Embed Size (px)

Citation preview

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 1/44

BY

Mrs. Shalu Dua Katyal

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 2/44

A business requires credit for the operationsof the business. Credit is generally requiredand supplied on short and long-term basis.The money market caters to short-termneeds only. The long- term capital needs are

met by Capital Market.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 3/44

Capital Market is a place where long-term

and medium term financial instruments aretraded. Thus it is a market for long termfunds- both equity and debts- and fundsraised within and outside the country. It

consists of a series of channels throughwhich the savings of the community are madeavailable for industrial and commercialenterprises.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 4/44

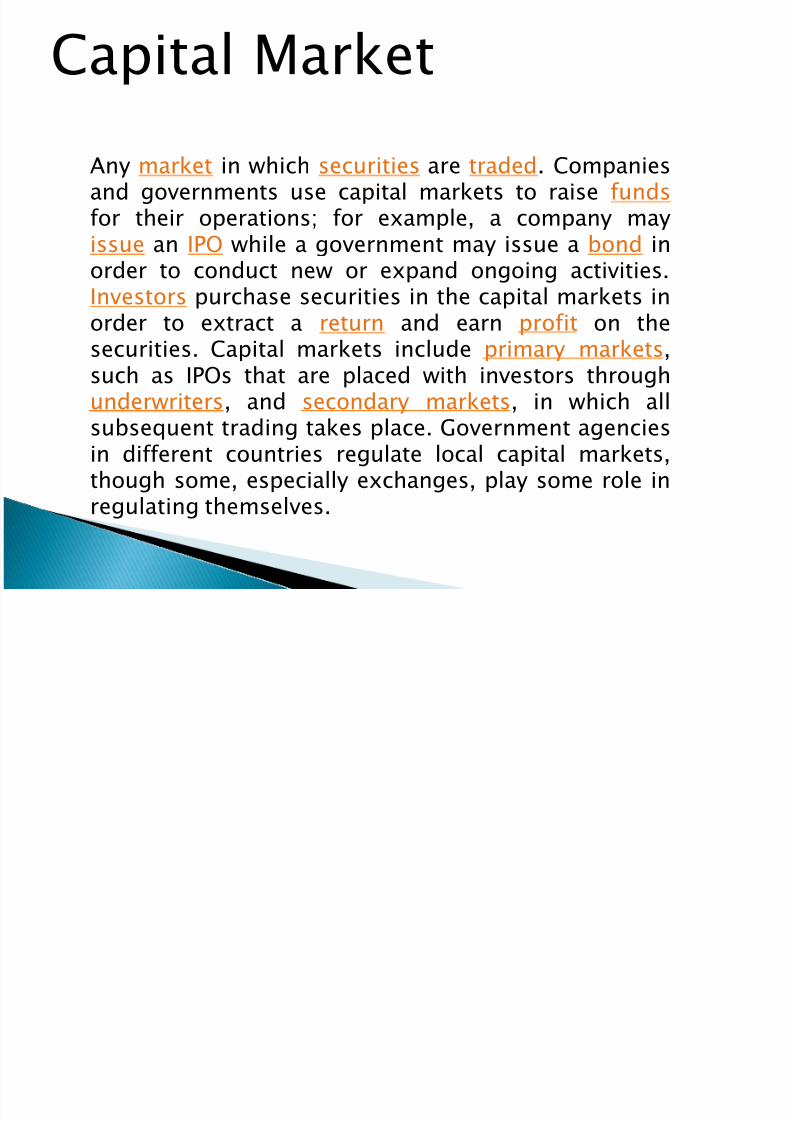

Any market in which securities are traded. Companiesand governments use capital markets to raise funds for their operations; for example, a company mayissue an IPO while a government may issue a bond in

order to conduct new or expand ongoing activities.Investors purchase securities in the capital markets inorder to extract a return and earn profit on thesecurities. Capital markets include primary markets,such as IPOs that are placed with investors throughunderwriters, and secondary markets, in which allsubsequent trading takes place. Government agenciesin different countries regulate local capital markets,though some, especially exchanges, play some role inregulating themselves.

Capital Market

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 5/44

Comprises Primary and Secondary Market Important constituents of the financial system. acts a link between savers and borrowers who need funds

to invest profitably and efficiently. helps firms to procure finances for long-term investments

such as buying plant & machinery, building, etc. obtains its funds through issue of various securities such

as equity shares, bonds, debentures and innovativesecurities like zero interest bonds and deep discountbonds.

functions thru’ various intermediaries such as

underwriters, bankers, stock brokers, etc. includes both individual investors and institutionalinvestors such as UTI, LIC, IDBI, etc

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 6/44

• Promotion of Industrial Growth• Mobilizing funds to meet Private and Public

company’s financial requirements.

• Raising long-term funds.

• Securing foreign Capital.

• Ready and continuous market

• Effective allocation of Financial Resources.

•

Hedging and reducing risks.• Helps in maintaining liquidity.

• Operational Efficiency.

Role of capital market

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 7/44

Screen-based trading Dematerialization of securities Shorter settlement cycle Foreign Institutional Investors Comprehensive Risk Management System Investor Protection Electronic Clearing services

Listing of securities Diversified Infrastructure Corporate Governance

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 8/44

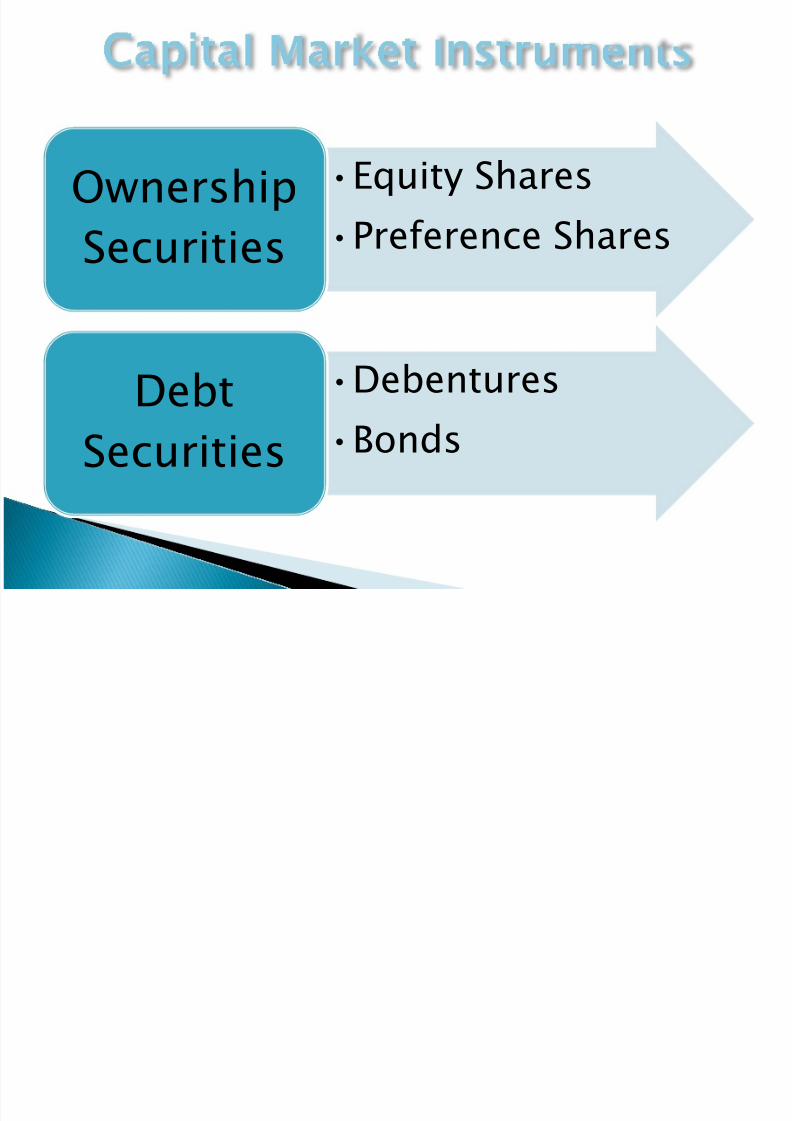

•Equity Shares

•Preference Shares

Ownership

Securities

•Debentures

•BondsDebtSecurities

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 9/44

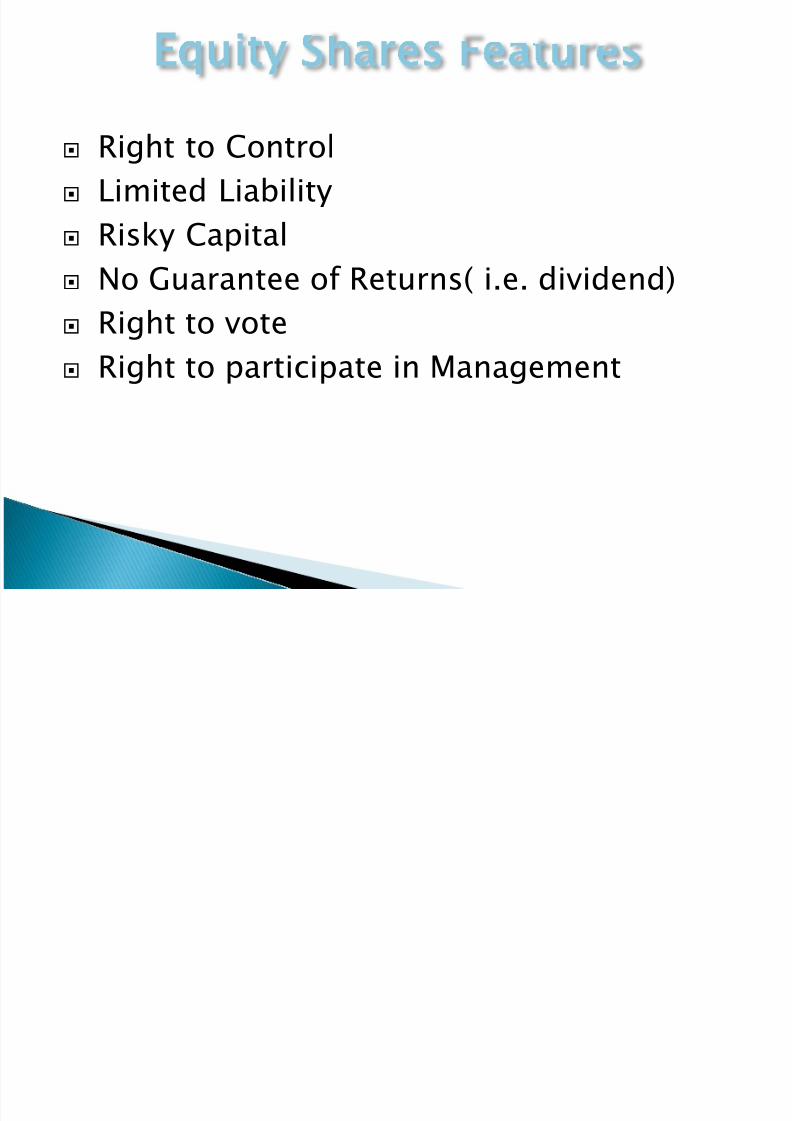

Right to Control

Limited Liability

Risky Capital

No Guarantee of Returns( i.e. dividend) Right to vote

Right to participate in Management

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 10/44

o Preference in dividends.

o Preference in assets in the event of

liquidation.o Convertible into common stock.

o No participation in management.

o Nonvoting.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 11/44

Cumulative

And

Non-cumulative

Redeemable

And

Irredeemable

Participating

And

Non-participating

Convertible

And

Non-Convertible

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 12/44

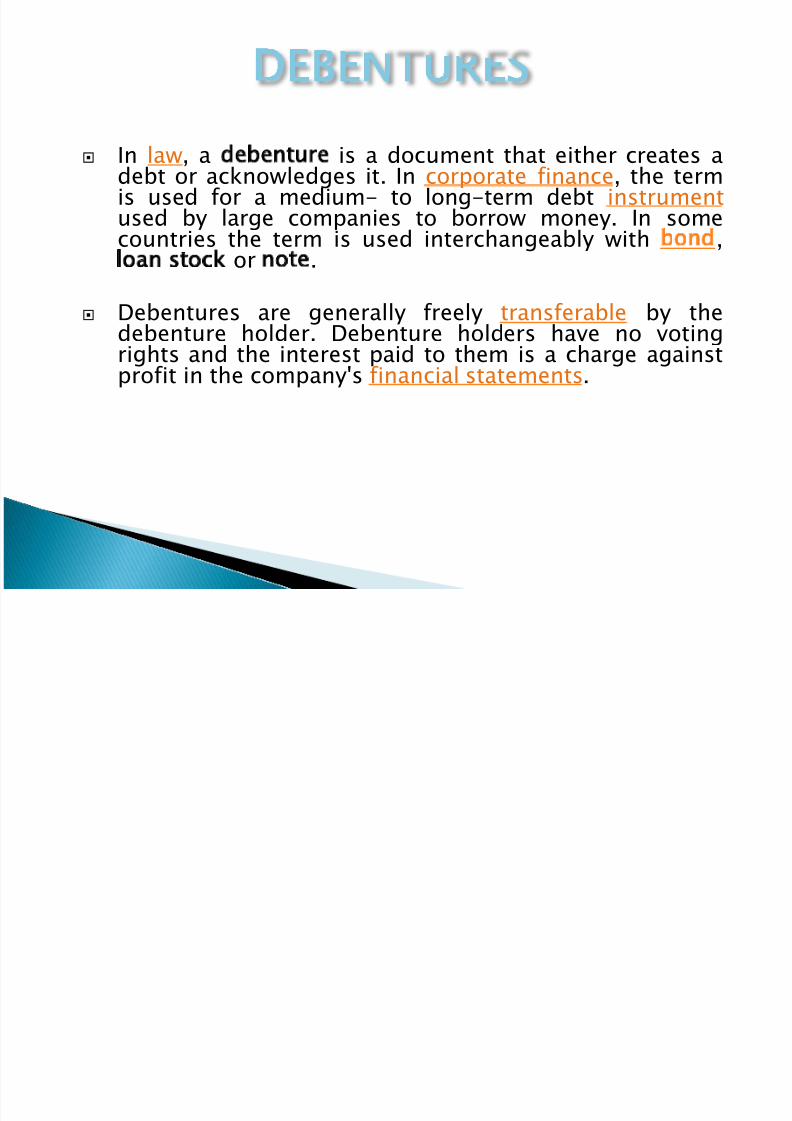

In law, a debenture is a document that either creates adebt or acknowledges it. In corporate finance, the term is used for a medium- to long-term debt instrument used by large companies to borrow money. In somecountries the term is used interchangeably with bond,loan stock or note.

Debentures are generally freely transferable by thedebenture holder. Debenture holders have no votingrights and the interest paid to them is a charge againstprofit in the company's financial statements.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 13/44

Lower and Fixed interest bearing securities. Fixed maturity.

Priority in repayment

No participation in management. Interest on debentures is a charge against

profits.

Flexibility in capital structure.

High stamp duty.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 14/44

Secured

And

Unsecured

Redeemable

And

Irredeemable

Convertible

And

Non-Convertible

Registered

And

Unregistered

Participating

And

Non-participating

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 15/44

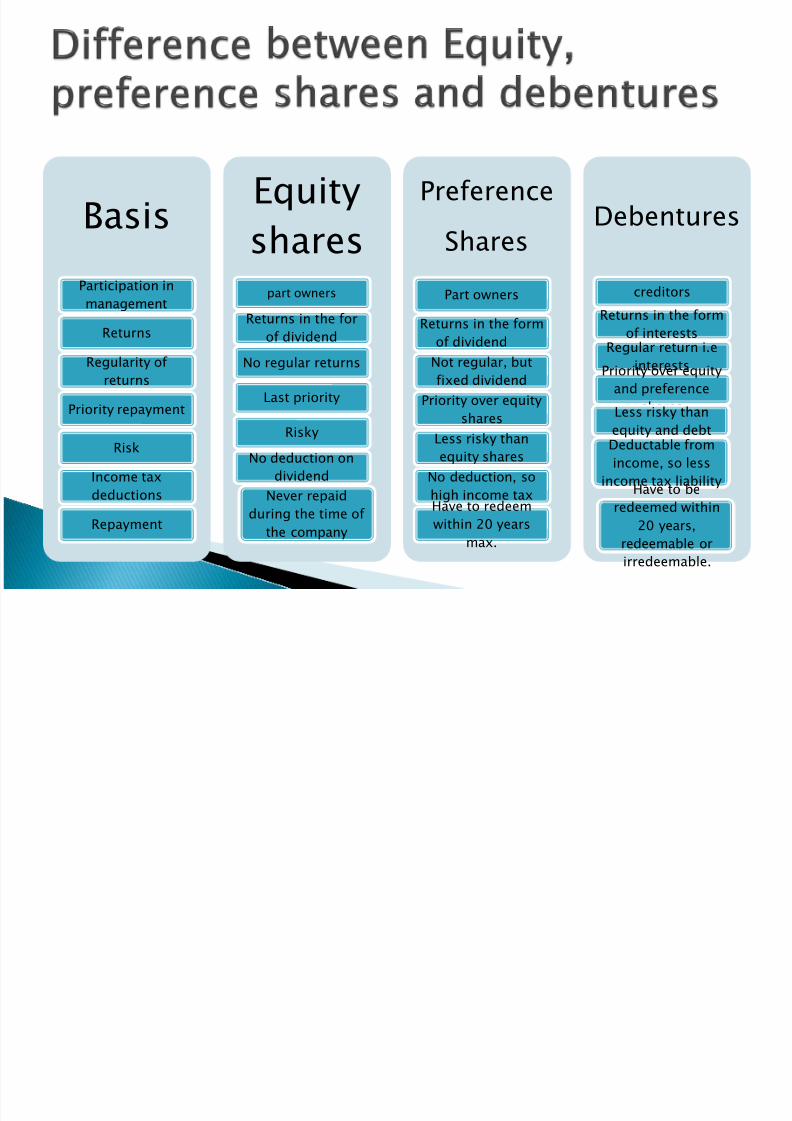

Basis

Participation in

management

Returns

Regularity of

returns

Priority repayment

Risk

Income tax

deductions

Repayment

Equity

sharespart owners

Returns in the for

of dividend

No regular returns

Last priority

Risky

No deduction on

dividend

Never repaid

during the time of

the company

Preference

Shares

Part owners

Returns in the form

of dividend

Not regular, but

fixed dividend

Priority over equity

shares

Less risky than

equity shares

No deduction, so

high income taxHave to redeem

within 20 years

max.

Debentures

creditors

Returns in the form

of interestsRegular return i.e

interestsPriority over equity

and preference

sharesLess risky thanequity and debtDeductable from

income, so less

income tax liabilityHave to be

redeemed within

20 years,

redeemable or

irredeemable.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 16/44

A Bond is a debt security, in which theauthorized issuer owes the holders a debtand, depending on the terms of the bond,

is obliged to pay interest (the coupon)and/or to repay the principal at a laterdate, termed maturity. A bond is a formalcontract to repay borrowed money withinterest at fixed intervals.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 17/44

PAR VALUE:-Amount paid to the stockholder on maturity of the bond.-Discount or premium

COUPON INTEREST:

-Annual/Semi-annual Naira interest paid to the bondholder

MATURITY DATE:-The date on which the issuer is obligated to pay thebondholder

SINKING FUND:-Periodical application of money towards redemption of thebonds before maturity.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 18/44

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 19/44

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 20/44

They are designed to meet the long termfunds requirements of the issuer andinvestors who are not looking forimmediate return and can be sold with along maturity of 25-30 years at a deepdiscount on the face value of debentures.

IDBI deep discount bonds for Rs 1 lakhrepayable after 25 years were sold at adiscount price of Rs. 2,700.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 21/44

The phrase `sweat equity' refers to equity shares given tothe company's employees on favorable terms, inrecognition of their work. Sweat equity usually takes theform of givingoptions to employees to buy shares of the company, sothey become part owners and participate in the profits,

apart from earning salary. This gives a boost to thesentiments of employees and motivates them to work harder towards thegoals of the company.The Companies Act defines `sweat equity shares' as equityshares issued by the company to employees or directors at

a discount or for consideration other than cash forproviding knowhow or making available rights in thenature of intellectual property rights or value additions, bywhatever name called.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 22/44

A negotiable certificate held in the bank of onecountry (depository) representing a specificnumber of shares of a stock traded on anexchange of another country. GDR facilitate tradeof shares, and are commonly used to invest in

companies from developing or emergingmarkets. GDR prices are often close to values of related shares, but they are traded and settledindependently of the underlying share.

If the depository receipt is traded in the United

States of America (USA), it is called an AmericanDepository Receipt, or an ADR. If the depositoryreceipt is traded in a country other than USA, it iscalled a Global Depository Receipt, or a GDR.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 23/44

A warrant is a security issued by companyentitling the holder to buy a given number of shares of stock at a stipulated price during aspecified period. These warrants are

separately registered with the stockexchanges and traded separately. Warrantsare frequently attached to bonds or preferredstock as a sweetener, allowing the issuer topay lower interest rates or dividends.

Ex-Essar Gujarat, Ranbaxy, Reliance issue thistype of instrument.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 24/44

This is a debt instrument that is fully convertedover a specified period into equity shares. Theconversion can be in one or several phases. Whenthe instrument is a pure debt instrument, interestis paid to the investor. After conversion, interestpayments cease on the portion that is converted.If project finance is raised through an FCD issue,the investor can earn interest even when theproject is under implementation. Once the

project is operational, the investor canparticipate in the profits through share priceappreciation and dividend payments

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 25/44

A convertible bond is a mix between a debt andequity instrument. It is a bond having regularcoupon and principal payments, but these bondsalso give the bondholder the option to convertthe bond into stock. FCCB is issued in a currency

different than the issuer's domestic currency.The investors receive the safety of guaranteedpayments on the bond and are also able to takeadvantage of any large price appreciation in thecompany's stock. Due to the equity side of the

bond, which adds value, the coupon payments onthe bond are lower for the company, therebyreducing its debt-financing costs.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 26/44

A tracking stock is a security issued by a parentcompany to track the results of one of its subsidiariesor lines of business; without having claim on theassets of the division or the parent company. It isalso known as "designer stock". When a parentcompany issues a tracking stock, all revenues andexpenses of the applicable division are separatedfrom the parent company's financial statements andbound to the tracking stock. Oftentimes, this is doneto separate a subsidiary's high-growth division froma larger parent company that is presenting losses.

The parent company and its shareholders, however,still control the operations of the subsidiary. Ex-QQQQ, which is an exchange-traded fund thatmirrors the returns of the Nasdaq 100 index

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 27/44

Also referred to as "P-Notes" Financialinstruments used by investors or hedge fundsthat are not registered with the Securities andExchange Board of India to invest in Indiansecurities. Indian-based brokerages buy India-based securities and then issue participatorynotes to foreign investors. Any dividends orcapital gains collected from the underlyingsecurities go back to the investors. These are

issued by FIIs to entities that want to invest in theIndian stock market but do not want to registerthemselves with the SEBI.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 28/44

There has been tremendous growth in the capital market in recent years both asregards turnover of securities and their prices specially after liberalization in1991.

Following are the main areas of growth:-

Establishment of SEBI. Entry in global market. Entry of foreign Institutional Investors. Establishment of National Securities depository Ltd. Appointment of market Makers. Establishment of Over the Counter Exchange of India (OTCEI). Establishment of National Stock Exchange(NSE). Establishment of Credit Rating Agencies.

Establishment of specialized financial Institutions like- UTI, IDBI, ICICI etc. Development of financial services. Increase in number of stocks exchanges (24). Growth of Mutual Funds. Development of Underwriting. Increase in awareness and confidence of investing public.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 29/44

Only few genuine investors. Trading in few strips only. Non-availability of tradable securities. Lack of confidence of genuine investors. Violent fluctuations in prices at stock exchange. Lack of transparency in dealings. Cumbersome procedure of settlement. Price-rigging. Prevalence of insider trading.

Dominance of financial institutions as investors. Loss of faith in private sector. Apathy of companies towards shareholders.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 30/44

There are various processes that Issuers of securitiesfollow or utilize in order to tap the savers for raisingresources. Some of the commonly used processesand methods are described below:Companies, new as well as old, can offer their sharesto the investors in the primary market. This kind of tapping the savings is called an IPO or Initial PublicOffering. SEBI regulates the way in which companiescan make this offering. Companies can make an IPOif they meet SEBI guidelines in this regard. The size of the initial issue, the exchange on which it can be

listed, the merchant bankers' responsibilities, thenature and content of the disclosures in theprospectus, procedures for all these are laid down bySEBI and have to be strictly complied with.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 31/44

Private PlacementMany companies choose to raise capital for theiroperations through various intermediaries bytaking what in marketing terms would be knownas the wholesale route. This is called in financialmarkets as private placement. The retail route of approaching the public is expensive as well astime consuming. SEBI has prescribed the

eligibility criteria for companies and instrumentsas well as procedures for private Placement.However, liquidity for the initial investors inprivately Placed securities is ensured as they canbe traded in the secondary market. But such

securitieshave different rules for listing as well as fortrading.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 32/44

Preferential Offer/Rights Issue

Companies can expand their capital by offeringthe new shares to their existing shareholders.Such offers for sale can be made to the existingshareholders by giving them a preferentialtreatment in allocation or the offer can be on a

rights basis, i.e., the existing holders can get byway of their right, allotment of new shares incertain proportion to their earlier holding. Allsuch offers have also to be approved by SEBIwhich has laid out certain criteria for these routesof tapping the public. These have to be compliedwith.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 33/44

Internet Broking

With the Internet becoming ubiquitous, many

institutions have set up securities tradingagencies that provide online trading facilities totheir clients from their homes. This has beenpossible since all the players in the securitiesmarket, viz., stockbrokers, stock exchanges,

clearing corporations, depositories, DPs, clearingbanks, etc., are linked electronically. Thus,information flows amongst them on a real timebasis.The trading platform, which was converted from

the trading hall to the computer terminals at thebrokers' premises, has now shifted to the homesof investors. This has introduced a higher degreeof transparency in transactions.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 34/44

The government has initiated a number of steps to strengthen the capital Market. Severalreform measures have been undertaken both in Primary Market and Secondary Market.

The Primary market reforms:-

The SEBI was given statutory powers in January 1992 for regulating the stock market.

The Capital Issue (Control) Act, 1947 was abolished in May 1992, allowing issuers of securitiesto raise capital without requiring the consent of any authority.

The requirement to issue share at par of Rs. 10 and Rs. 100 was withdrawn. This gavecompanies the freedom to determine a fixed value per share. This facility is available tocompanies which have dematerialized their shares.

Simplified issue procedures and improved disclosure standards have been prescribed.Companies are required to disclose all material facts, specific risk factors associated with theirprojects.

In order to reduce the cost of issue, underwriting by the issuer was made optional, subject tothe condition that if an issue was not underwritten and in case it failed to secure 90% of theamount offered to the public.

For integrating Indian Capital Market with the International Capital Markets, permission was

given to FIIs such as Mutual Funds and pension funds to operate in the Indian Market. Indian Companies have also been allowed to raise capital from the international capital markets

through issues of ADR’s , GDR’s, FCCBs, etc.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 35/44

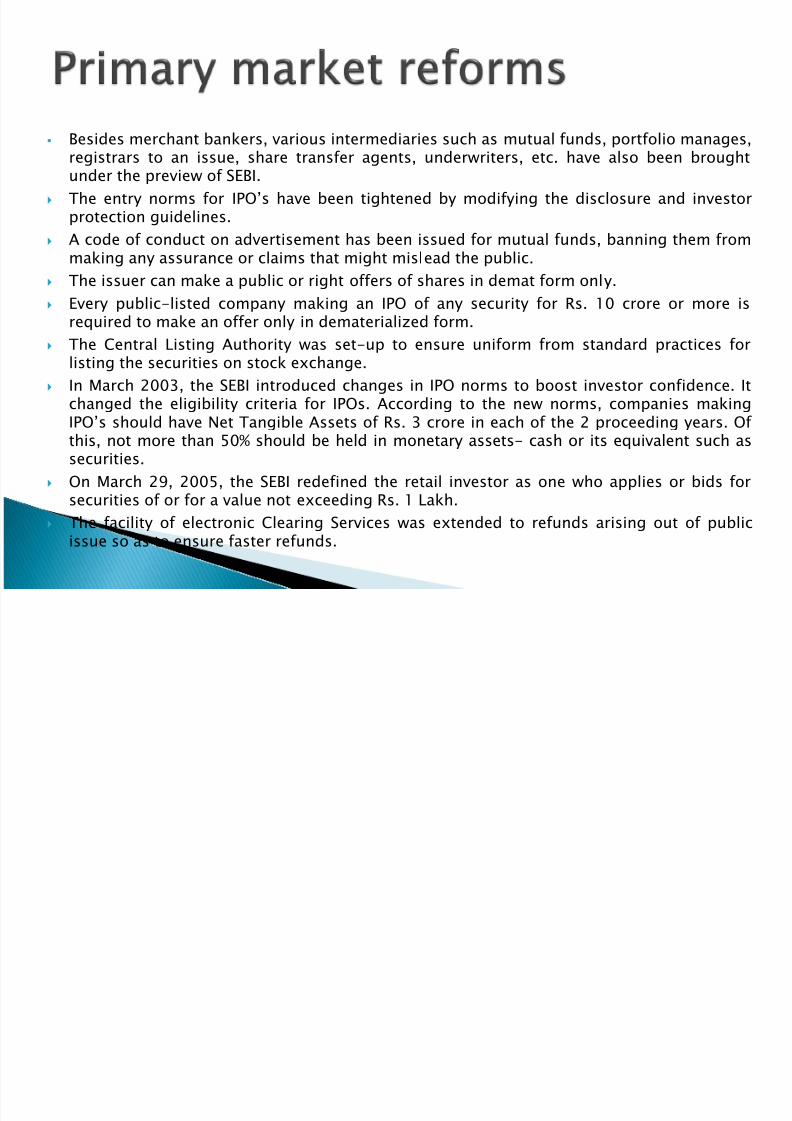

Besides merchant bankers, various intermediaries such as mutual funds, portfolio manages,registrars to an issue, share transfer agents, underwriters, etc. have also been broughtunder the preview of SEBI.

The entry norms for IPO’s have been tightened by modifying the disclosure and investorprotection guidelines.

A code of conduct on advertisement has been issued for mutual funds, banning them frommaking any assurance or claims that might mislead the public.

The issuer can make a public or right offers of shares in demat form only. Every public-listed company making an IPO of any security for Rs. 10 crore or more is

required to make an offer only in dematerialized form.

The Central Listing Authority was set-up to ensure uniform from standard practices forlisting the securities on stock exchange.

In March 2003, the SEBI introduced changes in IPO norms to boost investor confidence. Itchanged the eligibility criteria for IPOs. According to the new norms, companies making

IPO’s should have Net Tangible Assets of Rs. 3 crore in each of the 2 proceeding years. Of this, not more than 50% should be held in monetary assets- cash or its equivalent such assecurities.

On March 29, 2005, the SEBI redefined the retail investor as one who applies or bids forsecurities of or for a value not exceeding Rs. 1 Lakh.

The facility of electronic Clearing Services was extended to refunds arising out of publicissue so as to ensure faster refunds.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 36/44

The open system was replaced by the on-line screen based electronic trading.

3 new stock Exchanges at national level were set-up. These are the Over-the-counterExchange of India(1992), The National Stock exchange of India(1994) and Interconnected stockExchange of India(1999).

Trading and Settlement Cycles were uniformly reduced to 7 days from 14 days. Rollingsettlement(T+5) was introduced for the dematerialized segment, shortened to (T+3) in April 1,2002.

Depository system were introduced to provide protection to investors.

Companies have been allowed to buy back their own shares for Capital restructuring, subject

to the condition that the buy-back does not exceed 25% of the paid up capital and freereserves.

In order to prohibit insider trading, the insider trading regulations have been formulated bySEBI.

Internet trading was permitted in February 2000.

It is mandatory for listed companies to announce quarterly results.

It is mandatory for all brokers to disclose all details of block deals. Block deals include tradingwhich accounts for more than 0.5% of the equity shares of that listed company.

The SEBI has made it mandatory for every intermediary to apply for allotment of unique

identification number for itself and for its related persons.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 37/44

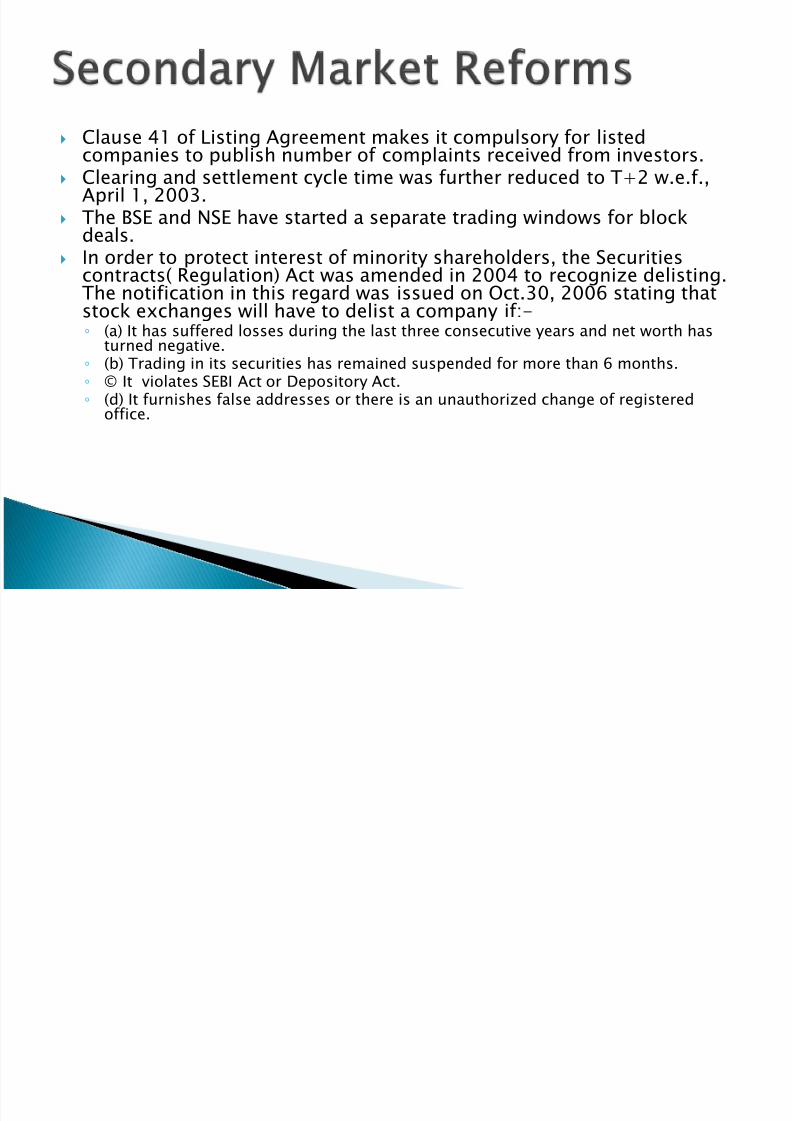

Clause 41 of Listing Agreement makes it compulsory for listedcompanies to publish number of complaints received from investors. Clearing and settlement cycle time was further reduced to T+2 w.e.f.,

April 1, 2003. The BSE and NSE have started a separate trading windows for block

deals. In order to protect interest of minority shareholders, the Securities

contracts( Regulation) Act was amended in 2004 to recognize delisting.The notification in this regard was issued on Oct.30, 2006 stating thatstock exchanges will have to delist a company if:-◦ (a) It has suffered losses during the last three consecutive years and net worth has

turned negative.◦ (b) Trading in its securities has remained suspended for more than 6 months.◦ © It violates SEBI Act or Depository Act.◦ (d) It furnishes false addresses or there is an unauthorized change of registered

office.

R l t F k f C it l

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 38/44

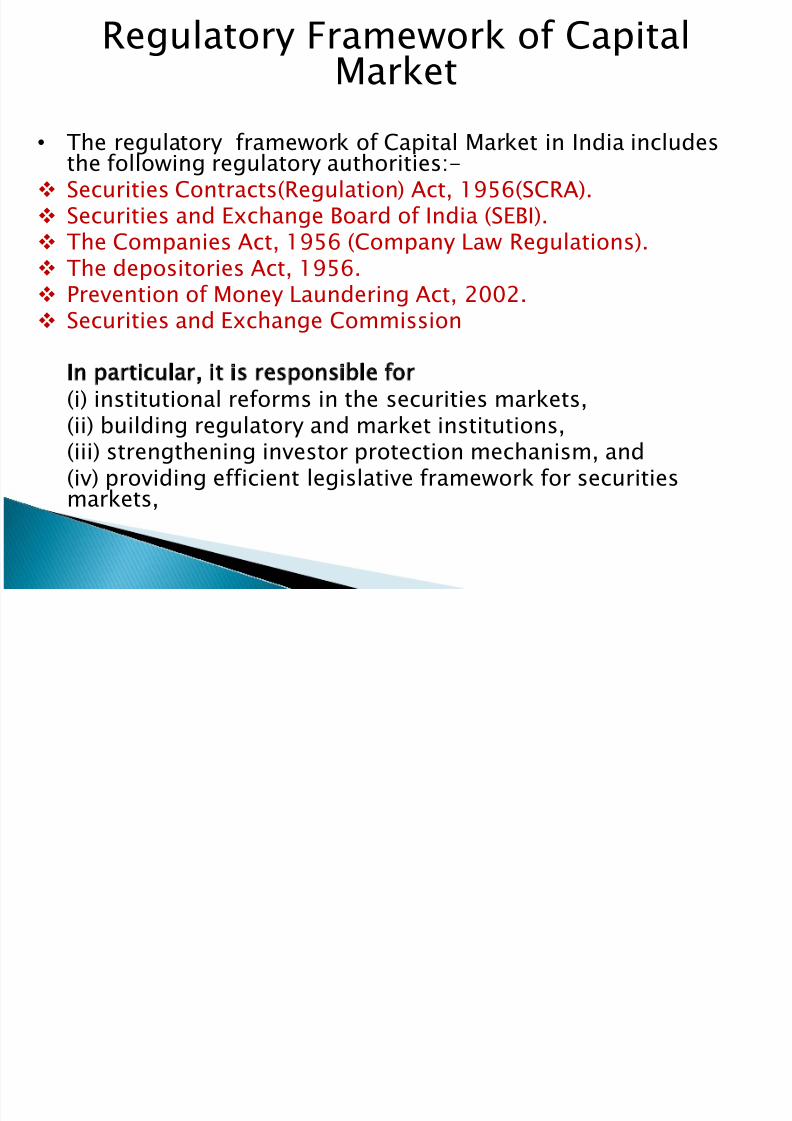

Regulatory Framework of CapitalMarket

• The regulatory framework of Capital Market in India includesthe following regulatory authorities:- Securities Contracts(Regulation) Act, 1956(SCRA). Securities and Exchange Board of India (SEBI). The Companies Act, 1956 (Company Law Regulations). The depositories Act, 1956. Prevention of Money Laundering Act, 2002. Securities and Exchange Commission

In particular, it is responsible for(i) institutional reforms in the securities markets,

(ii) building regulatory and market institutions,(iii) strengthening investor protection mechanism, and(iv) providing efficient legislative framework for securitiesmarkets,

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 39/44

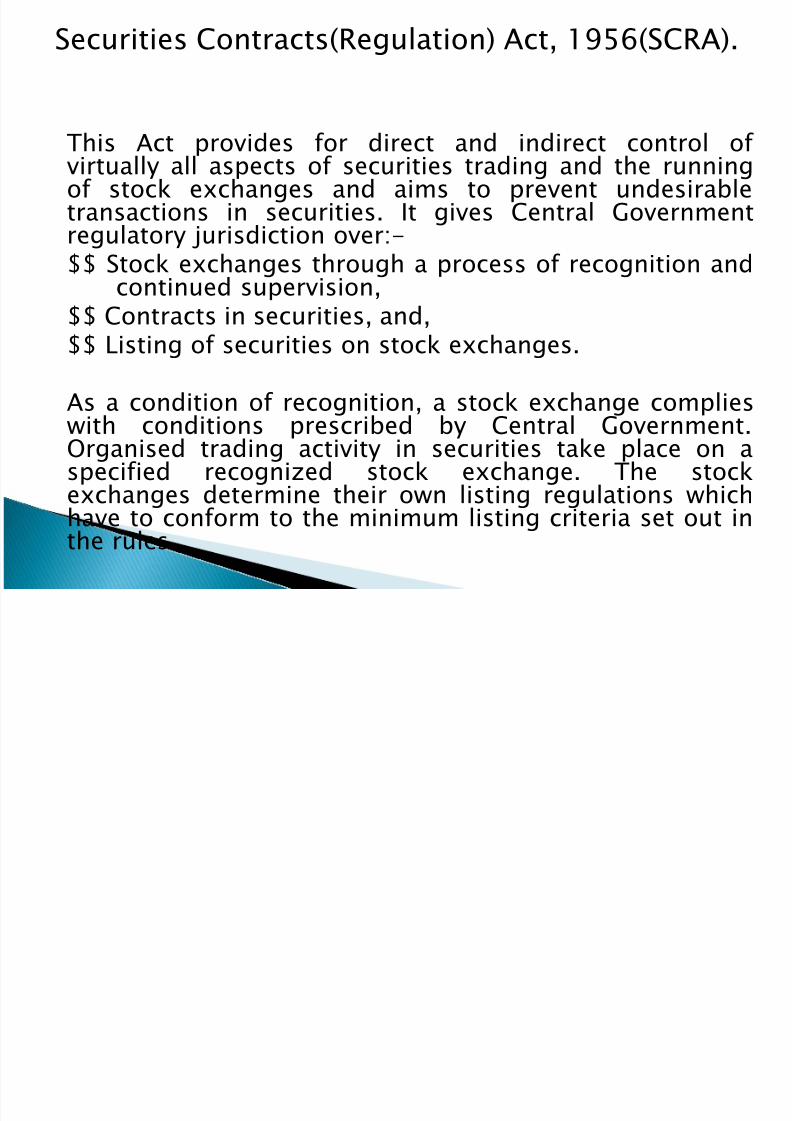

Securities Contracts(Regulation) Act, 1956(SCRA).

This Act provides for direct and indirect control of virtually all aspects of securities trading and the runningof stock exchanges and aims to prevent undesirabletransactions in securities. It gives Central Governmentregulatory jurisdiction over:-$$ Stock exchanges through a process of recognition and

continued supervision,$$ Contracts in securities, and,$$ Listing of securities on stock exchanges.

As a condition of recognition, a stock exchange complieswith conditions prescribed by Central Government.Organised trading activity in securities take place on aspecified recognized stock exchange. The stockexchanges determine their own listing regulations whichhave to conform to the minimum listing criteria set out inthe rules.

h

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 40/44

The Companies Act, 1956

• The Act deals with issue, allotment and transferof securities and various aspects relating tocompany management. It provides for standardof disclosure in public issue of capital,

particularly in the fields of companymanagement and projects, information aboutother listed companies under the samemanagement and management perception of risk factors. It also regulates underwriting, theuse of premium and discounts on issues, rightsand bonus issues, payment of interests anddividends, supply of annual report and otherinformation.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 41/44

Securities and Exchange Board of India (SEBI)

This is the regulatory authority established under the SEBI Act 1992, in order toprotect the interests of the investors in securities as well as promote thedevelopment of the capital market. It involves regulating the business in stockexchanges; supervising the working of stock brokers, share transfer agents,merchant bankers, underwriters, etc; as well as prohibiting unfair trade practicesin the securities market. The following departments of SEBI take care of theactivities in the secondary market:-

Market Intermediaries Registration and Supervision Department (MIRSD)- concerned with the registration, supervision, compliance monitoring andinspections of all market intermediaries in respect of all segments of themarkets, such as equity, equity derivatives, debt and debt related derivatives.

Market Regulation Department (MRD) - concerned with formulation of newpolicies as well as supervising the functioning and operations (except relating toderivatives) of securities exchanges, their subsidiaries, and market institutionssuch as Clearing and settlement organizations and Depositories.

Derivatives and New Products Departments (DNPD) - concerned withsupervising trading at derivatives segments of stock exchanges, introducing newproducts to be traded and consequent policy changes.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 42/44

THE DEPOSITORIES ACT, 1996:

• The paper based ownership and transfer of securities has been a major drawback of the IndianSecurities Markets since it often resulted in delay insettlement and transfer of securities and also leadto "bad delivery", theft, forgery etc.

• The Depositories Act, 1996 was therefore enactedto pave the way for smooth and free transfer of securities.

• It also helps in dematerializing the securities in thedepository mode.

• The act envisages transfer of ownership of securities electronically by book entry withoutmaking the securities move from person to person.

f

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 43/44

Prevention of MoneyLaundering Act, 2002

• The primary objective of the act is to preventmoney-laundering and to provide confiscationof property derived from or involved in money-laundering. The term money-laundering isdefined as whoever acquires, owns, possess or

transfers any proceeds of crime; or knowinglyenters into any transaction which is related toproceeds of crime either directly or indirectly orconceals or aids in the concealment of theproceeds or gains of crime within India oroutside India commits the offence of money-laundering, Besides providing punishment foroffence, the act also provides other measuresof prevention of money-laundering.

8/3/2019 bba 3rd cap. mkt.

http://slidepdf.com/reader/full/bba-3rd-cap-mkt 44/44

• Securities and Exchange

Commission

– The apex regulatory institution of thecapital market

– Established by Government

– Registers listed securities– Registration of stock exchanges anddealing members

– Sets the Rules and regulations and ensures

compliance– Market surveillance to prevent insiderabuse

– Dispute resolution

![St. Joseph's College Of Commerce (Autonomous) Class : 3rd Sem BBA … · Class : 3rd Sem BBA B[16] 46 16SJCCB149 MAHENDRA D KULKARNI Event Management 47 16SJCCB150 MANEESHA S Human](https://img.dokumen.tips/doc/110x75/5f057a9a7e708231d4132a2e/st-josephs-college-of-commerce-autonomous-class-3rd-sem-bba-class-3rd-sem.jpg)