Embed Size (px)

Citation preview

1

Best Practices inPortfolio ConstructionAre investors ready for lower growth for longer? How are they working to bridge the performance gap?

Moderator – Niall O’Leary , Head of EMEA Fixed Income Portfolio Strategy , State Street Global Advisors

This material is solely for the private use of CFA Netherlands members and is not intended for public dissemination. All the information contained in this presentation is as of date Indicated unless otherwise noted

Marketing communication

EMPRES-6671

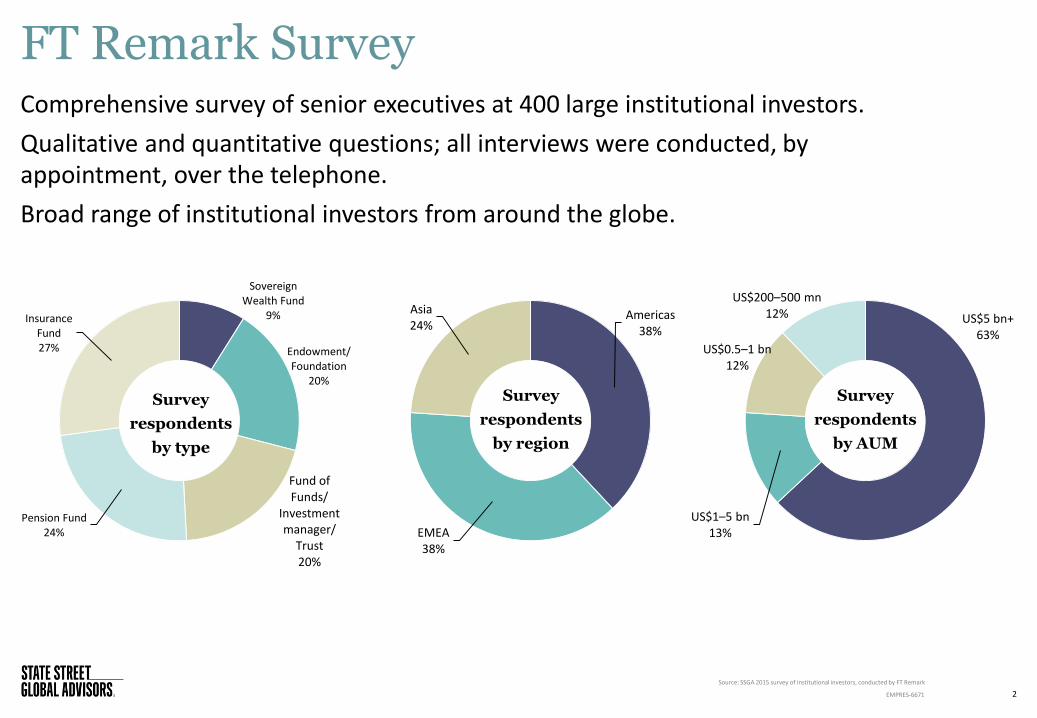

FT Remark SurveyComprehensive survey of senior executives at 400 large institutional investors.

Qualitative and quantitative questions; all interviews were conducted, by appointment, over the telephone.

Broad range of institutional investors from around the globe.

2

Source: SSGA 2015 survey of institutional investors, conducted by FT Remark

Sovereign Wealth Fund

9%

Endowment/Foundation

20%

Fund of Funds/

Investment manager/

Trust20%

Pension Fund24%

Insurance Fund27%

Survey

respondents

by type

Americas38%

EMEA38%

Asia24%

Survey

respondents

by region

US$5 bn+63%

US$1–5 bn13%

US$0.5–1 bn12%

US$200–500 mn12%

Survey

respondents

by AUM

EMPRES-6671

In the study, we explored

1. Current return expectations and investors’ confidence in their capacity to attain portfolio growth objectives over the medium to longer term.

2. The adoption of new asset allocation strategies to meet performance gaps amid today’s challenging markets.

3. The obstacles that may be constraining the uptake of potentially helpful new approaches, such as factor and objective-based investing.

3EMPRES-6671

Challenges for Investors

• To achieve investment objectives, investors need to work their asset allocation harder, and smarter, than ever before.

• For an increasing numbers of investors, this means challenging traditional strategic asset allocation models.

• Greater need to consider risk and stronger focus on the actual return drivers of chosen asset classes.

• But while alternative models — such as factor-based, liability-driven or other specialised approaches — provide potential pathways, obstacles to putting them into practice can arise.

4EMPRES-6671

5EMPRES-6671

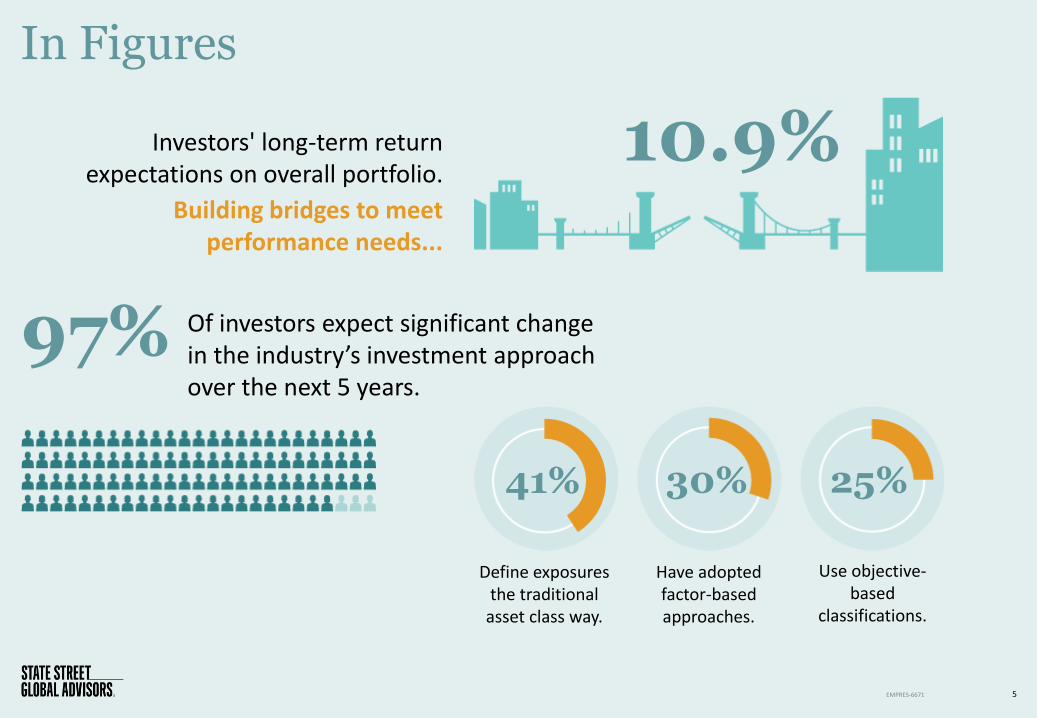

In Figures

Investors' long-term return expectations on overall portfolio.

Building bridges to meet performance needs...

97% Of investors expect significant change in the industry’s investment approach over the next 5 years.

10.9%

41% 30% 25%

Define exposures the traditional

asset class way.

Have adopted factor-based approaches.

Use objective-based

classifications.

Blenheim Capital Management

6

7EMPRES-6671

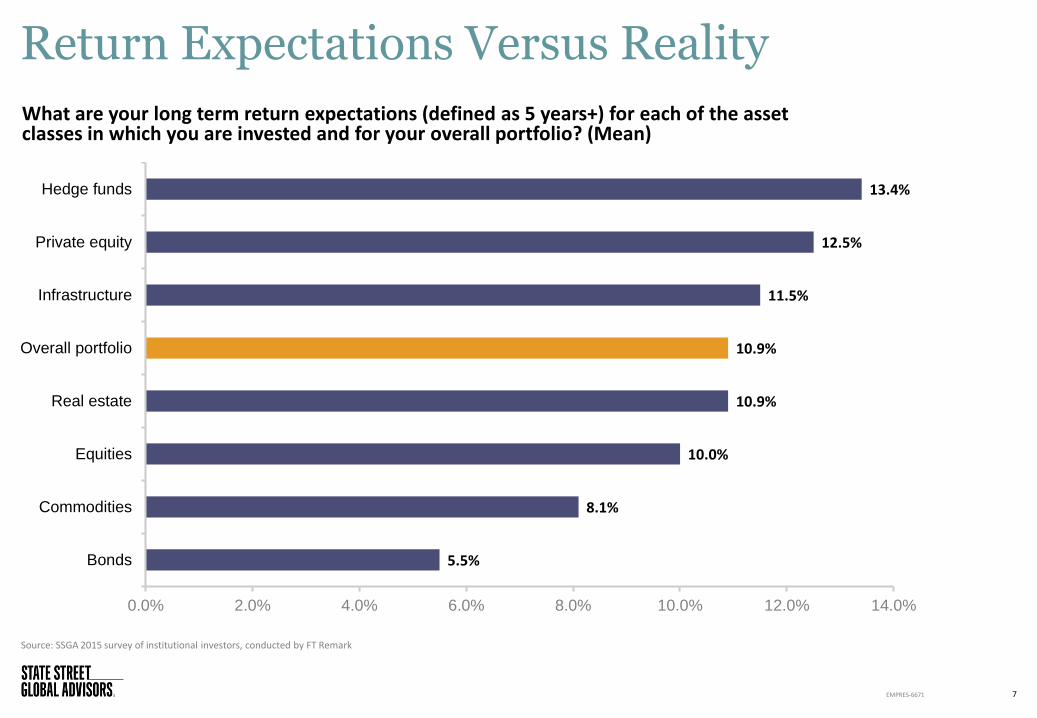

Source: SSGA 2015 survey of institutional investors, conducted by FT Remark

5.5%

8.1%

10.0%

10.9%

10.9%

11.5%

12.5%

13.4%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

Bonds

Commodities

Equities

Real estate

Overall portfolio

Infrastructure

Private equity

Hedge funds

What are your long term return expectations (defined as 5 years+) for each of the asset classes in which you are invested and for your overall portfolio? (Mean)

Return Expectations Versus Reality

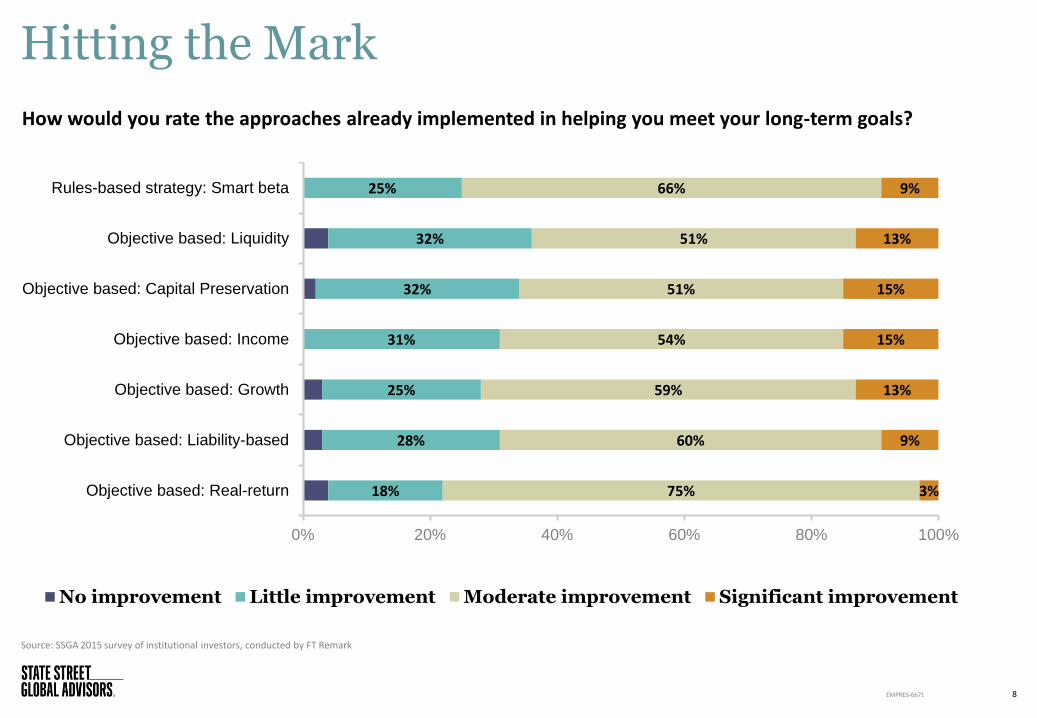

Hitting the Mark

8

Source: SSGA 2015 survey of institutional investors, conducted by FT Remark

18%

28%

25%

31%

32%

32%

25%

75%

60%

59%

54%

51%

51%

66%

3%

9%

13%

15%

15%

13%

9%

0% 20% 40% 60% 80% 100%

Objective based: Real-return

Objective based: Liability-based

Objective based: Growth

Objective based: Income

Objective based: Capital Preservation

Objective based: Liquidity

Rules-based strategy: Smart beta

No improvement Little improvement Moderate improvement Significant improvement

How would you rate the approaches already implemented in helping you meet your long-term goals?

EMPRES-6671

20%

6%

78%

77%

84%

2%

17%

16%

0% 20% 40% 60% 80% 100%

Passive

Active

Smart beta

Decrease Stay the same Increase

Increasing use of Active and Smart Beta

9EMPRES-6671

Source: SSGA 2015 survey of institutional investors, conducted by FT Remark

24%

6%

74%

75%

86%

2%

19%

14%

0% 20% 40% 60% 80% 100%

Passive

Active

Smart beta

For the equity portion do you expect the allocation to active, passive and smart beta to change over the next two years?

For the bond portion do you expect the allocation to active, passive and smart beta to change over the next two years?

Bridgewater

10

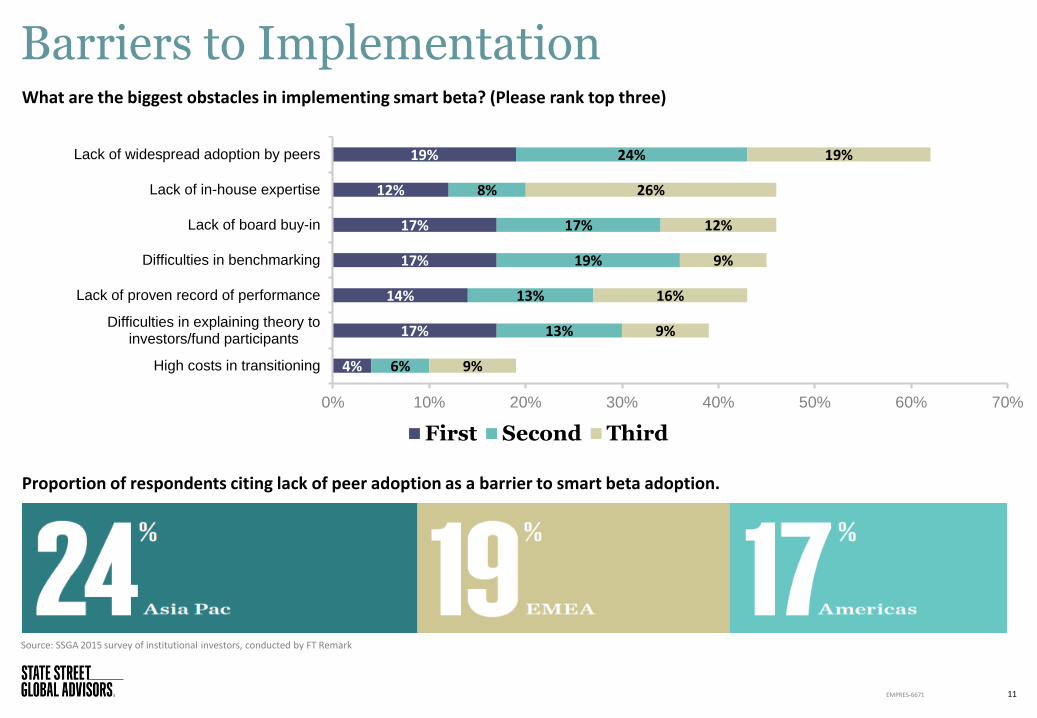

Barriers to Implementation

11EMPRES-6671

Source: SSGA 2015 survey of institutional investors, conducted by FT Remark

4%

17%

14%

17%

17%

12%

19%

6%

13%

13%

19%

17%

8%

24%

9%

9%

16%

9%

12%

26%

19%

0% 10% 20% 30% 40% 50% 60% 70%

High costs in transitioning

Difficulties in explaining theory toinvestors/fund participants

Lack of proven record of performance

Difficulties in benchmarking

Lack of board buy-in

Lack of in-house expertise

Lack of widespread adoption by peers

First Second Third

What are the biggest obstacles in implementing smart beta? (Please rank top three)

Proportion of respondents citing lack of peer adoption as a barrier to smart beta adoption.

MSCI

12

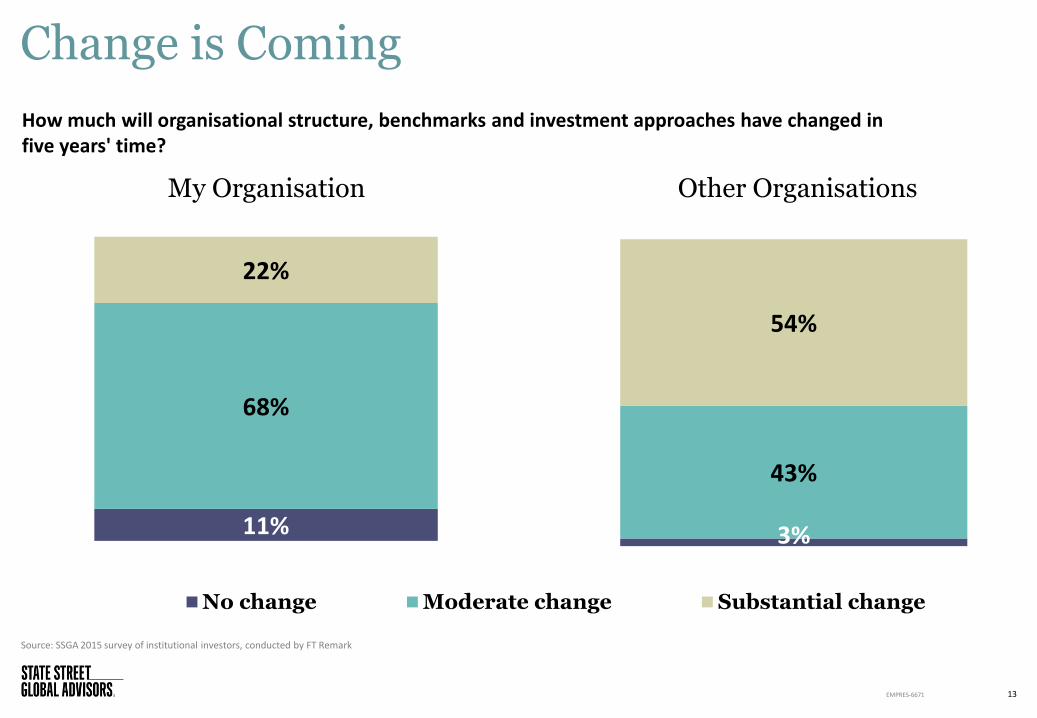

3%

43%

54%

No change Moderate change Substantial change

13EMPRES-6671

Source: SSGA 2015 survey of institutional investors, conducted by FT Remark

11%

68%

22%

How much will organisational structure, benchmarks and investment approaches have changed in five years' time?

Change is Coming

My Organisation Other Organisations

14

For more information, please contact your local State Street Global Advisors representative or visit ssga.com

EMPRES-6671

Important Information

FOR INVESTMENT PROFESSIONAL USE ONLY. Not for use with the public

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the European Communities (Markets in Financial Instruments) Regulations 2007. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA's express written consent.

The information provided does not constitute investment advice as such term is defined under the Markets in Financial Instruments Directive (2004/39/EC) and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any investment. It does not take into account any investor's or potential investor’s particular investment objectives, strategies, tax status, risk appetite or investment horizon. If you require investment advice you should consult your tax and financial or other professional advisor. All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

State Street Global Advisors Netherlands, Apollo Building, 7th floor Herikerbergweg 29, 1101 CN Amsterdam, Netherlands. Telephone: +31 20 7181701. SSGA Netherlands is a branch office of State Street Global Advisors Limited. State Street Global Advisors Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom

This communication is directed at professional clients (this includes eligible counterparties as defined by the [Netherlands Authority For the Financial Markets]) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

Web: www.SSGA.com

© 2016 State Street Corporation - All Rights Reserved

Tracking Number : EMPRES-6671

Expiration Date : 09/30/2017

15EMPRES-6671