Embed Size (px)

Citation preview

ww

MEDIAN DPI F OR 20 10 VC V IN TAGE S SURGE S

6P E I N ENERGY:PME CASE S TUDY

9PE HORIZON IRRs BY FUND SIZE

14

SPONSORED BY

BENCHMARKING+ F UND P ERF ORM A NCE

through 3Q 2015

Venue Data Room

WELCOME TO VENUE

®DEAL SOLUTIONS

At RR Donnelley, our Venue Deal Solutions streamline every step of the deal life cycle.

888.773.8379www.rrdonnelley.comwww.venue.rrd.comCopyright © 2016 R. R. Donnelley & Sons Company.All rights reserved.

Venue Data Room — Whether conducting due diligence for a merger, raising capital, or developing a

document repository, our Venue Data Room is your ideal workspace for Deals. Done. Simple.

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

ContentGARRETT JAMES BLACK Senior Analyst

NIZAR TARHUNI Senior Analyst

BRIAN LEE Senior Analyst

EVAN B. MORRIS Analyst

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2016 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Introduction 4

PE & VC KS PME Benchmarks 5

KS PME Case Study: Energy 6

IRR by Fund Type 7

Quartiles & Benchmarks 8

PE IRRs 9

PE Fund Return Multiples 10

PE Fund Cash Flows 11-12

VC IRRs 13

VC Fund Return Multiples 14

VC Fund Cash Flows 15

Select Top Funds by IRR 16

Methodology 17

Contents

3 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

IntroductionEach quarter, we seek to cover the full spectrum of activity in private equity

and venture capital, presenting multiple datasets along with analysis to inform

your decisions. Hence our initial quarterly reports—the U.S. and European

PE Breakdowns and the U.S. and European Venture Industry Reports—offer

overviews of quarter-over-quarter (QoQ) dealmaking, exits and fundraising.

But to round everything off, toward the end of the quarter we benchmark

global PE and venture fund performance, utilizing our most recent datasets

of fund performance to assess trends in distributions, IRRs, fund return

multiples and more. Surveying these latest numbers presents a useful, funds-

based perspective, particularly as the high tide of exit activity subsides, the

buyout cycle moves lower and the venture capital climate cools. Fund returns

are lagged, yet the picture they portray—particularly the sheer strength of

distributions across both PE and VC—helps explain current strong fundraising

across both PE and VC, as well as shifts in commitments across different

strategies, among other broader trends.

If you have any questions or comments, please don’t hesitate to reach out to us

at [email protected]. As a final note, all the funds return data within this

report is as of September 30, 2015; the lag is due to reporting cycles.

RR Donnelley is the world’s largest integrated communications company. The company works collaboratively with more than 60,000 customers worldwide to develop custom communications solutions that reduce costs, drive top-line growth, enhance ROI and increase compliance. Drawing on a range of proprietary and commercially available digital and

conventional technologies deployed across four continents, the company employs a suite of leading Internet based capabilities and other resources to provide pre-media, printing, logistics and business process outsourcing services to clients in virtually every private and public sector. Our Corporate Responsibility Report is available at www.rrdonnelley.com.

Our Venue® secure online workspace provides a powerful feature-set and an intuitive design that allows you to easily organize, manage, share and track all of your sensitive information. Venue® data rooms provide complete control, allowing you to manage who has access to your data room, which documents they see, and how they can interact with those documents.

Venue® data rooms are backed by RR Donnelley, a $10.5 billion corporation with more than 500 locations and nearly 60,000 employees worldwide. RR Donnelley’s total revenues are larger than all other virtual data room providers combined. Whether you’re conducting due diligence for a merger, raising capital, or developing a document repository, a Venue® virtual data room is the ideal virtual workspace for managing critical information.

RR Donnelley is the sponsor of the PitchBook Global PE & VC Benchmarking & Fund Performance Report. All information contained in this publication is for informational purposes only and should not be construed as legal, accounting, tax, or other professional advice of any kind, on any subject matter. RR Donnelley expressly disclaims all liability in respect to actions taken or not taken based on any or all the content herein.

MAKE WAY FOR

SMARTER, ON-THE-FLY MEETING PREP

US +1 206.623.1986

UK +44 (0)207.190.9809

pitchbook.com

Introducing PitchBook

Mobile. The same

excellent data, technology

and service from the

PitchBook Platform, now

available on a mobile

device.

Search:

“PitchBook”

Available for

4 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

KS PME Benchmarks

IRR and cash multiples have been the gold standard of benchmarking for decades, but one of their main drawbacks is that they cannot be directly compared to indices that are used in mainstream asset classes. Public-market equivalent benchmarks (PMEs) effectively address this problem, making it possible to directly compare alternative asset fund performance to the performance of indexed asset classes by using fund-level cash flows.

As there are multiple ways to calculate a PME, PitchBook has employed the Kaplan-Schoar PME method.

Kaplan-Schoar (KS) Method:

A white paper detailing the calculations and methodology behind the PME benchmarks can be found at pitchbook.com. PitchBook News & Analysis also contains several articles with PME benchmarks and analysis. These can be read here.

To find out how the PME benchmarks can be utilized to gauge performance of a specific fund or your fund portfolio, please contact us at [email protected].

PMEKS—TVPI, T =S t=0

distribution

I t

T tNAVTIT

( )+

AN INTRODUCTION

TO PME BENCHMARKS

S t=0T contribution

I t

t( )

PE KS PME Benchmark by vintage

VC KS PME Benchmark by vintage

Source: PitchBook

The KS PME charts on this page show the relative performance for a particular vintage of PE or VC funds against the specified index since the funds’ inception. Pre-2006 vintage PE funds outperformed the public markets consistently between 2002 and 2005, while VC funds across most vintages show overall underperformance. The stock market’s surge over the last couple of years has definitely cut into PME values for more recent vintages on the PE side in particular; though, in the event of a market downturn, it’s possible recent PE and VC fund vintages will begin to swing up if they generate returns better than stocks.

When using a KS PME, a value greater than 1.0 indicates outperformance of the public index (net of all fees). For example, the 1.13 value for 2005 vintage PE funds means investors in a typical vehicle from that year are 13% better off having invested in PE than if they had invested in public equities over the same period.

When using a KS PME, a value less than 1.0 indicates underperformance of the public index (net of all fees). For example, the 0.81 value for 2006 vintage VC funds means investors in a typical vehicle from that year would see only 81% of the value they would have in the public markets.

PME calculated using Russell 3000® Index

PME calculated using Russell 2000® Growth IndexSource: PitchBook

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

5 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

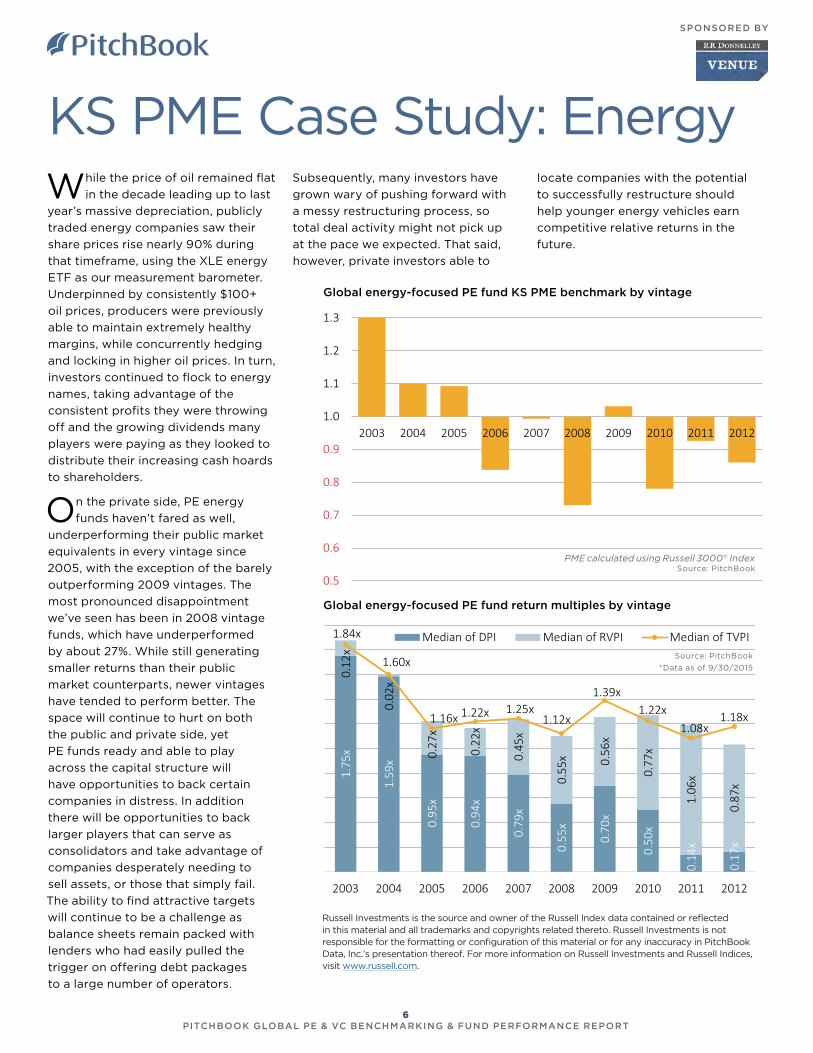

KS PME Case Study: EnergyW hile the price of oil remained flat

in the decade leading up to last

year’s massive depreciation, publicly

traded energy companies saw their

share prices rise nearly 90% during

that timeframe, using the XLE energy

ETF as our measurement barometer.

Underpinned by consistently $100+

oil prices, producers were previously

able to maintain extremely healthy

margins, while concurrently hedging

and locking in higher oil prices. In turn,

investors continued to flock to energy

names, taking advantage of the

consistent profits they were throwing

off and the growing dividends many

players were paying as they looked to

distribute their increasing cash hoards

to shareholders.

On the private side, PE energy

funds haven’t fared as well,

underperforming their public market

equivalents in every vintage since

2005, with the exception of the barely

outperforming 2009 vintages. The

most pronounced disappointment

we’ve seen has been in 2008 vintage

funds, which have underperformed

by about 27%. While still generating

smaller returns than their public

market counterparts, newer vintages

have tended to perform better. The

space will continue to hurt on both

the public and private side, yet

PE funds ready and able to play

across the capital structure will

have opportunities to back certain

companies in distress. In addition

there will be opportunities to back

larger players that can serve as

consolidators and take advantage of

companies desperately needing to

sell assets, or those that simply fail.

The ability to find attractive targets

will continue to be a challenge as

balance sheets remain packed with

lenders who had easily pulled the

trigger on offering debt packages

to a large number of operators.

Global energy-focused PE fund KS PME benchmark by vintage

Global energy-focused PE fund return multiples by vintage

Russell Investments is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. Russell Investments is not responsible for the formatting or configuration of this material or for any inaccuracy in PitchBook Data, Inc.’s presentation thereof. For more information on Russell Investments and Russell Indices, visit www.russell.com.

PME calculated using Russell 3000® IndexSource: PitchBook

Subsequently, many investors have

grown wary of pushing forward with

a messy restructuring process, so

total deal activity might not pick up

at the pace we expected. That said,

however, private investors able to

locate companies with the potential

to successfully restructure should

help younger energy vehicles earn

competitive relative returns in the

future.

Source: PitchBook

*Data as of 9/30/2015

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1.75

x

1.59

x

0.95

x

0.94

x

0.79

x

0.55

x

0.70

x

0.50

x

0.14

x

0.17

x

0.12

x

0.02

x

0.27

x

0.22

x

0.45

x

0.55

x 0.56

x

0.77

x

1.06

x

0.87

x

1.84x

1.60x

1.16x 1.22x 1.25x1.12x

1.39x1.22x

1.08x1.18x

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Median of DPI Median of RVPI Median of TVPI

6 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

IRR by Fund TypeGlobal horizon IRR by fund type

Source: PitchBook

*Data as of 9/30/2015

Global median IRR by fund type and vintage year

Source: PitchBook

*Data as of 9/30/2015

Vintage Year

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

PE 13.4% 11.5% 8.3% 7.5% 9.4% 10.8% 12.0% 9.5% 10.0% 10.7%

VC 3.4% 0.9% 4.6% 5.4% 6.7% 9.3% 12.9% 20.5% 13.9% 12.0%

Debt 6.9% 10.7% 6.3% 5.2% 8.1% 11.5% 11.0% 10.7% 10.0% 9.3%

FoF 9.2% 7.8% 7.5% 7.9% 9.1% 10.6% 10.9% 10.3% 10.7% 8.7%

PE funds remain outperformers in

the long run, outpacing all other

asset classes by a considerable margin.

This is attributable to a variety of

factors, including the historic M&A

environment that PE firms seized upon

in order to liquidate aging portfolios

amassed prior to the financial crisis.

It’s worth highlighting, in addition,

that there are a few outliers of debt

fund performance—for example, the

11.5% return in 2008 vintage funds

exemplifies how PE fund managers

were able to engage in regulatory

arbitrage, essentially filling in for

banks that could not lend during those

troubled times. Only venture stands

out among recent vintages, thanks

to the surge in unrealized valuations

generated by “private IPOs”—huge

late-stage rounds wherein secondary

buyers bought out earlier investors—as

well as initially well-performing IPOs

and the biggest contributor of all,

strategic acquisitions.

Source: PitchBook

*Data as of 9/30/2015

0%

5%

10%

15%

1-Year 3-Year 5-Year 10-Year

PE Funds VC Funds Debt Funds Funds-of-Funds

0%

5%

10%

15%

20%

25%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

PE Funds VC Funds Debt Funds Funds-of-Funds

7 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

Quartiles & Benchmarks Global PE IRR quartiles by vintage year

Source: PitchBook

*Data as of 9/30/2015

As more and more entrants have flocked to the PE

industry, finding alpha-generating opportunities

has become expectedly more difficult. As this trend

has proliferated since the 2000s, we’ve seen the

spread in fund returns from top-quartile to bottom-

quartile managers shrink from over 24% in 2001

vintages, to just 13.6% in 2012 vintages as of 3Q 2015.

While spreads are low relative to what we saw at

the turn of the century, they have crept higher over

recent vintages, including those of post-recession

vehicles.

Interestingly, top-quartile performance from 2012

vintages has been greater than any year since 2003.

With global growth, valuations and deal appetites

supporting selling managers in recent years, GPs

have been able to move companies to market quicker,

and thus, we’ve seen newer vintages generate

respectable returns. The bottom-quartile benchmark

for these newer vintages has also inched its way

higher as of 3Q 2015, which could be driven by some

of the smaller and more targeted vehicles we’ve

seen come to market finally finding opportunities to

realize returns as dealmakers have looked to smaller

transactions to avoid competition.

Global VC IRR quartiles by vintage yearThe extent to which IRRs can shift even in a

short amount of time can be easily seen when

comparing the table to the right with its counterpart

in the last edition of this report series. Through

the middle of 2015, the top quartile IRR of 2012

vintages was 33.0%—now, with another quarter’s

data inputted, it has declined to 23.0%. Even though

a small cadre of relatively young venture funds are

still seeing lofty performance for now, sooner rather

than later they will have to contend with a potential

liquidity crunch. Consequently, it’s to be expected

that as time goes on, even recent vintages will see

the spread of performance slide and tighten. It’s

worth remarking upon how low the bottom and

median quartiles actually slide in general, accounting

for a few outlier years. The higher risk of venture is

quite well illustrated by the width of the spread in

performance, even of recent vintages.

Source: PitchBook

*Data as of 9/30/2015

Vintage Year

2005 2006 2007 2008 2009 2010 2011 2012

Top Quartile IRR

12.4% 10.9% 14.0% 16.3% 17.2% 15.0% 17.3% 19.2%

Median 8.3% 7.5% 9.4% 10.8% 12.0% 9.5% 10.0% 10.7%

Bottom 3.0% 3.2% 4.9% 6.5% 7.6% 4.9% 3.8% 5.6%

Vintage Year

2005 2006 2007 2008 2009 2010 2011 2012

Top Quartile IRR

11.3% 11.2% 16.5% 18.5% 20.3% 33.5% 20.5% 23.0%

Median 4.6% 5.4% 6.7% 9.3% 12.9% 20.5% 13.9% 12.0%

Bottom -0.1% -4.8% 0.3% 0.5% 6.3% 10.0% 4.1% 3.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 201225th Percentile Median 75th Percentile

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 201225th Percentile Median 75th Percentile

8 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

Private Equity IRRs

Global PE horizon IRR by size bucket

Source: PitchBook

*Data as of 9/30/2015

PE horizon IRR by region

Source: PitchBook

*Data as of 9/30/2015

On an absolute basis, PE IRRs

continue to soften, and while 2015

experienced a consistent increase in

exit activity by value, the makeup of

the PE-backed assets being sold play

a significant role in how the realized

returns impact IRR calculations. The

ability of managers to capitalize in

an overarching sellers’ market was

in full effect as we arrived at the

midpoint of last year. In fact, despite

the market headwinds the investment

world experienced in 2H 2015, exit

activity continued to climb to record

highs by the end of the year. Yet the

deterioration in the credit markets

during that period—that forced deal

terms to shift and purchase prices

to move lower in many cases—cut

into the net fund cash flows used

to calculate horizon IRRs, which are

based on the aggregate capital flows

that come in and out of funds during

a specific time period, regardless of

vintage.

With that as the backdrop, 10-

year horizon IRRs across all

PE vehicles moved lower for the

fourth consecutive period to 13.1%,

while five-year horizons came in at

their lowest level since 4Q 2013 at

12.2%. Interestingly, vehicles between

$500 million and $1 billion in size

outperformed general PE returns by

about 1%, which could be driven by

vehicles in this size bucket able to

remain active in a more flexible fashion

across the middle market.

Outside of real estate vehicles,

secondaries funds outperformed

all fund types across a one-year

horizon. As LPs and specialist

investors have looked to chase alpha

by employing an increasing level of

active management across PE, the

market has experienced an influx of

institutional secondaries ready and

equipped to provide liquidity to selling

LPs. Armed with added transparency

into fund assets and an ability to

negotiate attractive discounts to NAV

over the last few years, this strategy

has done well by investors, despite its

returns relative to itself moving lower,

similar to what we’ve seen across the

entire PE realm.

0%

5%

10%

15%

1-Year 3-Year 5-Year 10-Year

Under $250M $250M-$500M $500M-$1B $1B+

0%

5%

10%

15%

20%

25%

30%

35%

40%

1-Year 3-Year 5-Year 10-Year

U.S. PE Funds European PE Funds Rest of World PE Funds

9 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

PE Fund Return MultiplesGlobal average PE DPI multiples over time by vintage

Global median PE fund return multiples by vintage

Source: PitchBook

*Data as of 9/30/2015

Source: PitchBook

*Data as of 9/30/2015

Fund return multiples have

continued to move incrementally

higher over time. Out of the vintages

included in the chart below, the

most substantial increase occurred

in 2008 vintage vehicles, which saw

the median TVPI for those vehicles

move higher to 1.42x compared to a

1.36x figure recorded during the last

edition of this report. The growth in

TVPI and DPI multiples associated

with vintages between 2006 and

2009 should stagnate, given an exit

environment we expect to move much

slower. While the multiples of more

recent vintages will continuously

inch higher, such an advance will also

happen at a noticeably slower pace,

as managers face the challenges that

come with a competitive deal market

and a declining supply of market-ready

targets.

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x

1 2 3 4 5 6 7 8 9 10Years since inception

2004 2005 2006 2007 2008 2009 2010

1.64

x

1.58

x

1.36

x

1.12

x

0.97

x

0.84

x

0.78

x

0.69

x

0.40

x

0.20

x

0.12

x

0.04

x

0.08

x

0.11

x

0.28

x

0.40

x

0.54

x

0.58

x

0.70

x

0.87

x

0.97

x

1.00

x

1.75x1.59x

1.50x1.41x 1.40x 1.45x 1.42x 1.42x

1.28x1.20x 1.17x

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Median of DPI Median of RVPI Median of TVPI

10 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

PE Fund Cash Flows

YEAR TOTAL CONTRIBUTIONS ($B)

TOTAL DISTRIBUTIONS ($B)

NET CASH FLOW ($B)

2001 ($54.5) $26.3 ($28.2)

2002 ($77.6) $32.0 ($45.7)

2003 ($78.1) $59.5 ($18.6)

2004 ($109.0) $142.5 $33.5

2005 ($137.6) $156.0 $18.4

2006 ($229.4) $177.9 ($51.5)

2007 ($307.8) $215.4 ($92.4)

2008 ($317.5) $121.5 ($196.0)

2009 ($166.2) $59.7 ($106.5)

2010 ($252.7) $172.5 ($80.3)

2011 ($257.5) $266.3 $8.8

2012 ($272.9) $325.9 $53.0

2013 ($228.3) $388.0 $159.6

2014 ($278.8) $463.6 $184.8

2015* ($224.8) $342.0 $117.3

Source: PitchBook

*Data as of 9/30/2015

Global PE funds’ annualized cash flow by year

Global net PE cash flows have

remained robust for LPs, coming

in at over $117 billion through the end

of 3Q 2015. While things started to

slow in terms of deal activity during

that period, exits continued to soar,

which was easily reflected by the

massive $126 billion that was returned

to LPs during 3Q 2015 alone. 4Q 2015

saw a record number of exits close,

and thus, we could be positioned to

see a record annual distribution figure

during the next edition of this report.

The end of 2015 did see deal flow

slow, however, which from a high

level could be interpreted as a sign

of declining growth to come in terms

of total contributions. While we think

this will likely be the case, there

are a couple of factors to consider

that could affect that outcome.

Although leverage ratios have moved

incrementally lower, deals in 4Q 2015

appeared to have bucked this trend.

We’ve mentioned before that many

of the transactions that closed during

-$400

-$300

-$200

-$100

$0

$100

$200

$300

$400

$500

$600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Total Contributions ($B) Total Distributions ($B) Net Cash Flow ($B)

Source: PitchBook

*As of 9/30/2015

Global PE funds’ net cash flows

11 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

YEAR TOTAL CONTRIBUTIONS ($B)

TOTAL DISTRIBUTIONS ($B)

NET CASH FLOW ($B)

2001 ($39.9) $21.1 ($18.7)

2002 ($56.0) $19.4 ($36.6)

2003 ($54.4) $46.0 ($8.5)

2004 ($74.0) $106.3 $32.3

2005 ($93.5) $107.5 $14.0

2006 ($150.0) $122.0 ($28.0)

2007 ($199.8) $141.7 ($58.1)

2008 ($204.7) $76.8 ($127.9)

2009 ($100.0) $46.3 ($53.7)

2010 ($148.7) $127.5 ($21.2)

2011 ($147.9) $162.1 $14.2

2012 ($158.4) $234.6 $76.2

2013 ($139.7) $253.0 $113.4

2014 ($169.5) $307.0 $137.5

2015* ($131.4) $200.9 $69.4

Source: PitchBook

*Data as of 9/30/2015

U.S. PE funds’ annualized cash flow by year

4Q were of higher quality, and that

deals of lesser quality were pushed

out of their target 4Q close periods

as negotiations ran long. Top-quality

deals were less affected by the debt

markets, so while equity portions

were lower for them, those deals also

closed at higher multiples, which

could offset any potential decline in

contributions growth simply due to

their larger transaction sizes. On the

other hand, we did see a move by

managers to source transactions in

the lower middle market. Closing such

deals in a lower-multiple environment

could certainly impact contributions as

managers would have had to call down

less from LPs to close these processes.

As we get complete 2015 data in a

couple of months, we’ll be able to get

a better picture of how the sluggish

2H 2015 market backdrop immediately

impacted LP cash flows and a better

grasp of what may be to come.

Source: PitchBook

*As of 9/30/2015

U.S. PE funds’ net cash flows

-$300

-$200

-$100

$0

$100

$200

$300

$400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Total Contributions ($B) Total Distributions ($B) Net Cash Flow ($B)

12 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

Venture Capital IRRs

Source: PitchBook

*As of 9/30/2015

Source: PitchBook

*As of 9/30/2015

Global VC horizon IRR by size bucket

VC horizon IRR by region

Much of the data on this page only

further reinforces longstanding

trends. In the medium term, larger

vehicles’ IRRs outpace those of their

smaller counterparts. In addition,

the surge in performance by recent

venture vintages has also been

remarked upon previously. It’s

rather impressive seeing just how

much top VC performers have been

driving that recent surge. The top

decile of 2010-2012 VC vintages are

posting IRRs near to or just eclipsing

50%. This is in part due to the recent

exit environment, so some will see

declines as time goes on, but the sheer

magnitude of the outperformance

should be emphasized, as it explains

the optimism of some VCs and

LPs that has withstood even the

global downturn, in terms of current

fundraising trends. Although some

VCs have been able to exit through

the aforementioned “private IPOs”,

some still remain invested in highly

valued late-stage companies, with

unclear paths to eventual, profitable

realizations.

For now, top VC funds of recent vintages are enjoying considerably lofty performance.

-5%

0%

5%

10%

15%

1-Year 3-Year 5-Year 10-Year

Under $100M $100M-$250M $250M-$500M $500M+

0%

5%

10%

15%

1-Year 3-Year 5-Year 10-Year

U.S. VC Funds Rest of World VC Funds

Global median VC IRR by vintage

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

VC Top Quartile VC Top Decile

Source: PitchBook

*As of 9/30/2015

13 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

VC Fund Return Multiples

Global average VC DPI multiples over time by vintage

Source: PitchBook

*As of 9/30/2015

Global median VC fund return multiples by vintage

Source: PitchBook

*As of 9/30/2015

More recent venture vintages

continue to see improvements

in key metrics, although implications

for long-term liquidity remain. The

TVPI multiples of several vintages

have risen yet again relative to the last

Benchmarking report, with 2009 in

particular seeing a surge from 1.49x to

1.60x. More promisingly for LPs, 2009

and 2010 vintages saw their median

DPI multiples increase considerably,

the former by 0.11x and the latter

by 0.17x. Given the relatively earlier

surge in average VC DPI multiples of

recent vintages, there are grounds for

optimism that many funds will make

good on the promise inherent in their

lofty TVPI figures. But there are also

grounds for concern. The timeline

for liquidity, particularly for the most

highly valued companies that have

helped push up those vintages’ paper

gains, has only been lengthening

as many companies opt to remain

private. Investors and consequently

LPs are having to wait longer to

see their money return, which has

potential negative implications for

future fundraising. Furthermore, in the

event of a global slowdown, realization

will only be more compromised, as

evidenced by how older vintages hit

by the recession have yet to unlock

much of their residual value. In short,

the sustained improvement in DPI

multiples is promising, but there

remains quite a ways to go for many

funds.

0.0x

0.1x

0.2x

0.3x

0.4x

0.5x

0.6x

0.7x

0.8x

1 2 3 4 5 6 7 8 9 10Years since inception

2004 2005 2006 2007 2008 2009 2010

0.81

x

0.92

x

0.83

x

0.40

x

0.63

x

0.43

x

0.56

x

0.32

x

0.32

x

0.43

x

0.03

x

0.13

x 0.16

x

0.22

x

0.45

x

0.59

x

0.69

x 0.85

x

0.97

x

1.12

x 1.16

x

1.14

x

1.17

x1.13x

1.17x 1.24x

1.05x

1.27x1.40x 1.35x

1.52x 1.60x 1.62x

1.26x 1.21x

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Median of DPI Median of RVPI Median of TVPI

14 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

VC Fund Cash Flows

Global VC funds’ annualized cash flow by year

YEAR TOTAL CONTRIBUTIONS ($B)

TOTAL DISTRIBUTIONS ($B)

NET CASH FLOW ($B)

2001 ($31.7) $13.2 ($18.5)

2002 ($26.5) $12.2 ($14.3)

2003 ($25.3) $32.0 $6.7

2004 ($30.5) $9.2 ($21.3)

2005 ($31.0) $13.7 ($17.3)

2006 ($40.8) $26.6 ($14.1)

2007 ($43.8) $32.5 ($11.2)

2008 ($43.5) $13.1 ($30.4)

2009 ($33.5) $14.5 ($19.0)

2010 ($39.6) $27.0 ($12.6)

2011 ($46.4) $32.3 ($14.0)

2012 ($42.8) $38.9 ($3.9)

2013 ($43.2) $41.6 ($1.6)

2014 ($34.8) $55.6 $20.8

2015* ($40.8) $46.4 $5.6

Source: PitchBook

*Data as of 9/30/2015

With only one quarter to go,

venture distributions back to LPs

in 2015 may well match the immense

tally of $55.6 billion in 2014. Since the

prior installment of this report series,

global distributions grew from $35.4

billion to $46.4 billion; if this pace

is maintained, then 2015 could crest

at well over $55 billion. Depending

on the flow of contributions, which

will subside given the decrease in VC

investment activity in the back half of

2015, last year may also end up with

positive net cash flow, making 2014

and 2015 the only back-to-back net

positive years in our datasets. Above

all else, these sums speak to how

successfully some fund managers

have been capitalizing on elevated exit

activity, as well as the considerable

incentive for LPs to recommit or

make a new commitment in hopes of

capturing a portion of those immense

gains. They should be or are likely

anticipating a timeline of considerable

length as well as relatively lesser

returns, however, given what has

transpired in the global venture capital

market recently. In the U.S., venture-

backed exits have fallen for several

quarters. Strategics’ appetite for

startups or other relatively young, VC-

backed companies is waning, which

could lead to diminishing distributions

in the future.

-$60

-$40

-$20

$0

$20

$40

$60

$80

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Total Contributions ($B) Total Distributions ($B) Net Cash Flow ($B)

Source: PitchBook

*Data as of 9/30/2015

Global VC funds’ net cash flows

15 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

Fund name Vintage IRR DPI

VSS Structured Capital II 2009 26.34% 1.47x

ICG Minority Partners Fund

2008 24.80% 1.66x

Fortress Investment Fund III PIK Notes

2009 20.24% 1.53x

Blackstone/GSO Capital Opportunities Fund II

2012 19.62% 0.41x

ABRY Senior Equity III 2010 17.60% 1.30x

Capital Royalty Partners II

2011 16.00% 0.36x

ICG Europe Fund V 2012 14.50% 0.16x

Select Top Funds by IRR 2008 to 2012 vintage mezzanine funds

Fund name Vintage IRR DPI

Baring Asia Private Equity Fund III

2005 53.08% 1.95x

JMI Equity Fund V 2005 39.50% 4.95x

Insight Venture Partners V

2005 21.00% 2.03x

RLH Investors II 2007 20.20% 1.93x

Insight Venture Partners VI

2007 20.20% 1.67x

Olympus Growth Fund V 2007 17.66% 0.60x

Aurora Resurgence Fund 2008 17.00% 0.55x

2004 to 2008 vintage growth funds 250M+

Fund name Vintage IRR DPI

Foundry Group Select Fund

2013 70.91% 0.37x

Institutional Venture Partners XIV

2012 61.66% 0.24x

Union Square Ventures Opportunity Fund

2010 56.99% 2.05x

Orbimed Private Investments IV

2010 39.10% 0.79x

Institutional Venture Partners XII

2007 27.20% 2.08x

Aisling Capital III 2008 24.15% 0.92x

2007 to 2013 vintage late-stage VC funds

Fund name Vintage IRR DPI

General Catalyst Group VI

2011 58.65% 0.00x

Third Rock Ventures Fund II

2010 47.59% 0.82x

Polaris Venture Partners VI

2011 34.51% 0.26x

Battery Ventures IX 2010 33.60% 0.55x

Spark Capital III 2010 33.17% 0.80x

MPM BioVentures V 2010 30.48% 1.10x

2009 to 2012 vintage Boston metro VC funds

Fund name Vintage IRR DPI

EnCap Flatrock Midstream Fund III

2014 46.51% 0.30x

POEP Co-invest 2012 31.81% 0.47x

EnCap Flatrock Midstream II

2012 26.36% 0.47x

Energy & Minerals Group Fund II

2011 25.76% 0.17x

Post Oak Energy Partners

2012 24.44% 0.60x

Rockland Power Partners II

2013 21.30% 0.00x

2011 to 2014 vintage energy funds

Fund name Vintage IRR DPI

Shamrock Capital Growth Fund III

2011 97.30% 2.18x

Vista Foundation Fund 1 2009 40.00% 1.90x

Levine Leichtman Capital Partners SBIC Fund

2011 34.10% 0.30x

Evergreen Pacific Partners II

2008 21.87% 0.66x

Vista Equity Partners Fund IV

2011 21.49% 0.41x

Ares Corporate Opportunities Fund III

2008 21.28% 0.88x

2008 to 2011 vintage U.S. West Coast buyout funds

Source: PitchBook Source: PitchBook

Source: PitchBook

Source: PitchBook

Source: PitchBookSource: PitchBook

Note: The funds return data on this page is as of 5/12/2016. Boston metro includes Waltham and Cambridge.

16 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

PitchBook currently tracks over 34,000 funds

around the world and has returns data on close

to 8,300 vehicles. In this edition of the quarterly

Benchmarking Reports, PitchBook examines

data from over 5,600 funds and 24,000

distinct LP commitments. We are constantly

adding historical performance data as it

becomes available; this explains many apparent

discrepancies that may appear between reports.

All returns data in this report is net of fees

through 3Q 2015, as reported by LPs.

DEFINITIONS

PE fund:

Unless otherwise noted, PE fund data includes

buyout, growth, co-investment, mezzanine,

restructuring and energy funds.

Debt fund:

For this report, the debt fund classification

includes general debt, mezzanine and distressed

debt.

Vintage year:

The vintage year as reported by the fund GP and

LPs, or the year in which a fund holds its final

close.

Internal rate of return (IRR):

IRR represents the rate at which a series of

positive and negative cash flows are discounted

so that the net present value of cash flows equals

zero.

Horizon IRR:

Horizon IRR shows the IRR from a certain point

in time. For example, the one-year horizon IRR

figures in this report show the IRR performance

for the one-year period from 3Q 2014 to 3Q

2015, while the three-year horizon IRR is for the

period from 3Q 2012 to 3Q 2015.

Distributions to paid-in (DPI):

A measurement of the capital that has been

distributed back to LPs as a proportion of the

total paid-in, or contributed, capital. DPI is

also known as the cash-on-cash multiple or the

realization multiple.

Remaining value to paid-in (RVPI):

A measurement of the unrealized return of a

fund as a proportion of the total paid-in, or

contributed, capital.

Total value to paid-in (TVPI):

A measurement of both the realized and

unrealized value of a fund as a proportion of

the total paid-in, or contributed, capital. Also

known as the investment multiple, TVPI can be

found by adding together the DPI and RVPI of

a fund. As the charts depict medians of fund

return multiples that are calculated based on

aggregated statistics, they may not necessarily

add up, whereas on an individual basis they

shall.

Methodology

17 PITCHBOOK GLOBAL PE & VC BENCHMARKING & FUND PERFORMANCE REPORT

SPONSORED BY

Contact PitchBook

pitchbook.com

RESEARCH [email protected]

EDITORIAL [email protected]

SALES [email protected]