Embed Size (px)

Citation preview

Behavioural FinanceASSOCIATE PROFESSOR JOANNE EARL

OCTOBER 2019

Acknowledging my research

partners

My Brief Today

• Converting plans into reality – understanding

factors that contribute to likely success

• Impact of cognitive decline in decision making –

how will people know if they are impacted?

• Differences in perceptions of what wealth and

poverty means.

• Factors affecting whether or not people plan

Key Concepts

Retirement• A process rather than an event• A career phase representing the repositioning of

work

Career• A person’s course or progress through life • The engagement of the individual with society

through involvement in the organisation of work

New concepts to impress your

friends

Work Centrality

Conditions of Exit

Mastery

FACTORS CONTRIBUTING TO

SUCCESS

WHAT IS SUCCESS?

11th October 2019

When we think about retirement….

Being well adjusted...more of this

8

• I am well adjusted to the changes

• I enjoy being retired

• I am busy

• Retirement has been better than I expected

• (If married or partnered) I enjoy being able to

spend more time with my spouse/partner

Being well adjusted…less of this

9

• I have real concerns about my financial situation

• I miss the stimulation that work gave me

• I wish I had started to plan for retirement earlier

• I miss the discipline that working gave me

• People don’t respect me as much now that I am

retired

• I have had to adjust to a big drop in my income

• I miss being part of the action

• Retirement has not lived up to my expectations

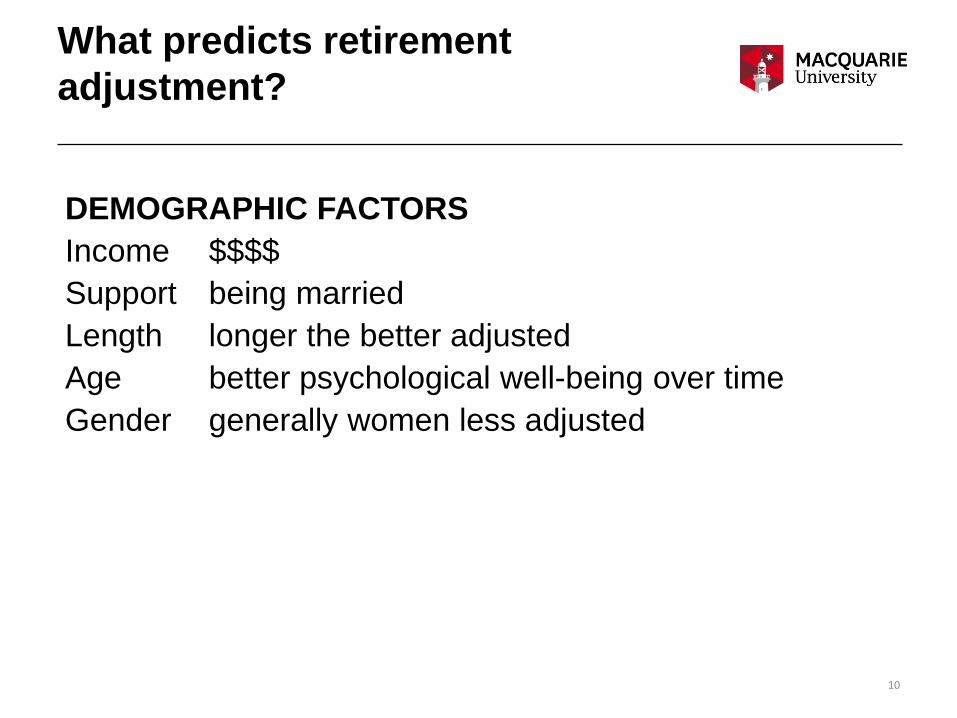

What predicts retirement

adjustment?

10

DEMOGRAPHIC FACTORS

Income $$$$

Support being married

Length longer the better adjusted

Age better psychological well-being over time

Gender generally women less adjusted

What predicts adjustment in

retirement?

11

ORGANIZATIONAL FACTORS

• Conditions of Exit

PSYCHOLOGICAL FACTORS

• Work Centrality

• Mastery

• Pre and post retirement planning

• Resource Accumulation

Dynamic Resources Model of

Retirement

12

DYNAMIC RESOURCE THEORY

• Our focus may be trained to be on Finances

• Interrelationships between the resources make it

impossible not to consider other influences such as

health, social support, cognitive skills, emotional

resilience and goal setting.

FINANCES HEALTH

Dynamic Resources Model of

Retirement

14

FINANCES

• Financial support to

cover family living

expenses

• personal savings

• investments

• superannuation

Dynamic Resources Model of

Retirement

15

HEALTH

• Absence of major

physical illnesses and

mental disorders

• Energy to carry out daily

activities or activities of

interest

Dynamic Resources Model of

Retirement

16

SOCIAL

• Friends and family

members

• Exchanging information

with others

• Getting emotional support

from others

• Tangible and practical

support (meals, chores,

repairs, transport)

Retirement in AustraliaTIMING: WHEN TO LEAVE AND WHY

Not as straight forward as you’d think – a lot of people

get it wrong

- 54% expect to live off Superannuation – reality is

33%

- 25% expect to live off Pension – reality is 49%

- 177,500 retired and then back out looking for work

- 37% full-timers plan to transition to part-time work

Source: ABS, 2017, Retirement Intentions Release No: 6238

With the help of…..

HOW MUCH DO I NEED TO RETIRE?

WHAT WILL I DO?

WILL MY HEALTH LAST?

19

Dynamic Resources Model of

Retirement

WHY DO I WANT TO LEAVE WORK?

WILL I BE HEALTHY ENOUGH?

HOW MUCH WILL I HAVE?

20

Dynamic Resources Model of

Retirement

21

Dynamic Resources Model of

Retirement

CAREERS

ADVISER

HEALTH

ASSESSMENT

FINANCIAL

ADVISER

Understanding

cognitive decline

WHY DOES IT

MATTER?

11th October 2019

What is dementia?Major and mild neurocognitive disorders (NCD):

• Alzheimer disease (50 – 75%) most common among older people,

especially women. Indications are short-term memory loss, apathy

and depression.

• Vascular dementia (20 – 30 %) usually caused by cerebrovascular

conditions such as strokes. Indicators include short term memory

loss and mood fluctuations.

• Frontotemporal dementia (5 - 10%) more common amongst men

and associated with early onset. Marked by mood and personality

changes, language problems and disinhibition.

• Dementia with Lewy bodies (5%). Characterised by a more rapid

onset than Alzheimer's. Presents similar to Parkinson’s disease, as

well as fluctuations in cognitive ability and visual hallucinations.

65 years

85 years

“The decade to 2020 will see the largest growth in

people with dementia (39%)”

Source: www.health.gov.au/dementia

Prevalence

Size of the Problem

• “These issues are a time bomb waiting to go

off if not addressed now”

• “….there is a risk that some with diminished

capacity to effectively manage their fund, may

nevertheless continue to do so.

• “Most don’t have a plan for what to do if they

get to this point”

Matt Bambrick, Assistant Commissioner, Self-Managed

Superannuation Funds Segment, ATO, Mar 2015

Mastery and Cognition

Mastery and Cognition related? Yes

• Increased errors on measures of cognition

related to lower levels of mastery

Evidence of withdrawal

Understanding the

difference between wealth

and poverty

IT’S NOT JUST ABOUT

THE MONEY

11th October 2019

When we think about retirement….

Gross household income

0% 10% 20%

$7,799 or less

$7,800 - $12,999

$13,000 - $18,199

$18,200 - $25,999

$26,000 - $33,799

$33,800 - $41,599

$41,600 - $51,999

$52,000 - $62,399

$62,400 - $72,799

$72,800 - $88,399

$88,400 - $103,999

$104,000 - $129,999

$130,000 - $155,999

$156,000 - $181,999

$182,000 - $207,999

$208,000 or more

Proportion of people (N=558)

0% 10% 20% 30%

$7,799 or less

$7,800 - $12,999

$13,000 - $18,199

$18,200 - $25,999

$26,000 - $33,799

$33,800 - $41,599

$41,600 - $51,999

$52,000 - $62,399

$62,400 - $72,799

$72,800 - $88,399

$88,400 - $103,999

$104,000 - $129,999

$130,000 - $155,999

$156,000 - $181,999

$182,000 - $207,999

$208,000 or more

Comfortably well off (45%)

Just enough (49%)

Not enough (6%)

Perceptions of wealth

Understanding who plans

AND WHO

DOESN’T…….

11th October 2019

Key Problems

• Not enough people plan

• People plan to leave for the wrong

reasons

• People make grand plans but do they

translate into reality?

Planning to work?

34

Self- insurance

Planning to work?

35

Self- protection

Who plans? For what?

36

Contact [email protected]