Embed Size (px)

Citation preview

26th Annual

Tuesday & Wednesday, January 24‐25, 2017 Hya Regency Columbus, Columbus, Ohio

Oh

io T

ax

Workshop OO

Basic:

Ohio CAT … Common Audit Issues Including

‘Agency Exclusion’

Wednesday, January 25, 2017 2:00 p.m. to 3:00 p.m.

Biographical Information

Javan A. Kline, Attorney at Law, Frost Brown Todd LLC 301 East Fourth Street, Suite 3300, Cincinnati, Ohio 45202

[email protected] (513) 651-6892

Javan A. Kline is an attorney in the Cincinnati office of Frost Brown Todd LLC focusing his practice on state and local tax matters. Mr. Kline advises clients on a variety of multistate, state and local tax matters involving sales and use taxes, business income and franchise taxes, the Ohio commercial activity tax, personal and real property taxes, personal income taxes, and incentive projects. Mr. Kline represents clients in tax controversies before the Ohio Department of Taxation, the Internal Revenue Service and other state and local taxing authorities. Mr. Kline is an Adjunct Instructor at the University of Cincinnati Lindner College of Business where he has taught courses on State and Local Taxation, IRS Practice and Procedure and Corporate Legal and Social Responsibility. Mr. Kline holds a B.B.A. (Finance) from the University of Notre Dame and a J.D. from the University of Cincinnati College of Law.

Kevin M. Zins, Partner and State and Local Tax Services Practice Leader (Cincinnati) Grant Thornton LLP, 3825 Edwards Road, Suite 430, Cincinnati, OH 45209 [email protected] 513-345-4528 Fax 513-241-6125

Kevin Zins specializes in multi-state tax matters and state tax planning. He has more than 25 years of experience working with manufacturing, distribution, retail and financial companies. Kevin’s experience covers both industrial and consumer products businesses. Outside of public accounting, his experience includes approximately four years in the accounting and tax department of Cintas Corporation, a corporate identity uniform manufacturer, distributor and industrial laundry service company with operations in about 40 states. Kevin has a broad base of federal tax, state tax and project management experience.

Kevin conducts multi-state tax return reviews for income, franchise, sales/use and payroll taxes; identifies state tax credit opportunities; develops, designs and implements strategic tax planning services for large and mid-size, multi-state corporations; participates in due diligence reviews relating to restructuring transactions (including acquisitions, divestitures and mergers); conducts nexus reviews and negotiates voluntary disclosure agreements to minimize liabilities and exposures; negotiates for audit defense, including representing clients for income, sales and use, and property tax challenges.

Kevin is a member of the AICPA, as well as the Society of Certified Public Accounts for Ohio, Kentucky and Indiana, in addition to serving as a Tax Committee Member and/or Contributor. Kevin is also a Tax Committee Member and/or Contributor to the Ohio, Kentucky and Indiana Chamber of Commerce. Kevin received his Bachelor of Business Administration in Accounting from Bowling Green State University.

Benjamin L. Waterman, Division Counsel – Commercial Activity Tax, Petroleum Activity Tax, Alcoholic Beverage Excise Tax, Tire Fee, Ohio Department of Taxation, Office of Chief Counsel,

4485 Northland Ridge Blvd., Columbus, OH 43229 [email protected] 614-995-5739

Ben joined the Department of Taxation in June of 2013 as a tax commissioner agent in the Commercial Activity Tax Division. After a brief stint as counsel to the Department’s Bankruptcy Division, Ben became Division Counsel for the commercial activity tax, petroleum activity tax, beer and wine excise taxes, and the replacement tire fee. As Division Counsel, Ben is primarily responsible for providing legal advice and analysis to multiple internal clients; drafting legislation, administrative rules, information releases, contracts, tax commissioner opinions, and correspondence; and working with taxpayers and tax professionals to resolve legal questions or issues. Ben is a graduate of The Ohio State University with a B.A. in English and earned his law degree from Capital University Law School in Columbus, Ohio.

Biographical Information

Geoffrey A. Frazier, Tax Director - State and Local Tax Services Grant Thornton LLP, 3825 Edwards Road, Suite 430, Cincinnati, OH 45209

[email protected] 513-345-4620 Fax 513-241-6125 Geoffrey Frazier specializes in state and local tax matters and tax planning. He has more than 25 years of experience in federal and state & local taxation. Geoff has experience in both public accounting and industry. In industry, he was tax manager at a large public retail company which had department stores located in eighteen states. In public accounting, he has focused on state and local tax consulting. Geoff helps large and midsize multi-state organizations manage their state and local tax liabilities. He has experience in numerous industries including retail, manufacturing, consumer products, construction, and services. He has broad experience in the areas of state income and franchise tax, municipal income tax, personal and real property tax, sales and use tax, payroll taxes including unemployment tax, procuring tax credits and incentives, gross receipts, and other miscellaneous taxes. He has assisted clients with state & local tax compliance and planning, nexus determinations and related voluntary disclosure and amnesty filings, tax audits, incentive negotiations, business acquisition/disposition due diligence and tax accounting issues. Geoff is a member of the AICPA, the Indiana CPA Society and the OSCPA, as well as the Indiana CPA Society Tax Resource Advisory Council and the Indiana Chamber of Commerce Tax Committee. Geoff is a graduate of the University of Cincinnati with a Bachelor of Business Administration – Accounting.

Darren S. Miller, Tax Examiner Manager, Ohio Department of Taxation 4485 Northland Ridge Blvd., Columbus, OH 43229

[email protected] 614-800-4158 Darren started his career with the Ohio Department of Taxation in the Zanesville District Office in 1984 as a Personal Property Tax Auditor. In 1986, Darren became an audit manager of a group of auditors specializing in personal property taxes. With the Commercial Activity Tax starting in 2005, Darren was part of the initial team of management to learn the tax, train personnel and assist in establishing an audit and compliance program for the Department. Darren’s current audit group completes reviews for commercial activity, petroleum activity and employer withholding taxes. Darren has served in numerous training and presentation roles for the Department. Darren is a graduate of Belmont College with degrees in Accounting and Computer Programming.

.

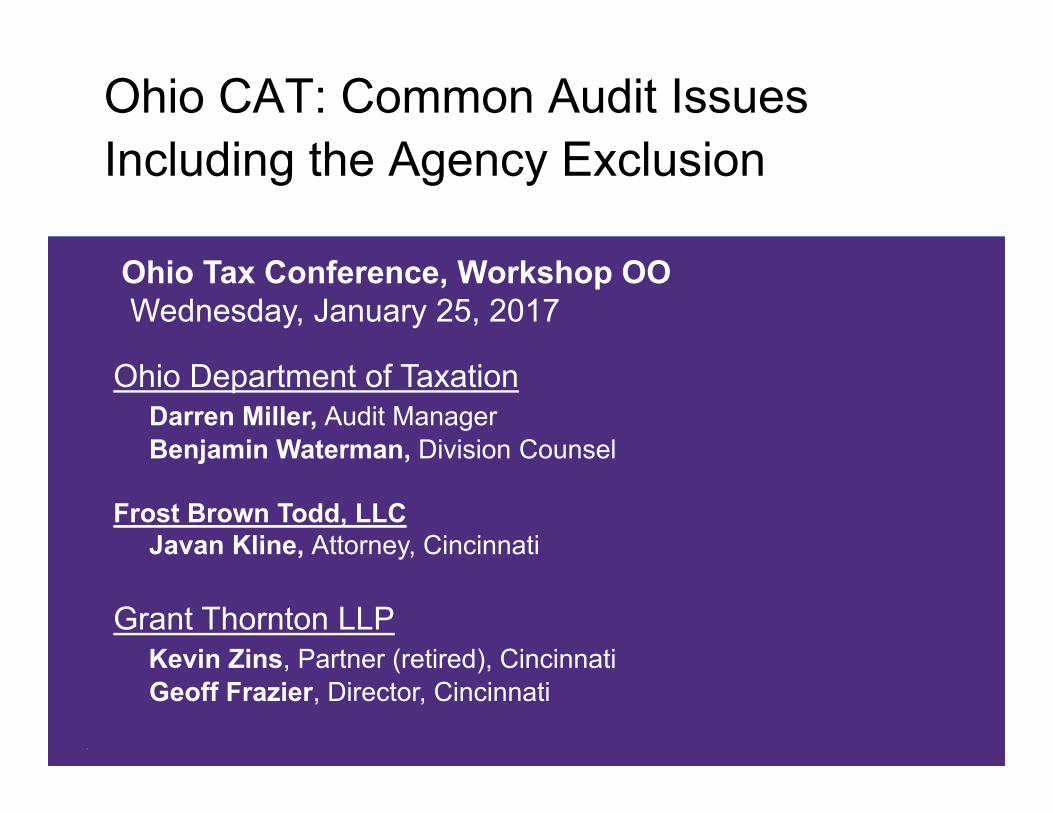

Ohio CAT: Common Audit IssuesIncluding the Agency Exclusion

Ohio Department of Taxation Darren Miller, Audit ManagerBenjamin Waterman, Division Counsel

Frost Brown Todd, LLCJavan Kline, Attorney, Cincinnati

Grant Thornton LLPKevin Zins, Partner (retired), Cincinnati Geoff Frazier, Director, Cincinnati

Ohio Tax Conference, Workshop OOWednesday, January 25, 2017

.2

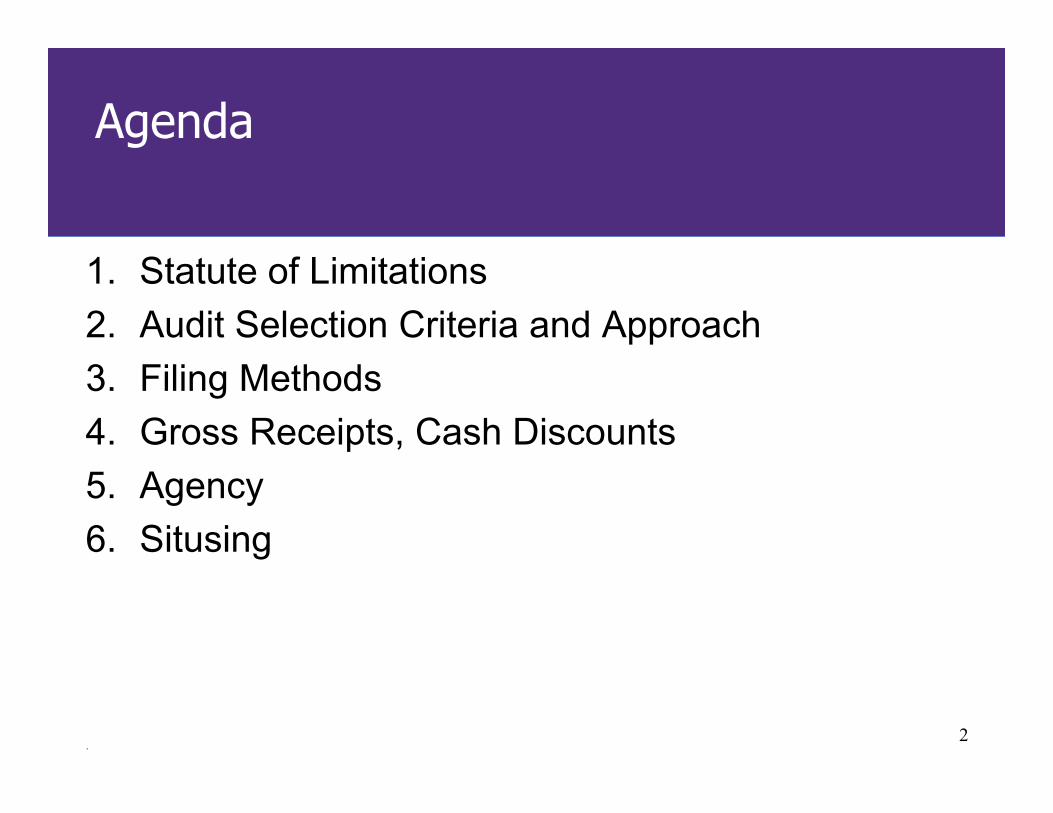

Agenda

1. Statute of Limitations2. Audit Selection Criteria and Approach3. Filing Methods4. Gross Receipts, Cash Discounts 5. Agency6. Situsing

© Grant Thornton LLP. All rights reserved.

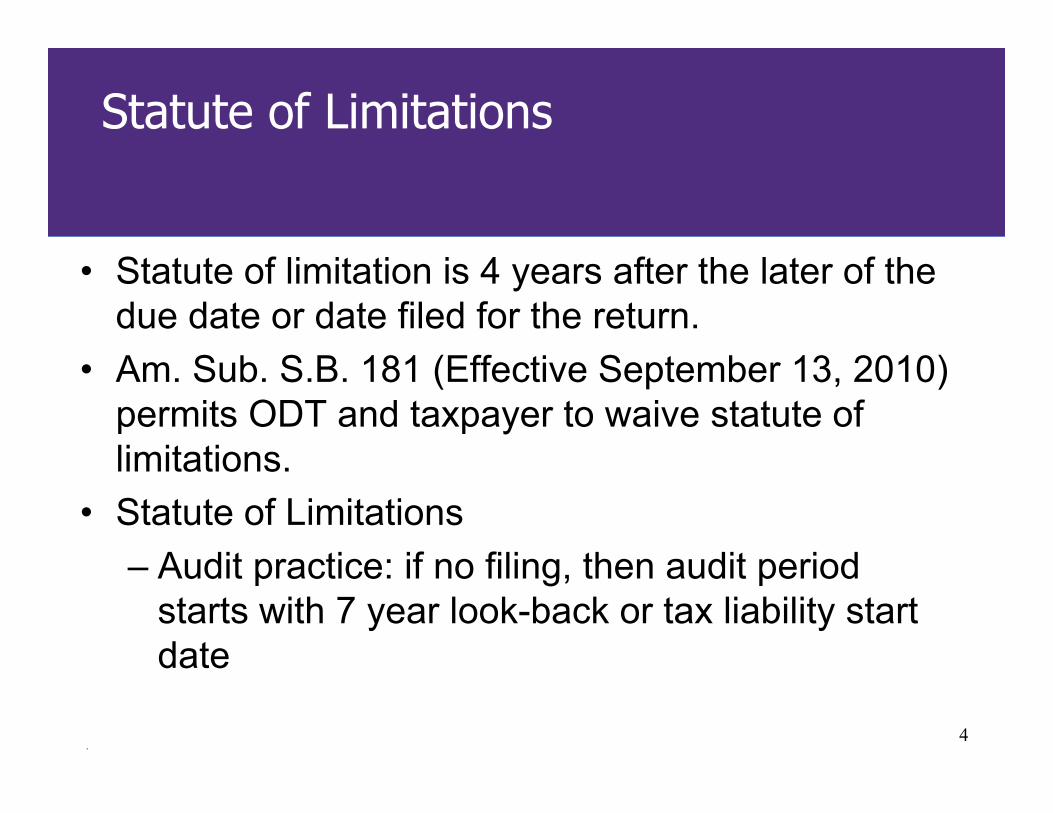

1. Statute of Limitations

.4

• Statute of limitation is 4 years after the later of the due date or date filed for the return.

• Am. Sub. S.B. 181 (Effective September 13, 2010) permits ODT and taxpayer to waive statute of limitations.

• Statute of Limitations– Audit practice: if no filing, then audit period

starts with 7 year look-back or tax liability start date

Statute of Limitations

© Grant Thornton LLP. All rights reserved.

2. Audit Selection Criteria and Approach

.6

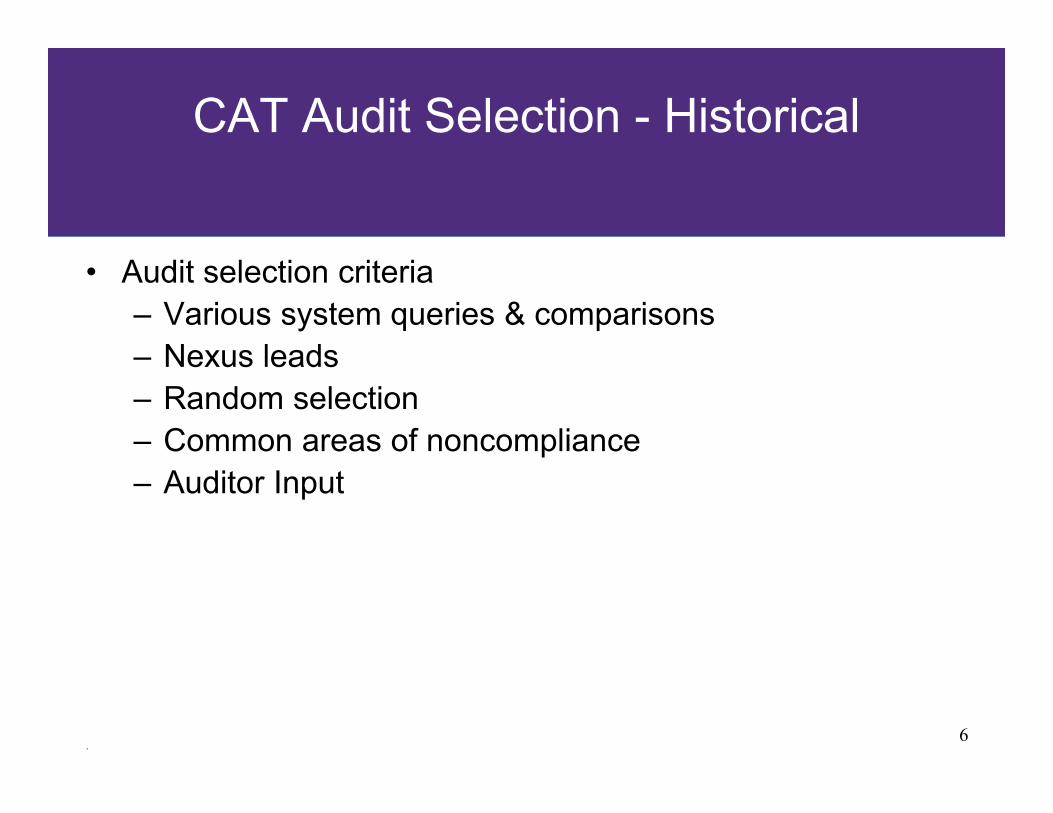

CAT Audit Selection - Historical

• Audit selection criteria– Various system queries & comparisons– Nexus leads– Random selection– Common areas of noncompliance– Auditor Input

.7

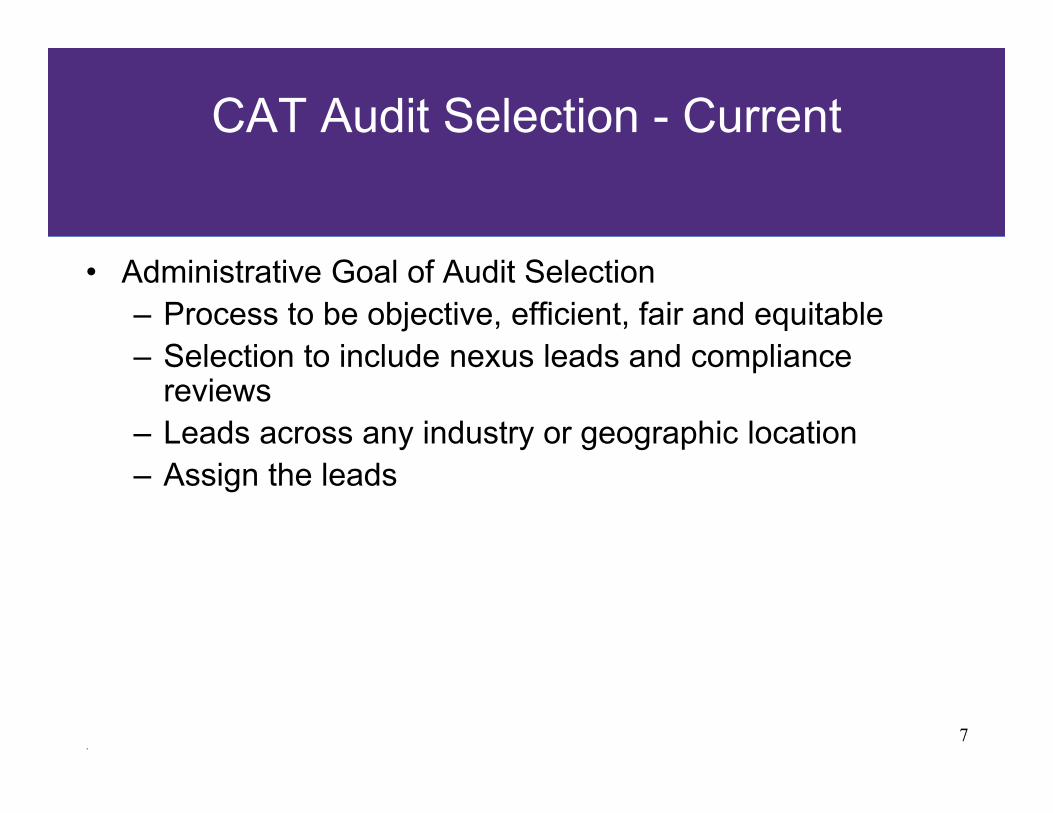

CAT Audit Selection - Current

• Administrative Goal of Audit Selection– Process to be objective, efficient, fair and equitable– Selection to include nexus leads and compliance

reviews– Leads across any industry or geographic location– Assign the leads

.8

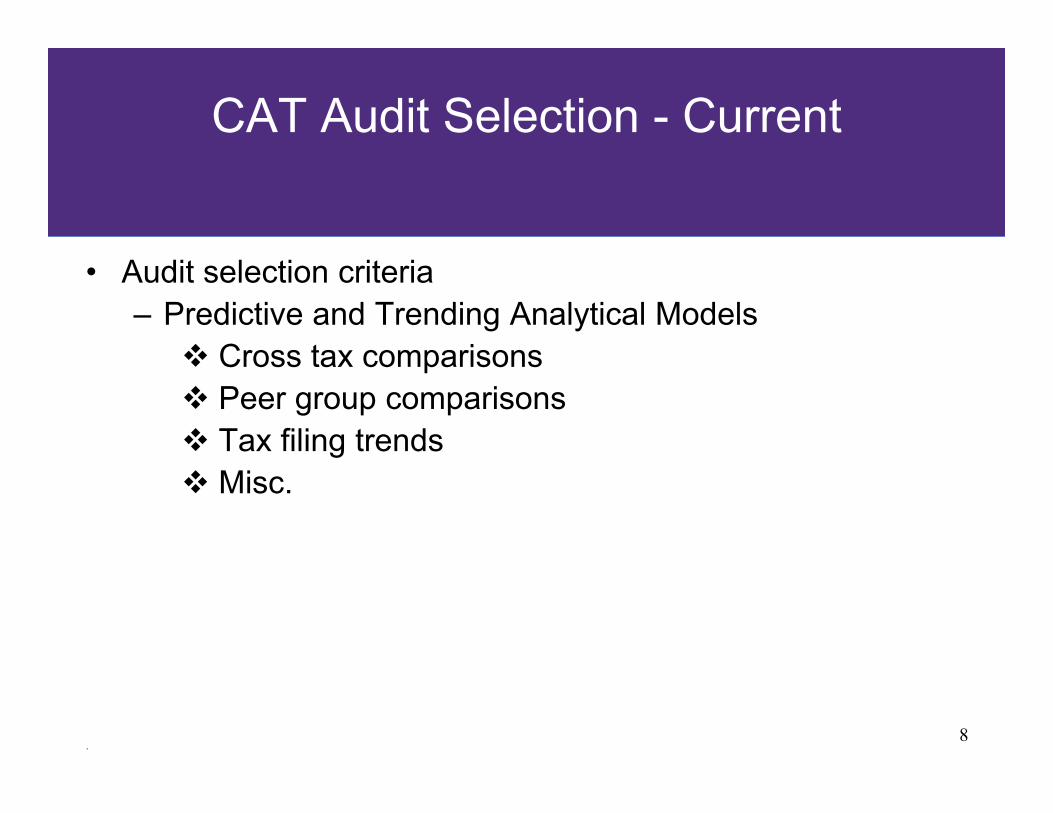

CAT Audit Selection - Current

• Audit selection criteria– Predictive and Trending Analytical Models Cross tax comparisons Peer group comparisons Tax filing trends Misc.

.9

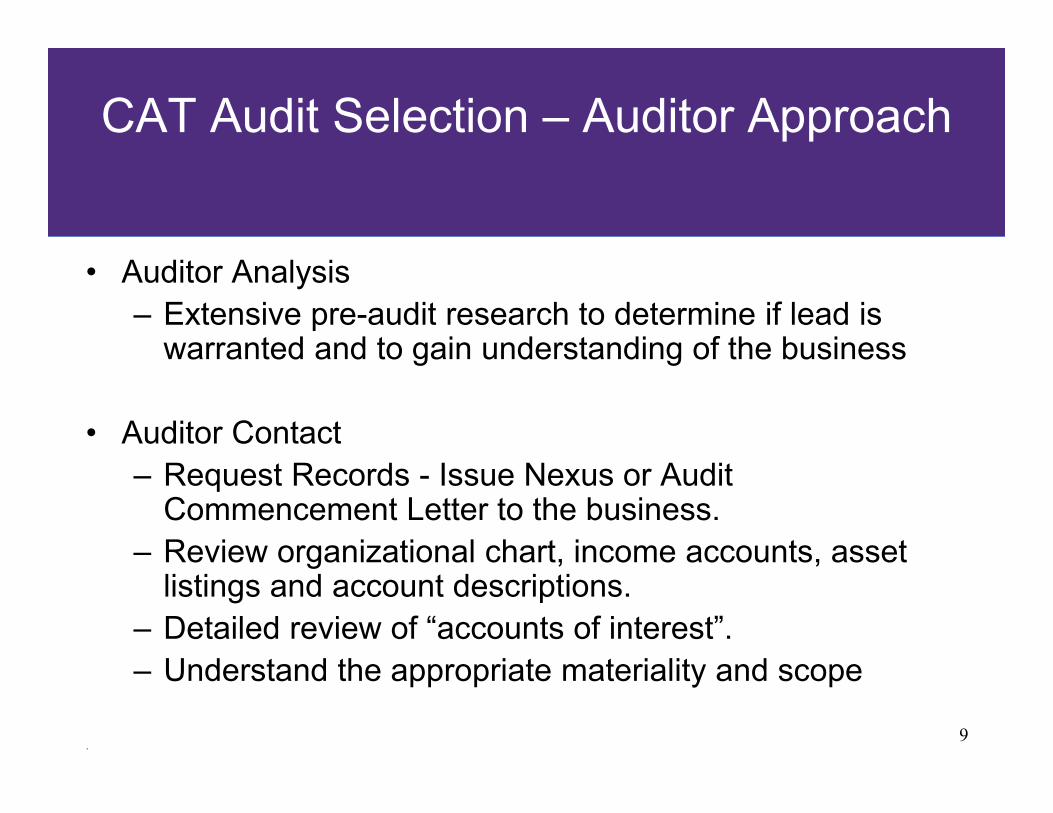

CAT Audit Selection – Auditor Approach

• Auditor Analysis– Extensive pre-audit research to determine if lead is

warranted and to gain understanding of the business

• Auditor Contact– Request Records - Issue Nexus or Audit

Commencement Letter to the business.– Review organizational chart, income accounts, asset

listings and account descriptions.– Detailed review of “accounts of interest”.– Understand the appropriate materiality and scope

.10

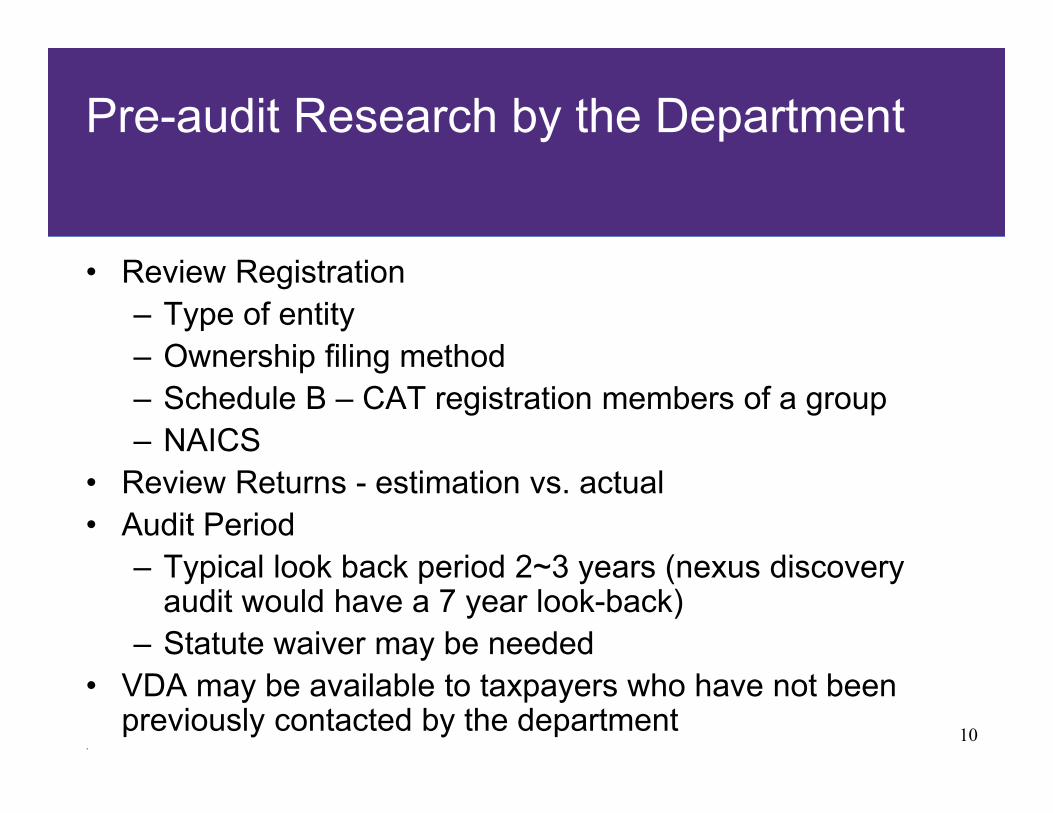

Pre-audit Research by the Department

• Review Registration– Type of entity– Ownership filing method– Schedule B – CAT registration members of a group– NAICS

• Review Returns - estimation vs. actual• Audit Period

– Typical look back period 2~3 years (nexus discovery audit would have a 7 year look-back)

– Statute waiver may be needed• VDA may be available to taxpayers who have not been

previously contacted by the department

.11

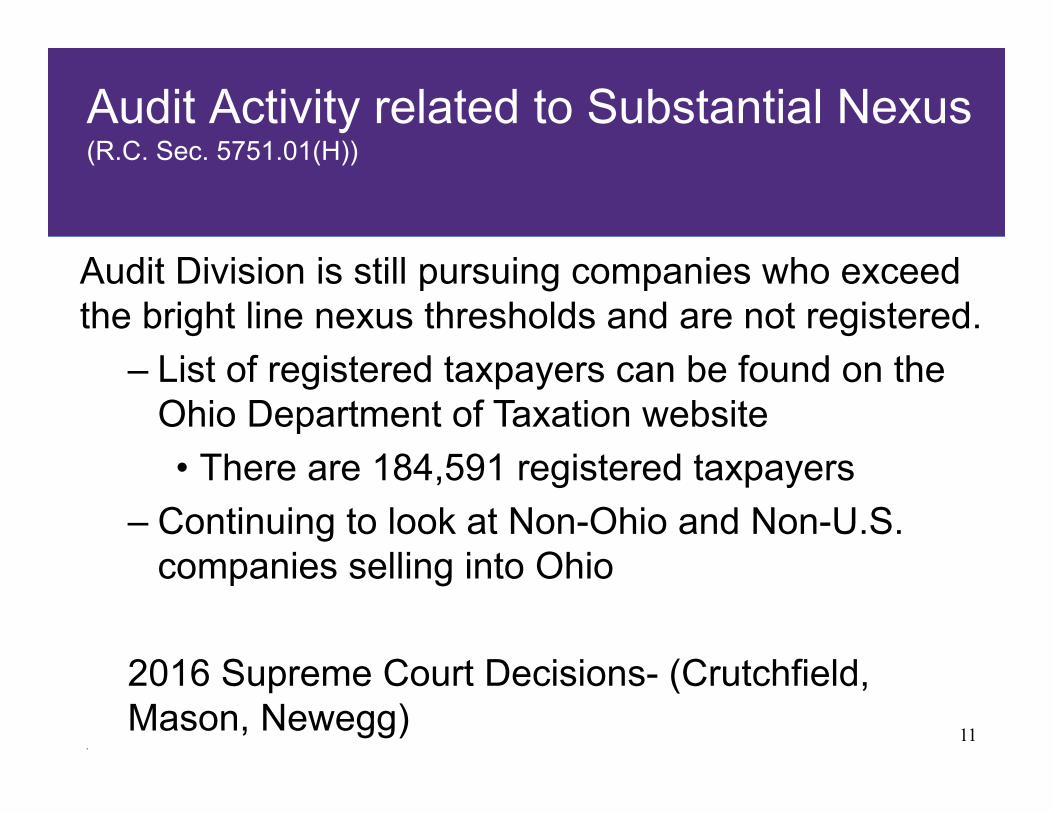

Audit Division is still pursuing companies who exceed the bright line nexus thresholds and are not registered.

– List of registered taxpayers can be found on the Ohio Department of Taxation website• There are 184,591 registered taxpayers

– Continuing to look at Non-Ohio and Non-U.S. companies selling into Ohio

2016 Supreme Court Decisions- (Crutchfield, Mason, Newegg)

Audit Activity related to Substantial Nexus (R.C. Sec. 5751.01(H))

.12

Interview Document and Construction of Audit Remarks

• Describe activity of taxpayer• Examine other tax type activity• Define scope of audit• Document audit findings• Describe any objections and their basis• Provide audit trail for appeals process

.13

ODT Resources for Background Investigation

• STARS• Ohio’s Workfront System – audit management

system• Review of prior audit records which are stored in a

central location• Review of other tax types

.14

Outside Resources for Background Investigations

• Taxpayer’s website• Internet searches (Google, Yahoo!)• Hoover’s• SEC documents• Government Agencies

– Secretary of State– IRS

© Grant Thornton LLP. All rights reserved.

3. Filing Methods

.16

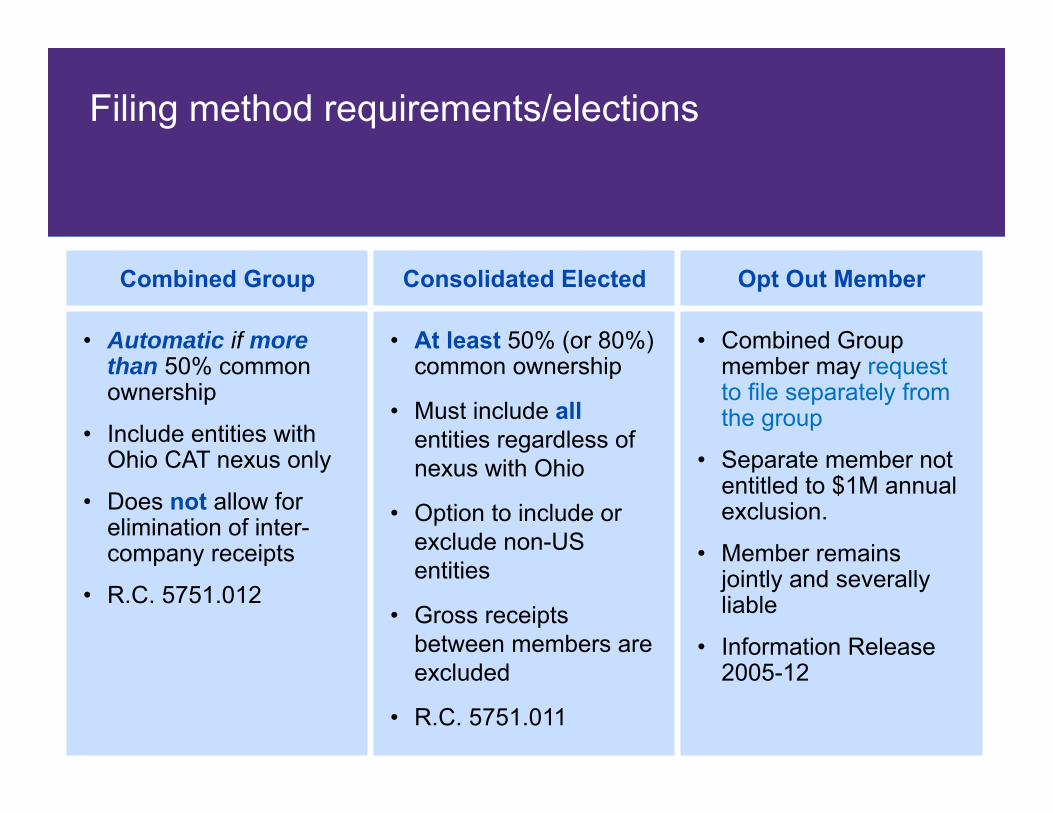

Filing method requirements/elections

Combined Group Consolidated Elected Opt Out Member

• Automatic if more than 50% common ownership

• Include entities with Ohio CAT nexus only

• Does not allow for elimination of inter-company receipts

• R.C. 5751.012

• At least 50% (or 80%) common ownership

• Must include allentities regardless of nexus with Ohio

• Option to include or exclude non-US entities

• Gross receipts between members are excluded

• R.C. 5751.011

• Combined Group member may request to file separately from the group

• Separate member not entitled to $1M annual exclusion.

• Member remainsjointly and severally liable

• Information Release 2005-12

.17

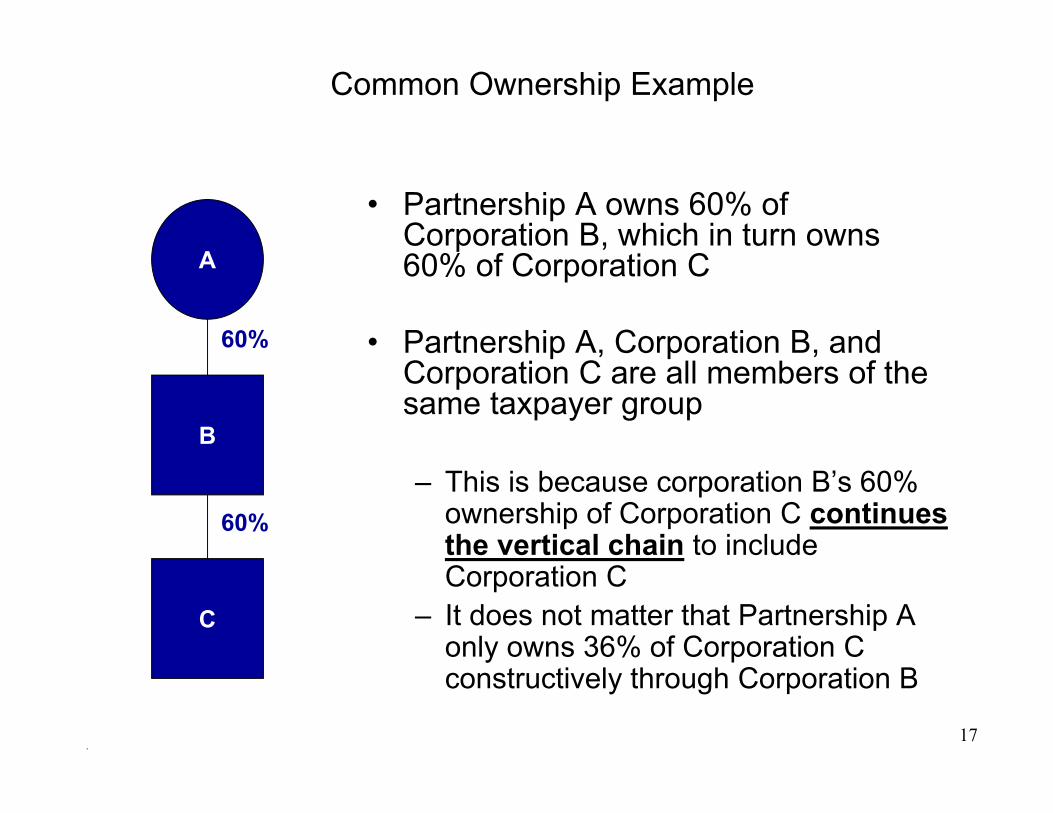

Common Ownership Example

A

B

60%

60%

C

• Partnership A owns 60% of Corporation B, which in turn owns 60% of Corporation C

• Partnership A, Corporation B, and Corporation C are all members of the same taxpayer group

– This is because corporation B’s 60% ownership of Corporation C continues the vertical chain to include Corporation C

– It does not matter that Partnership A only owns 36% of Corporation C constructively through Corporation B

.18

Common Ownership Audit Example

After Audit Review1. entire group is combined except for K2. result could be different depending on consolidation election

Taxpayer initial groupsgroup 1 – J, E, M, Tgroup 2 – S, Ogroup 3 – Y, Z, A

50% Consol Elected GroupJ-E-M-T-Y-Z-A-S-O

80% Consol Elected GroupJ-E-M-TS-O (sep. combined grp)Y-Z-A (sep. combined grp)

J

ME

K

Y

Z

100%100%75%25%

A

100%

100%

S

T

100%

75%

25%

O

100%

Future filing options

.19

Combined / Consolidated Ownership -Audit Issues

• Individuals (human beings) can be common owners

• Constructive ownership

• Vertical ownership and control test for consolidated elected and combined taxpayer groups– I.R.C. section 318 (family) attribution rules do NOT apply

• Election to file consolidated– what to do with the other potential Ohio filers– foreign entities

• Requests for retroactive consolidation generally not allowed– Original election – correction of group election – or potential invalid election?

.20

Combined / Consolidated Ownership –Equity Group Audit Issues

Equity ownership group issues• Ohio looks principally at the control (voting rights) for determination of

the combined group– GP has control, LLC managing member has control– LLC and LP ownership addressed in OAC 5703-29-02(D)(3)

• Trace the ownership up to the partners (Human Beings)• The real exposure…the exclusion amount for each entity or the

minimum tax

Possible solutions• Request to file separate• Portfolio group consolidated group opt out NOT an option

Challenges • Portfolio companies added and sold• What if you do not know the ownership structure

© Grant Thornton LLP. All rights reserved.

4. Gross Receipts, Cash Discounts

.22

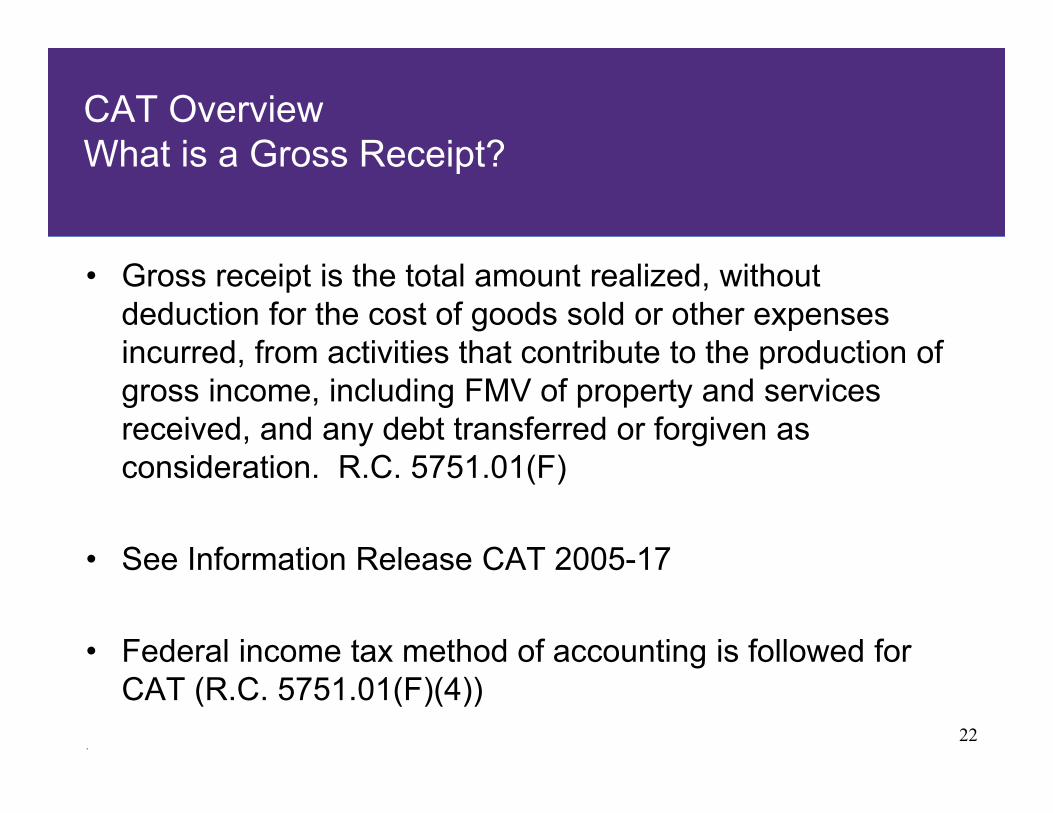

• Gross receipt is the total amount realized, without deduction for the cost of goods sold or other expenses incurred, from activities that contribute to the production of gross income, including FMV of property and services received, and any debt transferred or forgiven as consideration. R.C. 5751.01(F)

• See Information Release CAT 2005-17

• Federal income tax method of accounting is followed for CAT (R.C. 5751.01(F)(4))

CAT Overview What is a Gross Receipt?

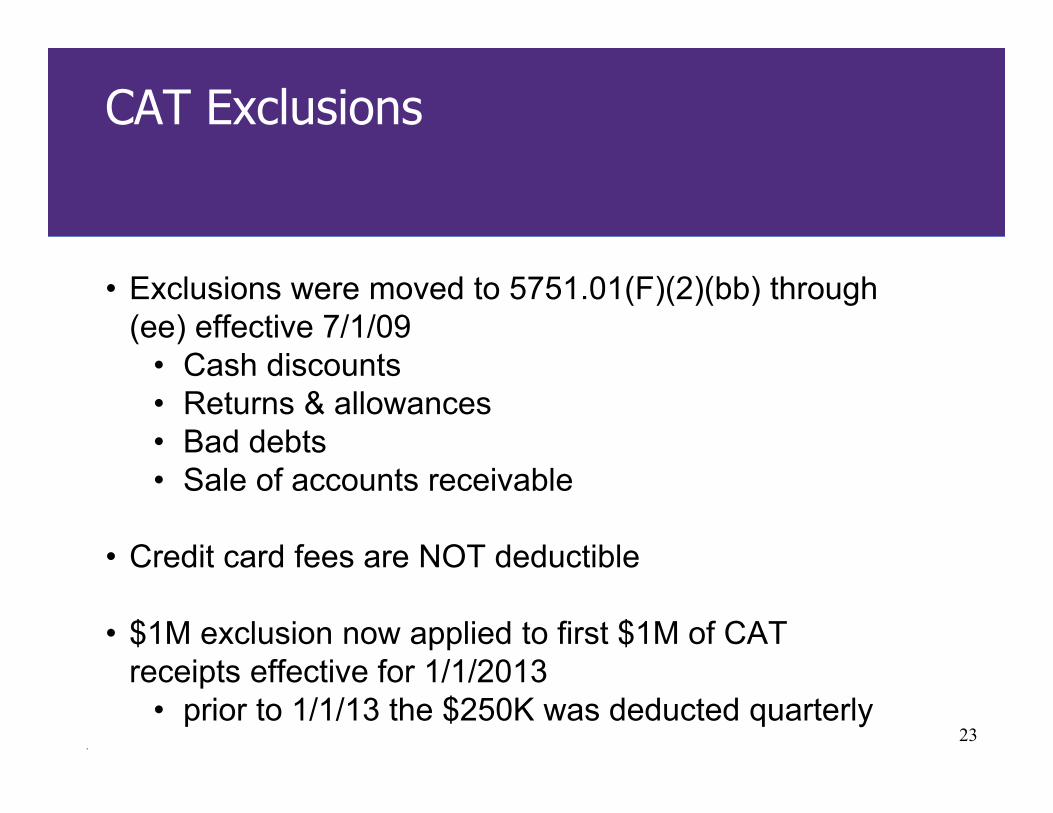

.23

• Exclusions were moved to 5751.01(F)(2)(bb) through (ee) effective 7/1/09

• Cash discounts• Returns & allowances• Bad debts• Sale of accounts receivable

• Credit card fees are NOT deductible

• $1M exclusion now applied to first $1M of CAT receipts effective for 1/1/2013

• prior to 1/1/13 the $250K was deducted quarterly

CAT Exclusions

.24

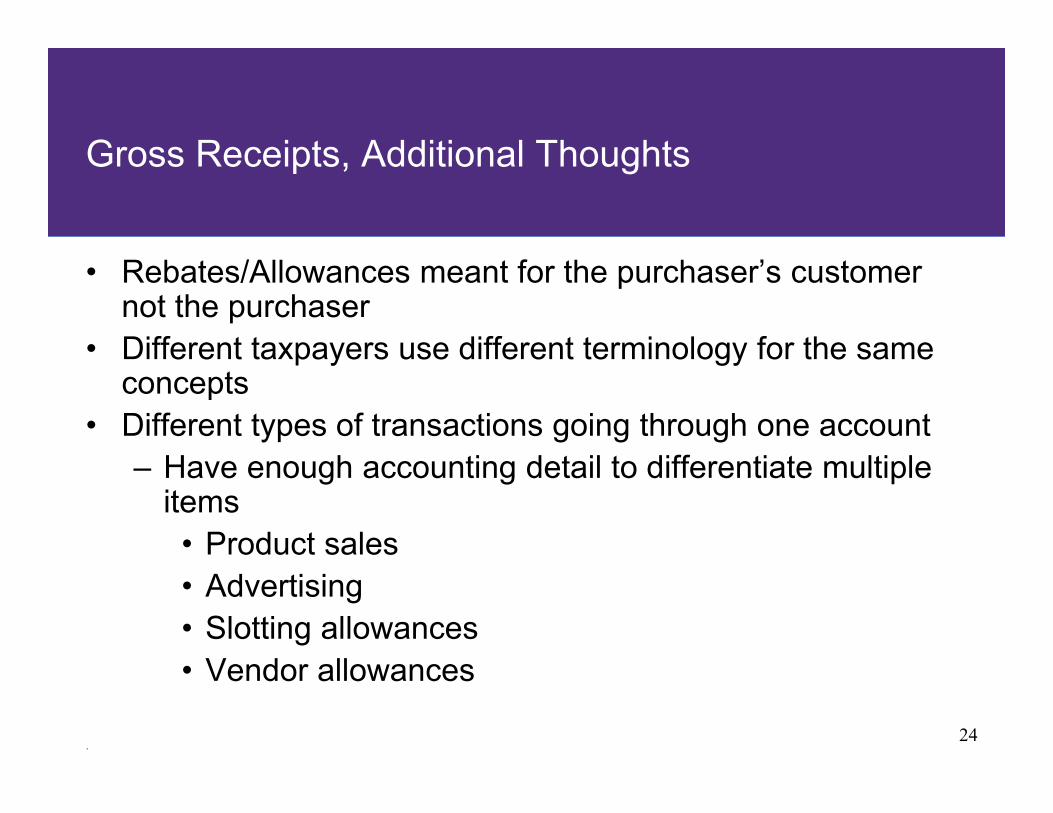

Gross Receipts, Additional Thoughts

• Rebates/Allowances meant for the purchaser’s customer not the purchaser

• Different taxpayers use different terminology for the same concepts

• Different types of transactions going through one account– Have enough accounting detail to differentiate multiple

items• Product sales• Advertising• Slotting allowances• Vendor allowances

© Grant Thornton LLP. All rights reserved.

5. Agency Exclusion

.26

• Statutory Exclusion. R.C. 5751.01(F)(2)(l) excludes from the definition of“gross receipts” all “[p]roperty, money, and other amounts received oracquired by an agent on behalf of another in excess of the agent’scommission, fee, or other remuneration.” (emphasis added).

• Definition of Agent. "Agent" means a person authorized by another person toact on its behalf to undertake a transaction for the other, including any of thefollowing…A person retaining only a commission from a transaction with theother proceeds from the transaction being remitted to another person.” R.C.5751.01(P).

Agency Exclusion

.27

• Regulation. O.A.C. 5703-29-13 provides additional guidance on thedefinition of an “agent” for purposes of the exclusion.

• Common law definition.

• Party claiming agency relationship exists bears burden of proof.

• Strict construal against exemption.

• “. . . the agency relationship should be explicitly stated in a contract thatis available to the tax commissioner to inspect. Absent such proof, it willbe presumed that no agency relationship exists . . . .” (emphasis added).

• Look beyond contractual language to actual facts and circumstances.

Agency Exclusion

.28

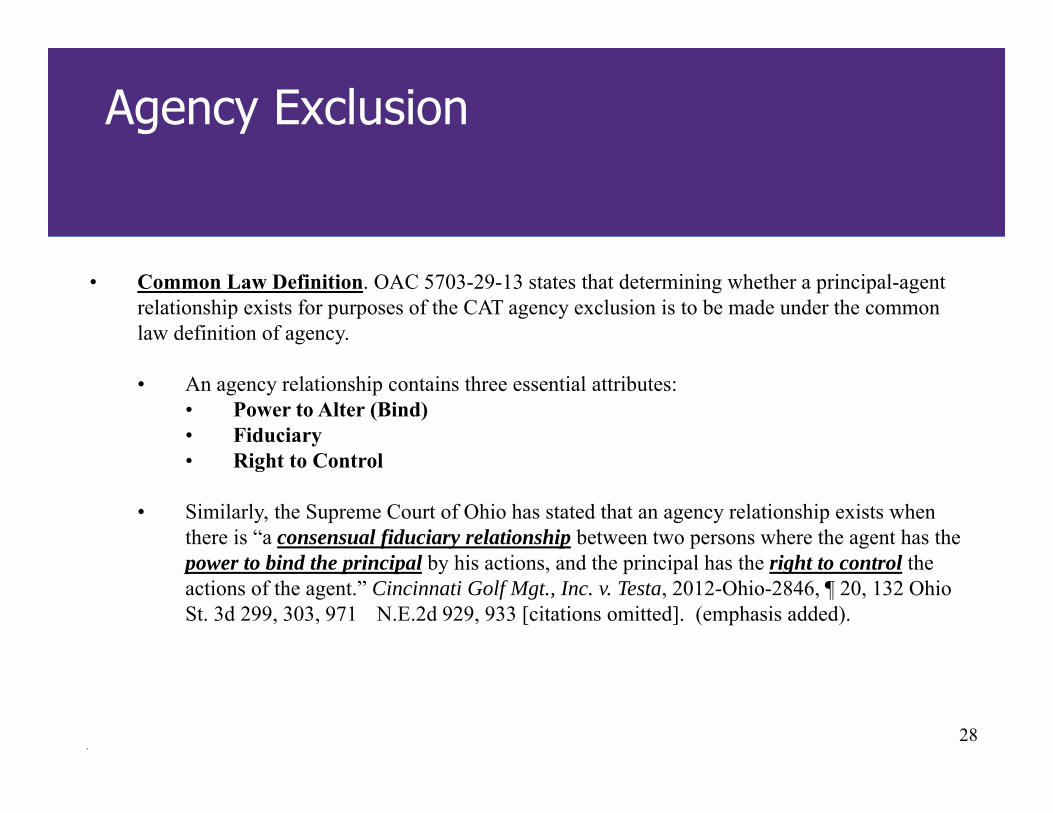

• Common Law Definition. OAC 5703-29-13 states that determining whether a principal-agent relationship exists for purposes of the CAT agency exclusion is to be made under the common law definition of agency.

• An agency relationship contains three essential attributes:• Power to Alter (Bind)• Fiduciary• Right to Control

• Similarly, the Supreme Court of Ohio has stated that an agency relationship exists when there is “a consensual fiduciary relationship between two persons where the agent has the power to bind the principal by his actions, and the principal has the right to control the actions of the agent.” Cincinnati Golf Mgt., Inc. v. Testa, 2012-Ohio-2846, ¶ 20, 132 Ohio St. 3d 299, 303, 971 N.E.2d 929, 933 [citations omitted]. (emphasis added).

Agency Exclusion

.29

• Written and Oral Contracts?

• Statutory Language – Written Contract Required?

• Regulation provides that the agency relationship should be explicitly stated in a contract.(OAC 5703-29-13(C)(2)(a)).

• Regulation provides that “The commissioner will look beyond the wording of the contractto the actual facts and circumstances of the situation to determine whether an agencyrelationship actually exists” (citing to H.R. Options, Inc. v. Zaino (2004), 100 Ohio St.3d37).

• Regulation defers to Ohio common law in determine whether an agency relationship exists.

• The Ohio Board of Tax Appeals has ruled in analogous context that even where acontract is required (pursuant to statute), written contracts are not necessary and oralcontracts are permitted. See e.g., Excel Temporaries, Inc. v. Tracy, (10/30/1998), OhioBTA 97-T-257; Advantage Services v. Tracy, (10/30/1998), Ohio BTA 95-T-1391.

Agency Exclusion

.30

• Willoughby Hills Development and Distribution Inc. v. Testa, BTA 2015-1069 (Jul. 5, 2016)• Refund claim by gasoline distributor claiming agency exclusion.• BTA ruled in favor of commissioner and against taxpayer.• Written contract “generically required” taxpayer to act in the purported

principal’s best interest in some respects.• BTA concluded this provided insufficient evidence that the purported principal

exercised control over the taxpayer as its agent.• Written contract included standard independent contractor / disclaimer of agency

language.• BTA noted that “it would seem appropriate, if not imperative, that a witness from

not only the agent's perspective, but also the principal's, be offered to support anegation of the contract language.”

Agency Exclusion

.31

• Corporate Services Group Holdings v. Testa, BTA 2016-875• Notice of appeal filed July 6, 2016.• Unless case management schedule amended, scheduled for discovery to

close December 5 and for hearing February 28.

Agency Exclusion

.32

• Final Thoughts on Agency• Should Apply to Buyer’s Agent and Seller’s Agent• Best Practice: Obviously, establish agency relationship at outset of

arrangement in written contract.• What if no written contract exists or not expressly addressed in written

contract?• Consider impact of securing exclusion upon legal relationship between

parties - do the parties want to have a principal/agent relationship?• Address for future periods

Agency Exclusion

© Grant Thornton LLP. All rights reserved.

6. Situsing

.34

• Definition of TPP R.C. 5751.01(J) (Same as sales tax RC 5739.01)• Gross Receipts are sitused to Ohio if the purchaser ultimately

receives the tangible personal property in Ohio– Ultimately Received - completion of the transportation to the purchaser

of the product whether by common carrier or by other means – Dock sale / customer pick-up– Terms of sale and title passage do not impact the situs– Need to determine “when the sale occurs”

• Consider - Risk of loss, billing for product, payment by customer, etc.

• Ohio purchaser ships the product back outside Ohio – taxable to seller unless out of state destination is known "at the time of

sale" and supported by the taxpayer’s books and records at the time of the sale (information release 2005-17)

Situsing of Gross Receipts Sale of TPP (ORC 5751.033(E))

.35

• Gross receipts from services are sitused to Ohio in the proportion that the purchaser’s benefit in Ohio with respect to what was purchased bears to the purchaser’s benefit everywhere with respect to what was purchased.

• The 3 critical questions for situsing services:– Who is the purchaser?– What is the purchaser's benefit?– Where is the benefit received?

Situsing Gross Receipts Services (ORC 5751.033(I))

.36

Situsing Gross Receipts – ServicesReasonable, Consistent & Uniform Safe Harbor Method

• Can request RCU method under O.R.C. 5751.033(H)• Provides a safe-harbor from penalties if ODT disagrees

with apportionment method.• Only applies to certain services• May use a different method for different services.• Must use the same method for similar services.• The taxpayer must:

– Use a RCU apportionment method to situs its services;– Method must be supported by the provider’s business records; and– Primary focus of the method must be on the location where the

purchaser ultimately uses or receives the benefit of the service.

.37

• Trademarks, trade names, patents, and copyrights, and similar IP sourced to state based on extent of use or right to use (depending on terms)

• Commercial domicile of payer versus location of use • Ability to document actual use versus use of population

(census data)– US versus world population

Situsing Gross Receipts from Intellectual Property

.38

Audit IssuesGross Receipts

• What is a gross receipt?– The total amount realized by a person that contributes to the

production of “gross income” of the person.

– Gross income is not a defined term in Chapter 5751 (the CAT law).• R.C. 5751.01(K) provides that if a term is not defined in Ohio’s code,

then may look to an IRC definition if the term is used in a like manner.

– To what extent does Internal Revenue Code apply?• If its not “gross income” on your federal tax return, is it a gross receipt?

– yes it can be• Gross vs. net reporting – Can you follow GAAP Financial statement

reporting requirements?– yes if tax accounting follows GAAP

.39

Audit IssuesGross Receipts

• Sale of inventory in an "asset sale“• Sale of Accounts Receivable• Managed property payroll cost reimbursement• Construction allowance taxable as TGR to retailer• Shelving allowance / product placement receipts are

considered TGR• Reward point program receipts are TGR• Trade-in received when selling product not allowed

as reduction in TGR• Pass-through freight

.40

Audit IssuesGross Receipts and/or situsing

• Contract Manufacturing• Tooling reimbursements from customers (contract

manufacturing)• Processing/service applied to TPP not owned• Management Intercompany Charges • Rebates/Allowances meant for the purchaser’s customer

not the purchaser• “Reimbursed” expenses – netting of expense accts

.41

Audit IssuesSitusing

• Ultimate Destination• Employment services / location of job site not sales

office• Professional services including accounting and

legal fees• Cloud computing / SAAS g

.42

Questions…