Embed Size (px)

Citation preview

BANK OF SYRIA AND OVERSEAS S.A.

FINANCIAL STATEMENTS AND AUDITOR’S REPORT YEAR ENDED DECEMBER 31, 2007

BANK OF SYRIA AND OVERSEAS S.A. FINANCIAL STATEMENTS AND AUDITOR’S REPORT

YEAR ENDED DECEMBER 31, 2007

TABLE OF CONTENTS Page Independent Auditor’s report 1 Financial Statements: Balance Sheet 2 Income Statement 3 Statement of Changes in Equity 4 Cash Flow Statement 5 Notes to the Financial Statements 6-52

3

BANK OF SYRIA AND OVERSEAS S.A. BALANCE SHEET

As of December 31, ASSETS Notes 2007 2006 SYP SYP Cash, compulsory reserve and Central Bank of Syria 5 13,799,527,332 13,877,830,602 Deposits with banks 6 33,663,478,096 27,681,660,253 Securities: Available for sale 7 50,000,000 50,000,000 Held to maturity 8 477,756,201 - Loans and advances 9 13,372,461,640 6,425,530,625 Customers' liability under acceptances 10 1,058,243,611 612,624,323 Other assets 11 29,563,329 10,409,919 Property and equipment 12 771,111,096 698,950,072 Intangible assets 13 86,366,980 91,819,493 Regulatory blocked fund 14 283,781,300 294,269,840 Total assets 63,592,289,585 49,743,095,127 LIABILITIES Deposits from banks and other financial institutions 15 1,200,415,277 569,633,414 Customers' and related parties' deposits and other credit balances 16 56,027,308,326 43,956,701,882 Cash margins 17 1,231,162,301 729,990,151 Liability under acceptances 10 1,058,243,611 612,624,323 Other liabilities 18 671,071,711 553,554,544 Total liabilities 60,188,201,226 46,422,504,314 EQUITY Capital 19 3,000,000,000 3,000,000,000 Legal reserve 20 73,985,118 39,873,270 Special reserve 20 73,985,118 39,873,270 Currency adjustments on structural position 21 ( 165,156,352) ( 57,535,419) Retained earnings 421,274,475 298,379,692 Total equity 3,404,088,359 3,320,590,813

Total liabilities and equity 63,592,289,585 49,743,095,127 FINANCIAL INSTRUMENTS WITH OFF-BALANCE SHEET RISKS: 27 Guarantees and stand by letters of credit 6,575,868,963 6,964,959,850 Documentary and commercial letters of credit 2,076,853,713 1,765,987,985

SEE ACCOMPANYING NOTES TO THE FINANCIAL STATEMENTS

4

BANK OF SYRIA AND OVERSEAS S.A. INCOME STATEMENT

For the year ended December 31, Notes 2007 2006 SYP SYP Interest income 22 2,774,023,914 1,547,972,467 Interest expense 23 ( 2,160,063,752) ( 1,126,497,017) Net interest income 613,960,162 421,475,450 Fee and commission income 24 349,627,232 240,750,921 Fee and commission expense ( 8,863,074) ( 10,141,790) Net fee and commission income 340,764,158 230,609,131 Net realized exchange losses ( 43,452,977) ( 10,069,411) Provision for fluctuations in exchange rates 18 - ( 2,483,000) Net unrealized exchange losses on structural position ( 107,620,933) ( 133,088,681) Net financial revenues 803,650,410 506,443,489 Allowance for impairment of loans and advances 9 ( 19,017,758) ( 9,989,188) Net financial revenues after allowance for impairment of loans and advances 784,632,652 496,454,301 Salaries and related charges 25 ( 216,952,273) ( 151,852,983) General operating expenses 26 ( 100,929,242) ( 85,095,034) Depreciation and amortization 12 & 13 ( 103,441,980) ( 66,361,969) Net miscellaneous expenses ( 311,611) ( 440,270) Total other expenses ( 421,635,106) ( 303,750,256) Profit inclusive of unrealized losses on structural position and before income tax 28 362,997,546 192,704,045 Income tax 18 ( 129,500,000) ( 88,885,000) Net profit for the year 28 233,497,546 103,819,045 Earnings per share: Basic 29 38.92 17.30 Diluted 29 38.92 17.30

SEE ACCOMPANYING NOTES TO THE FINANCIAL STATEMENTS

5

BANK OF SYRIA AND OVERSEAS S.A. STATEMENT OF CHANGES IN EQUITY

Currency adjustments Profit Legal Special on structural Retained for the Capital reserve reserve position earnings year Total SYP SYP SYP SYP SYP SYP SYP Balance as at December 31, 2005 3,000,000,000 16,182,497 16,182,497 75,553,262 108,853,512 - 3,216,771,768 Profit for 2006 - - - - - 103,819,045 103,819,045 Allocation of 2006 profit (Note 28) - 23,690,773 23,690,773 (133,088,681) 189,526,180 ( 103,819,045) -

Balance as at December 31, 2006 3,000,000,000 39,873,270 39,873,270 ( 57,535,419) 298,379,692 - 3,320,590,813 Dividend distribution - - - - (150,000,000) - ( 150,000,000) Profit for 2007 - - - - - 233,497,546 233,497,546 Allocation of 2007 profit (Note 28) - 34,111,848 34,111,848 (107,620,933) 272,894,783 (233,497,546) -

Balance as at December 31, 2007 3,000,000,000 73,985,118 73,985,118 (165,156,352) 421,274,475 - 3,404,088,359

SEE ACCOMPANYING NOTES TO THE FINANCIAL STATEMENTS

6

BANK OF SYRIA AND OVERSEAS S.A.

CASH FLOW STATEMENT For the year ended December 31, Notes 2007 2006 SYP SYP Cash flows from operating activities: Profit for the year before income tax 362,997,546 192,704,045 Adjustments for: Depreciation and amortization 103,441,979 66,361,969 Allowance for impairment of loans and advances 9 19,017,758 9,989,188 Currency adjustments on regulatory blocked funds 14 10,488,540 13,285,490 Amortization of discounts on securities 7&8 ( 44,590) - Provision for fluctuations in exchange rates - 2,483,000 Loss on disposal of fixed assets 47,139 - Net increase in loans and advances 9 ( 6,965,948,773) ( 1,796,680,184) Net (increase)/ decrease in other assets ( 19,153,410) 2,499,807 Increase in term deposits with banks ( 2,269,601,447) ( 1,671,624,055) Net (decrease)/ increase in deposits from banks ( 125,000,000) 125,000,000 Net increase in customers and, related parties deposits and other credit balances 16 11,989,256,306 22,668,356,677 Net increase in accrued interest receivable ( 190,065,511) ( 147,923,355) Net increase in accrued interest payable 78,617,520 133,289,879 Tax paid 18 ( 88,885,000) ( 50,227,000) Net increase in cash margins 17 498,797,127 288,850,996 Net increase in other liabilities 56,481,892 208,236,772 Net cash generated by operating activities 3,460,447,076 20,044,603,229 Cash flows from investing activities: Purchase of property and equipment 12 ( 168,497,160) ( 279,508,160) Purchase of intangible assets 13 ( 1,700,470) ( 34,783,750) Purchase of available for sale securities 7 - ( 50,000,000) Purchase of held to maturity securities 8 ( 474,013,250) - Net cash used in investing activities ( 644,210,880) ( 364,291,910) Cash flows from financing activities: Dividend distribution 34 ( 129,579,725) - Net cash used in financing activities ( 129,579,725) - Net increase in cash and cash equivalents 2,686,656,471 19,680,311,319 Cash and cash equivalents - Beginning of year 38,538,871,452 18,858,560,133 Cash and cash equivalents - End of year 31 41,225,527,923 38,538,871,452

SEE ACCOMPANYING NOTES TO THE FINANCIAL STATEMENTS

7

BANK OF SYRIA AND OVERSEAS S.A. NOTES TO THE FINANCIAL STATEMENTS

YEAR ENDED DECEMBER 31, 2007 1. BANK’S OBJECTIVES AND ACTIVITIES Bank of Syria and Overseas S.A. (The Bank) is a Syrian joint stock company, incorporated on November 19, 2003 and registered under No. 13900 on December 29, 2003 at the commercial register of Damascus district. The Bank is registered at the Governmental Commission under No.9 as a private bank, and conducts all banking services. The headquarter of the Bank is located in Harika, Bab Barid, Lawyers Syndicate Building, Damascus, Syria. As of December 31, 2007, the Bank had ten branches: two in Aleppo and one in each of Lattakia, Hama, Homs, Tartous and four in Damascus city. 2. ADOPTION OF NEW AND REVISED STANDARDS In the current year, the Bank has adopted IFRS 7 Financial Instruments: Disclosures which is effective for annual reporting periods beginning on or after 1 January 2007, and the consequential amendments to IAS 1 Presentation of Financial Statements. The impact of the adoption of IFRS 7 and the changes to IAS 1 has been to expand the disclosures provided in these financial statements regarding the Bank’s financial instruments and management of capital. Four Interpretations issued by the International Financial Reporting Interpretations Committee are effective for the current period. These are: IFRIC 7 Applying the Restatement Approach under IAS 29, Financial Reporting in Hyperinflationary Economies; IFRIC 8 Scope of IFRS 2; IFRIC 9 Reassessment of Embedded Derivatives; and IFRIC 10 Interim Financial Reporting and Impairment. The adoption of these Interpretations has not led to any changes in the Bank’s accounting policies. At the date of authorisation of these financial statements the following Standards and Interpretations were in issue but not yet effective: IAS 23 (Revised) Borrowing Costs (effective for accounting periods beginning on or after 1 January 2009); IFRS 8 Operating Segments (effective for accounting periods beginning on or after 1 January 2009); IFRIC 11 IFRS 2: Group and Treasury Share Transactions (effective for accounting periods beginning on or after1 March 2007); IFRIC 12 Service Concession Arrangements (effective for accounting periods beginning on or after 1 January 2008); IFRIC 13 Customer Loyalty Programmes (effective for accounting periods beginning on or after 1 July 2008); and

8

IFRIC 14 IAS 19: The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction (effective for accounting periods beginning on or after 1 January 2008). The Management anticipates that the adoption of all of the above Standards and Interpretations will have no material impact on the financial statements of the Bank in the period of initial application. 3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES A. Statement of Compliance The financial statements are prepared in accordance with International Financial Reporting Standards and the existing banking laws in Syria; assets and liabilities are grouped according to their nature and are presented in an approximate order that reflects their relative liquidity.

B. Basis of Preparation The financial statements have been prepared on the historical cost basis except for certain financial instruments that are stated at fair value. The financial statements are presented in Syrian Pounds (SYP), the functional and reporting currency.

C. Foreign Currencies

Transactions effected during the year in foreign currencies, including revenues and expenses, are translated to Syrian Pounds, the reporting currency, using rates of exchange prevailing at the transaction date. Monetary assets and liabilities denominated in foreign currencies are translated at the year end into Syrian Pounds at the exchange rates as published by the Central Bank of Syria (on December 31, 2007: SYP 48.05 for 1US Dollar and SYP 70.70 for 1 Euro). Translation gains and losses are included in the income statement. Cash flows in foreign currencies generated by and used in the various activities, as shown in the accompanying cash flow statement, are translated into Syrian Pounds at the exchange rates prevailing at the year end, except for cash and cash equivalents at the beginning of year which are translated at prior year closing exchange rates, and the effect of currency rate fluctuation, if any, is disclosed separately in the notes to the financial statements. The Council of Money and Credit issued decision number 249, that allowed banks operating in Syria to hold a structural position equivalent to 60% of their net equity. This decision stipulated that the currency adjustments on structural position be considered as unrealized profit / (loss), consequently theses gains / (losses) are not taxable and not available for distribution. Accordingly, these differences were transferred from the income statement to the statement of changes in equity as currency adjustments on structural position.

9

D. Financial Assets and Liabilities: Recognition and Derecognition: The Bank initially recognizes loans and advances, deposits, debt securities issued and subordinated liabilities on the date that they are originated. All other financial assets and liabilities are initially recognized on the trade date at which the Bank becomes a party to the contractual provisions of the instrument. The Bank derecognizes a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which all the risks and rewards of ownership of the financial asset are transferred. The Bank derecognizes a financial liability when its contractual obligations are discharged, cancelled or expire. Offsetting: Financial assets and liabilities are set off and the net amount is presented in the balance sheet when, and only when, the Bank has a legal right to set off the amounts or intends either to settle on a net basis or to realize the asset and settle the liability simultaneously. Fair Value Measurement: The determination of fair values of financial instruments traded in active markets is based on quoted market prices. For financial instruments where there is no quoted price, fair value is determined by using valuation techniques. Valuation techniques include net present value technique, the discounted cash flow method, and comparison to similar instruments for which market observable prices exist. Impairment of Financial Assets: Financial assets, other than those at fair value through profit or loss, are assessed for indicators of impairment at each balance sheet date. Financial assets are impaired where there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the asset, the estimated future cash flows of the investment have been impacted. Impairment losses on assets carried at amortized cost are measured as the difference between the carrying amount of the financial assets and the present value of estimated future cash flows discounted at the original effective interest rate. Losses are recognized in profit or loss and reduce the carrying amount of the asset to its estimated recoverable amount. If, in a subsequent period, the amount of the impairment loss decreases, the previously recognized impairment loss is reversed through profit or loss to the extent that the carrying amount of the investment at the date the impairment is reversed does not exceed what the amortized cost would have been had the impairment not been recognized. In respect of available-for-sale investment securities, the previously accumulated losses recorded under equity are recognized in profit or loss in case of impairment losses substantiated by a prolonged decline in fair value of the investment securities. Any increase in fair value subsequent to an impairment loss is not recognized in profit or loss for available-for-sale equity securities. Any increase in fair value subsequent to an impairment loss is recognized in profit or loss for available-for-sale debt securities.

10

E. Investment Securities: Investment securities are initially measured at fair value plus incremental direct transaction costs, and subsequently accounted for depending on their classification as either held-to-maturity or available-for-sale. Held-to-Maturity Investment Securities: Held-to-maturity investments are non-derivative assets with fixed or determinable payments and fixed maturity that the Bank has the positive intent and ability to hold to maturity, and which are not designated at fair value through profit or loss or available-for-sale. Held-to-maturity investments are carried at amortized cost using the straight line method where results approximate those resulting from the effective interest method. Available-for-Sale Investment Securities: Available-for-sale investments are non derivative investments that are not designated as another category of financial assets. Unquoted equity securities whose fair value cannot be reliably measured are carried at cost. All other available-for-sale investments are carried at fair value and unrealized gains or losses are included in equity, except for impairment losses which are included in the income statement, as applicable. The change in fair value on available-for-sale debt securities reclassified to held-to-maturity is segregated from the change in fair value of available-for-sale debt securities under equity and is amortized over the remaining term to maturity of the debt security as a yield adjustment. F. Loans and Advances Loans and advances are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and advances are disclosed at amortized cost net of unearned interest and after provision for credit losses where applicable. Bad and doubtful debts are carried on a cash basis because of doubts and the probability of non-collection of principal and/or interest. G. Financial Guarantees Financial guarantees contracts are contracts that require the Bank to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the terms of a debt instrument. These contracts can have various judicial forms (guarantees, letters of credit, credit-insurance contracts). Financial guarantee liabilities are initially measured at their fair value, and subsequently carried at the higher of this amortized amount and the present value of any expected payment (when a payment under the guarantee has become probable). Financial guarantee liabilities are included within other liabilities accounts.

11

H. Property and Equipment Property and equipment are stated at historical cost in Syrian Pounds, less accumulated depreciation and impairment losses, if any. Depreciation of property and equipment is charged on the straight-line method over the estimated useful life of the assets on the basis of the following annual rates: % Buildings 5 Furniture and office equipment 10-15 Computer equipment 20 Vehicles 20 Leasehold improvements 20 I. Intangible Assets - Key Money:

Key money is recorded at acquisition cost and is amortized on straight-line basis over a period of 20 years, or over the duration of rent contract, whichever is less.

- Software:

Software is recorded at acquisition cost and is amortized on straight-line basis over a period of 5 years.

J. Impairment of Tangible and Intangible Assets: At each balance sheet date, the Bank reviews the carrying amounts of its tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted. If the recoverable amount of an asset is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. An impairment loss is recognized immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease. Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the asset (cash-generating unit) in prior years. A reversal of an impairment loss is recognized immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

12

K. Social Security Contributions The Bank is registered in the Syrian Social Security Establishment and pays regular contributions for its employees to the Establishment. These contributions represent the Bank’s commitment towards its employees concerning end-of-service indemnities that will be allotted to them by the Social Security Establishment. The Bank has no other liability towards its employees’ end-of-service indemnity. L. Provisions: A provision is recognized if, as a result of a past event, the Bank has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability. M. Revenue and Expense Recognition: Interest income and expense are recognized on an accrual basis, taking into account the principal outstanding and the rate applicable, except for non-performing loans and advances for which interest income is only recognized upon realization. Interest income and expense include the amortization discount or premium. Fee and commission income and expense that are integral to the effective interest rate on a financial asset or liability (e.g. commissions and fees earned on loans) are included under interest income and expense. Other fee and commission income are recognized as the related services are performed. Dividend income is recognized when the right to receive payment is established. N. Income Tax The Bank computes its income tax in accordance with the provisions of law number 28 dated April 16, 2001 which sets the tax rate at 25% of the net taxable profit. Taxable profit differs from net profit as reported in the income statement because it excludes non-taxable income amounts and includes added-back non-deductible expense amounts.

13

4. CRITICAL ACCOUNTING JUDGMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY In the application of the Bank’s accounting policies, which are described in note 3, management is required to make judgements, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

A. Critical Accounting Judgments In Applying The Accounting Policies: Classification of Financial Assets: The Bank’s accounting policies provide scope for investment securities to be designated on inception into different categories in certain circumstances based on specific conditions. In classifying investment securities as held-to-maturity, the Bank has determined that it has both the positive intent and ability to hold these assets until their maturity. If the Bank fails to keep these investments until maturity, other than for specific circumstances, they will require reclassifying the entire category as available for sale that will be measured at fair value with the corresponding cumulative positive change in fair value booked in equity. B. Key Sources of Estimation Uncertainty: The following are the key assumptions concerning the future, and other key sources of estimation uncertainty at the balance sheet date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year. Allowances for Credit Losses: Specific impairment for credit losses is determined by assessing each case individually. This method applies to classified loans and advances, and the factors taken into consideration when estimating the allowance for credit losses include the counterparty’s credit limit, the counterparty’s ability to generate cash flows sufficient to settle the advances provided and the value of collateral and potential possession of assets satisfaction of debt. Impairment of Available-for-sale Equity Investment Securities: The Bank determines that available-for-sale equity investments are impaired when there has been a significant or prolonged decline in the fair value below its cost. This determination requires judgment. In making this judgment the Bank, among other factors, evaluates the normal volatility in share price.

14

5. CASH, COMPULSORY RESERVE, AND CENTRAL BANK OF SYRIA This caption includes the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Cash 700,287,713 417,385,639 1,117,673,352 Compulsory reserve 1,200,600,000 1,573,231,682 2,773,831,682 Central Bank of Syria 9,795,981,590 5,276,143 9,801,257,733 Clearing cheques 16,686,082 - 16,686,082 11,713,555,385 1,995,893,464 13,709,448,849 Accrued interest receivable 90,078,483 - 90,078,483

11,803,633,868 1,995,893,464 13,799,527,332 December 31, 2006 SYP F/Cy in SYP Total in SYP Cash 442,033,021 409,498,329 851,531,350 Compulsory reserve 755,600,000 1,171,863,707 1,927,463,707 Central Bank of Syria 11,074,896,379 10,799,656 11,085,696,035 12,272,529,400 1,592,161,692 13,864,691,092 Accrued interest receivable 13,139,510 - 13,139,510

12,285,668,910 1,592,161,692 13,877,830,602 Banking laws and regulations require banks to maintain cash compulsory reserve with the Central Bank of Syria in the form of deposit, calculated on the basis of 5% of total customers deposits (demand, savings and term) excluding housing savings deposit accounts as per decision (72/MN/84) dated December 8, 2004 issued by the Council of Money and Credit.

15

6. DEPOSITS WITH BANKS This caption comprises the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Current accounts 68,877,078 575,875,088 644,752,166 Interest earning term deposits - 31,176,840,672 31,176,840,672 Certificates of deposit 1,100,000,000 477,916,063 1,577,916,063 1,168,877,078 32,230,631,823 33,399,508,901 Accrued interest receivable 96,118,755 167,850,440 263,969,195

1,264,995,833 32,398,482,263 33,663,478,096 December 31, 2006 SYP F/Cy in SYP Total in SYP Current accounts 181,612,251 1,589,076,171 1,770,688,422 Interest earning term deposits 400,000,000 24,356,430,813 24,756,430,813 Certificates of deposit 1,000,000,000 - 1,000,000,000 1,581,612,251 25,945,506,984 27,527,119,235 Accrued interest receivable 54,648,137 99,892,881 154,541,018

1,636,260,388 26,045,399,865 27,681,660,253 Current accounts comprise the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Correspondent banks - Resident 68,877,078 24,157,935 93,035,013 Correspondent banks - Non resident - 292,172,443 292,172,443 Related banks - Non resident - 259,544,710 259,544,710

68,877,078 575,875,088 644,752,166 December 31, 2006 SYP F/Cy in SYP Total in SYP Correspondent banks - Resident 181,612,251 502,890,163 684,502,414 Correspondent banks - Non resident - 177,803,631 177,803,631 Related banks - Non resident - 908,382,377 908,382,377

181,612,251 1,589,076,171 1,770,688,422

16

Interest earning term deposits comprise the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Correspondent banks - Non resident - 30,208,888,172 30,208,888,172 Related banks - Non resident - 967,952,500 967,952,500

- 31,176,840,672 31,176,840,672 December 31, 2006 SYP F/Cy in SYP Total in SYP Correspondent banks - Resident 400,000,000 - 400,000,000 Correspondent banks - Non resident - 23,751,523,813 23,751,523,813 Related banks - Non resident - 604,907,000 604,907,000

400,000,000 24,356,430,813 24,756,430,813 Term deposits with nonresident correspondent banks as of December 31, 2007 include the counter value of USD 1,600,000 pledged by a correspondent bank to cover two documentary letters of credit for USD 800,000 each maturing in September 2008. Term deposits with related banks as of December 31, 2007 include the counter value of USD 1,000,000 pledged to cover the issuance of credit cards by the Bank. The average interest rate on interest earning term deposits by currency was as follows: December 31, 2007 USD EURO GBP AED Average Average Average Average interest interest interest interest Amount rate Amount rate Amount rate Amount rate SYP'000 % SYP'000 % SYP'000 % SYP'000 % Less than 3 months 24,386,434 5.00 3,568,489 4.46 96,120 5.85 19,567 3.13 Between 3 and 12 months 2,710,311 5.09 395,920 4.67 - - 27,096,745 3,964,409 96,120 19,567 December 31, 2006 USD EURO GBP SYP Average Average Average Average interest interest interest interest Amount rate Amount rate Amount rate Amount rate SYP'000 % SYP'000 % SYP'000 % SYP'000 % Less than 3 months 20,967,938 5.25 2,313,948 3.47 60,000 5.09 - Between 3 and 12 months 1,014,545 5.28 - - 400,000 5.00 21,982,483 2,313,948 60,000 400,000

17

Certificates of deposit comprise the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Certificates of deposit – Resident correspondent banks 1,100,000,000 - 1,100,000,000 Certificates of deposit - Non resident correspondent bank - 477,916,063 477,916,063 1,100,000,000 477,916,063 1,577,916,063 December 31, 2006 SYP F/Cy in SYP Total in SYP Certificates of deposit – Resident correspondent bank 1,000,000,000 - 1,000,000,000 1,100,000,000 - 1,000,000,000 Certificates of deposit issued by resident correspondent banks consist of 22 certificates for a value of SYP 50 million each, issued by the Real Estate Bank in Syria. As of December 31, 2007 these certificates are distributed based on maturity as follows: Interest Maturity Date Number Unit value Total value rate SYP SYP % April 2008 10 50,000,000 500,000,000 9.0 June 2008 2 50,000,000 100,000,000 9.5 November 2008 4 50,000,000 200,000,000 9.5 November 2009 4 50,000,000 200,000,000 10.0 November 2009 1 50,000,000 50,000,000 9.5 September 2010 1 50,000,000 50,000,000 10.0 22 1,100,000,000 Certificates of deposit issued by non resident correspondent banks represents the value of certificates having a par value in the amount of USD 10 million maturing in 2010 with an effective interest rate of 7.83%. This caption comprises as of December 31, 2007 the following: Counter value SYP in USD Balance, December 31, 2006 - - Par value of acquired certificates 480,500,000 10,000,000 Discount ( 2,594,700) ( 54,000) Net amount paid 477,905,300 9,946,000 Discount amortization 10,763 224 Carrying value, December 31, 2007 477,916,063 9,946,224

18

7. AVAILABLE FOR SALE SECURITIES This caption comprises the cost of 100,000 shares, out of 2 million shares in a related insurance company (representing 5% of ownership) acquired at the issue price of SYP 500. These shares were not recorded at fair value due to unavailability of quoted market prices.

19

8- HELD TO MATURITY SECURITIES This caption represents the value of investments in bonds with floating interest rates purchased from non resident banks with credit ratings varying between (A-) and (BBB+). These bonds comprise the following as of December 31, 2007: Effective Par Amortization Amortized cost at Maturity date interest rate value Discount Net Paid of discount December 31, 2007 % SYP SYP SYP SYP SYP

November 2013 7.51 96,100,000 - 96,100,000 - 96,100,000 January 2017 6.91 96,100,000 ( 2,762,875) 93,337,125 6,679 93,343,804 September 2015 6.70 96,100,000 ( 1,321,375) 94,778,625 31,569 94,810,194 April 2017 6.66 96,100,000 ( 1,321,375) 94,778,625 3,123 94,781,748 October 2016 6.22 96,100,000 ( 1,081,125) 95,018,875 3,219 95,022,094

480,500,000 ( 6,486,750) 474,013,250 44,590 474,057,840

Accrued interest receivable 3,698,361

477,756,201

In accordance with decision No. 2256/100 issued by the Central Bank of Syria on December 27, 2007, stipulating that all certificates of deposit should be classified under the "Deposits with banks" caption, a restatement of 2006 comparative figures was applied; consequently, certificates of deposit purchased from the Real-Estate Bank in Syria were reclassified under "Deposits with banks" caption.

20

9. LOANS AND ADVANCES This caption comprises the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Loans and advances to customers 7,622,937,606 573,267,924 8,196,205,530 Creditors accidentally debtors 46,471,240 16,767,987 63,239,227 Discounted commercial bills 3,506,851,698 - 3,506,851,698 Promissory notes 1,384,757,219 31,620,906 1,416,378,125 Advances on salaries 3,131,538 - 3,131,538 12,564,149,301 621,656,817 13,185,806,118 Classified Non-performing debts 210,024,314 5,508,128 215,532,442 Provision for impairment of loans and advances ( 28,876,920) - ( 28,876,920) 12,745,296,695 627,164,945 13,372,461,640 December 31, 2006 SYP F/Cy in SYP Total in SYP Loans and advances to customers 3,729,747,781 400,660,495 4,130,408,276 Creditors accidentally debtors 102,878,333 18,792,023 121,670,356 Discounted commercial bills 1,268,882,689 19,373,435 1,288,256,124 Promissory notes 784,005,743 20,842,932 804,848,675 Advances on salaries 3,139,330 - 3,139,330 5,888,653,876 459,668,885 6,348,322,761 Classified Non-performing debts 85,655,663 1,541,389 87,197,052 Provision for impairment of loans and advances ( 9,989,188) - ( 9,989,188) 5,964,320,351 461,210,274 6,425,530,625 Loans and advances to customers as of December 31, 2007 include an amount of SYP 606 million representing facilities granted to a related insurance company. The interest income on these facilities was SYP 20,020,721 in 2007 (SYP 9,205,069 in 2006).

21

Loans and advances to customers are distributed by economic sectors as follows: December 31, 2007 Corporate Individuals Total Percentage Percentage Percentage Amount to total Amount to total Amount to total Sector SYP’000 % SYP’000 % SYP’000 % Commercial 7,670,584 86.5 4,570,254 91.3 12,240,838 88.3 Industrial 307,311 3.5 167,096 3.3 474,407 3.4 Agricultural 74,535 0.8 3,486 0.1 78,021 0.6 Real Estate 182,952 2.1 69,651 1.4 252,603 1.8 Services and other sectors 628,276 7.1 196,146 3.9 824,422 5.9 8,863,658 100.0 5,006,633 100.0 13,870,291 100.0 Less : Deferred income ( 684,485) 13,185,806 December 31, 2006 Corporate Individuals Total Percentage Percentage Percentage Amount to total Amount to total Amount to total Sector SYP’000 % SYP’000 % SYP’000 % Commercial 4,945,320 89.2 1,983,286 94.2 5,928,606 90.9 Industrial 396,249 9.0 48,114 2.3 444,363 6.8 Agricultural 24,904 0.6 - 0.0 24,904 0.4 Services and other sectors 52,620 1.2 73,783 3.5 126,403 1.9 4,419,093 100.0 2,105,183 100.0 6,524,276 100.0 Less : Deferred income ( 175,953) 6,348,323 Classified non-performing debts comprise doubtful and litigated debts that were classified as non-performing debts due to the existence of doubts or non-collection probability over these debts and/or revenues there from. Classified non-performing debts comprise the following: December 31, 2007 Debt balance (net of unearned Provision for interest) impairment Net balance SYP SYP SYP Substandard debts 83,905,640 - 83,905,640 Doubtful debts 67,996,579 ( 11,813,165) 56,183,414 Bad debts 63,630,223 ( 17,063,755) 46,566,468

215,532,442 ( 28,876,920) 186,655,522

22

December 31, 2006 Debt balance (net of unearned Provision for interest) impairment Net balance SYP SYP SYP Substandard debts 25,641,065 - 25,641,065 Doubtful debts 61,555,987 ( 9,989,188) 51,566,799

87,197,052 ( 9,989,188) 77,207,864 The movement of unearned interest was as follows: 2007 2006 SYP SYP Balance January 1 2,806,000 - Additions 32,436,158 2,806,000 Settlements ( 1,077,700) -

Balance December 31 34,164,458 2,806,000 The movement of provision for impairment of loans and advances was as follows: 2007 2006 SYP SYP Balance January 1 9,989,188 - Additions, period charges 19,017,758 9,989,188 Write offs ( 130,026) -

Balance December 31 28,876,920 9,989,188 10. CUSTOMERS’ / BANKS’ LIABILITY UNDER ACCEPTANCES Customers’ liability under acceptances represents the liability to the Bank of its customers for shipping documents and drafts or bills of exchange, which have been accepted, by the Bank and/or other banks for its account. These balances relate to deferred payment documentary letters of credit on shipping document. The commitments resulting from these acceptances are stated as a liability in the balance sheet for the same amount.

23

11. OTHER ASSETS This caption comprises the following: December 31, 2007 2006 SYP SYP Prepaid rent 316,500 500,836 Other prepaid expenses 18,572,656 3,727,395 Stationery 3,042,065 3,505,500 Deferred charges 674,854 986,465 Stamps 506,147 440,842 Other debit balances 6,451,107 1,248,881 29,563,329 10,409,919

24

12. PROPERTY AND EQUIPMENT This caption comprises the following: Land Furniture Advances on and and office Computer Leasehold capital buildings equipment equipment Vehicles improvements expenditure Total SYP SYP SYP SYP SYP SYP SYP Historical Cost: Balance – December 31, 2005 232,857,428 30,717,626 20,252,465 6,347,600 135,395,952 26,735,661 452,306,732 Additions 83,825,905 25,990,390 12,007,758 - 94,490,769 63,082,901 279,397,723 Transfer from key money (Note 13) 71,000,000 - - - - - 71,000,000 Transfers 51,554,180 586,800 807,132 - - ( 52,948,112) - Balance – December 31, 2006 439,237,513 57,294,816 33,067,355 6,347,600 229,886,721 36,870,450 802,704,455 Additions 36,500,000 26,795,423 5,518,647 1,190,000 59,720,509 38,772,581 168,497,160 Disposals - ( 80,498) - - - - ( 80,498) Transfers - 4,605,944 7,018,192 - 3,995,790 ( 15,619,926) - Balance – December 31, 2007 475,737,513 88,615,685 45,604,194 7,537,600 293,603,020 60,023,105 971,121,117 Accumulated Depreciation: Balance – December 31, 2005 ( 4,873,793) ( 4,062,625) ( 4,210,347) ( 2,221,635) ( 22,451,491) - ( 37,819,891) Additions ( 11,222,063) ( 6,513,104) ( 5,422,867) ( 1,269,520) ( 34,813,212) - ( 59,240,766) Adjustments - 110,437 - - - - 110,437 Transfer from key money (Note 13) ( 6,804,163) - - - - - ( 6,804,163) Balance – December 31, 2006 ( 22,900,019) ( 10,465,292) ( 9,633,214) ( 3,491,155) ( 57,264,703) - ( 103,754,383) Additions ( 21,081,182) ( 13,309,723) ( 8,146,138) ( 1,348,853) ( 52,403,101) - ( 96,288,997) Disposal - 33,359 - - - - 33,359 Balance – December 31, 2007 ( 43,981,201) ( 23,741,656) ( 17,779,352) ( 4,840,008) ( 109,667,804) - ( 200,010,021) Net Book Value: Balance – December 31, 2007 431,756,312 64,874,029 27,824,842 2,697,592 183,935,216 60,023,105 771,111,096 Balance – December 31, 2006 416,337,494 46,829,524 23,434,141 2,856,445 172,622,018 36,870,450 698,950,072

25

Advances on capital expenditure include an amount of SYP 20 million representing the price of a real estate property acquired in Homs district for a potential branch opening. Up to the date of these financial statements, this property is still classified as a residential property and consequently can not be operated as a commercial property by the bank. Land and buildings include an amount of SYP 3,916,000 representing the cost of a plot of land acquired during 2006 in the region of Aadra for the purpose of opening a new branch. During 2006, the leased premises in Damascus, Nijmeh Square was acquired and the key money previously paid to the lessor was considered as a payment on account of the total cost of the real estate. The historical cost and accumulated amortization amounting to SYP 71,000,000 and SYP 6,804,163 respectively were reclassified under the Buildings caption (See Note 13). 13. INTANGIBLE ASSETS This caption comprises the following: Key Money Software Total SYP SYP SYP Historical Cost: Balance – December 31, 2005 132,000,000 6,658,842 138,658,842 Additions 30,000,000 4,783,750 34,783,750 Transfer to buildings (Note 12) ( 71,000,000) - ( 71,000,000) Balance – December 31, 2006 91,000,000 11,442,592 102,442,592 Additions - 1,700,470 1,700,470 Balance – December 31, 2007 91,000,000 13,143,062 104,143,062 Accumulated Amortization: Balance – December 31, 2005 ( 8,591,662) ( 1,714,397) ( 10,306,059) Additions ( 5,245,833) ( 1,875,370) ( 7,121,203) Transfer to buildings (Note 12) 6,804,163 - 6,804,163 Balance – December 31, 2006 ( 7,033,332) ( 3,589,767) ( 10,623,099) Additions ( 4,550,000) ( 2,602,983) ( 7,152,983) Balance – December 31, 2007 ( 11,583,332) ( 6,192,750) ( 17,776,082) Net Book Value: Balance – December 31, 2007 79,416,668 6,950,312 86,366,980 Balance – December 31, 2006 83,966,668 7,852,825 91,819,493

26

14. REGULATORY BLOCKED FUND According to paragraph B of Article 12 of Law No. 28/2001, private sector banks are required to block 10% of their capital as Regulatory Blocked Funds at the Central Bank of Syria as an interest-free blocked deposit. This caption comprises the following: December 31, 2007 2006 SYP SYP Blocked funds in Syrian Pounds 115,789,800 115,789,800 Blocked funds in US Dollars 167,991,500 178,480,040 283,781,300 294,269,840 The allocation of the blocked funds is as follows: Nominal Subscribed value per Blocked Blocked Currency Shares share Value Capital Capital SYP SYP % SYP Syrian Pounds 2,315,796 500 1,157,898,000 10 115,789,800 US Dollars 3,684,204 500 1,842,102,000 10 184,210,200 Negative difference in exchange - - ( 16,218,700) 6,000,000 3,000,000,000 283,781,300 The negative difference in exchange is derived as follows: Historical Value as at Negative Shares subscribed Number of Blocked capital translation Historical December 31, difference in USD shares in USD rate value 2007 in exchange USD SYP SYP SYP Original issuance 1,779,114 1,727,295 51.50 88,955,700 82,996,525 ( 5,959,175) Capital increase 1,905,090 1,768,886 53.85 95,254,500 84,994,975 ( 10,259,525) 3,684,204 3,496,181 184,210,200 167,991,500 ( 16,218,700)

27

15. DEPOSITS FROM BANKS AND OTHER FINANCIAL INSTITUTIONS This caption comprises the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Demand deposits - correspondent banks and institutions 217,501,231 315,121,820 532,623,051 Demand deposits - related banks and institutions 65,345,345 233,789,505 299,134,850 Term deposits - correspondent banks and institutions 24,683,218 252,376,613 277,059,831 Term deposits - related banks and institutions 27,286,986 63,178,461 90,465,447 334,816,780 864,466,399 1,199,283,179 Accrued interest payable 630,827 501,271 1,132,098 335,447,607 864,967,670 1,200,415,277 December 31, 2006 SYP F/Cy in SYP Total in SYP Demand deposits - correspondent banks and institutions 35,541,938 220,099,046 255,640,984 Demand deposits - related banks and institutions 9,012,556 12,844,940 21,857,496 Term deposits - related banks and institutions 166,626,484 64,095,690 230,722,174 211,180,978 297,039,676 508,220,654 Accrued interest payable 6,008,283 231,457 6,239,740 Clearing checks 55,173,020 - 55,173,020 272,362,281 297,271,133 569,633,414 16. CUSTOMERS’, AND RELATED PARTIES' DEPOSITS AND OTHER CREDIT BALANCES This caption consists of the following: December 31, 2007 SYP F/Cy in SYP Total in SYP Demand deposits 8,643,067,907 7,237,634,522 15,880,702,429 Term deposits 13,870,692,472 23,906,224,357 37,776,916,829 Savings accounts 1,260,126,171 358,845,755 1,618,971,926 Related party deposits 289,733,322 151,676,527 441,409,849 Cash margins against loans and advances 20,276,816 7,844,094 28,120,910 24,083,896,688 31,662,225,255 55,746,121,943 Accrued interest payable 182,510,284 98,676,099 281,186,383 24,266,406,972 31,760,901,354 56,027,308,326

28

December 31, 2006 SYP F/Cy in SYP Total in SYP Demand deposits 6,521,671,709 7,256,900,905 13,778,572,614 Term deposits 10,430,516,719 17,875,789,656 28,306,306,375 Savings accounts 1,110,921,377 267,655,998 1,378,577,375 Related party deposits 154,557,314 138,851,960 293,409,274 18,217,667,119 25,539,198,519 43,756,865,638 Accrued interest payable 122,711,759 77,124,485 199,836,244 18,340,378,878 25,616,323,004 43,956,701,882 Customers’ and, related parties’ deposits and other credit balances are distributed by brackets as follows: December 31, 2007 percentage of Percentage No. of of Bracket Number of Customers to Bracket Amount Customers Total Amount to total % SYP’000 % Less than SYP 500,000 33,892 74 2,409,715 4.3 Between SYP 500,001 and SYP 1,000,000 3,389 7 2,432,036 4.4 Between SYP 1,000,001 and SYP 10,000,000 7,196 16 22,305,844 40.0 More than 10,000,000 1,049 3 28,598,527 51.3 45,526 100 55,746,122 100.0 December 31, 2006 percentage of Percentage No. of of Bracket Number of Customers to Bracket Amount Customers Total Amount to total % SYP’000 % Less than SYP 500,000 17,990 68 1,370,021 3.2 Between SYP 500,001 and SYP 1,000,000 2,296 9 1,602,424 3.7 Between SYP 1,000,001 and SYP 10,000,000 5,181 20 15,848,470 36.2 Greater than 10,000,000 780 3 24,935,951 56.9 26,247 100 43,756,866 100.0

29

17. CASH MARGINS This caption comprises the following: December 31, 2007 2006 SYP SYP Cash margins against documentary letters of credit 475,814,879 331,790,819 Cash margins against acceptances 150,828,728 81,976,876 Cash margins against guarantees 360,198,492 269,219,443 Other margins 241,945,179 47,003,013 1,228,787,278 729,990,151 Accrued interest payable 2,375,023 - 1,231,162,301 729,990,151 18. OTHER LIABILITIES This caption consists of the following: December 31, 2007 2006 SYP SYP Provision for income tax 129,500,000 88,885,000 Withheld taxes on interest paid to customers 43,365,038 28,916,743 Withheld taxes on salaries 9,876,567 7,594,681 Other withheld taxes 5,222,768 3,460,512 Social security dues 6,586,738 5,884,287 Checks to be paid 382,559,352 355,946,918 Net inter-branch accounts 115,673 61,908 Fixed assets suppliers 8,006,037 3,839,905 Amounts refundable to shareholders 1,054,440 1,816,485 Dividends payable 20,420,275 - Fair value of financial guarantees 7,653,879 2,064,955 Accrued bonuses and incentives 23,300,000 15,000,000 Accrued electricity and telephone charges 3,840,000 4,499,959 Provision for fluctuations in of exchange rates 2,483,000 2,483,000 Accrued professional fees 2,462,490 1,282,964 Other liabilities 24,625,454 31,817,227 671,071,711 553,554,544 The movement of the provision for income tax was as follows: 2007 2006 Balance as of January 1 88,885,000 50,227,000 Settlement of prior year income tax ( 88,885,000) ( 50,227,000) Accrued income tax for the year 129,500,000 88,885,000 Balance as of December 31 129,500,000 88,885,000

30

The provision for income tax for 2007 was calculated as follows: SYP Profit for 2007 before income tax 362,997,546 Add: Unrealized exchange losses 107,620,933 Provision for doubtful debts 19,017,758 Non-tax-deductible expenses 28,250,102 Taxable profit 517,886,339 Income tax (25%) 129,500,000 Amounts refundable amounts to shareholders represent excess amounts paid by shareholders when subscribing for the capital increase during 2005. In accordance with decision No. 249 issued by the Council of Money and Credit during 2006, banks operating in Syria are required to set up a provision for fluctuations in exchange rates. This provision should equal 10% of the "Operational currency position". During 2007, this decision was suspended until issuance of its implementation instructions, and consequently, no provision was set up this year. 19. CAPITAL The Bank’s capital as at December 31, 2004 consisted of 3,000,000 nominative shares of SYP 500 par value each, authorized and fully paid. On May 25, 2004, the Extraordinary General Assembly decided to increase the Bank’s capital from SYP 1.5 billion to SYP 3 billion, by issuing 3,000,000 additional shares of SYP 500 each. The subscription in the new shares took place during the period from September 18, 2005 to October 10, 2005. The allocation of the new shares was approved by the Extraordinary General Assembly held on November 23, 2005. As of December 31, 2007, capital consists of 6,000,000 nominative shares of SYP 500 par value each, authorized and fully paid and is broken down by currency as follows: Currency Adjustment on No. of Historical Capital Funded Shares USD Equivalent in U.S. Dollars SYP SYP Original issuance: Capital funded in Syrian Pound 1,220,886 - 610,443,000 - Capital funded in U.S. Dollar (reflected in SYP) 1,779,114 17,272,950 889,557,000 ( 59,591,753) 3,000,000 1,500,000,000 ( 59,591,753) Capital increase: Capital funded in Syrian Pound 1,094,910 - 547,455,000 - Capital funded in U.S. Dollar (reflected in SYP) 1,905,090 17,688,860 952,545,000 ( 102,595,277) 3,000,000 1,500,000,000 ( 102,595,277) Total Capital: Capital funded in Syrian Pound 2,315,796 - 1,157,898,000 - Capital funded in U.S. Dollar (reflected in SYP) 3,684,204 34,961,810 1,842,102,000 ( 162,187,030) 6,000,000 3,000,000,000 ( 162,187,030)

31

Capital paid in US Dollars and reflected in Syrian Pounds comprises the following: Currency Historical Value as at Adjustment on Shares subscribed Number of Capital funded translation Historical December 31, capital funded in USD shares in USD rate value 2007 in USD USD SYP SYP SYP Original issuance 1,779,114 17,272,950 51.50 889,557,000 829,965,247 ( 59,591,753) Capital increase 1,905,090 17,688,860 53.85 952,545,000 849,949,723 ( 102,595,277) 3,684,204 34,961,810 1,842,102,000 1,679,914,970 ( 162,187,030) The Bank manages its capital to comply with the instructions of the Central Bank of Syria stipulated in decision Number 253 issued on January 24, 2007, regarding equity sufficiency. This decision requires that the Bank's solvency(or capital adequacy) ratio should not be less than 8% (BASEL 2). The capital adequacy ratio as of December 31, 2007 was 12.30%, calculated as follows: SYP,000 Net equity (excluding current year profit) 3,087,722 Risk-weighted assets 21,331,498 Risk-weighted off balance sheet items 2,238,201 Market and operational risks 1,534,219 25,103,918

Capital adequacy ratio 12.30% 20. RESERVES Article 246 of the Code of Commerce requires the set up of a legal reserve at 10% of annual net profit up to 50% of capital. This reserve is not available for distribution. Article 97 of the Money and Credit law require the set up of a special reserve at 10% of annual net profit up to 100% of capital. This reserve is not available for distribution. 21. CURRENCY ADJUSTMENTS ON STRUCTURAL POSITION On December 26, 2006 the Money and Credit Council issued Decision number 249, with effect from January 1, 2007, which allowed banks operating in Syria to hold a structural currency position equivalent to 60% of that equity. This decision considered the gains/(losses) resulting from valuation of the structural currency position, as unrealized gains/(losses) and, consequently, these gains are not subject to tax nor available for distribution. In prior years, the structural currency position of Bank of Syria and Overseas comprised only of the capital funded in US Dollars, and accordingly the resulting exchange differences used to be classified under "Currency adjustments on capital funded in US Dollars". As a result of the above decision, the

32

bank increased in 2007 its net asset position in foreign currencies (US Dollars) up to the allowable limit (approximately 60% of net equity), and consequently the caption was renamed to "Exchange adjustments on structural currency position". This caption, comprises the following as of December 31, 2007: SYP Unrealized negative differences of exchange on capital (note 19) 162,187,030 Unrealized negative differences of exchange on remaining structural currency position 2,969,322 165,156,352 22. INTEREST INCOME This caption consists of the following: Year ended December 31, 2007 2006 SYP SYP Interest income from: Loans and advances 606,538,598 358,502,110 Discounted bills and promissory notes 355,701,044 168,912,979 Deposits with non resident correspondent banks 1,500,871,780 876,970,572 Deposits with resident correspondent banks 86,544,565 23,887,268 Deposits with non resident related banks 123,782,649 74,585,648 Investments in securities 100,585,278 45,113,890 2,774,023,914 1,547,972,467 23. INTEREST EXPENSE This caption consists of the following: Year ended December 31, 2007 2006 SYP SYP Interest expense on: Term deposits 1,981,066,099 1,009,033,679 Savings deposits 41,129,449 42,388,416 Current accounts 104,660,337 73,801,593 Deposits from banks and other financial institutions 33,207,867 1,273,329 2,160,063,752 1,126,497,017

33

24. FEE AND COMMISSION INCOME This caption consists of the following: Year ended December 31, 2007 2006 SYP SYP Commission on: Banking operations 104,785,140 72,547,481 Discounted bills and promissory notes 46,424,160 16,818,744 Documentary letters of credit and acceptances 59,313,583 41,399,588 Guarantees 63,186,873 38,371,945 Collection documents and drafts 48,476,483 46,566,850 Other commissions 27,440,993 25,046,313 349,627,232 240,750,921 25. SALARIES AND RELATED CHARGES This caption consists of the following: Year ended December 31, 2007 2006 SYP SYP Salaries 133,964,125 90,992,898 Bonuses and incentives 61,603,381 43,775,315 Social security 15,523,597 11,556,123 Representation allowance 5,252,132 4,500,498 Other expenses 609,038 1,028,149 216,952,273 151,852,983 26. GENERAL OPERATING EXPENSES This caption consists of the following: Year ended December 31, 2007 2006 SYP SYP Travel 8,489,603 9,200,975 Entertainment 1,504,960 751,031 Subscriptions 9,674,868 1,663,848 Seminars and training expenses 1,215,450 1,155,425 Registration fees 1,535,644 2,493,224 Advertising and publicity 8,794,671 12,447,068 Professional fees 12,178,172 12,451,346 Maintenance and repairs 6,365,077 3,268,464 Energy and water 2,916,488 3,384,673 Telecommunication 9,856,416 10,350,056 Printing and stationery 7,240,711 6,670,608 Postage and freight 816,515 810,304 Rent 2,303,336 1,685,000 Risk and fire insurance 1,195,059 3,743,952 Other expenses 26,842,272 15,019,060 100,929,242 85,095,034

34

27. FINANCIAL INSTRUMENTS WITH OFF-BALANCE SHEET RISKS The guarantees and stand by letters of credit and the documentary and commercial letters of credit represent financial instruments with contractual amounts representing credit risk. The guarantees and stand by letters of credit represent irrevocable assurances that the Bank will make payments in the event that a customer cannot meet its obligations to third parties and are not different from loans and advances on the balance sheet. However, documentary and commercial letters of credit, which represent written undertakings by the Bank on behalf of a customer authorizing a third party to draw drafts on the Bank up to a stipulated amount under specific terms and conditions, are collateralized by the underlying shipment document of goods to which they relate and, therefore, have significantly less risks. 28. NET PROFIT FOR THE YEAR This caption includes the exchange adjustments on structural currency position, in compliance with Decision No. 249 issued by the Council of Money and Credit as follows: Year ended December 31, 2007 2006 SYP SYP Net profit for the year exclusive of unrealized losses 341,118,479 236,907,726 Unrealized loss ( 107,620,933) ( 133,088,681) Net profit for the year inclusive of unrealized loss 233,497,546 103,819,045 29. EARNINGS PER SHARE The computation of the basic earnings per share for ordinary shares is based on the Bank's net income, and the weighted average number of ordinary shares outstanding during the year. Year ended December 31, 2007 2006 SYP SYP Net profit for the year 233,497,546 103,819,045 Weighted average number of shares for computation of earnings per share 6,000,000 6,000,000 Earnings per share: Basic 38.92 17.30 Diluted 38.92 17.30

35

30. TRANSACTIONS WITH RELATED PARTIES The balance sheet as of December 31, 2007 includes the following balances with related parties: December 31, 2007 2006 SYP SYP Debit balances Currents accounts with banks 259,544,710 908,382,377 Interest earning term deposits with banks 967,952,500 604,907,000 Loans and advances 606,230,230 204,617,678 Credit balances Deposits from banks and other financial institutions 389,600,297 252,579,670 Deposits from customers and other credit balances 441,409,849 293,409,274 The following transactions with related parties were recorded in the income statement: Year ended December 31, 2007 2006 SYP SYP Interest income 143,803,378 83,790,717 Interest expense 19,448,487 4,039,012 General Manager remunerations 11,400,000 6,480,166 Guarantees and stand by letters of credit, documentary letters of credit and acceptances as of December 31, 2007 include around SYP 733 million, SYP 347 million and SYP 87 million respectively, conducted with related parties. 31. CASH AND CASH EQUIVALENTS This caption comprises the following: December 31, 2007 2006 SYP SYP Cash, compulsory reserves and deposits at Central Bank of Syria (excluding accrued interest receivable) 13,709,448,849 13,864,691,092 Deposits with banks with maturities of less than 3 months (excluding accrued interest receivable) 28,715,362,253 25,112,574,034 Deposits from banks and other financial institutions with maturities of less than 3 months (excluding accrued interest payable) ( 1,199,283,179) ( 438,393,674)

41,225,527,923 38,538,871,452

36

32. FINANCIAL RISK MANAGEMENT A- Credit risk Credit risk is the risk that one party will fail to discharge an obligation and cause the other party to incur a financial loss. The Bank monitors this risk by following up credit exposures, limiting transactions with specific counter-parties, and continually assessing the financial position and creditworthiness of the related borrowers.

Concentration of credit risk arises when a number of counter-parties are engaged in similar business activities in the same geographic region, or have similar economic features that would cause their ability to meet contractual obligations to be similarly affected by changes in economic, political or other conditions. Concentrations of credit risk indicate the relative sensitivity of the Bank’s performance to developments affecting a particular industry or geographical location.

1- Management of credit risk The Bank is managing credit risk through diversifying and spreading of its lending activities to ensure that no unjustified concentration exists with individuals, or group of individuals, in certain economic sectors or geographic areas, in addition to obtaining sufficient real collateral. The Bank’s Board of Directors is the main party responsible for the management of credit risk. The Board of Directors establishes the strategies and policies for risk management, and reviews, and suggests any adjustments imposed by the changes in the Bank’s environment. In addition to the Board of directors, the Bank has several committees participating in credit risk management. The main committees are: Credit committee/Credit department Responsible mainly for monitoring proper execution of the credit policy setup by the Board of Directors. Its main duties include: - Setting up the limit of loans to be granted for each borrower. - Reviewing, and classifying of loans and establishing appropriate provisions therefore. - Ascertain confirmation of the credit policy with the instructions of the Council of Money and Credit. Internal audit: Internal audit department is responsible for controlling and auditing the process of managing the different risks of the Bank, to ensure compliance with policies in place.

37

2- Measurement of credit risk In accordance with Decision number 94, issued by the Council of Money and Credit on December 19, 2004, the bank regularly reviews the portfolio of credit granted and classifies same according to the following categories: Ordinary loans Represent loans which are collectible, both principal and interest, with no likelihood for losses being incurred. Special mention loans Loans classified under this category are collectible, both principal and interest, but which shows non-encouraging sign of weakness sometimes, that might cause the Bank to incur possible losses in the future if the debt is not quickly dealt with and followed. The Bank is required to monitor and follow up these loans within a period not exceeding 6 months to complete the file and pending issues. Substandard loans These loans have the same characteristics of the "Special mention" loans in addition to other indications, mainly: Delay in settlement of installments or interest due; absence of settlement in the account movement for a period of three months; decrease in cash flow. Doubtful debts These are debts that have the same characteristics as the "Substandard loans" in addition to increased risk due to insufficient collateral and a high possibility for partial credit loss to the Bank represented by: - Non compliance with the settlement schedule for a period exceeding 3 months from maturity. - Absence of deposits for a period exceeding 3 months. - Existence of warnings and lawsuits raised by the Bank against the borrower. Bad debts These are debts that have the same characteristics of "Doubtful debts" in addition to: - Non-existence of collateral or insufficiency of its value, if it exists. - No possibility to contact the borrower. - Bankruptcy of borrower. - Amounts expected to be recovered from borrower are nil. - Guarantors not willing or unable to fulfill their guarantee commitment. Provisions for credit loss are set up by the Bank after review of the customers credit files, and in accordance with Decision No. 94 issued by the Council of Money and Credit.

3- Credit risk mitigation policies The Bank is managing credit risk through diversifying and spreading its lending activities to ensure that no unjustified concentration exists with individuals, or a group of individuals, in certain economic sectors or geographic areas, in addition to obtaining sufficient real guarantees, mainly as: Pledged deposits - Real estate mortgages - Bank guarantees…

38

4- Financial assets and related risk concentrations

Deposits with banks and other financial institutions December 31, 2007 Percentage No. of Percentage Bracket to total banks to total No. amount amount % SYP’000 % Less than SYP 100,000,000 7 20 294,319 0.9 Between SYP 100,000,001 and SYP 500,000,000 8 23 2,695,206 8.0 Between SYP 500,000,001 and SYP 1,000,000,000 5 14 3,866,768 12.1 More than SYP 1,000,000,000 15 43 26,807,185 79.6 35 100 33,663,478 100.0 December 31, 2006 Percentage No. of Percentage Bracket to total banks to total No. amount amount % SYP’000 % Less than SYP 100,000,000 7 23 258,564 0.9 Between SYP 100,000,001 and SYP 500,000,000 2 7 704,414 2.5 Between SYP 500,000,001 and SYP 1,000,000,000 9 30 7,116,916 25.7 More than SYP 1,000,000,000 12 40 19,601,766 70.9 30 100 27,681,660 100.0

39

Loans and advances

Loans and advances are distributed between brackets as follows: December 31, 2007 Percentage No. of Percentage Bracket to total banks to total No. amount amount % SYP’000 % Less than SYP 500,000 605 45 96,495 0.69 Between SYP 500,001 and SYP 1,000,000 233 17 165,478 1.17 Between SYP 1,000,001 and SYP 10,000,000 329 24 1,035,209 7.47 More than SYP 10,000,000 184 14 12,573,109 90.67 1,351 100 13,870,291 100.00 Less: deferred income ( 684,485) 13,185,806 December 31, 2006 Percentage No. of Percentage Bracket to total banks to total No. amount amount % SYP’000 % Less than SYP 500,000 233 42 20,490 0.30 Between SYP 500,001 and SYP 1,000,000 49 9 33,072 0.51 Between SYP 1,000,001 and SYP 10,000,000 155 28 605,157 9.15 More than SYP 10,000,000 119 21 5,865,557 90.04 556 100 6,524,276 100.00 ( 175,953) Less: deferred income 6,348,323

B - Liquidity risk Liquidity risk is the risk that the Bank will be unable to meet its net funding requirements. Liquidity risk can be caused by market disruptions or credit downgrades, which may cause certain sources and flows of funding to the Bank to dry up immediately.

Management of liquidity risk To minimize liquidity risk, management diversifies its funding sources and manage its assets within liquidity policy approach, represented by maintaining, a sufficient liquidity balance. Management manages the maturity profile of its assets and liabilities to ensure that adequate liquidity is maintained. In addition, and in accordance with the applicable Syrian laws and regulations, the Bank maintains with the Central Bank of Syria a compulsory cash reserve equal to 5% of customers deposits and a regulatory blocked deposit equal to 10% of its capital.

40

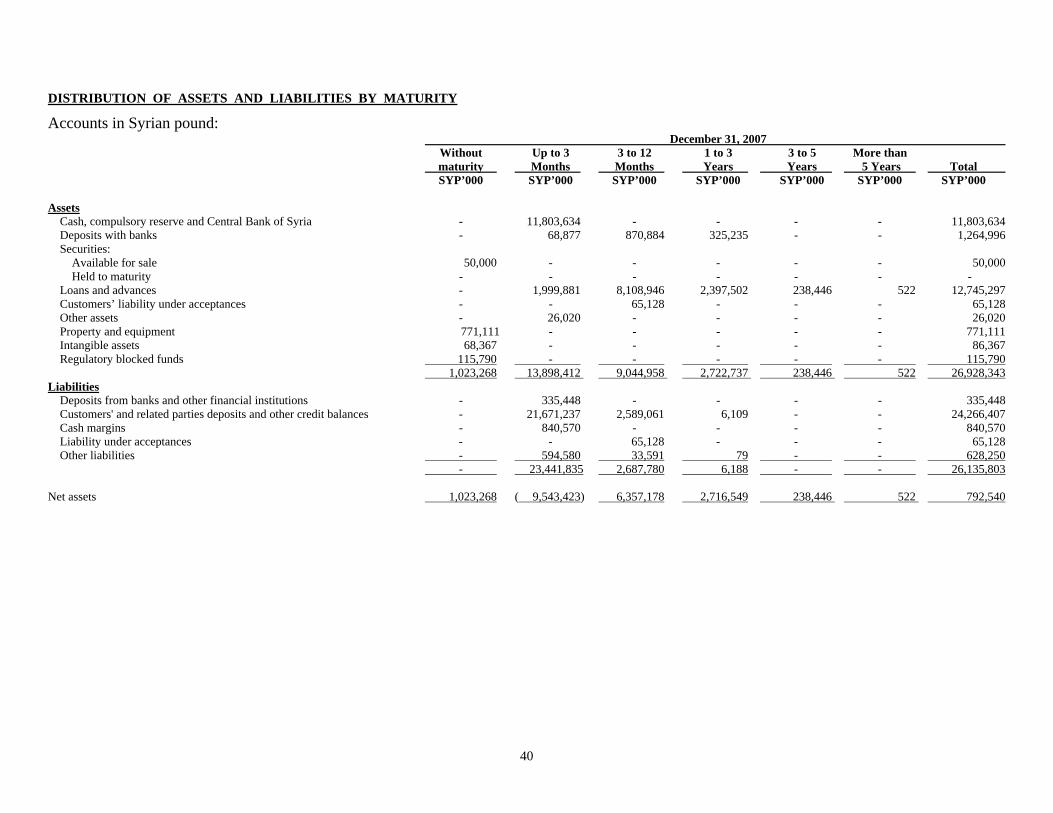

DISTRIBUTION OF ASSETS AND LIABILITIES BY MATURITY

Accounts in Syrian pound: December 31, 2007 Without Up to 3 3 to 12 1 to 3 3 to 5 More than maturity Months Months Years Years 5 Years Total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank of Syria - 11,803,634 - - - - 11,803,634 Deposits with banks - 68,877 870,884 325,235 - - 1,264,996 Securities: Available for sale 50,000 - - - - - 50,000 Held to maturity - - - - - - - Loans and advances - 1,999,881 8,108,946 2,397,502 238,446 522 12,745,297 Customers’ liability under acceptances - - 65,128 - - - 65,128 Other assets - 26,020 - - - - 26,020 Property and equipment 771,111 - - - - - 771,111 Intangible assets 68,367 - - - - - 86,367 Regulatory blocked funds 115,790 - - - - - 115,790 1,023,268 13,898,412 9,044,958 2,722,737 238,446 522 26,928,343 Liabilities Deposits from banks and other financial institutions - 335,448 - - - - 335,448 Customers' and related parties deposits and other credit balances - 21,671,237 2,589,061 6,109 - - 24,266,407 Cash margins - 840,570 - - - - 840,570 Liability under acceptances - - 65,128 - - - 65,128 Other liabilities - 594,580 33,591 79 - - 628,250 - 23,441,835 2,687,780 6,188 - - 26,135,803 Net assets 1,023,268 ( 9,543,423) 6,357,178 2,716,549 238,446 522 792,540

41

Accounts in foreign currencies – reflected in Syrian pound equivalent: December 31, 2007 Without Up to 3 3 to 12 1 to 3 3 to 5 More than maturity Months Months Years Years 5 Years Total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank of Syria - 1,995,893 - - - - 1,995,893 Deposits with banks - 30,319,726 1,600,840 477,916 - - 32,398,482 Securities: Available for sale - - - - - - - Held to maturity - 3,698 - - 96,100 377,958 477,756 Loans and advances - 47,090 580,075 - - - 627,165 Customers’ liability under acceptances - - 993,116 - - - 993,116 Other assets - 3,543 - - - - 3,543 Property and equipment - - - - - - - Intangible assets - - - - - - - Regulatory blocked funds 167,991 - - - - - 167,991 167,991 32,369,950 3,174,031 477,916 96,100 377,958 36,663,946 Liabilities Deposits from banks and other financial institutions - 864,967 - - - - 864,967 Customers' and related parties deposits and other credit balances - 30,202,127 1,544,298 14,476 - - 31,760,901 Cash margins - 390,592 - - - - 390,592 Liability under acceptances - - 993,116 - - - 993,116 Other liabilities - 41,836 926 60 - - 42,822 - 31,499,522 2,538,340 14,536 - - 34,052,398 Net assets 167,991 870,428 635,691 463,380 96,100 377,958 2,611,548

42

Accounts in Syrian pounds December 31, 2006 Without Up to 3 3 to 12 1 to 3 3 to 5 More than maturity Months Months Years Years 5 Years Total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank of Syria - 12,285,669 - - - - 12,285,669 Deposits with banks and financial institutions - 591,146 534,250 510,864 - - 1,636,260 Securities: Available for sale 50,000 - - - - - 50,000 Held to maturity - - - - - - - Loans and Advances - 256,116 5,095,307 612,898 - - 5,964,321 Customers’ liability under acceptances - - 92,886 - - - 92,886 Other assets 698,950 10,032 - - - - 10,032 Property and equipment - - - - - - 698,950 Intangible assets 91,819 - - - - - 91,819 Regulatory blocked funds 115,790 - - - - - 115,790 956,559 13,142,963 5,722,443 1,123,762 - - 20,945,727 Liabilities Deposits from banks and other financial institutions - 141,354 131,008 - - - 272,362 Customers' and related parties deposits and other credit balances - 14,669,432 3,667,344 3,603 - - 18,340,379 Cash margins - 376,868 - - - - 376,868 Liability under acceptances - 92,886 - - - - 92,886 Other liabilities - 474,595 35,333 - - - 509,928 - 15,755,135 3,833,685 3,603 - - 19,592,423 Net assets 956,559 ( 2,612,172) 1,888,758 1,120,159 - - 1,353,304

43

Accounts in foreign currencies reflected in Syrian pound equivalent: December 31, 2006 With no Up to 3 3 to 12 1 to 3 3 to 5 More than maturity Months Months Years Years 5 Years Total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank of Syria - 1,592,162 - - - - 1,592,162 Deposits with banks - 25,006,395 1,039,005 - - - 26,045,400 Securities: Available for sale - - - - - - - Held to maturity - - - - - - - Loans and advances - 447,511 13,699 - - - 461,210 Customers’ liability under acceptances - - 519,738 - - - 519,738 Other assets - 378 - - - - 378 Property and equipment - - - - - - - Intangible assets - - - - - - - Regulatory blocked funds 178,480 - - - - - 178,480 178,480 27,046,446 1,572,442 - - - 28,797,368 Liabilities Deposits from banks and other financial institutions - 232,943 64,328 - - - 297,271 Customers' and related parties deposits and other credit balances - 24,142,139 1,472,294 1,890 - - 25,616,323 Accounts payable and miscellaneous creditors - 353,122 - - - - 353,122 Liability under acceptances - - 519,738 - - - 519,738 Other liabilities - 43,627 - - - - 43,627 - 24,771,831 2,056,360 1,890 - - 26,830,081 Net assets 178,480 2,274,615 ( 483,918) ( 1,890) - - 1,967,287

44

C - Market risks Market risks are the risks that the fair value or future cash flows of financial instruments will be affected by changes in market prices, such as interest rates and exchange rates.

Management of market risks The Bank is exposed to the risks of currency transactions related to the effect of fluctuations;

exchange rates on its financial position and its cash flows.

The Bank takes preventive actions to mitigate this risk by setting up limits for the operating currency positions for cash currency and in total for both overnight and intra-day positions in line with the limits specified by the regulatory authorities.

DISTRIBUTION OF ASSETS AND LIABILITIES BY MAJOR CURRENCIES December 31, 2007 Other Syrian US Dollars Euro Currencies Pounds C/V SYP C/V SYP C/V SYP Total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000

Assets

Cash, compulsory reserve

and Central Bank of Syria 11,803,634 1,546,515 421,469 27,909 13,799,527

Deposits with banks 1,264,996 28,034,441 4,131,876 232,165 33,663,478

Securities:

Available for sale 50,000 - - - 50,000

Held to maturity - 477,756 - - 477,756

Loans and advances 12,745,297 496,486 130,551 128 13,372,462

Customers’ liability under acceptances 65,128 826,128 122,882 44,106 1,058,244

Other assets 26,020 3,214 328 1 29,563

Property and equipment 771,111 - - - 771,111

Intangible assets 86,367 - - - 86,367

Regulatory blocked fund 115,790 167,991 - - 283,781

26,928,343 31,552,531 4,807,106 304,309 63,592,289

Liabilities

Deposits from banks

and other financial institutions 335,448 649,984 211,681 3,302 1,200,415

Customers' and related parties

deposits and other credit balances 24,266,407 27,142,009 4,383,493 235,399 56,027,308

Cash margins 840,570 323,696 60,992 5,904 1,231,162

Liability under acceptances 65,128 826,128 122,882 44,106 1,058,244

Other liabilities 628,250 24,171 18,627 24 671,072

26,135,803 28,965,988 4,797,675 288,735 60,188,201

Net Assets 792,540 2,586,543 9,431 15,574 3,404,088

45

December 31, 2006 Other Syrian US Dollars Euro Currencies Pounds C/V SYP C/V SYP C/V SYP Total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000

Assets

Cash, compulsory reserve

and Central Bank 12,285,669 1,293,863 281,861 16,438 13,877,831

Deposits from banks 1,636,260 23,382,226 2,534,724 128,450 27,681,660

Securities:

Available for sale 50,000 - - - 50,000

Held to maturity - - - - -

Loans and advances 5,964,321 426,145 35,000 65 6,425,531

Customers’ liability under acceptances 92,886 393,668 65,000 61,070 612,624

Other assets 10,032 76 302 - 10,410

Property and equipment 698,950 - - - 698,950

Intangible assets 91,819 - - - 91,819

Regulatory blocked fund 115,790 178,480 - - 294,270

20,945,727 25,674,458 2,916,887 206,023 49,743,095

Liabilities

Deposits from banks

and other financial institutions 272,362 283,134 14,137 - 569,633

Customers' and related parties

deposits and other credit balances 18,340,379 22,671,501 2,818,155 126,667 43,956,702

Cash margins 376,868 319,067 26,687 7,368 729,990

Liability under acceptances 92,886 393,668 65,000 61,070 612,624

Other liabilities 509,928 40,810 2,767 50 553,555

19,592,423 23,708,180 2,926,746 195,155 46,422,504

Net Assets 1,353,304 1,966,278 ( 9,859) 10868 3,320,591

46

DISTRIBUTION OF ASSETS AND LIABILITIES BY INTEREST MATURITY

Accounts in Syrian pounds: December 31, 2007 Non Floating interest Fixed interest interest Up to 3 Up to 3 3 to 12 1 to 3 More than Final bearing months Total months months years 3 years Total total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank 11,803,634 - - - - - - - 11,803,634 Deposits with banks 164,996 - - - 800,000 300,000 - 1,100,000 1,264,996 Securities: Available for sale 50,000 - - - - - - - 50,000 Held to maturity - - - - - - - - - Loans and advances ( 726,764) 7,632,866 7,632,866 - 2,877,355 2,687,933 273,907 5,839,195 12,745,297 Customers’ liability under acceptances 65,128 - - - - - - - 65,128 Other assets 26,020 - - - - - - - 26,020 Fixed assets 771,111 - - - - - - - 771,111 Intangible assets 86,367 - - - - - - - 86,367 Regulatory blocked fund 115,790 - - - - - - - 115,790 Total assets 12,356,282 7,632,866 7,632,866 - 3,677,355 2,987,933 273,907 6,939,195 26,928,343 Liabilities Deposits from banks and other financial institutions 335,448 - - - - - - - 335,448 Customers' and related parties deposits and other credit balances 182,508 21,522,399 21,522,399 - 2,555,470 6,030 - 2,561,500 24,266,407 Cash margins 840,570 - - - - - - - 840,570 Liability under acceptances 65,128 - - - - - - - 65,128 Other liabilities 628,250 - - - - - - - 628,250 Total liabilities 2,051,904 21,522,399 21,522,399 - 2,555,470 6,030 - 2,561,500 26,135,803 Net assets 10,304,378 ( 13,889,533) ( 13,889,533) - 1,121,885 2,981,903 273,907 4,377,695 792,540

47

Accounts in foreign currencies reflected in Syrian pound equivalent: December 31, 2007 Non Floating interest Fixed interest interest Up to 3 Up to 3 3 to 12 1 to 3 More than Final bearing months Total months months years 3 years Total total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank of Syria 1,995,893 - - - - - - - 1,995,893 Deposits with banks 192,008 - - 30,141,565 1,586,992 477,917 - 32,206,474 32,398,482 Securities: Available for sale - - - - - - - - - Held to maturity 3,698 474,058 474,058 - - - - - 477,756 Loans and Advances ( 674) 620,484 620,484 - 7,355 - - 7,355 627,165 Customers’ liability under acceptances 993,116 - - - - - - - 993,116 Other assets 3,543 - - - - - - - 3,543 Fixed assets - - - - - - - - - Intangible assets - - - - - - - - - Regulatory blocked fund 167,991 - - - - - - - 167,991 Total assets 3,355,575 1,094,542 1,094,542 30,141,565 1,594,347 477,917 - 32,213,829 36,663,946 Liabilities Deposits from banks and other financial institutions 501 - - 864,466 - - - 864,466 864,967 Customers' and related parties deposits and other credit balances 98,676 30,106,643 30,106,643 - 1,541,106 14,476 - 1,555,582 31,760,901 Cash margins 390,592 - - - - - - - 390,592 Liability under acceptances 993,116 - - - - - - - 993,116 Other liabilities 42,822 - - - - - - - 42,822 Total liabilities 1,525,707 30,106,643 30,106,643 864,466 1,541,106 14,476 - 2,420,048 34,052,398 Net assets 1,829,868 ( 29,012,101) ( 29,012,101) 29,277,099 53,241 463,441 - 29,793,781 2,611,548

48

Accounts in Syrian pounds: December 31, 2006 Non Floating interest Fixed interest interest Up to 3 Up to 3 3 to 12 1 to 3 More than Final bearing months Total months months years 3 years Total total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank of Syria 12,285,669 - - - - - - - 12,285,669 Deposits with banks 45,114 - - 591,146 - 500,000 500,000 1,591,146 1,636,260 Securities: Available for sale 50,000 - - - - - - - 50,000 Held to maturity - - - - - - - - - Loans and advances ( 186,533) 4,019,952 4,019,952 - 1,480,381 633,050 17,471 2,130,902 5,964,321 Customers’ liability under acceptances 92,886 - - - - - - - 92,886 Other assets 10,032 - - - - - - - 10,032 Fixed assets 698,950 - - - - - - - 698,950 Intangible assets 91,819 - - - - - - - 91,819 Regulatory blocked fund 115,790 - - - - - - - 115,790 Total assets 13,203,727 4,019,952 4,019,952 591,146 1,480,381 1,133,050 517,471 3,722,048 20,945,727 Liabilities Deposits from banks and other financial institutions 96,722 - - 50,640 125,000 - - 175,640 272,362 Customers' and related parties deposits and other credit balances 122,712 14,586,335 14,586,335 - 3,627,770 3,562 - 3,631,332 18,340,379 Cash margins 376,868 - - - - - - - 376,868 Liability under acceptances 92,886 - - - - - - - 92,886 Other liabilities 509,928 - - - - - - - 509,928 Total liabilities 1,199,116 14,586,335 14,586,335 50,640 3,752,770 3,562 - 3,806,972 19,592,423 Net assets 12,004,611 ( 10,566,383) ( 10,566,383) 540,506 ( 2,272,389) 1,129,488 517,471 ( 84,924) 1,353,304

49

Accounts in foreign currencies reflected in Syrian pound equivalent: December 31, 2006 Non Floating interest Fixed interest interest Up to 3 Up to 3 3 to 12 1 to 3 More than Final bearing months Total months months years 3 years Total total SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 SYP’000 Assets Cash, compulsory reserve and Central Bank 1,581,362 - - 10,800 - - - 10,800 1,592,162 Deposits with banks 581,292 - - 24,449,563 1,014,545 - - 25,464,108 26,045,400 Securities: Available for sale - - - - - - - - - Held to maturity - - - - - - - - - Loans and advances ( 721) - - 448,232 13,699 - - 461,931 461,210 Customers’ liability under acceptance 519,738 - - - - - - - 519,738 Other assets 378 - - - - - - - 378 Fixed assets - - - - - - - - - Intangible assets - - - - - - - - - Regulatory blocked fund 178,480 - - - - - - - 178,480 Total assets 2,860,528 - - 24,908,595 1,028,244 - - 25,936,839 28,797,368 Liabilities Deposits from banks and other financial institutions 233,175 - - - 64,096 - - 64,096 297,271 Customers' and related parties deposits and other credit balances 77,124 - - 24,071,089 1,466,228 1,882 - 25,539,199 25,616,323 Cash margins 353,122 - - - - - - - 353,122 Liability under acceptances 519,738 - - - - - - - 519,738 Other liabilities 43,627 - - - - - - - 43,627 Total liabilities 1,226,786 - - 24,071,089 1,530,324 1,882 - 25,603,295 26,830,081 Net assets 1,633,743 - - 837,506 ( 502,080) ( 1,882) - 333,544 1,967,287

50