Embed Size (px)

Citation preview

BATH HOTEL FUTURES

2015

Final Report

Prepared for:

Bath & North East Somerset Council

July 2015

Bath Hotel Futures 2015

Hotel Solutions July 2015

CONTENTS

EXECUTIVE SUMMARY ................................................................... i

1. INTRODUCTION ...................................................................... 1 1.1 Background to the Study ........................................................................................... 1 1.2 Study Objective ........................................................................................................... 1 1.3 Uses of the Study ......................................................................................................... 2 1.4 Scope of the Study ..................................................................................................... 2 1.5 Study Methodology .................................................................................................... 3 1.6 Structure of the Report ............................................................................................... 4

2. BATH HOTEL SUPPLY ............................................................... 5 2.1. Current Supply ............................................................................................................. 5 2.2. Changes Since 2009 ................................................................................................... 8 2.3. Planned and Proposed Hotel Development ....................................................... 12 2.4. Comparisons with Other Historic Cities ................................................................. 16

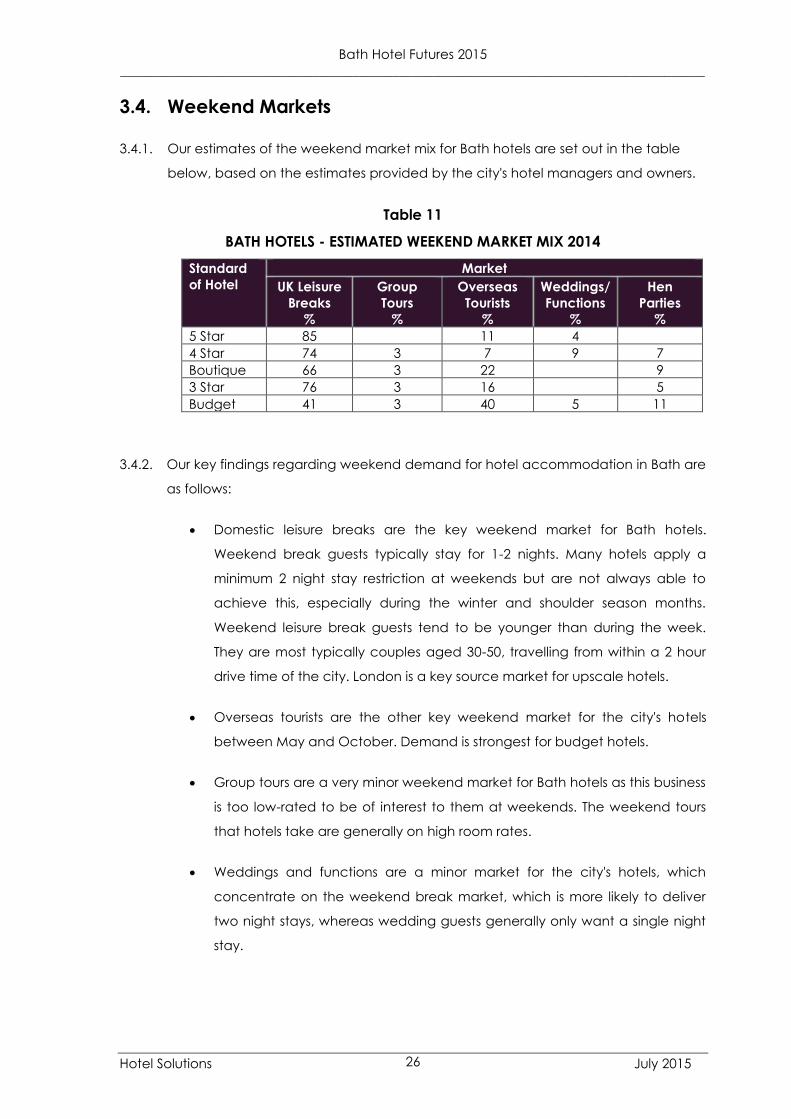

3. CURRENT HOTEL PERFORMANCE & MARKETS ..................... 20 3.1. Occupancy, Achieved Room Rates and Revpar .............................................. 20 3.2 Patterns of Demand ................................................................................................. 22 3.3. Midweek Markets ...................................................................................................... 24 3.4. Weekend Markets ..................................................................................................... 26 3.5. Market Trends ............................................................................................................. 28 3.6 Denied Business ......................................................................................................... 28 3.7. Prospects beyond 2015 ............................................................................................ 29 3.8. Growth in Hotel Demand 2008-2015 ..................................................................... 30

4. STRATEGIC CONTEXT AND DRIVERS OF GROWTH .............. 31 4.1. The Context for Future Growth in the Bath Hotel Market .................................. 31 4.2 The Sub-Regional Strategy for Growth .................................................................. 31 4.3. Economic Performance and Outlook in Bath ..................................................... 33 4.4. National Tourism Trends ............................................................................................ 35 4.5. The Characteristics of Tourism in Bath ................................................................... 37 4.6. Market and Consumer Response Data ................................................................ 39 4.7. Conference Tourism Performance in Bath ........................................................... 40 4.8. Bath Tourism Policies ................................................................................................. 41 4.9. Planning Policies Relevant to Hotel Development ............................................. 44 4.10. Key Projects Affecting Hotel Demand .................................................................. 50 4.11. Conclusions ................................................................................................................ 52

5. FUTURE POTENTIAL FOR HOTEL DEVELOPMENT ................... 53 5.1 Understanding The Requirements and Potential for New Hotel Supply ........ 53 5.2 Hotel Developer & Operator Interest in Bath ....................................................... 61 5.3 Hotel Site Availability ................................................................................................ 74

6. CONCLUSIONS & RECOMMENDATIONS ............................. 76 6.1. The Requirements & Potential for Hotel Development in Bath ........................ 76 6.2. Tackling the Sites Issue .............................................................................................. 79 6.3. The Timing of Hotel Development .......................................................................... 80 6.4. A Locational Strategy for Hotel Development in Bath ...................................... 81 6.5. Implications for the Placemaking Plan ................................................................. 82 6.6. Supporting Existing Hotels, Guest Houses and B&Bs ........................................... 82 6.7. Moving Forwards ....................................................................................................... 83 6.8. Concluding Remarks ................................................................................................ 84

Bath Hotel Futures 2015

Hotel Solutions July 2015

APPENDICES

1 Bath Hotels Interviewed

2 Glossary of Hotel Definitions

3. Heritage City Hotel Stock and Development Comparisons

4. Bath Hotel Developer Testing – Sampling & Response

Lynn Thomason Andrew Keeling

Hotel Solutions Hotel Solutions

Deleanor House Mill Field House

High Street Mill Fields

Coleby Bassingham

Lincoln Lincoln

LN5 0AG LN5 9NP

t. 01522 811255 t. 01522 789702

Bath Hotel Futures 2015

Hotel Solutions July 2015 i

EXECUTIVE SUMMARY

__________________________________________________________________________

The Purpose of the Study

The 2015 Bath Hotel Futures Study has been commissioned by Bath & North East Somerset

Council to provide an up-to-date assessment of the future potential and priorities for hotel

development in Bath through to 2030, to help inform the preparation, finalisation and

implementation of a number of key strategy and policy documents: the update of the

Bath Destination Management Plan, the finalisation of the Placemaking Plan, and the

implementation of the Bath City Riverside Enterprise Area Masterplan. The study updates

the findings of the Bath & North East Somerset Visitor Accommodation Study completed

by The Tourism Company and Hotel Solutions in 2009, in relation to hotel development

opportunities in the city.

Current Hotel Supply

Bath currently has 28 hotels and serviced apartment operations, with a total of 1,591 letting

bedrooms. This includes the Gainsborough Bath Spa which opened on 1 July 2015.

BATH HOTEL SUPPLY – JULY 2015

Standard Hotels Rooms % of

Rooms 5 star 4 306 19.2

Boutique 5 221 13.9

4 star 3 309 19.4

3 star 5 192 12.1

2 star 2 79 5.0

Upper-tier Budget1 1 126 7.9

Budget 3 299 18.8

Serviced Apartments 5 59 3.7

Total Hotels 28 1591 100.0

Notes:

1. Brands including Holiday Inn Express, Ramada Encore and Hampton by Hilton

Bath Hotel Futures 2015

Hotel Solutions July 2015 ii

The city's current hotel offer is weighted towards upscale, full service provision, with 5 star,

boutique and 4 star hotels accounting for 52.5% of total stock. Boutique hotels vary in style

and standard from the MGallery branded Francis Hotel to the luxury AA 3 Red star

Queensberry, midmarket Abbey Hotel and 3 star Metro Harington's Hotel. Budget/limited

service hotels account for 26.7% of Bath's current hotel supply.

Changes in Hotel Supply 2009-2015

Taking account of new hotel openings and changes to existing hotels, Bath's total stock of

hotel accommodation has increased by 18.2% (250 bedrooms) between 2009 and 2015.

The most marked trend has been the significant growth in boutique hotel provision through

the repositioning of 2 and 3 star hotels. There has also been an increase in 4 and 5 star

hotel provision through the upgrading of existing hotels. Other key trends have been an

increase in budget hotel supply, with the opening of a new Premier Inn in December 2013;

a reduction in midmarket full service hotel provision through upgrading to boutique and 4

star hotels; and the gradual increase in serviced apartment supply.

Pipeline Hotel Supply Changes to 2017

There are two hotels currently under construction in Bath - a 177-bedroom 4 star Apex

hotel, with extensive conference facilities for up to 400 delegates, and a 148-bedroom,

budget boutique Z Hotel as part of the Saw Close casino development. The Z Hotel is due

to open in 2016, while the Apex Hotel is scheduled to open early in 2017. The other

significant planned hotel project is the redevelopment of the Pratts Hotel and adjoining

Halcyon Hotel and other properties into a 121-bedroom Hotel Indigo boutique hotel.

Subject to planning permission being granted this hotel could open at the end of 2016. It

will result in a net increase of 54 bedrooms. There are also proposals at various stages for

further boutique hotels in Bath. Assuming that the Apex, Z Hotel and Hotel Indigo all open

by 2017, Bath's hotel stock will have increased by 47% (631 rooms) since 2009, with the

most significant changes being the increase in 5 star, 4 star and especially boutique hotel

provision, and the loss of 3 star stock.

Bath Hotel Futures 2015

Hotel Solutions July 2015 iii

CHANGES IN BATH HOTEL SUPPLY 2009-2017

Standard of Hotel Hotel Supply % Change

2009-2017

(Rooms) 2009 2017

Hotels Rooms Hotels Rooms 5 star 2 181 4 306 +69.1

Boutique 1 29 5 323 +1013.8

4 star 3 223 4 486 +117.9

3 star 10 449 4 146 -67.5

Lower Grade 3 101 2 79 -21.8

Budget/Limited Service 3 317 5 573 +80.7

Serviced Apartments 1 43 5 61 +41.8

Total 25 1343 29 1974 +47.0

Comparisons with Other Heritage Cities

In comparison to Oxford, Cambridge, Chester, York and Exeter:

In terms of total hotel supply Bath has the lowest number of hotel bedrooms;

Bath has the most upmarket hotel supply in terms of 5 star and boutique hotel

provision and 5 star guest houses, and more limited supplies of 3 star, 2 star and

budget hotels.

Hotel development trends have been similar across all six comparator cities

between 2009 and 2015: there has been a general move upmarket, with the

upgrading and repositioning of 3 star hotels as 4 star and boutique hotels, the

opening of new 5 star and boutique hotels in some cities, and some loss of poorer

quality 2 star/ lower grade hotel stock; new Premier Inn and/or Travelodge budget

hotels have opened in most of the cities (other than Oxford); and the supply of

serviced apartments and aparthotels has gradually increased:

All of the comparator cities look set to see more hotel development than Bath

going forward (if all of the current hotel proposals are progressed).

Bath Hotel Futures 2015

Hotel Solutions July 2015 iv

Current Hotel Performance and Markets

Estimated average annual room occupancies, achieved room rates and revpar figures for

Bath hotels for 2012 - 2014 and forecast figures for 2015 are summarised in the table

overleaf, based on the information provided by the city's hotel managers and owners.

Key points to note in relation to hotel performance in Bath and changes since 2012 are as

follows:

Hotel performance in Bath is very strong at all levels in the market, and well ahead

of national averages. Boutique, 3 star and budget hotels are performing particularly

well in the city. 5 star hotels achieve lower room occupancies but very high

average room rates, largely due to the numbers of suites that they have, which

command high prices but do not always fill.

Hotel performance in Bath has generally strengthened between 2012 and 2014 and

looks set to improve further in 2015.

Boutique hotel occupancies and average room rates dipped in 2013 as new

boutique hotels, guest houses and B&Bs have opened. Boutique hotel occupancies

have quickly recovered in 2014 and 2015 as the new boutique hotels have become

more established, and average room rates have started to increase for some

boutique hotels in 2015 .

5 star hotel occupancies have improved but average room rates have dropped

back slightly as hotels have reduced their room rates to drive occupancy.

3 star hotel performance has strengthened year on year.

The opening of the new Premier Inn in December 2013 does not appear to have

had anything other than a marginal impact on the city's established hotels, with

most hotels reporting occupancy and average room rate growth in 2014, and the

Premier Inn quickly achieving high occupancies.

Bath Hotel Futures 2015

___________________________________________________________________________________________________________________________________________

Hotel Solutions July 2015 v

BATH HOTEL PERFORMANCE 2012-2015

Standard of Hotel Average Annual Room

Occupancy

%

Average Annual Achieved

Room Rate4

£

Average Annual Revpar5

£

2012 2013 2014 2015f3 2012 2013 2014 2015f3 2012 2013 2014 2015f3

UK Provincial Hotels (All Standards)1 69.8 72.6 75 766 59.22 59.94 62.07 64.736 41.32 43.53 46.37 49.146

UK Provincial 3/4 Star Chain Hotels2 69.6 72.0 73.9 n/a 69.97 71.46 76.49 n/a 48.72 51.48 56.53 n/a

5 star 65 n/a 72 74 169 n/a 165 177 110 n/a 119 131

4 star n/a n/a 76 79 n/a n/a 92 100 n/a n/a 70 79

Boutique 86 80 85 86 129 112 116 121 111 89 99 105

3 star 77 81 82 83 73 74 77 78 56 60 63 64

Budget n/a n/a 87 88 n/a n/a 77 83 n/a n/a 67 73

Serviced Apartments n/a n/a 83 84 n/a n/a 107 114 n/a n/a 88 96

All Hotels n/a n/a 81 83 n/a n/a 100 107 n/a n/a 81 88

Source: Hotel Solutions – July 2015

Notes 1. Source: STR Global

2. Source: TRI Hotstats UK Chain Hotels Market Review

3. Based on forecast figures provided by hotel managers

4. The amount of rooms revenue (excluding food and beverage income) that hotels achieve per occupied room net of VAT, breakfast (if included) and

discounts and commission charges.

5. The amount of rooms revenue (excluding food and beverage income) that hotels achieve per available room net of VAT, breakfast (if included) and

discounts and commission charges

6. PwC UK Hotel Forecast 2015

Bath Hotel Futures 2015

__________________________________________________________________________________________

vi

Hotel Solutions July 2015

Friday and Saturday occupancies are very high for Bath hotels. Hotels of all

standards consistently fill and turn business away on Saturday nights throughout the

year and achieve high occupancies on Friday nights, particularly during the

summer months. Friday occupancies dip a little in winter for most hotels.

Midweek and Sunday occupancies are more seasonal. They are strong in the

summer but weaker during the winter months, especially January, February and

March. 3 star and budget hotels achieve the highest midweek occupancies, both

during the summer and in the winter. They attract stronger year-round demand

from more price conscious corporate customers and overseas tourists, and also

attract business from contractors working on construction and shop fitting projects

in the city. Some boutique hotels are also successfully driving midweek business

through OTAs (online travel agents such as booking.com and Expedia) and a more

flexible room rate strategy.

There is a significant difference between midweek and Friday and Saturday

achieved room rates at all levels in the Bath hotel market. A differential of £30-50 is

typical. Some hotels reported a differential of £80-100. There is also a differential

between summer and winter rates, particularly during the winter , when midweek

and Sunday room rates are much lower and Friday night prices also reduce.

The domestic leisure break and overseas tourist markets are the key markets for

Bath hotels. Weekend break demand is very strong and high-rated, particularly

from the London market. Midweek break business is more price driven, with the

focus primarily on attracting the grey market through OTAs. Overseas tourist

demand is strongest for budget and 3 star hotels, suggesting a significant price

conscious segment in this market. A lot of overseas tourists also book through OTAs.

Corporate demand for hotel accommodation in Bath is relatively weak: there are

few major companies in Bath that generate good volumes of business for the city's

hotels. Corporate demand is stronger for budget hotels, suggesting that this market

is largely price driven in Bath.

Residential conferences are a very minor market for most of Bath's hotels, other

than Bailbrook House, which has extensive conference facilities. Most of the city's

other hotels have very limited conference and meeting facilities so are unable to

target the residential conference market.

Bath Hotel Futures 2015

__________________________________________________________________________________________

vii

Hotel Solutions July 2015

Growth in Hotel Demand 2008-2015

In terms of total roomnight demand the Bath hotel market has grown by 23% between 2008

and 2015, driven by both an increase in hotel supply and an improvement in occupancy

performance. This equates to an average annual growth rate of 3.3% over the last 7 years.

BATH - GROWTH IN HOTEL DEMAND 2008-2015

Year Total Satisfied

Roomnight

Demand

% Increase in

Roomnights

2008-2015

%

2008 367,646

2015 452,001 + 23%

The Potential for Future Growth in Demand for Hotel Accommodation in Bath

An assessment of the strategic context for economic development and tourism growth in

Bath shows the following in terms of the potential for future growth in demand for hotel

accommodation in the city, and the potential for additional hotel development:

Sub-regional and local economic and tourism policies and spatial and land use

planning frameworks provide a strong basis for economic growth and the

development of Bath's visitor economy, presenting a confident environment for

continued growth in the city's hotel market and further hotel development.

National forecasts for domestic tourism show significant growth in markets for which

Bath has a comparative advantage. The additional boost provided by an even

stronger forecasted growth in overseas tourism will be important in securing new

tourist stays in Bath.

The planned significant growth in Bath's economy, improved transport

infrastructure, and the positive environment provided by the universities, are all

strong drivers for growth in hotel demand in the city. The Riverside Enterprise Area

provides a particular catalyst for growth.

Proposals for new leisure facilities and attractions, and an enhanced events

programme, should lead to future growth in demand for hotel accommodation in

the city from leisure markets.

Bath Hotel Futures 2015

__________________________________________________________________________________________

viii

Hotel Solutions July 2015

Future Requirements & Potential for Hotel Development in Bath

In order to gauge future requirements and potential for hotel development in Bath we have:

Calculated the level of new hotel provision that might be needed to achieve a 5%

p.a. growth in staying tourism in the city through to 2030;

Modelled potential requirements for additional hotel bedrooms under three (Low,

Medium and High) scenarios of potential future growth in midweek demand for

hotel accommodation in the city;

Spoken with national hotel companies to gauge their interest in opening new

hotels in Bath and identify any barriers that they are facing in terms of bringing

forward hotel schemes in the city.

These exercises show potential for significant hotel development in Bath both in terms of

market potential and hotel company interest. The key question is how much of this potential

does the city want to accommodate and at what level in the market? The answers to these

questions will depend on the future strategy for Bath as a visitor destination:

If the city wants to grow staying tourism volumes, it will clearly need more hotel

provision. With hotels trading at such high occupancies for much of the year

growth in staying tourism will need to be largely supply led. There is otherwise little

hotel capacity to support staying tourism growth. The quantum of new hotel

provision needed will depend on the targets for growing Bath's staying visitor

market. The type of new hotel provision required will depend on the markets that

the city wants to attract.

If the city wants to convert more day visitors to staying visitors it will need more

lower-priced hotel accommodation that is affordable for the visitors that currently

stay in hotels in surrounding locations and commute into Bath as day visitors.

If the city wants to attract more companies it will need a greater supply of hotel

accommodation at a price point that companies can afford to pay for single

occupancy room rates.

If Bath is to remain competitive as a staying visitor destination it will need a good

mix of high quality, contemporary hotel accommodation, including a strong

independent hotel offer. Care is needed to avoid undermining the independent

hotel sector, which is a key part of Bath's distinctiveness as a place to stay.

Bath Hotel Futures 2015

__________________________________________________________________________________________

ix

Hotel Solutions July 2015

Our assessments of the requirements and potential for additional hotel provision in Bath show

no immediate requirement before 2020 for additional upscale/full service hotel provision,

beyond the Gainsborough Bath Spa and pipeline Apex and Indigo hotels. The market needs

to absorb this new supply first. There remains very strong interest however from hotel

companies and independent hoteliers that would like to open upscale hotels in Bath. There is

no need to deter this interest, but no need either to actively encourage it. Further upscale

hotel development should be left to the market to determine.

Our growth projections show that Bath should be able to support another budget/limited

service hotel within the next 5 years, in addition to the Z Hotel. Beyond 2020 we are also

showing potential for further budget/limited service hotels through until at least 2030.

There are good reasons for encouraging budget/limited service hotel development in Bath in

terms of the clear demand/potential for more of this type of hotel accommodation in the

city; the new business that budget hotels will generate as a result of their brand strength and

customer base, national marketing, central reservations and referral business from sister

hotels; and the contribution that budget hotels can make to the evening restaurant

economy in the city. There are also some negatives as to why significant budget/limited hotel

development might not be so good for Bath in terms of their potential impact on the city's

remaining 3 star hotels, its guest house and B&B sector and hotels in the surrounding area,

and the potential that they may attract more stag and hen parties. Care is therefore needed

to attract budget/limited service hotel products and brands that will add to the city's hotel

offer, with the focus perhaps being more on attracting upper-tier budget brands e.g.

Hampton by Hilton, and/or some of the new budget boutique brands e.g. Moxy and Aloft.

Our research shows market potential for additional serviced apartment provision in Bath, and

possibly an aparthotel. This type of supply would broaden the city's hotel offer. It would

appeal to the corporate market, especially to longer staying corporate visitors. It is also

becoming increasingly popular with leisure visitors as a result of the greater space, flexibility

and sometimes value for money that it can offer. Serviced apartments have particular

appeal to families and overseas tourists for these reasons. The only potential negative from an

increase in serviced apartments is that they also appeal to the hen party market.

Bath Hotel Futures 2015

__________________________________________________________________________________________

x

Hotel Solutions July 2015

Tackling the Sites Issue

The availability of suitable and affordable sites for hotel development is the key barrier to

growing Bath's hotel supply. Relatively few sites come up and there is such strong competition

from student accommodation and residential development against which a hotel use

cannot compete on value. How best to address this issue should be a key consideration for

the Council. There are two key roles that it could play if it wants to intervene proactively to

address the hotel sites issue:

As landowner and developer/investor - many of the key regeneration/ development

sites in the city centre are in total or partial Council ownership. The Council thus has

more control over the type of uses that these sites go for, and the type of hotels that

could be included in development schemes (if a hotel use is seen as appropriate

within the mix).

By working with land and property owners to bring forward sites and buildings that

would be suitable for hotel development and match them with key target hotel

products and brands that will help to achieve the strategy for growing staying

tourism in the city (whatever that looks like when finally agreed).

If the Council decides to take either or both of the more interventionist approaches to

addressing the hotel sites issue discussed above, there are two aspects to consider - the

timing of when hotel development needs to come forward, and a locational strategy for

different types and standards of hotel, to optimise the use of available sites and to achieve

the strategy for staying tourism growth.

Bath Hotel Futures 2015

__________________________________________________________________________________________

xi

Hotel Solutions July 2015

The Timing of Hotel Development

In terms of the timing of new hotel development:

The most immediate requirement is for another budget/limited service hotel or an

aparthotel.

Additional upscale/full service hotel provision will not be required much before

2022/23.

The phased release of sites in the Enterprise Area, some of which could incorporate

a hotel, provides an opportunity to exert some control on when hotel schemes might

come forward; the trick will be to tie this in with the market need in terms of the most

appropriate type of hotel with both market and destination/scheme fit.

A Locational Strategy for Hotel Development

In terms of a locational strategy:

Prime sites in the historic core of the city centre should be prioritised for upscale/full

service hotel development;

Budget/limited service and aparthotel development can be more appropriately

developed on and steered towards edge of city centre and riverside sites;

There could be a case for considering budget hotel development in outer locations

that are well served by bus routes;

Buildings of character should be used for boutique hotels;

Redundant offices may be more suited for conversion to limited service hotels, but

might also present redevelopment rather than conversion opportunities where more

development/a better site solution and scheme could be achieved.

Once the locational strategy has been agreed, it will be important to communicate it to

stakeholders, including site owners and hotel companies; act on it as a Council where direct

intervention is achievable (e.g. where the Council is a full or partial site owner and/or could

act as the developer / investor for a scheme that includes a hotel); and where possible build

it into policy and strategy making, in order to give direction to the market about what the

Council is looking to see delivered in terms of new hotel provision

Bath Hotel Futures 2015

__________________________________________________________________________________________

xii

Hotel Solutions July 2015

Implications for the Placemaking Plan

In finalising the Placemaking Plan:

There is a need to plan for a greater number of additional bedrooms in the city

centre than is identified in the Core Strategy. This Hotel Futures update presents the

market evidence and rationale to do so, with clear links to the previous work and the

context of a much improved climate for investment.

Including the suggested locational strategy for hotel development within the Plan

should be considered as one route to directing and giving clarity to the hotel

development market.

Further work is needed to more closely assess the suitability of key regeneration sites

to the requirements of hotel developers and operators, and to match best fit hotel

products and brands in each case.

It may be appropriate for the Placemaking Plan to also address the issue of the

conversion of redundant office stock to hotel use, recognising the benefits this can

bring to the destination, without enforcing the replacement jobs criteria, which will

be a significant barrier to hotel conversion, particularly at the budget level.

Supporting Existing Hotels, Guest Houses and B&Bs

While further hotel development will be needed to achieve targets and capitalise on the

potential for growth in staying tourism, supporting existing (and new)hotels, guest houses and

B&Bs will also be important through:

Effective management, maintenance and improvement of the city's public realm

fabric;

Further development of the city's visitor offer to maintain and broaden its appeal as

a visitor destination and help encourage longer stays;

Effective marketing of Bath as a visitor destination, focused on boosting Sunday to

Thursday business, particularly during the winter;

Bringing forward office development to grow corporate demand for hotel

accommodation in the city.

Bath Hotel Futures 2015

__________________________________________________________________________________________

xiii

Hotel Solutions July 2015

Moving Forwards

In terms of moving ahead, further work will be needed in terms of:

Fleshing out the locational strategy for hotel development in terms of more

detailed assessment of sites and matching best fit hotel products and brands. This

could be expanded to include the identification and assessment of additional sites

with potential for hotel development, both within Council ownership and privately

owned. Both strands would involve working with site owners to communicate and

deliver the hotel investment strategy.

Targeting best fit hotel brands, with a particular focus on those that can most help

deliver the required growth in staying tourism and help grow the Bath hotel market

in terms of generating new demand and attracting new markets. This might

include some additional targets dependent upon the understanding that comes

out of the more detailed sites work.

Feeding into more detailed financial and physical appraisals being led by other

consultancy teams but requiring a specialist input.

Modelling the potential impact of additional budget/ limited service hotel provision

on Bath’s independent guest house sector.

Understanding the options for and potential benefits from direct Council

investment in hotel development schemes, as other local authorities across the

country are increasingly doing.

Concluding Comments

This is a time of great opportunity for B&NES Council to shape the future of Bath in the interests

of its long term viability, sustainability and well-being. The visitor economy undoubtedly has a

key role to play in this, but without increased hotel capacity will be unable to support the city

in fulfilling its potential for staying tourism growth. With such strong hotel performance in the

city; the levels of interest in opening new hotels here; and an emerging development

framework that involves planning for major areas of change, there is a real opportunity to

help overcome the obstacles to delivery faced by hotel developers. This is a unique

opportunity that it is critical to get right, using the evidence from this Hotel Futures Study as a

basis to inform and guide forward planning.

Bath Hotel Futures 2015

__________________________________________________________________________________________

1

Hotel Solutions July 2015

1. INTRODUCTION

1.1 Background to the Study

1.1.1 The 2015 Bath Hotel Futures Study has been commissioned by Bath & North East

Somerset Council to provide an up-to-date assessment of the future potential and

priorities for hotel development in Bath through to 2030, to help inform the

preparation, finalisation and implementation of a number of key strategy and policy

documents: the update of the Bath Destination Management Plan, the finalisation of

the Placemaking Plan, and the implementation of the Bath City Riverside Enterprise

Area Masterplan. The study updates the findings of the Bath & North East Somerset

Visitor Accommodation Study completed by The Tourism Company and Hotel

Solutions in 2009, in relation to hotel development opportunities in the city.

1.2 Study Objective

1.2.1 The objective of the study was to make a robust, independent, evidence-based

assessment of the potential for the future development of Bath's hotel offer, both in

terms of the opening of new hotels and the expansion, development and

repositioning of existing hotels, based on a thorough examination of the following:

The Bath hotel supply and how this has been changing and is set to change in

the future as pipeline hotel schemes are delivered;

The current performance of the city's hotel sector, at each level in the market;

The prospects for future growth in demand for hotel accommodation in Bath

from the key markets, and what will drive this growth;

Comparisons with hotel provision and development in other leading heritage

city destinations in England;

Hotel company interest in opening new hotels in Bath.

Bath Hotel Futures 2015

__________________________________________________________________________________________

2

Hotel Solutions July 2015

1.3 Uses of the Study

1.3.1 The study findings will be used to:

Inform the finalisation of the Placemaking Plan;

Input into the update of the Bath Destination Management Plan;

Inform the implementation of the Bath City Riverside Enterprise Area

Masterplan, particularly in terms of guiding Council decisions regarding the

inclusion of hotels within schemes for key regeneration and development sites

that are in full or partial Council ownership;

Guide decision-making on planning applications for new hotel development

projects;

Inform decision-making on planning applications for the expansion of existing

hotels;

Identify other interventions that the Council might consider to influence hotel

development in Bath in line with destination development priorities (once

agreed);

Identify other possible interventions that the Council can make to grow and

develop the city's hotel market to support existing and new hotels.

1.4 Scope of the Study

1.4.1. The geographic focus of the Hotel Futures Study has been on Bath city centre and

outskirts. The study has not covered other parts of Bath & North East Somerset.

1.4.2. In terms of types of hotel the study has looked at the potential for:

Full service 4 and 5 star hotels;

Boutique and lifestyle hotels;

Midmarket/ 3 star hotels;

Budget/limited service hotels;

Serviced apartments/ aparthotels;

1.4.3. Appendix 2 provides a glossary of definitions for these types of hotel.

1.4.4. The study has not looked at the Bath guest house and B&B sector, either in terms of its

future growth potential or the potential impact of new hotel development on guest

house and B&B performance.

Bath Hotel Futures 2015

__________________________________________________________________________________________

3

Hotel Solutions July 2015

1.5 Study Methodology

1.5.1. The study has involved the following modules of research and consultation:

An audit of the current (July 2015) hotel supply in Bath and how this has

changed since 2009 in terms of new hotel openings and the expansion,

development and repositioning of existing hotels. The audit has been based on

information provided by Bath Tourism Plus, supplemented by our own Internet

searches.

A review of hotel development proposals to identify the likely pipeline changes

to the city's hotel supply in terms of new hotel openings and the development

of existing hotels.

Benchmarking hotel provision and development activity in Bath against

current and pipeline hotel supplies in Oxford, Cambridge, York, Chester and

Exeter, as comparator heritage destinations, to provide a wider context for

considering hotel development requirements for Bath to remain competitive

against these destinations.

A survey of hotel managers and owners in the city to gather data and

information on room occupancy levels and trends, patterns of demand,

achieved room rates, market mix, levels of denials, market trends, and future

development plans. Interviews were conducted primarily through face-to-face

interviews supplemented with telephone interviews as required. We also

obtained hotel performance data from hotel company head offices for some

of the city's hotels, and derived hotel performance figures for one hotel that

declined to take part in our survey from information that we were able to

obtain from our industry contacts. A total of 18 hotels took part in the survey.

They are listed at Appendix 1. We are very grateful to all of the hotel managers

and owners that gave so freely of their time and information to enable us to

produce robust and accurate hotel performance data and market insight

information for the city.

A review of relevant policy and strategy documents and employment and

population forecasts to establish the policy framework for hotel development

in the city and identify likely drivers of future growth in hotel demand.

Bath Hotel Futures 2015

__________________________________________________________________________________________

4

Hotel Solutions July 2015

A review of national tourism trends and forecasts of relevance to Bath.

A review of available research information and data on leisure and

conference tourism in Bath and the city's visitor markets.

Stakeholder consultations to gather information on wider destination

development objectives and major developments with the potential to deliver

new demand for hotels.

The preparation of hotel demand projections (using our Hotel Futures hotel

demand forecasting model) to provide a quantitative estimate of the level of

new hotel development that future market growth might support in Bath

through until 2030.

A survey of national, regional and local hotel companies to test hotel

developer/operator interest in Bath, establish site and location requirements,

and identify any obstacles that hotel companies face relative to investing in

the city.

1.6 Structure of the Report

1.6.1. The report comprises chapters setting out the key findings and conclusions of the

study regarding:

Current hotel supply, recent changes, planned hotel development and

comparisons with other heritage cities;

Current hotel performance and markets:

Future market prospects and drivers of growth in hotel demand;

The future requirements and potential for hotel development in the city.

1.6.2. The final chapter sets out our recommendations for potential Council intervention to

guide and support future hotel development in Bath and grow the city's hotel market

to support existing and new hotels.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 5

2. BATH HOTEL SUPPLY

______________________________________________________________________________________

2.1. Current Supply

2.1.1. There are currently 28 hotels and serviced apartment operations in Bath, with a

total of 1,591 letting bedrooms. This includes the Gainsborough Bath Spa which

opened on 1 July 2015. This current hotel supply is analysed below by standard

and listed fully in the table overleaf.

Table 1

BATH HOTEL SUPPLY – JULY 2015

Standard Hotels Rooms % of

Rooms 5 star 4 306 19.2

Boutique 5 221 13.9

4 star 3 309 19.4

3 star 5 192 12.1

2 star 2 79 5.0

Upper-tier Budget1 1 126 7.9

Budget 3 299 18.8

Serviced Apartments 5 59 3.7

Total Hotels 28 1591 100.0

Notes:

2. Brands including Holiday Inn Express, Ramada Encore and Hampton by Hilton

2.1.2. Bath has a mix of different standards and styles of hotel. The city's current hotel

supply is weighted more towards upscale, full service provision, with 5 star,

boutique and 4 star hotels accounting for 52.5% of total stock. Boutique hotels

vary in style and standard from the MGallery branded Francis Hotel to the luxury

AA 3 Red star Queensberry, midmarket Abbey Hotel and 3 star Metro Harington's

Hotel. Budget/limited service hotels account for 26.7% of Bath's current hotel

supply. Most of the city's serviced apartment operations are small, with 2 or 3

apartments. SACO Bath Serviced Apartments is the only larger serviced

apartment operation.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 6

Table 2

BATH CITY HOTEL SUPPLY – JULY 2015

Hotel Standard1 Rooms Brand The Royal Crescent 5 star 45 Relais & Chateaux

The Bath Priory 5 star 33 Andrew Brownsword Hotels

Macdonald Bath Spa 5 star 129 Macdonald Hotels & Resorts

The Gainsborough Bath Spa 5 star 99 Leading Hotels of the World

Hilton Bath City 4 star 173 Hilton

Bailbrook House Hotel 4 star Country House 94 Hand Picked Hotels

Combe Grove Manor 4 star Country House 42 The Hotel Collection

Francis Hotel Bath Boutique (4 star) 98 MGallery (Accor Hotels)

The Queensberry Boutique (AA 3 Red star) 29

The Abbey Boutique (AA 3 star) 60

The Halcyon Boutique (VB Approved) 21

Haringtons Hotel Boutique (AA 3 star Metro) 13

Lansdown Grove 3 star 54 Coast & Country (Shearings)

The Royal 3 star 35

Pratt's VB Approved (was 3 star) 46 Atlas Hotels

Old Mill Hotel & Lodge, Batheaston 3 star 35

The County Hotel 3 star 22 Seasons Holidays

Redcar Lower Grade 41

Parade Park Lower Grade (VB Approved) 38

Holiday Inn Express Upper Tier Budget 126 Holiday Inn Express (IHG)

Premier Inn Budget 108 Premier Inn

Travelodge Bath Waterside Budget 125 Travelodge

Travelodge Bath Central Budget 66 Travelodge

SACO Bath Serviced Apartments Serviced Apartments 43 SACO

Harington's Apartments Serviced Apartments 3

Halcyon Apartments Serviced Apartments 8

Bath House Apartments Serviced Apartments 2

Bath Circle Serviced Apartments 3

Notes:

1. VisitBritain, AA, booking.com or TripAdvisor ratings. Boutique hotels are those that

describe themselves as such on their websites. There is no official designation of a

boutique hotel.

2.1.3. In addition to hotels, Bath also has 10 large 5 star and boutique guest houses and

B&Bs, with a total of 132 letting bedrooms, which compete to some extent with

the city's hotels.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 7

Table 3

BATH 5 STAR/ BOUTIQUE GUEST HOUSES/ B&Bs – JULY 2015

Establishment Standard Rooms The Ayrlington 5 star 16

Brindleys Boutique 6

Dorian House 5 star Boutique 13

Dukes Boutique 17

Grays Boutique 12

One Three Nine Boutique 10

Paradise House 5 star 11

Tasburgh House 5 star Boutique 12

The Windsor 5 star 15

Villa Magdala 5 star 20

2.1.4. Beyond Bath there are a further 9 hotels in surrounding locations including

Bradford-on-Avon, Colerne, Limpley Stoke, Freshford, Pensford, Trowle Common

and Wick, with a total of 309 letting bedrooms, which compete to some extent

with Bath hotels. They range from luxury 4 and 5 star country house hotels to 3 star

hotels.

Table 4

HOTEL SUPPLY SURROUNDING BATH – JULY 2015

Hotel/Location Standard Rooms Brand

Bradford-on-Avon Woolley Grange Luxury Family Hotel 25 Luxury Family Hotels

Best Western Leigh Park 3 star Country House 45 Best Western

Widbrook Grange 3 star 20

Trowle Common The Moonraker Hotel 3 star Country House 21

Limpley Stoke Best Western Limpley Stoke 3 star Country House 64 Best Western

Colerne Lucknam Park 5 Red star Country House 42 Relais & Chateaux

Pride of Britain Hotels

Freshford Homewood Park 4 star Country House 21 Longleat Hotels

Pensford The Pig near Bath Boutique Country House 29 The Pig

Wick

Tracy Park Golf & Country

Hotel

3 star Golf & Country House

Hotel

42

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 8

2.2. Changes Since 2009

New Hotels

2.2.1. Two new hotels have opened in Bath since 2009:

The Premier Inn Bath City Centre opened in December 2013, with 108

bedrooms.

The £16 million, 5 star Gainsborough Bath Spa hotel and spa opened on 1

July 2015, as the UK's first thermal spa hotel. It has 99 bedrooms and suites,

a spa village with thermal pools, saunas, steam rooms, an ice chamber,

treatment rooms and fitness suite; two function/ conference rooms, a

restaurant and bar. It is owned and operated by Malaysian luxury hotel

operator YTL Hotels and will trade at the very top end of the market, with

midweek room rates starting at £285 room only and prices for a Saturday

night starting at £395.

2.2.2. The city's serviced apartment supply has gradually increased in recent years with

the opening of the Halcyon Apartments (in 2014) and the Harington's, Bath House

and Bath Circle apartments.

2.2.3. The city's supply of boutique guest houses and B&Bs has gradually increased since

2009, with the repositioning of the Dukes Hotel as a boutique guest house and

Cheriton House guest house as the Grays boutique B&B, and the opening of

Brindleys boutique B&B.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 9

Hotel Extensions, Refurbishment and Repositioning

2.2.4. Our research has identified the following changes to Bath's hotel supply since

2009 in terms of investment in existing hotels:

The Royal Crescent underwent a complete, £5m refurbishment in 2013

and 2014 under its new owners Topland Group plc, to restore it to one of

the UK's leading luxury hotels.

The Macdonald Bath Spa is currently in the process of refurbishing 109

bedrooms in 2015.

Bailbrook House underwent a £10m refurbishment in 2013 following its

acquisition in 2012 by Hand Picked Hotels to reposition the property as a

4 star hotel. The work included the remodelling of the Mansion House to

create 13 new feature bedrooms.

The Francis Hotel was completely refurbished and repositioned as an

Accor MGallery boutique hotel in 2012 at a cost of £6m.

The Abbey Hotel was acquired by Ian and Christa Taylor in February 2012.

They have gradually upgraded and repositioned it as a midmarket

boutique hotel. The hotel left the Best Western marketing consortium in

September 2014 to operate as an independent hotel.

The 2 star George's Hotel reopened as The Halcyon boutique hotel in 2010,

following a £3m makeover.

The Hilton Bath City has added 23 bedrooms through the conversion of

some of its conference rooms.

Some of the Lansdown Grove Hotel's bedrooms have been upgraded in

the last 2 years.

The Royal has invested £700k in the upgrading of the hotel's bathrooms.

The 3 star Dukes Hotel has been repositioned as the Dukes boutique guest

house.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 10

The upgrading of the Holiday Inn Express to the new generation Holiday

Inn Express bedroom product will commence in August 2015.

The Travelodge Bath Waterside was upgraded to the new Travelodge

bedroom product in 2013, and the Travelodge Bath Central was

upgraded in 2014

2015 Changes in Hotel Ownership

2.2.4. The following hotels have changed ownership in 2015:

Ian and Christa Taylor, owners of the Abbey Hotel, acquired the 20-

bedroom Villa Magdala in June 2015 from its retiring owners. They

reportedly have plans to upgrade the property with new ideas and

concepts.

Rebecca Whittington, one of the sisters behind the Scarlet and Bedruthan

Steps eco-friendly boutique hotels in Cornwall acquired Combe Grove

Manor in July 2015 from The Hotel Collection.

Changes in Bath Hotel Supply 2009-2015

2.2.5. Taking account of new hotel openings and changes to existing hotels, Bath's total

stock of hotel accommodation has increased by 18.2% (250 bedrooms) between

2009 and 2015. There has been a substantial move upmarket in terms of hotel

provision in the city. The most marked trend has been the significant growth in

boutique hotel provision. This has increased sixfold since 2009, albeit from a low

base of just 38 bedrooms, through the repositioning of 2 and 3 star hotels. There

has also been an increase in 4 and 5 star hotel provision. Other key trends have

been an increase in budget/limited service hotel supply, with the opening of the

Premier Inn; a reduction in midmarket full service hotel provision through

upgrading to boutique and 4 star hotels; and the gradual increase in serviced

apartment supply.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 11

Table 5

CHANGES IN BATH HOTEL SUPPLY 2009-2015

Standard of Hotel Hotel Supply % Change

2009-2015

(Rooms) 2009 2015

Hotels Rooms Hotels Rooms 5 star 2 181 4 306 +69.1

Boutique 1 29 5 221 +662.1

4 star 3 223 3 309 +38.6

3 star 10 449 5 192 -57.2

Lower Grade 3 101 2 79 -21.8

Upper-Tier Budget 1 126 1 126 0

Budget 2 191 3 299 +56.5

Serviced Apartments 1 43 5 59 +37.2

Total 23 1343 28 1591 +18.5

Changes to the Hotel Supply in the Surrounding Area

2.2.6. Our research has identified the following changes to the hotel supply surrounding

Bath since 2009:

Luxury Family Hotels acquired Woolley Grange, near Bradford-on-Avon,

from the administrators of Von Essen Hotels in 2011 and has since

refurbished the hotel to a luxury boutique family country house hotel.

Longleat Hotels acquired Homewood Park at Freshford from the

administrators of Von Essen Hotels in 2011 and has since renovated it to a

contemporary country house hotel and spa.

The Old Manor at Trowle Common was acquired by new owners in 2013

and has been renamed as The Moonraker Hotel following refurbishment.

Widbrook Grange at Bradford-on-Avon has new owners.

Home Grown Hotels acquired Hunstrete House at Pensford in 2013 and

reopened it as The Pig near Bath boutique country house hotel in March

2014

The Tracy Park Hotel at Wick was fully refurbished and added 18 bedrooms

in 2013.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 12

2.3. Planned and Proposed Hotel Development

New Hotels Under Construction

2.3.1. There are two hotels currently under construction in Bath - a 177-bedroom 4 star

Apex hotel on James Street West, with extensive conference facilities for up to

400 delegates, and a 148-bedroom, budget boutique Z Hotel as part of the Saw

Close casino development. The Z Hotel is due to open in 2016, while the Apex

Hotel is scheduled to open early in 2017. Further details of the two hotels are

given in the table overleaf.

Proposed New Hotels

2.3.2. The only planning application that has been approved for another new hotel in

Bath is for the conversion of the former King Edward's School on Broad Street to a

12-bedroom boutique hotel and pub. Details are give in the table overleaf.

2.3.3. Bath & North East Somerset Council has also been in pre-application discussions

about a proposal for the conversion of an office building to a 56-bedroom hotel.

2.3.4. A planning application for a 98-bedroom Travelodge next to the Holiday Inn

Express at Brougham Hayes was refused in 2012 and lost at appeal.

2.3.5. A previous permission that was live at the time of the last study, for the conversion

of Green Park House to a hotel, has not happened. It is now to be developed for

student accommodation.

Bath Hotel Futures 2015

___________________________________________________________________________________________________________________________________________

Hotel Solutions July 2015 13

Table 6

BATH – PLANNED/ PROPOSED NEW HOTELS – AS AT JULY 2015

Proposed Hotel Location Standard No

Rooms

Current Status Planned

Opening Year Apex James Street West 4 star 177 Under construction following the demolition of the

Kingsmead House office building on the site. The hotel will

have extensive conference and events facilities for up to

400 delegates, a restaurant and bar, and a leisure pool

and gym. Total investment: £35m

Early 2017

Z Hotel Saw Close Budget

Boutique

148 Under construction. The hotel is being developed as part

of the £14m casino project at Saw Close

2016

Hotel Indigo South Parade Boutique 121 (54 new

rooms)

Atlas Hotels, owners of Pratt's Hotel, has acquired the

adjacent Halcyon Hotel and other linked properties on

South Parade, with a view to converting all of them into a

121-bedroom Hotel Indigo boutique hotel, with

restaurant, bar and gym, that it will operate under a

franchise agreement with InterContinental Hotels Group

(IHG)

2016

Carfax Hotel Great Pulteney

Street

Luxury

Boutique

40 On hold. Plans for the redevelopment and expansion of

the former Carfax temperance hotel into a 40-bedroom

high-end boutique hotel with restaurant and bar have

been dropped following opposition from local residents.

Owners, GECO Properties UK, have indicated that they

intend to draw up new proposals for the redevelopment

of the hotel to take account of the objections. Newbury-

based hotel operator The Vineyard Group is involved in

overseeing the development and management of the

hotel.

n/a

Former King

Edward's School

Broad Street Boutique 12 Planning permission was granted in 2010 and renewed in

2013 for the conversion of the former King Edward's

School into a12-bedroom hotel and pub.

n/a

Francis Hotel Queen Square Boutique 21 Planning permission was granted in 2012 for an extension

to provide an additional 21 bedrooms. It is not known

whether this will proceed.

n/a

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 14

Proposed Development of Existing Hotels

2.3.6. Our research has identified the following proposed investment in the expansion,

development and/or upgrading of existing hotels in Bath:

Atlas Hotels is planning to redevelop the Pratts Hotel and adjoining

Halcyon Hotel and other properties into a 121-bedroom Hotel Indigo

boutique hotel to be operated under a franchise agreement with

InterContinental Hotels Group (IHG). Subject to planning permission being

granted the company aims to open the new hotel at the end of 2016.The

scheme will result in a net increase of 54 bedrooms.

Plans to convert the former Carfax Hotel on Great Pulteney Street into a

40-bedroom high-end boutique hotel are currently on hold following

objections from local residents. The owners of the property, GECO

Properties, have indicated that they intend to draw up a revised scheme.

Further information is given in the table overleaf.

The Royal Crescent has plans to develop a new double-storey

conservatory in 2017 that will give the hotel a larger meeting space to

enable it to target the residential meetings market.

The Bath Priory will be refurbished in 2016.

The Macdonald Bath Spa has plans to redevelop its spa facilities.

The Abbey will refurbish all of its bathrooms in 2015, taking it to a 4 star

boutique standard. It is also adding 2 bedrooms in 2015 and considering

plans to develop a new meeting room.

One of Bath's budget hotels is considering a possible extension to add a

further 19 bedrooms.

The Halcyon Apartments is opening an additional two suites in July 2015.

Another of Bath's serviced apartment operations may add 6 apartments.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 15

Changes in Bath Hotel Supply 2009-2017

2.3.6. The trends in terms of growth in upscale and budget/limited service hotel

provision and the loss of midmarket stock are set to continue in 2016 and 2017

with the opening of the Apex and Hotel Indigo at the upper end of the market,

the Z Hotel in terms of budget/ limited service hotel provision, and the loss of the

Pratt's 3 star hotel to the Hotel Indigo conversion. By 2017 the city's hotel stock will

have increased by 47% (631 rooms) since 2009, with the most significant changes

being the increase in 5 star, 4 star and especially boutique hotel provision, and

the loss of 3 star stock.

Table 7

CHANGES IN BATH HOTEL SUPPLY 2009-2017

Standard of Hotel Hotel Supply % Change

2009-2017

(Rooms) 2009 2017

Hotels Rooms Hotels Rooms 5 star 2 181 4 306 +69.1

Boutique 1 29 5 323 +1013.8

4 star 3 223 4 486 +117.9

3 star 10 449 4 146 -67.5

Lower Grade 3 101 2 79 -21.8

Budget/Limited Service 3 317 5 573 +80.7

Serviced Apartments 1 43 5 61 +41.8

Total 25 1343 29 1974 +47.0

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 16

2.4. Comparisons with Other Historic Cities

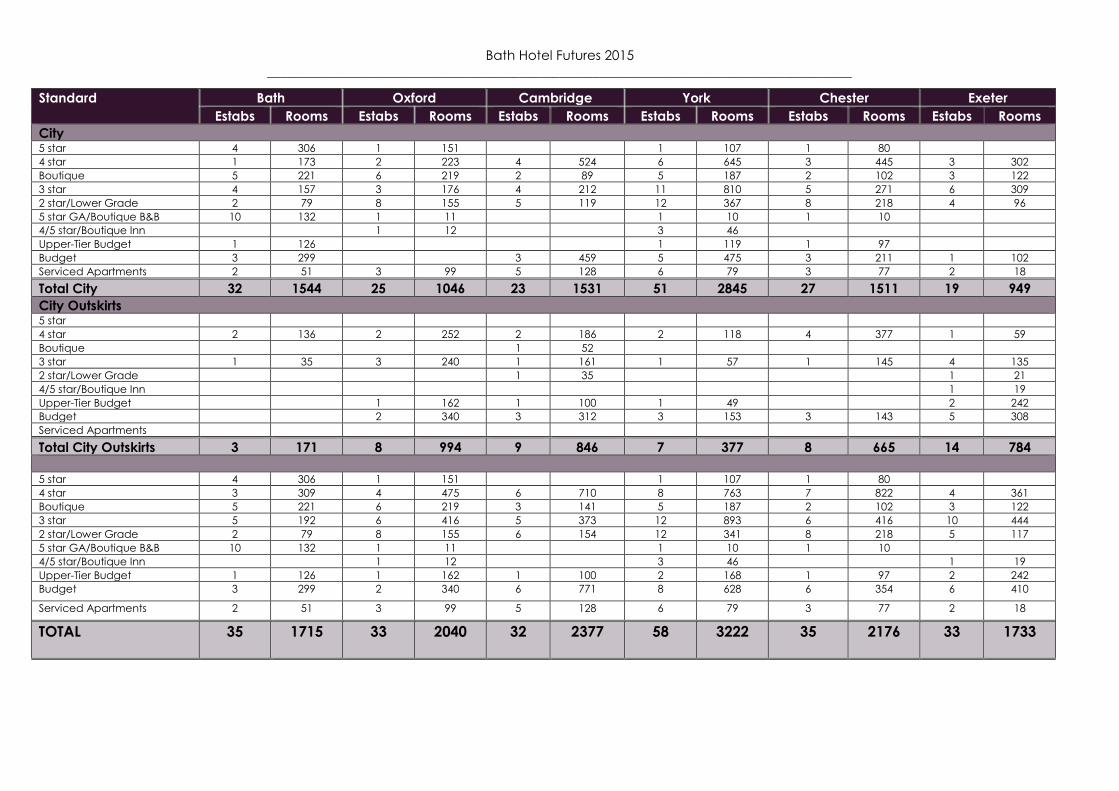

2.4.1. Appendix 3 provides comparisons of current (July 2015) hotel supply, changes in

hotel supply between 2009 and 2015, and planned hotel development in Bath

with Oxford, Cambridge, Chester, York and Exeter. Key observations on these

comparisons are as follows:.

a) Current Hotel Supply

Total Hotel Supply

2.4.2. In terms of total hotel supply Bath has the lowest number of hotel bedrooms of

any of the comparator cities:

York has the most significant hotel supply - almost double the number of

hotel bedrooms that Bath has.

Oxford, Cambridge and Chester have similar numbers of hotel bedrooms -

300-600 more than Bath.

Exeter has a similar number of hotel bedrooms to Bath.

Standard of Hotels

2.4.3. Bath has the most upmarket hotel supply in terms of 5 star and boutique hotel

provision and 5 star guest houses, and more limited supplies of 3 star, 2 star and

budget hotels.

Bath has four 5 star hotels compared to only one in Oxford, York and

Chester and none in Cambridge and Exeter.

Bath has a similar number of boutique hotel bedrooms to Oxford and York

but more than double the boutique hotel supplies of Cambridge, Chester

and Exeter.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 17

Boutique hotels in all six cities are predominantly independent hotels.

Boutique hotel brands represented in the cities are as follows:

o MGallery - Bath

o Malmaison - Oxford

o Hotel du Vin - Cambridge and York

o Hotel Indigo - York

o Abode - Chester and Exeter

o Chapter - Exeter

Bath has the lowest number of 4 star hotel bedrooms. Cambridge, York

and Chester have more than double the number of 4 star hotel bedrooms

that Bath has.

Bath has by far the lowest stock of 3 star and 2 star/lower grade hotel

bedrooms.

Bath has a significant stock of 5 star and boutique guest houses. This type

of accommodation has not so far developed to any extent in the other

cities: Oxford, York and Chester each have only one 5 star guest house,

while Cambridge and Exeter have none.

Exeter and York have two upper-tier budget hotels - a Holiday Inn Express

and a Hampton by Hilton in each case. Bath, Cambridge, Chester and

Oxford each have a Holiday Inn Express.

Bath has the lowest number of budget hotel bedrooms. York and

Cambridge have double the number of budget hotel bedrooms that Bath

has.

Serviced apartments and aparthotels comprise a relatively small element

of the hotel supplies of the six cities. Oxford, Cambridge, York and Chester

have more serviced apartments than Bath. Only Exeter has a smaller

supply of this type of accommodation.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 18

b) Hotel Development 2009-2015

2.4.4. Hotel development trends have been similar across all six comparator cities

between 2009 and 2015: there has been a general move upmarket, with the

upgrading and repositioning of 3 star hotels as 4 star and boutique hotels, the

opening of new 5 star and boutique hotels in some cities, and some loss of poorer

quality 2 star/ lower grade hotel stock; new Premier Inn and/or Travelodge

budget hotels have opened in most of the cities (other than Oxford); and the

supply of serviced apartments and aparthotels has gradually increased:

Bath and York are the only cities that have seen 5 star hotel development.

Bath has seen the most significant increase in boutique hotel provision. This

has been through the repositioning of existing 2 and 3 star hotels. No

entirely new boutique hotels have opened in Bath. All of the other five

cities have seen the opening of new boutique hotels, including a branded

Hotel Indigo in York and an Abode branded boutique hotel in Chester. In

Exeter the former Barcelona boutique hotel has been rebranded under

the Chapter Hotels boutique hotel brand.

None of the six cities have seen the opening of new 4 star hotels in the last

6 years. Two 4 star hotels in Chester have extended.

In terms of upper-tier budget hotel openings, Hampton by Hilton hotels

have opened in York and Exeter. In York the Ramada Encore has been

repositioned as a Travelodge, resulting in only a marginal net change in

the city's upper-tier budget hotel supply.

All of the cities apart from Oxford have seen an increase in budget hotel

provision. Cambridge has seen a significant increase in its budget hotel

supply, with the opening of two Premier Inn and two Travelodge hotels

since 2009. Exeter has seen the opening of two Premier Inns (with a third

due to open in October 2015), while York has seen the opening of a new

Premier Inn and the repositioning of the Ramada Encore to a Travelodge.

Chester has seen the opening of a new Premier Inn but the closure of the

former Comfort Inn. A Travelodge also opened in Chester in 2010 but was

subsequently sold in 2013 for conversion to student accommodation. Bath

has seen the opening of a Premier Inn.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 19

Bath, York and Chester have each seen the closure of a 2 star hotel.

All of the six cities have seen a gradual increase in serviced apartment/

aparthotel provision. Cambridge, York and Chester have seen more

significant rises in their supplies of these types of accommodation. Bath,

Oxford and Exeter have seen only a marginal growth in such provision.

c) Planned Hotel Development

2.4.5. All of the comparator cities look set to see more hotel development than Bath

going forward (if all of the current hotel proposals are progressed):

York and Cambridge are set to see an increase in 5 star hotel provision,

with the planned expansion of The Grand in York and the current

upgrading of the University Arms in Cambridge as a landmark hotel for the

city.

Bath is the only city with a new 4 star hotel currently under construction,

however proposals for new 4 star hotels are also being progressed in

Cambridge and look likely to come forward in Oxford, Exeter and possibly

York.

There are plans for Hotel Indigo boutique hotels in Bath and Oxford and

proposals for new small independent boutique hotels in Bath, Oxford and

Cambridge.

Bath is the only city that is set to see the opening of a budget boutique

hotel, with the Z Hotel being progressed here.

At the 3 star level, a Hilton Garden Inn is planned in York and 3 star hotel

schemes could come forward in Cambridge, Chester and Exeter.

A second Travelodge is currently under construction in Oxford, while a

fourth Premier Inn will open in Exeter in October 2015. There are plans for

Ibis budget hotels in Cambridge and Chester. Bath, York, Chester and

Oxford are all target locations for further Premier Inn hotels, while

Travelodge has Exeter, York and Bath as targets for additional hotels.

A 133-apartment aparthotel has been approved in Cambridge, while

Roomzzz has plans to open an aparthotel in York.

Bath Hotel Futures 2015

______________________________________________________________________________________

Hotel Solutions July 2015 20

3. CURRENT HOTEL PERFORMANCE & MARKETS

_______________________________________________________________________________________

3.1. Occupancy, Achieved Room Rates1 and Revpar2

3.1.1. Our estimates of average annual room occupancies, achieved room rates and

revpar figures for Bath hotels for 2012 - 2014 and forecast figures for 2015 are

summarised in the table overleaf. These figures are based on the information

provided by the city's hotel managers and owners.

3.1.2. Key points to note in relation to hotel performance in Bath and changes since 2012

are as follows:

Hotel performance in Bath is very strong at all levels in the market, and well

ahead of national averages.

Boutique, 3 star and budget hotels are performing particularly well in the

city. 5 star hotels achieve lower room occupancies but very high average

room rates, largely due to the numbers of suites that they have, which

command high prices but do not always fill.

Hotel performance in Bath has generally strengthened between 2012 and

2014 and looks set to improve further in 2015.

Occupancies and average room rates are rebuilding for some hotels

following reopening after major refurbishment.

Boutique hotel occupancies and average room rates dipped in 2013 as

new boutique hotels, guest houses and B&Bs have opened. Boutique hotel

occupancies have quickly recovered in 2014 and 2015 as the new boutique

hotels have become more established, and average room rates have

started to increase for some boutique hotels in 2015 .

1 The amount of rooms revenue (excluding food and beverage income) that hotels achieve per

occupied room net of VAT, breakfast (if included) and discounts and commission charges. 2 The amount of rooms revenue (excluding food and beverage income) that hotels achieve per

available room net of VAT, breakfast (if included) and discounts and commission charges.

Bath Hotel Futures 2015

___________________________________________________________________________________________________________________________________________

Hotel Solutions July 2015 21

Table 8

BATH HOTEL PERFORMANCE 2012-2015

Standard of Hotel Average Annual Room

Occupancy

%

Average Annual Achieved

Room Rate4

£

Average Annual Revpar5

£

2012 2013 2014 2015f3 2012 2013 2014 2015f3 2012 2013 2014 2015f3

UK Provincial Hotels (All Standards)1 69.8 72.6 75 766 59.22 59.94 62.07 64.736 41.32 43.53 46.37 49.146

UK Provincial 3/4 Star Chain Hotels2 69.6 72.0 73.9 n/a 69.97 71.46 76.49 n/a 48.72 51.48 56.53 n/a

5 star 65 n/a 72 74 169 n/a 165 177 110 n/a 119 131

4 star n/a n/a 76 79 n/a n/a 92 100 n/a n/a 70 79

Boutique 86 80 85 86 129 112 116 121 111 89 99 105

3 star 77 81 82 83 73 74 77 78 56 60 63 64

Budget n/a n/a 87 88 n/a n/a 77 83 n/a n/a 67 73

Serviced Apartments n/a n/a 83 84 n/a n/a 107 114 n/a n/a 88 96

All Hotels n/a n/a 81 83 n/a n/a 100 107 n/a n/a 81 88

Source: Hotel Solutions – July 2015

Notes 1. Source: STR Global

2. Source: TRI Hotstats UK Chain Hotels Market Review

3. Based on forecast figures provided by hotel managers

4. The amount of rooms revenue (excluding food and beverage income) that hotels achieve per occupied room net of VAT, breakfast (if included) and

discounts and commission charges.

5. The amount of rooms revenue (excluding food and beverage income) that hotels achieve per available room net of VAT, breakfast (if included) and

discounts and commission charges

6. PwC UK Hotel Forecast 2015

Bath Hotel Futures 2015

________________________________________________________________________________________

Hotel Solutions July 2015 22

5 star hotel occupancies have improved but average room rates have dropped

back slightly as hotels have reduced their room rates to drive occupancy.

3 star hotel performance has strengthened year on year.

Some 3 star and boutique hotels have successfully grown their occupancies by

driving more midweek business through more effective use of OTAs1, especially

booking.com, and greater flexibility on room rates.

The opening of the new Premier Inn in December 2013 does not appear to have

had anything other than a marginal impact on the city's established hotels, with

most hotels reporting occupancy and average room rate growth in 2014, and

the Premier Inn quickly achieving high occupancies.

3.2 Patterns of Demand

3.2.1. Our estimates of average annual weekday and weekend occupancies for hotels

in Bath for 2014 are summarised in the table below.

Table 9

BATH HOTELS - WEEKDAY/ WEEKEND OCCUPANCIES – 2014

Standard Typical Room Occupancy

%

Mon-

Thurs

Fri Sat Sun

5 Star Hotels Winter 56 71 91 45

Summer 72 90 95 67

4 Star Hotels Winter 70 82 93 54

Summer 81 90 97 71

Boutique Hotels Winter 73 90 99 67

Summer 88 92 99 81

3 Star Hotels Winter 78 86 89 61

Summer 91 96 99 73

Budget Hotels Winter 81 85 96 56

Summer 91 96 99 81

Source: Hotel Solutions – July 2015

1 Online travel agents, such as booking.com, LateRooms, Expedia, hotels.com,

lastminute.com

Bath Hotel Futures 2015

________________________________________________________________________________________

Hotel Solutions July 2015 23

3.2.2. Key points to note are as follows:

Friday and Saturday occupancies are very high for Bath hotels. Hotels of all

standards consistently fill and turn business away on Saturday nights throughout

the year and achieve high occupancies on Friday nights, particularly during the

summer months. Friday occupancies dip a little in winter for most hotels.

Midweek and Sunday occupancies are more seasonal. They are strong in the

summer but weaker during the winter months, especially January, February and

March. 3 star and budget hotels achieve the highest midweek occupancies,

both during the summer and in the winter. They attract stronger year-round

demand from more price conscious corporate customers and overseas tourists,

and also attract business from contractors working on construction and shop

fitting projects in the city. Some boutique hotels are also successfully driving

midweek business through OTAs (online travel agents such as booking.com and

Expedia) and a more flexible room rate strategy.

There is a significant difference between midweek and Friday and Saturday

achieved room rates at all levels in the Bath hotel market. A differential of £30-50

is typical. Some hotels reported a differential of £80-100. There is also a

differential between summer and winter rates, particularly during the winter ,

when midweek and Sunday room rates are much lower and Friday night prices

also reduce.

Bath Hotel Futures 2015

________________________________________________________________________________________

Hotel Solutions July 2015 24

3.3. Midweek Markets

3.3.1. Our estimates of the midweek market mix for Bath hotels are set out in the table

below, based on the estimates provided by the city's hotel managers and owners.

Table 10

BATH HOTELS - ESTIMATED MIDWEEK MARKET MIX 2014

Standard

of Hotel

Market

Corporate/

University

%

Contractors

%

Residential

Conference

%

UK Leisure

Breaks

%

Overseas

Tourists

%

Group

Tours

%

5 Star 7 5 72 15 1

4 Star 22 26 26 11 15

Boutique 16 1 55 20 8

3 Star 7 1 1 42 25 24

Budget 33 8 19 39 1

3.3.2. Our key findings regarding midweek demand for hotel accommodation in Bath are

as follows:

Corporate demand for hotel accommodation in Bath is relatively weak,

particularly at the top end of the market. There are few major companies in

Bath that generate good volumes of business for the city's hotels. Corporate

demand is stronger for budget hotels, suggesting that this market is largely

price driven in Bath. Few hotels reported attracting any corporate business

from Bristol companies.

Residential conferences are a very minor market for most of Bath's hotels,

other than Bailbrook House, which as a former residential conference centre

has extensive conference facilities. Most of the city's other hotels have very

limited conference and meeting facilities so are unable to target the

residential conference market. The residential conferences that the city's

hotels attract tend to be relatively small (10-30 delegates) and stay for 1-2

nights. Demand comes primarily from companies in London and the M4

Corridor.

Budget hotels attract midweek demand from contractors working on

construction and shop fitting projects in the city.

Bath Hotel Futures 2015

________________________________________________________________________________________

Hotel Solutions July 2015 25