Embed Size (px)

Citation preview

N9-708-511J U N E 2 , 2 0 0 8

________________________________________________________________________________________________________________ Professors Ramon Casadesus-Masanell and Neil Campbell (MBA 2008) prepared this case. This case was developed from published sources. HBS cases are developed solely as the basis for class discussion. Cases are not intended to serve as endorsements, sources of primary data, or illustrations of effective or ineffective management. Copyright © 2008 President and Fellows of Harvard College. To order copies or request permission to reproduce materials, call 1-800-545-7685, write Harvard Business School Publishing, Boston, MA 02163, or go to http://www.hbsp.harvard.edu. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any means—electronic, mechanical, photocopying, recording, or otherwise—without the permission of Harvard Business School.

R A M O N C A S A D E S U S - M A S A N E L L

N E I L C A M P B E L L ( M B A 2 0 0 8 )

Betfair vs. UK Bookmakers

“One of the great things about Betfair was that it was just the most disruptive idea imaginable to the betting industry. It drove a cart and horses through the whole bloody lot of it. And quite right, too.”

— Andrew Black, Betfair Co-founder, 20041

"Betfair, which started trading three years ago this Derby weekend, was labeled illegal by John Brown, chairman of William Hill, and it was a group of bookmakers in Australia who called [Betfair’s representative] a parasite.”

— The Guardian, 20032

In January 2008, Edward Wray, Chairman of Betfair reflected on what had been an incredible past 9 years. Since 1999, he and his co-founder, Andrew Black had built Betfair from the idea of applying free market principles to sports betting into the dominant global betting exchange, which grew at over 25% per year.3

Betting exchanges provided a platform for the general public to anonymously place bets between each other, cutting out the middle-man role traditionally played by the bookmaker. For creating such a system, Betfair endured the aggressive and prolonged attacks from the established bookmakers, overcame accusations that their website facilitated cheating in sports, and countered criticism from politicians and racing authorities that their service undermined the operation of the very sports that it relied upon.

But Betfair had weathered these criticisms admirably and built a highly successful business. Although still privately held, the April 2006 sale of 23% of the company’s equity to the Japanese technology group Softbank had valued the company at £1.5bn,4 on a par with the valuations of its largest incumbent rivals, Ladbrokes and William Hill (valued at £1.96bn and £1.43bn respectively).5

Having established itself in UK sports betting, Betfair had become the website of choice for professional gamblers and had attracted a dynamic younger consumer who would ‘trade’ in sports betting. Now, Wray had to determine what options to pursue to push the business forward to even further growth, and what elements of their extremely successful business model were worth sacrificing to do so. Should they capitalize on their brand name recognition by attracting the more casual punters that made up the majority of UK betters by offering Starting Price (SP) services and

708-511 Betfair vs. UK Bookmakers

2

multiples betting? Alternatively, should they push ahead with efforts to become the dominant exchange in every possible international market? Finally, could their brand name and reputation for fairness be used to expand their product portfolio further? While they had already added online poker and casino gaming, should they also be offering markets on subjects as varied as the weather, securities price movements, and other uncertain events?

The UK’s love affair with betting6

With over £44.4bna, staked in 2006 (£733 per capita) on sports betting7, the UK was truly the betting capital of the world (See Exhibit 1). While betting on other sports had increased markedly, the UK betting industry was intrinsically linked to horseracing, with estimates indicating that it accounted for a majority (though in recent years declining) share of all bets placed.8

Horseracing in the UK dated back to races organized by Roman soldiers in 200 AD; but the first recorded race was not held until 1174 at a horse fair in Smithfield, London. Early in the 16th century, investments in horse breeding, made by Henry VIII and James I, established the breeding of thoroughbreds and the establishment of the racing industry in Newmarket, Suffolk. After the end of England’s brief experience of Puritanism under Oliver Cromwell, horseracing flourished and was formally organized with the formation of the Jockey Club in 1752. Royal involvement in horse-racing continued to the present day with the sport colloquially referred to as “the sport of kings” and the Queen and other Royals being regular attendees at racing events, especially Royal Ascot, a 5 day racing festival held in June each year and run on crown-owned land.

Horseracing in the UK remained an integral part of the national consciousness. All leading race meetings were regularly televised on national television and nearly 50% of the population bet on the Grand National9 (the sport’s biggest race) either via bookmakers or within informally organized sweepstakes. Indeed, the most famous jockeys, such as flat jockey Frankie Dettori, and even the horses themselves were widely known celebrities.

Gambling on horseracing was as old as the sport itself and the bookmaking industry arose out of both the spectators wishing to profit from their knowledge and judgment, and racecourses seeking revenue by allowing individuals (the bookmakers) to operate on racecourses in exchange for a proportion of their earnings. In the early days of the industry, bookmaking was restricted to on-course betting; only those present at the racetrack could accept a bet.

Off-course betting was formally legalized by the Betting & Gaming Act of 1960.10 This legalization gave rise to an explosion in betting shops across UK high streets with over 8,700 existing by 200611 (See Exhibit 2). The taxation of gambling had also been revised over the years. Originally members of the public were taxed via a 9% charge on their winnings while bookmakers paid standard corporation tax on their operations. In 2001, this was changed to a gross profits tax where bookmakers paid the government 15% of their gross winb. This change was a major boost to the gambling industry since consumers received more money back and had a tendency to re-bet their winnings creating a multiplicative effect that boosted the overall market size. The bookmakers also continued to pay UK corporation tax on the net profits from their businesses. In addition to these cash flow streams flowing to the government, bookmakers also paid out to other parties. The most prominent of these was a statutory ‘levy’ imposed by the government that required that all

a £1 = $1.996, www.oanda.com accessed on April 22nd 2008. b Gross Win is defined as the amount of money that a bookmaker accepts in bets minus any winnings that are paid out to consumers.

Betfair vs. UK Bookmakers 708-511

bookmakers pay 10% of their gross win from horseracing to the British Horseracing Board to fund the horseracing industry, including the upkeep of courses, prize money, and training programs. Such funding was vital in allowing the industry to survive. Other sports, such as greyhound racing, also had levies that, although not statutory, were paid voluntarily by all major bookmakers.c

A beginner’s guide to traditional betting Over time, betting developed its own particular terminology and ways of operating. Individuals

who were willing to place money in order to gain from predicting that a specific outcome would occur in a particular uncertain event were referred to as “punters” due to their willingness to take a chance (“a punt” in colloquial slang) on that outcome occurring. In order to attract a punter’s money the bookmaker offered “odds” (also referred to as prices) on a particular outcome occurring. These odds reflected the payment that a bookmaker would make to a punter should his/her choice win.

“Bookmakers” (also known as “bookies” or “turf accountants”) were the individuals who took bets from punters and paid them out after the event occurred. Bookmakers therefore profited when an outcome that they had accepted a bet on failed to materialize. The term ‘bookmaker’ referred to the fact that they maintained a ‘book’ of bets and had to manage their exposure to any one of many possible outcomes in an event. Bookmakers often hedged their exposure by placing bets that reduced their exposure to one outcome by placing an offsetting bet with another bookmaker.

Odds were traditionally expressed as “fractional odds” such as 3/1 or 5/2 (pronounced “3 to 1” or “5 to 2”). This meant that if you were offered odds of 5/2 (e.g. on Liverpool to win their upcoming soccer match) then, if you placed a $1 bet (the “stake”) then if Liverpool won, you would receive 5 ÷ 2 x 1 = $2.50 + the return of the initial stake of $1 to give a total return of $3.50. On the other hand, if Liverpool did not win (they lose or the match is tied), you would lose the $1 stake; this was the bookmaker’s profit.

By betting such that he/she profited if a specific outcome occurred, the punter was said to be “backing” that participant. On the other side of the transaction (traditionally the bookmaker’s role), the person who profited when the outcome didn’t occur was said to be “laying” against that outcome. To attract a punter’s custom, those laying would compete with each other by offering “longer” (i.e. higher) odds on an outcome and thus the higher odds can be thought of as a lower (more attractive) price to the consumer.d The participant with the shortest odds was referred to as the “favorite” as it is considered the most likely to win. Less sophisticated gamblers were more likely to back the favorite in any one event, making the odds on the favorite a key way for bookmakers to attract custom.

In reality, the odds of a particular outcome reflected an “implied probability” of that outcome occurring. This probability can be calculated via a simple formula:

)1(1yProbabilitOdds+

= e.g. For 5/2: %29)5.21(

1)2/51(

1yProbabilit =+

=+

=

By summing up the individual implied probabilities, an indication of the competitiveness of the prices for a certain event could be calculated. This sum was called the “total percentage” or “book percentage” and it would always to sum to over 100%. If it did not add to more than 100% a profit c Casewriter’s interview with Edward Wray, May 2008 d In comparison to financial markets, backing an outcome is the equivalent of buying / going long on a security whereas laying an outcome is the equivalent of selling / shorting the security.

3

708-511 Betfair vs. UK Bookmakers

4

could be guaranteed regardless of outcome by betting on each outcome in proportion to its implied probability. The ‘over-round’ was defined as the book percentage minus 100% and the closer the over-round was to 0% the more competitive the odds offered for an event were. Conversely, the higher the over-round, the more profit was retained on average by the bookmaker. (See Exhibit 3a for an example).

Bookmakers also competed by offering further products to punters. In particular, “Starting Prices” and “Accumulators” were ubiquitous. A starting price (SP) allowed punters to place a bet in advance of the event but to receive the odds that prevailed just prior to the start of the event. This service reflected the reality that the parading of horses prior to the race allowed on-course punters to assess their demeanor and appearance and therefore better judge their chances of winning and that line-ups often changed at short notice. The odds for outcomes of a particular race could thus change dramatically in the thirty minutes before a race, thereby seriously disadvantaging those who had placed earlier bets. The starting price was determined using all available information near the start of the race by the market consensus of the bets the bookmakers had taken. It was not always the most competitive price for the punter (especially since the largest bookmakers could place bets at the racecourse to reduce the odds and hence their national exposure),e yet the service proved popular.

Accumulators (otherwise known as multiples betting) simply linked the money staked on several events together, allowing the punter to increase their payout when they correctly predicted the outcomes of several independent events. It was as if, on winning on one event the payout is automatically placed on the next bet thus multiplying the ultimate payout. In this way, punters with a relatively small stake could create very long odds by picking likely outcomes in several events rather than an unlikely outcome in just one event. However, if any bet did not win, all the money was lost. In providing an accumulator service the bookmaker was taking an added level of risk, since at the point of accepting the accumulator he had to quote prices for events, but when the time came to place the money on a later event the odds may have moved.

Traditional High Street Bookmakers As with betting in the UK, bookmakers originated as a purely on-course phenomenon, competing

with other on-course bookmakers to attract customers. (See Exhibit 4). The principal method to attract customers was via the price on the ‘favorite’, the horse thought most likely to win the race with the shortest odds. Bookmakers therefore adjusted the odds they offered based on two sources of information. Firstly, they used their knowledge of the horse’s past success (documented by national and trade newspapers such as the Racing Post), relationships with the trainers, and the viewing of the horse as it paraded before the race to adjust the odds of the horse. Secondly, they considered the bets they were receiving from punters on the racetrack to both gauge public opinion about a horse’s chances of winning and to manage their own exposure. Therefore, as they accepted bets in the run up to the start of a race, they constantly adjusted odds on their chalkboards to manage their exposure to various outcomes. Once the race was “under starter’s orders” and ready to begin, all further betting was suspended.

In addition to taking bets from the public, bookmakers also did business with each other. If a bookmaker felt too exposed to one particular outcome they had two courses of action they could follow. Firstly, they could hedge their exposure by taking a share of the bets they had collected on that outcome and back that outcome with another bookmaker. In this way if that particular outcome occurred they would also profit and could use this profit to pay part of their own obligations. (See e Casewriter’s interview with Edward Wray, May 2008

Betfair vs. UK Bookmakers 708-511

5

Exhibit 3b for an example). Secondly, they would shorten the odds on this outcome to ensure that they attracted less money on that particular outcome. This simultaneously signaled to other bookmakers that they had taken a lot of money on that outcome and they would adjust their prices accordingly. In this way, a certain level of arbitrage occurred between rival bookmakers, which kept prices close together.

Bookmaking was a regulated industry. To reassure customers that bookmakers had the financial resources to pay out on winning bets and to restrict supply, bookmakers were required to be licensed before they could operate. Regulation also appeared in other forms. In particular governments sold a national license for a form of betting called ‘totalizer’ (or pari-mutuel) betting. In totalizer betting, rather than offering specific odds in the run up to the race, punters instead picked a horse to win and only discovered the exact odds they were getting at the start of the race after all bets had been collected. The odds given were calculated to ensure that punters received a fixed overall payout typically in the region of 75% (an over-round of 33.3%). The remaining 25% was then retained; the operator/licensee holder keeping 5%, 10% going to the government as tax and 10% kept by the racecourse. In the UK, totalizer betting was a monopoly run alongside other forms of betting by a company called The Tote. However, in other European countries, such as France, totalizer betting was the only allowable method of off-course betting.

Business of Bookmaking

With the Betting & Gaming Act of 1960, bookmaking became a much larger industry. Free from the requirement to only take bets from those physically present at the racecourse, the amount of gambling increased dramatically and several bookmakers’ shops opened on every high street in the UK. Initially, these shops were independently run, with local bookmakers expanding their operations from on-course to the local towns. Subsequently, however, several powerful national brands arose creating a much more consolidated market. The industry leaders were Ladbroke’s and William Hill who had a combined share in excess of 50% of the UK market. (See Exhibits 5 and 6).

National scale conferred several advantages including advertising leverage, the ability to smooth outcome exposures from across the country (since local consumers often backed local teams), and the consolidation of back-office functions. However, at its heart bookmaking remained a risk management business. Bookmakers needed high volumes to cover their operating costs and with customer loyalty generally low (only 30% of punters had a preferred gambling shop12), the principal method of managing risk was via the odds offered. In particular, bookmakers aimed to be very competitive on the prices of favorites, as this was a major transparent price point with other bookmakers. This left bookmakers exposed to losses if favorites won and if this happened on a regular basis their profits suffered. As The Sunday Times noted about Paddy Power, Ireland’s leading bookmaking chain: “Favourites winning horse races reduced the industry win ratio in 2005 as the punters benefited. This hit Paddy Power's margins.”13

Bookmaking customers were stereotypically working class men who often spent lunchtimes and Saturday mornings in gambling shops as a form of entertainment. (See Exhibit 7 for a comparison with the general population and remote punters). Driven by this specific set of customers and legislation that required the inside of the bookmaker’s shops to not be visible from the street shops, the shops had a reputation as seedy, smoky locations that were largely impenetrable to those who did not gamble regularly. However, a general relaxation in the law and a need to attract new, more affluent customers, had encouraged major bookmakers to put large investments into their premises to make them more appealing.

708-511 Betfair vs. UK Bookmakers

6

Within shops, bookmakers had attempted to boost revenues and profitability by increasing the utilization throughout the day. To do this bookmakers had to overcome the restriction live UK sporting events had, which was that they generally only occurred on weekday early afternoons (mostly horseracing) and weekends (soccer and rugby matches). This involved broadcasting and taking bets on international sporting events, running ‘virtual events’ using anonymised recorded horseracing footage, and also the introduction of Fixed Odd Betting Terminals (FOBT). FOBT’s were essentially electronic roulette machines that had a fixed payout, thus removing any risk for the bookmaker. While boosting profits their installation had led to negative publicity that they contributed to a rise in gambling addiction.

Large bookmakers were also pro-active in other channels of distributions. Telephone betting had been common as it was the principal method by which companies interacted with ‘high-rollers’, wealthy gamblers who typically made large bets. Rather than making one-off bets these gamblers maintained an account with the bookmaker (sometimes with credit provided to the best customers) and had bets placed for them via telephone. Since bookmakers could monitor their accounts and restrict the bets accepted if they were being too successful, these customers were a large source of profits.f Bookmakers had also started to move online in 1998-1999, enabling them to provide similar account services at a low cost for all punters boosting customer loyalty. Online gambling was essentially the same as in-shop, with punters being able to back outcomes in various sporting events. However punters could more easily gain access to a wide range of sporting events. Top websites had also diversified into online poker and other forms of gambling, capitalizing on traffic to their websites and their gambling-associated brands.

Origins and early years of Betfair14

Betfair was the brainchild of Andrew Black, a university dropout and grandson of a deeply religious, anti-gambling, pro-censorship Conservative party MP.g Black had had a checkered past; dropping out of university after 2 years due to spending more time at the local bookies than on his studies, he took several part-time jobs including a retail shelf stacker and builder’s laborer. Continuing with his love of gambling he also played professional bridge for money, through which he met Jeremy Wray a kindred spirit, who became his best friend. After several years of working in research for City firms, he left to become a professional gambler again, but despite being successful initially, he started to lose when he felt there was no challenge anymore and that he hadn’t really created anything.h He entered the City again as a trader but eventually ended up programming at the Government Communications Headquarters (GCHQ), the UK government’s secretive intelligence organization. It was while at GCHQ that he had the idea of bringing the efficient competition and trading of the New York Stock Exchange to an inefficient market he knew well, gambling on horse-racing.

Black’s insight was that betting markets would be much more efficient if, like stock exchanges, they allowed people to trade freely with each other via an intermediary (the exchange) rather than one protected group of people accepting all bets. Black explained:

With the FTSE there are a lot of brokers who just put their prices up. In New York you ring your broker and say ‘I want to buy’ and he'll go and just stick your bid on the board. Anyone

f Casewriter’s interview with Edward Wray, May 2008 g Conservatives are the more right-wing of Britain’s two major political parties. h The City refers to the part of London where UK’s top financial institutions were located

Betfair vs. UK Bookmakers 708-511

7

can come and post their bid on the board, which creates a great big matching system. There is almost a beauty to a really efficient industry.15

Black’s idea was simply that the industry did not need bookmakers to provide the lay-side of the market, but that punters should be able to back and lay bets with each other by posting their bids on a website, with matching bids being made via a simple exchange mechanism. This was a direct translation of the principle of financial markets, where market participants regardless of their size were never considered as solely buyers or sellers; the betting exchange was born. The UK was the ideal location to launch such a venture not only because of the UK’s long history of gambling, but also because the Betting and Gaming Act of 1960 made person to person betting (such as that regularly practiced in office environments across the UK) legal, something which was not the case in many other countries.

Realizing the disruptive nature of his idea and influenced by the recent death of his father, Black took the plunge quitting GCHQ. He was joined by the brother of his best friend, Ed Wray, an investment banker. With Black developing the website and Wray working on legal and financials, they were soon ready to raise financing. However, they discovered that all of the available venture capital had been captured by Flutter.com, a rival set up by Josh Hannah and Vince Monical, two ex-Bain & Co. consultants who had moved to the UK from San Francisco specifically to benefit from less stringent gambling legislation. As Black recounted:

I could sense at the time that the internet would be a space filled by a series of players who totally own the space they are existing within. There is one pre-eminent auction house - Ebay. There is one pre-eminent search engine - Google. It's perhaps not the same in retailing but there's Amazon…Flutter sold themselves very well. Here's Ebay, it's massively successful. Everyone wants something like it. We will be the Ebay of betting. It turned out to be a fairly compelling story for venture capitalists. Ours didn't look like anything you've seen in your life before. There was nothing that looked like or smelled like Betfair.16

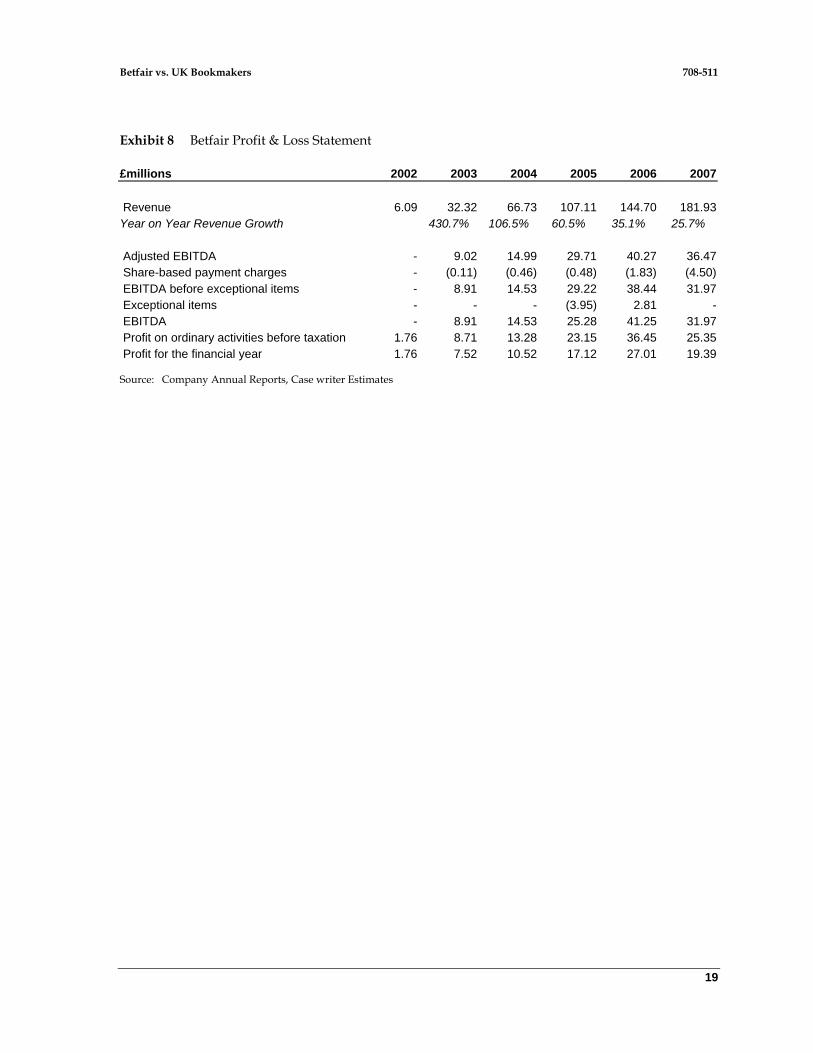

With Flutter.com receiving $43.7m17 in start-up capital, Black and Wray returned from the venture capitalists empty handed and turned to family and friends, mostly Wray’s investment banking colleagues for financing. They were able to eventually raise £1m and formed a small team to develop the proposition.i The company launched on Oaks Day in 2000 with only 20 customers (mostly their original investors) who matched £35,000 of bets between each other, but the proposition was clearly appealing and by 2005 they were matching £4.25m of bets on the Grand National alone. (See Exhibit 8 for Betfair’s financials).

In 2008, Betfair’s home screen (see Exhibit 9) allowed punters to both back and lay on a huge number of sporting events. On selection of an event, punters were given a selection of ‘markets’ such as, for example, the outright winner or the total number of goals scored. Within each market, punters were presented with a list of all possible outcomes and in betting had several options. If they liked the odds offered, then they could either choose to back or lay that particular outcome by clicking on one of the prices available. If their bet was particularly large then they might exhaust all demand at the first odds offered and the remainder of their bet would be matched at the next best available odds as shown in the market depth screen. If odds that the punter found favorable were not available then they could choose to post the odds that they were willing to take (if they were looking to back an outcome) or give (if they were looking to lay an outcome). If this was the case, then their bid would be posted on the website along with other bids, and could be matched in the future if the market moved in this direction. To guide their decision-making, punters could also call up a price history i Casewriter’s interview with Edward Wray, May 2008

708-511 Betfair vs. UK Bookmakers

8

chart for that particular outcome so that they could see how market sentiment had changed over time. To actually place the bet, customers had have their identity verified, then open an account with Betfair and credit it with money. This money was then available for them to back and lay outcomes as long as all possible exposure was covered.

In having their bets matched, punters were never aware who in particular was matching their bets and indeed many bets were probably matched by a collection of punters. Betfair then generated revenues by charging a 5% commission on the net winnings from any one market. Those who gambled in large volumes were rewarded with reductions in their commission rate with the biggest users of the site paying only 2% commission on net winnings. Losing punters paid nothing to the exchange. Betfair accepted no risk in the outcome of the event simply profiting from the winnings of individual punters.

Betfair vs Flutter.com

Based on Black’s vision of a stock exchange for gambling, Betfair set its system to appeal to ‘traders’, who would appreciate the benefits of a stock exchange-style platform. These choices stood in contrast to Flutter.com’s, which remained Betfair’s main rival during start-up. Firstly, in addition to having typical betting markets, Flutter.com, much like eBay, allowed punters to create any event on which they would accept bets. This gave the site a consumer-generated, community style. Betfair restricted all betting purely to markets created by its staff, with the number of markets restricted initially to only major sport events.

Secondly, following standard bookmaking practice Flutter.com described all bets in terms of fractional odds. Betfair choose to express all of its odds in ‘decimal odds’ with conversion provided via a separate help screen. Decimal odds were calculated by simply adding 1 to the fraction odds, such that odds of 5/2, became 5 ÷ 2 + 1 = 3.5. The decimal odds therefore represented the total return to a punter, including the return of their stake. For example, if we backed a horse with £1 at 7/4 then the decimal odds would be 2.75, meaning that if the horse won we would receive £2.75 in total. This decision was criticized in the popular press at the time. Derek McGovern, writing in the Daily Mirror, one of the UK’s leading tabloid newspapers said

I’ve always predicted that betting exchanges will fail to hook Britain’s punting public because of one big failing...their suicidal policy of using decimal, rather than fractional, odds. Punters in Britain have been brought up on 11-10, on 9-4, on 100-30. It’s a language we’ve all become fluent in. It’s our mother tongue. But the betting exchanges have demanded we learn another tongue. In their world 11-10 is not 11-10, it’s 2.10; 9-4 is 3.25; and even the simple 10-1 is 11.00. Why? What in God’s name was wrong with the fractions? I understood that Andre Agassi was hot favourite to win in Rome yesterday when I saw odds of 2-7. But his decimal odds of 1.29 meant nothing.18

Thirdly, whereas Flutter.com matched each person’s specific bet to another specific person willing to accept it, Betfair aggregated all bets such that users didn’t know who they were being matched with. Similarly, if there wasn’t enough demand to fulfill a request on Betfair, a punter could elect to have their bet partially met with the remainder being posted with the possibility it would be accepted at a later date. This was not an option on Flutter.com.j Lastly, Black developed an algorithm which calculated a punter’s total exposure to any one event and required that their user accounts have only enough credit to cover this. For example, if a punter was to lay three horses in the same event (such that only one could win and thus he would only have to pay out on one horse) with £500 exposure on j Casewriter’s interview with Edward Wray, May 2008

Betfair vs. UK Bookmakers 708-511

9

each. On Flutter.com the punter would have to have enough money in his account to cover all three bets (£1500). On Betfair the system recognized that regardless of which horse won, the punter would only ever have to pay out a maximum of £500 minus whatever money they had taken in stakes from punters and imposed this lower limit.

Enabled by large investments in technology infrastructure, Betfair’s trading platform and constantly updating website also enabled a very fluid dynamic market. This allowed the trading style punters to manage their exposures and trade in and out of positions as the market sentiment changed much like a stock market trader. Betfair even offered in-running / in-play trading on certain events. Here punters were able to bet in real-time after the event had actually started, giving even more trading opportunities as the price fluctuated widely in response to the differing fortunes of various competitors. While traditional bookmakers had copied this innovation for slow-moving events such as cricket and golf they simply could not offer such a service for an event as short in duration as a horse race.

Due to these choices, that created more liquidity within its markets, Betfair was able to grow its user base and matched bets much faster than Flutter.com and in December 2001 agreed to merge with them in a deal that was rumored to have valued Betfair at 10x its better funded rival.19 Utilizing Flutter.com’s remaining cash and IT platform, Betfair went on to dominate the betting exchange market overcoming a plethora of rival start-ups (over 40 betting exchanges were operating in 2004), many of which competed with lower commission rates20. From 2003 to 2007 Betfair’s revenue grew at an annual rate of over 54%, reaching £182m in £2007, a year in which it generated £19.3m in profits. In 2008, Betfair held approximately a 90% share of the betting exchange market, with the only viable competition being BetDaq, an Irish-owned exchange. BetDaq had a particular strength in soccer markets but was widely believed to have been unprofitable.

Betfair and the Bookmakers

Betfair announced its arrival on the scene as a serious threat to the industry. In a 2000 publicity stunt, the company paraded an actor dressed in the bookmaker’s stereotypical sheepskin coat and cloth hat, in a coffin through the streets of London. (See Exhibit 10). As Black explained, “[the campaign] was actually quite distasteful but it made the front page of The Sunday Times business section.”21 Since it replaced the bookmaker’s lay-side of the market with ordinary punters, the concept of an exchange clearly threatened the core business of bookmakers, something Black was unapologetic about:

One of the great things about Betfair was that it was just the most disruptive idea imaginable to the betting industry. It drove a cart and horses through the whole bloody lot of it. And quite right, too. We came along with a better mouse trap. They could have done it themselves.22

The major bookmakers could even have employed Black himself, but talks broke down, as Black describes, over him not fitting the typical bookmaking background, “I went to see Ladbrokes, we didn't get on. They didn't like me because I was too posh. Same with Hills.”23

The bookmakers’ (and others involved in the horseracing industry) accusations centered on several key themes. Firstly, they insisted that the vast majority of Betfair’s liquidity came from unlicensed bookmakers who were using the site to conduct illegal operations. Secondly, they maintained that by being able to lay outcomes as well as back outcomes, Betfair was likely to be used for those trying to cheat. For instance, a horseracing jockey could lay himself in a race and then profit

708-511 Betfair vs. UK Bookmakers

10

by not pushing his horse during the race. Lastly, they claimed that since they paid 15% of their gross win to the government and 10% in the form of the horseracing levy, Betfair maintained an unfair price advantage.

Betfair rigorously countered such claims. They worked with the UK government to pay the same taxes on their gross profits (commissions from their users) as other operators and the general move to gross profit taxation on the industry in 2001 removed any price advantage on the website. Similarly, they reached agreement with the British Horseracing Board to contribute their share to the horseracing levy and were also active in paying and offering to pay the non-statutory levies of other sports. In addition, they worked actively with the Jockey Club (the organizing authority for professional jockeys) and other sports’ governing bodies and law enforcement agencies to actively monitor and provide information on any suspected cheating or market manipulation. For example, Betfair’s active monitoring of all their markets led them to suspend all betting and ultimately void all bets on a Poland Open tennis match between Nikolay Davydenko and Martin Vassallo in August 2007.24 This was a result of higher than normal betting on the match with the market moving to peculiarly long odds on Davydenko to win despite his position as the top seed and the fact that he had won the 1st set. Davydenko retired from the match at the start of the 3rd set.

The government also seemed satisfied that Betfair was not breaking any laws. Despite several reviews, it made no move to change the laws relating to betting exchanges. Further promoting the integrity of its model, Betfair has published an annual report since 2004, despite (since they are a private company) no official requirement to do so. Also, in November 2004, Betfair stepped in and provided over £3.5m to rescue the accounts of customers of Sporting Options, one of its rivals. Sporting Options had gone bankrupt and in a desperate attempt to remain viable had illegally used customer funds, losing them all. Betfair guaranteed all funds which ex-Sporting Options customers could access via a new account on Betfair.25 They had also worked hard to keep clear from the controversy of offshore gambling in the US. Rival online gaming firms had been accused of illegally processing bets from US consumers and US-registered credit cards. In one notable case, the chairman of SportingBet (the UK owner of Paradise Poker), Peter Dicks was arrested in New York. The stock market valuations of many online gambling companies had suffered as a result of this and the tightening of US legislation on offshore gambling.

Looking to the Future Reflecting on a tumultuous 9 years, Black, Wray, and the Betfair management team were rightly

satisfied with what they had achieved. They had overcome great adversity to build their company into one of the UK’s fastest growing and most successful companies and in doing so had revolutionized an industry.

Looking to the future, they had to decide how and where to take their company next and were considering several options:

UK Sports Betting Growth

Firstly, did it make sense to press home the advantage of its business model to further dominate the UK betting industry? Betfair’s 25% revenue growth was currently outstripping all major competitors and it had been very successful at attracting a young, affluent consumer who was internet-savvy and used to the trading aspects that Betfair provided. To extend its penetration of UK gamblers, Betfair would have to copy some of the other services offered by bookmakers and regularly used by traditional punters.

Betfair vs. UK Bookmakers 708-511

11

For instance, should Betfair introduce a starting price service to compete with that of traditional bookmakers? Similarly, should they offer a multiples/accumulator service? Or should they even go as far as to consider expanding their presence by offering remote gaming terminals at racecourses and other locations such as pubs?

International Expansion

With the success of Betfair in the UK and with many different language versions of the website currently serving international customers, it was clear that the betting exchange model had appeal internationally. Should Betfair capitalize on their business model innovation and technological capability and continue expansion to other countries? Doing so would require navigating the legal minefield that surrounds betting in most countries and overcoming the myriad of vested interests that would attempt to hamper their progress much as they had done in the UK.

Weighing heavily on Betfair’s evaluation of this option had been their previous experience in Australia. Despite operating in Australia for many years, any marketing of the website was prohibited by their lack of a gambling license. Attempts to obtain a gambling licence via the Tasmanian state government had been severely hampered by protests and lobbying from bookmakers and racing authorities, one of whom had characterized Mark Davies, Betfair’s representative, as a ‘parasite’.26

Similarly, expansion efforts in France had faced opposition as the only gambling currently permitted was the state monopoly on pari-mutuel. Likewise, while Italy had opened discussions with Betfair about opening operations there, the authorities had argued that they should introduce a traditional bookmaking operation first as consumers would not understand exchange betting.k Should Betfair be willing to make such a sacrifice and change to its model to allow access to the market?

Product Diversification

Finally, Betfair had the option of capitalizing on its rapidly rising brand name and expanding gambling-focused customer base to diversify and become an online gaming company. Such a move would require a move beyond sports betting to include poker and casino games. However, as a company built on bringing fairness to betting, what advantage would they have in this market? Could the Betfair model be successfully applied to other forms of gaming?

Alternatively, could the Betfair trading platform be expanded to other non-gaming products? The main Betfair.com site already had a small presence in betting on basic stock exchange movements and political contests, could this be expanded to a more in-depth focus for those more interested in financial services, including perhaps the introduction of spread betting services?

k Casewriter’s interview with Edward Wray, May 2008

708-511 Betfair vs. UK Bookmakers

12

Exhibit 1 UK Gambling by Market Segment

£millions 2002 2004 2006 Betting 10,123 32,341 44,438 Football pools 144 112 90 Casinos 3,582 4,073 4,231 Gaming machines 10,340 10,710 10,300 Bingo 1,164 1,381 1,826 National Lottery 4,833 4,586 5,009 Total 30,186 53,203 65,894

Source: Mintel Leisure Intelligence, “Betting Shops”, August 2007

Exhibit 2 UK Betting Shops by Operator

2002 2004 2006 William Hill 1,540 1,590 2,165 Ladbrokes 1,825 1,920 2,141 Coral Eurobet 865 1,100 1,500 Betfred - - 670 Tote 340 460 540 Stanley* 635 600 - Others 3,395 3,070 1,684 Total 8,600 8,740 8,700

*Purchased by William Hill in 2005

Source: Mintel Leisure Intelligence, “Betting Shops”, August 2007

Betfair vs. UK Bookmakers 708-511

Exhibit 3a Basic Bookmaking Example

Source: Compiled by Casewriter

13

708-511 Betfair vs. UK Bookmakers

Exhibit 3b Basic Example of Bookmaker hedging his exposure

Source: Compiled by Casewriter

14

Betfair vs. UK Bookmakers 708-511

Exhibit 4 Traditional On-course Bookmakers

Bookmaker adjusting odds Competing Bookmakers

Source: http://www.bbc.co.uk/herefordandworcester/content/image_galleries/worcester_racecourse_gallery.shtml?2 and http://www.cheltenhamfestival.net/cheltenham%20festival%20bookmakers.jpg

15

708-511 Betfair vs. UK Bookmakers

16

Exhibit 5 Ladbrokes Segment Operating Information

£ millions 2001 2002 2003 2004 2005 2006 Total Amount Staked / Wagered European Retail 2,037.5 2,999.1 Telephone 284.7 393.2 eGaming 188.2 390.3 Other 110.6 30.4 Total 2,621.0 3,813.0 7,267.1 10,122.6 11,500.0 12,383.8 Gross Win European Retail 521.6 642.7 694.5 752.40 771.50 Telephone 27.4 28.9 46.1 20.60 45.80 eGaming 53.4 63.7 89.3 116.20 134.10 Total 602.4 735.3 829.9 889.2 951.4 Trading / Operating Profit European Retail 102.4 124.4 184.6 227.9 219.5 212.7 Telephone 3.6 8.1 9.4 17.8 -0.1 17.7 eGaming 2.0 11.3 14.2 21.3 41.4 47 Total 108.0 143.8 208.2 267 260.8 277.4 Gross Win Percentage European Retail - 17.4% Telephone - 7.0% eGaming - 13.7% Total - 15.8% 10.1% 8.2% 7.7% 7.7% Operating Margin (Profit / Gross Win) European Retail 23.8% 28.7% 32.8% 29.2% 27.6% Telephone 29.6% 32.5% 38.6% (0.5%) 38.6% eGaming 21.2% 22.3% 23.9% 35.6% 35.0% Total 23.9% 28.3% 32.2% 29.3% 29.2%

Note: The total amount staked/wagered, reflects all bets that are taken from punters. The gross-win is the net-profit which bookmakers make from gambling as it reflects the total amount staked minus any winnings paid out to punters. The gross win is therefore the best measure of a bookmaker’s ‘revenue’. The trading/operating profit reflects the profit made by gambling operations after accounting for costs such as store rent, staff costs etc, but excluding central corporate costs. The gross win percentage is simply the gross win divided by the total amount staked and represents the profitability (or price competitiveness) of the bookmaker’s bet taking. The operating margin is the operating profit divided by the gross win.

Source: Company Annual Reports

Betfair vs. UK Bookmakers 708-511

17

Exhibit 6 William Hill Segment Operating Information

£ millions 2001 2002 2003 2004 2005 2006 Total Amount Staked / Wagered Retail 1,721.6 2,460.4 4,751.8 7,020.7 9,285.5 11,486.0 Telephone 419.5 489.1 570.5 540.8 605.8 659.9 Interactive 273.7 389.3 592.6 696.3 826.0 1,060.3 Total 2,414.8 3,338.8 5,914.9 8,257.8 10,717.3 13,206.2 Gross Win Retail 416.7 418.9 505.6 548.1 623.4 736 Telephone 48 50.9 56.5 60.3 53.4 57.5 Interactive 35.4 54.9 84.9 106.1 123.3 130.5 Total 500.1 524.7 647 714.5 800.1 924 Trading / Operating Profit Retail 93.2 111.9 152.4 165.5 181.6 225.9 Telephone 15.5 17.3 22.2 22.1 13 16.7 Interactive 9.2 20.5 37.1 51.7 61.2 61.5 Total 117.9 149.7 211.7 239.3 255.8 304.1 Gross Win Percentage Retail 24.2% 17.0% 10.6% 7.8% 6.7% 6.4% Telephone 11.4% 10.4% 9.9% 11.2% 8.8% 8.7% Interactive 12.9% 14.1% 14.3% 15.2% 14.9% 12.3% Total 20.7% 15.7% 10.9% 8.7% 7.5% 7.0% Operating Margin (Profit / Gross Win) Retail 22.4% 26.7% 30.1% 30.2% 29.1% 30.7% Telephone 32.3% 34.0% 39.3% 36.7% 24.3% 29.0% Interactive 26.0% 37.3% 43.7% 48.7% 49.6% 47.1% Total 23.6% 28.5% 32.7% 33.5% 32.0% 32.9%

Note: The total amount staked/wagered, reflects all bets that are taken from punters. The gross-win is the net-profit which bookmakers make from gambling as it reflects the total amount staked minus any winnings paid out to punters. The gross win is therefore the best measure of a bookmaker’s ‘revenue’. The trading/operating profit reflects the profit made by gambling operations after accounting for costs such as store rent, staff costs etc, but excluding central corporate costs. The gross win percentage is simply the gross win divided by the total amount staked and represents the profitability (or price competitiveness) of the bookmaker’s bet taking. The operating margin is the operating profit divided by the gross win.

Source: Company Annual Reports

708-511 Betfair vs. UK Bookmakers

18

Exhibit 7 Demographics of UK Betters and Remote Betters (Telephone and Internet)

UK

Population All Betters Remote Betters

Gender Men 49% 51% 70%

Women 51% 49% 30%

Age 18-24* 15% 13% 22% 25-34 18% 19% 15% 35-44 19% 19% 30% 45-54 16% 17% 8% 55-64 13% 15% 10% 65+ 19% 18% 16%

Demographics*

AB 24% 16% 23% C1 28% 29% 36% C2 21% 24% 22% D 18% 16% 11% E 10% 15% 8%

Marital Status Married 63% 61% 61%

Not married 37% 39% 39%

Working Status Full-time 48% 55% Part-time

52% 14% 8%

Not working 26% 18% 25% Retired 22% 13% 13%

Source: Mintel Leisure Intelligence, “Remote Betting”, August 2005

*AB, C1 etc. is a demographic classification known as ACORN that is widely used in the UK. AB represents the highest income households, while E represents the unemployed and those living of the state.

Betfair vs. UK Bookmakers 708-511

19

Exhibit 8 Betfair Profit & Loss Statement

£millions 2002 2003 2004 2005 2006 2007 Revenue 6.09 32.32 66.73 107.11 144.70 181.93Year on Year Revenue Growth 430.7% 106.5% 60.5% 35.1% 25.7% Adjusted EBITDA - 9.02 14.99 29.71 40.27 36.47 Share-based payment charges - (0.11) (0.46) (0.48) (1.83) (4.50) EBITDA before exceptional items - 8.91 14.53 29.22 38.44 31.97 Exceptional items - - - (3.95) 2.81 - EBITDA - 8.91 14.53 25.28 41.25 31.97 Profit on ordinary activities before taxation 1.76 8.71 13.28 23.15 36.45 25.35 Profit for the financial year 1.76 7.52 10.52 17.12 27.01 19.39

Source: Company Annual Reports, Case writer Estimates

708-511 Betfair vs. UK Bookmakers

Exhibit 9 Betfair Operating Screens

Source: Company Website, http://www.betfair.com (accessed February 26, 2008).

20

Betfair vs. UK Bookmakers 708-511

Exhibit 9 (Cont.) Betfair Market Screens

Possible Outcomes / Winners

Market Event

Total amount matched on event

Book-Percentage

Price / Odds History, over

time (in this case presented as

implied probability)

Available Odds to back Ireland to win (another punter has an unmatched lay against Ireland)

Available amounts at these odds. Punters wishing to place more, will have to accept part of their bet at shorter odds

As Ireland progressed through the 6 nations tournament their probability of winning decreased on average (due to losing matches)

Source: Company Website, http://www.betfair.com (accessed February 26, 2008).

21

708-511 Betfair vs. UK Bookmakers

Exhibit 10 Betfair Publicity Stunt, 2000

Source: “The Definitive Guide to Betting Exchanges,” in The Definitive Guide to Betting Exchange, ed. Paul Kealy (Raceform, 2005), p. 28.

22

Betfair vs. UK Bookmakers 708-511

23

Endnotes

1 Buckley, Will, “The Man Behind a Betting Revolution,” The Observer, 6 February 2005.

2 “Interview - Andrew Black, founder of Betfair - Odds-on favourite.”; The Guardian, Simon Bowers, 7 June 2003

3 The 2007 Betfair Annual Review available from http://www.betfaircorporate.com/

4 “Betfair to sell stake to Softbank - Japan technology group to buy 23% - Deal values internet betting exchange at Pounds 1.5bn - Original investors see return of 130 times.”; Matthew Garrahan, Financial Times, 28 February 2006

5 http://uk.finance.yahoo.com, accessed on 7th April 2007. Market value of common equity.

6 This section is predominately gathered from http://en.wikipedia.org/wiki/Horseracing_in_Great_Britain

7 Mintel Leisure Intelligence, “Betting Shops, UK August 2007”

8 From casewriter’s conversation with Ed Wray, non-Executive Chairman of Betfair

9 Research conducted by Ladbrokes as reference on: http://www.karenearl.co.uk/insideinfo.cfm?action=view&id=324

10 “1960: Game on for British betting shops,” BBC, accessed on June 1, 2008 http://news.bbc.co.uk/onthisday/hi/dates/stories/september/1/newsid_2969000/2969846.stm

11 Mintel Leisure Intelligence, “Betting Shops, UK August 2007”

12 Mintel Leisure Intelligence, “Betting Shops, UK August 2007”

13 “Online betting keeps favouite out in front”; The Sunday Times, 9 April 2006

14 This section is predominately gathered from “The gambler who bet on himself”; Andrew Alderson, Sunday Telegraph, 29 May 2005 and “The Man Behind a Betting Revolution”; Will Buckley, The Observer, 6 February 2005.

15 Buckley,Will, The Observer, 6 February 2005.

16 Ibid.

17 Racing Post Expert Series “The Definitive Guide to Betting Exchanges”; Raceform

18 McGovern, Derek,“Derek McGovern at Large: What’s the Point?,” The Daily Mirror, 7 May 2005.

19 “Betfair buy spells the final flutter”; The Daily Telegraph, Simon Goodley, 22 December 2001

20 Racing Post Expert Series “The Definitive Guide to Betting Exchanges”; Raceform

21 Buckley, Will, The Observer, 6 February 2005.

22 Ibid.

23 Ibid.

24 http://news.bbc.co.uk/sport1/hi/tennis/6928635.stm

25 “Betfair steps in to bail out punters - Accounts to be replenished after Sporting Options collapse”; The Guardian, Simon Bowers, 17 November 2004

26 “Dealing out the dirt”; Colin Kruger as accessed on September 11, 2004 on http://www.smh.com.au/articles/2004/09/10/1094789680927.html?from=storylhs