Embed Size (px)

Citation preview

William Kong & Company http:\\www.williamkong.com.hk

1

Benefits of Hong Kong Holding Companies for making

International InvestmentsSpeaker: William Kong

William Kong & Companyhttp://www.williamkong.com.hk

William Kong & Company http:\\www.williamkong.com.hk

2

Context Investments in form of capital

Return in form of Dividend

Plan to exit by selling shares in company

Parent Company

Subsidiary

DividendWithholding

Tax

Tax on Foreign Dividend

William Kong & Company http:\\www.williamkong.com.hk

3

Glossary With Holding Tax – “WHT”

Tax on Foreign dividend

Double Taxation Agreement “DTA”

Dividend

Royalties

William Kong & Company http:\\www.williamkong.com.hk

4

Case Study: China and Japan Japanese Company Directly invest into China

Chinese – Japanese DTA in place.

China company pay dividend to Japanese parent, 10% needs to be with held by China

Japan will not tax this under their Foreign Dividend Exclusion System “FDES”

Requirement: parent to hold >25% subsidiary for 6 months.

Overall: 10% tax in China

Japanese Parent

Chinese Subsidiary

10% WHT

Foreign Dividend Tax 0%

Dividend

William Kong & Company http:\\www.williamkong.com.hk

5

Hong Kong intermediate holding comapny

Japan Parent

Hong Kong Intermediate

Chinese Subsidiary

William Kong & Company http:\\www.williamkong.com.hk

6

China Hong Kong DTA China subsidiary can pay dividend to

Hong Kong parent at 5% With holding tax.

Hong Kong charges no with holding tax when paid to a Japanese parent.

Overall: 5% tax

Saves 5% compared with a Japanese Parent going direct to China

Japan Parent

Hong Kong Intermediate

Chinese Subsidiary

5% WHT

0% Dividend Tax0% WHT

0% Foreign Dividend Tax

William Kong & Company http:\\www.williamkong.com.hk

7

Any catch? Hong Kong intermediate needs to carry out some trade to get the lower 5%

with holding tax in China

Hong Kong Audited accounts and tax return needs to be presented to China.

BUT: Trading activities in Hong Kong can all be managed abroad.

William Kong & Company http:\\www.williamkong.com.hk

8

China invest into JapanDirect Method:

Japanese profits tax at 30%, Japan WHT 10% under Japan - China DTA

China normally tax foreign dividend at 25%, but will give tax credit to 37% tax already paid. No Chinese tax. [(1-30%) x (1-10%)] / 100

Overall: 37%

Chinese Parent

Japanese Subsidiary

Profits Tax 30%10% WHT

25% Tax on dividend – Tax Credit given

William Kong & Company http:\\www.williamkong.com.hk

9

In-direct MethodIn-direct Method (via Hong Kong):

Lose tax credit of 37% paid to Japan.

China charges 25% tax on net after 37% already paid.

Overall: 52.75%!!! 1-(75% x 63%)

Not always comparable when country pairs are reverted.

Chinese Parent

Hong Kong Intermediate

Japanese SubsidiaryWHT 10%

Profits tax 30%

0% Dividend Tax0% WHT

25% Tax. No tax credit.

William Kong & Company http:\\www.williamkong.com.hk

10

Case Study: Europe invest into China The largest economies in Europe largely have DTA with China now

Dividend WHT at 10%.

Most EU countries charges tax on foreign dividend income

But give tax credit to Chinese tax/WHT paid.

Direct may be the better way.

Except for the United Kingdom

William Kong & Company http:\\www.williamkong.com.hk

11

Europe invest into China – continue United Kingdom does not tax foreign

dividend

So, China pays Hong Kong at 5% WHT and Hong Kong pays UK at 0% WHT

In direct method Overall 5% deduction

Direct method: China pays UK 10% WHT.

UK Parent

Hong Kong Intermediate

Chinese Subsidiary

William Kong & Company http:\\www.williamkong.com.hk

12

Exit route – selling your shares Capital Gain Tax

UK 18% - 28%

Japan 10% - set to increase to 20%

China – around 25%

Japanese Parent

Chinese Subsidiary

Chinese Capital Gain Tax at 25%

William Kong & Company http:\\www.williamkong.com.hk

13

Exit route – selling your shares – cont’d How about selling your Hong Kong

company shares instead?

Hong Kong charges 0% Capital Gain tax Hong Kong 0%

Capital Gain Tax

Japan Parent

Hong Kong Intermediate

Chinese Subsidiary

William Kong & Company http:\\www.williamkong.com.hk

14

Intellectual Properties - Royalties Model

Our Intellectual Property Company “IPC” owns the IP and receive royalties

The royalties are taxed at the jurisdiction of the IPC and paid out as dividend

Consideration given to both IPC receipt of royalties and the tax rate of the IPC on that royalty

William Kong & Company http:\\www.williamkong.com.hk

15

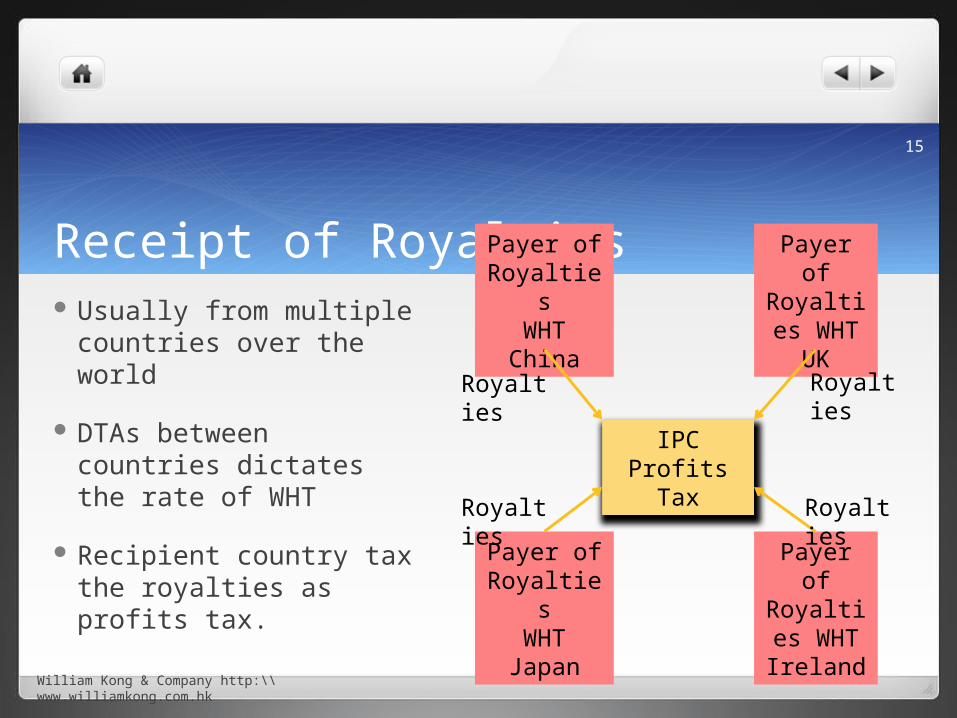

Receipt of Royalties Usually from multiple countries

over the world

DTAs between countries dictates the rate of WHT

Recipient country tax the royalties as profits tax.

IPCProfits Tax

Payer of Royalties

WHTChina

Payer of Royalties

WHTJapan

Payer of Royalties

WHTUK

Payer of Royalties

WHTIreland

RoyaltiesRoyalties

Royalties Royalties

William Kong & Company http:\\www.williamkong.com.hk

16

With holding tax of paying Royalties to Hong Kong

William Kong & Company http:\\www.williamkong.com.hk

17

Profits tax on Hong Kong Royalty income Profits tax 16.5% rate Closest contender is Luxembourg Even lower tax rate on IP at 5.75% However, certain conditions to be meet:

1. IP not transferred from owner to the Company

2. Expenses for the IP must be recorded as asset on the company balance sheet No particular requirements in HK May be taxed when Luxembourg company pays a dividend

William Kong & Company http:\\www.williamkong.com.hk

18

Selling your Intellectual Property Capital Gain lower at 0% in HK Capital Gain on Luxembourg is 5.75%