Embed Size (px)

Citation preview

Basic Accounting Concepts

AA Roundup

May 30, 2007

What is Accounting? Accounting is a process by which financial activities

are organized, recorded, analyzed and transformed into information in a consistent manner.

Financial activities (Transactions)

Accounting Processes,Internal Controls & Procedures

Financial Reports

Uses & Purpose of Accounting

Uses at Home Review accuracy of bank

statements Verify your credit card bills Make household expenses, pay

bills

Uses at Work Track hours worked Order supplies Pay items ordered Take student payments

It is used by everyone at home and at work

The purpose of Accounting is to provide information to help you analyze the financial situation of the company or household

Accounting Equation

Assets = Liabilities + Fund Balance (General Ledger)

(Revenue – Expenses) (Operating Ledger)

Double-Entry System

Assets = Liabilities + Fund Balance(Revenues – Expenses)

Received Food Services Revenue for $100.00

+ 100.00(Cash)

+ 100.00(Food Service Revenue)

Received Cash for Student Tuition for $500

+ 500.00(Cash)

-500.00(Accts Receivable)

Paid for expenses owed to vendors

-300.00(Cash)

-300.00(Accts Payable)

Every transaction must be two sided to keep the accounting equation in balance

Assets, Liabilities & Fund Balance

Assets – anything that is owned by the company and has money value

Liabilities – everything the company owes to others

Fund Balance (Equity) – represents how much really belongs to the company and is not owed to someone else.

LedgersAssets = Liabilities + Fund Balance (General Ledger)

(Revenue – Expenses) (Operating Ledger)

General Ledger keeps track of all the company’s assets, liabilities and fund balance accounts.

Operating Ledger keeps track of the company’s revenue and expense accounts.- At STC, most department organizations reflect expense accounts. Revenues are recorded in separate organizations.

Debits & Credits System Used to keep the accounting equation in

balance; every transaction has an equal debit and credit entry.

A debit and a credit act as an addition or subtraction depending on the type of account.

Debits – used to increase the value of an assets, to increase an expense, to reduce revenue or a liability account

Credits – used to increase a liability or revenue, to decrease an expense and an asset account

Debits & Credits RulesAssets Liabilities & Fund Balance

Debits Credits Debits Credits

Increases(+)

Decreases(-)

Decreases(-)

Increases(+)

Expenses Revenues

Debits Credits Debits Credits

Increases(+)

Decreases(-)

Decreases(-)

Increases(+)

Increases = normal balance of account group

T-Accounts

Used in traditional manual accounting to analyze the two sided (debit & credit) posting of transactions

Account

Debit Credit

Normal Balance – Activity # 1Account Asset Liability Expense Revenue

Cash

Tuition Revenue

Food Service Revenue

Accounts Payable

Fees Revenue

Loans Receivable

Salaries Paid

Food Purchases

Accounts Receivable

Supplies Expense

Normal Balance – Activity # 1Account Asset Liability Expense Revenue

Cash D

Tuition Revenue C

Food Service Revenue C

Accounts Payable C

Fees Revenue C

Loans Receivable D

Salaries Paid D

Food Purchases D

Accounts Receivable D

Supplies Expense D

Cash vs. Accrual Basis Accounting

Cash Accounting – transactions are recorded only when cash is involved. Example: a purchase is recorded when the items are paid.

Supplies Expense Cash

xxx xxx

Accrual Accounting – transactions are recorded as they happen, even if no cash is involved. Example: a purchase is recorded when the items are

ordered.When Order When Paid

Supplies Expense Accounts Payable Accounts Payable Cash

xxx xxx xxx xxx

Financial Statements Financial Statements are the main result of

Accounting. The most common statements include:Balance Sheet – reports ending balance of

assets, liabilities and fund balance accounts at a point of time (example: as of 8/31/07).

Income Statement – reports cumulative revenue and expense transactions for a period of time (example: Sept – Aug)

Cash Flow – reports uses and sources of cash

Calendar vs. Fiscal YearCalendar Year runs: Fiscal Year runs:

January 1st – December 31st September 1st – August 31st

Calendar Year Calendar Month Fiscal Year Fiscal Period

2005 09 2006 01

2005 10 2006 02

2005 11 2006 03

2005 12 2006 04

2006 01 2006 05

2006 02 2006 06

2006 03 2006 07

2006 04 2006 08

2006 05 2006 09

2006 06 2006 10

2006 07 2006 11

2006 08 2006 12

2006 09 2007 01

2006 10 2007 02

2006 11 2007 03

2006 12 2007 04

Posting Transactions ActivityStudent Receivable Tuition & Fee Rev

$600 $600

In-State Travel Exp Accounts Payable

$300 $300

Student Receivable Cash

$35 $35

Subscription Exp Accounts Payable

$100 $100

Accounts Payable Cash

$100 $100

Cash Subscription Exp

$15 $15

1) Student Registers for classes ($600)

2) Student pays registration fee ($35)

3) Order magazine subscription ($100)

4) Pay invoice for magazine subscription ($100)

5) Received refund for magazine subscription ($15)

6) Book in state travel ($300)

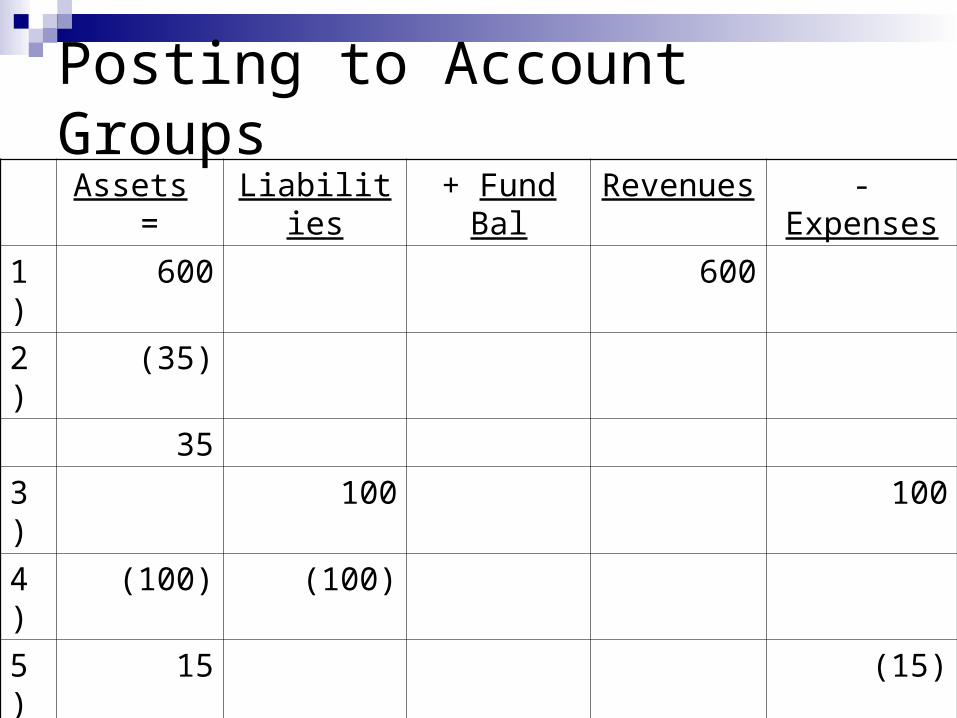

Posting to Account GroupsAssets = Liabilities + Fund Bal Revenues - Expenses

1) 600 600

2) (35)

35

3) 100 100

4) (100) (100)

5) 15 (15)

6) 300 300

515515 300300 215215 600600 385385

Closing the Periods When periods are closed, the net of revenues

and expenditures is added (or decreased) to the fund balance account.

Revenue – Expenses Income Statement $600 - $385 = $215

Fund BalanceBeginning Balance as of 9/1/06 $ 0Increase (Decrease) to Fund Balance $ 215Ending Balance as of 8/31/07 $ 215

Assets = Liabilities + Fund Balance Balance Sheet$ 515 = $300 + $215

Balance SheetASSETS

Cash (50)

Student Receivable 565

TOTAL ASSETS $515

LIABILITIES

Accounts Payable 300

TOTAL LIABILITIES $300

FUND BALANCE $215

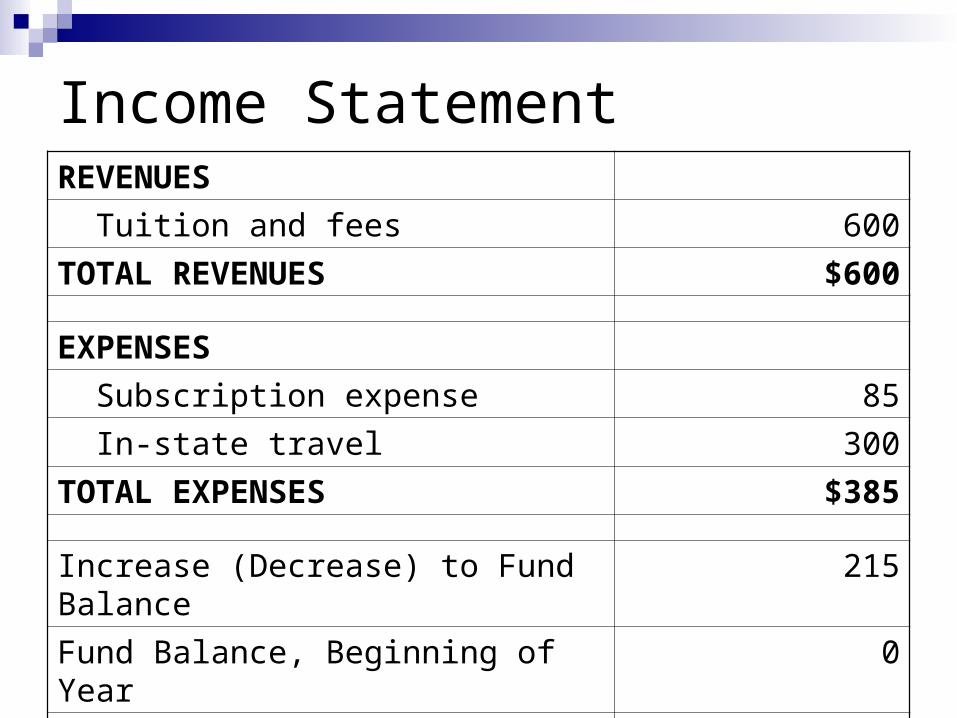

Income StatementREVENUES

Tuition and fees 600

TOTAL REVENUES $600

EXPENSES

Subscription expense 85

In-state travel 300

TOTAL EXPENSES $385

Increase (Decrease) to Fund Balance 215

Fund Balance, Beginning of Year 0

Fund Balance, End of Year $215

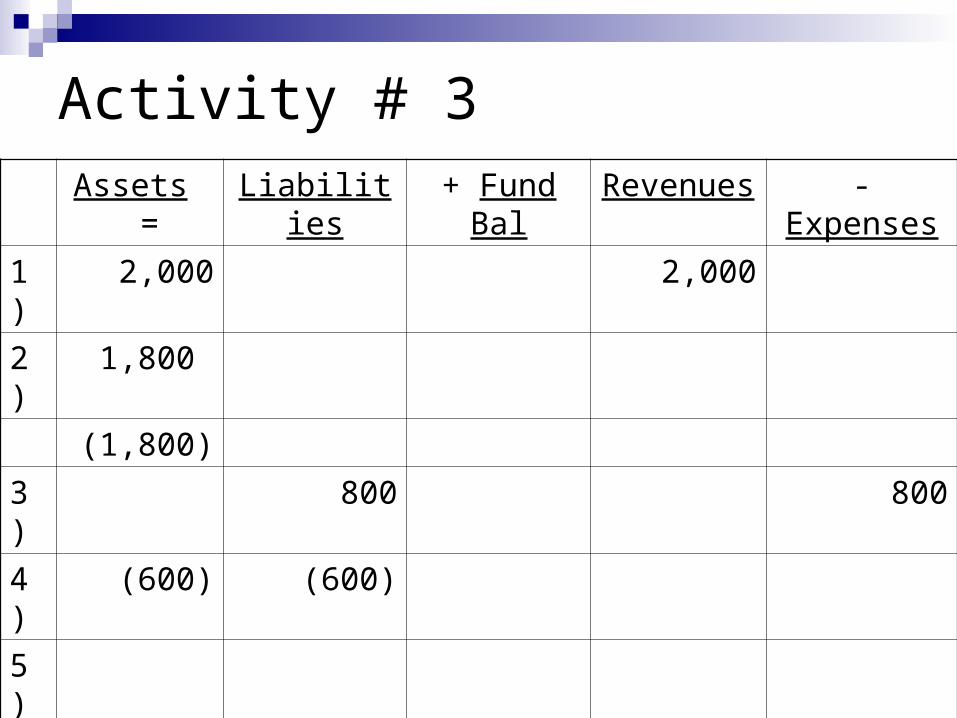

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2)

3)

4)

5)

6)

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2) 1,800

(1,800)

3)

4)

5)

6)

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2) 1,800

(1,800)

3) 800 800

4)

5)

6)

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2) 1,800

(1,800)

3) 800 800

4) (600) (600)

5)

6)

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2) 1,800

(1,800)

3) 800 800

4) (600) (600)

5) 400 400

6)

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2) 1,800

(1,800)

3) 800 800

4) (600) (600)

5) 400 400

6) 150 (150)

Activity # 3Assets = Liabilities + Fund Bal Revenues - Expenses

1) 2,000 2,000

2) 1,800

(1,800)

3) 800 800

4) (600) (600)

5) 400 400

6) 150 (150)

1,5501,550 200200 1,3501,350 2,4002,400 1,0501,050

Questions?Questions?

![AUDITORS AND ACCOUNTING STANDARDS MODULE · AA-3.3 [This Section was deleted in October 2012] 10/2012 AA-4 Accounting Standards AA-4.1 General Requirements 10/2010 AA-5 Role of External](https://img.dokumen.tips/doc/110x75/5fc53cc1a40c0333b063c079/auditors-and-accounting-standards-module-aa-33-this-section-was-deleted-in-october.jpg)