares held as treasury stock:

2011 to 2012: 1,884,000

2013: 1,866,365 I 2014: 1,835,318

2015: 1,824,383

All figures refer to continuing operations, unless otherwise stated

All figures refer to continuing operations, unless otherwise stated

2013 continuing operations (excl. Concessions, Construction and Offshore Systems)

2014 continuing operations

(also excluding Power)

2015 continuing operations (incl. Power, excl. divisions Building,

Reat Estate, Facilty Services, Water)

page 54

Disclaimer

Bilfinger SE | Company Presentation | October 2016 page 55

This presentation has been produced for support of oral information purposes only and contains

forward-looking statements which involve risks and uncertainties. Forward-looking statements are statements

that are not historical facts, including statements about our beliefs and expectations. Such statements made

within this document are based on plans, estimates and projections as they are currently available to Bilfinger

SE. Forward-looking statements are therefore valid only as of the date they are made, and we undertake no

obligation to update publicly any of them in light of new information or future events. Apart from this, a number

of important factors could therefore cause actual results to differ materially from those contained in any

forward-looking statement. Such factors include the conditions in worldwide financial markets as well as the

factors that derive from any change in worldwide economic development.

This document does not constitute any form of offer or invitation to subscribe for or purchase any securities. In

addition, the shares of Bilfinger SE have not been registered under United States Securities Law and may not

be offered, sold or delivered within the United States or to U.S. persons absent registration under or an

applicable exemption from the registration requirements of the United States Securities Law.