Embed Size (px)

Citation preview

T h e A u d i t o r - G e n e r a lAudit Report No.25 2000–2001Information Support Services

Benchmarking the Finance Function

A u s t r a l i a n N a t i o n a l A u d i t O f f i c e

2 Benchmarking the Finance Function

© Commonwealthof Australia 2000

ISSN 1036-7632

ISBN 0 642 44274 6

This work is copyright. Apart fromany use as permitted under theCopyright Act 1968, no part may bereproduced by any process withoutprior written permission from theCommonwealth, available fromAusInfo. Requests and inquiriesconcerning reproduction and rightsshould be addressed to:The Manager,Legislative Services,AusInfoGPO Box 1920Canberra ACT 2601or by email:[email protected]

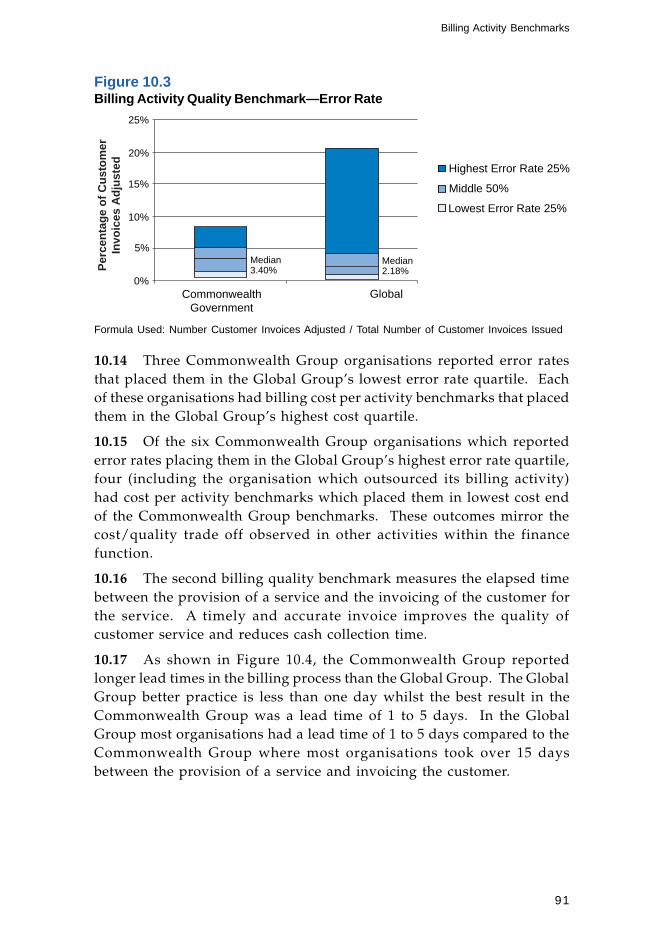

3

Canberra ACT22 December 2000

Dear Madam PresidentDear Mr Speaker

The Australian National Audit Office has undertaken abenchmarking study in accordance with the authority containedin the Auditor-General Act 1997. I present this report of thisaudit, and the accompanying brochure, to the Parliament. Thereport is titled Benchmarking the Finance Function.

Following its tabling in Parliament, the report will be placed onthe Australian National Audit Office’s Homepage—http://www.anao.gov.au.

Yours sincerely

P. J. BarrettAuditor-General

The Honourable the President of the SenateThe Honourable the Speaker of the House of RepresentativesParliament HouseCanberra ACT

4 Benchmarking the Finance Function

AUDITING FOR AUSTRALIA

The Auditor-General is head of theAustralian National Audit Office. TheANAO assists the Auditor-General tocarry out his duties under the Auditor-General Act 1997 to undertake performanceaudits and financial statement audits ofCommonwealth public sector bodies andto provide independent reports and advicefor the Parliament, the Government andthe community. The aim is to improveCommonwealth public sectoradministration and accountability.

Auditor-General reports are available fromGovernment Info Shops. Recent titles areshown at the back of this report.

For further information contact:The Publications ManagerAustralian National Audit OfficeGPO Box 707Canberra ACT 2601

Telephone (02) 6203 7505Fax (02) 6203 7798Email [email protected]

ANAO audit reports and informationabout the ANAO are available at ourinternet address:

http://www.anao.gov.au

Audit TeamEdward Hay

Grace GuilfoyleHayley MacGregor

5

Contents

Summary, Key Findings and RecommendationSummary 9Key Findings and Recommendation 12

Benchmark Study Findings and Conclusions1. Introduction 17

2. Overall Finance Function Benchmark 23Introduction 23Cost Dimension Benchmarks 25Quality Dimension Benchmarks 27

3. Financial Budgeting and Analysis Activity Banchmarks 31Introduction 31Cost Dimension Benchmark 31Efficiency Dimension Benchmark 33Better Practice Benchmark 34Better Practice Observations 35

4. Fixed Assets Activity Benchmarks 37Introduction 37Cost Dimension Benchmarks 38Efficiency Dimension Benchmark 39Quality Dimension Benchmark 40Better Practices Observations 41

5. Accounts Payable Activity Benchmarks 45Introduction 45Cost Dimension Benchmarks 46Efficiency Dimension Benchmarks 49Quality Dimension Benchmark 50Conclusion 52

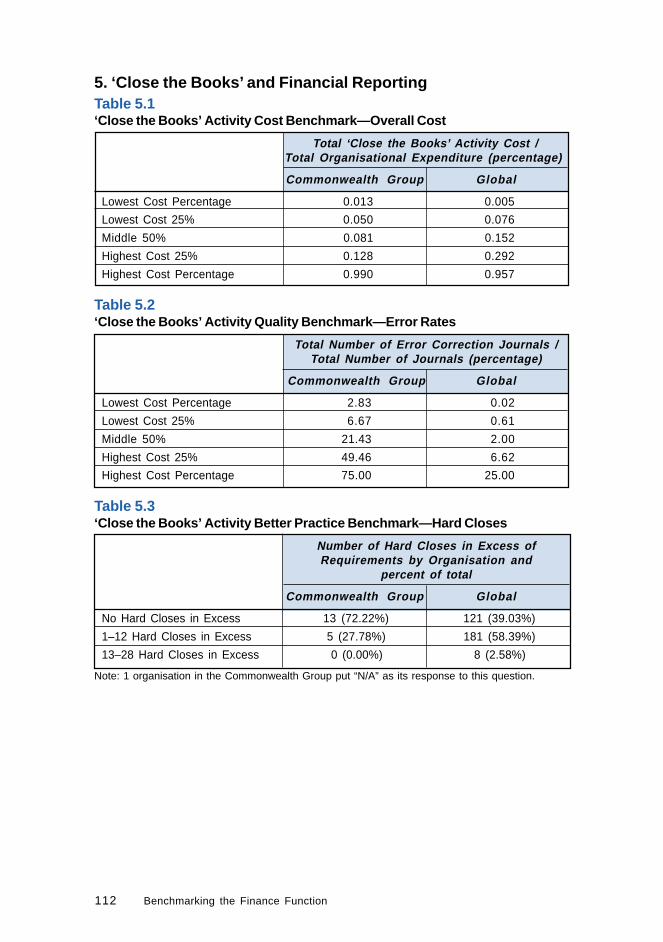

6. ‘Close the Books’ and Financial Reporting Activity Banchmarks 56Introduction 56Cost Dimension Benchmark 57Quality Dimension Benchmarks 58Conclusion 59Better Practice Observations 60

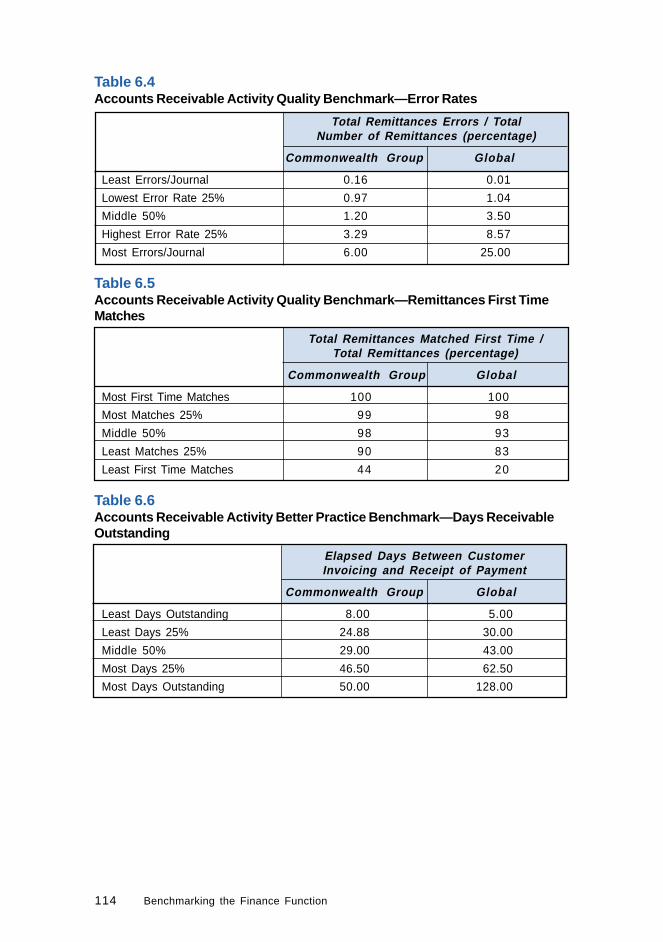

7. Accounts Receivable Activity Benchmarks 61Introduction 61Cost Dimension Benchmarks 62Efficiency Dimension Benchmark 64Quality Dimension Benchmarks 65Conclusion 68Better Practices Observations 68

6 Benchmarking the Finance Function

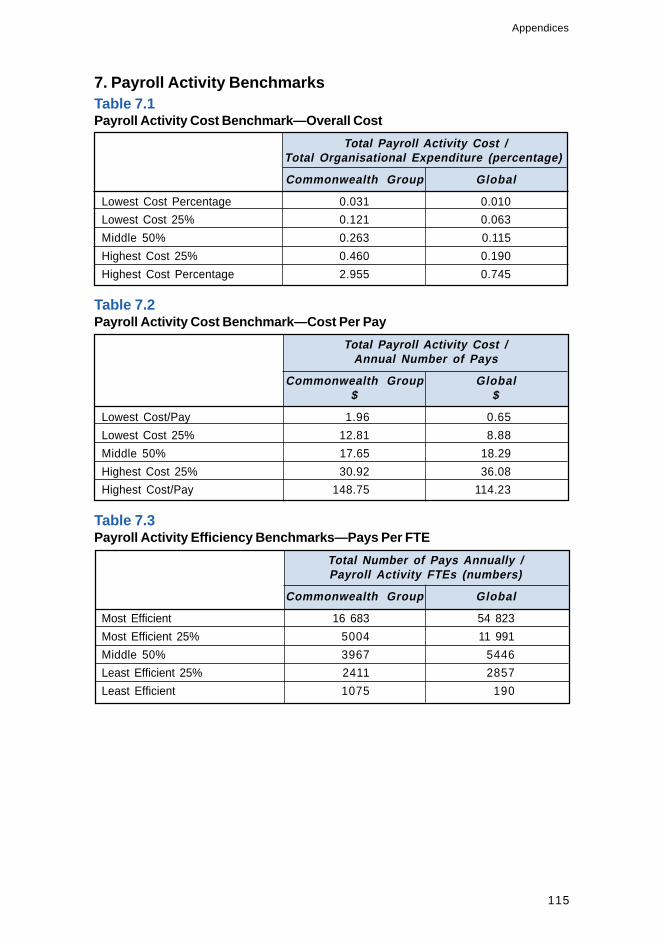

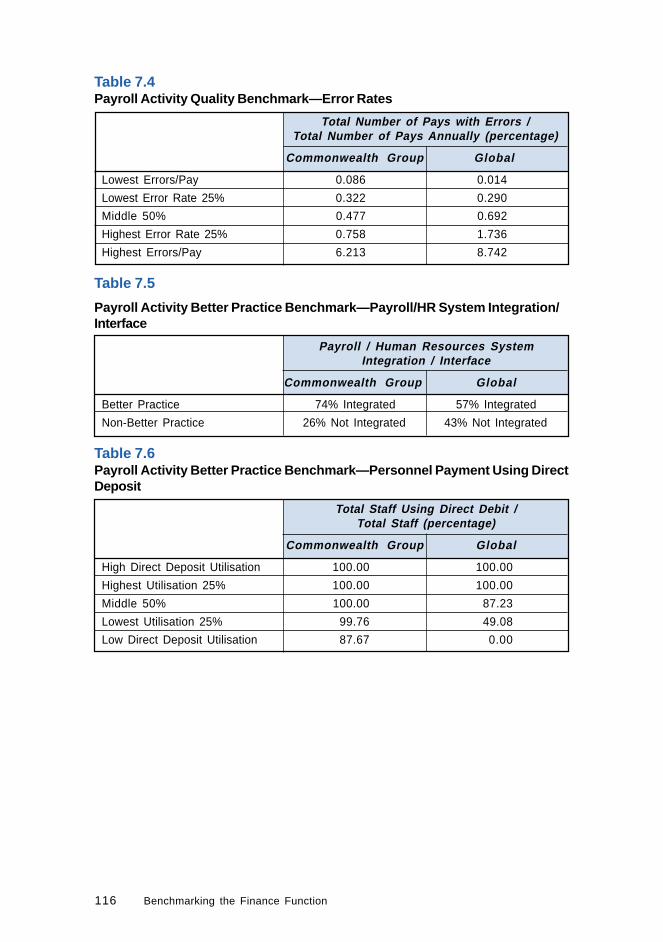

8. Payroll Activity Benchmarks 71Introduction 71Cost Dimension Benchmarks 72Efficiency Dimension Benchmark 73Quality Dimension Benchmark 74Conclusion 77Better Practice Observations 77

9. Travel Activity Benchmarks 80Introduction 80Cost Dimension Benchmarks 81Efficiency Dimension Benchmark 83Better Practice Benchmark 84Conclusion 85Better Practice Observations 86

10. Billing Activity Benchmarks 88Introduction 88Cost Dimension Benchmarks 88Quality Dimension Benchmarks 90Conclusion 93Better Practice Observations 93

11. Tax Activity Benchmarks 95Introduction 95Cost Dimension Benchmark 95Conclusion 96Better Practice Observations 97

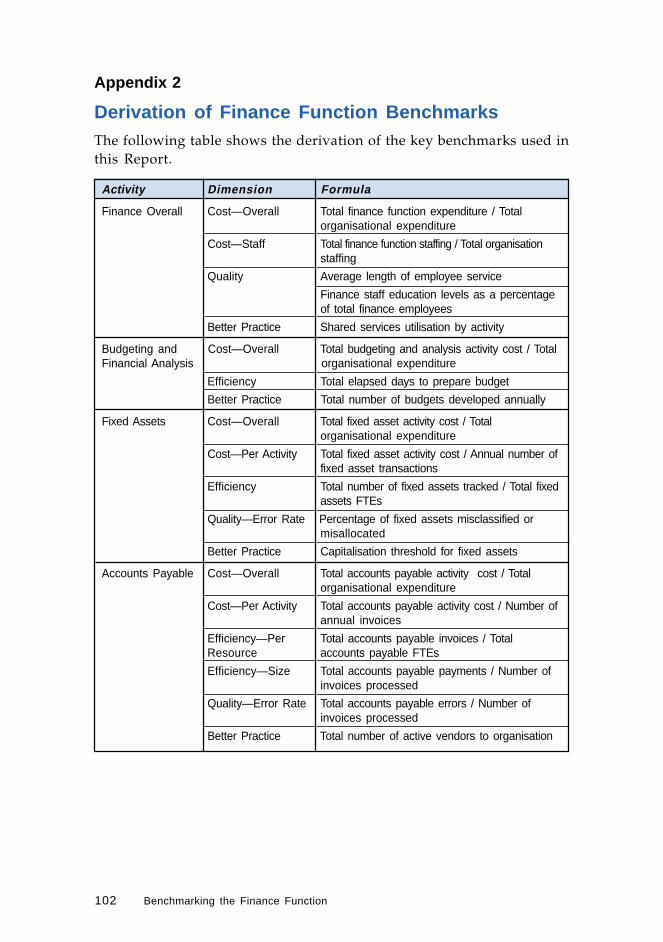

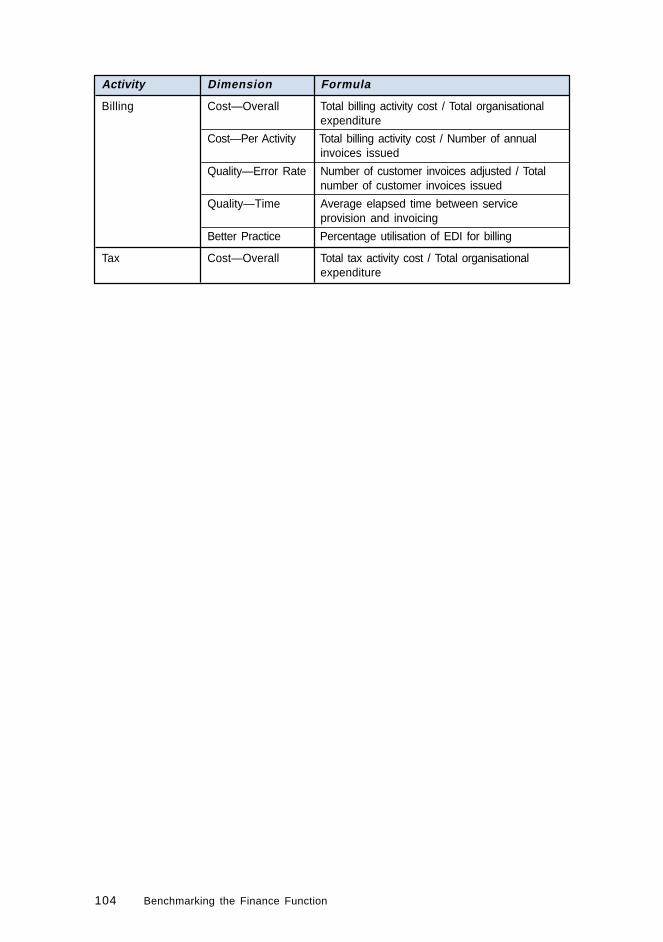

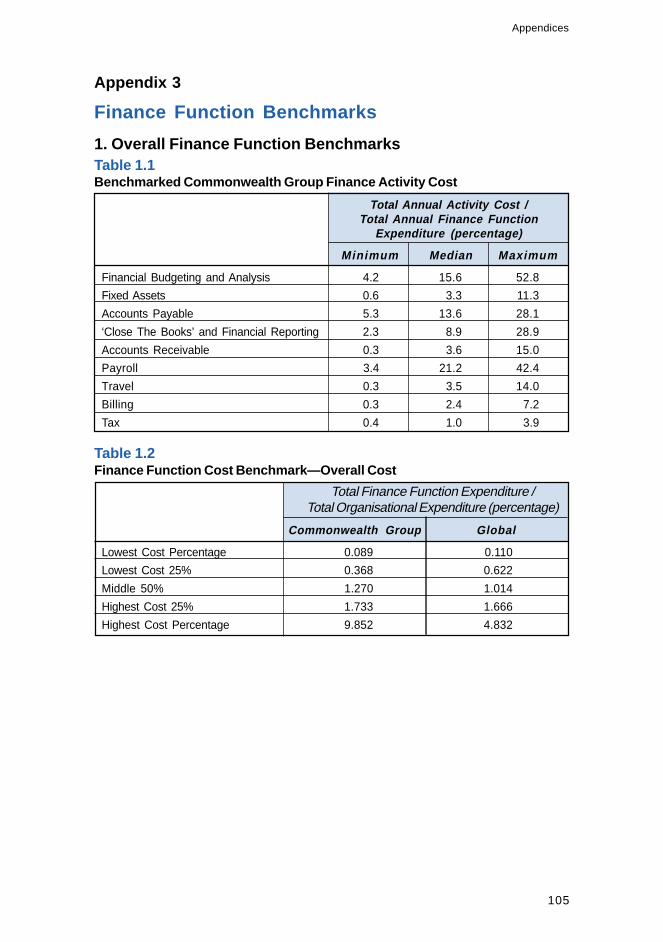

AppendicesAppendix 1: Benchmark Demographic Profiles 101Appendix 2: Derivation of Finance Function Benchmarks 102Appendix 3: Finance Function Benchmarks 105

1. Overall Finance Function Benchmarks 1052. Financial Budgeting and Analysis 1073. Fixed Assets Activity Benchmarks 1084. Accounts Payable Activity Benchmarks 1105. ‘Close the Books’ and Financial Reporting 1126. Accounts Receivable Activity Benchmarks 1137. Payroll Activity Benchmarks 1158. Travel Activity Benchmarks 1179. Billing Activity Benchmarks 11810. Tax Activity Benchmarks 120

Appendix 4: Previous Audit Coverage 121

Index 124Series Titles 125Better Practice Guides 127

7

Summary, Key Findingsand Recommendations

8 Benchmarking the Finance Function

9

Summary

1. This Report on the public sector finance function is part of a seriesof benchmarking studies being undertaken by the Australian NationalAudit Office (ANAO) into common business processes. The ANAO hasrecently published a report detailing a benchmarking study of the internalaudit function.1 and is currently undertaking a study relating to the humanresource management function. The primary purpose of these studies isto obtain and report quantitative and qualitative data on aspects ofperformance of the function or business process. The benchmark studiesare undertaken as part of the ANAO’s Information Support Services whichare also an important element of providing assurance to stakeholders.

2. The objective of the finance function benchmarking study was toobtain, and report on over time, quantitative and qualitative data relatingto finance function activities as they operate in Commonwealthorganisations.2 This Report provides the results from the first year ofthe benchmarking study. This data can be utilised by all public sectororganisations to develop appropriate measures of performance for theirown finance function as part of continuous improvement programs orbusiness re-engineering.

3. While the emphasis of the ANAO benchmarking studies is to makeavailable public sector benchmarks for use as an organisationalimprovement tool, they also provide an opportunity for an across-the-board assessment of the Commonwealth public sector for particularfunctions. This assessment is based on a comparison of responses fromparticipating Commonwealth organisations (the Commonwealth Group)and data from an international group (the Global Group).

4. Commonwealth organisations can compare their own performanceagainst the benchmarks and use the information to detect and diagnoseareas of concern in business processes in terms of the dimensions of cost,efficiency and quality and highlight opportunities for improvement.

1 Australian National Audit Office, Audit Report No.14 of 2000–01, Benchmarking the Internal AuditFunction, October 2000.

2 In this Report organisations refers to agencies subject to the Financial Management andAccountability (FMA) Act 1997 and statutory authorities subject to the Commonwealth Authoritiesand Companies (CAC) Act 1997.

10 Benchmarking the Finance Function

5. The finance function benchmarking study examines aggregatedbenchmarking measures of cost, efficiency, quality and better practicereported by nineteen Commonwealth organisations for 1998–99 andprovides aggregated benchmarking results. The Commonwealth publicsector organisations participating in the benchmark study have beenprovided with a comprehensive report comparing their results with thoseof other organisations in the Commonwealth public sector group andwith the global population.

6. Ten of the Commonwealth Group organisations are covered bythe Financial Management and Accountability Act 1997 (FMA) and nine bythe Commonwealth Authorities and Companies Act 1997 (CAC).

7. The Global Group used as a comparator throughout this Reportis from the Arthur Andersen benchmarking database and comprises morethan 500 organisations. The largest proportion of these organisations(45 per cent) is in the United States of America and over 95 per cent arein the private sector. Further information on the Commonwealth andGlobal benchmarking Groups is at Appendix 1.

8. The ANAO study collected benchmarking data on the followingactivities:

• overall cost of the finance function (chapter 2);

• financial budgeting and analysis (chapter 3);

• fixed assets (chapter 4);

• accounts payable (chapter 5);

• ‘close the books’ and financial reporting (chapter 6);

• accounts receivable (chapter 7);

• payroll (chapter 8);

• travel (chapter 9);

• billing (chapter 10); and

• tax (chapter 11)

9. The results are limited in scope to the extent that data in thestudy has been derived from self-assessments. The results do not takeaccount of, or distinguish between, the different environments in whichfinance functions operate, such as the public and private sectors. As aresult, the benchmark study can only provide a broad indication ofdifferences in performance between the two Groups.

11

10. Although the report makes a number of comparisons betweenthe two Groups, it is important to note that results against each of thebenchmarks should not be assessed in isolation as this rarely providesinsight into how different outcomes have been achieved. Discoveringthe specific practices responsible for high performance, and adapting andapplying them within an organisation as a basis for process improvementis not the role of this study. Thus the Report does not provide reasonsfor differences in performance, however it does provide guidance onsome of the factors that organisations may wish to consider whenevaluating their results.

Summary

12 Benchmarking the Finance Function

Key Findings andRecommendation

11. This finance function benchmarking study indicates thatorganisations in the Commonwealth Group perform equal to or betterthan the Global Group at the median in relation to:

• quality in terms of lower activity error rates (accounts payable,accounts receivable and payroll);

• level of staffing in the finance function;

• making greater use of shared services;

• number of actual budgets;

• number of days between invoicing and receipt of payment;

• processing cost per pay, higher utilisation of direct deposit andintegrated/interfaced payroll/human resources systems;

• making greater use of reimbursement through payroll and directdeposit for travel payments; and

• some elements of activity cost (‘close the books’, accounts receivable,travel, billing and tax). It should be noted that the CommonwealthGroup perform these activities to a lesser extent than the Global Group.

12. The benchmarking study also indicates that opportunities mayexist in some organisations for progress to be made in areas where theCommonwealth Group reported less favourable results overall than theGlobal Group. The main areas included are those where, at the median,there were:

• higher costs for the finance function overall;

• higher activity costs overall (budgeting and analysis, fixed assets,accounts payable, payroll, travel, and tax);

• higher activity cost per transaction (fixed assets, accounts payable,travel and billing);

• lower efficiency (budgeting and analysis, fixed assets, accountspayable, accounts receivable, payroll and travel);

• shorter lengths of employee service and lower levels of qualificationsfor finance function staff; and

• higher error rates (‘close the books’ and billing).

13

13. As previously mentioned this benchmarking study involvesmaking various comparisons between quantitative and qualititative dataderived from the Commonwealth and Global Groups. The Report doesnot attempt to provide reasons for the results. The Report does howeverprovide guidance as to the type of factors which organisations couldconsider when evaluating their results.

14. The nature of this benchmarking study precludes detailedrecommendations-indeed, as discussed previously, that is not its primarypurpose. However, one broad recommendation, directed to allCommonwealth organisations, can be made.

15. The ANAO recommends that organisations compare their performanceagainst the benchmarks in this Report (and any other relevant benchmarks) inorder to assist in the identification and diagnosis of areas where improvementsmay be made in their business processes.

Key Findings

14 Benchmarking the Finance Function

15

Benchmark Study Findingsand Conclusions

16 Benchmarking the Finance Function

17

1 Introduction

Background to the benchmarking study1.1 The adoption of accrual budgeting and accounting as part of theon-going government reforms affecting the Commonwealth public sectorhas necessitated, amongst other things, the introduction of newinformation systems and enhanced management reporting by many publicsector organisations to meet the demands for better and more timelyinformation for decision making. Various reports by the ANAO havedrawn attention to the importance of having in place effective controlstructures to underpin the new budgeting and accounting framework3.

Introduction1.2 The ANAO has undertaken a benchmarking study in relation tothe finance function of public sector organisations. The study is basedon data from the 1998–99 financial year, the year prior to the introductionof accrual budgeting. The results can then provide a baseline fororganisations to assess their performance in the future. While recognisingaccrual budgeting will introduce some additional complexity toorganisational budgeting, it would be reasonable to expect the currentanalysis to be improved over time as organisations streamline and improvethe integrity of their processes.

1.3 This Report examines measures of cost, efficiency, quality andbetter practice across a range of activities undertaken as part of the financefunction by Commonwealth government organisations. It is part of aseries of benchmarking studies being undertaken by the ANAO intocommon business processes. The primary purpose of these studies is toobtain and report quantitative and qualitative data on aspects ofperformance of the function or business process.

3 Australian National Audit Office Audit Report No.52 of 1999–2000 Control Structures as Part of theAudits of Financial Statements of Major Commonwealth Agencies for the Period Ended30 June 2000 and Audit Report No.21 of 1999–2000 Audits of the Financial Statements ofCommonwealth Government Agencies for the Period Ended 30 June 1999.

18 Benchmarking the Finance Function

1.4 Comparison against benchmarks alone however, rarely providesinsight into how superior outcomes have been achieved. Discoveringthe specific practices responsible for high performance, and adapting andapplying them within an organisation provides as a basis for processimprovement is not the role of this study. Thus the Report does notprovide reasons for differences in performance. The Report doeshowever provide guidance as to some of the factors that organisationsmay wish to consider when evaluating their individual results. Whereappropriate better practice observations, drawn from ANAO betterpractice guides, the Arthur Andersen global benchmarking database andfrom Reengineering Australia, are made throughout this Report to assistorganisations in identifying opportunities for improvements.

1.5 Research from the private sector indicates that the operation of afinance function is regarded as expensive with significant scope forperformance improvement. Research further indicates that the financefunction in the private sector has been transformed over recent years,partly as a result of increasing cost pressures, but also in response to agrowing demand from the users of financial information for more value-added information to assist in their decision-making.

1.6 As illustrated in the following diagram, better practiceorganisations are re-focussing their financial management function froma traditional base, where processing of transactions predominated,towards a lower cost, business management role.

Trends in financial management

DecisionSupport

Control

Reporting

TransactionProcessing

DecisionSupport

Control

Reporting

Transaction Processing

19

Study objective1.7 The objective of the benchmarking study was to obtain, over time,quantitative and qualitative benchmarks for the finance function as itoperates in Commonwealth organisations.

1.8 While the emphasis of the ANAO benchmarking studies is to makeavailable public sector benchmarks for use as an organisationalimprovement tool, they also provide an opportunity for an across-the-board assessment of the Commonwealth public sector for particularfunctions. This assessment is based on a comparison of responses fromparticipating Commonwealth organisations and data from an internationalgroup.

Scope of the study1.9 This Report includes aggregated benchmarking results fromnineteen Commonwealth organisations (the ‘Commonwealth Group’) for1998–99. Ten of the Commonwealth Group organisations are covered bythe Financial Management and Accountability Act 1997 (FMA) and nine bythe Commonwealth Authorities and Companies Act 1997 (CAC).

1.10 Information relating to organisational expenditure, financefunction expenditure and the number of staff in the finance function areprovided for the Commonwealth Group below.

Total organisation Number of Finance function Number ofexpenditure organisations expenditure organisations

< $100 million 5 < $1 million 2

$100—$500 million 5 $1—$5 million 13

> $500 million 9 > $5 million 4

TOTAL 19 TOTAL 19

Staff in the finance Number ofsection organisations

< 10 1

11–25 9

26–50 4

>50 5

TOTAL 19

1.11 The total expenditure of the Commonwealth Group was$11.8 billion in 1998–99. The Commonwealth Group organisations allocatebetween 0.09 and 9.85 per cent of their total expenditure to the financefunction. Other activities performed by the finance area that were notcovered by the diagnostic instrument used to collect the data include

Introduction

20 Benchmarking the Finance Function

strategic management, financial policy development, treasury, cashmanagement, devolved banking and finance help desk.

1.12 In order to provide the public sector organisations withbenchmarking services, the ANAO formed a strategic alliance with ArthurAndersen enabling the ANAO to access diagnostic questionnaires, globalbenchmarks and information on better practices. Data processing andanalysis was conducted jointly by the ANAO, Reengineering Australiaand Arthur Andersen.

1.13 The Global Group used as a comparator throughout this Reportis from the Arthur Andersen benchmarking database and comprises morethan 500 organisations. The largest proportion of these organisations(45 per cent) are in the U.S. and over 95 per cent are in the private sector.Further information on the Commonwealth and Global benchmarkingGroups is at Appendix 1.

1.14 The observations in this Report are based on the informationprovided by the Commonwealth Group in response to a questionnaire.Consequently, the standard of evidence relied on for the study must beconsidered persuasive, rather than conclusive, based as it is on self-assessment by organisations. These self-assessments were subject toquality assurance checks by the ANAO, but have not been audited by theANAO. Thus the quality assurance processes undertaken by the ANAOon the data are not of themselves sufficient to guarantee its integrity.

1.15 In most organisations data was obtained for the ‘central’ financearea only. Moreover, the benchmark information cannot take account of,or distinguish between, the different environments in which financefunctions operate, for example as between the public and private sectors.As a result, the benchmark study can only provide an insight intodifferences in performance and may raise further questions forinvestigation.

Evaluation criteria1.16 The diagnostic questionnaires completed by each participatingorganisation capture a wide variety of information from which the ANAOdetermined a range of benchmarks across cost, efficiency and qualitydimensions. These benchmarks—listed at Appendix 2—have been usedas the evaluation criteria for this Report. In terms of the structure of thisReport, the benchmarks have been categorised by the finance functionoverall and then each particular finance activity (e.g. financial budgetingand analysis, fixed assets). Detailed results for each benchmark are atAppendix 3.

21

Beyond Bean Counting 20001.17 In August 2000, the Public Sector Centre of Excellence of CPAAustralia published Beyond Bean Counting 2000 a benchmark of effectivefinancial management in the Australian Public Sector4. The intention of thisreport was to obtain the perspective of Chief Executive Officers (CEO)and the Chief Finance Officers (CFO) on financial management progressin their organisations since the survey conducted as part of the firstBeyond Bean Counting report commissioned by the ManagementAdvisory Board in 19975. Some care needs to be taken in comparing theresults of the Beyond Bean Counting 2000 survey with the ANAObenchmark study because of the type of organisations that participatedin it. The Beyond Bean Counting 2000 survey included ACT, State andlocal government organisations and a private sector company and covered12 Commonwealth organisations and indicates:

• a widespread acceptance of the value of accrual information by CEOs;

• CEOs and CFOs are taking a more dominant role and accountabilityfor financial results;

• continuing strong demands for quality accounting and financeprofessionals;

• the emergence of revenue and profit/loss targets in the annual budgetin place of a focus only on expenditure;

• a significant change in the budgetary control function;

• the widespread use of integrated financial management systemsassisting the devolution of financial management authority to linemanagers; and

• a significant shift in the main focus of internal managementaccountability from individual budget line items (e.g. travel, salaries,etc) towards a focus on financial results (operating result, key ratios).

Introduction

4 Beyond Bean Counting 2000 A Benchmark of Effective Financial Management in the AustralianPublic Sector, Public Sector Centre of Excellence, CPA Australia, August 2000.

5 Beyond Bean Counting Effective Financial Management in the APS—1998 & Beyond, ManagementAdvisory Board, December 1997.

22 Benchmarking the Finance Function

1.18 The perspective of the surveyed CEOs and CFOs provides animportant insight into the current strategic and leadership trends inAustralian Public Sector (APS) financial management. The ANAObenchmark study provides more detailed information on benchmarksfor the cost, efficiency, quality and better practice of the individualactivities of the finance function. Taken together these reports providepublic sector managers with a wealth of information directed towardsimproving financial management in the APS and to improved financialdecision making. Where appropriate, reference has been made to theBeyond Bean Counting 2000 report in this benchmark study.

Previous audit coverage1.19 The ANAO has undertaken significant research into how betterpractice organisations, in both the private and public sectors, approachthe collection, analysis, production and use of financial information. Asummary of relevant previous audit coverage and better practice guidesis provided in Appendix 4.

1.20 This audit was conducted in conformance with ANAO auditingstandards and cost approximately $340 000.

23

2. Overall Finance FunctionBenchmark

Introduction2.1 The primary business objective of the finance function is to provideaccounting services and financial information in a low cost, accurate andtimely manner.

2.2 The finance function includes the following activities:

• financial budgeting and analysis;

• fixed assets;

• accounts payable;

• ‘close the books’ and financial reporting;

• accounts receivable;

• payroll;

• travel;

• billing; and

• tax.

2.3 This Report provides details of benchmarks relating to cost,efficiency, quality and better practice associated with the finance functionin accordance with the activity categories listed above.

2.4 Figure 1.1 shows the range of costs, and the median cost, spentby the Commonwealth Group on each finance activity. As shown inFigure 1.1, payroll and budgeting account for the majority of the financefunction cost in the Commonwealth Group with individual organisationpercentages for each process varying considerably.

24 Benchmarking the Finance Function

Quality

Figure 2.1Benchmarked Commonwealth Group Finance Activity Cost

60%

Budge

ting

Per

cent

age

of T

otal

Ann

ual

Fin

ance

Fun

ctio

n E

xpen

ditu

re

Fixed

Asset

s

Accou

nts

Payab

le

Close

the

Books

Accou

nts

Receiv

able

Payro

ll

Trave

l

Billing Tax

50%

40%

30%

20%

10%

0%

15.6%

3.3%

13.6%8.9%

3.6%

21.2%

3.5% 2.4% 1.0%

Formula Used: Total Annual Activity Cost/ Total Annual Finance Function Expenditure

2.5 On average, finance staff in the Commonwealth Group accountfor some 3.5 per cent of total staffing, with individual organisation’sstaffing ranging between 6.3 and 165 full time equivalents (FTEs).

2.6 The overall finance function benchmarks provide a broadindication of relative cost by measuring the proportion of organisationalexpenditure required to pay finance and accounting related costs6 andfinance function staffing as a proportion of total staffing. Benchmarksrelating to the average length of employee service in the finance functionwithin each organisation and finance employee education levels have beenused to provide a broad indication of quality of information. The financefunction benchmarks selected by the ANAO are summarised in Table 2.1.

Table 2.1 Overall Finance Function Benchmarks

Dimension Formula

Cost—Overall Total finance function expenditure/Total organisational expenditure

Cost—Staffing Total finance function staffing/Total organisational staffing

Efficiency No Benchmark7

Average length of employee service in the finance function of theorganisation

Finance staff education levels as a percentage of total financeemployees

Better practice Shared services utilisation by activity

6 Total costs include direct labour, contracted labour, operating expenses (excluding rent,depreciation, or allocated overhead expenses), service bureau fees, and data processing costsrelated to support (direct labour, operating expenses, and vendor software licensing andmaintenance costs).

7 No efficiency benchmarks are available for the overall finance function. However, the efficiencydimension is considered for most finance activities in subsequent chapters of this Report.

25

Cost Dimension Benchmarks2.7 The ANAO used two measures of cost of the total finance function.The first captures cost at a global level and expresses total finance functioncost as a percentage of total organisational expenditure8. The second costmeasure captures the total finance function staffing and expresses it as apercentage of the total organisational staffing.

2.8 Figure 2.2 shows that the Commonwealth Group allocates between0.09 and 9.85 per cent of total expenditure to the finance functioncompared with 0.11 and 4.83 per cent for the Global Group. The medianallocation for the Commonwealth Group is 25 per cent higher than thatof the Global Group.

Figure 2.2Finance Function Cost Benchmark—Overall Cost

Overall Finance Function Benchmark

Formula Used: Total Finance Function Expenditure / Total Organisational Expenditure

2.9 It should be noted that nine of the Commonwealth organisationshave some level of administered expenses included when determiningtotal expenditure. Therefore, by their nature, these organisations wouldspend a lower percentage of their total (departmental plus administered)expenditure on the finance function relative to the other Commonwealthorganisations and the Global Group who do not have an equivalent non-entity expenditure9.

2.10 Six of the nineteen Commonwealth Group reported overall costbenchmarks which place them within the Global Group’s least costquartile. Six of the remaining Commonwealth Group reportedbenchmarks that placed them within the Global Group’s highest costquartile.

Commonwealth Government

Per

cent

age

of T

otal

O

rgan

isat

ion

Exp

endi

ture

Global

Highest Cost 25%

Middle 50%

Lowest Cost 25%

10%

8%

6%

4%

2%

0%

Median1.270%

Median1.014%

8 Total organisational expenditure for this benchmarking study is the operating expenditure of theorganisation, including (where applicable) any administered budgets or expenditure.

9 Departmental expenditure is controlled by the organisation, whereas administered expenditure iscontrolled by the Government and managed or oversighted by the organisation on theGovernment’s behalf.

26 Benchmarking the Finance Function

2.11 Two of the Commonwealth Group exceeded the Global Grouphighest overall cost benchmark. These were two of the smallestorganisations within the Commonwealth Group, suggesting that theabsence of economies of scale could be an issue in this respect.

2.12 An evaluation of cost benchmarks is provided in the followingchapters of this Report for each of the activities that constitute part ofthe finance function. An estimate of potential expenditure reductions ismade in these chapters on the basis that those organisations in theCommonwealth Group with costs above the Group median are movedto the median level. The potential reductions total some $10.6 million,or 20.7 per cent of current expenditure on the benchmarked financeactivities.10

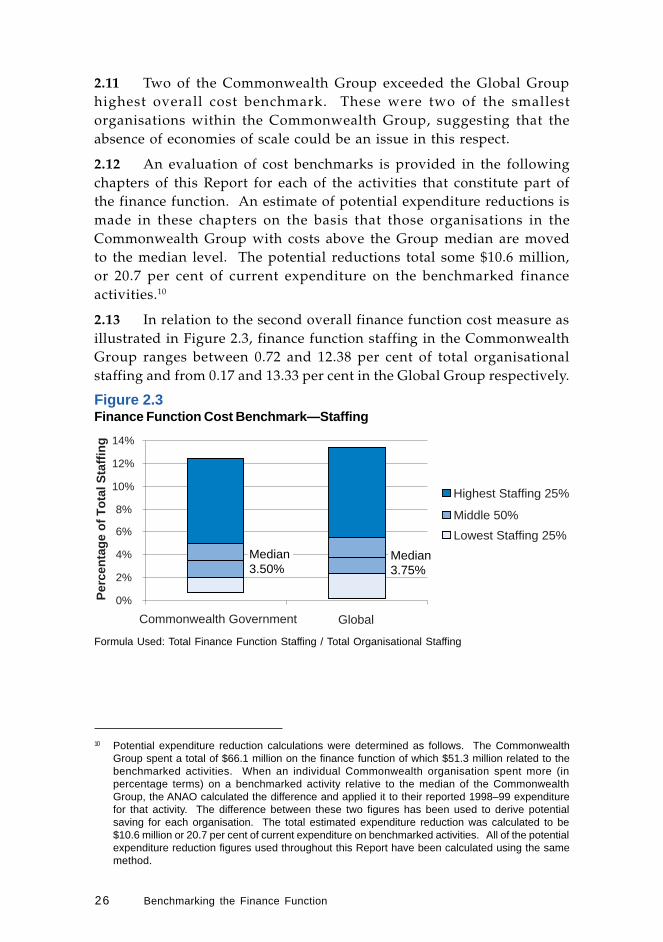

2.13 In relation to the second overall finance function cost measure asillustrated in Figure 2.3, finance function staffing in the CommonwealthGroup ranges between 0.72 and 12.38 per cent of total organisationalstaffing and from 0.17 and 13.33 per cent in the Global Group respectively.

Figure 2.3Finance Function Cost Benchmark—Staffing

Formula Used: Total Finance Function Staffing / Total Organisational Staffing

0%

2%

4%

6%

8%

10%

12%

14%

Commonwealth Government

Per

cent

age

of T

otal

Sta

ffing

Global

Highest Staffing 25%

Lowest Staffing 25%

Middle 50%

Median3.50%

Median3.75%

10 Potential expenditure reduction calculations were determined as follows. The CommonwealthGroup spent a total of $66.1 million on the finance function of which $51.3 million related to thebenchmarked activities. When an individual Commonwealth organisation spent more (inpercentage terms) on a benchmarked activity relative to the median of the CommonwealthGroup, the ANAO calculated the difference and applied it to their reported 1998–99 expenditurefor that activity. The difference between these two figures has been used to derive potentialsaving for each organisation. The total estimated expenditure reduction was calculated to be$10.6 million or 20.7 per cent of current expenditure on benchmarked activities. All of the potentialexpenditure reduction figures used throughout this Report have been calculated using the samemethod.

27

2.14 Seven of the Commonwealth Group reported staffing benchmarksplacing them in the lowest staff quartile of the Global Group with onlytwo reporting benchmarks placing them in the highest staffing quartileof the Global Group. The ANAO noted that the Commonwealth Grouporganisation reporting the lowest percentage of finance staff was alsothe largest of the organisations in the Commonwealth Group, suggestingpossible economy of scale benefits within the staffing of the function.

2.15 The results indicate that both the median and overall costbenchmark is higher in the Commonwealth Group than the Global Groupwhile the median and overall staffing is higher in the Global Group. Insubsequent chapters of this Report, the benchmarking analysis at theactivity level provides a more detailed view of relative performance.

Quality Dimension Benchmarks2.16 The first quality benchmark of the finance function overallmeasures the length of the employee service in the organisation’s financefunction as an indicator of stability and skill retention. As shown inFigure 2.4, the Global Group exhibits longer length of service, with themedian at eight years compared with five years for the CommonwealthGroup.

Figure 2.4Finance Function Quality Benchmark—Staff Retention

Overall Finance Function Benchmark

0

Commonwealth Government

Ave

rage

Len

ngth

of S

ervi

ce (

Yea

rs)

Global

Longest Service 25%

Middle 50%

Shortest Service 25%

5

10

15

20

25

Median8 yearsMedian

5 years

Formula Used: Average Length of Employee Service

2.17 This benchmark does not take into account the length of timestaff have spent in the finance areas of other organisations. Althoughrelevant to both groups, this could particularly effect the CommonwealthGroup where until recently many organisations had the same financemanagement systems and the same financial directions and regulations.

28 Benchmarking the Finance Function

2.18 The shorter average length of service for the CommonwealthGroup in comparison with the Global Group may manifest itself in someof the activity benchmarks in the following chapters.

2.19 The second overall benchmark which can provide a broadindication of quality relating to the finance function measures theeducational levels of finance employees—which can be a determinant ofthe roles these employees will fulfil within the organisation. Figure 2.5reveals that both staff and management in the Commonwealth Grouphave fewer qualifications than those in the Global Group. Seventy sixper cent of finance function staff and 35 per cent of finance functionmanagement within the Commonwealth Group do not have any of thespecified qualifications.

Figure 2.5Finance Function Quality Benchmark—Staff Qualifications

Formula Used: Finance Staff Education as a Percentage of Total Finance Staff

2.20 The effect of having different levels of staff with relevantqualifications within the organisations with the Commonwealth andGlobal Groups cannot be ascertained from these results. The ANAOnotes, however, that finance education levels and years of service shouldbe viewed as only two factors shaping the overall finance skill set. Otherfactors—such as types of education not considered by the qualificationsbenchmarking measure, employee training, and related workexperience—are relevant when evaluating the overall skill set of thefinance workforce.

Accounting Degree

CPA

MBA

CPA & MBA

None of Above

Percentage of Staff

0% 10% 20% 30% 40% 70%50% 60% 80%

Mgt - Commonwealth Government

Staff - Commonwealth Government

Mgt - Global

Staff - Global

29

2.21 The CPA Australia Report Beyond Bean Counting 2000, whichsurveyed some 12 Commonwealth organisations, reported that the numberof professionally qualified staff had increased over the past two years.The survey indicated that there has been a focus by the public sector torecruit and promote professionally qualified staff to financial managementpositions. Eighty two per cent of organisations surveyed have aprofessionally qualified accountant as their senior finance manager and95 per cent of CEOs rated their CFO’s skills as very good or excellent.Although there has been significant effort in training staff to operate inthe new environment, the CPA Australia survey results suggest that thistraining is not yet effective with significantly lower levels of satisfactionwith line managers’ financial management skills than in 1997.11

2.22 This suggests that, as mentioned above, that finance educationlevels are only one factor contributing to the overall skills and quality ofstaff involved in the finance function.

Better Practice Benchmark2.23 A benchmark used as an indicator of the adoption of generallyrecognised better practice is the utilisation of shared services within theorganisation. Shared services is a term that describes the consolidation,standardisation and reengineering of a support process into one or moreunits that serve the entire organisation. Better practice organisationsimplement a shared services strategy to:

• standardise work policies;

• employ and consolidate common systems;

• take advantage of economies of scale; and

• eliminate duplication of efforts

2.24 Figure 2.6 shows that the Commonwealth Group has aconsiderably higher shared services focus than the Global Group. Thismay be a consequence of the subsidiary company structure seen in manyprivate sector entities.

Overall Finance Function Benchmark

11 Op. cit, Beyond Bean Counting 2000 A Benchmark for Effective Financial Management in theAustralian Public Sector, p. 20.

30 Benchmarking the Finance Function

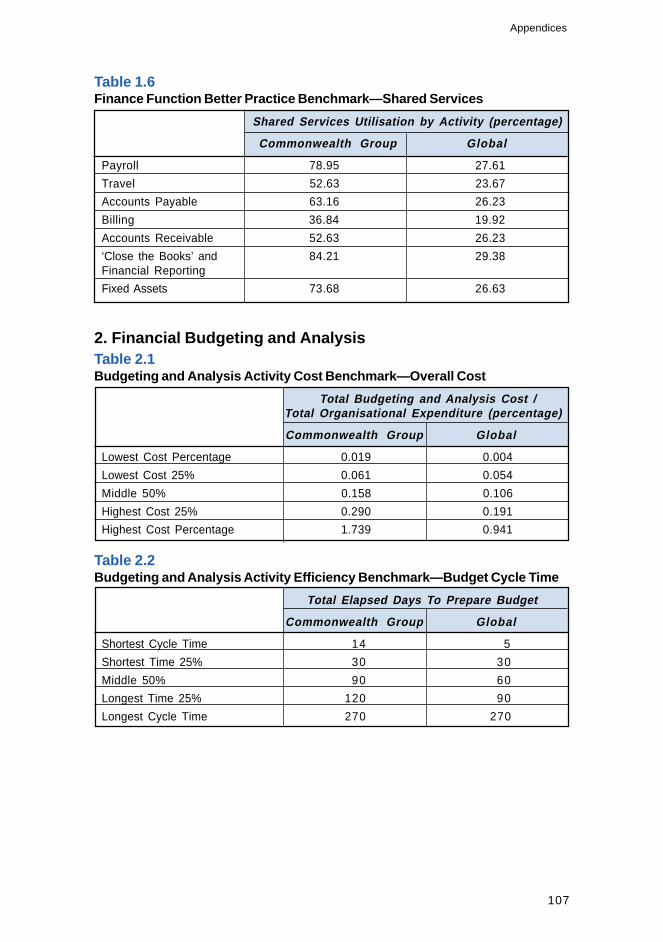

Figure 2.6Finance Function Efficiency Benchmark—Shared Services

Conclusion2.25 The benchmarking results indicate that the Commonwealthorganisations’ finance functions have a higher overall cost and loweroverall staffing than the Global Group. In addition, CommonwealthGroup staff exhibit shorter lengths of service in the finance function andhave fewer qualifications than their global counterparts. TheCommonwealth Group does however make greater use of shared serviceswhich is considered better practice.

Shared Services Utilisation

Commonwealth Government Global

Fixed Assets

Close the Books & Financial Reporting

Accounts Receivable

Billing

Payroll

Accounts Payable

Travel & Entertainment

0% 10% 20% 30% 40% 60% 70% 80% 90%50%

27.61%78.95%

23.67%52.63%

26.23%

19.92%36.84%

63.16%

26.23%52.63%

29.38%84.21%

26.63%73.68%

31

3. Financial Budgeting andAnalysis Activity Benchmarks

Introduction3.1 A budget is a systematic method of allocating financial, physicaland human resources in order to monitor progress toward organisationalgoals, help control spending and predict cash flow12. A primary businessobjective of financial budgeting and analysis is to effectively allocateresources among various activities and monitor the use of those resources.

3.2 Financial budgeting and analysis is, with payroll, one of the mostsignificant of the Commonwealth Group financial activities. It accountsfor a median 15.6 per cent of the total finance operating budget in theCommonwealth Group. Financial budgeting and analysis staff in theCommonwealth Group account for a median 12.2 per cent of the totalfinance function staffing, ranging between 0.65 and 27.32 FTEs inindividual organisations.

3.3 The cost, efficiency and better practice benchmarks selected bythe ANAO for the financial budgeting and analysis activity are set out inTable 3.1.

Table 3.1Budgeting and Analysis Activity Benchmarks

Dimension Formula

Cost—Overall Total budgeting and analysis activity cost / Total organisationalexpenditure

Efficiency Total elapsed days to prepare budget

Better Practice Total number of budgets developed annually

Cost Dimension Benchmark3.4 The cost benchmark captures the cost of budgeting and analysisat a global level and expresses this as a percentage of total organisationalexpenditure.

12 The public sector is required to prepare budget documents for the Parliament, including forAdditional Estimates as well as for internal management purposes. In contrast the private sectorprepares budgets for internal purposes only.

32 Benchmarking the Finance Function

3.5 As shown in Figure 3.1, the Commonwealth Group allocatesbetween 0.019 and 1.739 per cent of total organisational expenditure tofinancial budgeting and analysis activity, with the lowest cost quartileranging between 0.019 and 0.061 per cent. In comparison, the GlobalGroup allocates between 0.004 and 0.941 per cent of total organisationexpenditure. However, the highest result in Commonwealth Group rangeis significantly greater than the rest of the Commonwealth Group. Ifthis result is removed, the Commonwealth Group range becomes 0.019to 0.502 per cent, which is on par with the Global Group.

Figure 3.1Budgeting and Analysis Activity Cost Benchmark—Overall Cost

Formula Used: Total Budgeting and Analysis Activity Cost / Total Organisational Expenditure

3.6 At the median the Commonwealth Group spends some 50 percent more on budgeting and analysis than the Global Group. Therelatively high cost of budgeting and analysis in the CommonwealthGroup may be a reflection of a more complex budgeting process whichincludes, for example:

• involvement of other agencies and Ministers in the budgeting process;and

• high levels of transparency required by government and parliamentaryaccountability frameworks.

3.7 However, the benchmark data suggests a potential forimprovement in cost-efficiency. If the budgeting and analysis costs ofthe finance function activity of those organisations in the CommonwealthGroup above the Group median were reduced only to the median level,then expenditure reductions of some $3.4 million (29 per cent) wouldresult. The introduction of accrual budgeting with effect from 1 July 1999,the year after the benchmarking data was collected, may add further toCommonwealth budgeting costs.

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

Per

cent

age

of T

otal

Org

anis

atio

n E

xpen

ditu

re

Commonwealth Government Global

Higest Cost 25%

Middle 50%

Lowest Cost 25%

Median0.106%

Median0.158%

33

3.8 The difference in performance against cost benchmarks may be areflection of the significant nature of the financial budgeting and analysisactivity and the high levels of transparency required as part of the budgetprocess and accountability framework within government.

Efficiency Dimension Benchmark3.9 The ANAO selected the efficiency measure of the cycle time toprepare the budget. This measure illustrates the average elapsed time(in calendar days) to prepare the annual budget, from the release of thepreparation materials to the final budget approval. The benchmarkingresults, showing a median budget cycle time of 90 days for theCommonwealth Group, compared with 60 days for the Global Group,are set out in Figure 3.2.

Figure 3.2Budgeting and Analysis Activity Efficiency Benchmark—Budget Cycle Time

Financial Budgeting and Analysis Activity Benchmarks

Formula Used: Total Elapsed Days to Prepare Budget

3.10 With cycle times ranging between 14 and 270 days, theCommonwealth Group takes longer than the Global Group to preparebudgets—the cycle time is 50 per cent greater at the median. The ANAOnotes that public sector accountability arrangements may result in morebudgeting review, refinement and approval processes than in thepredominantly private sector Global Group, giving rise to the potentialfor longer cycle times.

3.11 The ASCPA survey found that the demands of the budgetingprocess are increasingly being seen as a drain on an organisation’sresources and a constraint on its ability to react quickly to changingcircumstances. There is a growing trend among private sectororganisations towards reducing the impact of the budget on corporateactivities, while in government the budget is becoming more

Ela

psed

Day

s T

o P

repa

re B

udge

t

Longest Cycle Time 25%

Middle 50%

Shortest Cycle Time 25%

CommonwealthGovernment

Global

300

250

200

150

100

50

0

Median90 Days Median

60 Days

34 Benchmarking the Finance Function

comprehensive in its coverage. The survey also found that 26 per cent oforganisations indicated that they spend five months or more on externalbudgeting, while a further 26 per cent spend three to four months13. Thedemand on resources is further increased as a result of many organisationsreporting budget information on both a cash and accrual basis14.

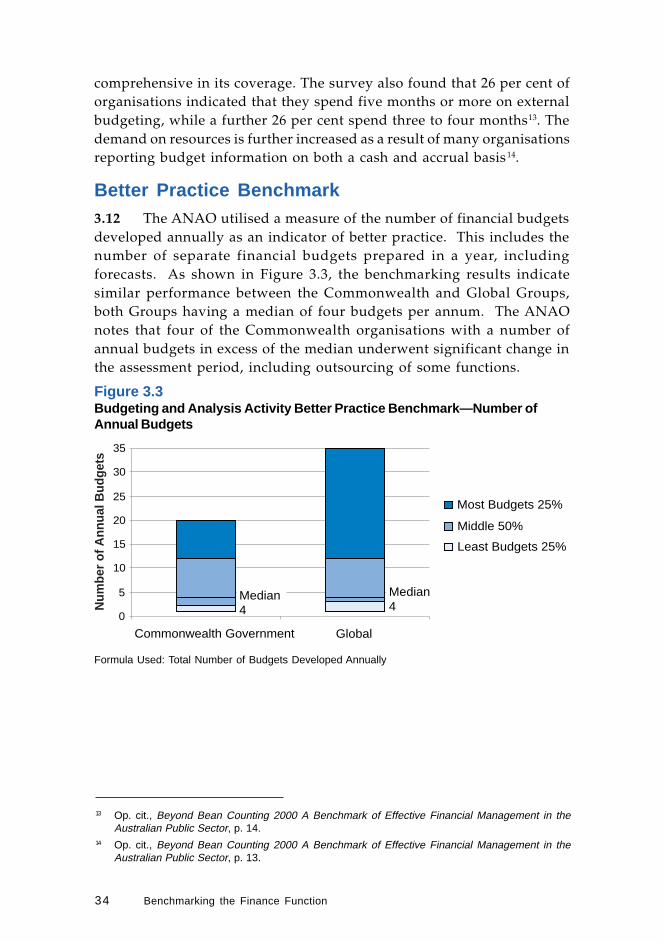

Better Practice Benchmark3.12 The ANAO utilised a measure of the number of financial budgetsdeveloped annually as an indicator of better practice. This includes thenumber of separate financial budgets prepared in a year, includingforecasts. As shown in Figure 3.3, the benchmarking results indicatesimilar performance between the Commonwealth and Global Groups,both Groups having a median of four budgets per annum. The ANAOnotes that four of the Commonwealth organisations with a number ofannual budgets in excess of the median underwent significant change inthe assessment period, including outsourcing of some functions.

Figure 3.3Budgeting and Analysis Activity Better Practice Benchmark—Number ofAnnual Budgets

13 Op. cit., Beyond Bean Counting 2000 A Benchmark of Effective Financial Management in theAustralian Public Sector, p. 14.

14 Op. cit., Beyond Bean Counting 2000 A Benchmark of Effective Financial Management in theAustralian Public Sector, p. 13.

Formula Used: Total Number of Budgets Developed Annually

0

5

10

15

20

25

30

35

Num

ber o

f Ann

ual B

udge

ts

Commonwealth Government Global

Most Budgets 25%

Middle 50%

Least Budgets 25%

Median4

Median4

35

Conclusion3.13 The benchmarking results indicate that the Commonwealth Groupspends more on budgeting and analysis activity component of the financefunction and, at the median, takes longer to prepare budgets relative tothe Global Group. Overall the Commonwealth Group develops a lowernumber of budgets annually but at the median has the same result as theGlobal Group.

Better Practice Observations 15

3.14 The following paragraphs outline some of the better practices thathave been adopted by organisations to deliver overall improvement inthe efficiency and effectiveness of the financial budgeting and analysisactivity.

3.15 Budgets should link to strategic and tactical planning, aligningthe budgeting process with the strategic direction of the organisationand enabling managers to understand how their day to day efforts movethe organisation toward its goals, leading to better coordination of tactics,better feedback about obstacles and opportunities and, ultimately, betterperformance.

3.16 To develop a strong link between budget development andcorporate strategy, better practice organisations take a series of steps,including:

• clearly defining the strategic goals before budgeting begins;

• establishing and fostering formal and informal channels ofcommunication;

• improving procedures and information systems; and

• providing training for budget developers and other employees so thatthey recognise how their efforts affect the organisational strategy.

3.17 Large organisations often use budget modelling systems, linkingcost management approaches and other data sources with budgeting.This improves the quality of information available for managers’ use indeveloping budgets and consequently the depth, accuracy and speed ofthe process.

Financial Budgeting and Analysis Activity Benchmarks

15 Arthur Andersen Global Best Practices® KnowledgeBase and Reengineering Australia.

36 Benchmarking the Finance Function

3.18 Budget preparation performance can be further improved by:

• implementing or improving standardisation of budget guidelines;

• reviewing the appropriate level of detail in budget preparation;

• improving allocation issue resolution procedures and timeframes; and

• reducing the number of budget centres and levels of decentralisedauthority.

3.19 Budgets should be developed to accommodate change, forexample by including materiality levels for budget revisions. This enablesbusiness units to respond to changing conditions and can obviate theneed to overstate their budgets to cover unforeseen developments.

37

4 Fixed Assets ActivityBenchmarks

Introduction4.1 Fixed assets are physical resources used for production of anorganisation’s goods and services. They are long-term in nature andusually subject to depreciation. Such assets include equipment (machinery,furniture, tools), building structures (offices, factories, warehouses) andland.

4.2 Accurate and timely acquisition, tracking, maintenance anddisposal of fixed assets are aims of asset management. This entailsrecording, adding, updating, depreciating and disposing of fixed assetsin the accounting records in a timely and accurate manner.

4.3 The fixed assets activity in the Commonwealth Group accountsfor a median 3.3 per cent of the total finance operating budget. At median,fixed assets staff in the Commonwealth Group accounts for 2.86 per centof the total finance function staffing, with staffing in individualorganisations ranging between 0.08 and 16.75 FTEs.

4.4 The cost, efficiency, quality and better practice benchmarksselected by the ANAO for the fixed assets activity are set out in Table 4.1.

Table 4.1Fixed Assets Activity Benchmarks

Dimension Formula

Cost—Overall Total fixed assets activity cost / Total organisationalexpenditure

Cost—Per Activity Total fixed assets activity cost / Annual number of fixed assetstransactions

Efficiency—Per Resource Total number of fixed assets tracked / Total fixed assets fulltime equivalent

Quality Percentage of fixed assets that are misallocated ormisclassified

Better Practice Capitalisation threshold for fixed assets

38 Benchmarking the Finance Function

Cost Dimension Benchmarks4.5 The ANAO used two measures of cost related to fixed assetaccounting. The first captures fixed assets cost at a global level andexpresses this as a percentage of total organisational expenditure. Thesecond fixed assets cost benchmark measures costs per transaction.

4.6 As shown in Figure 4.1, the Commonwealth Group allocatesbetween 0.003 and 0.167 per cent of total organisational expenditure tofixed assets activity, with the lowest cost quartile ranging between 0.003and 0.018 per cent. In comparison, the Global Group allocates between0.001 and 0.146 per cent of total organisational expenditure to fixed assetsactivity.

Figure 4.1Fixed Assets Activity Cost Benchmark—Overall Cost

Formula Used: Total Fixed Assets Activity Cost / Total Organisational Expenditure

4.7 The Commonwealth Group total fixed assets activity cost, at themedian, is twice that of the Global Group. Two of the CommonwealthGroup have benchmarks which place them within the lowest cost quartileof the Global Group and eleven of the remaining organisations are withinthe Global Group’s highest cost quartile.

4.8 If the fixed assets activity costs component of the finance functionof those organisations in the Commonwealth Group above the Groupmedian were reduced to the median level, then expenditure reduction ofsome 31 per cent could result.

4.9 The second fixed assets cost benchmark measures costs pertransaction. The benchmarking results—which show the CommonwealthGroup’s median cost per transaction as $46, compared with the GlobalGroup’s $40—are illustrated in Figure 4.2.

0.00%

0.02%

0.04%

0.06%

0.08%

0.10%

0.12%

0.14%

0.16%

0.18%

Per

cent

age

of T

otal

Org

anis

atio

nal E

xpen

ditu

re

Highest Cost 25%

Lowest Cost 25%

Middle 50%

Commonwealth Government Global

Median0.040% Median

0.020%

39

Figure 4.2Fixed Assets Activity Cost Benchmark—Cost / Fixed Asset Transaction

Fixed Assets Activity Benchmarks

Formula Used: Total Fixed Assets Activity Cost / Annual Number of Fixed Assets Transactions

4.10 Although there is a higher median cost per fixed asset transactionin the Commonwealth Group, four of the Commonwealth Group havecost per activity benchmarks which place them within the lowest costquartile of the Global Group. Only three of the Commonwealth Groupare placed within the highest cost per activity quartile of the Global Group.It should also be noted that the highest result in the CommonwealthGroup ($1464) was substantially higher than the rest of the group whichadversely affects the result of the Commonwealth Group. The next highestcost per fixed asset transaction was $310, which is lower than the worstresult in the Global Group ($487).

4.11 The ANAO notes that the four of the Commonwealth Group withbenchmarks within the lowest cost per activity quartile of the GlobalGroup were all placed within the Global Group highest overall costquartile. This could indicate that these organisations are relatively capitalintensive, or that they are processing more assets transactions than theirGlobal Group counterparts.

Efficiency Dimension Benchmark4.12 The ANAO selected the benchmark of annual volume of fixedassets tracked per full-time equivalent (FTE) which provides a measureof employee output and productivity and can be used as a broad indicatorof efficiency. The benchmarking results are summarised in Figure 4.3,which shows a median efficiency level in the Global Group 2.4 times thatof the Commonwealth Group.

$-

$250

$500

$750

$1,000

$1,250

$1,500

Cos

t / F

ixed

Ass

ets

Tra

nsac

tion

Highest Cost 25%

Middle 50%

Lowest Cost 25%

Commonwealth Government Global

Median$40

Median$46

40 Benchmarking the Finance Function

0

10,000

20,000

30,000

40,000

50,000

Fix

ed A

sset

s T

rack

ed /

FT

E

Middle 50%

Most Efficient 25%

Least Efficient 25%

Commonwealth Government

Global

Median8353

Median3502

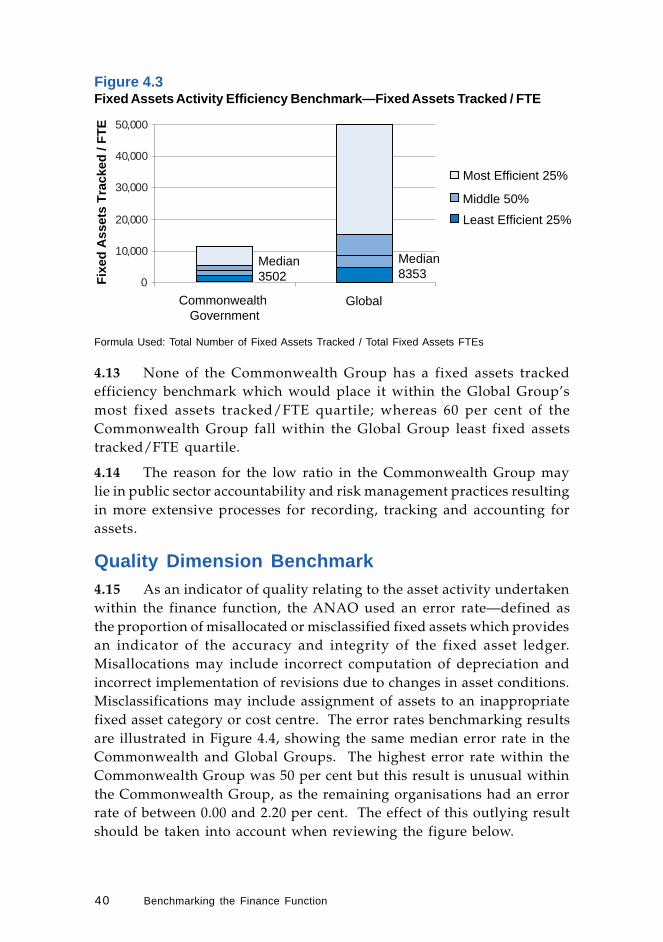

Figure 4.3Fixed Assets Activity Efficiency Benchmark—Fixed Assets Tracked / FTE

Formula Used: Total Number of Fixed Assets Tracked / Total Fixed Assets FTEs

4.13 None of the Commonwealth Group has a fixed assets trackedefficiency benchmark which would place it within the Global Group’smost fixed assets tracked/FTE quartile; whereas 60 per cent of theCommonwealth Group fall within the Global Group least fixed assetstracked/FTE quartile.

4.14 The reason for the low ratio in the Commonwealth Group maylie in public sector accountability and risk management practices resultingin more extensive processes for recording, tracking and accounting forassets.

Quality Dimension Benchmark4.15 As an indicator of quality relating to the asset activity undertakenwithin the finance function, the ANAO used an error rate—defined asthe proportion of misallocated or misclassified fixed assets which providesan indicator of the accuracy and integrity of the fixed asset ledger.Misallocations may include incorrect computation of depreciation andincorrect implementation of revisions due to changes in asset conditions.Misclassifications may include assignment of assets to an inappropriatefixed asset category or cost centre. The error rates benchmarking resultsare illustrated in Figure 4.4, showing the same median error rate in theCommonwealth and Global Groups. The highest error rate within theCommonwealth Group was 50 per cent but this result is unusual withinthe Commonwealth Group, as the remaining organisations had an errorrate of between 0.00 and 2.20 per cent. The effect of this outlying resultshould be taken into account when reviewing the figure below.

41

Figure 4.4Fixed Assets Activity Quality Benchmark—Error Rates

Fixed Assets Activity Benchmarks

Formula Used: Percentage of Fixed Assets Misallocated or Misclassified

4.16 Three of the Commonwealth Group have benchmarks whichwould place them within the Global Group least errors quartile. TheANAO notes that these particular organisations also have a relativelyhigh cost per fixed assets transaction. Individual organisations need toconsider the appropriate risk management profile to minimise costs whilekeeping error rates within acceptable limits.

Better Practice Benchmark4.17 The ANAO also benchmarked the value at which assets arecapitalised within the organisations within the two Groups. The assetcapitalisation threshold is a monetary reporting threshold thatorganisations establish in order to reduce the number of assets reportedin the financial statements to only those which are significant in value.Generally the threshold is set to ensure that at least 95% of the totalvalue of non-current assets is reported in the financial statements. Theestablishment of such a threshold is an attempt to weigh the cost ofgathering data against its usefulness or significance to the readers of thefinancial statements. The asset capitalisation threshold does not relateto whether organisations need to record the existence of assets. This isan asset management decision based on the importance of the asset orgroup of assets to an organisation and accountability criteria.

4.18 The benchmarking results are shown in Figure 4.5, with mediancapitalisation thresholds of $2000 and $1628 in the Commonwealth andGlobal Groups.

0%5%

10%15%20%25%

30%35%40%

45%50%

Commonwealth Government

Global

Most Errors 25%

Middle 50%

Least Errors 25%

Per

cent

age

of F

ixed

Ass

ets

Mis

clas

sifie

d or

Mis

allo

cate

d

Median1.00%

Median1.00%

42 Benchmarking the Finance Function

Figure 4.5Fixed Assets Activity Better Practice Benchmark—Capitalisation Threshold

Formula Used: Capitalisation Threshold for Fixed Assets

4.19 In almost all of the Commonwealth Group, the minimumcapitalisation threshold is set at $2000, somewhat below the Global Grouphighest threshold quartile which ranges between $4071 and $16 284, butabove the Global median. The ANAO notes that an asset capitalisationthreshold of $2000 had been mandatory for the majority ofCommonwealth public sector organisations until recently.

Conclusion4.20 The Commonwealth Group overall fixed assets activity costs morewhen compared with the Global Group and the Global Group performedbetter on the selected efficiency benchmark. Quality as measured byreported error rates was equal at the median.

4.21 Accountability requirements, risk management practices and useof technology or other means to enhance process efficiency may beappropriate areas for consideration by organisations wishing toinvestigate differences in the benchmark results.

Better Practice Observations 16

4.22 The ANAO has undertaken two recent audits of assetmanagement: the first—in 1995–9617—was followed up in 1997–9818. Inconjunction with the 1995–96 Audit Report the ANAO produced an Asset

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

Commonwealth Government

Cap

italis

atio

n T

hres

hold

Global

Highest Threshold 25%

Lowest Threshold 25%

Middle 50%

Median$2000

Median$1628

16 Australian National Audit Office Audit Report No.27 of 1995–96 Asset Management, AustralianNational Audit Office Audit Report No.41 of 1997–98, Asset Management and Arthur AndersenGlobal Best Practices® KnowledgeBase.

17 Australian National Audit Office Audit Report No. 27 of 1995–96 Asset Management.18 Australian National Audit Office Audit Report No. 41 of 1997–98 Asset Management.

43

Management Better Practice Guide19 and the Asset ManagementHandbook20 which was designed to assist managers interpret andimplement the assets management principles developed in the Report.In the 1997–98 Report the ANAO noted that, while there had beensignificant acceptance by public sector organisations of therecommendations of Audit Report No.27, 1995–96, many organisationsreviewed had not fully adopted a strategic assets management approachto maximise performance and accountability for outputs and outcomes.

4.23 The following paragraphs outline some of the better practices thathave been adopted by organisations to deliver overall improvement inthe efficiency and effectiveness of the fixed assets activity.

Principles4.24 Five principles which underpin better practice asset managementare:

• Integrated Planning—Asset management decisions are integrated withstrategic planning. This is achieved by establishing clear links betweenassets, corporate objectives and program or service delivery standards.

• Acquisition Planning—Asset planning decisions are based on anevaluation of alternatives to ownership, including non-asset solutionsand demand management. The evaluations should include acomparison of life-cycle costs, benefits and risks.

• Accountability—An effective framework is established to identifythose responsible for assets. In particular, the framework shouldinclude mechanisms which establish accountability for asset condition,use and performance.

• Disposal Planning—A framework for the disposal process should bein place. In particular, disposal decisions should be based on an analysisof the methods which achieve the best net return; and disposalperformance should be monitored for effectiveness.

• Control Framework—An effective internal control structure isestablished for asset management, including asset policies andprocedures and use of appropriate information systems.

Fixed Assets Activity Benchmarks

19 Australian National Audit Office Asset Management Better Practice Guide June 1996.20 Australian National Audit Office Asset Management Handbook June 1996.

44 Benchmarking the Finance Function

Technology4.25 Integration of the fixed asset system with the human resourcemanagement information system allows the tracking of employeepossession of attractive and portable items.

4.26 Integration of the asset register with the purchasing, capitalplanning, preventative maintenance, accounts payable (to captureacquisitions) and general ledger (to validate cost centre coding) systemseliminates potential for errors, duplicate data entry and processing.

4.27 Electronic marking (bar codes or electronic markers) and scanningcan enhance the efficiency of identifying the inventory and location ofassets.

Policies4.28 Raising the capitalisation threshold (in accordance withorganisational accounting, risk management and the businessrequirements) can decrease the total number of fixed assets that have tobe recorded and tracked.

4.29 Establishment of standards and policies maintenance of fixedassets, including preventative maintenance, can result in reducedequipment failure, reduced costs and increased utilisation.

45

5. Accounts Payable ActivityBenchmarks

Introduction5.1 For most organisations, accounts payable is a linear process thatbegins with receiving an invoice and ends with issuing payment to thesupplier. Organisations generally follow a standard set of activities forprocessing an invoice for payment, including:

• receiving the invoice via mail, fax, e-mail or electronic data interchange(EDI);

• categorising the invoice, entering it into a system, and scheduling itfor further processing;

• reviewing the invoice for authenticity and arithmetic accuracy;

• documenting the invoice by attaching receiving paperwork and thepurchase order;

• obtaining the required approval to pay the invoice;

• scheduling the invoice for payment, taking into consideration theorganisation’s priorities for payment, the invoice due date and possibleprompt-payment discounts; and

• on the appropriate day, paying the invoice via cheque or electronicmeans and notifying the supplier of payment.

5.2 Additional tasks include responding to inquiries from suppliersand others within the organisation; resolving payment issues and disputes;keeping the master file of suppliers up-to-date; and managing accountingpolicies that affect supplier relationships and cash management.

5.3 The increasing use of ‘electronic commerce’ (e-commerce) willchange the payment processes employed by organisations. E-commerceis regarded as the execution of business transactions using electroniccommunications networks and is used by organisations to streamlinebusiness processes.

5.4 Next to payroll and budgeting, accounts payable is one of themore significant activities conducted within the finance function activityarea of the Commonwealth Group, accounting for a median 13.6 per centof the total finance budget.

5.5 In the Commonwealth Group, the median accounts payableprocessing staff is 14.45 per cent of the total finance function staffing,with individual organisation staffing ranging between 1 and 32 FTEs.

46 Benchmarking the Finance Function

5.6 The quality of design of the accounts payable process—and howwell the process is executed—has an impact on two areas important tothe organisation: supplier relationships and cash flow. The primarybusiness objective of accounts payable is to be an efficient, low-costcontributor to the “obtain materials and supplies” process. This can beaccomplished by making timely and accurate payments for goods andservices purchased and thereby optimising cash flow through effectivemanagement of disbursements, credit terms and discounts.

5.7 The accounts payable benchmarks selected by the ANAO addressdimensions of cost, efficiency, quality and better practice as set out inTable 5.1.

Table 5.1Accounts Payable Activity Benchmarks

Dimension Formula

Cost—Overall Total accounts payable activity cost / Total organisationalexpenditure

Cost—Per Activity Total accounts payable cost / Number of annual invoices

Efficiency—Per Resource Total accounts payable invoices / Total accounts payable FTEs

Efficiency—Size Total accounts payable payments / Number of invoicesprocessed

Quality—Error Rate Total accounts payable errors / Number of invoices processed

Better Practice Total number of active vendors to organisation

Cost Dimension Benchmarks5.8 The ANAO selected two benchmarks to gain an indication of thecost of the accounts payable activity within the finance function. Thefirst captures the accounts payable cost at a global level and expresses itas a percentage of total organisational expenditure, and is illustrated inFigure 5.1. The Commonwealth Group allocates between 0.007 and0.870 per cent of their total organisational expenditure on their accountspayable activity, with the lowest cost quartile ranging between 0.007 and0.080 per cent. These results indicate a higher proportion of expenditureby the Commonwealth Group than the Global Group, with the GlobalGroup benchmarks ranging between 0.005 and 0.350 per cent of totalorganisational expenditure.

47

0.00%

0.15%

0.30%

0.45%

0.60%

0.75%

0.90%

Highest Cost 25%

Middle 50%

Lowest Cost 25%

Commonwealth Government Global

Per

cent

age

of T

otal

Org

anis

atio

n E

xpen

ditu

re

Median0.164% Median

0.120%

Figure 5.1Accounts Payable Activity Cost Benchmark—Overall Cost

Accounts Payable Activity Benchmarks

Formula Used: Total Accounts Payable Activity Cost / Total Organisational Expenditure

5.9 Although four of the Commonwealth Group are in the lowestcost quartile of the Global Group, nine are placed within the Global Grouphighest cost quartile. At the median, organisations in the CommonwealthGroup are spending 37 per cent more on the accounts payable activitythan the Global Group.

5.10 The ANAO notes that higher than normal costs may have beenincurred by some of the Commonwealth Group because of theimplementation of new information technology systems during thebenchmark survey year. The benchmark data highlights that there maybe opportunities to investigate reasons for the differences and possiblyreduce cost. If the accounts payable cost component of the financefunction of those organisations in the Commonwealth Group above theGroup median was reduced to the median level, then expenditurereductions of some $1.3 million (15 per cent) would result.

5.11 The second cost dimension benchmark utilised by ANAOmeasures the accounts payable activity cost per invoice processed. Asdisplayed in Figure 5.2, none of the Commonwealth Group are in thelowest cost quartile of the Global Group. At the median, theCommonwealth Group processing cost per invoice is 72 per cent higherthan the Global Group.

48 Benchmarking the Finance Function

Formula Used: Total Accounts Payable Activity Cost / Number of Annual Invoices

5.12 A contributing factor to the higher accounts payable cost in theCommonwealth Group may be that the Commonwealth Group undertakesmore extensive checking to detect errors before payments are processed.The lower error rates in the Commonwealth Group are reviewed later inthis chapter.

5.13 The ANAO notes that previous ANAO audit reports determineda benchmark for Commonwealth agencies relating to cost per invoiceprocessed (for direct labour cost only) at $10 in 198721 and $11 in 199622.Adjusted for inflation the figures at 30 June 1999 are $14.64 and $11.62respectively23. The data from this benchmarking exercise indicates a figureof $14.54 (30 June 1999) for the direct labour cost component of cost perinvoice processed.

$0

$20

$40

$60

$80

$100

$120

Cos

t / A

ccou

nts

Pay

able

Invo

ice

Highest Cost 25%

Middle 50%

Lowest Cost 25%

Commonwealth Government Global

Median$18.88 Median

$10.99

21 Department of Finance, 1987, Efficiency Scrutiny on Processing of Accounts—A Report for theMinister of Finance.

22 Australian National Audit Office Audit Report No.16 of 1996–97 Payment of Accounts.23 Figures have been adjusted using the “General Government Final Consumption Expenditure—

Other” price index from the Australian Bureau of Statistics publication Australian System ofNational Accounts (ABS Catalogue No. 5204.0). The 1987 figure was calculated as follows:$10/68.3 * 100 = $14.64 and the 1996 figure was calculated as: $11/94.6 * 100 = $11.62.

Figure 5.2Accounts Payable Activity Cost Benchmark—Cost / Invoice

49

Accounts Payable Activity Benchmarks

0

10,000

20,000

30,000

40,000

50,000

Invo

ices

Pro

cess

ed /

Acc

ount

s P

ayab

le F

TE

Commonwealth Government Global

Most Efficent 25%

Middle 50%

Least Efficent 25%

Median7412Median

3667

Efficiency Dimension Benchmarks5.14 The ANAO used two benchmarks to provide a broad indicator ofefficiency for the accounts payable activity. The first measures the numberof accounts payable invoices processed per FTE, providing a reflectionof employee output and productivity. The results are provided in Figure5.3. The second accounts payable efficiency benchmark used by the ANAOmeasures the average accounts payable payment size. These results arepresented in Figure 5.4.

5.15 In Figure 5.3, only one of the Commonwealth Group has a numberof invoices per accounts payable/FTE ratio which places it in the mostefficient quartile of the Global Group. Seventy five per cent of theorganisations in the Commonwealth Group have ratios that place themwithin the least efficient quartile of the Global Group.

Figure 5.3Accounts Payable Activity Efficiency Benchmark—Processed Invoices / FTE

Formula Used: Total Accounts Payable Invoices / Total Accounts Payable FTEs

5.16 The ANAO notes that the relatively high cost may also beattributed, in part, to more thorough checking of invoices resulting inlower error rates. In this (and all other activities), organisations need toconsider the balance of cost, efficiency and quality dimensions.

5.17 The second accounts payable efficiency benchmark used by theANAO measures the average accounts payable payment size. Optimisingthe size of individual payments—for example by rationalising the numberof vendors or consolidating a number of invoices into one payment—canlead to more efficient accounts payable processes through reducedtransaction volumes and costs. As illustrated in Figure 5.4, theCommonwealth Group has a substantially smaller average payment sizeprofile than the Global Group.

50 Benchmarking the Finance Function

Formula Used: Total Accounts Payable Payments / Number of Invoices Processed

Quality Dimension Benchmark5.18 The ANAO used a measure of the total number of errors as apercentage of total accounts processed to supplement the accounts payablecost and efficiency benchmarks.

5.19 Accounts payable errors include incoming voucher errors, voucherprocessing errors and cheque errors. Incoming voucher errors relate tothe completeness, accuracy and proper authorisation of vouchers. Thisincludes missing documentation, lack of required approvals, missing orinaccurate information (eg. account coding) or discrepancies ininformation between various documents. Voucher processing errors areerrors rejected by the accounts payable system in relation to the validityof account distribution coding, vendor account numbers etc. Chequeerrors are errors related to the production and dissemination ofpayments.

5.20 The error rates benchmark indicates (as illustrated in Figure 5.5)that, while the accounts payable costs of the Commonwealth Group maybe relatively high in comparison with the Global Group, the quality ofthe outcomes in respect of error rates is better. Seven of theCommonwealth Group have error rates within the best quartile of theGlobal Group, and none of the Commonwealth Group are ranked nextto the Global Group highest error rates quartile. The median error rateof the Commonwealth Group is some 45 per cent lower than that of theGlobal Group.

$0

$20 000

$40 000

$60 000

$80 000

$100 000

$120 000

$140 000

$160 000

$180 000

CommonwealthGovernment

Aver

age

Acc

ount

sPay

able

Pay

men

t

Most Efficient 25%

Middle50%

Least Efficient 25%

Global

Median$9224

Median$13 167

Figure 5.4Accounts Payable Activity Efficiency Benchmark—Average Payment

51

Figure 5.5Accounts Payable Activity Quality Benchmark—Error Rates

Accounts Payable Activity Benchmarks

Formula Used: Total Accounts Payable Errors / Number of Invoices Processed

5.21 There is a correlation between the cost of processing and errorrates and this information may indicate that the Commonwealth Groupis investing more time and effort in checking payments. The ANAOnotes that the organisation in the Commonwealth Group that had thebest performance in respect of the two accounts payable cost dimensionbenchmarks and the efficiency benchmark, had the second highest errorrate, indicating that the potential trade-off between cost and quality maybe a factor in the results.

Better Practice Benchmark5.22 Optimising the number of vendors is often implemented todevelop closer working relationships and improve the efficiency of theaccounts payable process. The ANAO used a benchmark based on thenumber of active vendors to provide an indication of the adoption ofbetter practices within the two groups.

5.23 The results of benchmarking the number of active vendors areshown in Figure 5.6.

0%

5%

10%

15%

20%

25%

30%

35%

CommonwealthGovernment

Err

ors/

Pay

men

t Highest Error Rates 25%

Middle50%

Lowest Error Rates 25%

Global

Median1.52%

Median2.74%

52 Benchmarking the Finance Function

Formula Used: Total Number of Active Vendors to Organisation

5.24 One of the Commonwealth Group has a benchmark which placesit in the Global Group least vendors quartile. However, of the remainingCommonwealth Group, half have benchmarks which place them in theGlobal Group most vendors quartile. At the median, the CommonwealthGroup has 2.4 times as many active vendors than the Global Group. Thissuggests that organisations in the Commonwealth Group may benefitfrom reviewing their accounts payable operations to ascertain whetherthere is scope to take advantage of any benefits associated with reducingthe number of active vendors.

5.25 From the data examined, the ANAO noted that the number ofactive vendors is not necessarily a function of the size of the organisationbut may be connected to the role of the organisation within theCommonwealth. Several large benchmarking participants having feweractive vendors than some of the smaller Commonwealth organisations.

Conclusion5.26 At the median, the Commonwealth Group generally reportedlower performance across the range of cost and efficiency benchmarksof the accounts payable process. Increases in the number of paymentsprocessed per accounts payable FTE and the average size of paymentsand a reduction in the number of vendors could result in a reduction inexpenditure. However, it should be noted that the Commonwealth Groupachieved substantially fewer errors, highlighting the trade off betweencost and quality.

-

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

Num

ber

of A

ctiv

e V

endo

rs