Embed Size (px)

Citation preview

The New Normal - living with continuous regulatory change in the financial markets

BCBS239: the behemothlumbers on

2 © GFT 2015

Introduction

Across the financial system, Global Systemically Important

Banks (G-SIBs) are continuing to wrestle with the

regulatory behemoth that is BCBS239 as they near the

compliance deadline. More so than many regulations, the

sheer size and scale of BCBS239 makes it a particularly

daunting challenge for banks to overcome. Annual

budgets of tens of millions of dollars, and total programme

costs typically in the 50 to 150 million dollar range attest

to the scale of the challenge. With the January 2016

deadline rapidly approaching, there still remains a very

large question mark over the extent to which G-SIBs will be

compliant.

In January 2015, the Basel Committee on Banking

Supervision published its second report on the progress

made by the G-SIB banks in their attempts to comply with

the 11 banking Principles of BCBS239. The report, entitled

“Progress in adopting the principles for effective risk data

aggregation and risk reporting” provides an update and a

report on progress towards the 11 Principles set out in the

January 2013 BIS Document.

Although generally improvements have been made since

the first progress report was released in December 2013,

some banks have reported a downgrade in their ability to

meet compliance requirements. 14 of the 31 G-SIBs said

they would be unable to comply with at least one of the 11

Principles by January 2016.

The picture that emerges is one where many banks

are struggling to establish strong governance, data

aggregation, architecture and processes. BCBS239

requires the implementation of large-scale, global strategic

IT infrastructure, which is difficult enough, but also needs

the cultural, business process and governance changes to

support it. The BIS has also highlighted the concern that

many banks continue to rely on manual workarounds to

achieve compliance.

Despite the mixed response from some banks, many

still believe that full compliance will be possible by

January 2016. With so much still to be achieved, is this a

sign of overconfidence? It is likely that banks may have

overestimated their predicted levels of compliance, and

what is now required is a thorough and honest appraisal

by each individual G-SIB on what they still need to do to

comply with BCBS239.

The challenges facing G-SIBs

The origins and drivers of BCBS239 can be traced

back to the 2008 financial crisis; as a response to the

analysis and interrogation that inevitably followed. At the

height of the crisis, it became apparent that banks were

unable to aggregate data quickly or effectively enough,

preventing them from identifying risk exposures and acting

appropriately on them. As the crisis unfolded, their ability

to make appropriate business decisions was compromised

by data quality issues and their inability to aggregate risk

information quickly and accurately.

The Principles of BCBS239 require banks to strengthen

their risk data aggregation capabilities and internal risk

reporting practices. If banks are going to comply with

these Principles by the January 2016 deadline, they need

urgently to review their current governance structures,

data architectures, IT infrastructure and capabilities, as well

as think about the overall culture that exists within their

individual institution towards data and risk analysis.

The self-assessments by the G-SIBs clearly show how

difficult complying with the Principles has proven to be.

The size, scope, and complexity of this regulation pose

a set of unique challenges, on top of other local and

regional regulations that banks are already tackling. The

self-assessments demonstrate that there is still much to be

accomplished, including: addressing the heavy reliance on

manual processes and tactical fixes, creating consistent

documented processes for the aggregation of risk data

at the Group level, improving the handling, aggregation

and proper accounting of collateral, and improving

the reconciliation and control processes for risk data

aggregation. The question now is whether G-SIBs have

enough time remaining to comply with the deadline, and if

their remediation programmes are currently delivering the

required changes to make this happen.

BCBS239 is a “non-prescriptive” regulation; the onus is

on the banks to decide how they intend to interpret the

Principles as well as set and defining their own minimum

standards for compliance. By way of a motoring analogy,

if banks are driving along the road towards a destination

called “BCBS239 Compliance”, each G-SIB is currently

at a different stage of the journey, with some having

much further to travel than others. For some, they are still

struggling to determine exactly where “Compliance” is on

the map, or the best route to get there!

3 © GFT 2015

With the growing awareness that time is running out,

there is increasing pressure to simply meet the “letter

of the law” (i.e. to tick the boxes for compliance), rather

than to embrace the full spirit of the regulation as hoped

for by BIS; with banks seeking to implement significant

operational and cultural change in the management

of their risk data. With limited time remaining, it is very

likely that many of the G-SIBs will now only be capable

of achieving the minimal standards for compliance, with

many manual workarounds and legacy issues to be

resolved at a later date.

Problematic areas for compliance

¬ Governance structures

BSBS239 states that banks should have in place strong

governance frameworks. However, achieving this

has proven highly problematic. A robust governance

framework should be the foundation which banks can

use to help build their BCBS239 solution – without this,

compliance becomes increasingly difficult to achieve.

Due to their size, G-SIBs will naturally face many

challenges relating to their data architectures and the

roles and responsibilities associated with this architecture.

Poor quality data can be linked to the existence of many

data sources and formats with perennial questions about

formats, data quality, SLAs and ownership. Improved

governance is vital, but it also requires G-SIBs to define

clear data standards, identifying where high quality data

comes from and what it should look like. G-SIBs need to

document exactly how their data is managed in terms of

the processes, controls, responsibilities and reporting.

Mapping the “data lifecycle” and making it accessible and

available to relevant stakeholders will be vital.

A key aspect, however, is that governance structures

are not just robust, but flexible. Banks must be able to

aggregate data across different entities, business lines

and risk types, not simply for a particular point in time,

but to evolve over time and keep up with business, legal

and regulatory changes. Significantly more flexible data

architectures must be in place to allow for real-time and

ad-hoc reporting in both normal and stressed conditions,

such as the 2008 global financial crisis.

¬ Risk data activities

Risk data management has been raised by BCBS239 to a

new level. During the financial crisis, it became clear that

weak risk data aggregation, reporting capabilities and

an overreliance on manual processes were major issues.

Many of the limitations and deficiencies in these areas

arose because firms had numerous, disparate data sources

using different formats, technologies, nomenclature and

data quality assurance processes. These problem areas

were highlighted in the most recent progress report, with

8 firms reporting that they would not be fully compliant on

Principle 3 (Accuracy and integrity).

Key elements of compliance on Principle 3 will include

improved and more robust quality assurance processes

and the introduction of standardised taxonomies and

data protocols.

Ultimately, improved risk data will help banks improve their

decision-making, identifying where their exposures lie and

reporting this data as quickly as possible to those who can

do something about it. For example, with better visibility of

aggregated risk data, a risk manager could identify issues

quickly, before they become problems. The recent Russian

debt crisis provides a classic example, whereupon many

firms were unable to understand their exposure to the

problem, and were therefore unable to do anything about

it.

¬ Information technology

High quality data aggregation cannot be achieved

without the appropriate information technology (IT) and

data architecture. The regulators reported that during

the financial crisis, the IT systems and data architectures

found in many banks were inadequate to support the

management of financial risk. The regulators noted that

those institutions which had better risk data management

processes were the ones that had the appropriate

technology, and platforms in place to help them analyse

their risk data better.

BCBS239 will stimulate the need to reassess existing

legacy systems and technology and consider whether

firms can deliver data in the required format to answer the

questions being asked of them. This will require major IT

infrastructure projects for many G-SIBs, which may include

updating or replacing core legacy systems, to avoid

leaving themselves a looming “technical debt” for the

future.

4 © GFT 2015

¬ Legacy technologies

Updating embedded legacy systems is, however, no easy

task, and will inevitably lead to an increase in spending by

banks on their risk aggregation technology. The level of

investment required and the scale of projects deployed

will depend on how entrenched the legacy platforms are

and the selection of appropriate replacements. These

challenges are compounded by the need to continue to

meet bank risk and reporting obligations, while at the

same time overhauling their legacy technologies.

¬ Manual workarounds

The 2015 progress report revealed that G-SIBs are

continuing to rely heavily on manual workarounds to deal

with the demands of complying with BCBS239. Manual

workarounds and tactical mitigants are typically major

constraints on the flexibility, adaptability and operational

robustness of BCBS239 solutions. Although manual

workarounds and tactical mitigants (such as end-user

applications) are sometimes difficult to avoid, it must be

remembered that they increase “process debt” which

carries a heavy penalty to be paid at some point in the

future.

As with any debt which accumulates over time with a

crippling rate of interest, technical and process debt can

reach unmanageable proportions as complexity rises

unabated. This situation increases the potential risk to the

firm and also inflates the cost to eventually make a more

strategic change in future. G-SIBs have been advised to

“simplify their current IT architecture and data flows across

departments and legal entities” in order to streamline the

aggregation process and to enable quick aggregation

of risk data during times of stress. However, with such

embedded systems and processes, accumulated over

many years, this is easier said than done.

Banks need to understand and monitor closely the amount

of technical and process debt they are storing up for the

future, and ensure that there are plans and a budget in

place to address this challenge. One such plan would be to

include implementation debt assessment and remediation

strategies into regular technical and business audits.

¬ Leadership requirements

Delivering the projects required for BCBS239 compliance

requires effective leadership within every G-SIB. The 2015

progress report recommended greater engagement from

senior management and boards of directors, and more

awareness of the risk and data aggregation capabilities

within each bank.

Senior management and board members have to start

thinking differently about risk data management. They

need to create a culture where everyone begins to think

about data in a more in-depth and holistic way. Senior

management has to understand the value of IT and data

and demonstrate to all stakeholders how it impacts on

the ability to make better business decisions, as well as

meeting the requirements of BCBS239 compliance.

Board members should take an active interest in, and

responsibility for, the data quality and aggregation

capabilities which ultimately underpin risk management

strategy and decision-making. Accountability for risk is not

something that can be delegated; ultimate responsibility

for risk management sits with the board and executive

committee members.

Senior management needs to monitor and engage more

actively in the delivery of projects, paying close attention

to the progress and to become cognisant of trade-offs in

terms of “strategic” versus “tactical” approaches, as well as

the long term viability and robustness of solutions. As with

many regulatory change initiatives, BCBS239 has too often

been viewed simply as an issue for IT to resolve.

This thinking has to change. The ability to store, deliver

and report the required risk data is intrinsically linked

to the IT capabilities within each bank, but senior

management should be seeking to develop a framework

that allows them to work more collaboratively with IT

stakeholders to create effective policies and strategies

for risk management. Board members should be directly

involved in assessing whether the project implementation

is on track, as well as identifying and enabling the timely

resolution of any obstacles to implementation. It requires

those in IT departments and those managing data to

think about IT along business lines rather than in an

organisational silo.

5 © GFT 2015

What has been the North American

experience?

Historically, BCBS239 has not been not high on the

agenda for US domestic banks, compared with their

European counterparts, yet the more vigorous action-

oriented approach of American regulators has already

provided strong incentives to make progress on some

BCBS239 Principles.

OCC Enforcement Actions have been very effective in

forcing compliance, with recent examples touching on data

aggregation principles. Interestingly, these enforcement

actions tend to be quite specific, and also call for

Executive Committee and sometimes board involvement in

supervision and monitoring.

What can D-SIBs learn from the

G-SIB experience?

Under the BCBS239 guidelines, D-SIBs are not required

to implement BCBS239 by January 2016, but the Bank for

International Settlements (BIS) recommended that regional

regulators apply a three year timeframe for compliance,

commencing with the individual organisations’ designation

as a D-SIB. Since the regulators’ recognition of D-SIBs is

not a globally synchronised process, there is a blurring of

timelines, but D-SIBs are now beginning to budget, plan

and mobilise their BCBS239 programmes.

Starting from scratch, and with three years to implement,

D-SIBs should be able to take advantage of the

experiences and lessons learned by many of the G-SIBs,

such as not launching a programme without clear data

taxonomies or governance processes, and ensuring

attention is paid to the proper inclusion of collateral in the

programme. By avoiding these costly mistakes, using time

and budget more efficiently, and ensuring that appropriate

tools, processes and accelerators are utilised, D-SIBs can

reduce project risk and aim for a better quality and more

timely end result.

Moreover, D-SIBs who seize the opportunity to get it right

the first time will also be able to avoid the near-ubiquitous

tactical mitigants and manual processes found in the

approach of G-SIBs. They can focus on strategic build,

rather than burden themselves with costly technical and

process debt for years to come.

In sharp contrast to the majority of G-SIBs, it is even

possible that some D-SIBs will realise the gains in

efficiency, reduced probability of losses, enhanced

strategic decision-making, and increased profitability cited

by the BIS as the core benefits of improving their risk data

aggregation capabilities.

The challenges and problem characteristics for D-SIBs

are of course different from G-SIBs. However, D-SIBs are

smaller and typically less complex than G-SIBs, with fewer

distinct entities and source systems, so the scale of the

costs and challenges are reduced and, in principle at least,

more easily managed. On the other hand, D-SIBs will also

generally be more sensitive to budgetary pressures and

cost of ownership. In addition, D-SIBs will not necessarily

have the large regulatory change and execution teams

required to undertake this ambitious and far-reaching

regulatory project.

D-SIBs who undertake BCBS239 programmes with a more

strategic approach, and pay close attention to the painful

lessons learned by G-SIBs, should be able to reduce

risks and project costs, and achieve compliance, but an

integrated risk aggregation platform which adds value.

Conclusion

On 1st of January 2016 what can we expect to find? Will the

G-SIBs be in a position to confidently say they have met all

the Principles asked of them, or will they be desperately

seeking an extension from the regulators? It is clear from

the progress report that many banks do not expect to

achieve full compliance and they will likely have significant

additional remediation and implementation activities

beyond this date.

G-SIBs with outstanding items will then need to

demonstrate adherence to agreed plans that specifically

focus on those areas that need urgent attention, and they

will risk regulatory censure or penalties if they fail to meet

their commitments.

6 © GFT 2015

Succeeding with BCBS239

The key to success for any firm should begin with senior

management taking the lead in embracing the importance

and value of risk data management within each institution.

Those firms who succeed not only in complying by the

deadline, but also improving their strategic aggregation

and management of their risk, will be those that:

1. Embrace the strategic opportunity for change

and ensure appropriate strategy, commitment

and investment

2. Implement a complete system of robust governance,

project supervision and reporting

3. Minimise manual workarounds for compliance,

thereby reducing their future technical debt, process

debt and end-user application policies

4. Establish risk data taxonomies, with consistent

documentation of the aggregation process

5. Include all collateral positions and sources in addition

to firm exposures

6. Implement robust reconciliation and data quality

control processes

We have seen that many firms faced by the huge

demands of BCBS239 and other competing regulations

rely heavily on manual workarounds and tactical

mitigants in order to comply with requirements. Such

solutions compromise long-term value and indeed can

work counter to the spirit and objectives of BCBS239.

Such firms should be identifying how they can make

the transition towards implementing more strategic

solutions.

Taking and managing risk is at the very core of banking,

so it is profoundly appropriate that firms should be able

to flexibly and accurately aggregate risk information.

Whether they are a G-SIB or a D-SIB, firms should

appreciate that BCBS239 is not simply another form of

regulation that requires compliance; it is an opportunity

to entirely re-evaluate their risk data aggregation,

management and reporting, ultimately leading to better

governance, better decision-making and improved

operational efficiency.

7 © GFT 2015

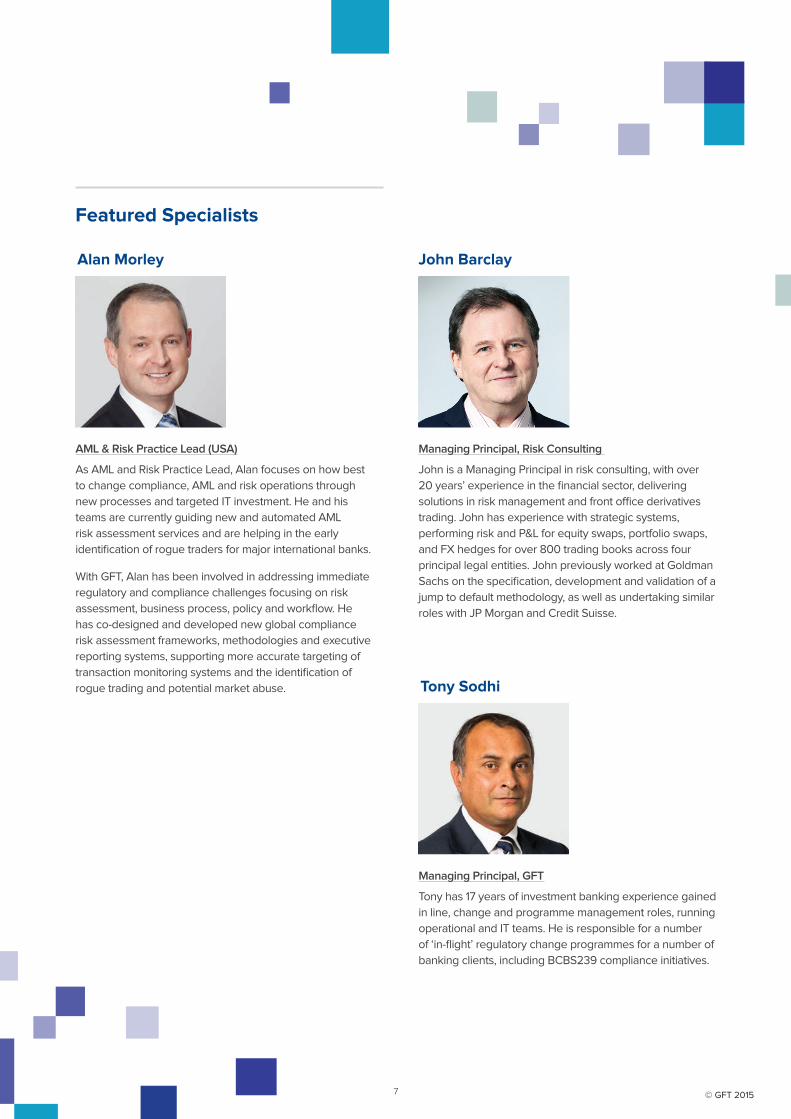

AML & Risk Practice Lead (USA)

As AML and Risk Practice Lead, Alan focuses on how best

to change compliance, AML and risk operations through

new processes and targeted IT investment. He and his

teams are currently guiding new and automated AML

risk assessment services and are helping in the early

identification of rogue traders for major international banks.

With GFT, Alan has been involved in addressing immediate

regulatory and compliance challenges focusing on risk

assessment, business process, policy and workflow. He

has co-designed and developed new global compliance

risk assessment frameworks, methodologies and executive

reporting systems, supporting more accurate targeting of

transaction monitoring systems and the identification of

rogue trading and potential market abuse.

Managing Principal, Risk Consulting

John is a Managing Principal in risk consulting, with over

20 years’ experience in the financial sector, delivering

solutions in risk management and front office derivatives

trading. John has experience with strategic systems,

performing risk and P&L for equity swaps, portfolio swaps,

and FX hedges for over 800 trading books across four

principal legal entities. John previously worked at Goldman

Sachs on the specification, development and validation of a

jump to default methodology, as well as undertaking similar

roles with JP Morgan and Credit Suisse.

Managing Principal, GFT

Tony has 17 years of investment banking experience gained

in line, change and programme management roles, running

operational and IT teams. He is responsible for a number

of ‘in-flight’ regulatory change programmes for a number of

banking clients, including BCBS239 compliance initiatives.

Featured Specialists

Alan Morley

Tony Sodhi

John Barclay

8 © GFT 2015

About GFT

GFT is one of the world’s leading solutions

providers in the finance sector offering

consulting, implementation and maintenance

for a broad range of IT applications.

Combining technological expertise and

seamless project management with a deep

understanding of the financial industry, GFT

is a reliable partner for well-known companies

all around the globe.

Headquartered in Germany, GFT has stood

for technological expertise, innovative strength

and outstanding quality for over 25 years.

› gft.com

This report is supplied in good faith,

based on information made available to GFT at

the date of submission. It contains confidential

information that must not be disclosed to third

parties. Please note that GFT does not warrant

the correctness or completion of the information

contained. The client is solely responsible for

the usage of the information and any decisions

based upon it.