Embed Size (px)

Citation preview

Investor PresentationAlways Advancing to Protect What’s Important

August 2020

2

Forward-Looking Statements

Statements in this presentation that are not historical, including statements relating to the expected future performance of the Company, are considered “forward looking” and are presented pursuant to the safe harbor provisions of the Private Securities Litigation Reform

Act of 1995. You can identify forward-looking statements because they contain words such as “believes,” “expects,” “may,” “will,” “should,” “would,” “could,” “seeks,” “approximately,” “intends,” “plans,” “estimates,” “anticipates,” “outlook,” or “looking forward,” or

similar expressions that relate to our strategy, plans or intentions. All statements we make relating to our estimated and projected earnings, margins, costs, expenditures, cash flows, growth rates and financial results or to our expectations regarding future industry trends

are forward-looking statements. In addition, we, through our senior management team, from time to time make forward-looking public statements concerning our expected future operations and performance and other developments. These forward-looking statements are

subject to risks and uncertainties that may change at any time, and, therefore, our actual results may differ materially from those that we expected.

Important factors that could cause actual results to differ materially from our expectations, which we refer to as cautionary statements, are disclosed under “Risk Factors” and elsewhere in our Annual Report on Form 10-K and subsequent filings with the Securities and

Exchange Commission, including, without limitation, in conjunction with the forward-looking statements included in this presentation. All forward-looking information and subsequent written and oral forward-looking statements attributable to us, or to persons acting on

our behalf, are expressly qualified in their entirety by the cautionary statements. Some of the factors that we believe could affect our results include: (1) risks associated with our substantial indebtedness and debt service; (2) changes in prices and availability of resin and

other raw materials and our ability to pass on changes in raw material prices on a timely basis; (3) performance of our business and future operating results; (4) risks related to acquisitions, integration of acquired businesses and their operations (including the integration of

RPC Group Plc (“RPC”), and realization of anticipated cost savings and synergies and in the anticipated amounts or within the contemplated timeframes or cost expectations, the inability to realize the anticipated revenues, expenses, earnings and other financial results and

operational benefits, and the anticipated tax treatment; (5) reliance on unpatented proprietary know-how and trade secrets; (6) increases in the cost of compliance with laws and regulations, including environmental, safety, and production and product laws and regulations;

(7) risks related to disruptions in the overall economy and the financial markets that may adversely impact our business; (8) risk of catastrophic loss of one of our key manufacturing facilities, natural disasters, and other unplanned business interruptions; (9) risks related to

market acceptance of our developing technologies and products; (10) general business and economic conditions, particularly an economic downturn; (11) risks that our restructuring programs may entail greater implementation costs or result in lower cost savings than

anticipated; (12) ability of our insurance to fully cover potential exposures; (13) risks of competition, including foreign competition, in our existing and future markets; (14) uncertainty regarding the United Kingdom’s withdrawal from the European Union and the outcome of

future arrangements between the United Kingdom and the European Union; (15) risks related to the phase-out of the London Interbank Offered Rate (LIBOR), or the replacement of LIBOR with a different reference rate or modification of the method used to calculate LIBOR;

(16) new legislation or new regulations and the Company’s corresponding interpretations of either may affect our business and consolidated financial condition and results of operations; (17) risks related to international business, including as a result of the RPC transaction,

including foreign currency exchange rate risk and the risks of compliance with applicable export controls, sanctions, anti-corruption laws and regulations; and (18) the other factors discussed under the heading “Risk Factors” in our Annual Report on Form 10-K and

subsequent filings with the Securities and Exchange Commission. We caution you that the foregoing list of important factors may not contain all of the material factors that are important to you. Accordingly, readers should not place undue reliance on those statements. All

forward-looking statements are based upon information available to us on the date of this release. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise

required by law.

This presentation should be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto included in our public filings.

Non-GAAP Financial Measures

This presentation includes certain non-GAAP financial measures such as operating EBITDA, adjusted EBITDA, adjusted net income, and free cash flow intended to supplement, not substitute for, comparable measures under generally accepted accounting principles (GAAP).

Investors are urged to consider carefully the comparable GAAP measures and the reconciliations to those measures provided in our earnings release, presentations, and SEC filings. For further information about our non-GAAP measures, please see our earnings release, SEC

filings and supplemental data at the end of this presentation.

Website Information

We often post important information for investors on our website, www.berryglobal.com, in the “Investor Relations” section. We use this website as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation

FD. Accordingly, investors should monitor the Investor Relations section of our website, in addition to following our press releases, SEC filings, public conference calls, presentations, and webcasts. The information contained on, or that may be accessed through our website,

is not incorporated by reference into, and is not a part of this document.

No profit forecast

Nothing contained herein shall be deemed to be a forecast, projection or estimate of the future financial performance of RPC or the combined business following the completion of the combination, unless otherwise stated.

LTM Information

LTM information presented herein is the Last Twelve Months of reported information as of the date represented.

Certain information included in this presentation has been sourced from third parties. Berry does not make any representations regarding accuracy, completeness or timeliness of such third party information. Permission to cite such information has neither been sought nor

obtained.

Safe Harbor Statements

3

Never Ending Commitment to Identifying, Managing, and Eliminating Risk

Our #1 priority and core value is the health and safety of our people

OH

SA I

nci

de

nt

Ra

te

Industry Average

Significantly lower than the

industry recordable average

Safety

Berry Overview

3

5

Low cost manufacturer of thousands of products in stable end markets

Strong, growing, dependable, and predictable cash flows

Proven growth platform

A leading global supply, design, and

engineering company for value-added

packaging and protective solutions

Information is pro forma estimates for most recent acquisitions along with management estimates as of fiscal 2019.

$12.6 B Annual Revenues

293Facilities

~47,000 Employees

39Countries

100,000+Items Manufactured

6

Food & Beverage

Home, Health & Personal Care

Specialties

Distribution

North America

EMEA

Asia Pacific

ROW

Berry Overview

~$12.6 Brevenue

~$12.6 Brevenue

Revenue FY19

by End MarketRevenue FY19

by Geography

~70% of sales are in stable, consumer-oriented end markets

34%

30%

25%

11%

51%

40%

5%

4%

Information is pro forma estimates for most recent acquisitions along with management estimates as of fiscal 2019.

7

Four Complementary Segments

Information is pro forma estimates for most recent acquisitions along with management estimates for fiscal 2019.

-Berry produces components of some of the products in the HH&S segment.

Consumer Packaging -

North America

24% of Revenue

Revenue

$3.0B

• Closures

• Drink cups

• Bottles

• Prescription vials

• Containers

• Tubes

Consumer Packaging -

International

36% of Revenue

Revenue

$4.6B

• Closures

• Containers

• Bottles

• Consumer & industrial

flexible packaging

• Medical devices

• Recycling & waste mngt.

solutions

Engineered Materials

20% of Revenue

Revenue

$2.5B

• Consumer and industrial

flexible packaging

• Industrial & specialty tapes

• Can liners

Health, Hygiene &

Specialties

20% of Revenue

Revenue

$2.5B

• Diapers

• Adult incont.

• Feminine care

• Medical garments

• Disinfectant wipes

• Dryer sheets

• Filtration

A unique global consumer packaging platform

A One-Stop Shop Offering with a Global Manufacturing Platform

8

Key Investment Highlights

Global leadership position with scaleGlobal leadership position with scale

Consistent, predictable, & dependable free cash flowConsistent, predictable, & dependable free cash flow

History of revenue and EBITDA growthHistory of revenue and EBITDA growth

A leading innovator backed by investments in design and engineering….A leading innovator backed by investments in design and engineering….

….and is at the forefront of sustainability….and is at the forefront of sustainability

Unique long-term M&A strategy opportunity with a proven track recordUnique long-term M&A strategy opportunity with a proven track record

Margin stability across various input cost cyclesMargin stability across various input cost cycles

Serves stable end markets with favorable long-term dynamicsServes stable end markets with favorable long-term dynamics

1

2

3

4

5

6

7

8

9

Global Leadership Position with Scale

• Largest resin buyer with ~7 billion lbs

procured annually

• Leadership position across the majority of

our product portfolio

• The most expansive product offering and

global footprint

Berry revenue represents pro forma for most recent acquisitions. Competitor group represents plastic producing peers. Competitor group revenue based on public LTM data as of November 21, 2019.

1

$12.6

Revenue

Low Cost Manufacturer – Sustainable Competitive Advantage

$13.0

$5.4 $4.8 $4.5

$2.9

$-

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

AMC BERY SON SEE SLGN ATR

10

$436

$517

$601 $634

$764

$830

$900

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020E Normalized

Guidance Actual

(1) Based on latest shares outstanding and stock price as of the most recent reported quarter.

(2) Packaging peer group includes: Amcor, Aptar Group, Ball Corporation, Crown Holdings, Graphic Packaging, Owens Illinois, Sealed Air, Silgan, and Sonoco. Packaging peer

average based on the latest calculated public data available as of August 4, 2020. Free cash flow calculated as cash flow from operations less net capital expenditures

from public cash flow statements.

Note: Normalized free cash flow is expected free cash flow assuming the achievement of expected cost synergies and the exclusion of restructuring and integration costs

associated with achieving synergies, on a tax adjusted basis.

Berry’s FY ’20E FCF Yield is >14% (1) – Well Above Peers LTM Average of ~8% (2)

• 5-year free cash flow CAGR of >20%

• Exceeded free cash flow guidance every

year since IPO

• Normalized FCF of $900+ million

Consistent, Predictable, & Dependable Free Cash Flow2

Free cash flow yield (1) ~14% ~15%

+

11

$302

$436

$517

$601$634

$764

$200

$300

$400

$500

$600

$700

$800

2014 2015 2016 2017 2018 2019

$1.56$1.70

$2.48

$3.09$3.37 $3.41

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

2014 2015 2016 2017 2018 2019

$72

$1,530

$0

$400

$800

$1,200

$1,600

1999 2004 2009 2014 2019

$329

$8,878

$0

$2,000

$4,000

$6,000

$8,000

1999 2004 2009 2014 2019

Strong Financial Performance Track RecordRevenue Free Cash Flow

Adjusted Earnings Per Diluted ShareOperating EBITDA

Dollars in millions, except per share data. Represents fiscal revenue and operating EBITDA for respective years

3

Proven Track Record of Growth

12

A leading innovator backed by investments in design and

engineering…..

4

Selected examples of innovation

Next generation trigger pumps

Breathable film

Pre-compression

technology keeps the

trigger sprayer

perpetually primed,

dispensing output at

high velocity

Breathable film allows

moisture control for

hygiene applications

with soft, quiet

features enabling

comfort and discretion

• Investment in innovative product design, process and conversion

technologies

• Currently 30+ focused design and innovation centers with thousands

of patents

• Innovation capability is a key competitive advantage over smaller

competitor base

• Innovation examples across all of our segments, e.g. patented sports

caps, breathable film technology, fully recyclable flexible pouch, and

next generation tripper pumps

13

A leading innovator backed by investments in design and

engineering….

Engineered MaterialsHealth, Hygiene, & Specialties

Consumer Packaging (Global)

• E-Commerce

• Material science

• Improved load management

• Film strength

• Emerging Markets (Higher growth GDP)

• Rising middle class

• Infection prevention

• Adult Incontinence

• One-stop shop

• Design flexibility

• Clarity & sustainability

• Convenience

4

Advantaged Products in Targeted Markets

14

On-site recycling facilities

….and is at the forefront of sustainabilityInnovative design solutions

• Recyclability, recycled content, and

reusability are increasingly a sought after

design consideration

• Berry is uniquely positioned to help

customers through our design and

engineering capabilities

• We anticipate more sustainable designs but

no move back to other materials given

plastics unique advantages

5

Sustainability is an Opportunity for Berry

Berry does not manufacture any products that

are restricted under any legalized bans

• Alliance to End Plastic Waste (AEPW)

• Impact 2025

• Signed Ellen MacArthur Foundation

• Partnership with SABIC – chem. recycling

Berry’s Partner Initiatives

• Best-in-class UK-based plastic waste

recycler

• Closed-loop recycler in ag, commercial, and

industrial solutions

• Growth in our reliable collection system to

enhance waste mngt. and increase

recycling, as well as, avoid litter and plastic

leakage into the environment

15

49%

27%

24%

49%

24%

27%

41%

29%

30%

Rigid Plastics NonwovensFlexible Plastics

• Top priority is to de-lever to 3.x

• Completed 46 acquisitions to date

• Average ~5% cost synergies of acquired targets revenue

Source: Plastics News (N.A. only) and Nonwoven Industry Magazines. Rigid Plastics includes thermoforming, blow molding and injection molding. Flexible Plastics includes film and sheet.

Rigid and flexible markets is North American only. Nonwovens is global market.

Top 3

#11-100

#4-10

6

We Believe There Will be Decades of Consolidation Opportunities in a Growing Substrate

N.A.

only

Market fragmentation

Long-term consolidation opportunities - drive future inorganic growth and shareholder returns

16

Margin stability - resin is a pass-through

Resin – Primary raw material

• Resin comprises approximately

50% of COGS

• ~70% of resin pounds sold are

on contractual pass through

• Approximately 55% of our buy

is polyethylene and 40% is

polypropyleneLTM EBITDA

Margin

Ce

nts

pe

r LB

7

~7 Billion Pounds Purchased Annually

Over the past 8 quarters resin volatility was ~40%;

Berry margins remained in a small range

40

50

60

70

80

90

PE Price

PP Price

18.0% 17.5% 17.4% 17.5% 17.4% 17.2% 17.0% 17.1% 17.6%

17

Plastic Packaging Offers:

2000 2015 2025 E• Durability

• Protection/Safety

• Design versatility

• Cost advantage

• Clarity

• Lowest carbon footprint

• Lightweight, lower freight

• Recyclability

37%< 30% 40+%

Plastic Packaging Other Packaging

Global Packaging Market

Sources: WPO Market Statistics and Future Trends in Global Packaging and Smithers Pira

8

Plastic Packaging is Expected to be a Long-Term Growth Substrate

Growing Substrate

18

Sustainability

19

Benefits of Plastics – Lightweight Products

• Shelf stability

• Multi-use

• Protection

• Strength/protection

• Spoilage assurance

• Lightweight

• Versatile options

• Adaptable

• Closable & reusable

• Lightweight

Packaging Characteristic AdvantagesIf plastic packaging was replaced with alternatives,

like paper, metal, and glass:

Alternatives would generate 4x as much

greenhouse gas emissions as plastics

Plastic Packaging has a Lower Overall Environmental Impact than Other Packaging Alternatives

PlasticAlternative Packaging

Materials

Alternatives would require 2x as

much energy as plastics

Alternatives would require 6x as

much water as plastics

Alternatives would generate 5x

as much solid waste as plastics

Winning CharacteristicInfluential Trend

At-home Consumption

Increased e-Commerce

Adoption

Elevated Focus on

Health & Hygiene

Sustainability

20

Impact 2025

Products PartnersPerformance

Minimize product impacts Minimize operational impacts Maximize positive impacts

by engaging partners on key issues

Climate Change

• Reduce greenhouse gas emissions

25% by 2025 versus our 2016

baseline*

Continuous Improvement

• Reduce landfill waste

5% per year*

• Reduce energy and water

consumption 1% per year*

Operation Clean Sweep®

• Prevent resin loss through OCS

• Implement OCS at acquisition sites

within the first year

End Plastic Waste

• Expand and modernize waste

infrastructure to increase recovery

and prevent loss of plastic to the

environment

• Engage the plastics industry on

OCS

Limit Global Warming

• Increase renewable energy

• Expand the use of plastic in place

of alternative materials

• Promote science-based targets

Optimize Design

• Lightweight products

• Design 100% of packaging to

be reusable, recyclable, or

compostable

Sustainable Sourcing

• Increase recycled content

• Encourage the development

of renewable materials

21

Recycled Content: We set a new record for annual usage of post-consumer plastic in FY19 of 70,000 metric tons (154

million pounds). Much of the increase was driven by our acquisition of RPC, which is included on a pro forma basis.

Greenhouse Gas Emissions (GHG): We continued our long-term reduction in Scope 1+2 GHG emissions intensity, having

reduced our intensity 3% year-over-year and 46% since the we began measuring its carbon footprint in 2008. We are

ahead of schedule for achieving our science-based target of a 25% reduction in Scope 1+2 GHG emissions intensity by

2025, having already achieved a 14% reduction vs. our 2016 baseline.

Landfill Waste: We realized a 13% reduction in its landfill waste intensity from 2018 to 2019. This exceeds the our goal

of a 5% reduction year-over-year.

Energy: For the year, we reduced its energy intensity by 3% year-over-year. This exceeds the our goal of a 1% reduction

year-over-year.

Water: In the year 2019, we decreased absolute water intensity 12% from 2018 to 2019, far exceeding the 1% year-

over-year reduction target.

Ahead of Schedule for Impact 2025 Targets

22

As a global leader in food, hygiene, healthcare, personal care and other protective packaging, we play a crucial role and are

an essential part in the supply chain, for safety of necessities, such as food, medicines, sanitizing products and protective

healthcare apparel.

Packaging promotes hygiene and prevents spread of disease. It keeps food safe, prevents spoilage, and preserves its original

properties and it avoids waste. Families and healthcare professionals rely on sterile packaging and plastic packaging to help

protect health and hygiene.

We Play an Essential Role in the Supply Chain

FoodCleaning MedicinesHygiene/Safety

23

“We donated ~100,000 face shields to local first responders and healthcare workers”

“We supplied necessary protective gear to a nearby hospital in Barcelona, Spain”

“We donated 1,500 airless bottles to the University hospitals in France”

“Our facilities in South Africa, donated plastic sheeting for the manufacture of 300 visors for medical use”

We donated over 50,000 hand sanitizer bottles to communities and businesses to aid in the protection of spreading the infection

“We produced gowns for England’s National Health Services in a matter of days”

Supporting Our Local Communities

24

• 40+ global companies from the plastics and consumer goods value chain

• Goal to deploy $1.5 billion to solutions over the next five years

• The Alliance will develop and bring to scale solutions that will minimize and manage plastic waste and promote

solutions for used plastics by helping to enable a circular economy

• Infrastructure development – to collect and manage waste and increase recycling

• Innovation – to advance and scale new technologies that minimize waste, make recycling and recovering

plastics easier, and create value from all post-use plastics

• Education and engagement – of governments at all levels, businesses, and communities to mobilize action

• Clean up – of concentrated areas of plastic waste already in the environment, particularly major rivers that

carry vast amounts of land-based waste to the ocean

• Berry already has a history of reducing the amount of resin annually in our products, as well as, using post-consumer

recycled materials in our product offerings

Alliance To End Plastic Waste (AEPW)

https://endplasticwaste.org/

25

Provides examples of the work Berry has done to:• Reduce waste to landfill

• Source renewable energy

• Test and evaluate new, more efficient equipment

• Institute standardized management plans to reduce environmental impacts

• Conduct product life cycle assessments and explore sustainable materials

• Promote social initiatives in the communities where we live and work

Impact Report & GRI Index

Report in accordance with Global Reporting Initiative (GRI) Standards, includes assurance

statements for absolute energy, carbon emissions, and renewable purchases

Current and past reports can be found here:

https://sustainability.berryglobal.com/resources/

26

Berry Strategy

27

50%

25%

25%

$1.45 Billionprojected in FY 2020

$620 million

Target leverage 3.x

Further long-term opportunities

Cash Flow From Operations

Capex

Debt Pay Down

projected in FY 2020 Targeted capital

spending for organic growth

& cost reduction

Longer-term

opportunity with

experienced teams

Additional share repurchases

Dividends

M&A

Disciplined and

conservative strategyOur Top Priority

Strong, Dependable, and Stable Free Cash Flow Allows Quick De-leveraging

Cost reduction

Maintenance

Growth

Clear Strategy Focused on Value Creation

28

$436

$517

$601 $634

$764

$830

$900

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020E Normalized

Guidance Actual

5.1x

3.9x

4.9x

~4.0x

Leverage@ Close

2-YearsPost Close

Leverage@ Close

2-YearsPost Close

• Exceeded free cash flow guidance every year

since IPO

• Incremental free cash flow from RPC

Strong, consistent free cash flow Ability to rapidly de-lever post acquisition

Case Study Projected

$900+ Million of Normalized Free Cash Flow

4.8x

Enhanced FCF Generation and De-leveraging History

+

3.X

+

29

Appendix: Current Topics

29 20

30

- Lower debt leverageKey Objectives - Grow organically

- Integrate RPC acquisition= Maximize Shareholder Value

Note: Dollars in millions.

We have not provided guidance for the most directly comparable U.S. GAAP financial measure because such information is not

available without unreasonable effort due to the high variability, complexity, and low visibility with respect to certain items,

including tax accruals, restructuring charges, gains and losses related to acquisition and divestiture of businesses, the ultimate

outcome of certain legal or tax proceedings and other unusual gains and losses. These items are uncertain, depend on various

factors, and could be material to our results computed in accordance with U.S. GAAP.

Fiscal Year 2020 Guidance

Cash flow from operations $ $1,450

Less: capital expenditures (620)

Free cash flow $ $830

Free cash flow $ 830

Capital expenditures 620

Cash interest expense 430

Taxes 170

Working capital & other costs 50

Operat ing EBITDA $ 2,100

31

• Over $3 billion of interest rate hedges (swapped variable to fixed)

• ~70% of our revenue is in stable, consumer-centric end markets

• Consistent and defensive cash flow

A 0.25% change in LIBOR would impact our annual interest expense by ~$8 million on variable term loans

Note: Dollars in millions

Euro = +/- $5.5 million of EBITDA A 1% move in:

GBP = +/- $1.5 million of EBITDA

• Over $3 billion of cross currency swaps (Euro & GBP)

• 60% USD, 30% Euro and 10% GBP debt allocation

• Objective of matching geographic debt with earnings

Interest expense exposure

Foreign currency exposure

Liquidity

• $906 million cash on hand

• $850 undrawn ABL Revolver

~$1.8 billion total liquidity

• No financial maintenance covenants

• No near-term debt maturities

Interest Expense, Foreign Currency Exposure, and Liquidity

Term Loans 6,213$

Term Loan Hedges (3,207)

Total Variable 3,006$ 28%

Capital leases and other 40$

Term Loan Hedge 3,207

1st & 2nd Lien Notes 4,507

Total Fixed 7,754$ 72%

32

RPC Overview

33

Leading European rigid and flexible packaging manufacturer serving a range of

consumer, healthcare, and industrial markets

Expansive commercial and operational presence

Balanced long and short-run production capabilities, enhanced by specialty

innovation, engineering, and recycling expertise

Leading consolidator in Europe

Platforms: Injection, blow and rotational molding, thermoforming, and blown

film extrusion

RPC: European leader with a unique design and innovation platform

Recycled and sustainable input polymers

Innovative design solutions

34

Food & beverage

Containers

Convenience foods

Dry foods

Coffee capsules

Closures and caps

Consumer goods

Personal care, beauty

Healthcare & hygiene

Household chemicals

Medical inhaler devices

Drug delivery/dosing systems

Other consumer products

Specialties

Material handling/waste management

Automotive

Tobacco, nicotine delivery systems

Tooling/machinery

Construction

% of legacy RPC sales

~40%

~40%

~20%

Product samplesEnd markets

RPC: End Market Overview

35

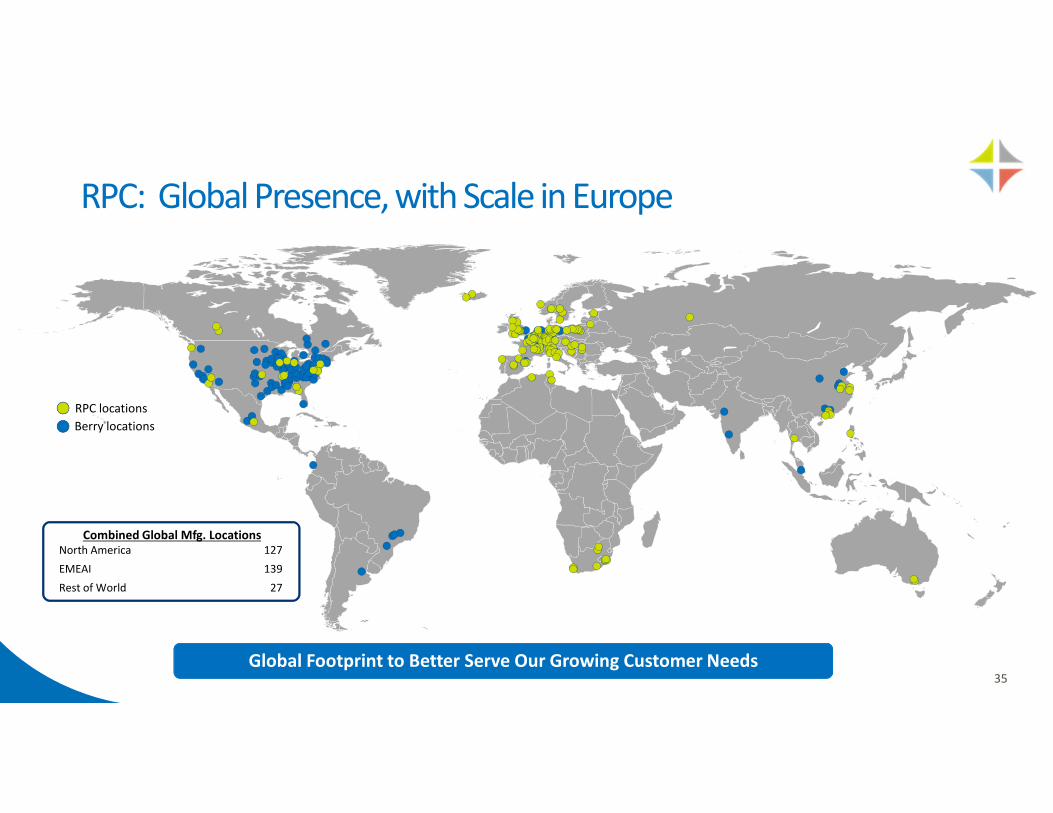

RPC: Global Presence, with Scale in Europe

RPC locations

Berry locations

Combined Global Mfg. LocationsNorth America

EMEAI

Rest of World

127

139

27

Global Footprint to Better Serve Our Growing Customer Needs

36

RPC: Provides enhanced ability to serve customers

Significant Capabilities and Solutions Serving an Attractive Customer Base

• Local, national, and international reach,

quality and service

• Long-term relationships

• Disciplined cost management

• Differentiated standardization and

customization capabilities

• Premium, low-cost and sustainable

solutions

• Local, in-market presence

• Deep product breadth and selection

Common Approaches

37

Appendix: Our Businesses

28

38

Tom Salmon

Chairman & CEO

Passionate leader focused on improving Berry’s financial

performance, creating an entrepreneurial-like workplace

while helping our customers succeed

• Named CEO February 2017

• Prior 12 years with Berry: various leadership roles,

including President and COO; led both Engineered

Materials and Consumer Packaging divisions

• Prior experience includes leadership roles at Tyco

Adhesives, Honeywell and General Electric

Mark Miles

CFO & Treasurer

Disciplined and financially driven leader highly focused on

creating long-term value for Berry

• Named CFO January 2014

• Previous 11 years with Berry as EVP, Controller and

Treasurer

• Started with Berry in 1997 as Corporate Controller

• Integral part of management for 36 of Berry’s 45

acquisitions

Our Leadership

39

• 20,000+ customers globally

• Top customer represents <5% of total revenue

• Top 10 customers represent ~20% of total revenue

• Longstanding relationships with diverse mix of leading

multi-national, regional & local customers

• ~70% of our portfolio is consumer non-discretionary

products such as food and beverage and home, health and

personal care

Blue Chip Customers Include:

Diverse and Stable Customer Base

40

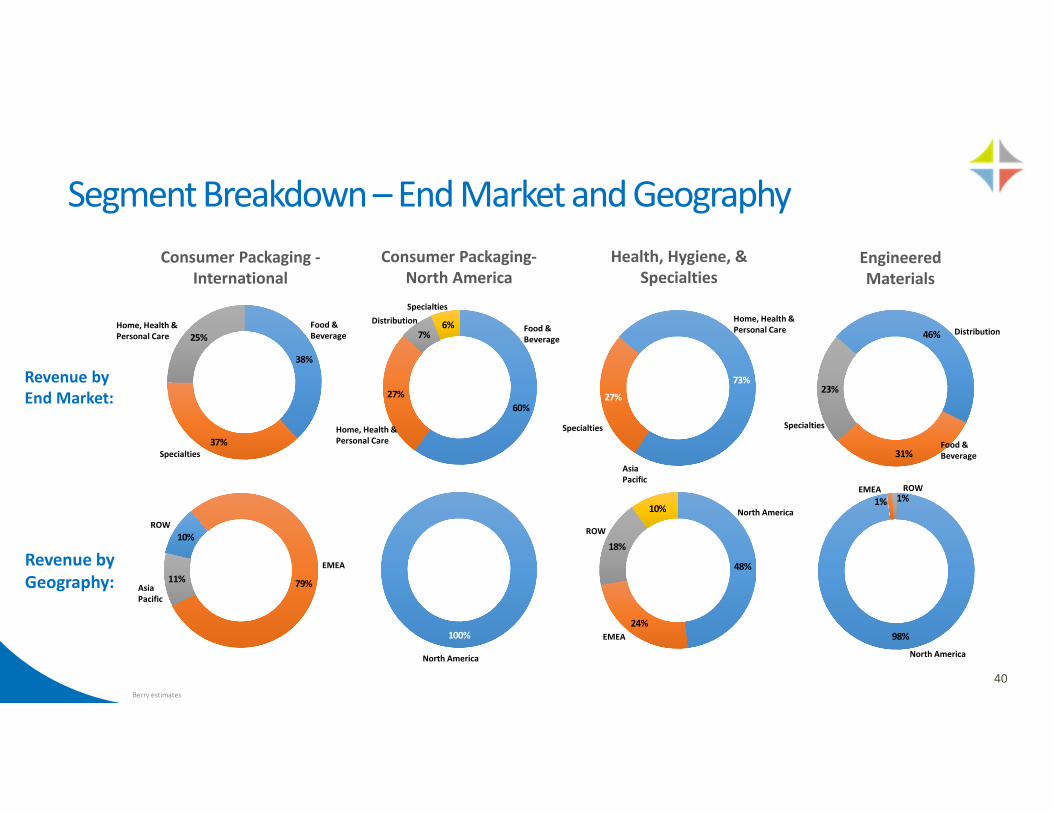

10%

79%11%

98%

1%1%

46%

31%

23%

48%

24%

18%

10%

73%

27%

38%

37%

25%

100%

60%

27%

7%6%

Berry estimates

Revenue by

End Market:

Revenue by

Geography:

Consumer Packaging -

International

Consumer Packaging-

North America

Health, Hygiene, &

SpecialtiesEngineered

Materials

Food &

Beverage

Home, Health &

Personal Care

Specialties

DistributionFood &

BeverageHome, Health &

Personal Care

Specialties

North America

EMEA

ROW

Asia

Pacific

Home, Health &

Personal Care

Specialties

North America

EMEA

ROW

Asia

Pacific

North America

EMEA ROW

Food &

Beverage

Distribution

Specialties

Segment Breakdown – End Market and Geography

41

Containers Closures Beverage Healthcare Personal Care Household Specialties

Product

Examples

Competitors

Not inclusive of all products or competitors

Amcor

Alpla

Coveris

Greiner

Albea

Aptar

Gerresheimer

Nemera

Albea

Aptar

Alpla

Coveris

Amcor

Aptar

Alpla

Plastipak

Greif

Husky

OnePlastics Grp

SULO

Aptar

Reynolds

Mold-Rite

Silgan

Alpla

Bericap

ITW Hi-Cone

Reynolds

Consumer Packaging - International

42

Containers Closures Drink Cups Bottles Tubes Rx Vials Overcaps Jars

Product

Examples

Competitors

Not inclusive of all products or competitors

Airlite

IPL

Polytainer

Alpha

Amcor

Reynolds

Silgan

Albea

CCL

Essel Propack

Viva

Apothecary

Products

Centor

Tri State

Aptar

Cobra

Dubuque

Underwood

Aptar

Reynolds

Mold-Rite

Silgan

Dart

LidWorks

Reynolds

Alpha

Mold-Rite

Intrapack

Omega

Consumer Packaging – North America

43

Diapers Feminine CareAdult

Incontinence

Surgical Products &

Medical Packaging

Pharmaceutical

& Rigid Medical

Wipes Filtration Geosynthetics Ag & Other Building Wraps

Product

Examples

Competitors

Product

Examples

Competitors

Not inclusive of all products or competitors

Avgol

Fitesa

Gulsan

Toray

Ahlstrom-

Munksjö

Amcor

Fitesa

SAAF

Gerresheimer

Nypro

West

Pharmaceutical

Jacob Holm

Sandler

Spuntech

Suominen

Freudenberg

John Mansville

Mogul

Low & Bonar

Naue

TenCate

Thrace

Fitesa

Mogul

Owens Corning

TenCate

Avgol

Fitesa

Pegas

RKW

Avgol

Fitesa

Gulsan

Pegas

Barricade

DuPont

Kingspan

Health, Hygiene, & Specialties

44

Stretch Films Can Liners Tapes Converter Films

Shrink Films Food Films Retail Bags PVC Films

Product

Examples

Competitors

Product

Examples

Competitors

Not inclusive of all products or competitors

All American

Amcor

Colormasters

Hillside

Amcor

Printpack

Sealed Air

WinPak

3M

IPG

Scapa

Shurtape

Clorox

Polyamerica

Reynolds

Aluf

Inteplast

Novolex

Sigma

Inteplast

Malpack

Paragon

Sigma

Amcor

Charter NEX

Next Gen

Sealed Air

Anchor

Fine Pkg

Polyvinyl

Reynolds

Engineered Materials

45

Appendix: Supplemental Data(1) Adjusted EBITDA, free cash flow, and adjusted net income should not be considered in isolation or construed as an alternative to our net income (loss) or other measures as determined in accordance with GAAP. In addition, other companies in our

industry or across different industries may calculate adjusted EBITDA, free cash flow, and adjusted net income and the related definitions differently than we do, limiting the usefulness of our calculation of adjusted EBITDA, free cash flow, and adjusted

net income as comparative measures. EBIT, operating EBITDA, adjusted EBITDA, free cash flow, and adjusted net income are among the indicators used by the Company’s management to measure the performance of the Company’s operations and thus

the Company’s management believes such information may be useful to investors. Such measures are also among the criteria upon which performance-based compensation may be based

41

46

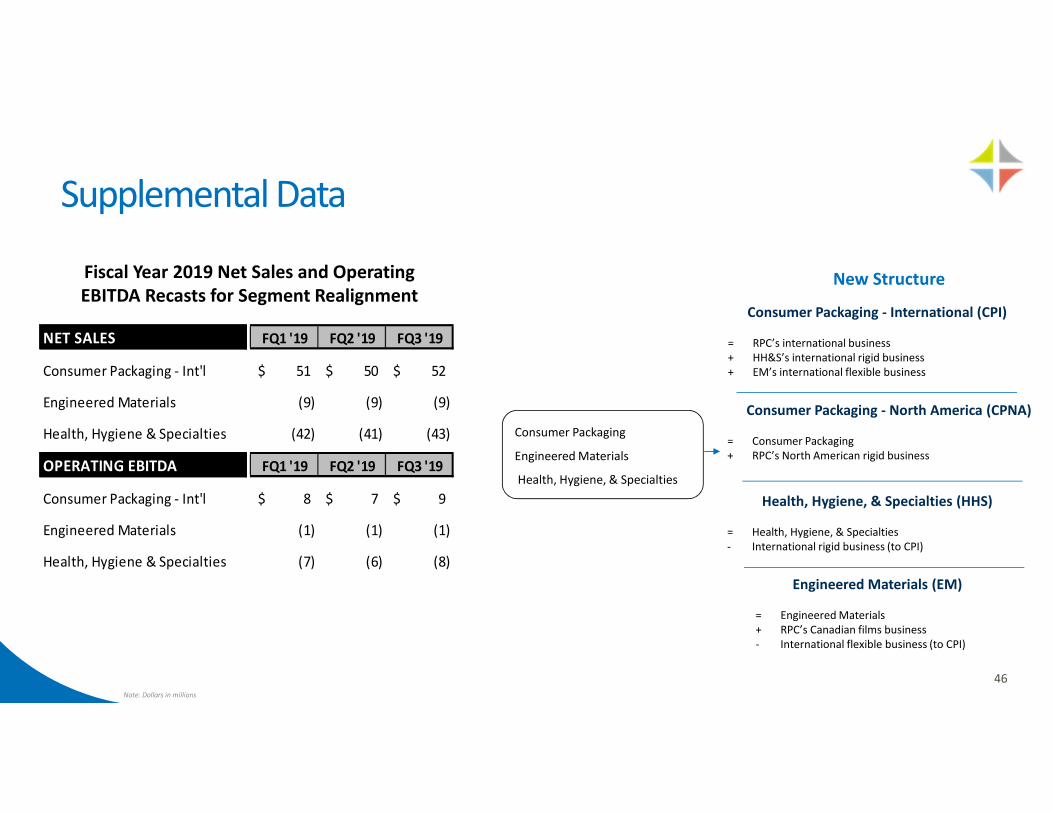

Supplemental Data

Note: Dollars in millions

Fiscal Year 2019 Net Sales and Operating

EBITDA Recasts for Segment RealignmentNew Structure

Consumer Packaging - International (CPI)

= RPC’s international business

+ HH&S’s international rigid business

+ EM’s international flexible business

Consumer Packaging - North America (CPNA)

= Consumer Packaging

+ RPC’s North American rigid business

Health, Hygiene, & Specialties (HHS)

= Health, Hygiene, & Specialties

- International rigid business (to CPI)

Engineered Materials (EM)

= Engineered Materials

+ RPC’s Canadian films business

- International flexible business (to CPI)

NET SALES FQ1 '19 FQ2 '19 FQ3 '19

Consumer Packaging - Int'l 51$ 50$ 52$

Engineered Materials (9) (9) (9)

Health, Hygiene & Specialties (42) (41) (43)

OPERATING EBITDA FQ1 '19 FQ2 '19 FQ3 '19

Consumer Packaging - Int'l 8$ 7$ 9$

Engineered Materials (1) (1) (1)

Health, Hygiene & Specialties (7) (6) (8)

Consumer Packaging

Engineered Materials

Health, Hygiene, & Specialties

47

Non-GAAP Financial Measures

Note: Dollars in millions

Guidance

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Cash flow from operations $637 $857 $975 $1,004 $1,201 $1,450

Capital expenditures, net (162) (283) (263) (333) (399) (620)

Payment of tax receivable agreement (39) (57) (111) (37) (38) -

Free cash flow $436 $517 $601 $634 $764 $830

Actual

48

Non-GAAP Financial Measures

Note: Dollars in millions, except per share data

(1) Includes integration expenses and other business optimization costs.

(2) Primarily includes expenses related to acquisitions and gains related to the sale of assets.

Fiscal Year 2014 2015 2016 2017 2018 2019

Net income per diluted share 0.51$ 0.70$ 1.87$ 2.54$ 3.67$ 3.00$

Other expense (income) 0.20 0.52 (0.18) 0.03 0.18 1.15

Non-cash amortization 0.25 0.17 0.24 0.24 0.21 0.21

Restructuring and transaction activities (2)

0.17 0.07 0.26 0.18 0.27 (0.98)

Other non-cash charges - - 0.38 0.22 0.04 0.29

Business optimization 0.43 0.24 0.20 0.13 0.13 0.05

Tax reform adjustments, net - - - - (0.92) -

Income tax impact on items above - - (0.29) (0.25) (0.21) (0.31)

Adjusted net income per diluted share 1.56$ 1.70$ 2.48$ 3.09$ 3.37$ 3.41$

Fiscal Year 1999 2004 2009 2014 2019

U.S. GAAP Operating income $34 $94 $186 $316 $974

Add: restructuring and transaction activities 5 6 11 30 (132)

Add: business optimization and other costs (1)

2 - 39 81 75

Add: depreciation & amortization 31 61 254 358 613

Operating EBITDA $72 $161 $490 $785 $1,530

(2)

49

Non-GAAP Financial Measures

Note: Dollars in millions

LTM operating EBITDA margins calculated by dividing the sum of the previous four quarters operating EBITDA by the sum of the previous four quarters net sales

(1) Primarily includes other non-cash charges, such as stock compensation expense.

(2) Primarily includes expenses related to acquisitions and transaction activities.

Operating Depreciation & Restructuring & Operating LTM Operating

Quarterly Period Income Amortization Transaction Activities (2)

Other (1)

EBITDA Net Sales EBITDA Margins

Sept '17 199 138 7 6 350 1,881

Dec '17 163 129 13 5 310 1,776

Mar '18 188 132 15 15 350 1,967 18.2%

Jun '18 216 136 15 7 374 2,072 18.0%

Sept '18 194 141 10 1 346 2,054 17.5%

Dec '18 176 138 13 4 331 1,972 17.4%

Mar '19 185 132 22 15 354 1,950 17.5%

Jun '19 215 127 - 6 348 1,937 17.4%

Sept '19 398 216 (162) 45 497 3,019 17.2%

Dec '19 199 216 18 18 451 2,818 17.0%

Mar '20 284 213 19 23 539 2,975 17.1%

Jun '20 347 209 19 6 581 2,910 17.6%

50

Dustin M. StilwellDirector, Head of Investor Relations

Berry Global Group, Inc.

101 Oakley Street, 3rd floor

P. O. Box 959

Evansville, IN 47706

Tel: +1.812.306.2964

www.berryglobal.com