Embed Size (px)

Citation preview

Consumer-Driven Health Plans 1

Blue-by-DesignSM

Health Reimbursement Accounts: A New Era in Benefit Plans

2 Empower

Today’s employers are taking steps to control

healthcare costs while still offering affordable

benefits. They want to give their employees a

greater role in healthcare management. Employers

want to offer more choices, increased control and

new tools to help with healthcare decisions.

Empower

Consumer-Driven Health Plans 1

PPO with HRA Plans

Healthcare consumers play an active role in deciding which doctors and facilities they use, the services they want and the amount they are willing to spend. Empowered consumers are more likely to seek out the information and resources needed to make wise decisions about healthcare.

PPOs with HRAs offer a unique approach to healthcare benefits. They combine a financial donation by the employer with more

choices and control for the members. The employer deposits a set amount of money into a tax-free account called a Health Reimbursement Account (HRA) for each employee. Members use the HRA funds to pay for medical expenses. In addition to the HRA, the employer also offers a traditional health plan to cover other medical bills.

Members manage the funds in their HRA. They have the freedom to choose their own doctors and caregivers and decide what healthcare solutions best meet their needs.

PPO with HRA Plans 1

2 Empower

IRS guidelines dictate how an HRA plan must be set up to qualify for tax advantages:

■ The employer must fund the entire HRA. Members may not fund the HRA in any way.

■ HRAs can reimburse only medical care expenses, as defined by Internal Revenue Code Section 213(d), incurred by members and their eligible dependents.

■ The HRA can pay only those expenses incurred after the employer adopts the

plan and member coverage begins.■ HRAs can pay only substantiated expenses not covered by another plan and not deducted on tax returns.■ The HRA reimburses expenses up to a maximum dollar amount for a coverage period.

Per IRS guidelines, employers do not have to make the entire HRA balance available to members at all times, but only as they contribute funds to the account during the covered benefits period. HRAs can reimburse claims incurred in one covered period in a later covered period.

HRA plans must comply with COBRA and HIPAA regulations. The nondiscrimination rules that prohibit offering better benefits to higher paid individuals also apply to HRAs.

The employer sets a maximum dollar amount of HRA coverage for the employee or for the family (employee and dependents). Members cannot count reimbursements madeunder the HRA against taxable income.

IRS Rules and Regulations for HRAs

2 Empower

Consumer-Driven Health Plans 3

Qualifying Expenses

An HRA reimburses qualifying expenses for members and their eligible dependents. This means HRAs reimburse only those expenses that qualify as “medical care” and are not also reimbursed by insurance or other sources.

“Medical care” expenses as defined by Internal Revenue Code Section 213(d) include amounts paid for the diagnosis, treatment or prevention of disease, and for treatments affecting any part or function of the body. The expenses must improve or prevent a physical defect or illness.

Members can use their HRA dollars for any healthcare costs covered by the benefits plan. The following are examples of reimbursable expenses: ■ Office visits ■ Urgent care ■ Lab and X-ray services ■ Prescription drugs ■ Outpatient services ■ Hospital visits

Expenses for products or services used solely for cosmetic purposes do not qualify as medical care. Neither do products and services that are merely beneficial to general health. Examples of ineligible expenses include: ■ Cosmetic surgery ■ Health club dues ■ Marriage or family counseling ■ Vacations ■ Teeth whitening ■ Vitamins taken for general health purposes

When a claim is submitted, a claims processor reviews the expense to determine if itqualifies for reimbursement under the HRA. Empower

PPO with HRA Plans 3

4 Empower

Consumer-Driven Health Plans 5

Freedom

Blue-by-DesignSM:A Flexible Health Plan

6 Empower

Blue-by-DesignSM is BlueCross’ PPO with HRA plan. It

combines the security of a traditional health plan with

greater flexibility, more control and new tools to help

manage your healthcare spending decisions. It offers

a low cost, high-deductible medical plan along with an

employer-funded health reimbursement account (HRA).

Freedom

Consumer-Driven Health Plans 7

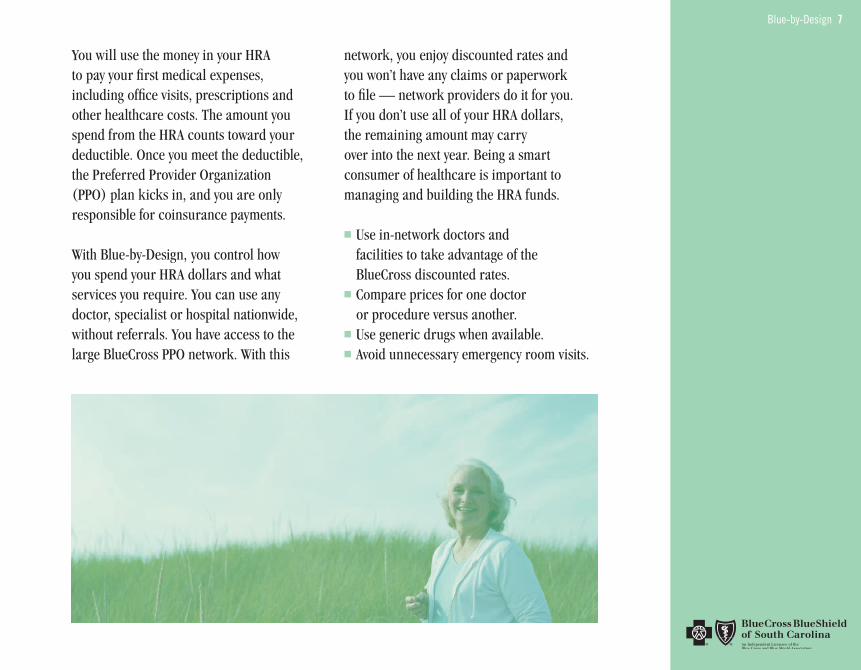

You will use the money in your HRA to pay your first medical expenses, including office visits, prescriptions and other healthcare costs. The amount you spend from the HRA counts toward your deductible. Once you meet the deductible, the Preferred Provider Organization (PPO) plan kicks in, and you are only responsible for coinsurance payments.

With Blue-by-Design, you control how you spend your HRA dollars and what services you require. You can use any doctor, specialist or hospital nationwide, without referrals. You have access to the large BlueCross PPO network. With this

network, you enjoy discounted rates and you won’t have any claims or paperwork to file — network providers do it for you.If you don’t use all of your HRA dollars, the remaining amount may carry over into the next year. Being a smart consumer of healthcare is important to managing and building the HRA funds.

■ Use in-network doctors and facilities to take advantage of the BlueCross discounted rates.

■ Compare prices for one doctor or procedure versus another.

■ Use generic drugs when available.■ Avoid unnecessary emergency room visits.

Blue-by-Design 7

8 Empower

How Does the Blue-by-Design Plan Work?

A Blue-by-Design health benefits plan has three main parts: a health reimbursement account (HRA), a bridge and a health plan. Both employee-only and family plans are available.

Part One: The Health Reimbursement Account (HRA)Your employer puts a set amount of money in your HRA. You should use the HRA funds for all medical costs covered by your benefits plan that you incur during the benefits year. These include office visits and prescription drugs. For family coverage, you can use the HRA fund to pay for services received by any member under your benefits plan.

When you or your dependents have an eligible expense, you will receive reimbursement from your HRA. Expenses your HRA funds pay for count toward the deductible for your health plan. You will be able to monitor and track your healthcare expenses and HRA balance online. If you do not spend all of your HRA funds during the benefits period, it may roll over to the next year’s HRA balance. Check your plan materials for more information about your HRA.

Part Two: The BridgeIf you spend all of the funds in your HRA, you will pay additional healthcare expenses out-of-pocket until you meet the PPO plan deductible. There may be a gap in time between reimbursement from the HRA fund and when the benefits from the PPO health plan begin. Careful planning is important.

Part Three: The Health PlanOnce you meet your deductible, your healthcare benefits begin, and you will only pay your coinsurance payments. Under the family plan, there is just one deductible for the entire family to meet. The plan’s out-of-pocket maximum limits your total coinsurance expenses. If you meet your out-of-pocket maximum, the plan begins paying eligible expenses at 100%. This maximum protects you from catastrophic expenses.

8 Empower

Consumer-Driven Health Plans 9

Is Blue-by-Design the Right Choice for You?

Blue-by-Design protects you against high expenses with the traditional PPO plan. But if you have few expenses and don’t use all of your HRA funds, you will not have any out-of-pocket claim costs. Dollars left at the end of

the benefit year could roll over creating a larger opening balance for the following year. The goal of a Blue-by-Design plan is to strike a good balance between managing expenses and the cost of the PPO plan coverage.

Blue-by-Design 9

A Sample Blue-by-Design Plan:

10 Empower

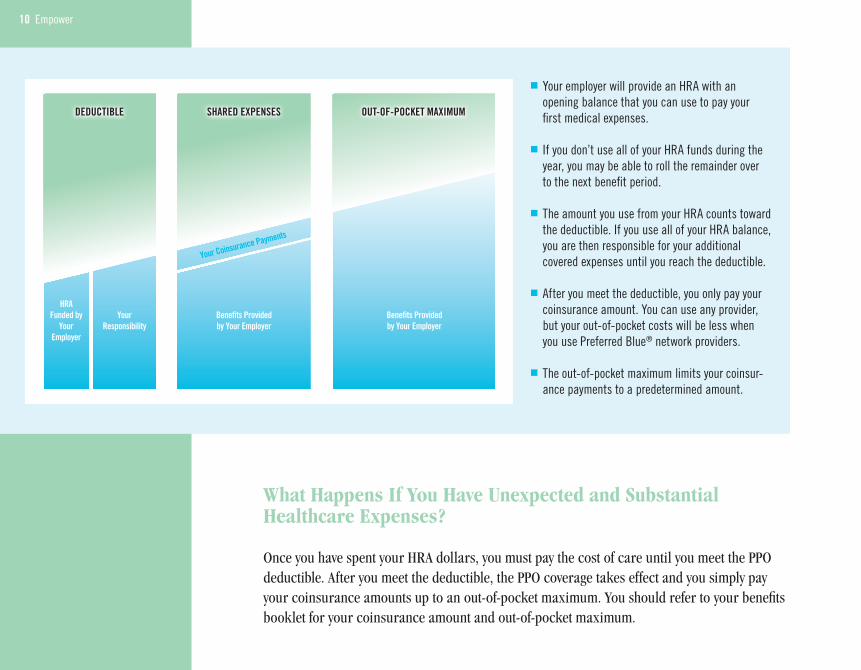

■ Your employer will provide an HRA with an opening balance that you can use to pay your

first medical expenses.

■ If you don’t use all of your HRA funds during the year, you may be able to roll the remainder over

to the next benefit period.

■ The amount you use from your HRA counts toward the deductible. If you use all of your HRA balance, you are then responsible for your additional covered expenses until you reach the deductible.

■ After you meet the deductible, you only pay your coinsurance amount. You can use any provider, but your out-of-pocket costs will be less when you use Preferred Blue® network providers.

■ The out-of-pocket maximum limits your coinsur-ance payments to a predetermined amount.

10 Empower

What Happens If You Have Unexpected and Substantial Healthcare Expenses?

Once you have spent your HRA dollars, you must pay the cost of care until you meet the PPO deductible. After you meet the deductible, the PPO coverage takes effect and you simply pay your coinsurance amounts up to an out-of-pocket maximum. You should refer to your benefits booklet for your coinsurance amount and out-of-pocket maximum.

���������� ��������������� ���������������������

������������

������������

������������������

���������������������������������

�������������������������

���������������������������������

Consumer-Driven Health Plans 11

Freedom

What Are the Advantages for Individuals Covered by Blue-by-Design? ■ Your employer completely funds the Blue-by-Design HRA, and the funds are tax-free.■ With Blue-by-Design, you can visit any physician or hospital,

in or out of network, with no referral required.■ You can take advantage of the discounted rates offered by the healthcare professionals and facilities in the large, nationwide BlueCross PPO network.■ Blue-by-Design empowers you to spend your

healthcare dollars in a way that fits your needs.■ Funds left in the HRA at the end of the coverage period may carry over to the next year’s HRA balance — an excellent way to save for future healthcare expenses.■ You have access to all of the value-added programs and

discounts that BlueCross members enjoy for services, such as massage therapy, acupuncture, chiropractic care,

cosmetic surgery, LASIK surgery, eyewear and hearing care.■ Any HRA funds spent count toward the deductible of the health plan.

Tracking Your HRA Balance

You can monitor and track your HRA balance online through the Blue-by-Design section of our Web site. This service is secure and confidential. After you enroll as a Blue-by-Design member, you will receive a welcome letter that contains your username and password for the HRA tracking system.

Once you login for the first time, you can change these to a username and password of your preference. If you forget your password, you can have it e-mailed to you from the site. From your HRA home page, you can view your account history to monitor your remaining balance and transaction activity. You’ll find answers to questions such as:

■ Did they receive my claim?■ Were the expenses approved or denied, and why?■ What is the balance remaining in my HRA account?

You can see a summary of all employer contributions, claims processed and reimbursements paid for your HRA account since the beginning of the plan. You can view your claims history and an Explanation of Payment (EOP) for any claim that has been processed. You can also check the status of pending claims to see when your reimbursement is released. An online user guide is available for your reference.

In other sections of our Web site, you can:■ Download and print forms for your health plan■ Access eligibility, benefits, coverage and claim information ■ Search for network providers at home or around the world■ Review the Preferred Drug List using My Pharmacy Manager■ Research health and wellness topics in our reference library■ Send a question to Customer Service■ Learn more about the discount and added value programs available to all members

Blue-by-Design 11

12 Empower

Consumer-Driven Health Plans 13

Discover

Frequently Asked Questions

14 Empower

How Does Blue-by-Design Work?Blue-by-Design combines the protection of a traditional health plan with an employer-paid health reimbursement account (HRA). You have the freedom to use the doctors and facilities of your choice without a referral. You have access to a large network of discounted physicians and hospitals, as well as the option to seek out-of-network care for a higher out-of-pocket cost.

You use the dollars in your HRA to finance medical care during the year. Once you meet your deductible, you are only responsible for your coinsurance payments.

What Is an HRA?An HRA is a medical reimbursement plan paid solely by the employer. When creating the HRA (and then on an annual basis), the employer sets the maximum HRA fund balance per employee.

Discover

Consumer-Driven Health Plans 15

Under an HRA plan, the employer reimburses you for qualified medical expenses. The HRA reimburses you up to the maximum dollar amount your employer sets for the coverage period. Any unused portion may carry forward to the next year’s balance.

What Is the Cost to Someone Who Selects Blue-by-Design?Blue-by-Design provides an employer-paid health fund for medical expenses and a traditional health plan with preset coinsurance percentages. With Blue-by-Design, you can go to any doctor. However, you will receive discounts when you receive care in BlueCross’ large network of physicians and hospitals.

If you don’t use all of your HRA dollars, the remaining amount may carry over into the next year. If you deplete the fund in a given year, you will pay expenses to meet a deductible. Once you meet the deductible, a traditional health plan goes into effect, including coinsurance. Your employer sets the maximum annual expense you must pay out-of-pocket.

When you select Blue-by-Design, you can expect to save on coverage costs compared to traditional plans.

Frequently Asked Questions 15

16 Empower

For example, how much does it really cost to carry a health benefits policy with a low copayment? Let’s assume the copayment is $15. This month, you send one family member to the doctor. The cost? “Just 15 bucks.” A closer look reveals a key fact — we can’t forget to include the medical premium deducted from your paycheck. After all, the total amount of money out of your pocket is just that — money out of your pocket.

Let’s assume a typical family plan costs $650 in monthly premiums. Wouldn’t it then be more accurate to state that your total expense for the month was $665? After all, you had to pay the $650 for the convenience of the $15 copayment. What if that was the ONLY doctor visit for the year? Now how much did that one visit cost? The annual premium is $7,800 PLUS $15 for the doctor’s visit, so your annual cost is $7,815.

The annual premium for Blue-by-Design is typically lower than a standard PPO or HMO plan. When comparing the total costs for plan options, you must factor in premium costs. Even if you spend your HRA funds and have to pay costs until you meet your deductible, the money you saveon Blue-by-Design premiums may make it the better value.

As with most BlueCross plans, there are opportunities to save on alternative health services and hearing care and to enjoy discounts on eyewear, contact lenses, cosmetic surgery and LASIK surgery.

How Do I Track My HRA Balance?You can monitor and track your HRA balance online. Log onto the BlueCross Web site, enter the members’ section and click on the Blue-by-Design button. On the Blue-by-Design screen, click in the space indicated to check your Health Reimbursement Account. From there you will enter the login page for Health Reimbursement Account Administration. The HRA Administration service is private and secure.

16 Empower

Consumer-Driven Health Plans 17

Can HRA Funds Be Carried Over into Future Years?All or part of any funds remaining at the end of the coverage period may qualify to be carried forward. Check your plan materials for information about your HRA’s carry-over provisions.

Can You Contribute to Your HRA?No, only employers can fund HRA plans. The employer may elect to offer an employee-funded Flexible Spending Account (FSA) option in connection with the Blue-by-Design plan. Members can contribute pre-tax dollars to an FSA, but unlike the HRA, you cannot rollover money left in the FSA at year’s end, per IRS rules.

Does COBRA Apply to Blue-by-Design?HRA plans are group health plans generally subject to the COBRA requirements. If a member elects COBRA continuation coverage, an HRA plan complies with COBRA requirements. The HRA will provide for the continuation of the maximum reimbursement amount for the member at the time of the COBRA qualifying event. It will also increase that maximum amount at the same time and by the same increment that it is increased for similarly situated non-COBRA beneficiaries (and by decreasing it for claims reimbursed).

Where to Find Additional InformationIf you have questions about your Blue-by-Design plan, call your benefits administrator or your employer’s Human Resources department.

Frequently Asked Questions 17

Discover

18 Empower

Consumer-Driven Health Plans 19

Glossary of terms

Allowable Charge: Charges for medical services or supplies provided by a hospital or physician that qualify as covered expenses as stated in the health plan’s Schedule of Benefits.

Benefit: The amount of money a health plan pays for the cost of covered services, as defined in the Schedule of Benefits.

Benefit Period: The maximum length of time for which the health plan will pay benefits.

Case Management: A standardized program that focuses on coordinating a number of services needed by members with prolonged, expensive, or chronic conditions. It includes a standardized, objective assessment of the patient’s needs, and the development of a goal-oriented, individualized service or care plan.

Claim: An itemized statement of healthcare services and their costs from a hospital, physician’s office, or other provider facility. Claims are submitted to the insurer for payment of the costs incurred by the member.

COBRA (Consolidated Omnibus Budget Reconciliation Act): A federal law that, among other things, requires employers to offer employees and their dependents, who would otherwise lose their group health plan eligibility, continuation of coverage under the firm’s group plan. Employers must make health plans available for periods ranging from 18 to 36 months.

Coinsurance: An amount or percentage that health plan members must pay for healthcare products or services in conjunction with their employer’s benefit plan. For example, in an 80% / 50% plan, the health plan pays 80% of your in-network healthcare expenses, and you pay 20%. For non-network expenses, both you and the health plan pay 50%.

Covered Services: Services for which you receive benefits under your employer’s healthcare benefits plan.

Deductible: Set amount that a health plan member must spend before the benefits plan begins to pay for covered medical services.

Glossary of Terms 19

20 Empower

Dependent: An individual other than a health plan member who is eligible to receive healthcare services under the member’s contract. Generally, dependents are limited to the member’s spouse and minor children.

Explanation of Benefits (EOB): A statement a health plan sends to a member who files a claim. It lists the services provided, the amount billed, and the payment made. The EOB also explains why a claim was or was not paid, and provides information about the individual’s rights of appeal.

Explanation of Payment (EOP): A health plan statement sent to a member who requests reimbursement from his or her HRA account. The EOP informs the member whether the request was approved or denied, if there were funds available in the HRA account and the amount of any payment made, either by check or by direct deposit, to the member.

First-Dollar Coverage: Applies to items that Blue-by-Design covers, but are not subject to the plan’s deductible. Items may include preventive care such as annual physicals, well-child visits and mammograms. (Actual coverage varies by employer.)

Flexible Spending Accounts (FSAs): Employee-owned accounts used to pay for medical and/or dependent care throughout the year. Contributions to FSAs reduce employees’ taxable income, but any amount that remains in the account at year-end is forfeited; employees must “use it or lose it.”

Generic Drug: Drugs that are chemically equivalent to Brand Name Drugs whose patent has expired and which are approved by the Federal Food and Drug Administration (FDA).

Health Benefit Plan: The health insurance product that is defined by the benefit contract and represents a set of covered services and provider network.

Health Reimbursement Accounts or Arrangements (HRAs): Nontaxable employer-owned and funded accounts that employees use to pay for healthcare services throughout the year. Unlike FSAs, employees may be able to roll over unused funds from year to year.

HIPAA (Health Insurance Portability and Accountability Act of 1996): A federal law that lets people qualify immediately for comparable health insurance coverage when they change jobs. It also gives the Department of Health and Human Services (HHS) the authority to mandate the use of standards for the electronic exchange of healthcare data. HHS also specifies what medical and administrative code sets should be used within those standards. It requires the use of national identification systems for healthcare patients, providers, payers (or plans) and employers (or sponsors). It also specifies the types of measures required to protect the security and privacy of personally identifiable healthcare information.

Identification (ID) Card: A card issued by a health plan to a covered person and possibly his or her dependents. It identifies the member to a healthcare professional or facility for services. The physician or facility uses the card to determine benefit levels and to prepare the billing statement.

In-Network: Refers to the use of providers who participate in the health plan’s network. Many benefit plans encourage members to use participating (in-network) providers to reduce the amount paid by the member.

Inpatient: A person who is admitted to a hospital for medical care, is assigned a bed designated for routine, special, psychiatric, or rehabilitation care, and occupies the bed for 24 hours or more.

20 Empower

Consumer-Driven Health Plans 21

Medically Necessary: Covered services required to preserve and maintain the health status of a member according to accepted standards of medical practice in the medical community where services are rendered. In other words, services or treatments are considered medically necessary and appropriate if omitting them would adversely affect the patient’s condition or the quality of medical care provided.

Network: A specific group of healthcare professionals or facilities that have contracted with a health benefits company to provide services.

Out-of-Network: The use of healthcare professionals and facilities who have not contracted with the health plan to provide services. Members enrolled in preferredprovider organizations (PPO) can go out-of-network, but will pay more of the costs.

Out-of-Pocket: Costs that a member must pay outside of his or her health benefits plan.

Out-of-Pocket Maximum: A cap on the amount a health plan member must pay outside of his or her benefits plan for covered services. Refer to your Benefit Booklet for specific details on the type of expenses that count toward your plan’s Out-of-Pocket Maximum.

Outpatient: A patient who receives medical services at a health facility without being admitted to the facility for an overnight stay. Also referred to as Ambulatory.

Preventive Care: Programs or services that can help maintain good health, such as annual physical exams, or are meant to detect early signs of health problems or disease, such as mammograms and colon cancer screenings.

Preferred Provider Organization (PPO): A health benefits plan that lets members choose any healthcare professional without designating a primary care physician, but offers lower costs to members who choose a “preferred” or in-network physician or hospital.

Qualified Medical Care Expenses: Expenses paid for medical care as described in Section 213(d) of the Internal Revenue Code and defined amounts paid to diagnose, treat or prevent disease, and to treat any part or function of the body. The expenses must be to alleviate or prevent a physical defect or illness. Expenses for solely cosmetic reasons generally are not expenses for medical care. Also, expenses that merely benefit one’s general health are not expenses for medical care.

Glossary of Terms 21

22 Empower

For more information, please call the customer service number on the back of your ID card or visit

www.SouthCarolinaBlues.com

® Registered marks of the Blue Cross and Blue Shield Association SM Service mark of the Blue Cross and Blue Shield Association