Embed Size (px)

Citation preview

1

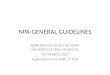

Bank Branch Audit

PLANNING AND DOCUMENTATION

CA. V.K.Viswanathan

B.Sc, F.C.A., DISA (ICA)

BANK AUDIT - CPE SEMINAR

25/03/2017

BANK BRANCH AUDIT

INTEGRATED WORK PAPER FILE

Bank Name

Branch

Year 2016-17

Date of Commencement

Date of Completion

Partner In Charge

File reference

Number of Staff deployed

Advances Value Rs.

Address of the Branch

Name of the Manager

Phone Number

Circle Office Contact

2

INTRODUCTION

A well planned audit will make the entire assignment of bank branch audit more

pleasurable while an ill-planned audit will end in chaos.

Impact of Information Technology Right approach and Techniques For quality audit and completion of audit within a small time span.

1. Objective and Scope of audit:

1.1. We have been appointed as the Statutory Auditors of the ……………………… Branch of

……………………………………….. ……………………………… Bank for the year 2016-17

1.2. The appointment letter dated ………………… has been accepted by us

on……………………………………………. after due communication to the previous year auditor

vide letter dated …………………………………….

1.3. The key terms of reference is to certify the financial statements of the branch as at March 31, 2017

with reference to a True and Fair perspective

1.4. The Branch audit instructions as received from the Head / Circle office have been duly cognised for

in the preparation of this integrated work paper document

1.5. The following key reports / certificates are required to be issued by us

Branch Auditors report

Memorandum of Changes if any

Certified / Attested financial statements

Long Form Audit Report

Schedules and Certificates as per index attached in the next segment

Tax Audit report under Section 44AB of the Income tax Act

1.6. The audit was commenced on ……………. and completed on …………………. By the following

team

1.7. The Key risks in Bank Branch Audits are as under

Misstatement of income, expenses, Assets or Liabilities.

Unrecorded liabilities and contingent liabilities

Asset Classification and NPA provisions not adequate for impaired assets , Asset

Classification and Income Recognition especially for restructured assets

KYC / AML norm compliance related issues

Internal control failures over banking operations including potential / undetected /

detected frauds

Wrong certification

3

1.8. The details of Bank Staff from whom data / records / information and explanations were solicited /

obtained for the purpose of this audit are as under

2. ACCEPTANCE OF APPOINTMENT:

Disqualifications – As per The Companies Act, 2013

The following persons shall not be eligible for appointment as an auditor of a company, namely:-

Sec. 141 (3)(a) - a body corporate other than a limited liability partnership registered under the Limited Liability Partnership Act, 2008;

Sec. 141 (3)(d) (i) – A person or his relative or partner is holding any security of or interest in the company or its subsidiary, or of its holding company or associate company or a subsidiary of such holding company. Provided that the relative may hold security or interest in the company of face value not exceeding Rs. 1 lakh

– See also Rule 10 of Companies (Audit and Auditors) Rules, 2014

Rule 10 of Companies (Audit and Auditors) Rules, 2014

Sub-Rule (1)

For the purpose of proviso to sub-clause (i) of Sec.141 (3) (d), a relative of an auditor may hold securities

in the company of face value not exceeding rupees one lakh: Provided that the condition under this

sub-rule shall, wherever relevant, be also applicable in the case of a company not having share

capital or other securities:

Name Designation Days From To

Partner

Qualified Paid Assistant

Audit Assistant

Articleship trainee

Designation Name Grade

Branch Manager

Loans Officer

Deposit Officer

Other Officers

4

Sec. 141 (3) (d) (ii) – A person or his relative or partner is indebted to the company, or its subsidiary, or its holding or associate company or a subsidiary of such holding company, in excess of Rs.5 lakh - See also Rule 10 of Companies (Audit and Auditors) Rules, 2014

Rule 10 of Companies (Audit and Auditors) Rules, 2014

Sub-Rule (2)

For the purpose of sub-clause (ii) of clause (d) of Sec.141 (3) (d), a person who or whose relative or

partner is indebted. to the company or its subsidiary or its holding or associate company or a subsidiary of

such holding company, in excess of rupees five lakh shall not be eligible for appointment.

Sec. 141 (3)(d) (iii) - A person who or whose relative or partner has given a guarantee or provided any security in connection with the indebtedness of any third person to the company, or its subsidiary, or its holding or associate company or a subsidiary of such holding company, for Rs. 1 lakh – See also Rule 10 of Companies (Audit and Auditors) Rules, 2014

Rule 10 of Companies (Audit and Auditors) Rules, 2014

Sub-Rule (3)

For the purpose of sub-clause (iii) of clause (d) of Sec.141 (3) (d), a person who or whose relative or

partner has given a guarantee or provided any security in connection with the indebtedness of any third

person to the company, or its subsidiary, or its holding or associate company or a subsidiary of such

holding company, in excess of one lakh rupees shall not be eligible for appointment.

Sec. 141 (3)(f) - a person whose relative is a director or is in the employment of the company as

a director or key managerial personnel;

It is suggested to refer Sec. 141of The Companies Act, 2013 to get a first hand

information

about “Eligibility, Qualification and Disqualification of Auditors”

Change in constitution of the firm since application to ICAI If there is any change in constitution inform the bank and wait for confirmation

Acceptance letter and Secrecy and Fidelity letter to Head Office. To send by Registered Post and A/D due. Communication with previous auditor

5

3. REFRESHER COURSE FOR AUDIT TEAM;

RBI circulars - Income Recognition and Provisioning Norms – Master circular on IRAC Norms - Advances Certificates to be issued Account closing instructions – H.O / Z.O Circulars Salient features of LFAR and Tax Audit Audit procedure in a computerised environment.

4. CONDUCT AUDIT IN TWO STAGES:

Pre-closure and post-closure of books

Pre-closure

Review of sanction of large advances, terms and conditions – 5% of Total Advances or Rs. 2 Crore whichever is less

Status of accounts already identified as NPA Stock statements and insurance cover Documentation Generate at the Branch the Reports like Special Watch Accounts or Weekly Alert A/c’s – Status

regarding overdue Compare February 2017 Report with March 2017 Report Problem accounts becoming good or regular Unit visit or inspection Test check of interests received and interest paid Test check of major heads of Income and Expenditure

Post-closure

Account closing statements Certificates Verification of advance accounts closed during the fag end of the year Source of funds for closure

5. DEVELOPMENT OF AN OVERALL AUDIT PLAN:

In developing an overall plan for the audit, the auditor needs to give particular attention to:

- the assessment of materiality

- the assessment of audit risk

- the expected degree of reliance on internal control

- the extent of EDP and EFT systems used by the bank

- the work of internal audit

- the complexity of the transactions undertaken by the bank and the documentation in respect

thereof

6

- the existence of significant areas of audit concern not readily apparent from the bank’s financial

statements

- the existence of related party transactions

- the involvement of other auditors

- management’s representations, and

- the work of supervisors

6. PLANNING ACTIVITY:

Plan the audit by establishing audit strategy commensurate with nature and size of the branch under

audit by:

- Selecting the important areas for the audit

- Audit Materiality and Audit Risk with respect to the size and scale of the branch, To enable

detection of material misstatements.

- Understand the Materiality as per the accounting policy of the bank for different items of income

/ expenditure / asset or liability

- Plan to cover all advances above Rs.2 crore or 5% of outstanding advances of the branch,

preferably a lower limit is desirable

- Orient the team members, by updating them with the extent, scope and changes in the norms

when compared to previous year

- Go through the closing circular as well as the Master Circulars of RBI and the latest issue of

Guidance Note on Audit of Banks issued by the Institute of Chartered Accountants of India,

mark important areas of concern for the branch / branches under audit

- Based on the information received, plan out the audit of financial statements, in respect of the

statement of affairs, audit of incomes, expenditures, or advances with specific reference to /

Potential NPA accounts under Standard Category, verification of restructured accounts vis a vis

their Asset Classification

7

7. Branch Overview

7.1. Key data

7.2. Target Vs Accomplishment

7.3. Advances Overview - top 10 advance categories of the branch

Description 2016-17 2015-16

Rs . lakhs Rs . lakhs

Total Assets

Total liabilities

Total Advances

Total Deposits

Income

Expenditure

Profit / Loss

Description 2016-17 2016-17

Target

Rs . lakhs

Actual

Rs . Lakhs

Total Advances

Total Deposits

Rating of the Branch

S No Category of advances 2016-17 2016-17 2015-16 2015-16

Rs . lakhs No of accts Rs . lakhs No of accts

1 Cash Credit

2 Overdraft

3 Term loans

4 Crop loans

5 Housing loans

6 Jewel loans

7 Other advances

Total Advances

8

7.4. Large Advance Profiling

List of advances greater than Rs 2 Crores or individually accounting for 5% of the total advances whichever is

lower to be covered for detailed checking are as under

7.5. Customer wise advances

Based on our discussions with the branch manager, these advances belong to the same party and are

considered for checking on a collective basis as slippage in one account could result in NPA status for all

accounts

7.6. Advance profiling by value

S No Account reference / name 2016-17 2016-17 2015-16 2015-16

Rs . lakhs No of accts Rs . lakhs No of accts

1

2

3

S No Customer Name Facilities 2016-17

Rs . lakhs

1 1

2

2 1

2

3 1

2

S No Slab - Rs Lakhs outstanding 2016-17 2016-17

Rs . lakhs No of accts

1 < Rs 1 lakh

2 Rs 1 – 5 lakhs

3 Rs 5 – 10 lakhs

4 Rs 10 - 50 lakhs

5 Rs 50 lakhs – Rs 1 Crore

6 Rs 1 to 2 Crores

7 Rs 2 to 5 Crores

8 Rs 5 to 10 Crores

9 > Rs 10 Crores

9

7.7. Deposit profiling

7.8. Restructured advances

The following are the advances restructured by the branch and to be reviewed for compliance with restructuring

terms and conditions as per revised sanctions. Repeated restructured accounts will also be reviewed

7.9. Interest rate and other charges on major advances

Advances Type Interest % Charges % Charges % Charges %

7.10. Interest rate on deposits

Deposit type Days Interest %

7.11. Any frauds reported

Note on frauds reported at the branch in the last few years

S No Category of deposit accounts 2016-17 2016-17 2015-16 2015-16

Rs . lakhs No of accts Rs . lakhs No of accts

1

2

3 Others

Total Deposits

S No Account reference / Name During

2016-17

Upto

2015-16

2016-17

Rs . lakhs Rs. Lakhs Rs . lakhs

1

2

10

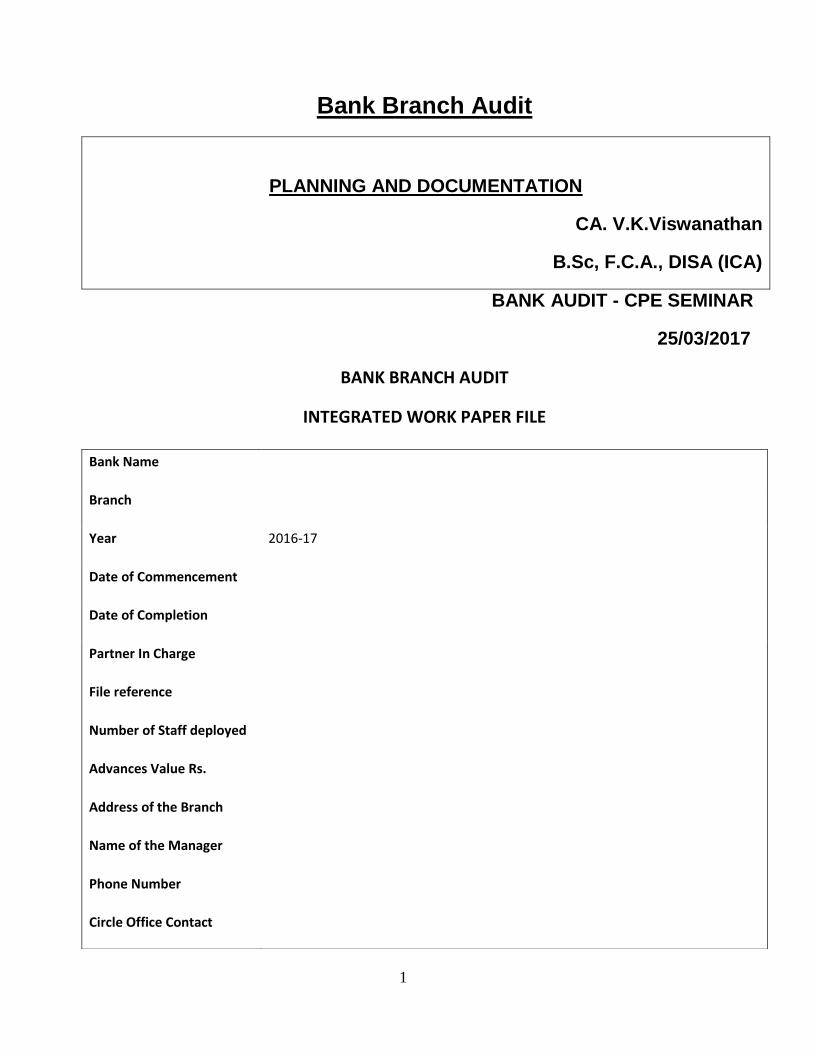

8. Various Internal/Special/Other Audits carried out at Branch,

period covered under audit and status of compliance thereof eg.

RBI Inspection

Concurrent Audit

I.S. Audit

Migration Audit

Stock Audit

Others

Internal Audit Rating assigned:

(Poor/Satisfactory/Good/Excellent)

Risk rating assigned by the internal auditors/I.S.Auditors.

(Low/Medium/High/very High)

9. Review Notes of Concurrent, Risk Based Audit, Inspection Reports

Concurrent Audit

S No Account reference / nature of issue / date of report

Amount Present Status – Rectified, LFAR, MoC, Unadjusted

Impact, if any on audit strategy

Risk Based Internal Audit

S No Account reference / nature of issue / date of report

Amount Present Status – Rectified, LFAR, MoC, Unadjusted

Impact, if any on audit strategy

11

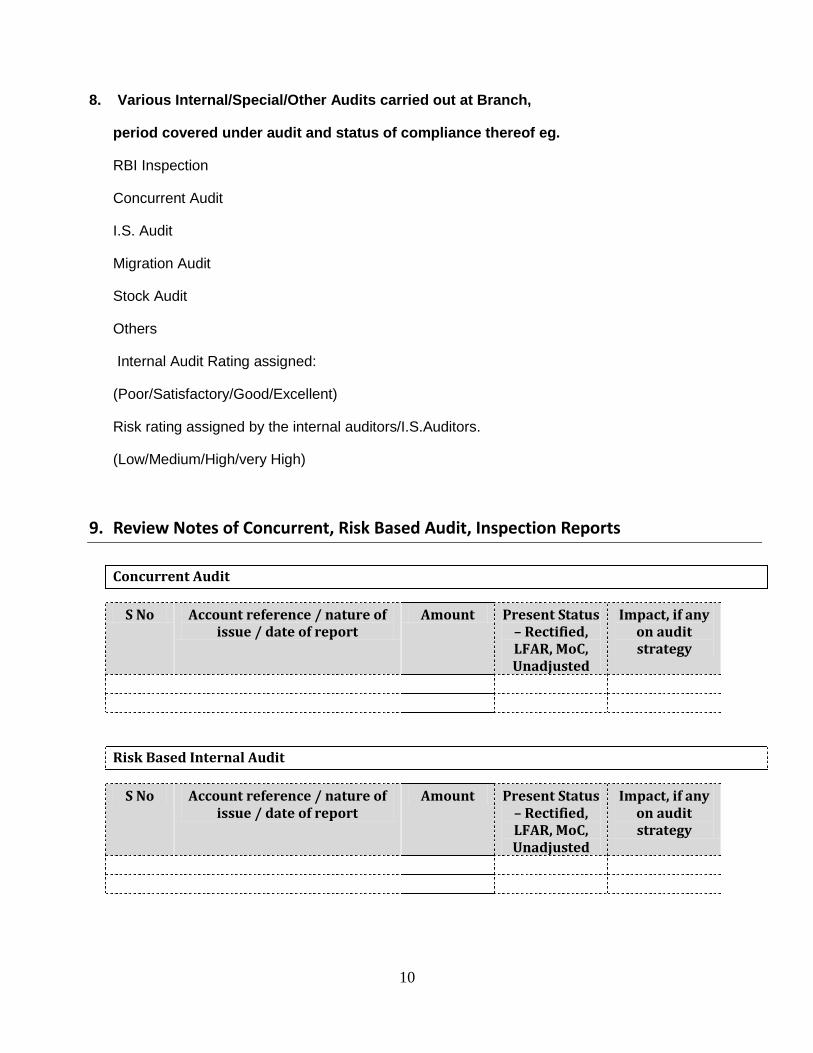

Inspection Reports

S No Account reference / nature of issue / date of report

Amount Present Status – Rectified, LFAR, MoC, Unadjusted

Impact, if any on audit strategy

Previous Year LFAR / Audit report issues

S No Account reference / nature of issue / date of report

Amount Present Status – Rectified, LFAR, MoC, Unadjusted

Impact, if any on audit strategy

10. Audit Strategy

Based on our high level review of the branch data, loans and deposits CBS files and based on

discussions with the Branch manager the following is proposed as the audit strategy

10.1. Top Down Approach to audit

The audit strategy will envisage a top down approach which involves understanding the Balance Sheet

and P & L and a drill down to perform compliance and substantive procedures at a component /

transaction level

10.2. Utilisation of Other Audit reports

The branch has been covered under Concurrent audits / Risk based internal audits as well as

Inspections. These reports will be reviewed to gain a quick understanding of the control framework and

the efficient functioning at the branch.

10.3. Sample selection

CBS reports will be downloaded converted to excel and samples selected across loan types,

accounting periods, rates , value slabs

10.4. Advances

Understand and appreciate target related pressures and potential impact on misstatements

Top accounts ( Rs 2 Crs / 5% advance ) will be checked 100% to cover all accounts

12

Samples of ….. accounts will be taken across all categories of advances to check sanction,

documentation, income accrual and monitoring controls

Particular attention will be paid to the following accounts based on our review of the Concurrent

/ inspection reports

o ………………..

o ……………….

o ……………….

The following unit visits will be undertaken to perform inspection of books / assets held by

customers

o ………………..

o ……………….

o ……………….

All accounts with irregularities as indicated in CBS ( based on loan balance file ) will be

undertaken for review with bank manager to identify potential NPA cases. The Irregular loan

balance report will also be reviewed in detail and documented

Sanity checks of advances file will be undertaken for interest rate inconsistencies / sub rate / off

standard rates for the particular categories

Interest and processing charge accruals will be test checked for 10 random months across ….

Loan files and CCOD files ( periodic / daily interest computation )

Large disbursements close to year / quarter end will be reviewed in detail on a test basis

Clean loans / bullet loans to be reviewed in detail

Special emphasis on restructured advances

10.5. Deposits

Top deposit accounts will be checked to review completeness, adequacy , relevance of

documentation

Large deposits placed at year end will be reviewed in detail

Sanity checks of advances file will be undertaken for interest rate inconsistencies / sub plr / off

standard rates for the particular categories

10.6. Other items

Checklist driven approach guided by key control aspects as stated in the LFAR

13

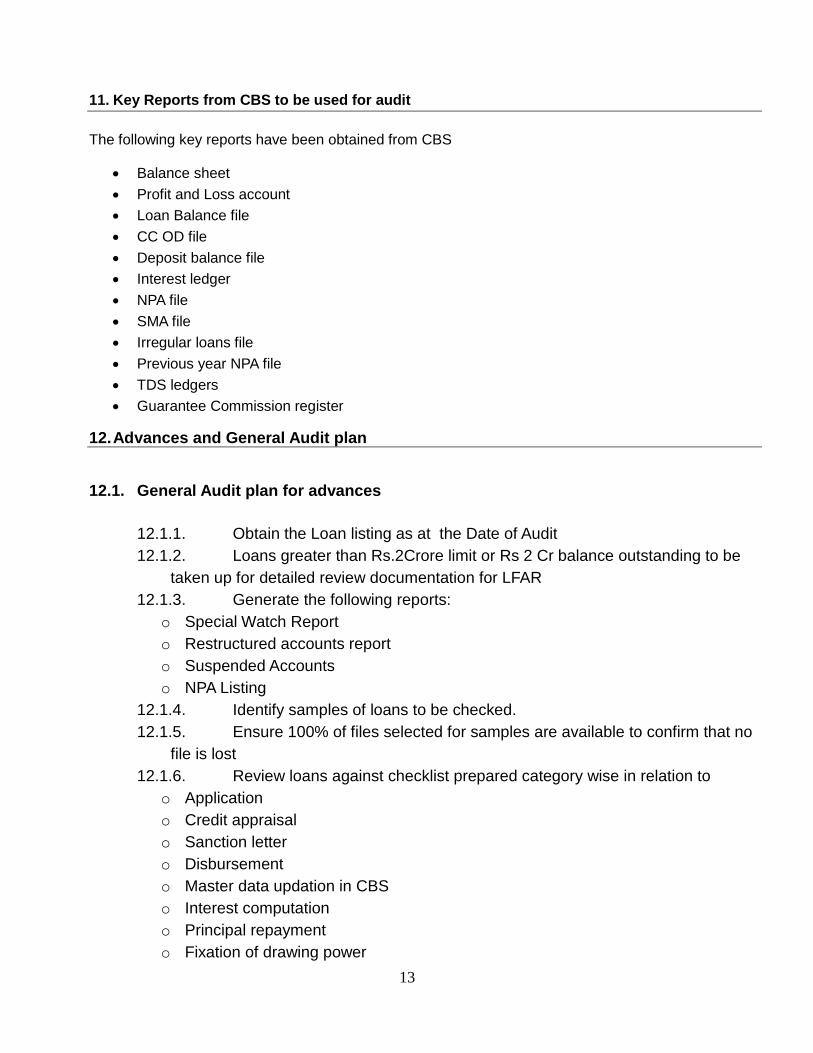

11. Key Reports from CBS to be used for audit

The following key reports have been obtained from CBS

Balance sheet

Profit and Loss account

Loan Balance file

CC OD file

Deposit balance file

Interest ledger

NPA file

SMA file

Irregular loans file

Previous year NPA file

TDS ledgers

Guarantee Commission register

12. Advances and General Audit plan

12.1. General Audit plan for advances

12.1.1. Obtain the Loan listing as at the Date of Audit

12.1.2. Loans greater than Rs.2Crore limit or Rs 2 Cr balance outstanding to be

taken up for detailed review documentation for LFAR

12.1.3. Generate the following reports:

o Special Watch Report

o Restructured accounts report

o Suspended Accounts

o NPA Listing

12.1.4. Identify samples of loans to be checked.

12.1.5. Ensure 100% of files selected for samples are available to confirm that no

file is lost

12.1.6. Review loans against checklist prepared category wise in relation to

o Application

o Credit appraisal

o Sanction letter

o Disbursement

o Master data updation in CBS

o Interest computation

o Principal repayment

o Fixation of drawing power

14

o Verification of securities

o Submission of stock and book debts

o Submission of financial statements

Any other documentation

13. Special Note on Audit of Restructured Advances

13.1. Indicative Checklist

Obtain a general understanding of the type of advance which has been restructured –

project / non project advances, prior to or after Commencement of Commercial

production etc as per the RBI master circular which deals in detail on manner and

mode of treatment of restructured advances

Restructured advances to be reviewed with reference to revised terms of sanction

properly approved by the relevant sanctioning authority

Repeated restructuring to be reviewed for NPA classification

All terms of revised sanction are complied with ( including but not limited to revision in

commercial production, interest rate revision, rescheduling of repayments, additional

security cover, promoters contribution enhancements, escrow requirements etc ). In

case of non-compliance, appropriate reclassifications have been considered

Alteration in the terms & conditions of the sanctioned limits and Alteration in repayment

period.

Alteration in installment amounts – without changing the total repayment period or

ballooning amount of repayments.

For e.g. Qly installments of Rs.5 Lakh may be altered to Rs. 4 Lakh for the first few

years and thereafter be increased to Rs.5.5 Lakh etc..

Alteration in ROI – to benefit the borrower.

Fresh moratorium period

Where unserviced interest has been funded as FITL – Funded Interest Term Loan.

The following accounts cannot be restructured

i) Loss accounts

ii) Fraud accounts

iii) Willful defaulters.

15

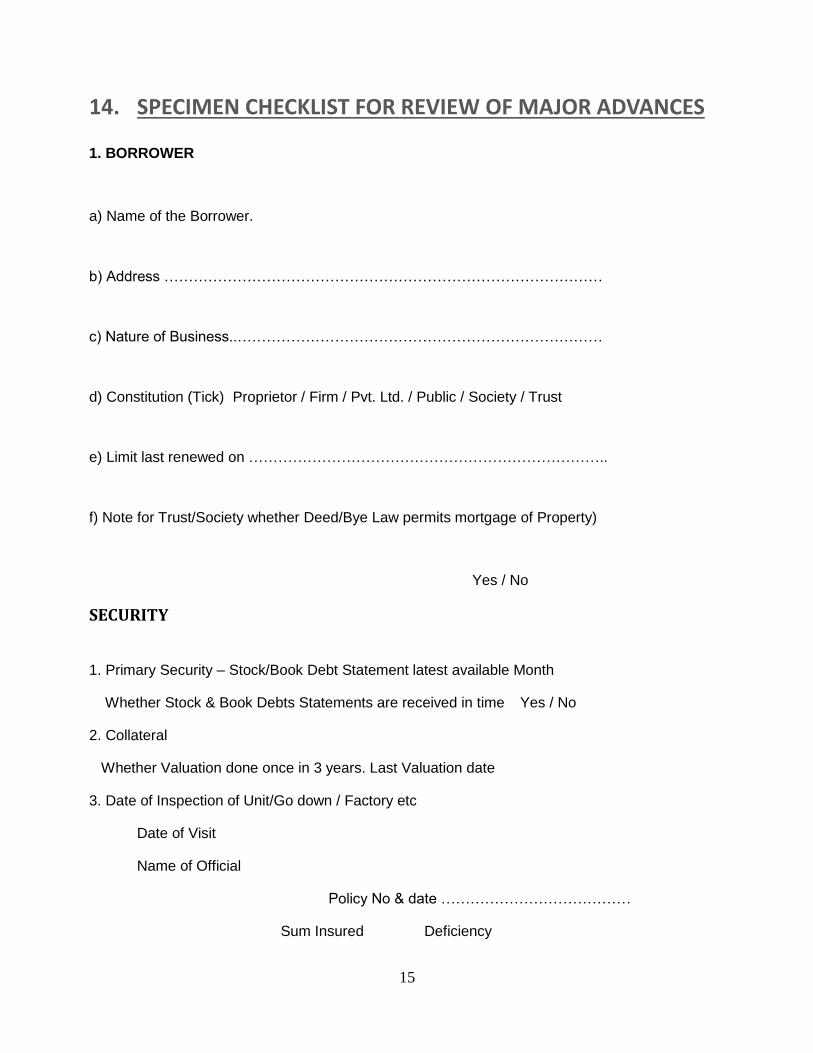

14. SPECIMEN CHECKLIST FOR REVIEW OF MAJOR ADVANCES

1. BORROWER

a) Name of the Borrower.

b) Address ………………………………………………………………………………

c) Nature of Business..…………………………………………………………………

d) Constitution (Tick) Proprietor / Firm / Pvt. Ltd. / Public / Society / Trust

e) Limit last renewed on ………………………………………………………………..

f) Note for Trust/Society whether Deed/Bye Law permits mortgage of Property)

Yes / No

SECURITY

1. Primary Security – Stock/Book Debt Statement latest available Month

Whether Stock & Book Debts Statements are received in time Yes / No

2. Collateral

Whether Valuation done once in 3 years. Last Valuation date

3. Date of Inspection of Unit/Go down / Factory etc

Date of Visit

Name of Official

Policy No & date …………………………………

Sum Insured Deficiency

16

5. Insurance

Rs. In Lakhs ………………. …………..

Expiry Date of Policy...

6. For Term Loan whether assets are properly insured

Value of Stock Sum Insured Deficiency Policy No & Date

Expiry Date of Policy

GENERAL 01.04.2016 31.03.2017

1. Latest Audited accounts available. ……………

2. Whether explanations for any divergent trends noticed and reason obtained?

a) Loss making? Yes/No

b) High Sundry Debtors/High Stocks/ Yes/No

c) Has the borrower advance money to Sister Concerns

(Inter firm advance) Yes/No

If YES is the Advance amount substantial compared to Loan?

3. Whether there is deficiency in document noticed/cited in the RBI/Other Audit Reports

NOTE YOUR COMMENTS AND VIEWS ABOUT THIS ACCOUNT. MARK SEPERATELY ITEMS

THAT SHOULD BE CONSIDERED FOR REPORTING IN LFAR ETC.

Verified by Name and Signature Name and Signature of Partner

17

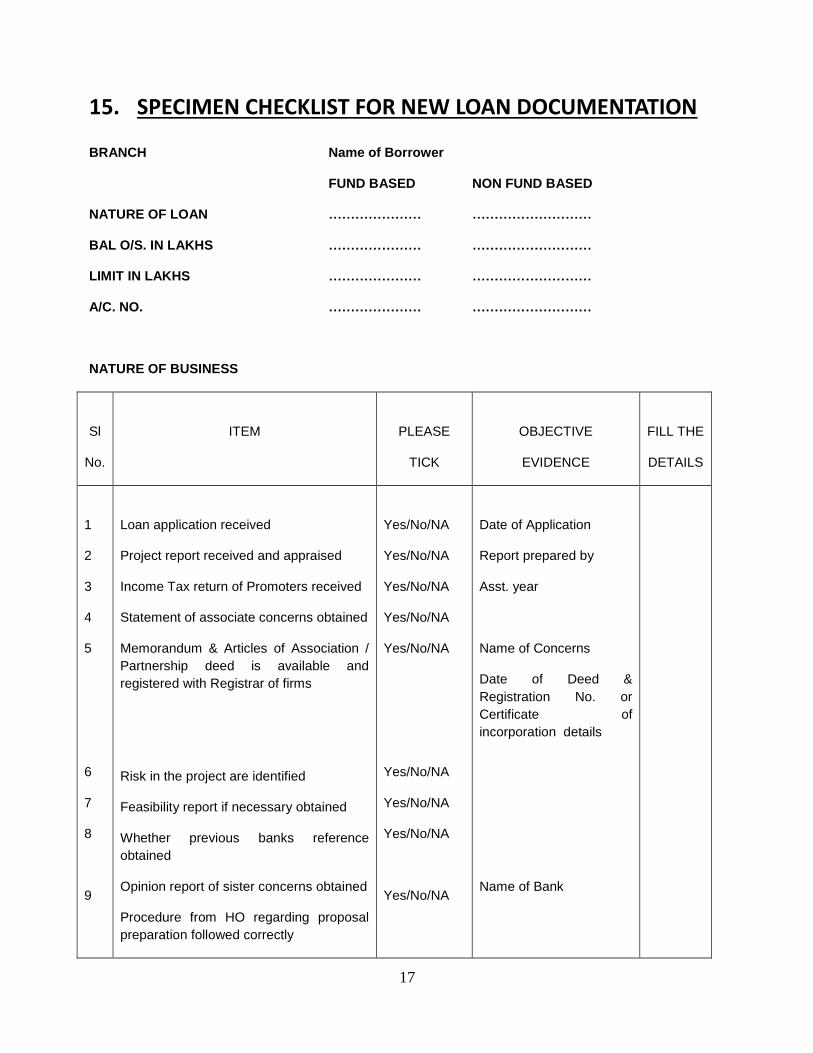

15. SPECIMEN CHECKLIST FOR NEW LOAN DOCUMENTATION

BRANCH Name of Borrower

FUND BASED NON FUND BASED

NATURE OF LOAN ………………… ………………………

BAL O/S. IN LAKHS ………………… ………………………

LIMIT IN LAKHS ………………… ………………………

A/C. NO. ………………… ………………………

NATURE OF BUSINESS

Sl

No.

ITEM

PLEASE

TICK

OBJECTIVE

EVIDENCE

FILL THE

DETAILS

1

2

3

4

5

6

7

8

9

Loan application received

Project report received and appraised

Income Tax return of Promoters received

Statement of associate concerns obtained

Memorandum & Articles of Association /

Partnership deed is available and

registered with Registrar of firms

Risk in the project are identified

Feasibility report if necessary obtained

Whether previous banks reference

obtained

Opinion report of sister concerns obtained

Procedure from HO regarding proposal

preparation followed correctly

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Date of Application

Report prepared by

Asst. year

Name of Concerns

Date of Deed &

Registration No. or

Certificate of

incorporation details

Name of Bank

18

10

11

12

13

14

15

16

17

18

19

20

Whether the power is correctly exercised

for sanction

Facility are disbursed after complying

sanction letter

Sanction letter in file

Promoters contribution is properly made

Mortgage of property proper

Legal opinion valid-Give details

All documents in legal opinion obtained

Copy of IT Acknowledgement obtained

Original of documents for Vehicle loan

obtained

Registration of charges available

Interest rates fed in computer is tallying

with sanction letter

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Yes/No/NA

Date of Sanction &

Authority

Amount brought in

Name of Lawyer &

Opinion date

Date of filling return

Regn. Certificate Date

Date of filling Form No 8

Interest rate in sanction

letter vis a vis computer

Verified by : Name and Signature Name and Signature of Partner

19

16. Check list and questionnaire to be submitted to the Branch before

commencement of audit.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Copy of other Audit Reports, period covered, status of compliance

there

a) Previous year Branch Audit Report

b) RBI Inspection Report,

Concurrent Audit,

I.S. Audit,

Revenue Audit,

Stock Audit,

Migration Audit

Others.

List of Large Advances

Having Limits or Balance outstanding in excess of 5% of the branch

or Rs.2 Crore, whichever is less

List of Advances sanctioned during the year

List of Advances where documentation is still pending

List of Advances where Renewal was due during the year, but not

completed.

List of DPNs to be renewed during the year

List of Rescheduled/Rephased advances

List of BIFR accounts and accounts considered for revival,

rehabilitation

List of accounts closed on one time settlement

List of Advances where stock statements have not been received

regularly.

20

11.

12.

13.

14.

15.

16.

17.

18.

19.

List of cases where valuation report of securities is more than 3

years old.

List of non-corporate entities where aggregate advances is more

than Rs.20 lacs

The accounts where Audit Report as per RBI guidelines have been

obtained.

Have all the credit card dues have been recovered promptly. It not,

the dues as on 31.03.17

DICGC/ECGC claims

a) Claims at the beginning of the year

b) Claims lodged during the year

c) Claims settled

d) Details of sharing of recoveries, in claims settled accounts.

Details of outstanding amount of guarantees invoked and funded by

the branch as at the end of the year

Details of outstanding amounts of letters of credit and co-

acceptances funded by the branch.

Details of outstanding entries in IBIT, if any

Details of outstanding entries in Sundry Assets and Suspense a/c.

Details of outstanding entries in Sundry Deposits.

a) Quantum of overdue/matured term deposits at the end

of the year

b) Details of interest accrued and provided on overdue deposits.

List of major items of contingent liabilities (other than Liabilities

such as guarantees, letters of credit, acceptances, endorsements

etc.) not acknowledged as debt by the branch.

Particulars of fraud, if any, discovered during year and details of

report to H.O. compliant lodged with police etc.

21

20.

21.

22.

23.

24.

25.

PMRY Loans

a) No. of loans sanctioned during the year

b) Details of limits, amount disbursed

c) Subsidy claims

d) Subsidy received

Cash Department

Cash Retention limit

Dates on which cash balance exceeded the limit

Reporting to controlling authorities and approval thereof

Whether any steps have been taken to increase the cash retention

limit, if the frequency of cash balance exceeding the limits is more.

Insurance coverage held by the branch for cash on hand and cash in

transit whether in force.

Cash Remittance Register

Cash outward remittance

Cash inward remittance

Key Movement Register

Joint custody

Exchange of custody between officers of the branch

Cash verification done by

Officers of Other branch of the bank

Does the branch have accounts with RBI, SBI or any other banks

Balance confirmation letter as at the end of the year

BRS if needed.

Does the branch have any investments on behalf of H.O. If yes,

details thereof

List of advances where stock audit, has to be conducted during the

years.

22

26.

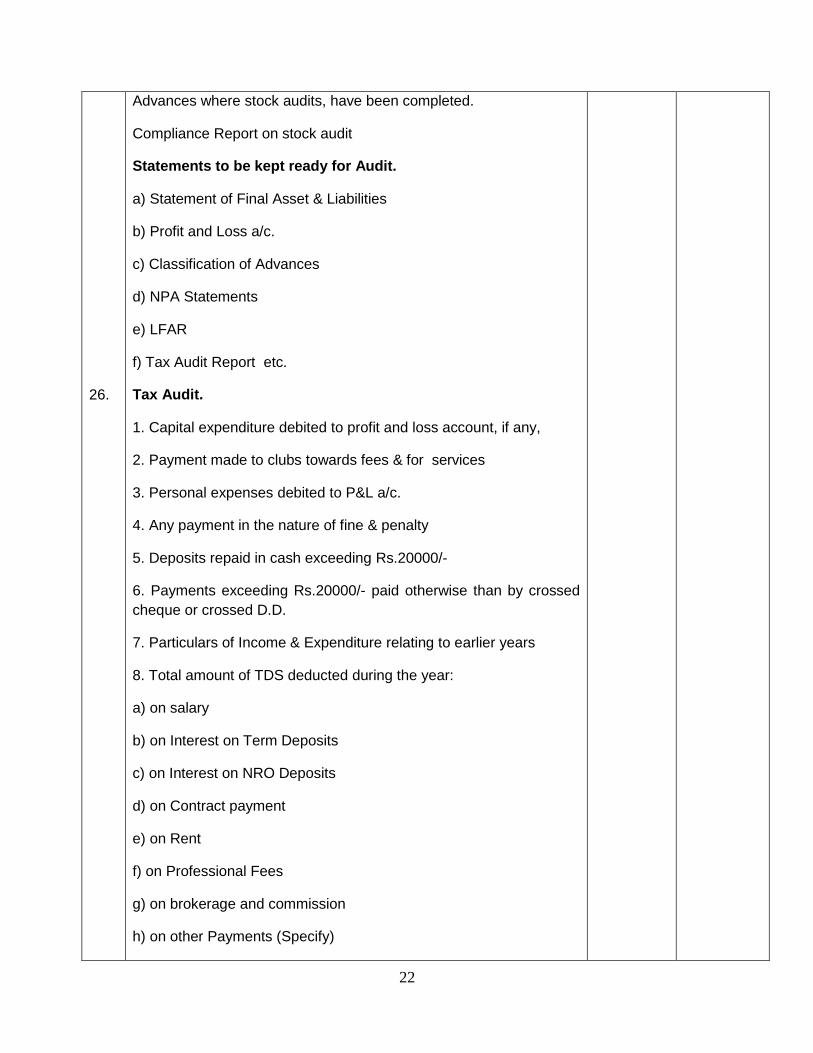

Advances where stock audits, have been completed.

Compliance Report on stock audit

Statements to be kept ready for Audit.

a) Statement of Final Asset & Liabilities

b) Profit and Loss a/c.

c) Classification of Advances

d) NPA Statements

e) LFAR

f) Tax Audit Report etc.

Tax Audit.

1. Capital expenditure debited to profit and loss account, if any,

2. Payment made to clubs towards fees & for services

3. Personal expenses debited to P&L a/c.

4. Any payment in the nature of fine & penalty

5. Deposits repaid in cash exceeding Rs.20000/-

6. Payments exceeding Rs.20000/- paid otherwise than by crossed

cheque or crossed D.D.

7. Particulars of Income & Expenditure relating to earlier years

8. Total amount of TDS deducted during the year:

a) on salary

b) on Interest on Term Deposits

c) on Interest on NRO Deposits

d) on Contract payment

e) on Rent

f) on Professional Fees

g) on brokerage and commission

h) on other Payments (Specify)

23

Signature of the Manager.

Date

17. Exceptional Reports

Major Audit Tools Contains dishonored cheques, large withdrawals, overdrawn accounts etc. Generally contain following details

Debit / credit balance change

Maturity record deleted

Inactive accounts reactivated

Excess allowed over limits

Debits to Income head accounts

Overdue bills and returned

Withdrawals against clearings

Deposits accounts debit balance

Temporary O/D beyond sanctioned limit

Standing instruction failed in day

Irregular term loan accounts with number of arrears of installments

and interest with amounts

Time barred demand promissory notes

Unchecked transactions

Password errors

Debit balance accounts without interest rate

inter-branch transactions with age-wise details

27.

9. Date of filing of TDS Returns (Quarterly)

10. Details of Form 15G & 15H obtained & submission to

Commissioner of Income Tax.

Other Items

a) Amount recovered during the year out of bad debts written off in

earlier years

b) Locker rent arrears – due during the year and remains

unrecovered.

24

18. CHECK LIST FOR VERIFICATION OF ADVANCES

Facility

Name of the Borrower and Account No. A/c. No.

(For various Accounts)

1. Have you checked whether the branch has complied with the requirements such as obtaining loan applications, preparation of proposals, grant / renewal of advances, enhancement of limits etc.

2. Have you checked whether the facility has been granted beyond such delegated powers of the branch?

3. If so, whether the same has been reported to the higher authorities.

4. Have you checked whether the terms of sanction has been complied with?

5. Have you checked whether all the documentation formalities have been complied with before release of facilities by the branch?

6. Have you checked whether in the cases of corporate borrowers due charges have been registered with the Registrar of Companies?

7. Have you verified receipt of stock statements? Have you verified that the follow up action of the branch is adequate?

8. Have you checked whether periodic stock audits have been conducted? Have you perused the latest stock audit report?

9. Have you checked the procedure adopted by the branch for periodically verifying the assets charged to the bank?

10. Have you perused the account to ensure that there are no frequent over drawls, shortfall in the value of security?

11. Have you checked whether the assets charged to the branch have been adequately insured?

12. Has the account been classified as per IRAC norms?

13. If not, have you made out a detailed working for proposing MOC?

14. Has the branch furnished the relevant information required for the purpose of reporting in LFAR?

15. Have you checked whether the branch has obtained valuation reports?

16. Have you verified whether there is any compromise

proposals/write offs in this account?

25

19. TREATMENT OF ASSETS FALLING UNDER CLASSIFICATION OF RESTRUCTURING

The classification of a Restructured account depends on the following guidelines:

a) Restructuring done before commencement of commercial production

b) Restructuring done after commencement of commercial production but before the asset

has been classified as sub-standard

c) Restructuring done after commencement of commercial production and after the asset

has been classified as sub-standard

Rescheduling of Principal alone Rescheduling of Interest

Before commencement of production Account will continue as

Standard Asset provided the

loan/credit facility is fully secured

Account will continue as Standard Asset

subject to the condition that the amount

of sacrifice, if any in the element of

interest, measured in present value

terms, is either written off or provision is

made to the extent of the sacrifice

involved.

After commencement of commercial

production but before the asset has

become sub-standard

Do - Do -

After commencement of commercial

production and after the asset has

become sub-standard

Account will continue in the sub-

standard category for specified

period of one year provided the

loan/credit facility is fully secured

Account will continue in the sub-standard

category for specified period of one year

subject to the condition that the amount

of sacrifice, if any, in the element of

interest, measured in present value

terms, is either written off or provision is

made to the extent of the sacrifice

involved

20. WHETHER NPA AND PRUDENTIAL NORMS ARE APPLICABLE TO ALL STAFF

ACCOUNTS

the respective due dates and interest can be continued to be recognized in spite of non-recovery The answer is in

the affirmative. There is no specific exemption given to the staff accounts regarding classification as Non

performing Asset.

However, in the case of housing loan or similar advances granted to staff members where interest is payable after

recovery of entire principal, interest need to be considered as overdue from the first month onwards. Such

loans/advances should be classified as NPA only when there is a default in repayment of installment of principal

or payment of interest on.

26

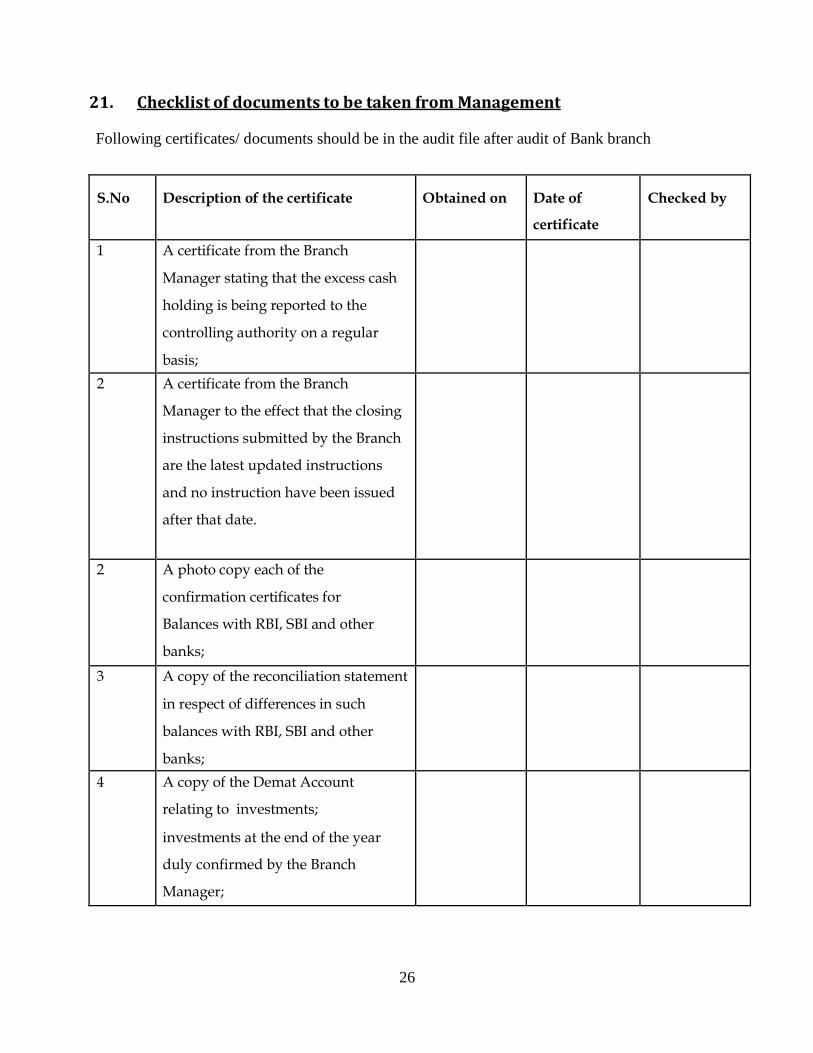

21. Checklist of documents to be taken from Management Following certificates/ documents should be in the audit file after audit of Bank branch

S.No

Description of the certificate

Obtained on

Date of

certificate

Checked by

1 A certificate from the Branch

Manager stating that the excess cash

holding is being reported to the

controlling authority on a regular

basis;

2 A certificate from the Branch

Manager to the effect that the closing

instructions submitted by the Branch

are the latest updated instructions

and no instruction have been issued

after that date.

2 A photo copy each of the

confirmation certificates for

Balances with RBI, SBI and other

banks;

3 A copy of the reconciliation statement

in respect of differences in such

balances with RBI, SBI and other

banks;

4 A copy of the Demat Account

relating to investments;

investments at the end of the year

duly confirmed by the Branch

Manager;

5 List of large advances i.e. those in

respect of which the outstanding

amount is in excess of 5% of the

aggregate advances of the Branch or

Rs.2.00 crores whichever is less duly

certified by the Branch Manager;

6 List of renewal proposals pending at

Branch Level at the end of the year

duly

confirmed by the Branch

Manager;

7 A copy of the letter from Head

Office regarding Sanction limit of

the Branch Manager;

8 List of proposals sanctioned during

the year;

9 List of cases where registration of

creation of charge with Registrar

of Companies pending at the

end of the year;

10 List of cases where the prescribed

period of 30 days for registration of

creation of charge is over as at the

end of the year;

28

11 List of cases where search

reports obtained from

professionals for loans

sanctioned to various

companies;

12 List of cases where the Branch has

not obtained acknowledgement of

Debt (AOD)/ Balance Confirmation

letters at the end of the year;

13 List of cases where the Branch has

not obtained stock/book debts

statements at the end of the year;

14 List of cases where the stock audit

is mandatorily required to be

carried out

15 Compliance on Adverse features

noted in stock audit reports and

whether all issues

are closed.

16 A certificate from the Branch

Manager for inspection or physical

verification of securities charged to

the Bank;

29

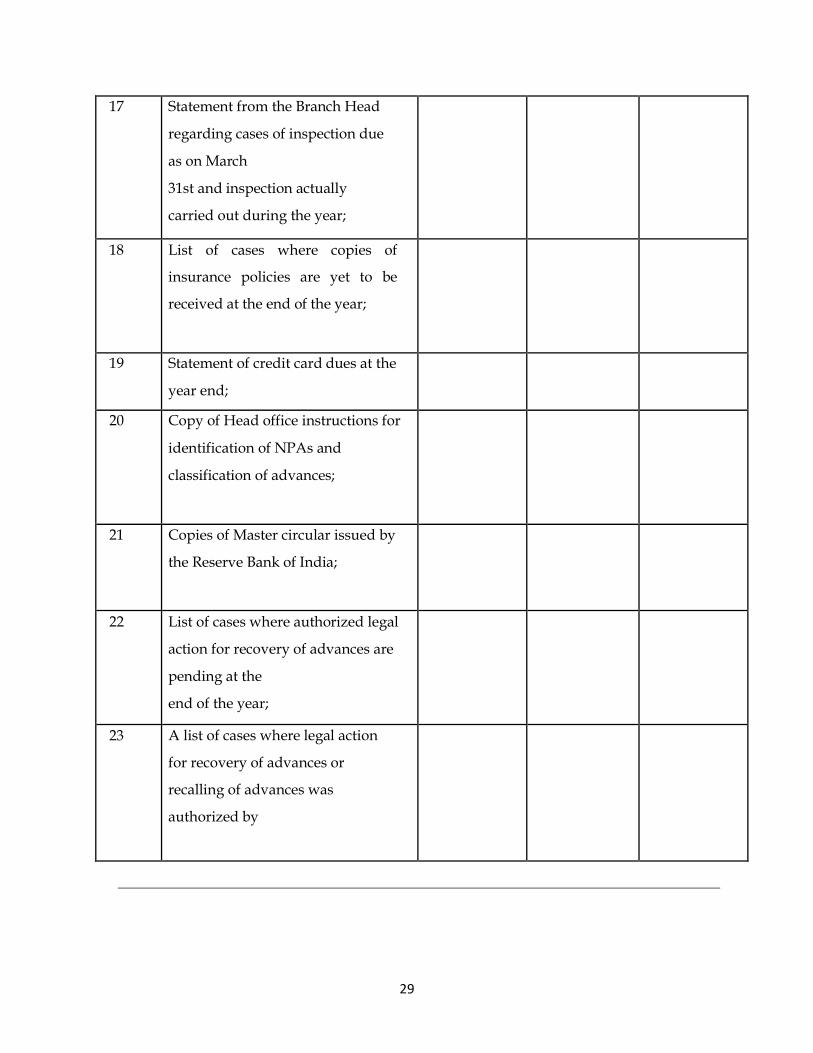

17 Statement from the Branch Head

regarding cases of inspection due

as on March

31st and inspection actually

carried out during the year;

18 List of cases where copies of

insurance policies are yet to be

received at the end of the year;

19 Statement of credit card dues at the

year end;

20 Copy of Head office instructions for

identification of NPAs and

classification of advances;

21 Copies of Master circular issued by

the Reserve Bank of India;

22 List of cases where authorized legal

action for recovery of advances are

pending at the

end of the year;

23 A list of cases where legal action

for recovery of advances or

recalling of advances was

authorized by

30

22. Auditing Review and Other Standards

The work has been planned and performed in accordance with the following Auditing, Review

and Other Standards as prescribed by the Institute of Chartered Accountants of India to the

extent applicable for the engagement

SA reference Description

SA 200 OVERALL OBJECTIVES OF THE INDEPENDENT AUDITOR AND THE CONDUCT OF AN AUDIT IN ACCORDANCE WITH STANDARDS ON AUDITING.

SA210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS.

SA220 QUALITY CONTROL FOR AN AUDIT OF FINANCIAL STATEMENTS.

SA230 AUDIT DOCUMENTATION.

SA240 THE AUDITOR’S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS

.

SA250 CONSIDERATION OF LAWS AND REGULATIONS IN AN AUDIT OF FINANCIAL STATEMENTS.

SA265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT.

SA300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS.

SA315 IDENTIFYING AND ASSESSING THE RISK OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT.

SA320 MATERIALITY IN PLANNING AND PERFORMING AN AUDIT.

SA330 THE AUDITOR’S RESPONSES TO ASSESSED RISKS.

SA402 AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION.

SA450 EVALUATION OF MISSTATEMENTS IDENTIFIED DURING THE AUDIT.

SA500 AUDIT EVIDENCE.

SA501 AUDIT EVIDENCE—SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS.

SA530 AUDIT SAMPLING.

SA540 AUDITING ACCOUNTING ESTIMATES, INCLUDING FAIR VALUE ACCOUNTING ESTIMATES, AND RELATED DISCLOSURES.

SA560 SUBSEQUENT EVENTS.

SA580 WRITTEN REPRESENTATIONS.

SA600 USING THE WORK OF ANOTHER AUDITOR.

SA610 USING THE WORK OF INTERNAL AUDITORS.

SA700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS.

SA706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR’S REPORT.

31

23. PEER REVIEW

Once a Practice Unit is selected for Review, its assurance engagement records pertaining to the

Peer Review Period shall be subjected to Review.

The Reviewer is required to adopt a combination of compliance approach and substantive

approach in the Review process.

As per SA 230 Audit Documentation is a record of audit procedures performed, relevant audit

evidence obtained and conclusions reached by the auditor

Audit Documentation assists

The auditor in planning and performing the audit

In supervision and review work

In creating accountability in work

In retaining a record of significant matters for future audits

In enabling the conduct of quality control reviews and inspections in accordance with

SQC-1

Form of Documentation can be in any of the following forms

Paper – working papers

Electronic – System files

Other media

Examples of Audit Documentation

Audit Plan

Audit Programmes

Copies of agreements entered into by the client

Checklists

Analysis done – ratio analysis

Letter of Representation

Correspondence (including e-mails) regarding significant matters

32

Nature, Timing & Extent of Audit Documentation

Identifying the characteristics of the specific items or matters tested

Who performed the audit work and the date such work was completed

Who reviewed the audit work performed and the date and extent of such review

Documentation of ―significant matters‖ discussed with the management and others

(including the nature of the significant matters discussed and when and with whom the

discussions took place) and related significant professional judgements

If there was information about a significant matter which was identified as not being in

concurrence with the auditor’s final conclusion regarding it, the auditor shall document

how the inconsistency was addressed

A pivotal factor in determining the form, content and extent of audit documentation for

significant matters is the extent of ―professional judgement‖ exercised in performing and

reviewing the work

24. Ensure that the following are available in the bank audit file

1) Copy of letter sent to the previous auditors

2) Engagement letter as envisaged by AAS 26

3) Audit plan

4) Audit program

5) Papers and records which would provide the basis for relying on the internal controls

6) The basis for deciding on the ‘sample selection’ for scrutiny

7) All confirmations and certificates wherever necessary

8) In areas where difference of opinion exists, the views of the organization should be obtained in

writing and recorded.

9) Significant ratio and trend analysis

10) Significant audit observations culled out from other audit reports

11) Circulars, notifications and directives from Government / Regulatory Authority etc which have a

bearing on the audit

33

12) Checklists duly filled up, indexed and cross referenced to the working papers

13) Note on resolution of major observations with specific reference to NPA & provisioning

14) Management letter of representation

25. OTHER SALIENT FEATURES

1. Sharing of recoveries made in DI&CGC claim settled accounts Certificate

2. PMRY subside claim certificate 3. Technology Up gradation Fund Scheme – TUF Scheme Interest subsidy certificate

4. Verification of Miscellaneous expenditure accounts. 5. Verification of Miscellaneous Income accounts 6. EPF Turnover commission 7. Interest subvention for Agricultural Loans Certificate 8. Interest subvention for Housing Loan 9. Interest subvention for Education Loan

26. COMPILING THE REPORT

Two Audit Reports One Short Form – Expressing Opinion on the Financial Statements of the branch Other – Long Form Audit Report Ensure that all queries and observation have been discussed with the Branch Manager

and replies obtained Discussion on a daily basis Obtain a Management letter of representation

At the end of audit (before you leave the branch)

Obtain certificate from Branch Manager with regard to persons attended, No of days taken for audit. Receive one set of all statements meant for the auditor. Prepare list of traveling and conveyance expenses

Ensure that permanent and current files are properly prepared and all the papers

pertaining to the audit are serially numbered

34

27. Members are requested to visit Branch web site which contains the

following materials.

i ) List of various laws applicable to the branch

ii) Specimen of No Objection Letter

iii) Specimen Management Representation Letter

iv) Specimen Checklist for Special Considerations in CBS environment

v) Non corporate entities- W. C. limit exceeding Rs 20 lakh-

RBI Audit Report Format

LAST WORDS

IF YOU FAIL TO PLAN, YOU PLAN TO FAIL

------------------------------------------------------------------------------------------------------------

Thank you V.K.V

CA V.K. VISWANATHAN

Off : 0452 – 2628440

Mob: 9443497301, 9626014871

e-mail : [email protected] and [email protected]