Embed Size (px)

Citation preview

Bank of America SecuritiesBank of America SecuritiesEnergy ConferenceEnergy Conference

November 14, 2008

Presenter:Denny SmithDirector, Corporate Development

Page 2

Forward Looking StatementWe often discuss expectations regarding our markets, demand for our products and services, and our future performance in our annual and quarterly reports, press releases, and other written and oral statements. Such statements, including statements in this document incorporated by reference that relate to matters that are not historical facts are “forward-looking statements” within the meaning of the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These “forward-looking statements” are based on our analysis of currently available competitive, financial and economic data and our operating plans. They are inherently uncertain and investors must recognize that events and actual results could turn out to be significantly different from our expectations.

You should consider the following key factors when evaluating these forward-looking statements:

• fluctuations in worldwide prices and demand for natural gas and oil;• fluctuations in levels of natural gas and crude oil exploration and development activities;• fluctuations in the demand for our services;• the existence of competitors, technological changes and developments in the oilfield services industry;• the existence of operating risks inherent in the oilfield services industry;• the existence of regulatory and legislative uncertainties;• the possibility of changes in tax laws;• the possibility of political instability, war or acts of terrorism in any of the countries in which we do business and;• general economic conditions.

Our businesses depend, to a large degree, on the level of spending by oil and gas companies for exploration, development and production activities. Therefore, a sustained increase or decrease in the price of natural gas or oil, which could have a material impact on exploration and production activities, could also materially affect our financial position, results of operations and cash flows.

The above description of risks and uncertainties is by no means all inclusive, but is designed to highlight what we believe are important factors to consider.

Page 3

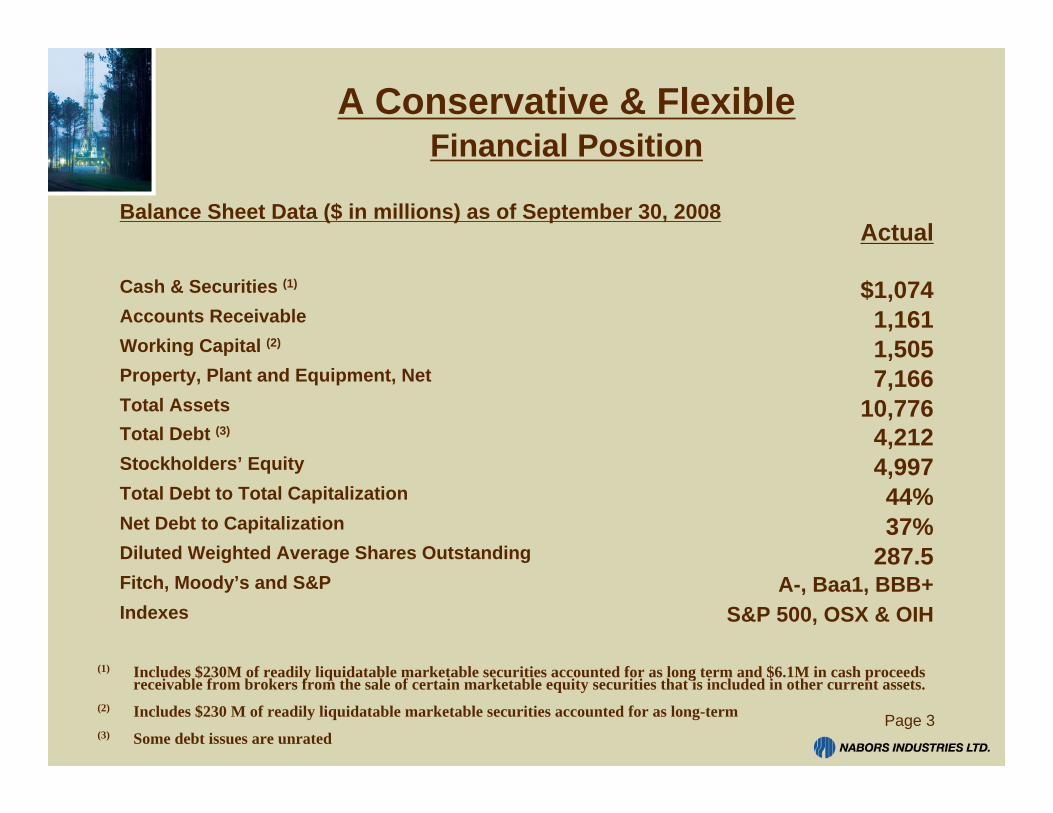

A Conservative & Flexible Financial Position

Balance Sheet Data ($ in millions) as of September 30, 2008

287.537%44%

4,9974,212

10,7767,1661,5051,161

$1,074

Actual

S&P 500, OSX & OIHA-, Baa1, BBB+

Stockholders’ Equity

IndexesFitch, Moody’s and S&PDiluted Weighted Average Shares OutstandingNet Debt to CapitalizationTotal Debt to Total Capitalization

Total Debt (3)

Total AssetsProperty, Plant and Equipment, NetWorking Capital (2)

Accounts ReceivableCash & Securities (1)

(1) Includes $230M of readily liquidatable marketable securities accounted for as long term and $6.1M in cash proceeds receivable from brokers from the sale of certain marketable equity securities that is included in other current assets.

(2) Includes $230 M of readily liquidatable marketable securities accounted for as long-term(3) Some debt issues are unrated

Page 4

Globally Positioned Portfolio of High-End Assets

13 JACK-UPS> 8 Drilling> 5 Workover

3 BARGE RIGS 37 PLATFORM RIGS> 23 Workover/Re-Drilling> 14 Drilling

700 LAND WORKOVER RIGS 525 LAND DRILLING RIGS

Actively Marketed Rigs OnlyAs of September 30, 2008

DRILLINGINSTRUMENTATION

TOP DRIVEMANUFACTURING

OILFIELDSERVICES

Page 5

Global Working Rig Fleet Status

566142424

394.521.561

53162367

2005Avg.

53987452

45823104

311827212

Current

443753Canada

535505581Total W.O./Well Servicing90114147Canada445391434US Lower 48

W.O./Well Servicing

466407431Total Drilling232120Int’l Offshore (1)1039579Int’l Land (1)

International

181616GOM Offshore267229255US 48 Drilling1198Alaska

North America

4Q08Expected

2007Actual

2006Avg.Drilling

As of November 7, 2008

Page 6

Current Environment

> North America Drilling (U.S. Lower 48)• Rig count still near all-time high of 273 but expected to fall off December through April.• 81 new rigs currently operating and setting performance records.• 32 new rig commitments scheduled to deploy 3Q08 - 3Q09 at margins 2x current average

for legacy rigs.• Expect much higher resiliency than 2006 - 2007 market.

> North America Drilling (Canada)• Secured 2 new build commitments.• 4-6 more probable.• Slower Alberta activity substantially offset by Saskatchewan (Bakken) and British Colombia

Shales (Horn River & Montney).• Market softening overall – Nabors expects year over year to be flat to down slightly.

> International• Rig count and margins still improving.• Expanding operations into two new areas (Romania & Kuwait).• Bid prospects still strong – some areas slowing.• 2009 EBIT expected to be +$100 million over 2008.

Page 7

Current Environment

> U.S. Offshore:• 3Q08 Strong pricing & activity: margins over $20k per rig day and four

additional rigs working since 2Q08.• Two new MODS platform rigs in process for term commitments.• Barge 100 damaged in Hurricane Gustav.• Market still strong but vulnerable to slowing in jack-ups and barges.

> Alaska:• Increasing demand driven by accelerated recovery effort in existing fields, new

field development & strong exploration.• 2 new rigs deployed plus 1 under construction.• 3 existing rigs undergoing upgrades for long-term contracts.• Some deferral of projects possible.

> Other Segments:• Increasing financial significance with strong growth in Canrig, EPOCH and

Ryan, potential increase of 60% 2007 over 2008.• Increasing, but seasonal/volatile, activity and pricing in Alaska JVs.

Page 8

Upside Drivers/Downside Mitigators

> Higher overall resiliency to market down turns

> New rig additions:•190 new rigs globally by mid 2010

•Increased weighting to higher margin rigs

– U.S. Lower 48 land, International, Alaska and US Offshore

> International growth

> Alaska growth

> Oil & Gas growth

> Other segments growth

Page 9

Largest Global New Rig Additions New Build Commitments (2005-2009)

Significant Further Potential

190121213162Total

1697Canada

312Alaska

431**1140International

13112US Offshore

1152*113US Lower 48

TotalPlatformJack-UpBargeRigs

Coil TubingDrilling

OffshoreLand

Includes new build commitments still to be deployed

*Note: Includes one rig working for Nabors Well Services

**Note: Platform-type rig mounted inside drillship

Page 10

Nabors USA Initiatives Critical to Record Rig Count

> Continue to Design Custom Rig Solutions for Today’s Drilling Challenges

> 2005 New Build Program• PACE M Series• PACE F Series• Canadian PACE• SuperSundowner

> 2008 New Build Program• Updated PACE M Series for the Haynesville and Woodford Shales,

Piceance Basin and California• New PACE 1500 Design for the Haynesville Shale and Oklahoma• New Box-on-Box PACE 1500 Design for the Bakken

Page 11

Nabors USA Rig Fleet TransitionNew Technology Financed Term - Contracts

33%34%33%August 2010

0%53%47%August 2005

ACSCRMechanical

67% of Fleet

Page 12

PACE Rig Fleet GrowthPrimarily Driven by Unconventional Plays

Bakken – 6

Barnett – 14

Piceance/Pinedale – 25

Woodford/Fayetteville – 16

Haynesville/Bossier - 45

106 out of 113 PACE rigs working in Shale developments

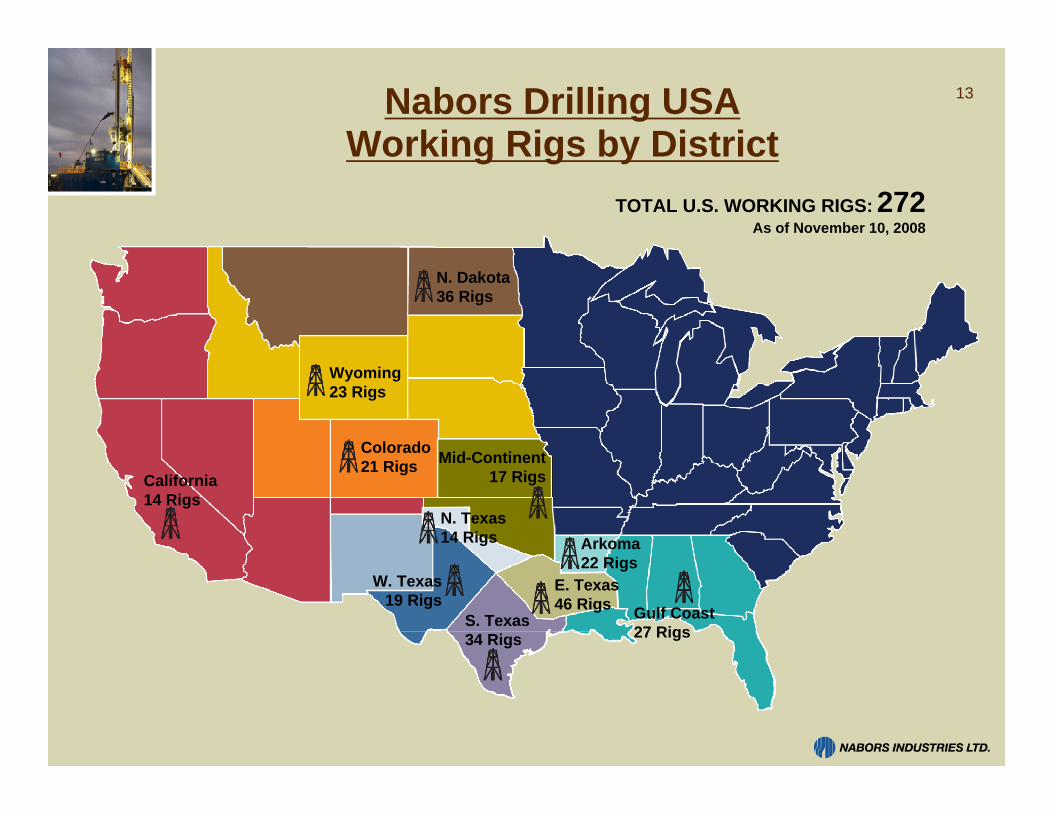

13Nabors Drilling USAWorking Rigs by District

California14 Rigs

Wyoming23 Rigs

S. Texas34 Rigs

N. Texas14 Rigs

W. Texas19 Rigs

E. Texas46 Rigs

N. Dakota36 Rigs

Colorado21 Rigs

Gulf Coast27 Rigs

Mid-Continent17 Rigs

Arkoma22 Rigs

TOTAL U.S. WORKING RIGS: 272As of November 10, 2008

Page 14

Record Breaking Well - Anadarko Carthage, TX

Page 15

Piceance Basin Nabors SSD 573 vs. ‘06 Conventional Rig Average

Page 16

NBR PACE 101 – 1,000 HPRecord Breaking Well – Wamsutter June 08

> Nabors Rig 101eclipsed both the previous directional & vertical records for all operators in the field

> Previous best well stood since March 2005

-87%2.10%16.30%Well Non Productive Time %

-61%6.416.35Well Cycle Time (days)-59%4.410.73Days to 10k feet

Change

Nabors PACERig 101

Record Well2007 Field

Average

Page 17

Increasing Rig Demand and SophisticationLimited Production Response with Higher Decline Rates

Page 18

US Lower 48 Land MarginsVolatile But Steadily Increasing

As of October 2008

Page 19

U.S. Lower 48 Land DrillingTerm Contracts in Force at September 30, 2008 (1)

EBIT - $Millions $320$360$540

FY2010FY20094Q08

Annualized

# of rigs subject to term contracts 637996120155173

4Q093Q092Q091Q094Q083Q08

(1) Represents the minimum number of contracts in force with no incremental contract awards in the future.

Page 20

International Margins & Rig CountThree-fold Increase in Seven Years & Inflecting Upwards

21

International Market Share Growth

20

40

60

80

100

120

140

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

0%

2%

4%

6%

8%

10%

12%

14%

NDIL Rig YearsNabors Market Share

Page 22

Nabors Drilling International Elements of Upside Potential

+/- $100 Million+/- $90 Million$123 MillionY/Y increase in EBIT

-15%-37%-12%Cost & Utilization % Changes

31%65%44%Contract Renewals

56%23%24%Prior Year Start-Ups

28%49%44%New Rig Start-ups

Consensus Implied

2008 – 2009 Consensus Implied

2007 – 2008 Actual

2006 – 2007

Sources of year-over-year incremental % change in EBIT

Page 23

Strong International Bid FlowRecent and Prospective Rig Inquiries

107 +/-15Africa & Far East10North Africa6Mexico27Middle East27Russia & FSU22South America

As of September 2008 - Number of

RigsRegion

Note: Bids pending, working & expected including renewals, extensions and incremental requirements

Page 24

*Subsidiary operating income from continuing operations before corporate expenses & inter-company consolidation

High Growth Visibility –Internationally and Alaska

Actual and Implied Operating Income Distribution

25High Growth Visibility2001–2009 Operating Income

Subsidiary operating income from continuing operations before corporate expenses and inter-company consolidation (000’s)

$3.10 $2.70

Page 26

AUXILIARYINFORMATION

Page 27

Margins and Activities

(1)Margin = gross margin per rig per day for the period. Gross margin is computed by subtracting direct costs from operating revenues for the period.

37.08,27816.97,27835.87,644Canada

Rig HrsRev/HrRig HrsRev/HrRig HrsRev/HrWell Servicing

Rig YrsMargin (1)Rig YrsMargin (1)Rig YrsMargin (1)

72,593$70240,257$70367,141$675Canada

274,084$460272,101$455290,680$473US Lower 48

117.912,860121.514,757121.315,989International

8.413,52810.421,55211.017,787Alaska

14.415,72817.120,18519.218,124US Offshore

221.6$8,852242.3$8,891263.3$10,065US Lower 48

3Q 072Q 083Q 08

Page 28

Quarterly Adjusted IncomeDerived from Operating Activities

42,29131,46842,433Nabors Well Services

16,920(14,326)13,396Canada

88,574101,752111,048International

4,21413,46610,159Alaska

9,24517,98318,456US Offshore

$130,761$134,322$176,819US Lower 48

3Q 072Q 083Q 08($000’s)

Page 29

Non-GAAP Financial Information

Within the preceding slides in this presentation, we present, both historically and on a forward-looking basis, our adjusted income (loss) derived from operating activities, which is a “non-GAAP” financial measure under Regulation G. The components of adjusted income derived from operating activities are computed using amounts which are determined in accordance with accounting principles generally accepted in the United States of America (GAAP). Adjusted income derived from operating activities is computed by: subtracting direct costs, general and administrative expenses, and depreciation and amortization, and depletion expense from Operating revenues and then adding Earnings from unconsolidated affiliates. Such amounts should not be used as a substitute to those amounts reported under GAAP. However, management evaluates the performance of our business units and the consolidated company based on several criteria, including adjusted income (loss) derived from operating activities, because it believes that this financial measure is an accurate reflection of the ongoing profitability of our company. We have provided within the table presented below a reconciliation for the applicable historical and forward-looking periods of adjusted income derived from operating activities to income before income taxes, which is its nearest comparable GAAP financial measure.

Page 30

Non-GAAP Financial Information (continued)

The following table provides a reconciliation of adjusted income derived from continuing operating activities for our reportable segments to income before income taxes for the three months ended September 30, 2008, June 30, 2008 and September 30, 2007, using historical information determined in accordance with GAAP:

(1) Represents the elimination of inter-segment transactions and unallocated corporate expenses.

$215,893$266,132$306,702Income from continuing operations before income taxes

(30,524)(3,158)(10,875)(Losses) gains on sales of long-lived assets, impairment charges and other (expenses) income, net

(27,466)25,057(22,235)Investment income(13,450)(21,676)(25,506)Interest expense287,333265,909365,318Total(32,837)(36,117)(42,945)Other Reconciling items (1)

10,29719,00618,375Other Operating Segments17,868(1,645)17,577Oil & Gas

292,005284,665372,311Subtotal Contract Drilling88,574101,752111,048International16,920(14,326)13,396Canada

4,21413,46610,159Alaska9,24517,98318,456US Offshore

42,29131,46842,433US Land Well-Servicing$130,761$134,322$176,819US Lower 48 Land Drilling

Contract Drilling:Adjusted income derived from continuing operating activities:

September 30, 2007June 30, 2008September 30, 2008(in thousands)

Three Months Ended