Embed Size (px)

Citation preview

BANKING TODAY- REDEFINED ANDRE-ENGINEERED

INDIAN BANKING - THE CHANGING LANDSCAPE

AGENDA FOR THE SESSION

o To Sensitize the Participants to the

Latest Changes in Banking Industry

o What is the Response to the Current

Trends from Bankers and Customers?

INDUSTRY PROFILE

Public Sector banks

Private Indian Banks New Generation

Banks

Private Foreign Banks –

Cooperative Banks

Non Banking Financial Institutions

Banking Sector Reforms – Post-Liberalization … 1st Narasimham Committee Report on

Financial Sector Reform – 1991 Introduction of Capital Adequacy Norms and

Prudential Norms - 1992 Deregulation of Interest Rates, Prudential

Norms for Maximum NPA – 1993 Introduction of Banking Ombudsman Scheme

– 1994

Banking Sector Reforms – Post-LiberalizationConcept of Local Area Banks

Introduced – 19951st Shared Payment Network System &

conditional autonomy to PSU’s – 19962nd Narasimham Committee Report of

Banking Sector Reforms – 1997Guidelines on Risk Management – 1998

RECENT TRENDS IN BANKS Entry of New Generation Banks Change in the Process, Methods &

Techniques New Products and Services Collaboration between Banking &

Insurance Companies. Improvement in Service Quality Increasing focus on Retail Banking Shift Towards Branchless Banking

RECENT TRENDS IN BANKS Change in Customer Expectations Outsourcing of Resources [Human&Non-

human] Steady Reduction in Interest Rates Increasing Non- Interest and Fee Based

Income Corporate governance and Business

Transformation Mergers, Acquisitions and Consolidations

CHANGING PERCEPTION OF CUSTOMER

Servicing the Customer – 1950’s to 1960’s Satisfying the Customer - 1960’s to 1980’s Pleasing the Customer - 1980’s to 1990’s Delighting the Customer -1990’-2000 Retaining the Customer – 2000 and beyond

WHAT CHANGES ? Electronic Fund Transfer (EFT) Electronic Clearing System (ECS) Automated Teller Machines (ATM) Shared Payment Network System (SPNS) Credit Cards/ Debit Cards Point of Sale Terminal Tele-banking Mobile Banking Net Banking Electronic Data Interchange Corporate Banking Terminals

WHERE ARE WE GOING? Anywhere Anytime Anyplace Banking Timeless and Placeless Banking Banking at Convenience Good by to Traditional Instruments

(Cheques &DD) & Invitation to new Instruments

Disappearance of Conventional Risk and Arrival of New Risks

Leading to currency-less monetary system Dismantling of Physical Structure

WHAT IS THE TRIGGER? Hyper Competition Shrinking Margins Need to Reduce Cost Take Advantage of Technology Changing Customer Expectations Simplify the Procedure and Process Reduce Traditional Risk Offer Better / Improved Service Some Constraints

[Policy/Resources/Physical/Structure]

Author for Change – Players in the Banking Business Eco-System

Shareholders Management Depositors Borrowers Employees Government Regulatory Authorities – RBI Competitors

PHASE OF TECH BANKING

PSB

PIB

PFB

CB

NBFI

SBI, SBT ETC.

ICICI,IDBI,HDFC,UTI BANK ETC..

CITI BANK,SC BANK, ETC..

SCB,UCB,DCBs/SCBs

INDUSTRY

SOME EARLY ADOPTERS

BANK____________CHANNEL

HSBC

BankHDFCBank

UTI Ban

k

CITI BANK ICICI Bank

ATM (No.) 250 500 550 174 1000

ATM Share(%)

40 50 NA 80 45

Other Channel[%] (mobile, phone, net)

35 15 NA 15 15

Branch Banking[%]

25 35 NA 5 40

STRATEGIES OF BANKS

Citibank: Parallel Banking

HSBC : Leveraging branches to grow C’

ICICI B : Reducing importance of branch

HDFC B: Conservative migration

UTI B : ATM’s as a force multiplier

Issues and Challenges

What will happen to the traditional rural credit institutions like, Cooperative Banks, RRB’s and Low performing Public Sector Banks?

What are all the options for the Public Sector Banks?

Issues and Challenges

Can the machines establish a strong connecting link with customers?

Is the Convenience Banking good for all segment and all seasons?

Is it not challenges the conventional wisdoms (keeping close contact with the customers)?

Issues and Challenges

Does IT confer Competitive advantage or is it just the cost of staying in business?

How do we dispose the existing human resource?

What are the new security issues? Is this changes a customer demanded/bank

wanted? Are the customers happy and comfortable with the shift?

THANK YOU

Electronic Fund TransferTransfer of funds between

banks located in different cities in place of DD/MT/Telegraphic transfer.

Electronic Clearing System

Facilitates inter-bank settlements - both Debit & Credit clearances through INFINET.

CC: Companies who have to make bulk payments to a large number of beneficiaries prepare the credit instructions on the magnetic media and submit the same to RBI for payment.

DC: Payment to utility companies by banks on behalf of the customers.

Tele-bankingUsing automatic voice recorder

it facilitates both cash & non-cash transactions for the bank and customers.

Automated Teller Machines

Device used for withdrawal of money, depositing of money and balance enquiry and verification for 24 hours of a day.

Shared Payment Network System

Facilitates Use of ATM cards across participating banks at ATM centers using Master/Visa Cards. In case of using other banks ATM – one may have to pay service charges.

Credit Cards/ Debit CardsCREDIT CARD: It is a card that

empowers the Customer to spend up to the fixed value of money limit fixed - A prepaid card.

DEBIT CARD: It is a post paid card and money is transferred after the spending.

Corporate Banking TerminalsFacilitates the Corporate

customers to log on into the banks data base and have access to their account for balance verification etc. with defined powers.

Point of Sale TerminalComputer terminal that is

linked online to computerised customer information files that facilitates purchase from retail shops as it credits the retailer account online.

Electronic Data Interchange

Transmit financial information and payments in electronic form.- reduces transmitting cost and risk.

JAMMU

CHANDIGARH

DELHI

JAIPUR

AHMEDABAD

MUMBAI

PUNE

BANGALORE

THIRUVANANTHAPURAM

CHENNAI

HYDERABAD

BHUBANESHWAR

CALCUTTA

PATNAKANPUR

GUWAHATI

BHOPAL

Back up NMS at Mumbai

NMS at Hyderabad

Integration of VSAT network with Terrestrial network

DESIGN OF TERRESTRIAL NETWORK AND INTEGRATION WITH VSAT NETWORK

2 mbps leased line

64/128 kbps leased line

VSAT Network

NAGPUR

KOCHI

GOA

LUCKNOW

INFINET - INDIAN FINANCIAL NETWORK (LEASED LINE CONNECTIVITY AND INTEGRATION WITH IDRBT VSAT

NETWORK)

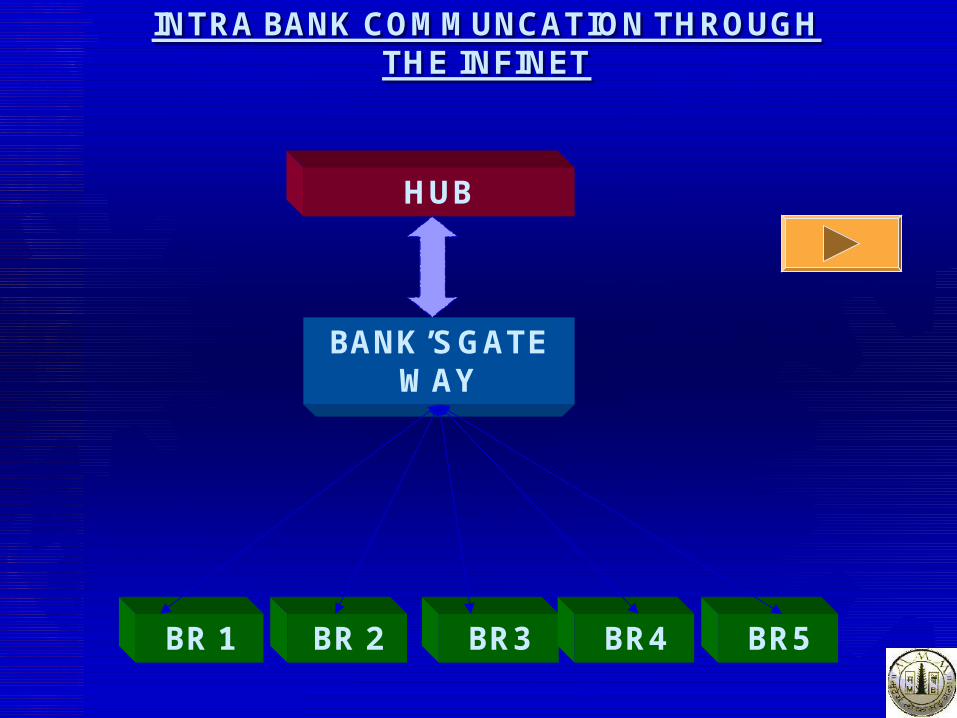

INTRA BANK COMMUNCATION THROUGH THE INFINET

INTRA BANK COMMUNCATION THROUGH THE INFINET

BR 1 BR 2 BR3 BR4 BR5

BANK’S GATE WAY

HUB

BR 1 BR 2 BR 3

HUB

INTER BANK COMMUNCATION THROUGH THE INFINET

BR 1 BR 2 BR 3

BANK 1 GATE WAY

BANK 2 GATE WAY

ArchitectureArchitecture

INFINET IP Network (IIPN)

Gateway 1

Bank SiteBank Site Bank Site

Gateway 2

Bank SiteBank Site Bank Site

Gateway N

Bank SiteBank Site Bank Site

….

Central HUB•Safe storage

•Direct Routing to intra-bank sites•Routing to ‘others’ Bank sites via Central HUB

•Safe storage of inter-bank messages•Direct Routing to destination Bank Gateway•Access Validation

•Common IIPN access point•Safe storage

Corporate Institution

Corporate Institution’s Bank

Clearing House

Destination Bank

ECS - How it works

Destination Bank Destination Bank

Branches of destination banks

Investors

11

How ECS Works - Process flow

User InstitutionBeneficiaries’

A/Cs

Destination banks’service branches

Destination branches

Clearing House

Sponsor Bank

Data on Day-1 Reports on Day-2

Reports on Day-3

Credit on Day-4

Enc

rypt

ed

Dat

a on

Day

-1

ECS - Processing of Uncredited Payment Instructions contd...

User Institution

Destination banks’service branches

Destination branches

Clearing HouseSponsor Bank

Encrypted Output Data on Post Settlement

Day-2

Return Data submitted on Post Settlement

Day-1

Return Advice on Post Settlement Day-1

Enc

rypt

ed O

utpu

t D

ata

on

Pos

t Set

tlem

ent

Day

-2

How to Participate in ECS - Registration Procedure

Corporate Institution

Sponsor Bank

Clearing House

Agreement

Collect a copy of the ECS brochure and ECS

Procedural Guidelines

Identify your Sponsor Bank ( a member of the Clearing House)

Submit an Application -Form annexed to the ECS brochure/Guidelines

Obtain the Unique User Registration number from Sponsor Bank

Good Bye Paper Warrants

and...

32

Switch over to

ECS- The best way to Pay

![Workplace Redefined[1]](https://img.dokumen.tips/doc/110x75/541c69077bef0a16088b4852/workplace-redefined1.jpg)