Embed Size (px)

Citation preview

Financial Reportfor the year ended 31 December 2020

Baptist Financial Services Australia LimitedABN 56 002 861 789 AFSL 311 062

Registered Office: Level 4, 5 Saunders Close, Macquarie Park NSW 2113 Phone: 1300 650 542 Email: [email protected] A Delegated Body Of Australian Baptist Ministries

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

ii

Page

Directors’ Report 1

Auditor’s Independence Declaration 7

Consolidated Statement of Profit or Loss and Other Comprehensive Income 8

Consolidated Statement of Financial Position 9

Consolidated Statement of Changes in Equity, Accumulated Funds & Reserves 10

Consolidated Statement of Cash Flows 11

Notes to the Consolidated Financial Statements 12

Directors’ Declaration 35

Independent Auditor's Report 36

Contents

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

1

The Directors of Baptist Financial Services Australia Limited (BFS) submit herewith their report together with the Annual Financial Report of the consolidated entity, being Baptist Financial Services Australia Limited (the Company) and its Controlled Entity (the Group) for the financial year ended 31 December 2020 and the Independent Auditor’s Report.

Directors details

The names, qualifications, experience and special responsibilities of each Director in office at any time during the year and up to the date of this report are:

Owen Hsiao-Fen Chew Lee BSc, BCA, FCA, GAICD

Board Chair to 2 July 2020; Deputy Board Chair to 11 December 2014; Chair of Assets and Liabilities Committee to 27 June 2019 and continuing member of the Committee; Member of Board Governance & Remuneration Committee from 12 December 2014 to 13 August 2020; Chair of Investment Committee (Baptist Impact Fund) since 2 July 2020; and Board Chair Baptist Development Australia Pty Ltd from 12 November 2015.

Member of Gordon Baptist Church, NSW

Appointed a Director from 22 July 2008

Over 25 years financial services experience in banking, including senior roles in Regulatory Affairs (International and Domestic), Treasury, Strategy, Mergers and Acquisitions, Finance and Corporate Finance in Australia and Asia. Qualified as a Chartered Accountant with Ernst & Young.

Gregory Paul Holland BBus (Accounting), CPA, GAICD

Chair of the Board Governance & Remuneration Committee to 27 June 2019; Member of Audit Risk and Compliance Committee from 18 February 2016, Member of Assets & Liabilities Committee from 27 June 2019.

Member of Lake Joondalup Baptist Church, WA

Appointed a Director from 11 February 2014

Head of Finance & Administration for the Baptist Churches of Western Australia. Former Chief Executive Officer of Ray Village Aged Services Inc., WA, former General Manager Finance / Chief Financial Officer and General Manager HR and Shared Services at Capricorn Society Ltd, WA, former Chief Financial Officer of University of Western Sydney, NSW and former Director Management Services of Edith Cowan University, WA.

Karen James BSEE, MSEE, MAICD, MIE

Member of the Board Governance & Remuneration Committee from 28 June 2018; Member of Credit Committee from 14 September 2018.

Member of Seaforth Baptist Church

Appointed a Director from 22 February 2018.

CEO of Business for Development since January

2019. Former senior roles at On Purpose Hub

(Founder), Commonwealth Bank including General

Manager of Affiliate Business Banking for Corporate

Financial Services & General Manager, Direct

Sales and Service for Local Business Banking.

Former senior management, consulting and project

roles in systems, network and product engineering.

Ross Martin Langford BCom, MAICD, F.FINSIA

Board Chair from 2 July 2020; Deputy Board Chair to 2 July 2020; Member of Audit, Risk & Compliance Committee from 28 May 2015 until 18 February 2016; Member of Assets & Liabilities Committee from 18 February 2016; Chair of Credit Committee from 14 September 2018 to 27 June 2019 and continuing member of the Committee; Member of the Board Governance & Remuneration Committee from 27 June 2019; member of Investment Committee (Baptist Impact Fund) since 2 July 2020 and Director of Baptist Development Australia Pty Ltd from 25 October 2019.

Member of Gymea Baptist Church, NSW

Appointed a Director from 13 March 2015

Head of Loan Review with a major overseas bank (Rabobank). Formerly Head of Finance, Property & Administration at St George Christian School and formerly Senior Relationship Management, Regional Lending Manager and Senior Manager

Directors’ Report

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

2

positions with Commonwealth Bank, BankWest and State Bank NSW. Former Director of Christian Super 2008 - 2020.

Darren Leigh McDonald BA (Accounting), CPA, MBA

Deputy Board Chair from 2 July 2020, Chair of Assets and Liabilities Committee from 27 June 2019, Member of Assets & Liabilities Committee from 20 June 2014; Chair of Audit Risk & Compliance Committee to 27 June 2019 and continuing member of the Committee; Chair of Credit Committee from 28 July 2020, Member of Credit Committee from 14 September 2018.

Member of King’s Baptist Church Inc., SA

Appointed a Director from 29 May 2014

Business Manager of Kings Baptist Grammar School Inc., SA; former Executive / Finance Manager of Woolworths Ltd, Board of Kings Baptist Grammar School Inc., SA including 2 years as Chair, Chair and Treasurer of King’s Baptist Church Inc., SA; Public Officer and Director of King’s Baptist Mount Barker Inc., SA.

Sally Anne Mullins BBus (Business Administration), Grad Dip HR & IR

Chair of Board Governance & Remuneration Committee from 27 June 2019, Member of the Board Governance & Remuneration Committee from 9 December 2015.

Member of Ashburton Baptist Church, VIC

Appointed a Director from 9 December 2015

Manager Communications and Administration at The Village Church, Mt Eliza. Previously Organisational Development and Projects Manager at a boutique Leadership and Talent consultancy business and formerly a Senior Human Resource Consultant at National Australia Bank with over 20 years’ experience in various HR roles in Australia and overseas.

Peter Jeffrey Murphy M.Comm; MA (C.S.); B.Bus; FCPA; FASFA; GAICD

Member of Audit, Risk & Compliance Committee from 23 March 2018; Member of Credit Committee from 14 September 2018; Member of the Board Governance & Remuneration Committee from 27 June 2019 and member of Investment Committee (Baptist Impact Fund) since 2 July 2020.

Member of Mortdale Oatley Baptist Church.

Appointed a Director from 1 August 2017.

Executive Director – Jefferson and Shea Group, Chair – Best Health Solutions, Deputy Chair - Scripture Union Australia, Director - Baptist Care NSW and ACT, Director - Olive Tree Media.

Former CEO of an Industry Superannuation Fund, Administrative Dean of a Theological College, Company Secretary of Aged Care Provider, Business Manager of School and Director – Finance of Not for Profit organisation within a range of faith based organisations.

Allan Kenneth Priest Unrestricted Building Work & Plumbing/Gasfitting contracting and restricted Electrical Worker licenses, Diploma for Public Health Inspectors, MAICD

Deputy Chair from 18 February 2016 until 27 June 2019. Member of Audit, Risk & Compliance Committee (Chair of committee to 12 December 2014); Member of Assets and Liabilities Committee; Member of Board Governance & Remuneration Committee to 12 December 2014; Member of Credit Committee from 14 September 2018 and Chair of the Credit Committee from 27 June 2019.

Member of Rostrevor Baptist Church Inc., SA

Appointed a Director from 31 May 2005

Director then Managing Director of family plumbing and building business 1972-2003; Manager of two Commercial Rental Properties 1989 - 2013; Member of Baptist Churches of South Australia Inc. (BCSA) Assembly Board 2004 - 2015, including as President 2006-2009, also past service (including as Chair) on numerous other BCSA Committees and working parties; Chair of Baptist Care (SA) Inc. 2007 - 2015 after joining Board in 2006; current Director and Deputy Chair of Baptist Care (SA) Foundation Nominees Pty Ltd and Member of Kings

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

3

Baptist Association of Kings Baptist Grammar School Inc.; Member of the Australian Institute of Company Directors; and 28 years' past service in numerous senior leadership roles of Rostrevor Baptist Church Inc. (SA) including as Treasurer, Administrator & Chair.

Ceased being a director on 21 May 2020.

Alan Leslie Soden FAIML, MAIE

Chair of Audit, Risk and Compliance Committee from 28 June 2019, Member of the Board Governance & Remuneration Committee from 20 June 2014, Member of the Assets and Liabilities Committee to 12 December 2014, Member of the Audit, Risk and Compliance Committee to 12 December 2014.

Appointed a Director from 13 August 2002

Member of Port Macquarie Baptist Church, NSW

Previously, Interim Pastor, Port Macquarie Baptist Church, former Director and Chief Executive Officer of Kairos Prison Ministry Australia, former Member of Baptist Churches of New South Wales Property Trust, former Trustee Director BCS Foundation, Certified CEO and alumni of the CEO Institute, former Chair of Hopestreet, former General Secretary of the Association of Baptist Churches of NSW & ACT, former Board Member and Vice President of the Bible Society of NSW, former National Secretary and Member of the National Council of the Baptist Union of Australia and former Secretary of Baptist Insurance Management Pty Ltd, former Director Chrysalis Public Relations, previous management roles in training, marketing, public affairs and sales with the Australian Gaslight Company.

Debbie Uy BScCom (Marketing), BA (Psychology), MBA, GAICD

Member of Assets and Liabilities Committee from 27 June 2019, Member of Credit Committee from 27 June 2019, Director of Finance & Administration and Union Secretary of the Baptist Union of Victoria, Director of Surrey Hill Baptist Child Care Centre

Appointed a Director from 23 May 2019.

Member of Oakleigh Baptist Church, VIC

Over 19 years-experience in corporate business management and over 8 years-experience in executive leadership in Not For Profit sector and professional training in Human Resources management. Former Head of Operations at Crossway LifeCare Ltd. Former ex-officio member of Crossway LifeCare Finance Committee. Former Assistant Manager and Corporate Secretary at TSI Contracts Inc. Member, Australian Human Resources Institute.

Company Secretaries

David Slinn

Alan Soden

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

4

Meetings of Directors

During the year, 33 meetings of directors (including committees of directors) were held. Attendances by each Director during the year are set out below:

State

Board ARCCo ALCo BGRCo CCo

H A H A H A H A H A

Owen H Chew Lee NSW

9 9 5 5 4 3

Gregory P Holland WA

9 8 4 4 5 5

Ross M Langford NSW

9 9 2 2 5 5 4 4 11 11

Darren L McDonald SA

9 9 4 4 5 5 11 10

Sally A Mullins VIC

9 9 4 4

Allan K Priest SA

4 4 1 1 2 2 4 3

Alan L Soden NSW

9 9 4 4 4 4

Karen James NSW 9 9 4 4 11 9

Peter Murphy NSW 9 9 4 3 4 4 11 7

Debbie Uy VIC 9 9 5 5 11 11

H=Meetings held during the year, or during the term of appointment; A=Attended; ARCCo=Audit, Risk & Compliance Committee; ALCo=Assets & Liabilities Committee; BGRCo= Board Governance & Remuneration Committee; CCo – Credit Committee.

Principal activities The principal activities of the Company during the financial year were the provision of financial solutions for the particular needs of churches and Christian ministries, the facilitation of the financing of churches and ministries through participating State Baptist Unions/Associations and the Baptist Union of Australia, and, subject to capital adequacy needs, the making of grants to State Baptist Unions/Associations and the Baptist Union of Australia for ministry.

There has been no significant change in those activities during the financial period. The entity's short term strategic objectives are to:

Maintain and introduce relevant financial services for Baptist entities and Christian ministries in Australia Maintain the adequacy of funds and reserves Address all relevant regulatory requirements

The entity's long term objectives are to:

Further develop recognition of BFS by the Australian Baptist community as its primary financial services provider

Continue to extend the use of BFS services within Baptist Churches, congregations and Christian organisations across Australia

To assist churches and ministries as they pursue development opportunities and realise increased resources for ministry.

To achieve these objectives, the entity has adopted the following strategies:

Sponsor nationally oriented support services for Churches Appoint and develop staff in accordance with the Strategic Priorities Continue to enhance existing financial services and develop new products Review relevant regulatory frameworks for the ongoing provision and extension of BFS services Upgrading client systems and technology platforms Reviewing and progressing redevelopment options for a range of church sites Continued development of effective relationships with Stakeholders and clients.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

5

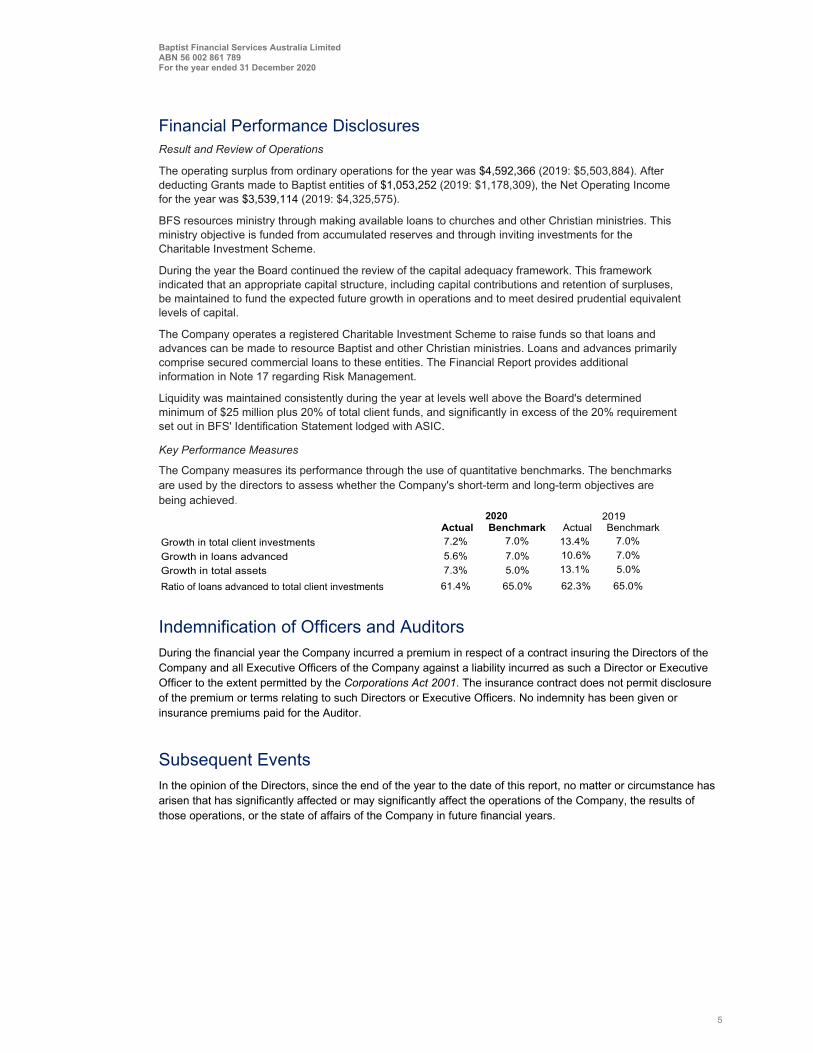

Financial Performance Disclosures Result and Review of Operations

The operating surplus from ordinary operations for the year was $4,592,366 (2019: $5,503,884). After deducting Grants made to Baptist entities of $1,053,252 (2019: $1,178,309), the Net Operating Income for the year was $3,539,114 (2019: $4,325,575).

BFS resources ministry through making available loans to churches and other Christian ministries. This ministry objective is funded from accumulated reserves and through inviting investments for the Charitable Investment Scheme.

During the year the Board continued the review of the capital adequacy framework. This framework indicated that an appropriate capital structure, including capital contributions and retention of surpluses, be maintained to fund the expected future growth in operations and to meet desired prudential equivalent levels of capital.

The Company operates a registered Charitable Investment Scheme to raise funds so that loans and advances can be made to resource Baptist and other Christian ministries. Loans and advances primarily comprise secured commercial loans to these entities. The Financial Report provides additional information in Note 17 regarding Risk Management.

Liquidity was maintained consistently during the year at levels well above the Board's determined minimum of $25 million plus 20% of total client funds, and significantly in excess of the 20% requirement set out in BFS' Identification Statement lodged with ASIC.

Key Performance Measures

The Company measures its performance through the use of quantitative benchmarks. The benchmarks are used by the directors to assess whether the Company's short-term and long-term objectives are being achieved. 2020 2019

Actual Benchmark Actual Benchmark

Growth in total client investments 7.2% 7.0% 13.4% 7.0%

Growth in loans advanced 5.6% 7.0% 10.6% 7.0%

Growth in total assets 7.3% 5.0% 13.1% 5.0%

Ratio of loans advanced to total client investments 61.4% 65.0% 62.3% 65.0%

Indemnification of Officers and Auditors During the financial year the Company incurred a premium in respect of a contract insuring the Directors of the Company and all Executive Officers of the Company against a liability incurred as such a Director or Executive Officer to the extent permitted by the Corporations Act 2001. The insurance contract does not permit disclosure of the premium or terms relating to such Directors or Executive Officers. No indemnity has been given or insurance premiums paid for the Auditor.

Subsequent Events In the opinion of the Directors, since the end of the year to the date of this report, no matter or circumstance has arisen that has significantly affected or may significantly affect the operations of the Company, the results of those operations, or the state of affairs of the Company in future financial years.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

6

Contribution in winding up The Company is incorporated under the Corporations Act 2001 and is an entity limited by guarantee. If the Company is wound up the constitution states that each member is required to contribute a maximum of $100 towards meeting any outstanding obligations of the entity. At balance date the total amount that members of the Company are liable to contribute if the company was wound up was $900 (2019: $1,000).

Auditors Independence Declaration

A copy of the Auditor’s Independence Declaration as required under s.60-40 of the Australian Charities and Not-for-profits Commission Act 2012 is included in page 7 of this financial report and forms part of the Directors’ Report.

Signed in accordance with a resolution of the Directors.

Director Dated at Sydney this 15th day of April 2021

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389

‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to the ir clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are

delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to

Grant Thornton Australia Limited.

Liability limited by a scheme approved under Professional Standards Legislation.

www.grantthornton.com.au

Level 17, 383 Kent Street Sydney NSW 2000

Correspondence to: Locked Bag Q800 QVB Post Office Sydney NSW 1230

T +61 2 8297 2400 F +61 2 9299 4445 E [email protected] W www.grantthornton.com.au

Auditor’s Independence Declaration

To the Directors of Baptist Financial Services Australia Limited

In accordance with the requirements of section 307C of the Corporations Act 2001 and section 60 – 40 of the Australian

Charities and Not-for-profits Commission Act 2012, as lead auditor for the audit of Baptist Financial Services Australia Limited

for the year ended 31 December 2020, I declare that, to the best of my knowledge and belief, there have been:

a no contraventions of the auditor independence requirements of the Corporations Act 2001 in relation to the audit; and

b no contraventions of any applicable code of professional conduct in relation to the audit.

Grant Thornton Audit Pty Ltd

Chartered Accountants

Madeleine Mattera

Partner – Audit & Assurance

Sydney, 15 April 2021

7

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

8

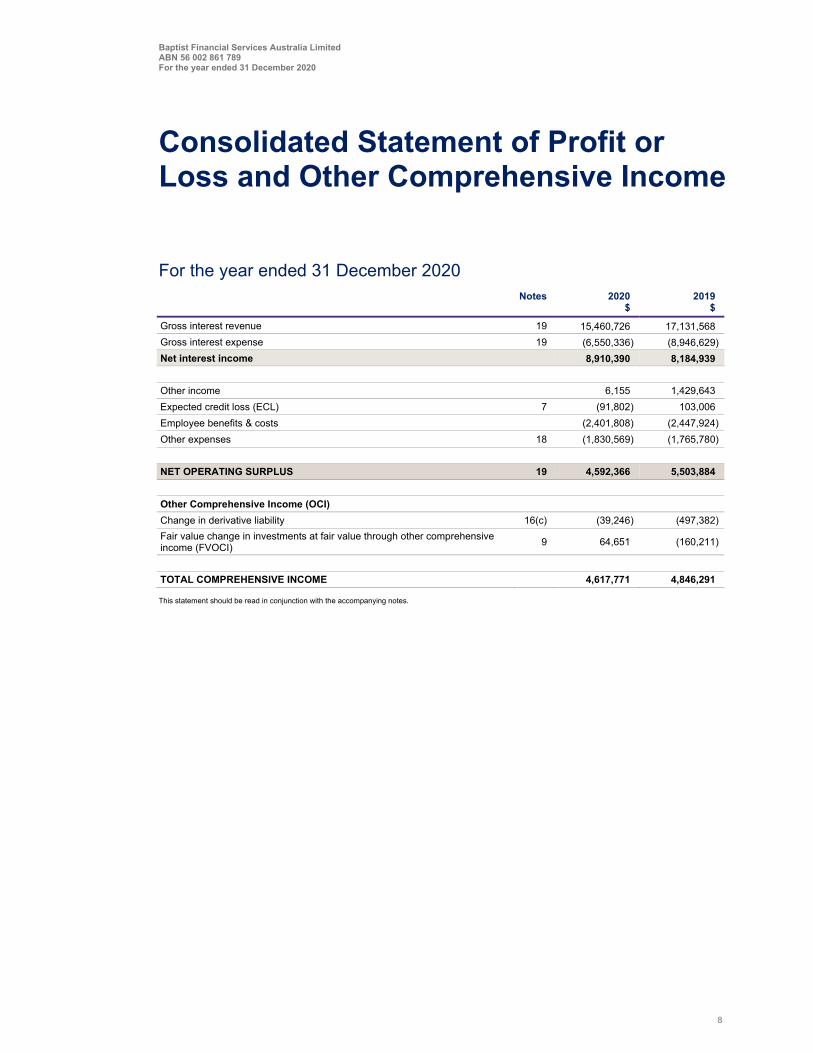

For the year ended 31 December 2020 Notes 2020 2019 $ $

Gross interest revenue 19 15,460,726 17,131,568

Gross interest expense 19 (6,550,336) (8,946,629)

Net interest income 8,910,390 8,184,939

Other income 6,155 1,429,643

Expected credit loss (ECL) 7 (91,802) 103,006

Employee benefits & costs (2,401,808) (2,447,924)

Other expenses 18 (1,830,569) (1,765,780)

NET OPERATING SURPLUS 19 4,592,366 5,503,884

Other Comprehensive Income (OCI)

Change in derivative liability 16(c) (39,246) (497,382)

Fair value change in investments at fair value through other comprehensive income (FVOCI)

9 64,651 (160,211)

TOTAL COMPREHENSIVE INCOME 4,617,771 4,846,291 This statement should be read in conjunction with the accompanying notes.

Consolidated Statement of Profit or Loss and Other Comprehensive Income

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

9

As at 31 December 2020 Notes 2020 2019 $ $

Assets

Cash and cash equivalents 4 32,123,545 25,250,974

Other receivables and prepayments 8 1,531,530 980,185

Investment securities at fair value through other comprehensive income 9 187,056,041 175,998,192

Loans and advances - interest bearing 5 286,753,786 271,477,147

Property, plant and equipment 10 428,539 326,210

Right-of-use-assets 11 578,440 19,140

Total assets 508,471,881 474,051,848

Liabilities

Payables - interest bearing 12 467,108,854 435,783,375

Swap derivative liability 939,184 899,938

Trade and other payables 13 2,693,732 2,813,536

Lease liability 14 595,890 19,159

Total liabilities 471,337,660 439,516,008

Net assets 37,134,221 34,535,840

Equity

Accumulated funds 15 21,496,543 19,019,154

Contributions reserve 16(a), 3(g) 14,950,000 14,950,000

Future grants reserve 16(b), 3(h) 1,061,725 966,138

Fair value through other comprehensive income reserve 16(c) (374,047) (399,452)

Total equity 37,134,221 34,535,840 This statement should be read in conjunction with the accompanying notes.

Consolidated Statement of Financial Position

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

10

For the year ended 31 December 2020

Accumulated

Funds Contributions

Reserve Future Grants

Reserve FVOCI Reserve Total

$ $ $ $ $

2020

Balance brought forward 19,019,154 14,950,000 966,138 (399,452) 34,535,840

Net Operating Surplus 4,592,366 - - - 4,592,366

Change in derivative liability - - - (39,246) (39,246)

Fair value change in investments at FVOCI

- - - 64,651 64,651

Total Comprehensive Income 4,592,366 - - 25,405 4,617,771

Grants to Baptist Entities (1,053,252) - (966,138) - (2,019,390)

Transfer (to)/from reserves (1,061,725) - 1,061,725 - -

Balance at 31 December 2020 21,496,543 14,950,000 1,061,725 (374,047) 37,134,221

2019

Balance carried forward 15,659,717 14,950,000 927,478 258,141 31,795,336

Net Operating Surplus 5,503,884 - - - 5,503,884

Change in derivative liability - - - (497,382) (497,382)

Fair value change in investments at FVOCI

- - - (160,211) (160,211)

Total Comprehensive Income 5,503,884 - - (657,593) 4,846,291

Grants to Baptist Entities (1,178,309) - (927,478) - (2,105,787)

Transfer (to)/from Reserves (966,138) - 966,138 - -

Balance at 31 December 2019 19,019,154 14,950,000 966,138 (399,452) 34,535,840 This statement should be read in conjunction with the accompanying notes.

Consolidated Statement of Changes in Equity, Accumulated Funds & Reserves

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

11

For the year ended 31 December 2020 Notes 2020 2019 $ $

Operating services

Interest received from loans 11,700,667 11,606,216

Interest from other investments 4,036,922 5,978,461

Donations, subscriptions & sundry income 5,285 1,513,421

Interest paid to investors (6,497,021) (8,880,624)

Cash paid to suppliers and employees (4,231,858) (4,292,006)

Net cash provided by operating activities 21(2) 5,013,995 5,925,468

Investing activities

Church & other loans advanced (49,455,990) (55,812,525)

Church & other loan payments received 34,087,549 29,893,030

Payments for leasehold improvements, software & web design, furniture & computers

(257,666) (107,721)

Grants paid to Baptist Entities (2,019,390) (2,105,787)

Decrease/ (Increase) in other receivables (828,207) (235,950)

Decrease/ (Increase) in investments (10,993,199) (22,503,110)

Received from investors (net) 31,325,479 51,374,197

Net cash provided by / (used in) investing activities 1,858,576 502,134

Net change in cash and cash equivalents 6,872,571 6,427,602

Cash and cash equivalents, beginning of year 25,250,974 18,823,372

Cash and cash equivalents, end of year 4, 21(1) 32,123,545 25,250,974 This statement should be read in conjunction with the accompanying notes.

Consolidated Statement of Cash Flows

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

12

1. General Information and Statement of Compliance

The financial report includes the consolidated financial statements of Baptist Financial Services Australia Limited (“BFS” or “the Company”) and its controlled entity Baptist Development Australia Pty Ltd (“BDA”) (together "the Group").

These consolidated financial statements are general purpose statements that have been prepared in accordance with Australian Accounting Standards - Reduced Disclosure Requirements, to satisfy the requirements of the Australian Charities and Not-for-profits Commission Act 2012. The consolidated financial report complies with Australian equivalents to International Financial Reporting Standards (AIFRS). Baptist Financial Services Australia Limited is a not for profit entity for the purpose of preparing the financial statements.

The Group has carefully considered the impact of COVID-19 in preparing its financial statements for the year ended 31 December 2020, including the application of critical estimates and judgments. The key area of consideration is impairment of financial assets (refer Note 7).

The consolidated financial statements for the year ended 31 December 2020 were approved and authorised for issue by the Board of Directors on 15 April 2021.

2. Changes in accounting policies

2.1 New standards adopted as at 1 January 2020

Accounting standards issued but not yet effective and not been adopted early by the Group

There were no new accounting standards issued but not yet effective from 1 January 2020 which the group have early adopted deemed to have a significant impact on the Group’s financial results or position.

3. Summary of Significant Accounting Policies

a) Overall consideration

The significant accounting policies that have been used in the preparation of these consolidated financial statements are summarised below. The consolidated financial statements have been prepared using the measurement bases specified by Australian Accounting Standards for each type of asset, liability, income and expense. The measurement bases are more fully described in the accounting policies below.

Australian Accounting Standards set out accounting policies that the AASB has concluded could result in financial statements containing relevant and reliable information about transactions events and conditions. Significant accounting policies adopted in the preparation of these consolidated financial statements have been consistently applied unless otherwise stated.

Notes to the Consolidated Financial Statements

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

13

3. Summary of Significant Accounting Policies (continued)

b) Basis of Consolidation

The Group financial statements consolidate those of the parent company and all of its subsidiaries as of 31 December 2020. The parent controls a subsidiary if it is exposed, or has rights, to variable returns from its involvement with the subsidiary and has the ability to affect those returns through its power over the subsidiary. All subsidiaries have a reporting date of 31 December.

All transactions and balances between Group companies are eliminated on consolidation, including unrealised gains and losses on transactions between Group companies. Where unrealised losses on intra-group asset sales are reversed on consolidation, the underlying asset is also tested for impairment from a group perspective. Amounts reported in the financial statements of subsidiaries have been adjusted where necessary to ensure consistency with the accounting policies adopted by the Group.

Profit or loss and other comprehensive income of subsidiaries acquired or disposed of during the year are recognised from the effective date of acquisition, or up to the effective date of disposal, as applicable.

Non-controlling interests, presented as part of equity, represent the portion of a subsidiary’s profit or loss and net assets that is not held by the Group. The Group attributes total comprehensive income or loss of subsidiaries between the owners of the parent and the non-controlling interests based on their respective ownership interests.

c) Property, Plant and Equipment

Land and Buildings are recognised at cost less any subsequent accumulated depreciation on Buildings and accumulated impairment losses. Property, plant and equipment, with the exception of freehold land, are depreciated on a straight line basis so as to write off the net cost of each asset over its expected useful life to the Company. The useful lives are adjusted if appropriate at each reporting date. Estimated useful lives as at the reporting date are as follows:

Computers 33.33%

Furniture and Equipment 10.00%

Leasehold Improvements Remaining term of lease

The carrying values of Property, Plant and Equipment are reviewed for impairment when events or changes in circumstances indicate the carrying value may not be recoverable.

d) Income Tax

No income tax has been provided for in these consolidated financial statements as the Company has been endorsed by the Australian Taxation Office as an income tax exempt charitable institution, and is also registered as a Charity with the Australian Charities & Not-for-profits Commission.

e) Membership

The Company is a company limited by guarantee. Membership consists of each person who is a member of the Board. At balance date there were 9 members. The liability of members in the event of a deficit upon winding up the Company is limited to $100. If upon winding up there remains a surplus, then the first part of the surplus, up to the limit of Contributions Reserve, will be repaid to the Contributor, and any remaining surplus given or transferred to State Baptist Unions and Associations or, failing that, to some other institution(s) having objectives and restrictions on distributions similar to the Company, such institutions being determined by the members.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

14

3. Summary of Significant Accounting Policies (continued)

f) Financial instruments

Recognition, initial measurement and derecognition

Financial assets and financial liabilities are recognised when the Group becomes a party to the contractual provisions of the financial instrument, and are measured initially at fair value adjusted by transactions costs, except for those carried at fair value through profit or loss, which are measured initially at fair value. Subsequent measurement of financial assets and financial liabilities are described below.

Financial assets are derecognised when the contractual rights to the cash flows from the financial asset expire, or when the financial asset and all substantial risks and rewards are transferred. A financial liability is derecognised when it is extinguished, discharged, cancelled or expires.

Classification and subsequent measurement of financial assets

Except for those trade receivables that do not contain a significant financing component and are measured at the transaction price, all financial assets are initially measured at fair value adjusted for transaction costs (where applicable).

For the purpose of subsequent measurement, financial assets other than those designated and effective as hedging instruments are classified into the following categories upon initial recognition:

amortised cost

fair value through profit or loss (FVPL)

debt instruments at fair value through other comprehensive income (FVOCI)

equity instruments at fair value through other comprehensive income (Equity at FVOCI)

Classifications are determined by both:

The entity’s business model for managing the financial asset

The contractual cash flow characteristics of the financial assets

All income and expenses relating to financial assets that are recognised in profit or loss are presented within finance costs, finance income or other financial items, except for impairment of trade receivables, which is presented within other expenses.

Subsequent measurement financial assets

Financial assets at amortised cost

Financial assets are measured at amortised cost if the assets meet the following conditions (and are not designated as FVPL):

they are held within a business model whose objective is to hold the financial assets and collect its contractual cash flows; and

the contractual terms of the financial assets give rise to cash flows that are solely payments of principal and interest on the principal amount outstanding.

After initial recognition, these are measured at amortised cost using the effective interest method. Discounting is omitted where the effect of discounting is immaterial.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

15

3. Summary of Significant Accounting Policies (continued)

Debt instruments at fair value through other comprehensive income (Debt FVOCI)

Financial assets with contractual cash flows representing solely payments of principal and interest and held within a business model of collecting the contractual cash flows and selling the assets are accounted for at debt FVOCI.

Any gains or losses recognised in OCI will be reclassified to profit or loss upon derecognition of the asset. This category includes investments that were previously classified as held to maturity under AASB 139.

The Group does not have any assets in the categories FVPL or Equity FVOCI.

Impairment of Financial assets

AASB 9’s impairment requirements use more forward looking information to recognise expected credit losses - the ‘expected credit losses model’. Instruments within the scope of the new requirements included loans and other debt-type financial assets measured at amortised cost and FVOCI, trade receivables and loan commitments and some financial guarantee contracts (for the issuer) that are not measured at fair value through profit or loss.

The Group considers a broader range of information when assessing credit risk and measuring expected credit losses, including past events, current conditions, reasonable and supportable forecasts that affect the expected collectability of the future cash flows of the instrument.

In applying this forward-looking approach, a distinction is made between:

financial instruments that have not deteriorated significantly in credit quality since initial recognition or that havelow credit risk (‘Stage 1’) and

financial instruments that have deteriorated significantly in credit quality since initial recognition and whosecredit risk is not low (‘Stage 2’).

‘Stage 3’ would cover financial assets that have objective evidence of impairment at the reporting date.

‘12-month expected credit losses’ are recognised for the first category while ‘lifetime expected credit losses’ are recognised for the second category. Measurement of the expected credit losses is determined by a probability-weighted estimate of credit losses over the expected life of the financial instrument. They are measured as follows:

financial assets that are not credit-impaired at the reporting date: as the present value of all cashshortfalls (i.e. the difference between the cash flows due to BFS in accordance with the contract and thecash flows that BFS expects to receive);

financial assets that are credit-impaired at the reporting date: as the difference between the grosscarrying amount and the present value of estimated future cash flows; and

undrawn loan commitments: as the present value of the difference between the contractual cash flowsthat are due to BFS if the commitment is drawn down and the cash flows that BFS expects to receive.

Credit-impaired financial assets

At each reporting date, BFS assesses whether financial assets carried at amortised cost are credit-impaired. A financial asset is ‘credit-impaired’ when one or more events that have a detrimental impact on the estimated future cash flows of the financial asset have occurred.

Evidence that a financial asset is credit-impaired includes the following observable data:

significant financial difficulty of the borrower or issuer; a breach of contract such as a default or past due event; the restructuring of a loan or advance by BFS on terms that BFS would not consider otherwise; it is becoming probable that the borrower will enter bankruptcy or other financial reorganisation; or the disappearance of an active market for a security because of financial difficulties.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

16

3. Summary of Significant Accounting Policies (continued)

A loan that has been renegotiated due to a deterioration in the borrower’s condition is usually considered to be credit-impaired unless there is evidence that the risk of not receiving contractual cash flows has reduced significantly and there are no other indicators of impairment.

In making an assessment of whether an investment in debt securities is credit-impaired, BFS considers the following factors:

The market’s assessment of creditworthiness as reflected in the bond yields; The rating agencies’ assessments of creditworthiness; The issuer’s ability to access the capital markets for new debt issuance; and The probability of debt being restructured, resulting in holders suffering losses through voluntary or

mandatory debt forgiveness.

Presentation of allowance for expected credit loss (ECL) in the statement of financial position

Loss allowances for ECL are presented in the statement of financial position as follows:

financial assets measured at amortised cost: as a deduction from the gross carrying amount of the assets;

loan commitments: generally, as a provision; and where a financial instrument includes both a drawn and an undrawn component, and BFS cannot

identify the ECL on the loan commitment component separately from those on the drawn component: BFS presents a combined loss allowance for both components. The combined amount is presented as a deduction from the gross carrying amount of the drawn component. Any excess of the loss allowance over the gross amount of the drawn component is presented as a provision.

Write-off

Loans and debt securities are written off (either partially or in full) when there is no realistic prospect of recovery. This is generally the case when BFS determines that the borrower does not have assets or sources of income that could generate sufficient cash flows to repay the amounts subject to the write-off. However, financial assets that are written off could still be subject to enforcement activities in order to comply with BFS’ procedures for recovery of amounts due.

Trade and other receivables

The Group makes use of a simplified approach in accounting for trade and other receivables and records the loss allowance at the amount equal to the expected lifetime credit losses. In using this practical expedient, the Group uses its historical experience, external indicators and forward-looking information to calculate the expected credit losses using a provision matrix. The Group assesses impairment of trade receivables on a collective basis as they possess credit risk characteristics based on the days past due. The Group allows 0% for trade receivables based on their record for collecting outstanding debt.

Classification and measurement of financial liabilities

As the accounting for financial liabilities remains largely unchanged from AASB 139, the Group’s financial liabilities were not impacted by the adoption of AASB 9. However, for completeness, the accounting policy is disclosed below.

The Group’s financial liabilities include customer investments and trade and other payables. Financial liabilities are initially measured at fair value, and, where applicable, adjusted for transaction costs unless the Group designated a financial liability at fair value through profit or loss. Subsequently, financial liabilities are measured at amortised cost using the effective interest method except for derivatives and financial liabilities designated at FVPL, which are carried subsequently at fair value with gains or losses recognised in profit or loss (other than derivative financial instruments that are designated and effective as hedging instruments).

All interest-related charges and, if applicable, changes in an instrument’s fair value that are reported in profit or loss are included within finance costs or finance income.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

17

3. Summary of Significant Accounting Policies (continued)

g) Contributions Reserve

Contributions by State Baptist Unions and Associations to financially support the company are taken to this reserve. In the event of a winding up, these amounts are subordinated to all creditor obligations.

h) Future Grants Reserve

A proportion of the Surplus determined by the Directors is set aside each year to the Future Grants Reserve for Baptist ministry. The allocation of grants is principally in accordance with Memorandums of Understanding entered into between BFS and the Baptist Unions and Associations of New South Wales, Victoria, South Australia, Tasmania, Western Australia and the Baptist Union of Australia Inc. In addition, grants may be made as approved by the Directors to Baptist ministry. There is no expectation of any refund of these grants from the recipients as these funds will be applied to Baptist ministry (refer Note 19).

i) Impairment of intangible assets

Items of computer software which are not integral to the computer hardware and web design owned by the Group are classified as intangible assets. Computer software and web design are amortised over the expected useful life of three years.

j) Revenue

Revenue is recognised to the extent that it is probable that the economic benefits will flow to the entity and the revenue can be reliably measured. The following specific recognition criteria must also be met before revenue is recognised.

Interest earned

Term loans – interest is calculated on the basis of the daily balance outstanding and is charged in arrears to the account on the last day of each month.

Overdraft – interest is calculated initially on the basis of the daily balance outstanding and is charged in arrears to the account on the 1st day of each month.

Non-accrual loan interest – while still legally recoverable, interest is not brought to account as income where the company is informed that the account holder has deceased, or, where a loan is impaired.

Loan origination fees and discounts

Loan establishment fees and discounts, if applicable, are initially deferred as part of the loan balance, and are

brought to account as income over the expected life of the loan as interest revenue.

Transaction costs

Transaction costs are expenses which are direct and incremental to the establishment of the loan. These costs

are initially deferred as part of the loan balance, and are brought to account as a reduction to income over the

expected life of the loan, and included as part of interest revenue.

Fees on loans

The fees charged on loans after origination of the loan are recognised as income when the service is provided or

costs are incurred.

Net gains and losses

Net gains and losses on loans to clients to the extent that they arise from the partial transfer of business or on securitisation, do not include impairment write downs or reversals of impairment write downs.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

18

3. Summary of Significant Accounting Policies (continued)

k) Comparative Figures

Where necessary the comparative figures have been changed to reflect the accounting policies and Accounting Standards applied in the current year.

l) Cash & Cash Equivalents

Cash and cash equivalents include cash on hand, deposits held at-call or on 31 days’ notice with banks and other short-term highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of change in value.

m) Goods and Services Tax (GST)

Where relevant, revenues, expenses and assets are recognised net of the amount of GST, except where the amount of GST incurred is not recoverable from the Australian Taxation Office. In these circumstances the GST is recognised as part of the cost of acquisition of the asset or as part of an item of expense. Receivables and payables in the Statement of Financial Position are shown inclusive of GST.

n) Significant Management Judgement in Applying Accounting Policies

When preparing the financial statements, management undertakes a number of judgements, estimates and assumptions about the recognition and measurement of assets, liabilities, income and expenses.

Estimation uncertainty

Information about estimates and assumptions that have the most significant effect on recognition and measurement of assets, liabilities, income and expenses is provided below. Actual results may be substantially different.

Impairment

In assessing impairment, management estimates the recoverable amount of each asset or cash-generating units, based on expected future cash flows and uses an interest rate to discount them. Estimation uncertainty relates to assumptions about future operating results and the determination of a suitable discount rate.

Useful lives of depreciable assets

Management reviews its estimate of the useful lives of depreciable assets at each reporting date, based on the expected utility of the assets. Uncertainties in these estimates relate to technical obsolescence that may change the utility of certain software and IT equipment.

Long service leave

The liability for long service leave is recognised and measured at the present value of the estimated cash flows to be made in respect of all employees at the reporting date. In determining the present value of the liability, estimates of attrition rates and pay increases through promotion and inflation have been taken into account.

Fair value of financial instruments

Management uses valuation techniques to determine the fair value of financial instruments (where active market quotes are not available) and non-financial assets. This involves developing estimates and assumptions consistent with how market participants would price the instrument. Management bases its assumptions on observable data as far as possible but this is not always available. In that case management uses the best information available. Estimated fair values may vary from the actual prices that would be achieved in an arm’s length transaction at the reporting date.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

19

4. Cash and Cash Equivalents

Cash and cash equivalents, consists of the following: 2020 2019 $ $

Cash and cash equivalents at call 32,123,545 25,250,898

Cash and cash equivalents at 31 days’ notice - 76

Total 32,123,545 25,250,974

5. Loans and Advances – interest bearing 2020 2019

$ $

Secured Loans (see below) 287,518,250 272,423,285

Other interest bearing loans (unsecured) 426,754 499,896

Secured Loans to related entities (Note 22) 2,241,592 1,894,975

Less: Allowance for Impairment of loans (see below) (3,432,810) (3,341,009)

Total Net Loans 286,753,786 271,477,147

Mortgage securities, offset arrangements, an undertaking from the Baptist Churches of New South Wales Property Trust to enter into a Mortgage or guarantees, are held for secured loans and certain loans to related entities.

The average of the total security value held against all secured loans (Loan to Value Ratio - LVR) at 31 December 2020 was 35% (2019: 33%) with a median ratio of 35% (2019: 36%). The current policy of the group is that loans to Baptist entities are not to exceed 75% of the security valuation and loans to other entities are not to exceed 67% of security valuation. This loan to value ratio can be varied by the provision of other appropriate security at the discretion of the Directors. This is not to imply that all existing loans meet these criteria.

6. Financial Commitments

2020 2019 $ $

Outstanding Loan Commitments

Loans approved but not advanced 49,672,497 62,570,437

Loan Redraw Facilities

Loan redraw facilities available 30,815,074 30,437,474

Undrawn Overdraft Loan Facilities

Loan facilities available for overdraft loans are as follows:

Total value of facilities approved 26,263,842 16,835,000

Amounts advanced (included in Secured Loans – Note 5) (18,081,106) (14,374,265)

Net undrawn value 8,182,736 2,460,735

These commitments are contingent on borrowers maintaining credit standards, loan terms & conditions and ongoing repayment terms on amounts drawn.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

20

6. Financial Commitments (continued)

Computer Software Licensing & Maintenance

The Company has costs committed under contracts for software licensing & maintenance as follows:

2020 2019

$ $

Not later than one year 348,473 165,440

Later than one year but not later than two years 154,753 383,975

Later than two years but not later than five years 38,507 189,760

Over five years - -

541,733 739,175

Bureau and Settlement Services The Company has costs committed under a contract for Bureau & Settlement services as follows:

Not later than one year 163,200 160,800

Later than one year but not later than two years - -

Later than two years but not later than five years - -

Over five years - -

163,200 160,800

Analysis of Loans and Advances

2020 2019 $ $

Debts Receivable:

Overdrafts 18,240,274 14,374,265

No longer than 3 months 15,961,790 17,420,341

Longer than 3 months and not longer than 12 months 30,729,788 25,253,472

Longer than 1 year and not longer than 5 years 76,393,776 74,727,523

Longer than 5 years 148,860,968 143,042,555

Allowance for Impairment of Loans (3,432,810) (3,341,009)

286,753,786 271,477,147

7. Impairment of Financial Assets 2020 2019

$ $

Expected credit loss on loans:

Opening balance 3,341,009 3,444,015

Charge for the year 91,802 (103,006)

Amount written off - -

Closing balance 3,432,810 3,341,009

Measures to support loan clients impacted by COVID-19 were implemented during the period. At their peak these measures applied to approximately 15% of the loan book. However, by year end the majority of these clients no longer required this temporary support, with measures remaining in place for approximately 3% of the loan book. One loan client moved from Stage 1 to Stage 2 following the onset of COVID-19 due to a combination of COVID related and other factors.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

21

The expected credit loss breakdown is as follows:

Stage 1 Stage 2 Stage 3

12 months ECL

Collectively assessed

Lifetime ECL Individually assessed

Lifetime ECL Individually assessed

Total

Secured lending 1,449,420 1,927,537 - 3,376,957

Unsecured lending 39,818 16,035 - 55,853

Total 1,489,238 1,943,572 - 3,432,810

8. Other Receivables & Prepayments 2020 2019

$ $

Interest Accrued 289,874 566,717

Other Receivables 1,241,656 413,468

1,531,530 980,185

9. Investments 2020 2019 $ $

Investments held at fair value through other comprehensive income by credit rating (S&P)

AAA 56,546,305 6,696,822

AA 101,081,108 124,604,853

A 8,406,500 21,583,149

BBB 13,694,615 18,392,987

BB 6,111,512 1,500,500

Not rated 1,216,000 3,219,881

187,056,041 175,998,192

2020 2019

Reconciliation of fair value movement during the year: $ $

Opening Balance 500,486 660,697

Fair value adjustments during the year 64,651 (160,211)

Closing Balance 565,137 500,486

Investments – Maturity Analysis 2020 2019

$ $

At call - -

Not longer than 3 months 67,238,246 79,940,234

Longer than 3 months and not longer than 12 months 37,028,098 51,494,510

Longer than 1 year and not longer than 2 years 28,430,856 14,589,550

Longer than 2 years and not longer than 3 years 26,827,736 4,268,498

Longer than 3 years and not longer than 4 years 20,521,743 4,472,454

Longer than 4 years and not longer than 5 years 6,024,531 11,427,629

Longer than 5 years - 8,886,067

Maturity at discretion of issuer 984,830 919,250

187,056,041 175,998,192

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

22

10. Property, plant and equipment 2020 2019 $ $

Furniture and Equipment

Leasehold Improvements, Furniture & Computers - at cost (opening) 283,138 472,930

Additions 147,164 22,070

Disposals - (211,862)

Leasehold Improvements, Furniture & Computers - at cost (closing) 430,302 283,138

Accumulated Depreciation (opening) (218,895) (372,052)

Disposals - 211,862

Depreciation (38,348) (58,705)

Accumulated Depreciation (closing) (257,243) (218,895)

173,059 64,243

Intangible Assets

Software & Web Design - at cost (opening) 566,425 830,682

Additions 110,503 82,805

Disposals - (347,062)

Software & Web Design - at cost (opening) 676,928 566,425

Accumulated Amortisation (opening) (304,458) (610,081)

Amortisation (116,990) (41,439)

Disposals - 347,062

Accumulated Amortisation (closing) (421,448) (304,458)

255,480 261,967

428,539 326,210

11. Right-Of-Use Assets 2020 2019 $ $

Right-of-use Assets

Right-of-use assets 727,308 21,985

Less: Accumulated Depreciation (148,868) (2,845)

578,440 19,140

The company has recognised right of use assets of $705,320 and lease liabilities of $705,320 at 1 January 2020 for Macquarie Park. The right-of-use assets related to office premises and items of office equipment. The incremental borrowing rate used as the discount rate to determine lease liabilities on initial recognition was 4.0%. This rate was determined by estimating the discount rate implied by the lease terms compared with outright purchase.

12. Payables

Payables – Interest bearing based on actual maturity date

2020 2019

$ $

Investments at call 160,046,451 122,065,240

Investments at 31 days’ notice 101,014,371 111,438,968

Term Investments 206,048,032 202,279,167

467,108,854 435,783,375

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

23

Payables – Interest bearing based on withdrawal experience

Current Liabilities – payable not later than 12 months

Investments from Baptist & Christian organisations 35,525,352 34,868,949

Loan offset Savings Accounts 6,978,019 4,821,466

Investments from Individuals & other organisations 13,549,691 12,603,590

56,053,062 52,294,005

Non-Current Liabilities - payable later than 12 months

Investments from Baptist & Christian organisations 260,519,248 255,705,625

Loan offset Savings Accounts 51,172,140 35,357,418

Investments from Individuals & other organisations 99,364,404 92,426,327

411,055,792 383,489,370

Investments are classified according to maturity date and the rollover experience

Term Investments and BFS Borrowings from Clients – Maturity Analysis

At call 160,046,451 122,065,240

Longer than at call and not longer than 3 months 173,880,332 201,005,280

Longer than 3 months and not longer than 12 months 116,032,612 88,209,034

Longer than 1 year and not longer than 2 years 15,539,647 17,882,972

Longer than 2 years and not longer than 5 years 1,609,812 6,620,849

Longer than 5 years - -

467,108,854 435,783,375

Concentration of Payables

There were no individuals or organisations which in aggregate represent more than 10% of the liabilities for Payables - Interest Bearing. The majority of the payables are with Baptist Churches in Australia or with individuals or organisations having an association with Baptist Churches in Australia.

13. Trade and Other Payables

2020 2019 $ $

Accrued term investment interest 1,716,863 2,045,568

Sundry creditors 589,907 463,299

Employee benefit provisions 386,962 299,669

Make good provision - 5,000

Total trade and other payables 2,693,732 2,813,536

14. Lease Liability

2020 2019 $ $

Lease liability 595,890 19,159

Lease liability 595,890 19,159

The incremental borrowing rate used as the discount rate to determine lease liabilities on initial recognition was 4.0% (refer to Note 11).

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

24

15. Accumulated Funds2020 2019

$ $

Accumulated Funds - Total

Balance at beginning of year 19,019,154 15,659,717

Operating Surplus 4,592,366 5,503,884

Grants expended to Baptist ministries (1,053,252) (1,178,309)

Transfer (to)/from Reserves (1,061,725) (966,138)

Balance at end of year 21,496,543 19,019,154

Accumulated Funds - New South Wales & ACT

Balance at beginning of year 10,620,332 8,631,652

Share of Operating Surplus before Grants 2,780,642 3,204,802

Share of Grants expended to Baptist ministries (580,339) (644,198)

Transfer (to)/from Reserves (660,085) (571,924)

Balance at end of year 12,160,551 10,620,332

Accumulated Funds - Victoria

Balance at beginning of year 2,594,306 2,147,320

Share of Operating Surplus before Grants 650,208 811,418

Share of Grants expended to Baptist ministries (210,951) (235,884)

Transfer (to)/from Reserves (131,776) (128,548)

Balance at end of year 2,901,787 2,594,306

Accumulated Funds - South Australia

Balance at beginning of year 2,412,039 2,041,178

Share of Operating Surplus before Grants 439,962 584,043

Share of Grants expended to Baptist ministries (92,326) (106,526)

Transfer (to)/from Reserves (104,290) (106,656)

Balance at end of year 2,655,385 2,412,039

Accumulated Funds - Northern Territory

Balance at beginning of year 55,644 42,031

Share of Operating Surplus before Grants 17,422 18,502

Share of Grants expended to Baptist ministries (902) (974)

Transfer (to)/from Reserves (4,956) (3,915)

Balance at end of year 67,208 55,644

Accumulated Funds – Tasmania

Balance at beginning of year 350,846 303,608

Share of Operating Surplus before Grants 76,530 90,867

Share of Grants expended to Baptist ministries (27,146) (30,044)

Transfer (to)/from Reserves (14,815) (13,585)

Balance at end of year 385,415 350,846

Accumulated Funds - Western Australia

Balance at beginning of year 2,777,145 2,302,758

Share of Operating Surplus before Grants 566,489 738,864

Share of Grants expended to Baptist ministries (111,148) (128,049)

Transfer (to)/from Reserves (136,601) (136,428)

Balance at end of year 3,095,884 2,777,145

Accumulated Funds - Baptist Union of Australia

Balance at beginning of year 208,841 191,169

Share of Operating Surplus before Grants 61,113 55,388

Share of Grants expended to Baptist ministries (30,439) (32,634)

Transfer (to)/from Reserves (9,202) (5,082)

Balance at end of year 230,313 208,841

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

25

In accordance with Memorandums of Understanding entered into between BFS and the Baptist Unions and Associations of New South Wales, Victoria, South Australia, Tasmania, Western Australia and the Baptist Union of Australia Inc, a portion of the surpluses will be allocated in accordance with the directions of those entities.

16. Reserves

a. Contributions Reserve

2020 2019 $ $

Contributions Reserve - Total

Balance at beginning of year 14,950,000 14,950,000

Contributions Received - -

Balance at end of year 14,950,000 14,950,000

Contributions Reserve - New South Wales

Balance at beginning of year 8,000,000 8,000,000

Contribution Received - -

Balance at end of year 8,000,000 8,000,000

Contributions Reserve - Victoria

Balance at beginning of year 3,250,000 3,250,000

Contribution Received - -

Balance at end of year 3,250,000 3,250,000

Contributions Reserve - South Australia

Balance at beginning of year 1,275,000 1,275,000

Contribution Received - -

Balance at end of year 1,275,000 1,275,000

Contributions Reserve - Tasmania

Balance at beginning of year 425,000 425,000

Contribution Received - -

Balance at end of year 425,000 425,000

Contributions Reserve - Western Australia

Balance at beginning of year 1,500,000 1,500,000

Contribution Received - -

Balance at end of year 1,500,000 1,500,000

Contributions Reserve - Baptist Union of Australia

Balance at beginning of year 500,000 500,000

Contribution Received - -

Balance at end of year 500,000 500,000

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

26

16. Reserves (continued)

b. Future Grants Reserve2020 2019

$ $

Future Grants Reserve - Total

Balance at beginning of year 966,138 927,478

Transfer (to)/from accumulated funds (See Note 15) 1,061,725 966,138

Expended during current year (966,138) (927,478)

Balance at end of year 1,061,725 966,138

Future Grants Reserve - New South Wales

Balance at beginning of year 571,924 523,724

Transfer (to)/from accumulated funds 660,085 571,924

Grants expended to Baptist ministries (571,924) (523,724)

Balance at end of year 660,085 571,924

Future Grants Reserve - Victoria

Balance at beginning of year 128,548 120,160

Transfer (to)/from accumulated funds 131,776 128,548

Grants expended to Baptist ministries (128,548) (120,160)

Balance at end of year 131,776 128,548

Future Grants Reserve - South Australia

Balance at beginning of year 106,656 114,244

Transfer (to)/from accumulated funds 104,290 106,656

Grants expended to Baptist ministries (106,656) (114,244)

Balance at end of year 104,290 106,656

Future Grants Reserve - Northern Territory

Balance at beginning of year 3,915 4,083

Transfer (to)/from accumulated funds 4,956 3,915

Grants expended to Baptist ministries (3,915) (4,083)

Balance at end of year 4,956 3,915

Future Grants Reserve - Tasmania

Balance at beginning of year 13,585 12,746

Transfer (to)/from accumulated funds 14,815 13,585

Grants expended to Baptist ministries (13,585) (12,746)

Balance at end of year 14,815 13,585

Future Grants Reserve - Western Australia

Balance at beginning of year 136,428 138,177

Transfer (to)/from accumulated funds 136,601 136,428

Grants expended to Baptist ministries (136,428) (138,177)

Balance at end of year 136,601 136,428

Future Grants Reserve - Baptist Union of Australia

Balance at beginning of year 5,082 14,344

Transfer (to)/from accumulated funds 9,202 5,082

Grants expended to Baptist ministries 5,082 (14,344)

Balance at end of year 9,202 5,082

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

27

16. Reserves (continued)c. Fair value through other comprehensive income reserve

2020 2019$ $

Balance at beginning of year (399,452) 258,141

Changes in derivative liability (39,246) (497,382)

Fair value change in investments at FVOCI (Note 9) 64,651 (160,211)

Balance at end of year (374,047) (399,452)

17. Risk Management

Risk management framework

The Board of Directors has overall responsibility for the establishment and oversight of the Consolidated Entity's risk management framework. The Board maintains an Audit, Risk & Compliance Committee (ARCCo), an Assets & Liabilities Committee (ALCo), a Board Governance & Remuneration Committee (BGRCo) and a Credit Committee (CCo) to oversee the financial reporting and audit and risk management processes.

The ARCCo’s major role, within the BFS risk management organisational structure, is to monitor BFS’s approved policies and procedures in relation to:

Internal Controls & Risk Management Statutory and Financial Reporting Requirements Auditor Independence & Performance Internal Audit Compliance with Law, Regulations & Policies Review any other matters as determined by the Board from time to time.

The ALCo’s major role is to monitor BFS’s approved policies and procedures in relation to the management and control of:

Credit Risk Liquidity Risk Market Risk Balance Sheet Risk Capital Management Risk

The BGRCo's major role is to make recommendations to the Board in respect of:

The Nomination and Roles of New Directors The Nomination of Directors to Board Committees Annual Board & Committee Assessment Professional Development of Directors & Staff Conflict of Interest Disclosure & Management The Selection, Interview of a CEO, Establish Objectives and Review Performance The Selection, Interview of Special Board Appointees and Review Performance in conjunction with the

CEO the Monitoring of staff performance & salaries, director remuneration, continuous improvement systems

and processes with the CEO

The CCo’s major role is to approve certain loans or variations to existing loans within delegated limits from the Board and to recommend changes to Loans Policy to the Board.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

28

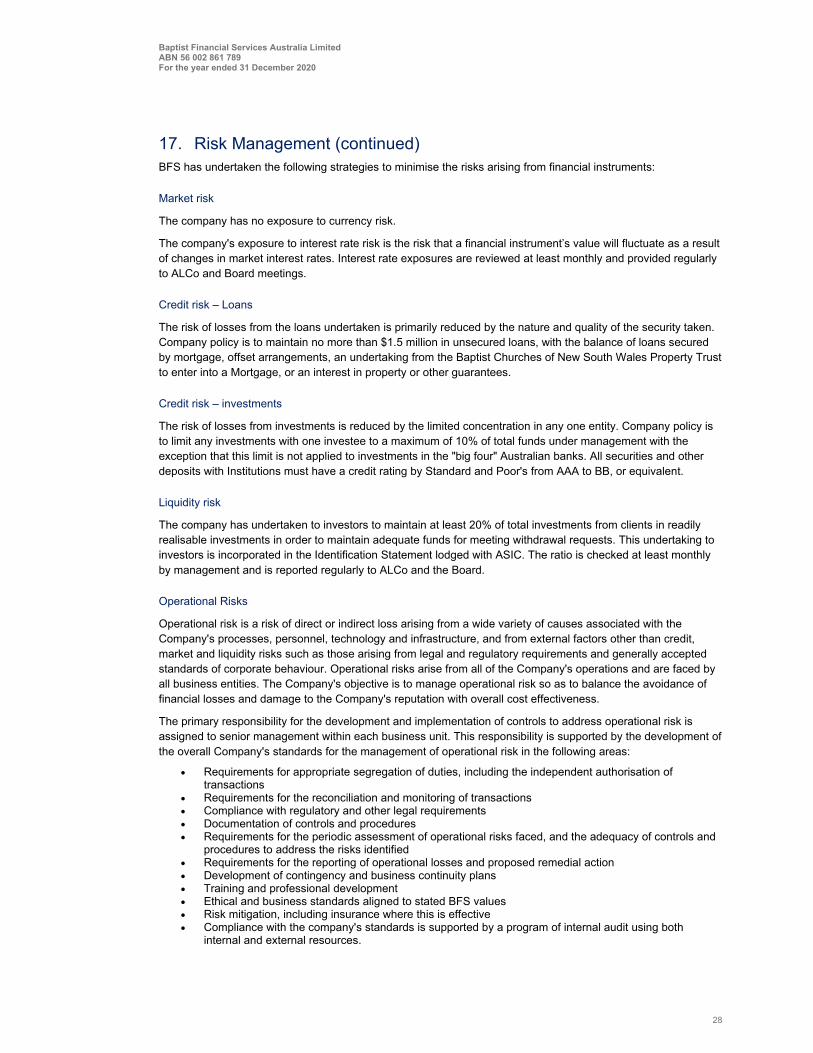

17. Risk Management (continued)BFS has undertaken the following strategies to minimise the risks arising from financial instruments:

Market risk

The company has no exposure to currency risk.

The company's exposure to interest rate risk is the risk that a financial instrument’s value will fluctuate as a result of changes in market interest rates. Interest rate exposures are reviewed at least monthly and provided regularly to ALCo and Board meetings.

Credit risk – Loans

The risk of losses from the loans undertaken is primarily reduced by the nature and quality of the security taken. Company policy is to maintain no more than $1.5 million in unsecured loans, with the balance of loans secured by mortgage, offset arrangements, an undertaking from the Baptist Churches of New South Wales Property Trust to enter into a Mortgage, or an interest in property or other guarantees.

Credit risk – investments

The risk of losses from investments is reduced by the limited concentration in any one entity. Company policy is to limit any investments with one investee to a maximum of 10% of total funds under management with the exception that this limit is not applied to investments in the "big four" Australian banks. All securities and other deposits with Institutions must have a credit rating by Standard and Poor's from AAA to BB, or equivalent.

Liquidity risk

The company has undertaken to investors to maintain at least 20% of total investments from clients in readily realisable investments in order to maintain adequate funds for meeting withdrawal requests. This undertaking to investors is incorporated in the Identification Statement lodged with ASIC. The ratio is checked at least monthly by management and is reported regularly to ALCo and the Board.

Operational Risks

Operational risk is a risk of direct or indirect loss arising from a wide variety of causes associated with the Company's processes, personnel, technology and infrastructure, and from external factors other than credit, market and liquidity risks such as those arising from legal and regulatory requirements and generally accepted standards of corporate behaviour. Operational risks arise from all of the Company's operations and are faced by all business entities. The Company's objective is to manage operational risk so as to balance the avoidance of financial losses and damage to the Company's reputation with overall cost effectiveness.

The primary responsibility for the development and implementation of controls to address operational risk is assigned to senior management within each business unit. This responsibility is supported by the development of the overall Company's standards for the management of operational risk in the following areas:

Requirements for appropriate segregation of duties, including the independent authorisation oftransactions

Requirements for the reconciliation and monitoring of transactions Compliance with regulatory and other legal requirements Documentation of controls and procedures Requirements for the periodic assessment of operational risks faced, and the adequacy of controls and

procedures to address the risks identified Requirements for the reporting of operational losses and proposed remedial action Development of contingency and business continuity plans Training and professional development Ethical and business standards aligned to stated BFS values Risk mitigation, including insurance where this is effective Compliance with the company's standards is supported by a program of internal audit using both

internal and external resources.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

29

17. Risk Management (continued)

Average Balance Sheet and Interest Rates

The effective weighted average interest rates on classes of financial assets and financial liabilities are as follows:

Average Balance

Interest (At rates applicable

at balance date) Average Rate

$ $ %

2020

Financial Assets

Cash and liquid assets 32,277,966 191,982 0.59

Investments with other financial institutions 177,975,150 3,618,346 2.03

Loans and Advances 280,201,697 13,567,578 4.84

490,454,813 17,377,906 3.54

Financial Liabilities

Client Investments 453,212,245 8,053,757 1.78

2019

Financial Assets

Cash and liquid assets 21,672,892 338,322 1.56

Investments with other financial institutions 179,043,977 5,133,790 2.87

Loans and Advances 257,650,001 13,297,331 5.16

458,366,870 18,769,443 4.09

Financial Liabilities

Client Investments 425,355,896 10,231,619 2.41

Credit Risk

The maximum exposure to credit risk at balance date in relation to loans and advances is the carrying amount.

At balance date this amounted to $286,753,786 (2019: $271,477,147). Loans and advances primarily comprise commercial loans to Baptist and other Christian entities secured by mortgage over freehold property, offset arrangements or an interest in property. The loan portfolio comprises a mix of loan to value ratios, ranging from conservative to high.

The total risk exposure for all unimpaired loans exceeding $2 million at balance date was $163,086,453 representing 38 borrowers (2019: 30 totalling $124,842,765). Each of these loans is fully secured by mortgage over freehold property, offset arrangements or an interest in property.

The total of loans past due are $49,945 at year end (2019: $128,026).

Refer to Note 7 for further explanation of the Allowance for Impairment.

There is no credit risk exposure to any single borrower or group of borrowers under financial instruments entered into by it which in aggregate represents more than 10% of Loans and advances - interest bearing.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

30

18. Other Expenses

2020 2019$ $

Website, Software and Computer Systems 414,353 310,249

Occupancy 56,389 122,783

Depreciation and Amortisation 301,360 102,989

Other General Administration Expenses 1,058,467 1,235,204

Total Other Expenses 1,830,569 1,765,780

19. Net Operating Surplus

2020 2019$ $

Operating surplus 4,592,366 5,503,884

Is arrived at after including as revenue:

Interest earned 15,460,726 17,131,568

And after charging as expenses:

Auditor’s Remuneration

Audit Fees – Grant Thornton Audit Pty Ltd 73,630 72,200

(No other benefits were received by the auditor)

Amortisation and Depreciation of software, furniture & equipment andleasehold improvements

155,337 100,145

Depreciation of right-of-use assets 146,023 2,845

Interest incurred 6,550,336 8,946,629

Employee benefits and costs 2,401,808 2,442,479

Payment of Grants are shown in the Statement of Changes in Accumulated Funds and Reserves

Grants paid from current year result 1,053,252 1,178,309

Grants paid from Future Grants Reserve 966,138 927,478

The total number of employees at balance date was 22 (2019: 19) which represented 20.2 (2019: 18.0) full-time equivalent (FTEs).

20. Other Information

The Company is a National Baptist Ministry, being a Delegated Body of the Baptist Union of Australia Inc, and provides the facilitation of the financing of Baptist entities affiliated with participating Baptist Unions and other Christian Churches & organisations.

The Company holds and operates with an Australian Financial Services Licence - AFSL 311062.

A long term objective of BFS is to assist churches and ministries as they pursue development opportunities and realise increased resources for ministry. These activities are a particular focus of its controlled entity Baptist Development Australia Pty Ltd.

Baptist Financial Services Australia Limited ABN 56 002 861 789 For the year ended 31 December 2020

31

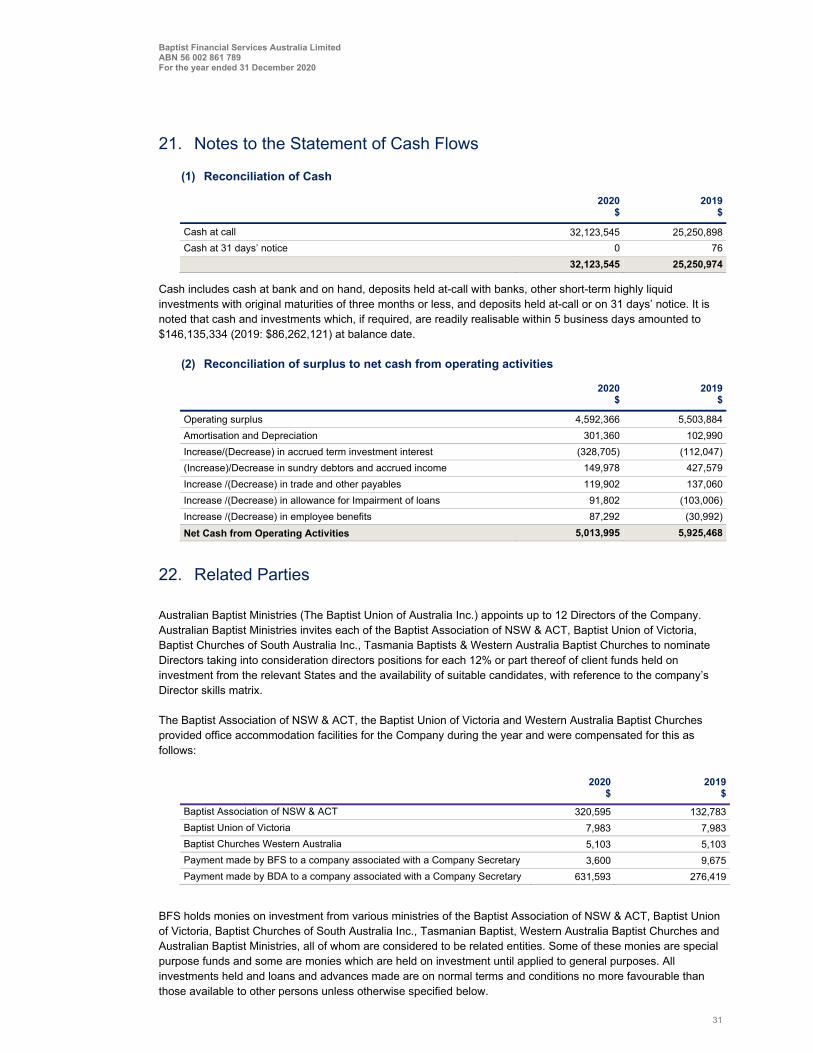

21. Notes to the Statement of Cash Flows

(1) Reconciliation of Cash

2020 2019$ $

Cash at call 32,123,545 25,250,898

Cash at 31 days’ notice 0 76

32,123,545 25,250,974

Cash includes cash at bank and on hand, deposits held at-call with banks, other short-term highly liquid investments with original maturities of three months or less, and deposits held at-call or on 31 days’ notice. It is noted that cash and investments which, if required, are readily realisable within 5 business days amounted to $146,135,334 (2019: $86,262,121) at balance date.

(2) Reconciliation of surplus to net cash from operating activities

2020 2019$ $

Operating surplus 4,592,366 5,503,884

Amortisation and Depreciation 301,360 102,990

Increase/(Decrease) in accrued term investment interest (328,705) (112,047)

(Increase)/Decrease in sundry debtors and accrued income 149,978 427,579

Increase /(Decrease) in trade and other payables 119,902 137,060

Increase /(Decrease) in allowance for Impairment of loans 91,802 (103,006)

Increase /(Decrease) in employee benefits 87,292 (30,992)

Net Cash from Operating Activities 5,013,995 5,925,468

22. Related Parties

Australian Baptist Ministries (The Baptist Union of Australia Inc.) appoints up to 12 Directors of the Company. Australian Baptist Ministries invites each of the Baptist Association of NSW & ACT, Baptist Union of Victoria, Baptist Churches of South Australia Inc., Tasmania Baptists & Western Australia Baptist Churches to nominate Directors taking into consideration directors positions for each 12% or part thereof of client funds held on investment from the relevant States and the availability of suitable candidates, with reference to the company’s Director skills matrix.

The Baptist Association of NSW & ACT, the Baptist Union of Victoria and Western Australia Baptist Churches provided office accommodation facilities for the Company during the year and were compensated for this as follows:

2020 2019$ $

Baptist Association of NSW & ACT 320,595 132,783

Baptist Union of Victoria 7,983 7,983

Baptist Churches Western Australia 5,103 5,103

Payment made by BFS to a company associated with a Company Secretary 3,600 9,675

Payment made by BDA to a company associated with a Company Secretary 631,593 276,419