Embed Size (px)

Citation preview

AGENCY FOR INTERNATIONAL DVELOPMENT IOR AID USE ONLY

WASINGTON D C 20318

BIBLIOGRAPHIC INPUT SHEET A PNIMARY

1 SUBJECT Development and economics DA00-0000G800 rLA$SI-

FICATION a $FtalAIRY

General--Southeast Asia 2 TITLE AND SUBTITLEEconomic interdependence inSoutheast Asiafinal report

3 AUTHOR(S)

(101) Wis Univ Deptof Economics

4 DOCUMENT DATE I5 NUMBER OF PAGES I6 ARC NUMBER 1970 1 ApRC

7 REFERENCE ORGANIZATION NAME AND ADDRESSWis

0 SUPPLEMENTARY NOTES (SponseoIng Organlatlons Publiahera A valabilfy)

Research summary)

9 ABSTRACT

0 CONTROL NUMBER 1ItPRICE OF DOCUMENT

12 -DESC RIP TO RS 1 P O E T N M ECooperation II PROJECT NUMBER

Economic developnment 14 CONTRACT NUMBER Re 4onal planning CSD-355 ResSoutheast Asia isTYPE OF DOCUMENT

AID 3390-1 4-741

ECONOMIC INTERDEPENDENCE

IN SOUTHEAST ASIA

FINAL REPORT

The University of Wisconsin

AID Research Program

(Contract csd3565)

March 17 1970

Preface

In the spring of 1963 before Southeast Asia became so conspicuous

a problem of foreign policy as it later became the Agency for International

Development invited a number of US universities to consider the possibility of basic research on economic development in Southeast Asia and on economic

cooperation within the region AID also sought to encourage a rapid inshycrease in the number of American and Asian economists doing research in the field Eleven universities submitted proposals two were invited in final competition to revise and resubmit their proposals A contract was signed with the University of Wisconsin on March 23 1964 With extensions the

contract continued through 1967 and editing and publication work under the

contract has continued into 1970

The University of Wisconsin already had on its stdff a number of economists who had held teaching research or advisory roles in Southeast Asia and whose interest in that region was continued in their research and

teaching in the United States The University accepted the contract because of the promise of its fitting with mutual support into regular programs

of teaching research and exchanges both with respect to economic developshy

ment generally and Southeast Asia in particular

The University was disposed toward a broad framework in definition of the region and conceptually including basic issues of development

regional cooperation and planning within which to place the specific issues

of economic interdependence in Southeast Asia

The operation plan of the Contract was set out in Appendix B A - To ascertain as accurately as possible the nature and extent of

benefits that might accrue to certain South and Southeast Asian countries through increased economic co-operation

B - To stimulate research by qualified researchers both in the United States and in the Asian countries in the field of regional economic co-operation

C - To hold such meetings as necessary including working conferences in the United States and Asia to discuss and criticize research in progress and

D -To appraise AID by written reports of the political aspects of its analysis and to advise AID by written reports on the best way to use its resources to attain alternative policy objectives

2

The Contract projection of the research to be done was more indicative than specific Wisconsin agreed to use its best effort

a - To evaluate the economic advantage to countries of the region from economic co-operation and co-ordination

b - To assess the theory and experience of ecoyiomic growth and of common market and free trade association ventures and other forms of economic co-operation as compared with Southeast Asian possibilities

c -To assess the extent to which national plans have implications or specifications with respect to economic integration in the areaand the extent to which success or failures in implementationhave had any systematic relation to regional economic interest

d - To indicate future AID strategy with respect to regional economic co-operation In this camptegory Contractor shall advise AID what policiesof AID can most effectively encourage the economic co-operation measures that best serve the interests of the region

Most of the research done under this contract has gone into 62 papers

including 5 longer and summary studies The majority have been circulated to

AID or have been incorporated in a book published in 1969 by the University of Wisconsin Press Economic Interdependence in Southeast Asia The material

in this Report does not in general duplicate the basic papers though it often draws on them This Report attempts to meet more narrowly and specishy

fically the questions posed by the Contract summaries and conclusions

depend in part on material not reproduced here

The 42 people listed below have been authors in part or wholly of one or more of the Project papers (For those not now (March 1970)

at the University of Wisconsin we have put down the institution with which

they are connected) Among them Professors Everett D Hawkins Seiji

Naya Nyle Spoelstra K C Sen and Mrs Fag el Nour have been especially

close to the Project Professor Hawkins was in touch with the work from

the beginning contributed throughout and was for a time Director of

Research He has been a most helpful critic of this Report Professor Spoelstra

carried much of the administrative and editing burden during the whole Contract

period

Bernhard Abrahamsson Benjamin Higgins (Univ of Denver) (Univ of Montreal)

3

Dorra Alwan Harley Hinricks (Univ of Maryland) (Univ of Maryland)

Robert E Baldwin Kai-Loo Huang (Moravian College)

AN Bhagat (UN Econ Yune Huntrakoon (Bank of Com for Africa) Thailand)

Angela Bilkey Nurul Islam (Pakistan Inst of

Amado Castro (Univ of the Development Economics) Philippines)

KR Chou (Nan Yang Univ)

HNS Karunatilake (Central Bank of Ceylon)

PT Ellsworth (Univ of Allen C Kelley

California Riverside) Hiroshi Kitamura (UN Econ Com Naval Fag El Nour (American

for Asia and the Far East)

University Cairo) DT Lakdawala (Univ of Bombay)

Everett D Hawkins Robert J Lampman

Lim Chong Yah (Univ of JC Leith (Univ of Western Singapore) Ontario)

Theodore Morgan DV Ramana (Asian Inst for

Hla Myint (London School of Economics)

Econ Devel and Planning)

Stephen E Reynolds (Univ of

Seiji Naya (National Bureau of Utah)

Econ Research Univ of John Richards Hawaii)

Kenichi Odawara KC Sen (Asian Development Bank)

(Sophia University Tokyo) IM Singh (Ohio State University)

J PanglAykim (Australian National Univ)

I-Shuan Sun (Central Bank of China)

Douglas S Paauw (National Planning Association Washington)

Nyle Spoelstra (Nat Inst of Devel Administration Bangkok)

RH Patil (Univ of Bombay) Anthony Tang (Vanderbilt Univ)

4

John Power (Univ of the Kenneth D Thomas (La Trobe Philippines) Univ Melbourne)

Jeffrey G Williamson

Ta-Yeh Wu (UN Econ Devel Board Singapore)

Suparb Yossundara (Bank of Thailand)

The following 44 people have served as consultants to the research program being one or several days at Madison and holding formal and informal meetings with the research group and usually speaking at a Workshop

Herbert Grubel (Univ of Pennsylvania) Gottfried Haberler (Harvard University) Robert Z Aliber (Univ of Chicago) W M Corden (Oxford Univ)Ronald McKinnon (Stanford Univ) Guy Black (Council of Economic Advisers

WashingtonDC)Irma Adelman (Northwestern Univ) Adam Marton (Budapest Hungary) W Arthur Lewis (Princeton Univ) Clair Wilcox (Swarthmore College)Pan A Yotopoulos (Stanford Univ) D A Snider (Miami Univ) Hollis B Chenery (Harvard Univ) Lloyd J Reynolds (Yale Univ) Richard E Caves (Harvard Univ)Arthur T Mosher (Econ Devel Council

New York)Hla Myint (London School of Econ) Frank H Golay (Cornell Univ)Gerhard Tintner (Univ Calif Los Angeles) Kang Chao (Univ of Wisconsin)Nathan Keyfitz (Univ of Chicago)Emile Despres (Stanford Univ) Clifton R Wharton Jr (Michigan State Univ) Gustav F Papanek (Harvard Univ)Lauchlin Currie (National Univ of Columbia) Edward Fei (Agency for Int Devel

Washington D C)Richard Goode (Int Monetary Fund

Washington D C)Benjamin Higgins (Univ of Montreal) G Sicat (Univ of the Philippines)Douglas Fontein (Int Bank for Recon and Devel) J Strasma (Univ of Wisconsin)

5

A Ravenholt (Amer Univ Field Service Manila) Bela Balassa (Johns Hopkins Univ and IBRD) HK Mazumdar (Indian Statistical Institute Calcutta) Robert R Nathan (Nathan Associses Washington DC) Reed Irvine (Federal Rcmerve Board Washington DC) Julian H Singman (Washington DC) Lloyd I Rudolph (Univ of Chicago) George Dalton (Northwestern Univ) CH Thompson (Int Bank for Rec and Devel) Stephen Enke (Dept of Defense Washington DC) John H Power (University of the Philippines) Harry G Johnson (Univ of Chicago and London School

of Economics) I Robert Sinai (New York Univ)

A conference on Economic Interdependence in Southeast Asia was held at

Bangkok at Sala Santithan (ECAFE) in January 1967 Contributors are listed

in the first group above

The views presented here are of course personal ones and do not necesshy

sarily reflect those of the United States Agency for International Development

the University of Wisconsin or the other organizations with which various

contributors are or have been associated

Theodore Morgen Director of Research

University of Wisconsin

March 17 1970

6

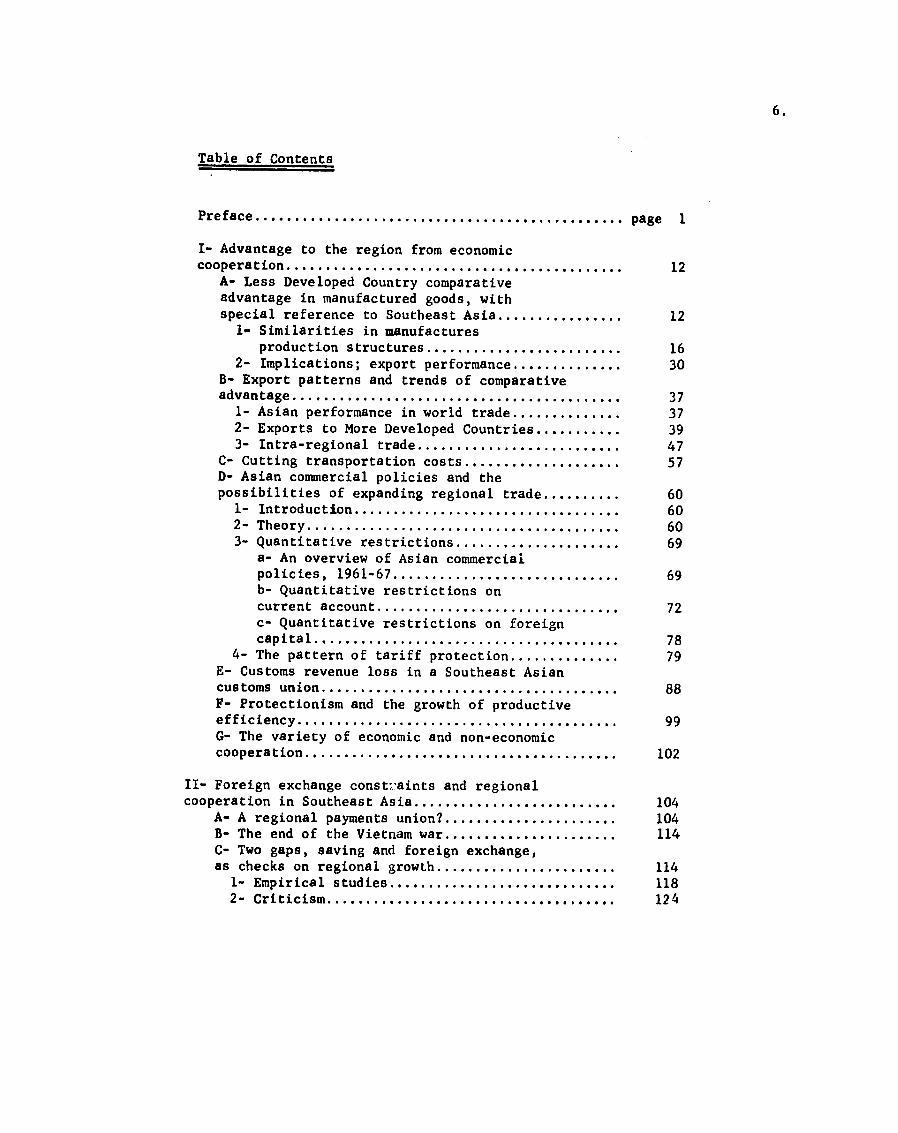

Table of Contents

Preface page 1

I- Advantage to the region from economic cooperation 12

A- Less Developed Country comparative advantage in manufactured goods with special reference to Southeast Asia 12 I- Similarities in manufactures

B- Export patterns and trends of comparative

D- Asian commercial policies and the

a- An overview of Asian commercial

b- Quantitative restrictions on

c- Quantitative restrictions on foreign

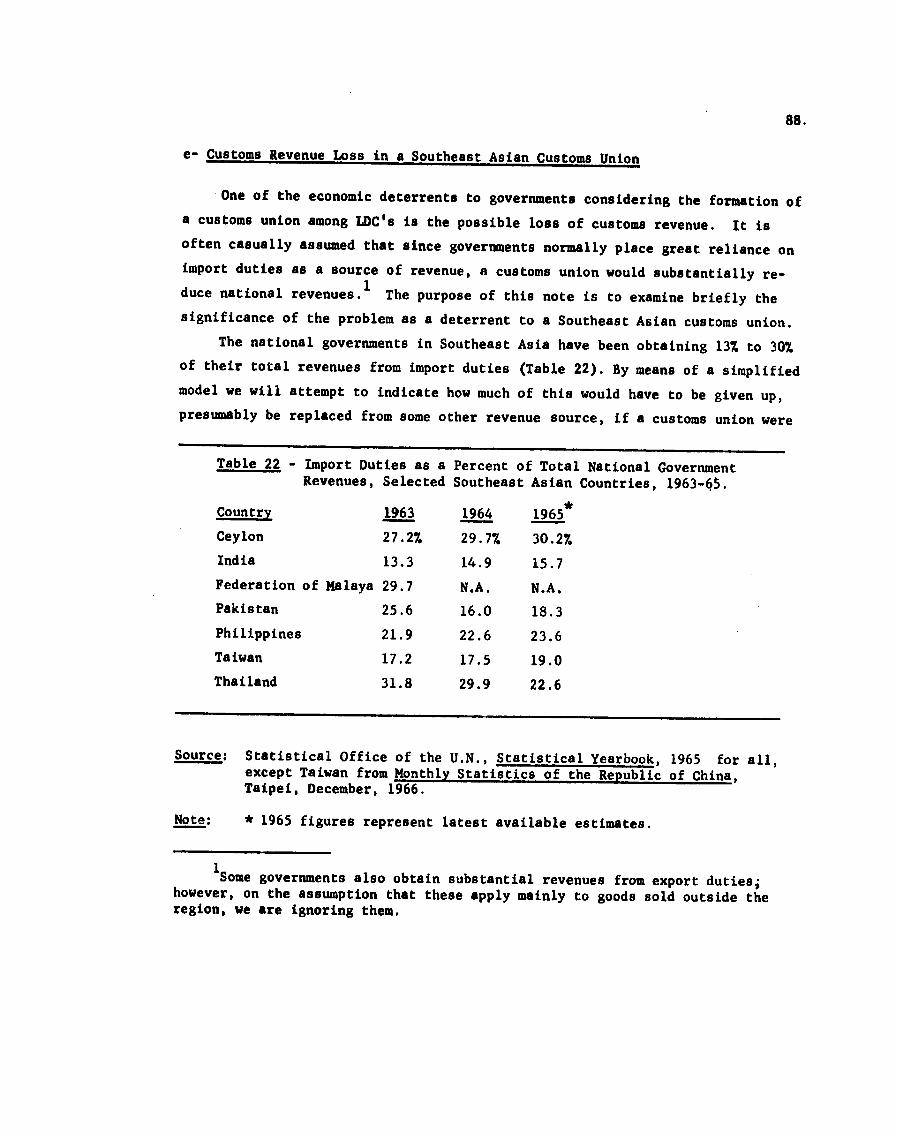

E- Customs revenue loss in a Southeast Asian

F- Protectionism and the growth of productive

G- The variety of economic and non-economic

production structures 16 2- Implications export performance 30

advantage 37 1- Asian performance in world trade 37 2- Exports to More Developed Countries 39 3- Intra-regional trade 47

C- Cutting transportation costs 57

possibilities of expanding regional trade 60 1- Introduction 60 2- Theory 60 3- Quantitative restrictions 69

policies 1961-67 69

current account 72

capital 78 4- The pattern of tariff protection 79

customs union 88

efficiency 99

cooperation 102

II- Foreign exchange const7aints and regional cooperation in Southeast Asia 104

A- A regional payments union

C- Two gaps saving and foreign exchange

104 B- The end of the Vietnam war 114

as checks on regional growth 114 1- Empirical studies 118 2- Criticism 124

7

III- Major cautions on the statistics 126

3- Effect of adjusting trade data by the

B- Inaccuracies and misleading concepts in

2- Misleading categories for LDC growth

pageA- Inaccuracies in Southeast Asia trade data 126

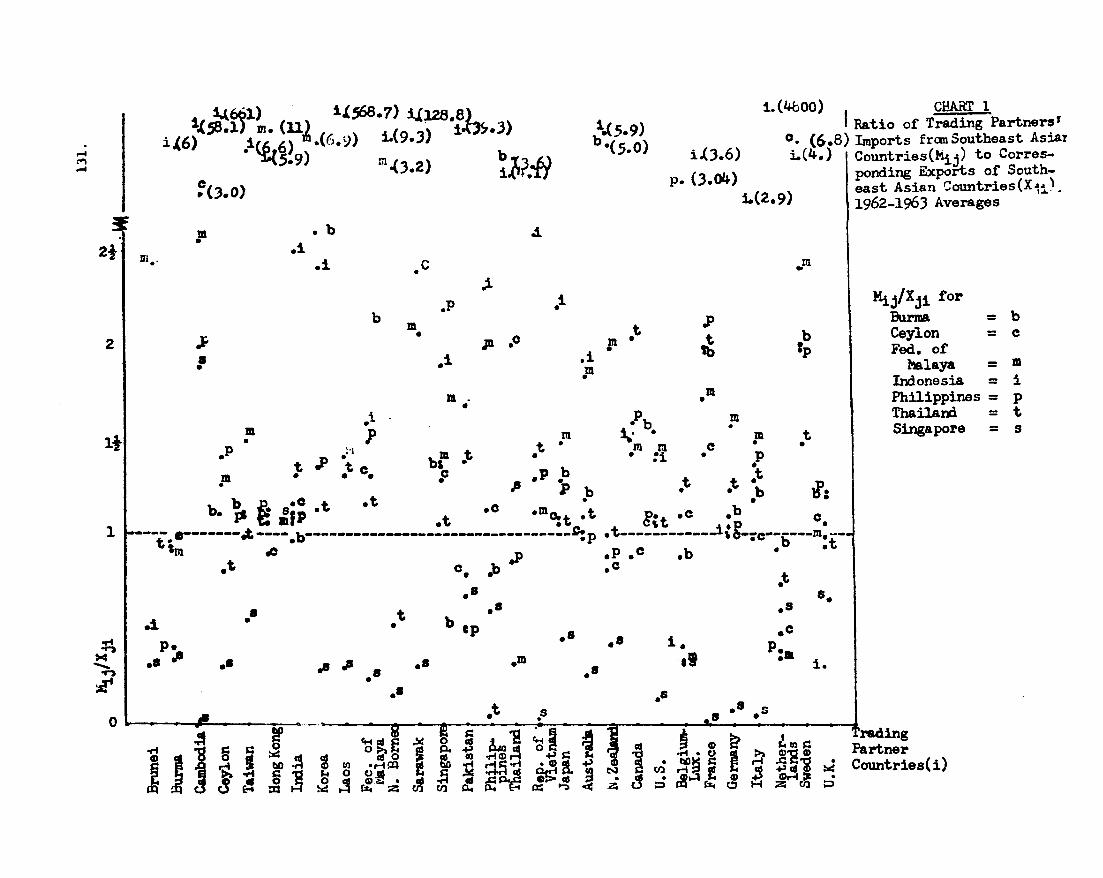

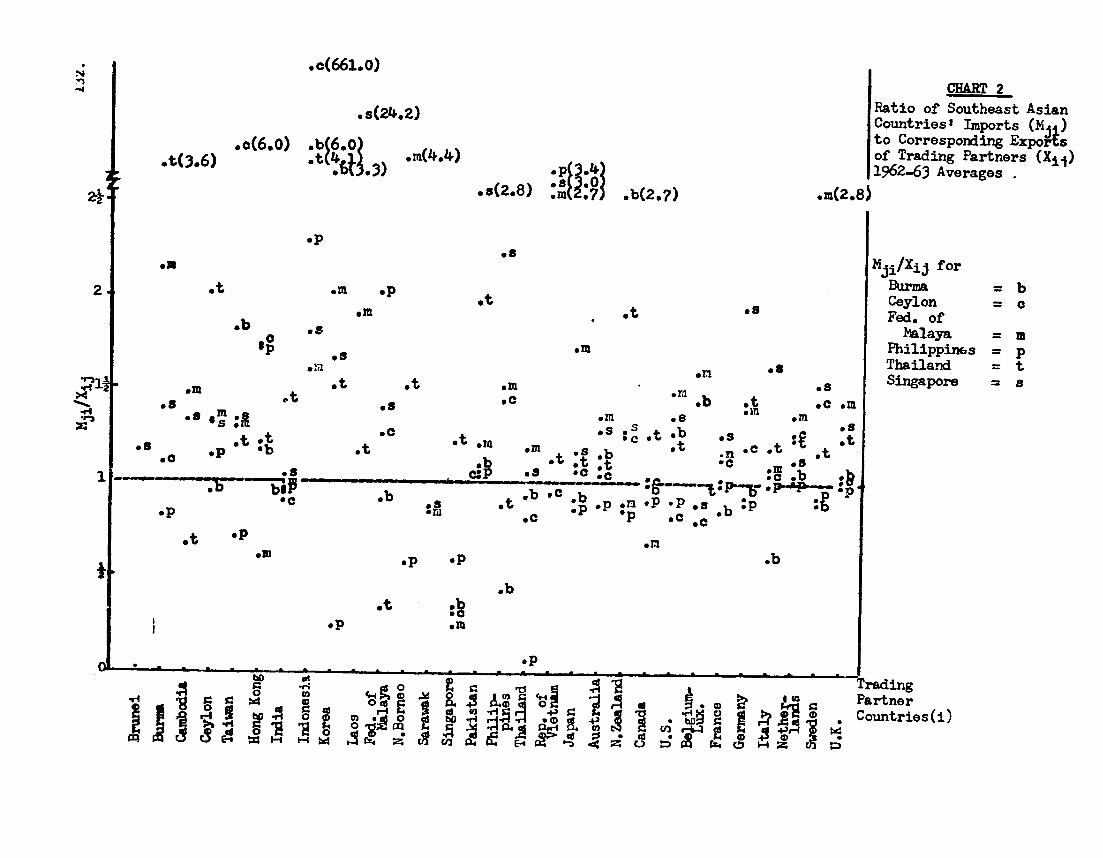

- The problem procedure 126 2- The errors 128

exchange rate 137 4- Commodity trade statistics in detail 140 5- Concluding comment 142

the standard national income statistics 144 1- Errors in LDC social accounts 144

analysis 146

IV- National plans and regional integration in Southeast Asia 150

A- Planning patterns

D- Spill-overs Plan Harmonization and

150 I- Two directions of policy in LDCs 151 2- Two patterns of growth in Southeast Asia 152 3- A recent trend 153

B- Planning in five countries a summary 154 1- Indonesia 155 2- Thailand 156 3- Singapore 158 4- The Philippines 159 5- Malaysia 159

C- Multiple objectives 161 1- Ditficulties as seen by the planners 161 2- The purposes of planning 162

bilateral agreements 164 1- The spill-over effect 164 2- The regional harmonization proposal 165 3 - Bilateral agreements 169

E- Some conclusions 170

V- Regional cooperation in Southeast Asia--forms policy 172

- Degree of formality and government A- Taxonomy 172

commitment 172 2- Cooperation within the region only 175 3- Other categories 175

B- The political hurdles 176 C- Guidlines for policy 177

VI- Summary policy implications 179

Appendix Research papers written in the Project 188

8

Tables

1 - ISIC classification 17

2 - Indices of value-added per employee wages and salaries per employee and non-wage valueshyadded per employee for manufactures in selected Southeast Asian Countries (ISIC 2-3 = 100) 1963 18

3 - Consistency in value-added by industries in Asia 20

4 - Manufactures satisfying low value added peremployee criteria in the Philippines 23

5 - Manufactures satisfying low value added per employee criteria in the States of Malaysia 27

6 - Export performance of nine Asian Countries 1962-65 32

7 - Manufactured exports of dynamic character for selected Southeast Asian Countries 35

8 - Export directions by regions 38

9 - The compositional and competitive effects of exports to more developed countries by Asian Countries - averages of 1956-57 and 1964-65 41

10 - The composition and competitive effect of exports of Asian Countries by commodity groups averages of 1956-57 (I) and 1964-65 (II) in percentages 44

11 - Export growth and shares of intra-regional exports averages of 1956-57 and 1964-65 48

12 - Commodity composition of total and intra-regional exports of selected Asian Countries 1962 and 1965 50

13 - Commodity composition of total and intra-regional imports of selected Asian Countries 1962 and 1965 51

14 - Competitive and compositional effects of intra-Asian Trade by country 1962-65 53

15 - The compositional and competitive effects of less developed Asias export to more developed areas 1956-57 to 1964-65 56

16 - Asian commercial policies 70

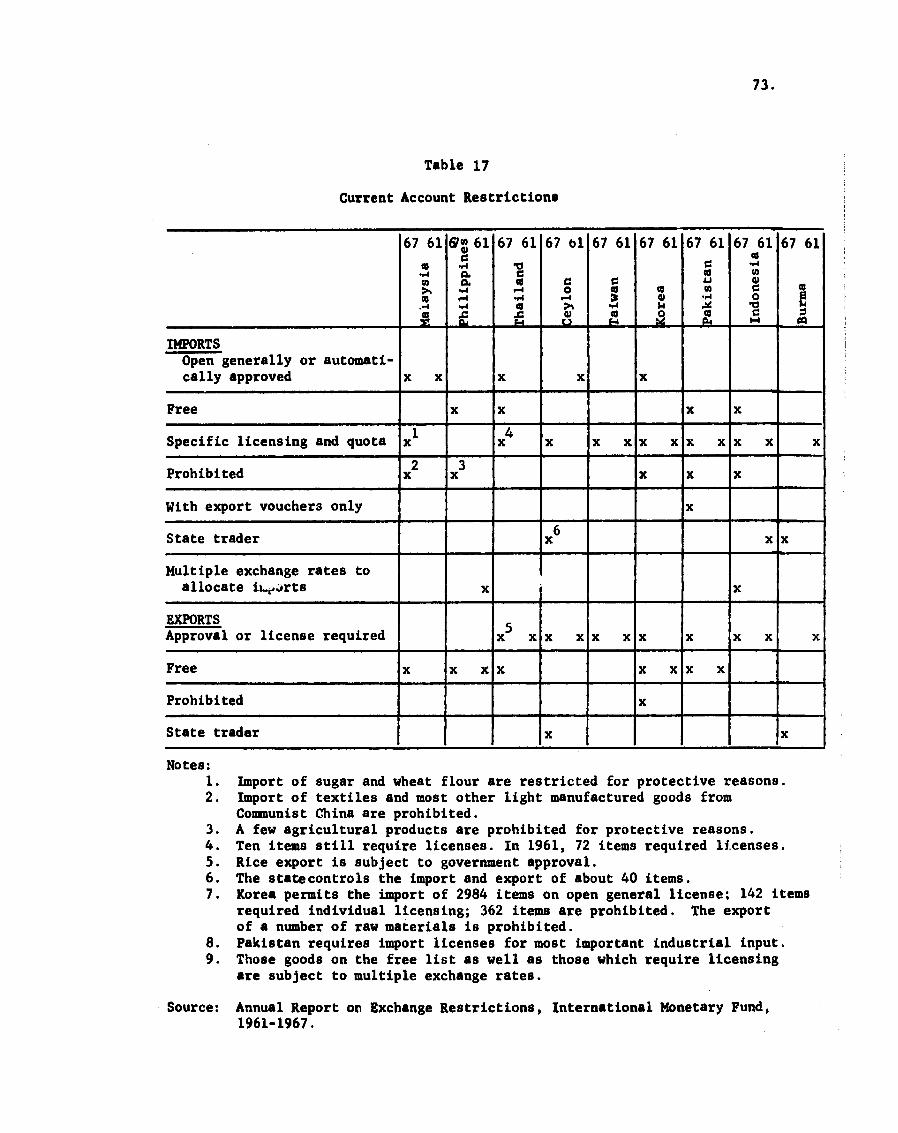

17 - Current account restrictions 73

9

18 - Significant changes in current account policy 74

19 - Restrictions on current account 76

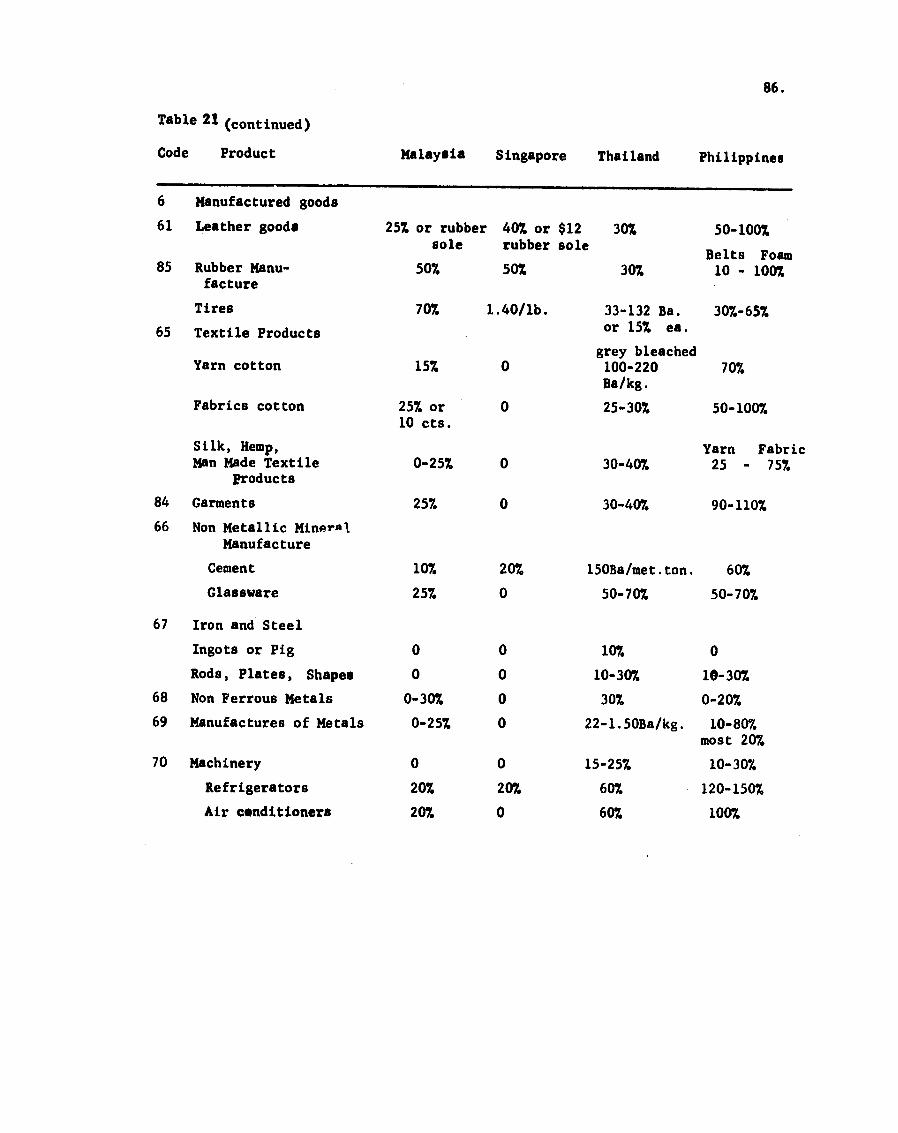

20 shy Tariffs-Major categories 82

21 - Sample commodities duties (Ad valorem or specifices equivalent) 84

22 - Import duties as a percent of total national government revenues selected Southeast Asian countries 1963-65 88

23 - Hypothetical calculations of revenue losses 93

24 - Federation of Malaysia revenues of Federal and State governments 94

25 - Malaysia revenue collected on imports from Two Partner Countries 1963 96

26 - Potential revenue loss 98

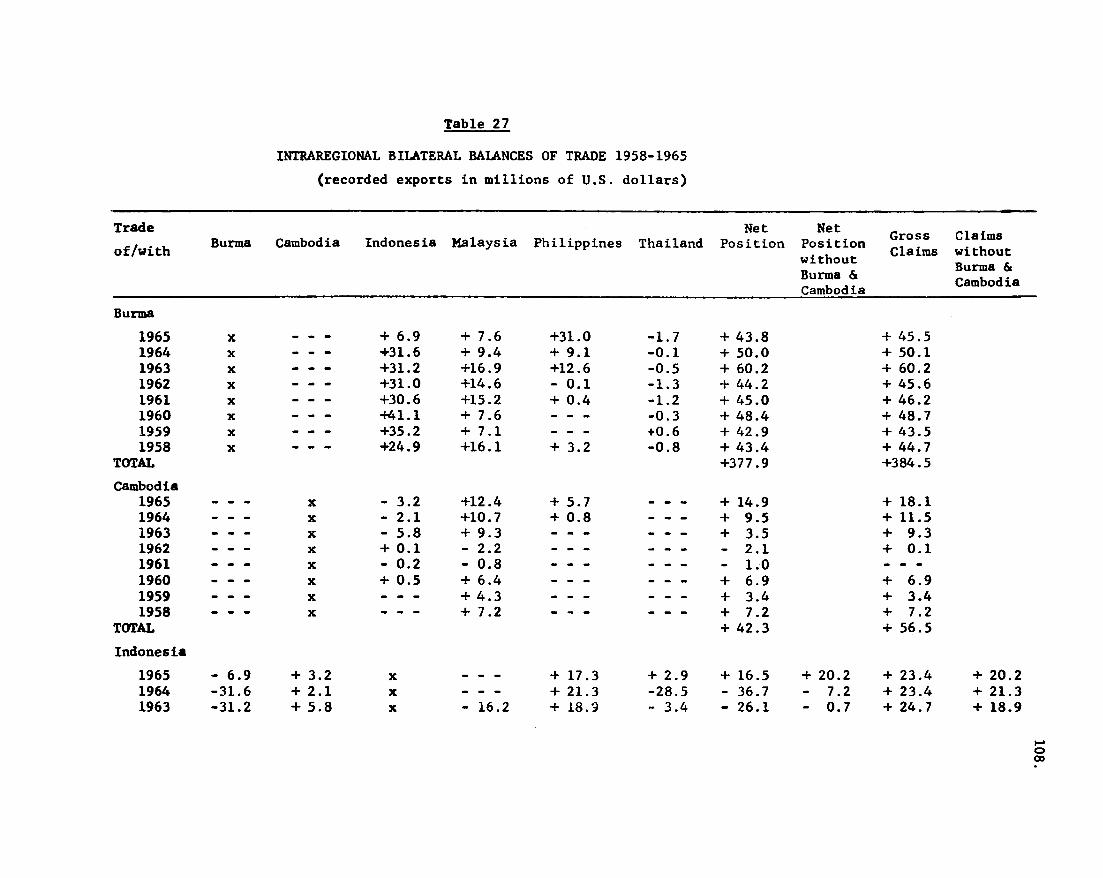

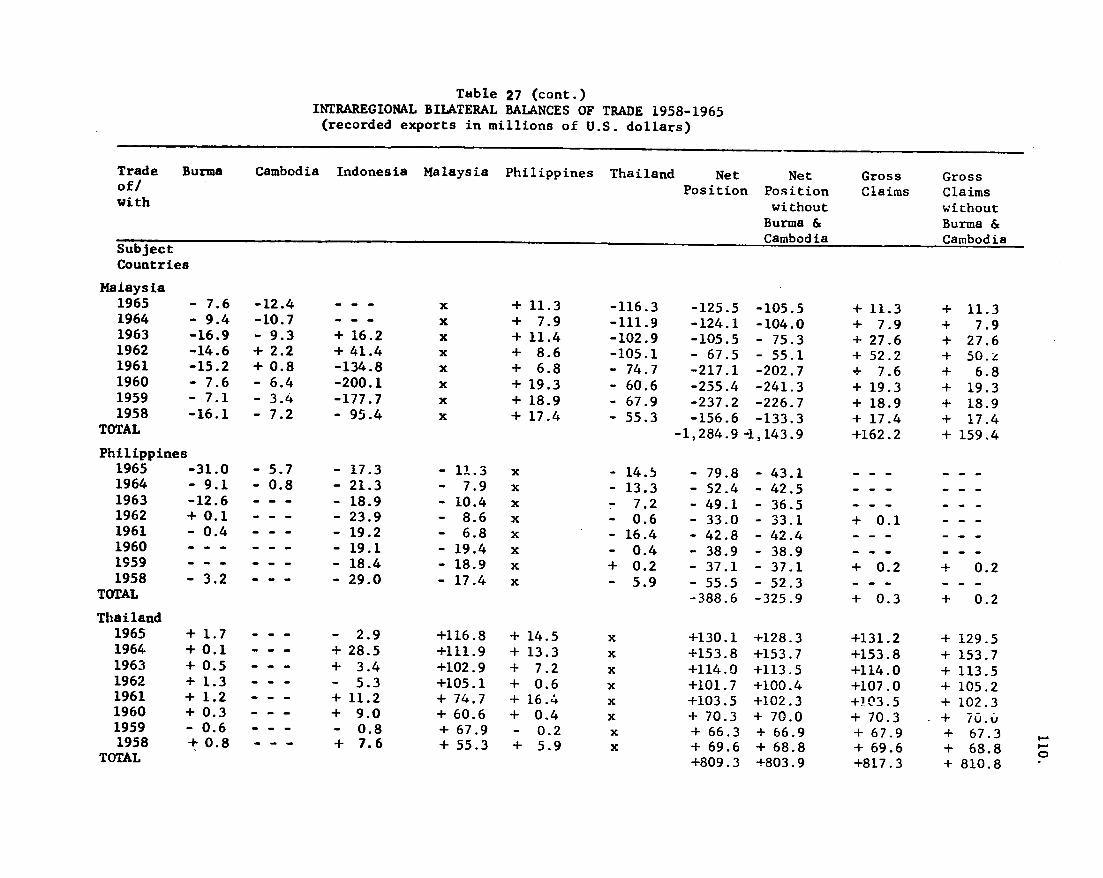

27 - Intraregional bilateral balances of trade 1958-65 108

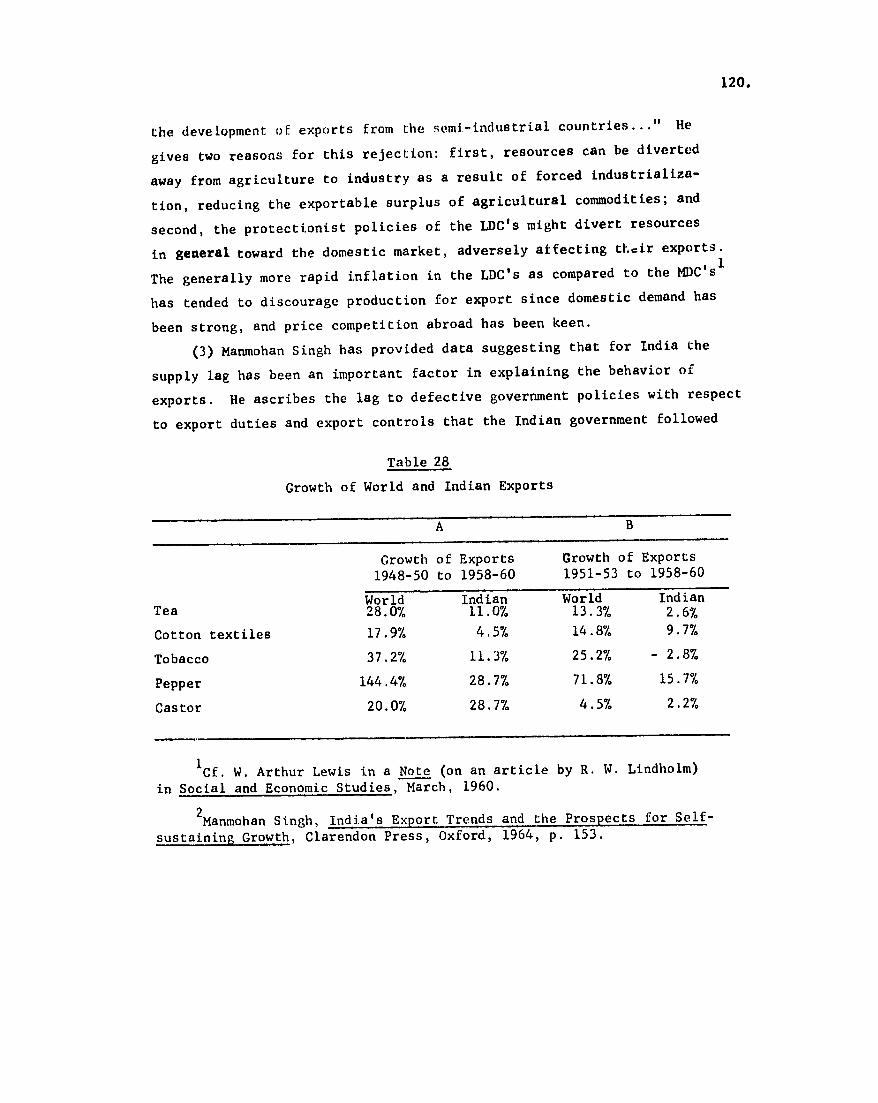

28 - Growth of world and Indian exports 120

29 - Indicies of gross profits in Indian industries (1950-100) 121

30 - A zest of average export ratios (MiX i) assuming ar expected value of 1 10ij 133

31 - A test of average import ratios (MX) assuming an exrected value of 11031 133

32 - A test on variability of export and import ratios of Southeast Asian countries with Asian and more developed country partners 136

33 - The averages of export and import ratios standard deviations and coefficients of varishyations on the basis of adjusted data 139

34 - Philippine export ratios and import ratios by commodities with the four largest and with all Partner Countries 141

10

Charts

1 - Ratio of trading partners imports from Southeast Asian Countries to corresponding exports of Southeast Asian countries 131

2 - Ratio of Southeast Asian countries imports to corresponding exports of trading partners 132

ECONOMIC INTERDEPENDENCE IN SOUTHEAST ASIA

12

I - Advantage to the Region from Economic Cooperation

One purpose of the Contract was to evaluate the economic advantage

(or disadvantage) to the region from economic cooperation and coordination

(Appendix B pp B 1-2) Our response to this injunction is given below

under seven headings A to G

A - Less Developed Country (LDC) Comparative Advantage in Manufactured

Goods with Special Reference to Southeast Asia

A basic point underlying any discussion of development policies of

LDCs is the fact that although international trade may not be serving as an engine of growth it cannot be disregarded The degree of dependence of

LDCs on international trade has been and still is typically high In

many cases exports of these countries constitute more than 15 percent

of their national income and 50 percent or more of their export earnings

is derived from one or two commodities Recurrent discussions have emanated

from the United Nations and other sources relating to the present and future

prospects of a large trade gap for less developed countries These discusshy

sions run in terms of a growing need for foreign exchange by the LDCs to

meet their economic development programs Such foreign exchange needs are

presumably to be met by exports of their traditional primary commodities

or by expanding their recent venture into trade in manufactured goods

Trade projections of prospects of world demand and potentialities

for expanding exports of traditional primary commodities conducted by the

FAO the ECAFE and others reflect very modest rates of increase over the coming decades It thus becomes of great importance for LDCs to expand

their exports of manufactured goods

To the advantage of LDCls recent trends in international trade

point to a tendency toward convergence in world specialization and exchange

Contrary to the long established dichotomy in world production and trade

between predominantly primary goods production and export by less developed

countries and manufactured goods production and export by developed

countries recent trends indicate more diverse specialization patterns

The export of manufactures by LDCs though still much concentrated in origin and destination has also Xecently exhibited high rates of growth

Despite the difficulties inherent in attempts to generalize on production possibilities for various countries including the LDCs1

various attempts have been made to assess the implications of recent developments in world trade as an indication of the possibility of the LDCs developing a comparative advantage in the production of certain manufactured goods If one is to generalize broadly on the LDC comparashytive advantage area within manufactures one must choose for both logical and empirical reasons the area of relatively low skill-labor intensive2

manufactures This gives rise to the need to apply soue theoretically sound and workable criteria for the delineation of some manufactures potentially successful for LDCs specialization and trade The choice of any such criteria would to a large extent be influenced by the nature of

the data available for LDCs

The analysis of LDCs prospective comparative advantage in the production of certain manufactured commodities thus starts with the basic assumption that the LDCs have relatively little accumulated capital in either conventional or human-skills form Hence any comparative advantage they may have in manufactures apart from the resource oriented ones arises from their abundant labor The implication then is to specialize in the prcduction of those industries with a strong labor orientation defined to incorporate low capital requirements in the forms both of plant

and eqlpment and of education and training (human capital)3

1Particularly the presence of nonmonetized sector and the rigiditiesin the structure of their economies impeding factor mobility

2The importance of the availability of different levels of laborskills as the major factor explaining the patterns of international location and trade is emphasized by Donald B Keesing Labor Skillsand International Trade Evaluating Many Trade Flows with a Single Measurshying Device Review of Economics and Statistics (August 1965) pp 287-293

3Hal B Lary Imports of Manufactures from Less Developed CountriesNational Bureau of Economic Research New York 1968 p 4

14

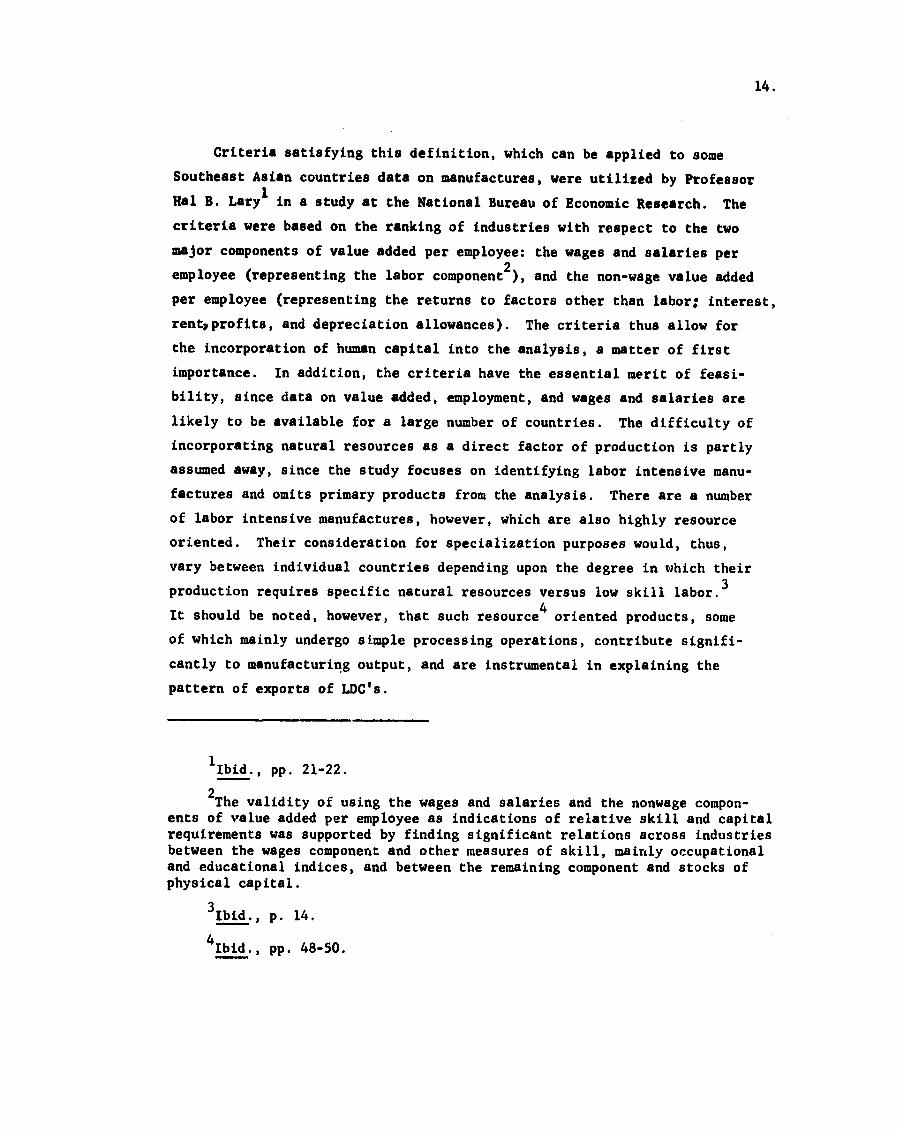

Criteria satisfying this definition which can be applied to some

Southeast Asian countries data on manufactures were utilized by Professor

Hal B Lary 1 in a study at the National Bureau of Economic Research The

criteria were based on the ranking of industries with respect to the two

major components of value added per employee the wages and salaries per

employee (representing the labor component2) and the non-wage value added

per employee (representing the returns to factors other than labor interest

rentpprofits and depreciation allowances) The criteria thus allow for

the incorporation of human capital into the analysis a matter of first

importance In addition the criteria have the essential merit of feasishy

bility since data on value added employment and wages and salaries are

likely to be available for a large number of countries The difficulty of

incorporating natural resources as a direct factor of production is partly

assumed away since the study focuses on identifying labor intensive manushy

factures and omits primary products from the analysis There are a number

of labor intensive manufactures however which are also highly resource

oriented Their consideration for specialization purposes would thus

vary between individual countries depending upon the degree in which their

production requires specific natural resources versus low skill labor3

It should be noted however that such resource4 oriented products some

of which mainly undergo simple processing operations contribute signifishy

cantly to manufacturing output and are instrumental in explaining the

pattern of exports of LDCs

1lbid pp 21-22

2The validity of using the wages and salaries and the nonwage componshyents of value added per employee as indications of relative skill and capital requirements was supported by finding significant relations across industries between the wages component and other measures of skill mainly occupational and educational indices and between the remaining component and stocks of physical capital

3Ibid p 14

4Ibid pp 48-50

15

The entire analysis rests on the factor proportions theory with its underlying assumption of the comparability of the factor intensities for different countries It aloo assumes the possibility of approximating empirically to the Heckcher-Ohlin version of the theory of comparative advantage and the nonexistence or at least the practical irrelevance

of factor intensity reversal1

Because of the importance of the assumptions underlying the factor proportions theory in the specification of those manufactures potentially profitable for LDCs further research was undertaken in the NBER study on those points Comparison of value added per employee and its components for nine countries2 over the thirteen industry groups appearing in the UN The Growth of World Industry3 indicated a high degree of conformity as measured by Kendalls coefficient of concordance Thus based on the analysis of value added and its components for array of US iniustries the study pointed that the LDCs should have comparative advantage in manufactures which have (1) a low level of value added per employee and (2) low levels of both components of value added wages and salaries per employee and other remaining components These manufactures were found to be textiles and clothing wood products furniture leather products miscellaneous manufactures and a number of special manufactures in other

1Some qualifications result from studies by W Leontief Domestic Production and Foreign Trade The American Capital Position ReexaminedProceedings of the American Philosophical Society Sept 1953 In a secondarticle however Leontief put more emphasis on the skill requirements forthe different industries--a factor which is excluded in analysis based on examination of stocks of physical capital and man hours of labor W Leontief Factor Proportions and the Structure of American Trade Further Theoretical and Empirical Analysis Review of Economics and StatisticsNovember 1956 It should also be noted that in one of the calculations inwhich Leontief excluded natural resource sectors the paradox disappearedthe US was found to export more capital intensive products

BS Minhas The Homohypallagic Production Function Factor IntensityReversal and the H-O Theorem Journal of Political Economy April 1962Hinhas introduces the CES production function which permits the occurrenceof factor intensity reversal and points to the existence of some factor reversals Leontief however conducted more extensive tests and confirmed the empirical irrelevance of factor reversal W Leontief International Factor Costs and Factor Use AER June 1964

2United States Canada Australia Sweden United Kingdom BrazilJapan Mexico and India Lary opcit p 71

3United Nations TheGrowth of World Industry 1936-1961 National Tables (United Nations 1963)

16 1

major groups

1 Similarities in Manufactures Production Structure

Applying the criteria based on analysis of value added per employee to

data on manufactures for selected Southeast Asian countries yields results

generally in agreement with the NBER study findings Detailed analysis of

individual groups of manufactures however indicates somewhat wider possibilshy

ities for specialization

In general as shown in Table 2 there was much similarity in the rankshy

ings of the different manufacturing groups for the countries considered

The Kendall coefficient of concordance2 and the chi square test computed for six Southeast Asian countries over twenty industry groups for 1963 and for

the same countries plus Japan over eighteen industry groups yielded results

significant at the 001 confidence level The results of this test are in

Table 3 below

The major groups of manufactures that satisfied the relatively low

skill labor criteria 3 for practically all of the countries considered were

1Examples of such manufactures are plastic goods footwear glasswearand china jewelry optical goods cutlery aad hardware electrical apparatus and appliances non electrical machinery printed matter and processing and preserving of fish and fruits and vegetables

2The Kendall coefficient of concordance provides a measure of the relashytion among several rankings of N variables ie determines the association among N variables It constitutes an index of the divergence of the actual agreement shown in the data from the maximum possible (perfect) agreement See Sidney Siegel Nonparametric Statistics for the Behavioral Sciences (New York McGraw Hill Book Company Inc 1956) pp 229-239

3The relatively low skill labor manufactures are defined as those manufactures having (1) relatively low value added per employee below the overall average for the manufacturing sector of each country and (2) levels of both wages and salaries per employee and non-wage value added per employee below the overall average

17

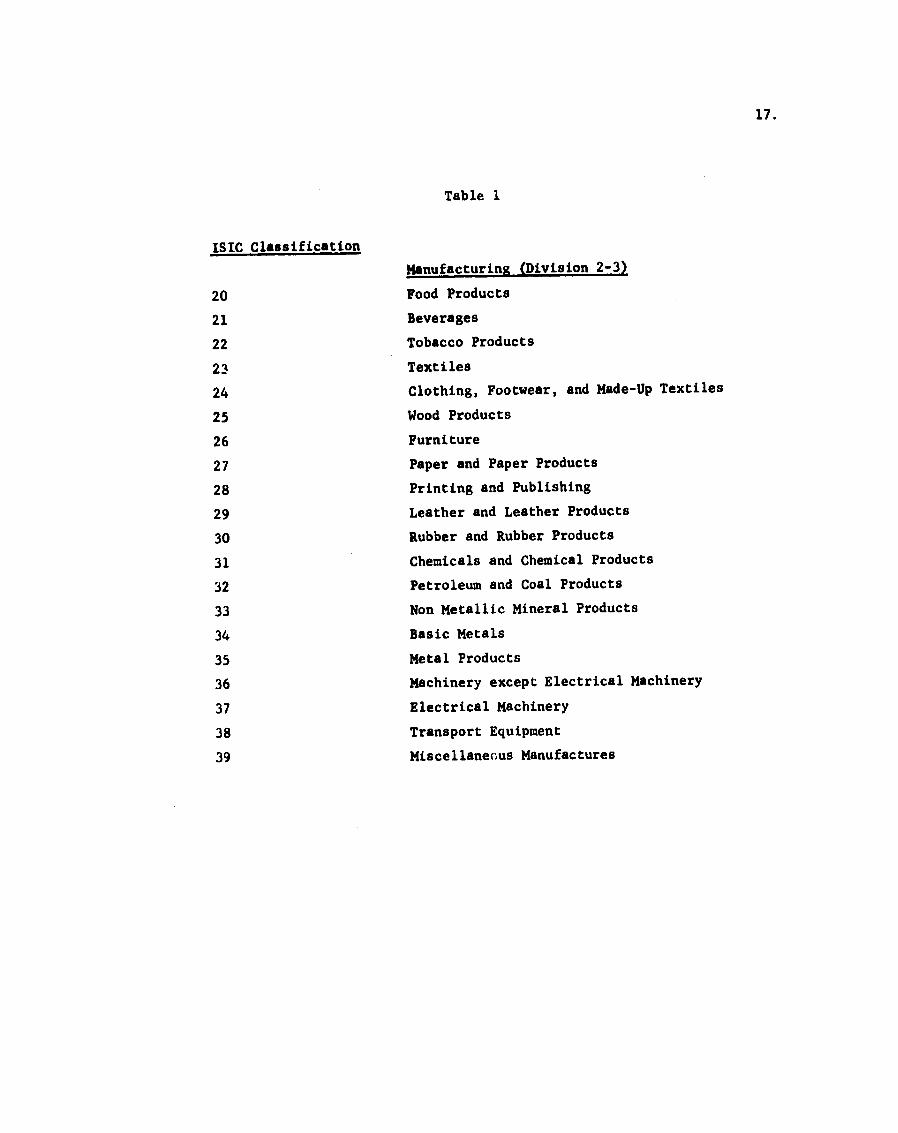

ISIC Classification

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

Table 1

Manufacturing (Division 2-3)

Food Products

Beverages

Tobacco Products

Textiles

Clothing Footwear and Made-Up Textiles

Wood Products

Furniture

Paper and Paper Products

Printing and Publishing

Leather and Leather Products

Rubber and Rubber Products

Chemicals and Chemical Products

Petroleum and Coal Products

Non Metallic Mineral Products

Basic Metals

Metal Products

Machinery except Electrical Machinery

Electrical Machinery

Transport Equipment

Miscellaneous Manufactures

Table 2 -- Indices of ValueAdded per Employee Wages and Salaries per Employee and Non-WageValue-Added per Employee for Manufactures in Selected Southeast Asian Countries (ISIC 2-3 =_ 100) 1963 (r)

ISIC _(2-3) 20 21 22 23 24 25 26 27 28 29Value Added Per Employee (2)Japan(2) Taiwan India Rep of

10000 10000 10000 10000

9130 11555 9082 10289

12826 40360 14289 23782

---67741 6301

60326

6413 5521 8165 6220

5326 6034 6420 5948

5869 6185 6390

11514

6739 6963 7662 5693

10869 9297 12751 13516

11739 4079 9319

10102

8913 8311 7396 6664

Korea Singapore 10000 Malaysia(5) 10000

6657 9080

16699 11900

21994 13800

3834(3) 6660 7260

6053 8260

9620 6400

5898 10320

9564 8600

6320 7000

(West)Philippines 10000 12850

(6)15812 9878 4990 3480 5027 3613 9900 5856 4839

Wages amp Salaries Per Employee (2)Japan 10000 7575 8484 --- 7272 6363 7575 8484 10606 13333 10303Taiwan 10000 9285 12857 15357 7619 6904 9166 7380 11428 10238 9285India 10000 6354 8125 5208 9843 9270 5833 8958 10312 10989 7291Rep of 10000 8195 11403 17807 8254 8490 11341 8910 10609 14110 10699Korea (3)Singapore 10000 7975 8947 6396 5384 10242 13279 5668 11740 6072

Malaysia (5) (6)(West) 10000 8901 10989 7637 7307 7472 11263 7472 8241 12582 5494Philippines 10000 9185 14253 7466 7828 5610 8099 7918 11538 13212 8325

Non Wage Value Added Per EmployeeJapan 10000 10000 15254 593252) 4745 4915 5762 11016 10847 8135Taiwan 10000 11959 45450 7500 5112 5855 5608 6869 8873 2905 8108India 10000 12671 22397 7739 5958 2671 7123 5958 15958 7123 7534 Rep of

Korea 10000 11034 18185 75451 5496 5044 11576 4549 14550 8676 5229Singapore 10000 5956 t0817 30279 3010(3) 3827 7677 6021 8408 6451 Malaysia(5) (6)

(West) 10000 9182 12421 17327 6289 7138 6540 5786 11509 6320 7661Philippines 10000 14035 16315 10657 4078 2792 4035 2222 9371 3479 3713Source Data calculated from United Nations The Growth of World Industry (United Nations 1968) (1) Figures for the Philippines and India refers to 1962 and figures for Taiwan refer to 1961 (2) Data excludes tobacco manufacturers (ISIC22)(3) figure stands for textiles clothing and footwear (ISIC 23 and 24)

Table 2 ------- continued

ISIC 30 31 32 33 34 35 36 37 38 39Value Added Per Employeejapan(Z) 9239 18804 22826 10217 11304 8804 10217 10434 12934 8260Taiwan 8899 11593 25578 8804 14857 8045 5939 7988India 6660 899423698 23254 55502 8816 10917 10562 11183Rep of 11745 10177 89056029 14707 6743 10706 10366 6341 6395 9121 6430 5561 KoreaSingapore 8820 27247(4) 11179 17556 9873 7668 9522Malaysia(5) 8820 19440 7500 5407

(6) 11000 10280 8400 6820 15660 7500 30400(6)(West)Philippines 14607 15524 17690 11270 8320 8265 11911 9215 10994 5038Wages amp Salaries Per EmployeeJapan 9090 13030 14242 9696 14242 10000 11818 9696 12727Taiwan 90909404 12500 13095 10119 15714 9166 11071 10238 13333India 833316041 13281 27083 7552 12604 10312 11458Rep of 11718 11979 92189274 11974 8825 11847 12308 8476 10540 9801 13196 6943Korea (4)Singapore b23 13157 10688 10121 9757 10890 15870 12550 6356

Malaysia(5)(West) 9010 11648 (6) 10000 11758 9340 10439 11868 11978Philippines 11312 15610 16813 (6)29004 11493 10995 11085 12714 10361 12398 8235Non Wage Value Added Per EmployeeJapan

Taiwan India

9322 8783 33767

22033 11396 36369

27627 27882 92876

10508 8536

10479

9661 8135 9322 14662 7815 4954 8698 10890 10821

10847 13050 7554 5382

11780 7808

7796 9099 8493

Rep of Korea

Singapore 4874 8924

15679 6002 34731(4)

10300 11440

9676 21505

5582 9935

4921 5956

8879 6150

4024 4817

5069 4903

Malaysia(West) 8710

Philippines 15672 23899 (6) 15497 186038

11572 11198

9433 7456

7861 4748 7353 11652

17830 4937 8845 10540

38176(6) 4005

(4) figure stands for chemical and petroleum products (ISIC 31 and 32)(5) Data for Malaysia excludes tailors and dressmakers (part of ISIC 24) in smelting industry(part of ISIC 342) motor vehicles and bicycle repair shops (ISIC 384 and 385) goldsmithing(part of ISIC 394) and processing of agricultural products on estates comprising tea factories(part of ISIC 209) rubber processing on estates (part of ISIC 30) and copra kilns and palm

(6) oil milling (part of ISIC 312)Breweries and manufacturing of malt (ISIC 213) and manufactures of products of petroleumand coal (ISIC 32) are included under miscellaneous manufacturing industries (ISIC 39)

4 ~ ~v-gt 444 420~

~ ~ ~ ~ ~ ~~~~~~ ~

r 1963 data 0203 707244cou

gt 41e 44gt~ 4 ii iltlii ]IIR ii 1 144 4

Tile 44144 os Cocodnc eaursth CefCon onisecy rakfgt4 Of

Ii i ]CoFffice41t itC of h 4gt

(for seven Co 1963=iiL 60 8 7 n ris data)i

44t e nt s- on c lt4444v gt-4c KI19 6 pp 4 lt29-4 )Y~~ 4

~~lt4441~ ~ ~~ K - 1I 44 4 44 44KK

an Concardanccluduare

4it a p i f chanc o e4 (S SL441 e

ab r o f n un r es c nc rn d f r te 11ii th ve sh wn - h l am c CIiLIS111=

d~isa r em n iwoul Chi All e nde lsbe 0iltii~iii 7-~ theii Sq a a i r r

CulatedI )i over Itwenty industrial groupsiifor i i Fo Se ton l~ of the ta le th ab v co ntie Jap IltF ei IIILIS + [+

incude Ther areiover~lI eihte inutilgois rus2

21

similarly those of textiles (23) clothing and apparel (24) wood and wood products (25) furniture (26) leather and leather products (29) and miscellaneous manufactures (39)

In addition other groups of manufactures have alsc exhibited relatively low capital requirements measured by low indices of valueshyadded-per-employee and non-wage-value-added-per-employee These groups were mainly printing and publishing (28) metallic products (35) nonshyelectric machinery (36) and transport equipment (38) Such low indices also appeared for individual countries in groups (37) of electrical

machinery (34) of basic metals (33) of non-metal mineral products and (20) of food products The finding therefore encourages these countries to expand the production and export of some manufactures within the specified groups However wages and salaries were higher for groups 28 35 36 and 38 than for groups 23 24 25 26 and 39 suggesting somewhat high skill requirements The difference might however have reflected heterogeneity in groups 35 36 and 38 or in the other groups Hence a detailed study of two of the countries the Philippines and Malaysia I was

carried out

Our detailed analysis of manufacturing sectors in the Philippines

and Malaysia gives support to favoring disaggregated consideration of LDC specialization in manufacturei production In addition to manufactures in groups 23 24 25 26 and 29 all of which generally satisfy the criteria both of low-value-added-per employee and low wages and salaries and non-wages-added-per-employee there are subgroups here and there in virtually all of the remaining manufacture categories that show the same

characteristics

1Bureau of the Census and Statistics Annual Survey of Manufactures1960 Volume V (Manila Philippines 1962) and

Department of Statistics of Malaysia Census of ManufacturingIndustries in the States of Malaya 1963 (Kuala Lumpur Malaysia 1965)

22

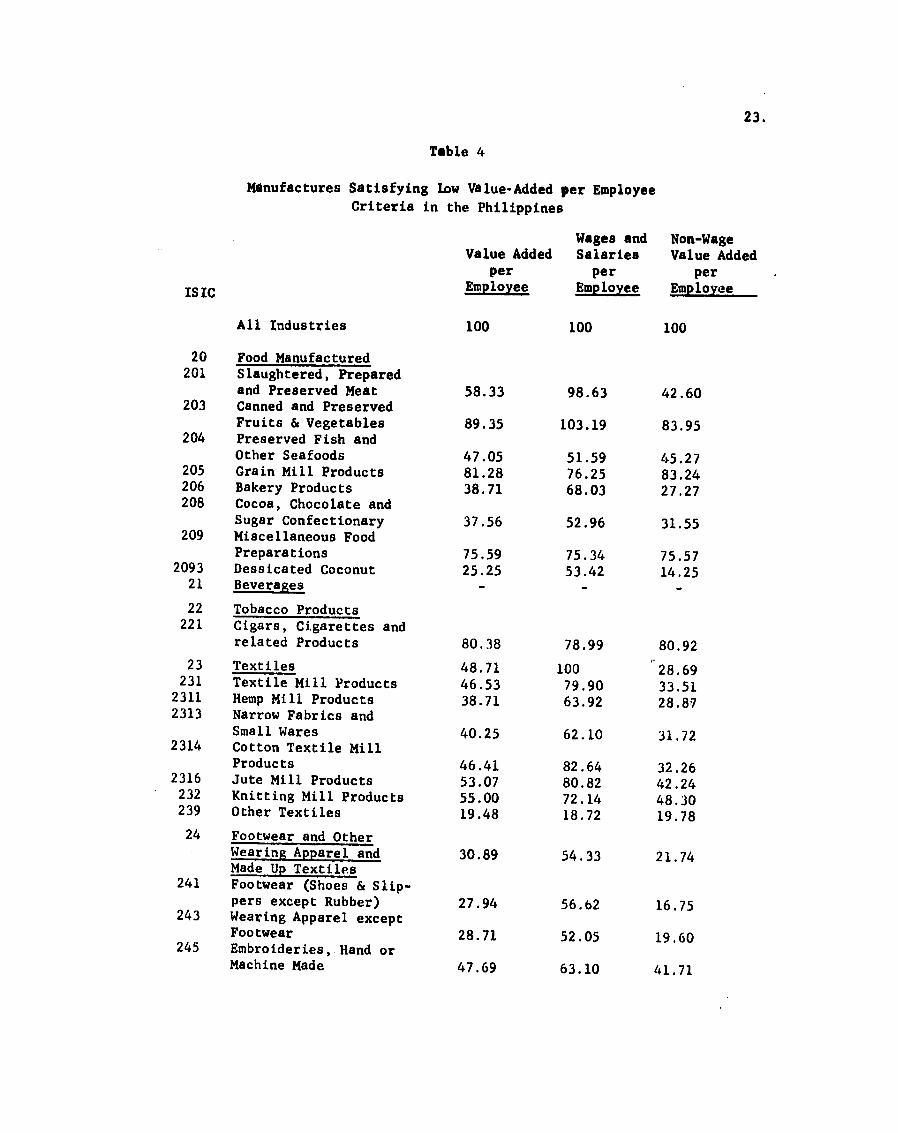

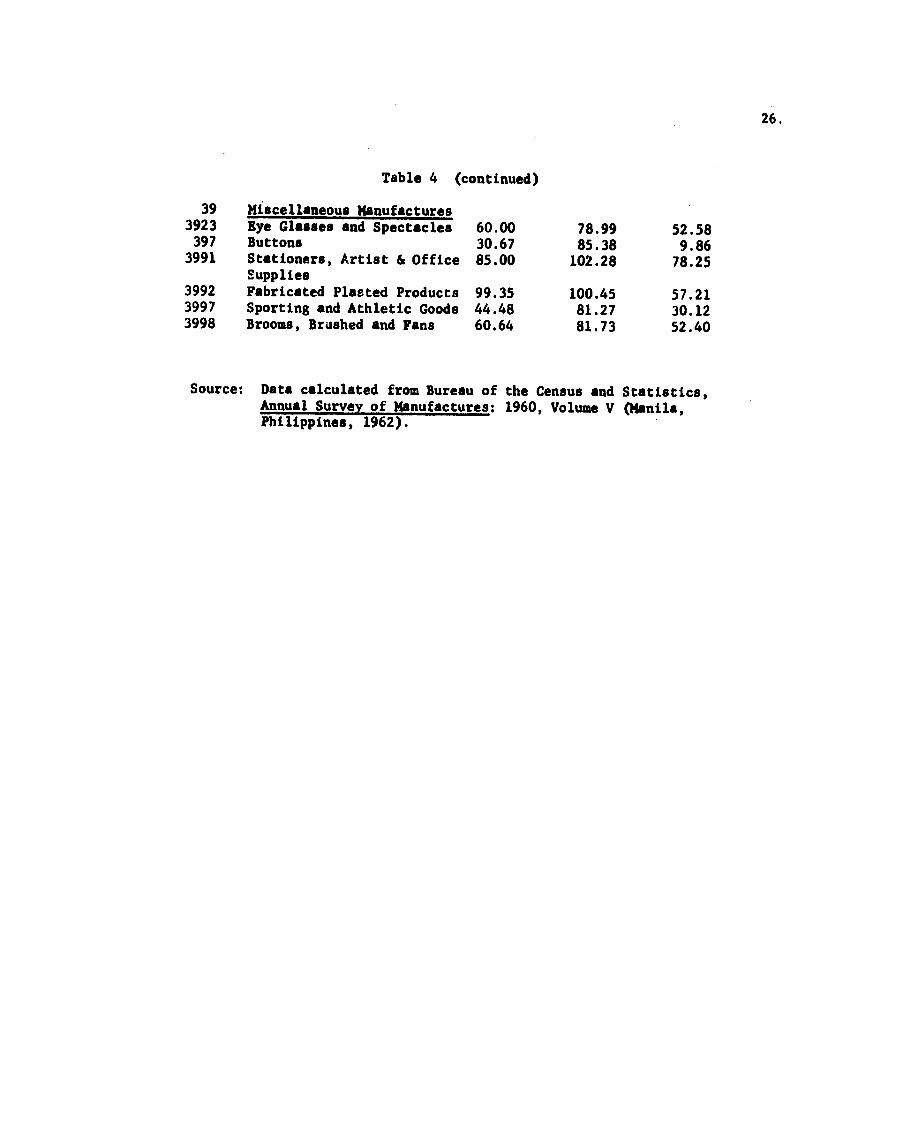

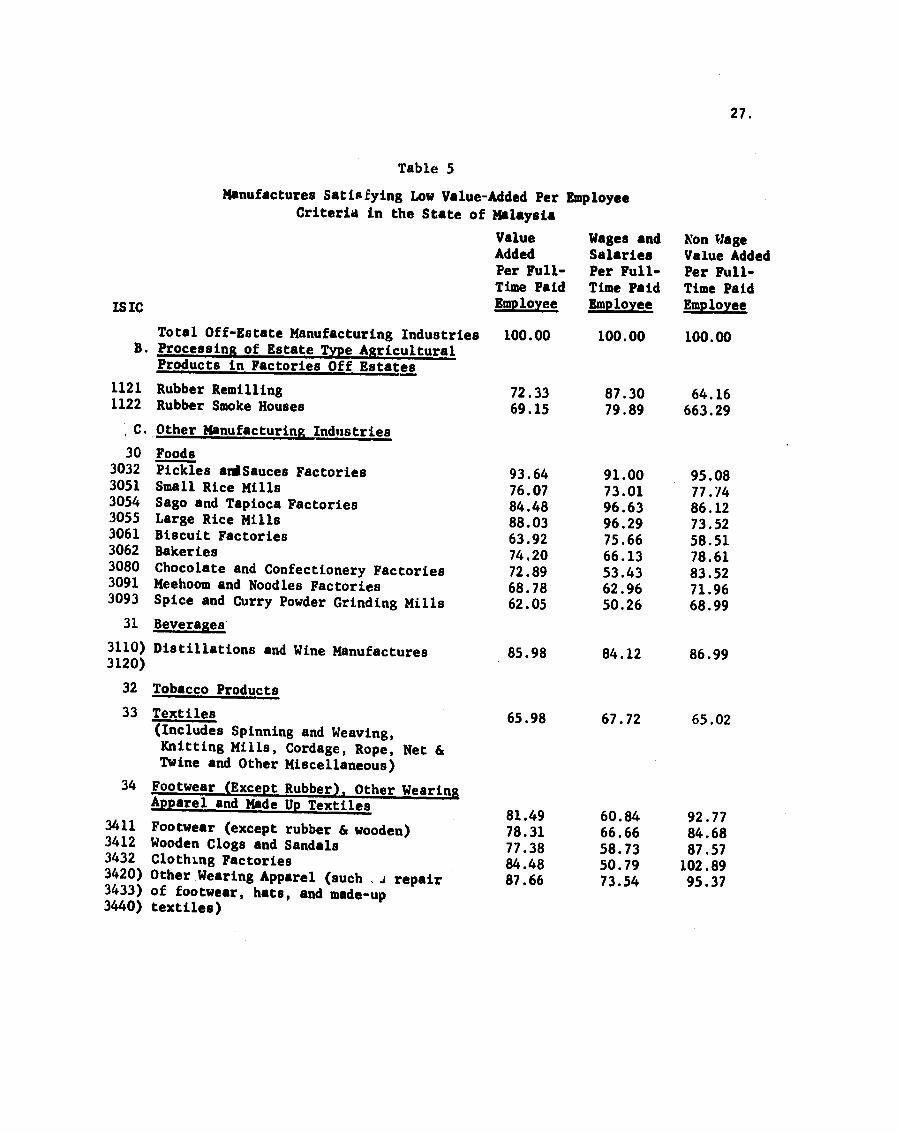

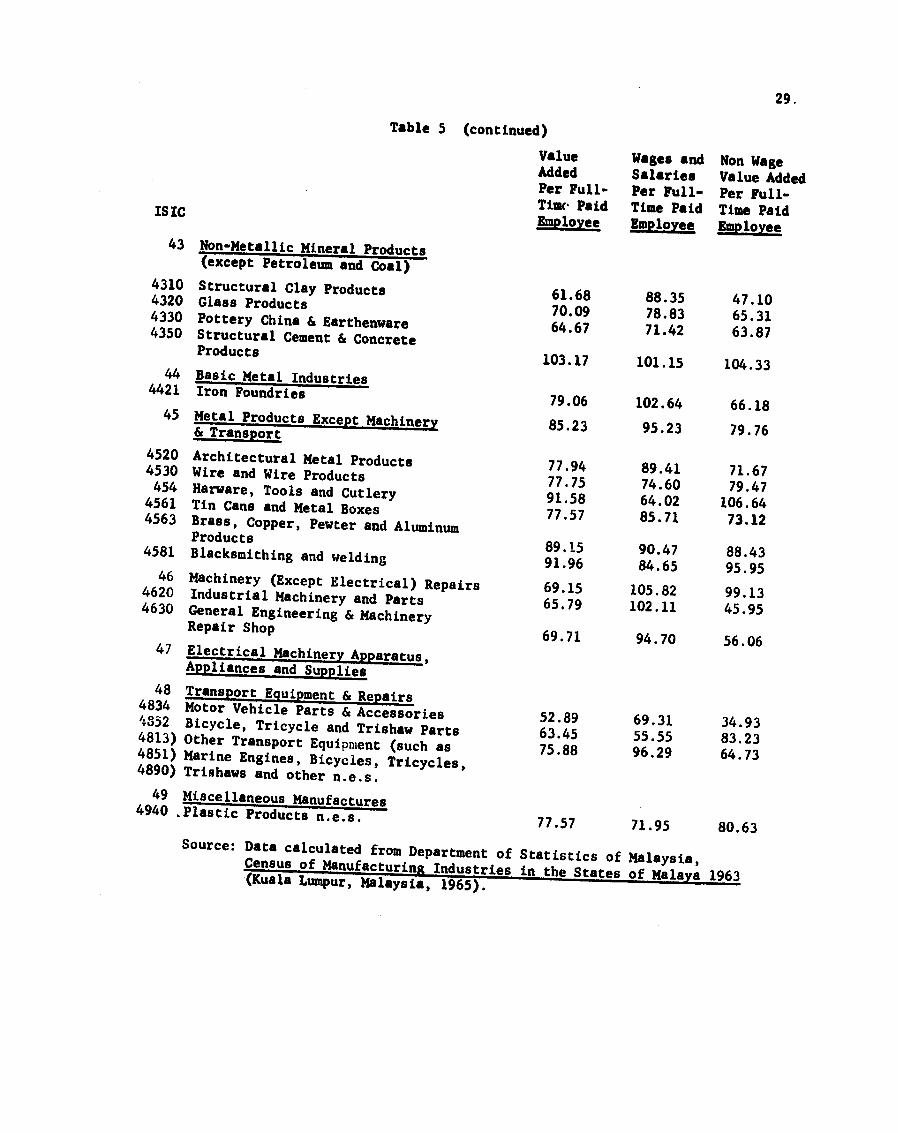

We list below in Tables 4 and 5 those manufactures for the Philippines and Malaysia that qualify by the above criteria and so invite considerations as serious candidates for LDC production It is interesting to note that the manufactures listed below to a very large extent encompass those identified as labor intensive in the study sumnarized in Table 2 It is important to emphashysize however the wider possibilities for specialization that emerge from examination of individual LDC data on manufactures

23

Table 4

Manufactures Satisfying Low Value-Added per Employee Criteria in the Philippines

Wages and Non-Wage Value Added Salaries Value Added

per per per ISIC Employee Employee Employee

All Industries 100 100 100

20 Food Manufactured 201 Slaughtered Prepared

and Preserved Meat 5833 9863 4260 203 Canned and Preserved

Fruits amp Vegetables 8935 10319 8395 204 Preserved Fish and

205 Other Seafoods Grain Mill Products

4705 8128

5159 7625

4527 8324

206 Bakery Products 3871 6803 2727 208 Cocoa Chocolate and

Sugar Confectionary 3756 5296 3155 209 Miscellaneous Food

2093 Preparations Dessicated Coconut

7559 2525

7534 5342

7557 1425

21 Beverages - -

22 Tobacco Products 221 Cigars Cigarettes and

related Products 8038 7899 8092 23 Textiles 4871 100 2869

231 Textile Mill Products 4653 7990 3351 2311 Hemp Mill Products 3871 6392 2887 2313 Narrow Fabrics and

Small Wares 4025 6210 3172 2314 Cotton Textile Mill

2316 Products Jute Mill Products

4641 5307

8264 8082

3226 4224

232 Knitting Mill Products 5500 7214 4830 239 Other Textiles 1948 1872 1978

24 Footwear and Other Wearing Apparel and 3089 5433 2174 Made Up Textiles

241 Footwear (Shoes amp Slipshypers except Rubber) 2794 5662 1675

243 Wearing Apparel except Footwear 2871 5205 1960

245 Embroideries Hand or Machine Made 4769 6310 4171

24 Table 4 (continued)

25 Wood and Cork Products 4525 8127 3119 Except Furniture

251 2521 2551

Sawmill and Planning Mill Veneer and Plywood Sawah Nipa and Bamboo

4641 4576

3051

8127 8584

6712

3279 3012

1622 26

2611 2621

2631

2641

2661

Furniture and Fixtures Rattan Furniture except Wood Furniture except Upholstered Venetian Blinds and Other Screens Metal Furniture except Upholstered Mattresses and Bedshy

4217 2294

3384

4500

4102

7397 4931

7351

8310

8401

2976 1264

1836

3012

2424

Springs 6743 7579 6417

27 Paper and Paper Products 28 Printed and Published

2821 Materials (mainly) Books and Pamphlets 8987 9771 8680

29 Leather Products

2911

2921

except Footwear Leather Tanned or Finished Luggage Handbags and Small Leathergoods

4961

5076

5205

7534

7945

7214

3957

3957

4420

30 3011 309

Rubber Products (mainly)Rubber Shoes and Slippers Miscellaneous Rubber

6384 10000 4973

Products 5987 10365 4278

31 Chemicals and Chemical

3121 Products (mainly)Vegetables Oils 7705 10182 6737

32 Products of Petroleum and Coal (combined with ISIC 39 of Miscellaneous)

33 Non-Metallic Mineral

331

Products (mainly) except Products of Petroshyleum and Coal Strictural Clay Products 5487 8082 4474

339 Other Non-Metallic Mineral Products such as statuary conshycrete lime statuary

8995 6269 5204

25

Table 4 (continued)

art goods and cut stone products

34 3412

Basic Metal Products (mainly) Iron and steel FoundryProducts 6346 9223 5222

35

351

Metal Products Except Machinery and Transport Equipment Tin and Aluminum Ware

352 356

3561

3563

3594

36

(except household and hospital utensils)

Cutlery and Hand Tools Heating Cooking and Plumbing Equipment Heating and Cooking Appashyratus Metal Plumbing Fixtures and Fittings Needles Pins and Fasteners Machinery Except electrishy

6192

4769

5217

3628

6820

6347

9041

9315

8401

9817

6131

3101

3618

1764

5650

364 3641

365

369

cal (mainly)Special Industry Machinery Food Products Machinery and Euipment General Industrial Machinery amp Equipment Other Machinery

5230

4282

3282 5487

9452

9269

7853 10228

3582

2335

1497 3636

37

371

Electrical Machinery Apparatus Appliance and Supplies Electrical Industrial

8474 10410 7718

3711 3712

Apparatus Motors and Generators Electrical Distribution

6269 3461

7808 7260

5668 1978

3722

3741

3749

and Control Apparatus 7641 Household Radios Phonogrpahs amp TV Sets 6769 Household Cooking amp Heating Equipment 3858 Other Household Electrical

8036

9817

7990

7486

5579

2245

Appliances 7346 9908 6345 38

381 3832

3841

3851

Transportation EquipmentShipbuilding and Repairing Motor Vehicle Engines Parts amp Bodies Motor Vehicles Repair shop Products Bicycles

3333

4858

5730 5384

10000

8767

10365 9132

730

3333

3921 3921

26

Table 4 (continued)

39 Miscellaneous Manufactures 3923 Eye Glasses and Spectacles 6000 7899 5258 397 Buttons 3067 8538 986

3991 Stationers Artist amp Office 8500 10228 7825 Supplies

3992 Fabricated Platted Products 9935 10045 5721 3997 Sporting and Athletic Goods 4448 8127 3012 3998 Brooms Brushed and Fans 6064 8173 5240

Source Data calculated from Bureau of the Census and Statistics Annual Survey of Manufactures 1960 Volume V (Manila Philippines 1962)

27

Table 5

Manufactures Satisfying Low Value-Added Per Employee Criteria in the State of Malaysia

Value Wages and Non Wage Added Salaries Value Added Per Full- Per Full- Per Full-Time Paid Time Paid Time Paid

IS IC Employee Employee Employee

Total Off-Estate Manufacturing Industries B Processing of Estate Type Agricultural

10000 10000 10000

Products in Factories Off Estates 1121 Rubber Remilling 7233 8730 6416 1122 Rubber Smoke Houses 6915 7989 66329

C Other Manufacturing Industries

30 Foods 3032 3051 3054 3055 3061 3062 3080 3091 3093

Pickles andSauces Factories Small Rice Mills Sago and Tapioca Factories Large Rice Mills Biscuit Factories Bakeries Chocolate and Confectionery Factories Meehoom and Noodles Factories Spice and Curry Powder Grinding Mills

9364 7607 8448 8803 6392 7420 7289 6878 6205

9100 7301 9663 9629 7566 6613 5343 6296 5026

9508 7774 8612 7352 5851 7861 8352 7196 6899

31 Beverages

3110) Distillations and Wine Manufactures 8598 8412 8699 3120)

32 Tobacco Products

33 Textiles 6598 6772 6502 (Includes Spinning and WeavingKnitting Mills Cordage Rope Net amp Twine and Other Miscellaneous)

34 Footwear (Except Rubber) Other WearingApparel and Made Up Textiles 8149 6084 9277

3411 Footwear (except rubber amp wooden)3412 Wooden Clogs and Sandals 3432 Clothing Factories 3420) Other Wearing Apparel (such _j repair

7831 7738 8448 8766

6666 5873 5079 7354

8468 8757 10289 9537

3433) of footwear hats and made-up 3440) textiles)

28

Table 5 (continued)

Value Added Per Full-

Wages and Salaries Per Full-

Non Wage Value Added Per Full-

ISIC Time Paid Employee

Time Paid Employee

Time Paid Employee

35 Wood Rattan Mena and Cork

Kuang Attap

3531 3591

Wooden Boxes Cases and Crates Carpentary Shops Other Wood Products (such as Wood Preserved Rattan Processing Basketware Attap Products and other wood and Cork Products

5700 8485

7345

7195 5978

9841

4884 9855

5982

36 Furniture and Fixtures includes

6728 7513 6300

361) Household Furniture 362) Office and Connercial Furniture 367) Furniture Finishing and Repairing 364) Mattress Manufacturing 369) Other Miscellaneous Manufacture of

Furniture

37 Paper and Paper Products

38 Printing and Publishing 382 Job Printing Bookbinding amp Printing

Service 7289 8730 6502

39 Leather and Leather Products except Footwear and Wearing Apparel 7570 5291 8815

40 Rubber Products 4010) Rubber Products except Retreading and 4021) Vulcanizing of Tires and Tubes (inshy

cludes 4030) rubber footwear tires and tubes

foam

6485 8095 5606

4090) rubber products amp other Miscellaneous

41 4195

Chemicals and Chemical Products Matches

6093 9084 6300

42 Coal and Petroleum Products (included Under All Other Industries)

29

Table 5 (continued)

Value Added Per Full-

Wages and Salaries Per Full-

Non Wage Value Added Per Full-

ISIC Timc Paid Time Paid Time Paid Employee Employee Employee

43 Non-Metallic Mineral Products

4310 4320 4330

4350

(except Petroleum and Coal) Structural Clay Products Glass Products Pottery China amp Earthenware Structural Cement amp ConcreteProducts

6168 7009 6467

8835 7883 7142

4710 6531 6387

10317 10115 10433 44 BasicMetal Industries

4421

45

Iron Foundries

Metal Products Except Machinery amp Transport

7906

8523 10264

9523 6618

7976

4520 Architectural Metal Products 4530 Wire and Wire Products 454 Harware Tools and Cutlery

4561 Tin Cans and Metal Boxes 4563 Brass Copper Pewter and AluminumProducts

7794 7775 9158 7757

8941 7460 6402 8571

7167 7947

10664 7312

4581

46 4620

4630

Blacksmithing and welding Machinery (Except Electrical) RepairsIndustrial Machinery and Parts General Engineering amp MachineryRepair Shop

8915 9196

6915 6579

6971

9047 8465

10582 10211

9470

8843 9595

9913 4595

5606 47 Electrical Machinery Apparatus

Appliances and Supplies 48 Transport Equipment amp Repairs4834 Motor Vehicle Parts amp Accessories

4332 Bicycle Tricycle and Trishaw Parts4813) Other Transport Equipment (such as 4851) Marine Engines Bicycles Tricycles4890) Trishaws and other nes

5289 6345 7588

6931 5555 9629

3493 8323 6473

49 Miscellaneous Manufactures4940 Plastic Products nes 7757 7195 8063 Source Data calculated from Department of Statistics of Malaysia

Census of Manufacturing Industries in the StatesofMalaya1963(Kuala Lumpur Malaysia 1965)

30

2 Implications Export Performance

For the purpose of estimating comparative advantage possibilities available data suffer sharply from their aggregation--that isthey suffer from the heterogeneity of products included under a given classification Guidance is needed for very specific kinds of specialization But aggregated data lead only to rough guidelines and if the rules of behavior and parashymeter shifts of individual segments happen to combine malevolently aggregated data can lead to generalizations inverse to the real facts

The problem we face in trade matters stems from definitions of products that are heterogeneous with respect to factor requirements We should be on guard LDCs in general and Southeast Asian countries in particular may be able to specialize efficLently in the production of a large variety of manushyfactures that are labor intensive and require only modest skills irrespective of the general group within which they fall

Greater awareness of this diversity would free policy in thesecountries toward a wider area of choice and greater degree of adaptability It would also enable them to take advantage of favorable export prospects among the more numerous plausible sub-groups of manufactures

It is a major complaint of LDCs that world demand for their traditional primary exports is unpromising Preoccupation with only a few manufactures which alone are supposed to have export potential risks earning the same disappointment There are valid factor-supply reasons for considering a wide range of industries and sub-industries and of course also on tle demand side their long-run demand prospects

A study of future prospects of world trade in manufactures by Maizels1 has projected a declining share of textiles and clothing2 and other miscellshyaneous manufactures for industrial semi-industrial and non-industrial

IAlfred Maizels Industrial Growth and World Trade (Cambridge CambridgeUniversity Press 1963) pp 402-406

2The share of textile and clothing exports as a percentage of world trade in manufactures declined from 20 in 1937 to 10 in 1959 and is projected todecline further to only 5 by 1970-75

31

countries between the years 1959 and 1970-75 At the same time capital goods and chemical products were projected to attain an increasing share of total imports of virtually all countriesI

A survey of the export(1) performance of nine Asian countries -Singapore Malaya Philippines Hong Kong Taiwan India Pakistan Thailand and also the Republic of Korea - tends to support the arguments so advanced The ast general tendency is that although primary products still constitute the highest percentage of total exports they are a declining share As is shown in Table 6 the percentage share of SITC groups (0-2) that is food beverages tobacco and crude materials has declined from 59 percent of the value of total exports of the nine countries in 1962 to 53 percent in 1965 The largest decline has been for SITC 2 (crude materials) partially as a result of the decline in the export prices of such products as natural rubber Expanding products in this group are oil seeds nuts and kernels wood lumber and cork and crude fertilizers SITC group 0 (food and live animals) has almost maintained its share of total exports between 1962 and 1965 at 22 percent This is partly a result of the high rates of growth of the exports of such processed food products as fish and preparations cereals and preparashytions fruits and vegetables (almost half of its export proceeds from canned and preserved fruits and vegetables) and animal feeding stuff Such products as sugar coffee and tea have shown either very low rates of increase or a declining trend

SITC groups 3-5 (animal and vegtable oils and fats chemical proshyducts and petroleum and coal products) have remained stable maintaining a 7 percent share of the value of total exports with petroleum and its products contributing almost 4 percent The most rapidly growing was SITC 4 (vegetable oils and fats) rising by 455 percent between 1962 and 1965 Exports of chemical products increased by 345 percent and petroleum and products by 14 percent

1Harry Johnson includes such goods among others as manufactures ofexport interest to less developed countries Harry G Johnson EconomicPoliciesTowardLess Developed Countries (New York Frederick A Praeger1967) pp 174-75

(1)From United Nations Commodity Trade Statistics 1965 and UnitedNations Foreign Trade Statistics of Asia and the Far East 1962

32

Table 6

Export Performance of Nine Asian Countries 1962-65

SITC Composition Z Rate of Growth

1962 1965 1962-1965

(0 1 amp 2) 5900 5336 1421

0 Food and Live Animals 2258 2187 2227

1 Beverages and Tobacco 152 136 1314

2 Crude Materials 3489 3012 905

(3 4 amp 5) 708 707 2605

3 Mineral Fuels 386 349 1415

4 Animal and Vegetable 170 196 4553

5 Chemicals 151 161 3453

(6 7 amp 8) 3287 3778 4517

6 Basic Manufactures 2184 2384 3786

7 Machinery and Transport 304 334 3873

8 Miscellaneous Manufactures 798 1059 6763

33

SITC groups 6 7 and 8 encompassing the bulk of manufactured exports-shybasic manufactures machinery and transport equipment and miscellaneous manufactures have gained an increasing share rising from 33 percent in 1962 to 38 percent in 1965 The largest contribution is made by SITC group 6 (basic manufactures) which accounted for 238 percent of total exports in 1965 The most important product under this group is textile yarn and fabshyrics (14) with India Pakistan and Hong Kong followed by Taiwan and Singashypore supplying the largest proportion of its exports SITC 68 of nonferrous metals is the second in significance (45) with tin mainly originating from Malaysia Other important products are wood manufactures mainly suppliedby Philippines Taiwan Korea and Singapore Ocnmetal mineral manufactures mainly originating from India Singapore Taiwan Hong Kong and Thailand iron and steel products from India Singapore Korea and Taiwan leather products basically from India and Pakistan metal products from Hong KongSingapore India Taiwan and Malaya and rubber manufactures from Malaya India and Singapore

SITC group 7 (machinery and transport equipment) constituted 33 pershycent in 1965 and increased by 387 percent between 1962 and 1965 with exshyports of electrical and nonelectrical machinery rising at a higher rate than exports of transport equipment Exports of SITC 8 (iniscellaneous manushyfactures) exhibited the highest rate of growth 676 percent betweeki the two years and contributed 106 percent of total exports in 1965 The most important product in this group was clothing followed by toys and sportinggoods footwear plumbing heating and lighting equipment furniture printshyed ratter and articles of plastic Most of the exports of this group origshyinated from Hong Kong

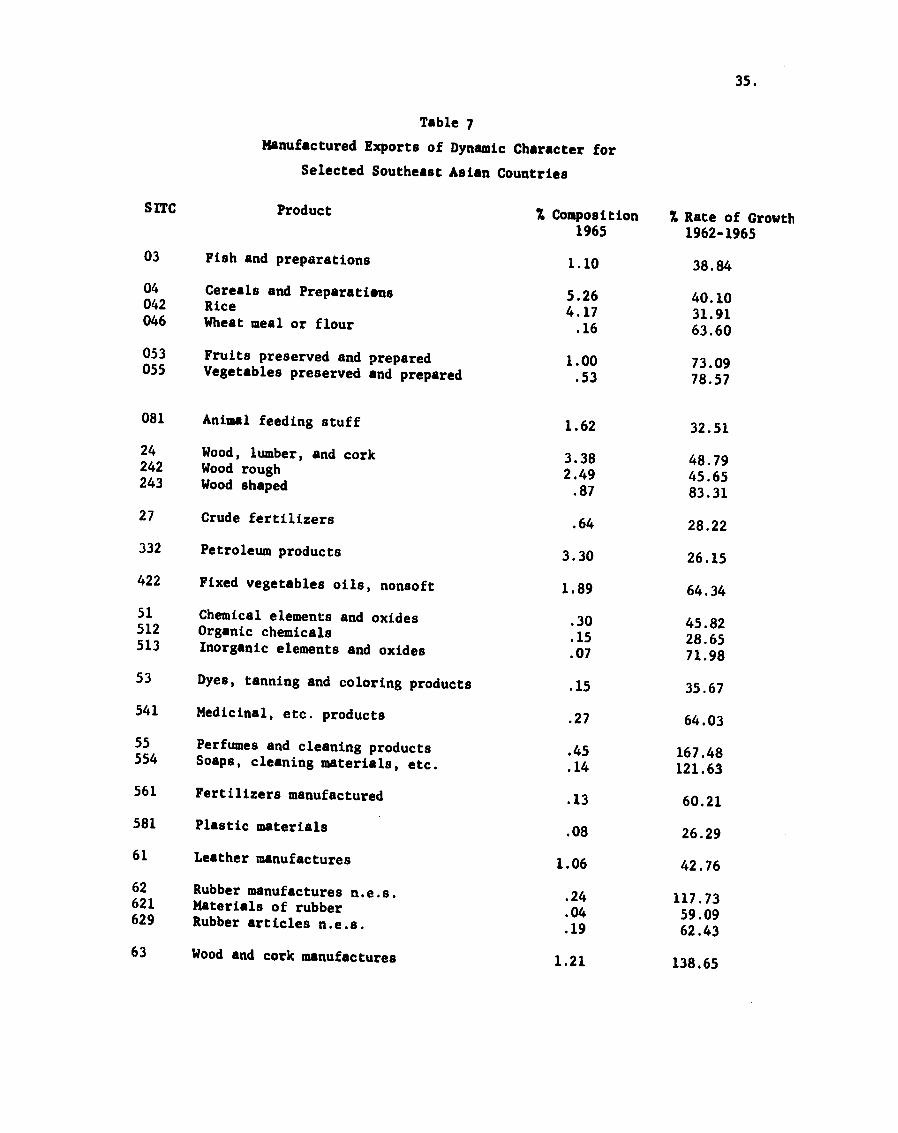

The following table (7) lists goods with rapid export growth It shows rates of growth and percentage composition of the above products and

other manufactured and semi-manufactured goods of dynamic charactertwo and three SITC digit classifications

in

1Indicating rates of increase above that of total exports (26 percent)

--

34

It is interesting to note that the list to a very large extent consists of manufactures that were shown to be labor intensive by examination of these countries data Most worthy of noting is also the fact that rapidshyly growing manufactured exports from Southeast Asian countries though still concentrated in origin are spread over almost all manufactured groups and extend far beyond the traditional products to which analysis of LDCs comshyparative advantage in manufactures has often been restricted

We should emphasize in conclusion that the right choice of potentiallysuccessful manufacturing industries needs to be complemented by a right mix of policies for promoting exports including conspicuously reasonable exchange rates We need to hope also that the HDCs adopt favorable import policies

It is important for LDCs to maintain price competition in the production of the manufactures in which they specialize a matter of the domestic pricelevel exchange rates and of specific policies There are indications that it is basically those LDCs with favorable export policies that are more successful in their general development efforts

Another important implication involves the skill composition of the labor force Skills including organization and administrative capacity are a scarce resource They should be considered soalong with quantity of capital natural resources and foreign exchange in planning for industrial development Skill availability over the course of time has relevance to the appropriate product mix of individual countries It directly influences the levd of current productivity and productivity potentials for the future

As development proceeds successfully the importance of industries low in skill and capital requirements will subside relative to those more demanding in their requirements

A final caution is relevant Experience in the United States indicates that the kind of industry or sub-industry that a business is in a poor guide to its individual success or failure Expanding fields which on the average are doing well have a built-in check the individual business faces increased competition from expansion of others and new entrants Its fortunes dependcrucially on its management which can cause it to sink in calm seas or sail sturdily through rough weather

35

Table 7 Manufactured Exports of Dynamic Character for

Selected Southeast Asian Countries SITC Product Composition Z Rate of Growth

1965 1962-1965 03 Fish and preparations 110 3884

04 Cereals and Preparatiens 526 4010042 Rice 417 3191046 Wheat meal or flour 16 6360

053 Fruits preserved and prepared 100 7309055 Vegetables preserved and prepared 53 7857

081 Animal feeding stuff 162 3251

24 Wood lumber and cork 338 4879242 Wood rough 4565243 Wood shaped

249 87 8331

27 Crude fertilizers 64 2822

332 Petroleum products 330 2615

422 Fixed vegetables oils nonsoft 189 6434

51 Chemical elements and oxides 4582512 Organic chemicals 30 15 2865513 Inorganic elements and oxides 07 7198

53 Dyes tanning and coloring products 15 3567

541 Medicinal etc products 27 6403

55 Perfumes and cleaning products 45 16748554 Soaps cleaning materials etc 14 12163

561 Fertilizers manufactured 13 6021

581 Plastic materials 08 2629

61 Leather manufactures 106 4276

62 Rubber manufactures nes 24 11773621 Materials of rubber 04 5909629 Rubber articles nes 19 6243

63 Wood and cork manufactures 121 13865

36

65 Textile and yarn fabric 1419 3115 651 Textile yarn and thread 141 5297 652 Cotton fabrics woven 438 4881 657 Floorcoverings tapestry etc 041 2986

66 Non metal mineral manufactures 110 8027 664-5 Glass and glassware 010 2682 667 Pearls precious and semi precious stones 063 16681

67 Iron and steel products 107 13889 673 Iron and steel shapes 036 9259 674 Iron and steel universals plates sheets 025 17618 678 Iron and steel tubes pipes etc 018 12802

68 Non ferrous metals 449 4950 684 Aluminum 010 7169 687 Tin 429 4874

69 Metal Products nes 093 2669 695 Tools 004 3038 696 Cutlery 007 20298

71 Machinery non electric 095 2647 711 Power machinery non electric 020 4657 715 Metal working machinery 003 6400

72 Electrical machinery 130 10064 723 Electrical distributing machinery 006 4267 724 Telecommunication equipment 055 24230 729 Electrical machinery nes 045 5440

812 Plumbing heating and lighting equipment 0301 5133

831 Travel goods handbags 0131 3885

841 Clothing 539 7050

851 Footwear 072 5320

861 Instruments and apparatus 0121 4482 89 Miscellaneous manufactured goods nes 354 8052 892 Printed matter 028 3318 893 Articles of plastic 024 11654 894 Toys and sporting goods 108 12341 896 Works of art etc 013 6475 897 Gold silverware and jewelry 015 4686

Source Calculated from United Nations Commodity Trade Statistics 1965 United Nations Foreign Trade Statistics of Asia and the Far East 1962 and United Nations Yearbook of International Trade Statisshytics 1965

1India not included

37

B - Export Patterns and Trends of Comparative Advantage

The need of Asian countries for sustained export expansion has been much emphasized in recent years These countries have in general experienced slow growth compared to their import and servicing-of-loans requirements As means of meeting the need regional cooperation and integration have been proposed as possible courses of action

But although the export growth of the region has been slow differences in performance among the countries are considerable Differences in export performance would affect the outcome of any preferential scheme that might be adopted and also the willingness of the countries to integrate or to move toward economic integration

This section examines the export performance and the trends of comshypetitiveness of individual Southeast Asian countries Problems of transport costs are treated in C Some implications for regional cooperation are drawn in this section a fuller analysis is given later on An analysis of the accuracy of Asian trade and income statistics on which we must rely throughshyout are presented in III below

This section is divided into

1-Asian performance in world trade 2- Trade with more developed countries (MDCs)

3- Intra-regional trade 1-Asian Performance inWorld Trade

Exports of less developed Asia have grown slowly compared to those of most other world regions (Table 8 ) Its exports to within the region have fallen somewhat (from 29 between 1955-56 and 1965-66) at the same time its exports to more developed countries have remained about stable Asias exports to high income countries are a much larger share of its total exports than its exports to any other region But all the other less developed regions export to high income countries a higher proportion of their total exports than does Asia

In two respects less developed Asia is unique among the worlds lower income regions All the other less developed countries export to the more developed countries (MDCs) a higher proportion of their total exports than does Asia (60 recently) Also Asia has a much larger share of its trade flow to within the region (25 recently) than does any other LDC region

TABLE 8

Export Directions by Regions

A-Less Developed

Asia Exports Less Latin Less Less

Developed America Developed Developed Middle

East More

Developed All

The

Exports of less developed Countries Asia Africa Countries World

Asia to the indicated regions (in $s million FOB) 1955-56 $2535 $140 $2020 $190 $143 $4020 $6870

1965-66 3080 116 2345 308 240 5690 9520

Share of total exports from less developed Asia going to the indicated regions (in ) 1955-56 37 2 29 3 2 59 1007

1965-66 32 12 25 3 3 60 100

B-Exports from the Regions Listed

Exports to more developed countries from the indicated 1938 72 80 7(r 84 68 69 region (in of total exports 1955-56 72 79 59 82 68 67 of the region) 1965-66 72 73 60 80 74 75

Exports to within the same 1938 22 6 1 6 14 69 region (as of total exports 1955-56 24 9 6729 10 13 of each region) 1965-66 21 10 25 7 6 75

C-Exports of the indicated 1938 25 7 5 4 2 41 100Region as of total 1955-56 24 8 7 5 3 65World Exports 1965-66 18 6

100 5 4 3 69 100

Definitions and coverage make 1938 figures not strictly comparable with later data Part of the table is notcarried back to 1938 because of lack of comparability All percentages are rounded to the nearest whole percent We estimate that the accuracy of the data does not warrant putting down fractions of a per cent

Sources United Nations Yearbook nf International Trade Statistics 1966 pp 20-31 op cit 1962 various pages

39

The lagging growth of the regions exports slower than that of Africa and the Middle East is usually explained by the extremely high concentrashytion of exports of traditional primary products combined with a progressively smaller export surplus of food and raw materials Primary commodities (SITC 0 through 4) are three-fourths of the regions total exports We will examine data relevant to this usual explanation below

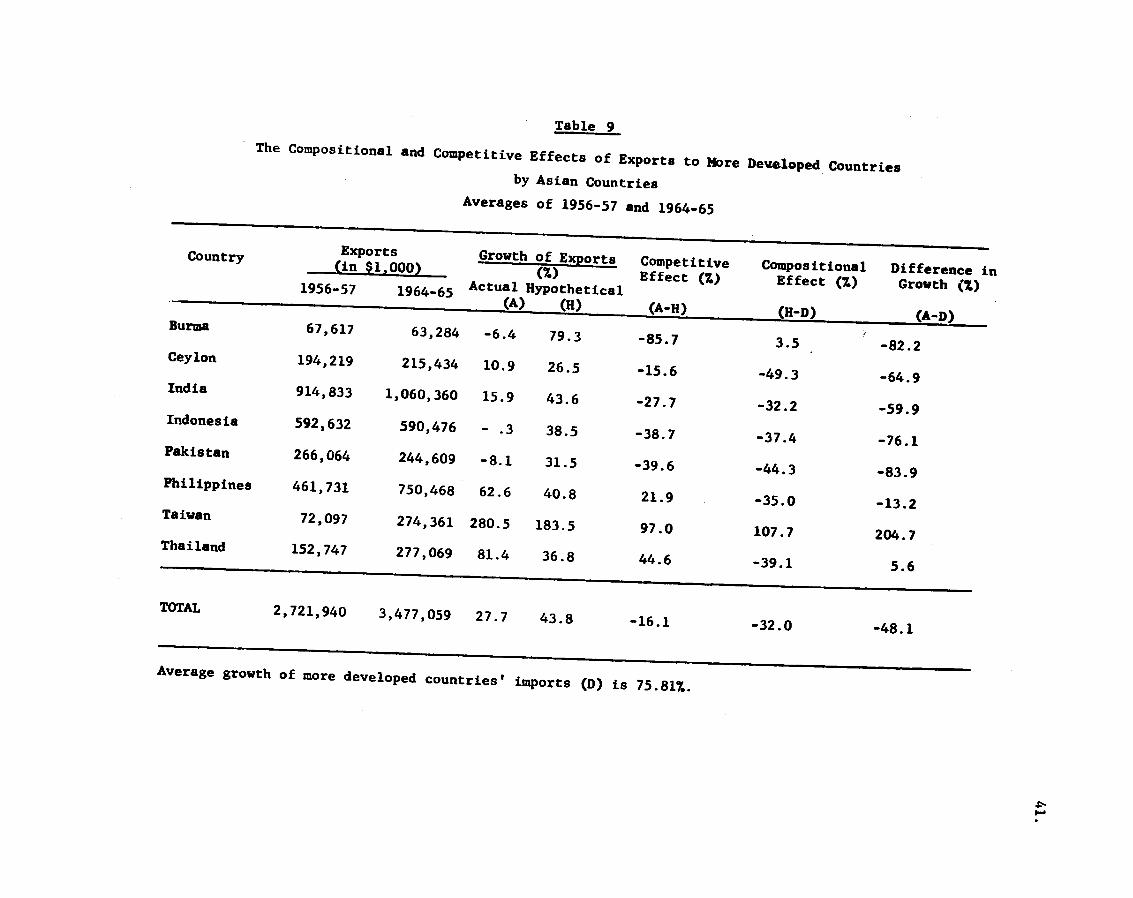

2- Exports to More Developed Countries

The regions share of total world exports has been falling (7 in 1956shy57 and 5 in 1965-66) But the share of its total exports going to MDCs appears not to have changed greatly the share was 60 in 1965-66 and seems to have been only moderately higher before World War II

The share varies widely for individual countries ranging in 1965 from 95 for the Philippines to 46 for Thailand and 31 for Burma

In evaluating the pattern of individual countries we analyze the extent to which export growth has been affected by two interrelated factors

(1) the compositional effect showing the changing proportion ofworld exports consisting of goods exported by a given regional country

and (2) the competitive effect denoting the changing proportion of world exports of a given commodity that the country provides

To find quantitative values for these effects the hypothetical export growth (h) of a given Asian country (J) is first computed This growth is based on the assumption that the country is able to maintain the same share in each commodity for each export market in the second period as in the first In notational form Js hypothetical export growth (HJ) is as follows

c

Hj =

c i xji where X refers to Js exports to another country i and Mi to is total imports Superscript c indicates the commodity and 1 and 2 refer to periods

The competitive effect ismeasured as the actual export growth (A)of the country minus its hypothetical growth (H) The compositional effect isdefined as H minus D which is the weighted average import growth of its trading partshyners The sum of these effects (A - -H + H D) is the difference between growth rate of the countrys exports and its partners imports (A - D)

40

In computing these effects with respect to the MDCs two periods have been selected Period I (1956 and 1957) and Period II (1964 and 1965) In

each period the average of the two years is used to minimize the yearly

fluctuation of trade values The country-by-coumodity trade data on Asian countries are not readily available especially for the earlier period

(except Malaya-Singapore) To overcome the scarcity-of-data problem the export patterns of Asian countries are approximated from the import data of

their trading partners

The growth rate of the regions as well as individual countries exports to the selected MDCs in terms of the compositional and competitive effects

is given in Table 91 As shown in the last row the region has labged for both composition ind competitive reasons Exports grew only 28 while

total imports of the MDCs rose by 76 from 1956-57 to 1964-65 -- a lag

of 482

The low growth rate for exports of the region is partly due to regional concentration on primary products that have been expanding slowly in the world market This negative compositional effect is not surprising The emphasis

on and effort in Asian countries toward export diversification and toward industrialization is partly a reaction to slowly growing world markets for

primary products

The remainder of the export lag the (negative) competitive effect of 16 or one-third the total export lag of -48 (A-D) is unexpectedly large Even when the unfavorable compositional effect is taken into account the position of the regions exports in various commodities vis-a-vis other world

exporters has declined

l1n computing these effects SITC Group r (Unclassified Goods) ia

excluded The group makes up an almost neglIgible proportion of total exports

2Also see Seiji Nayas Project Research Paper The Commodity Pattern and Export Performance of Developing Asian Countries to the Developed Areaspublished in Economic Development and Cultural Change (July 1967) in which the regions but not individual countries exports to various developed countries are analyzed employing the same method used here with 1962-63 as the terminal period

Table 9 The Compositional and Competitive Effects of Exports to More Developed Countries

by Asian Countries Averages of 1956-57 and 1964-65

Country Exports(in $1000) Growth of Exports Competitive() CompositionalEffect (Z) Difference inEffect (Z)1956-57 Growth ( )1964-65 Actual(A) Hypothetical(H) (A-H) (H-D) (A-D)Burma 67617 63284 -64 793 -857 35 -822 Ceylon 194219 215434 109 265 -156 -493 -649 India 914833 1060360 159 436 -277 -322 -599 Indonesia 592632 590476 - 3 385 -387 -374 -761 Pakistan 266064 244609 -81 315 -396 -443 -839 Philippines 461731 750468 626 408 219 -350 -132 Taiwan 72097 274361 2805 1835 970 1077 2047 Thailand 152747 277069 814 368 446 -391 56

TOTAL 2721940 3477059 277 438 -161 -320 -481

Average growth of more developed countries imports (D) is 7581

42

Within this over-all picture of the region considerable variation exists

in the performance of individual countries Striking differences are revealed

the increase in exports of Taiwan(281) Thailand (81) and the Philippines

(63) is outstandingly high compared with that of other countries some of

whose export values fell absolutely (Indonesia -028 Burma -6 Pakistan-8)

A negative compositional effect is common to most countries considered

reflecting unfavorable commodity shifts in MDC markets for these countries

goods (Taiwan is the main exception)1

But there is a distinctive difference in competitive effects The

countries with fast-rising exports (Taiwan Thailand and the Philippines)

show positive competitive effects Countries with relatively stagnant exports

(Burma Ceylon Pakistan Indonesia and India) show negative effects Furthershy

more the relative sizes of the negative competitive effects (as well as unshy

favorable compositional effects) that have hindered export expansion are large

in some cases more than or close to one-half the total lag (A-D) However

the Philippines was able to offset her unfavorable compositional change conshy

siderably and Thailand more than sufficiently What is implied in Table 11

then is the importance of the competitive effect in influencing relative

export performance

1The country-by-commodity trade data for Malaya and Singapore are most ready available since these countries were the only reporting developingAsian countries in Commodity Trade Statistics until the latter part of the 1950s But they are excluded in Tables 11 and 12 and Appendix Table 17 since the trade data for these two countries are reported together for early years but separately for recent years other reporting countries (MDCs) do not consistently use the same definitiofi of these countries from year to year there are large reporting differences especially in Singapores trade figures probably because of its entrepot trade See Seiji Naya and Theodore Morgans project research paper The Accuracy of International Trade Data The Case of Southeast Asian Countries Journal of the American Statistical Association July 1969

The results based on combined figures for these two countries and which should be interpreted cautiously for the above reasons are as follows 919 (A) 4381 (H) -3661 (A-H) -3001 (H-D) and -4807 (A-D) Comparable results on the intra-regional trade pattern for the two countries are given separately in Table 16

43

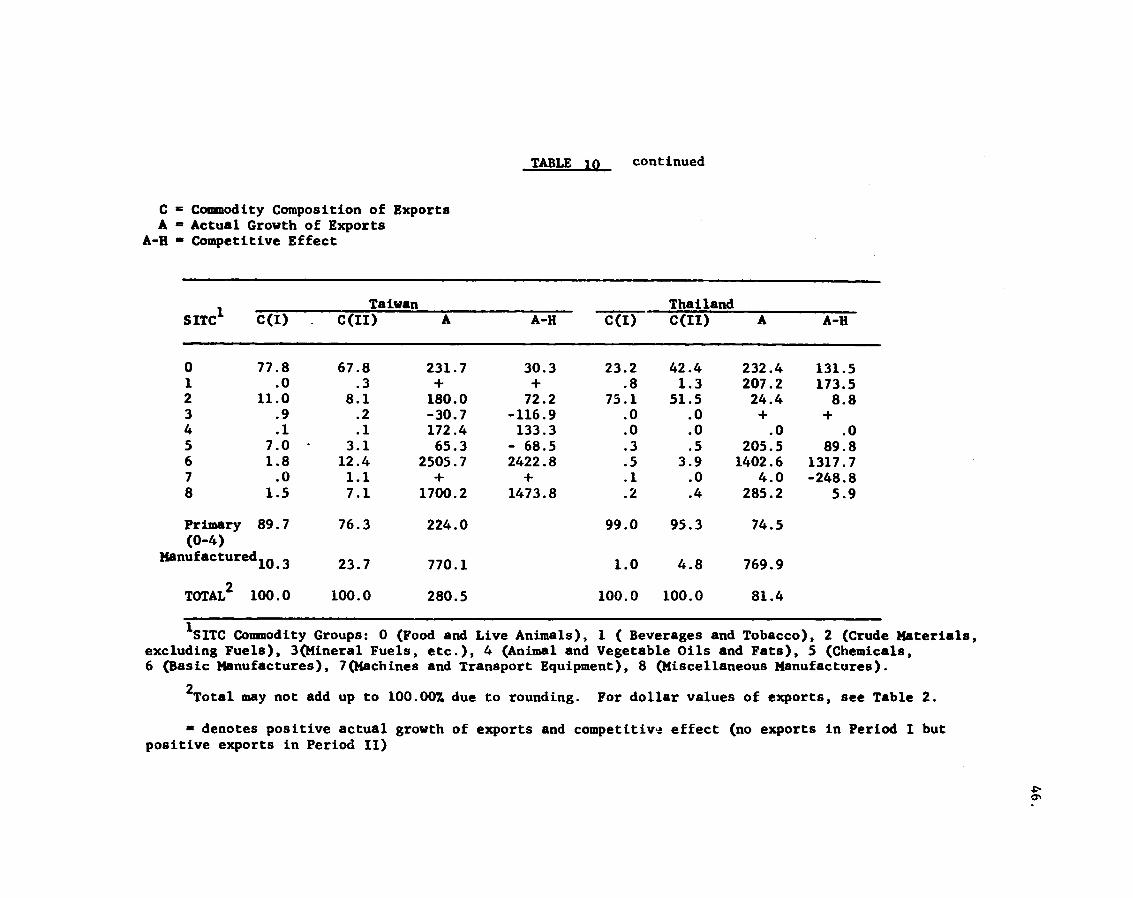

In order to determine which commodity groups are responsible for this effect the same computation was made for each comnodity group The results are given in Table 10 together with the commodity composition of exports1

The differences again are striking For Thailand the Philippines and Taiwan positive competitive effects are shown in a relatively large number of comshymodity groups The reverse is true for the other countries although numershyical values differ from commodity to commodity and country to country Furthershy

more in relating Tables 9 and 10 the negative (or positive) competitive effect of a countrys exports (Table 9 ) is shown to be largely due to the negative (or positive) values in primary products especially those that comprise a relatively large proportion of total exports (SITC Groups 0 and 2) That is given the slow expansion of these products in MDC markets the lag in export growth of many Asian countries can be attributed to their inability to maintain even this low growth rate of primary exports

Changes in commodity compositions and export increases by two broad categories primary and manufactured are shown in Table 10 together with total exports of Thailand the Philippines and Taiwan The experience of these countries stands in clear contrast to stagnation for the other countries The commonly held view that countries with high concentrations in primary exports perform poorly is not supported Thailand and the Philippines have done remarkably well and they have a high degree of specialization in primary

exports

1The hypothetical export growth for a given commodity used for this purpose is computed from the formula (page 39)

2The sluggish expansion of primary products inMDC markets (comparedto manufactured products) is reflected in low hypothetical increases (H) ofthese exports Numerical values of the increases for individual commodity groups are not shown in Table 10 They can be found by subtracting competshyitive effect from actual growth A - (A-H) - H

3Examinations of the three-digit commodity exports reveals that these two countries have been able to diversify within primary commodities therebyoff setting the decline of some traditional primary exports by increases ofothers (eg maize and kenaf in the case of Thailand lumber and minerals in the case of the Philippines)

Table 10

The Composition and Competitive Effect of Exports of Asian Countries by Commodity Groups

Averages of 1956-57 (I) and 1964-65 (I1) In PercentagesC - Commodity Composition of Exports

A = Actual Growth of Exports A-H = Competitive Effect

Burma Ceylon India

SITC1 C(I) C(nI) A A-H C(I) C(II) A A-H C(I) C(II) A A-H

0 673 510 -292 -1324 781 798 132 -155 326- 3081 0 0 99 1300 - 206 0 0 02 295 0 25 25 143 -150416 321 85 164 1513 20 -162 320 259 - 607 -46411 426 32 2 0 0 -402 74 4 -374 -8500 0 0 1 39 37 39 200 39 55 -845 -9060 0 0 -2000 6 6 142 -9586 23 60 8 9 217 -12521469 535 8 216 -758 2647 2 4 1300 911 7 374 646 -1191 1 2045 -215 2 68 1986 -1800 0 0 -2900 1 0 0 -3301 10 10 161 -3006

Primary 975 936 -102 986 985 108 716 602 -26(0-4)Manufactured 25 64 1411 14 15 213 284 398 626

(5-8)

TOTAL2 1000 1000 - 64 1000 1000 109 1000 1000 159

Table 10 continued

C Commodity Composition of Exports A = Actual Growth of Exports

A-H - Competitive Effect

SITC1

C(I) Indonesia

C(II) A A-H C(I) Pakistan C(II) A A-H C(I)

Philippines

C(II) A A-i

0 1 2 3 4 5 6 7

8

127 44

553 207 49

6 14 1

0

150 22

393 378 43

9

5

0

0

174 -486 -291 822

-136 520

-623 -494

387

-581 -602 -555 347

-338 -1194 -1891 -2622

-2877

55 1

890 0 0 2

41 3

9

51 0

699 1 0 2

221 8

19

-147 0

-279 +

0 - 53 3928 1241

2918

-430 -618 -541 +

- 19 -1524 3185 - 701

- 234

294 6

600 0

47 3

11 0

39

273 16

541 0

76 2

49 0

43

510 3351 465

+ 1621 435 6398

0

793

304 2505

81 +

1445 513

5761 -2285

-1604

Primary 980 986 3 945 750 -270 948 906 555 (0-4)

Manufactured 20 15 -292 55 250 3199 53 94 1915 (5-8)

TOTAL2 1000 1000 - 3 1000 1000 - 81 1000 1000 626

CONTINUED

TABLE Io continued

=C Comodity Composition of Exports A = Actual Growth of Exports

A-H - Competitive Effect

Taiwan Thailand SITC C(I) C(II) A A-H C(I) C(II) A A-H

0 778 678 2317 303 232 424 2324 1315 1 0 3 + + 8 13 2072 1735 2 110 81 1800 722 751 515 244 88 3 9 2 -307 -1169 0 0 + + 4 1 1 1724 1333 0 0 0 0 5 70 31 653 - 685 3 5 2055 898 6 18 124 25057 24228 5 39 14026 13177 7 0 11 + + 1 0 40 -2488 8 15 71 17002 14738 2 4 2852 59

Primary 897 763 2240 990 953 745 (0-4)

Manufactured 103 237 7701 10 48 7699

TOTAL2 1000 1000 2805 1000 1000 814

1SITC Commodity Groups 0 (Food and Live Animals) 1 ( Beverages and Tobacco) 2 (Crude Materials excluding Fuels) 3(Mineral Fuels etc) 4 (Animal and Vegetable Oils and Fats) 5 (Chemicals 6 (Basic Manufactures) 7(Machines and Transport Equipment) 8 (Miscellaneous Manufactures)

2Total may not add up to 10000 due to rounding For dollar values of exports see Table 2

- denotes positive actual growth of exports and competitive effect (no exports in Period I but positive exports in Period II)

47

In contrast to the varied performances of primary exports the rapid rise in exports of manufactures common to almost all countries is very encouraging (A notable exception is Indonesia with an absolute decline of 29 which is however understandable in view of the countrys political difficulties during the period covered) Some groups of manufactured goods have grown at rates even higher than the relevant import growth of the MDCs indicating positive competitive effects It is worth noting that those countries with expanding primary products tend to perform better in manufactured exports as well

Examination of commodity detail shows that much of manufactured exports are suitable to the factor endowments of this region Among these are textile products footwear plywood and leather These exports have expanded rapidly despite high import protection (especially high effective rates of protectshyion) generally accorded by MDCs on commodities of this type

3- Intra-Rexional Trade

Intra-regional trade (which is strikingly larger than that of other LDC regions) is analyzed here although the record is handicapped by lack of availability of adequate data

The share of intra-Asian trade of the individual countries varies widely ranging from 79 for Laos to 57 for Singapore and 50 for Burma to 6 for Ceylon and 4 for the Philippines (in 196465 Table 11) Most countries show a decline in this trade evident in the Lowered shares from 1956-57 to 1964-65 The large absolute decline of intra-regional shares for Hon- Kong and Indonesia stands out Deviating from this trend are Pakisttn Korea and the Philippines who have had rapid increases in their intra-regional

trade shares

Of course using intra-regional trade shares alone can be misleading A share may be kept fairly constant simply as a reflection of low growth of both total and regional exports as for Burma Or a share may fall at the same time regional trade rises rapidly ie exports to the rest of the world grow faster than intra-regional trade as for Taiwan Cambodia and Thailand The latter pattern is more encouraging than the former

The close association of the relative expansion of intra-regional exports with the export growth to the HDCs is interesting Intra-regional export growth rates for Burma and Indonesia(India also) are extremely low compared with those for the Philippines Taiwan and Thailand That is the latter

48

Table 11 Export Growth and Shares of Intra-Regional Exports Averages of 1956-57

and 1964-65

Country Total Exports (millions ofdollars)

Intra-Regional Ex-ports as of total

Percent Change in Value of

Total Intra-Regional

1956-57 1964-65 1956-57 1964-65 Exports Exports

Burma 2398 2315 518 505 -35 -60 Cambodia 445 965 358 316 1171 915 Ceylon 3587 4015 55 58 119 179 Hong Kong 5461 10775 510 220 973 -148 India 13252 17155 110 97 295 133 Indonesia 9257 6830 332 105 -262 -766 Korea 234 1470 137 234 5282 10734 Laos 12 12 833 792 0 -50 Pakistan 3493 5105 52 198 411 538 Philippines 4355 7545 26 37 732 1451 Taiwan 1333 4415 332 289 2312 1885 Thailand 3495 6100 542 466 745 501 Vietnam 628 420 134 151 -331 -244 Malaya 7260 9610 na 270 324 na Singapore 11285 9434 na 571 -164 na