Embed Size (px)

Citation preview

COUNTRY REPORT

BangladeshThe full publishing schedule for Country Reports is nowavailable on our web site at http://www.eiu.com/schedule.

3rd quarter 1999

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newsletters toannual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1000Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Jeremy Eagle Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023

This publication is available on the following electronic and other media:

Online databases

FT Profile (UK)Tel: (44.20) 7825 8000

DIALOG (US)Tel: (1.415) 254 7000

LEXIS-NEXIS (US)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.20) 7930 6900

NewsEdge Corporation (US)Tel: (1.718) 229 3000

CD-ROM

The Dialog Corporation (US)SilverPlatter (US)

Microfilm

World Microfilms Publications(UK)Tel: (44.20) 7266 2202

Copyright© 1999 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-431X

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

Bangladesh 1

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Contents

3 Summary

4 Political structure

5 Economic structure

6 Outlook for 1999-2000

9 Review9 The political scene

13 Economic policy16 The economy17 Agriculture19 Energy and power22 Infrastructure and communications23 Money and finance25 Foreign trade and payments26 Aid and development

27 Quarterly indicators and trade data

List of tables

8 Forecast summary15 Fiscal trends, 1995-200016 Gross domestic product by sector17 Investment/GDP ratios18 Growth in agricultural subsectors19 System loss in the power sector22 Gas reserves, July 199923 Biman Bangladesh Airlines: income and losses24 Average stockmarket capitalisation25 Money supply26 Tourism indicators27 Quarterly indicators of economic activity28 Foreign trade

List of figures

7 Current-account balance9 Gross domestic product9 Taka real exchange rate

Bangladesh 3

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Summary

3rd quarter 1999

Outlook for 1999-2000: Political agitation will increase as the oppositionsteps up its campaign. The economy will perform better in the latter half of theforecast period and inflation will fall in 1999, but pressures on the currentaccount will persist. Foreign-exchange reserves will remain stable. Furtherdevaluations of the taka are likely in 1999.

The political scene: The opposition has intensified its anti-governmentmovement. The leader of the Bangladesh National Party , Khaleda Zia, plans tocontinue her programme of road marches. The transshipment of Indian goodsby land routes has been permitted. The deadlines for upazila (local council) andcity corporation polls have been extended again. A crackdown on criminals haspaid dividends, but crime levels have increased. There has been controversyover the purchase of eight MIG-29s from Russia.

Economic policy and the economy: The government claims that theeconomy registered growth of 5.2% in 1998/99. GDP per head has risen.Revenue collection has fallen short of targets and the budget deficit haswidened. Workers of state-owned enterprises have staged a 48-hour strike.

Sectoral trends: According to the government, a bumper boro rice harvestpropelled agricultural growth to 5% in 1998/99. Boro procurement targets havebeen changed. Load-shedding in the energy sector has continued to disrupteveryday life, but the roots of the power crisis have been identified. Expertshave opposed the vertical separation of functions in the sector. An agreementhas been signed with AES for the development of the Meghnaghat plant and adeal on power transmission has been agreed with RPG Transmissions of India.New wells will ultimately increase gas production by 250m cu ft per day.Pressure has mounted to allow gas exports. The commercial operation of theDhaka-Calcutta bus service has begun. A trans-Asian railway has beenproposed. The privatisation of Biman Bangladesh Airlines is planned by nextyear. Sheba Telcom has struck a deal with a Canadian firm.

Money and finance: The taka has been devalued again. The stockmarket hasrisen, reflecting somewhat stronger domestic investor confidence. Allotment-letter trading has been banned by the DSE. The stockmarket watchdog hasencountered difficulties. The money supply has risen.

Foreign trade and payments: Export growth fell to just below 6% in1998/99, but imports rose by 8.5%. The trade deficit widened to $2.24bn.Bangladesh is to participate in ELVIS.

Aid and development: Japan has awarded a $47m grant for themodernisation of the fertiliser plant. The World Bank has approved $33m for afisheries project. Food aid is being provided by the UN.

Editor: Kilbinder DosanjhAll queries: Tel: (44.20) 7830 1007 Fax: (44.20) 7830 1023

Next report: Our next Country Report will be published in November

August 6th 1999

4 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

Political structure

People’s Republic of Bangladesh

Parliamentary democracy, following a constitutional amendment in September 1991

The prime minister is the chief executive and the head of the cabinet (Council ofMinisters), which the prime minister selects; the president has a largely ceremonial role,but appoints members of the cabinet and the judiciary, and has the power to dissolveparliament

Jatiya Sangshad, a unicameral legislature, consisting of 300 members directly electedfrom single territorial constituencies and 30 seats reserved for women; the legislature iselected for a five-year term

June 12th 1996; next election due by June 2001

Sheikh Hasina Wajed’s Awami League (AL) won the largest number of parliamentaryseats in the 1996 election, which was overseen by a caretaker government. The JatiyaParty (JP) provided the AL with the support necessary to form a majority government,but withdrew its support in March 1998. A member of the JP holds a cabinet post in theAL government. The Jatiya Samajtantrik Dal (JSD) also has a representative in the cabinet

Awami League (AL); Bangladesh National Party (BNP); Jatiya Party (JP); Jamaat-e-Islami(Jamaat); Jatiya Samajtantrik Dal (JSD)

President Shahabuddin AhmedPrime minister & minister of defence establishment & energy Sheikh Hasina Wajed

Commerce & industry Tofael AhmedCommunications Anwar Hossain Manju (JP)Education, science & technology A S H K SadekEnvironment & forestry Syeda Sajeda ChowdhuryFinance S A M S KibriaFood & agriculture Matia ChowdhuryForeign affairs Abdus Samad AzadHealth & family welfare Salahuddin YusufHome affairs Mohammad NasimLaw & justice Abdul Matin KhasruLocal government, rural development & co-operatives Zillur RahmanWater resources Abdur Razzak

Farashuddin Ahmed

National legislature

Form of government

Official name

National elections

National government

Main political organisations

Key ministers

Central bank governor

The executive

Bangladesh 5

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Economic structure

Latest available figures

Economic indicators 1994 1995 1996 1997 1998

GDP at current market pricesa (Tk bn) 1,030.4 1,170.3 1,301.6 1,403.0 1,548.3

Real GDP growth at constant market pricesa (%) 4.2 4.4 5.3 5.9 5.7

Consumer price inflation (av; %) 3.6 5.8 2.7 5.6 9.5

Population (mid-year; m) 116.5 118.2 120.0b 122.0b 123.8b

Rice productiona (m tonnes) 18.04 16.84 17.69 18.88 18.20b

Jute productiona (m tonnes) 0.8 1.0 0.7 0.9 0.8b

Exports fob ($ m) 2,934 3,733 4,009 4,840 5,144b

Imports fob ($ m) 4,351 6,057 6,285 6,588 6,749b

Current-account balance ($ m) 200 –824 –991 –327 –230b

Reserves excl gold ($ m) 3,139 2,340 1,835 1,582 1,905

Total external debt ($ m) 16,222 16,296 16,083 15,948 16,532

Exchange rate (av; Tk:$) 40.21 40.28 41.79 43.89 46.98

Fiscal year exchange ratea (av; Tk:$) 40.00 40.20 40.84 42.70 45.46

August 2nd 1999 Tk49.5:$1

% of % ofOrigins of gross domestic product 1997/98 total Components of gross domestic product 1997/98 total

Agriculture 28.6 Private consumption 78.3

Manufacturing 9.6 Government consumption 14.1

Construction 6.0 Gross fixed investmentc 14.0

Trade 8.9 Exports of goods & services 17.2

Transport & communications 11.2 Imports of goods & services –23.6

Public administration & defence 5.9 GDP at market prices 100.0

Banking & insurance 2.0

GDP at market prices incl others 100.0

Principal exports 1996/97 $ m Principal imports 1996/97 $ m

Garments & knitwear 2,316.8 Textiles & yarn 1,732.3

Fisheries products 327.2 Machinery & transport equipment 958.3

Jute goods 311.5 Chemicals 491.3

Leather 210.3 Iron & steel 436.5

Raw jute 126.0 Petroleum & petroleum products 375.4

Main destinations of exports 1997 % of total Main origins of imports 1997 % of total

US 33.3 India 11.6

Germany 9.5 China 9.1

UK 8.9 Japan 6.9

France 6.3 Hong Kong 6.3

Italy 5.3 South Korea 5.5

a Fiscal years ending June 30th of year stated. b EIU estimate. c Includes stockbuilding.

Sources: GDP, GDP growth and origins of GDP; rice and jute production: from the Bangladesh Bureau of Statistics, Monthly Statistical Bulletin of Bangladesh. Consumer price inflation; population;exports (fob), imports (fob) and current-account balance; reserves and exchange rate; components of GDP: from IMF, International Financial Statistics. Debt data: from World Bank, GlobalDevelopment Finance. Fiscal-year exchange rate; export and import breakdown: from the Statistics Department of the Bangladesh Bank, Economic Trends. Destination of exports and origin ofimports: from IMF, Direction of Trade Statistics.

6 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

Outlook for 1999-2000

Political disturbances will continue, as the alliance of the right and centre-rightopposition parties, led by the Bangladesh National Party (BNP), steps up itsnationwide programme of strikes, processions, road marches and massmeetings, in an attempt to bring down the Awami League (AL) government.The government’s decision to allow the transshipment of Indian goodsthrough Bangladesh has fuelled growing public disenchantment with theadministration, exacerbated by water and power crises, rising crime and othergovernment failures. The opposition will capitalise on these issues to try toforce the government to hold all the major elections—municipal, citycorporation, upazila (local council) and parliamentary—under a neutralcaretaker government. Upazila polls are expected to be held by November1999, while the city corporation polls are due by January 2000. It is unlikelythat the general election will be held earlier than its scheduled date of June2001, as the government is unlikely to agree to the suggestion of a caretakergovernment. It is also possible that municipal and city corporation electionswill cause a rift within the BNP coalition, as some partners participate againstthe wishes of the BNP leadership.

The BNP-led opposition claims that by agreeing to provide transshipmentfacilities and by conspiring to export gas to India (see Energy and power), theAL government has undermined the political sovereignty and territorialintegrity of Bangladesh. In addition, the opposition claims that the power andwater crises that have paralysed the economy are the result of governmentnegligence. The opposition is also frustrated by the government’s failure tomeet its demands for the release of political detainees, the withdrawal of falsecases against political leaders, and the replacement of the country’scontroversial election commissioner, Abu Hena.

Unwilling to make concessions to the BNP, the AL counts on the support ofsmaller left and centre-left parties, but has so far failed to form a solid alliance.Further consolidation of these smaller parties does not seem likely. Under theseconditions, politics will remain confrontational at least until the next generalelection, as the opposition will receive further impetus if the governmentproceeds with the upazila and city corporation polls without ensuring theparticipation of the major opposition parties, particularly the BNP and theJatiya Party (JP, or Ershad).

The government has claimed that the rate of GDP growth was 5.2% in fiscalyear 1998/99 (July 1st-June 30th), despite the floods which caused chaos in theproductive sectors of the economy in July-September 1998. The governmentclaimed that the agricultural sector was behind the stronger than expectedgrowth rate, owing to a bumper harvest of the boro rice crop after the floods.However, export growth has been estimated at less than 6% in 1998/99,compared with average growth of 16% in the early and mid-1990s. In addition,a shortfall in revenue collection raised the overall budget deficit from 4.2% ofGDP in 1997/98 to 5.3% in 1998/99, the highest level since 1994/95.Nevertheless, the economy has recovered more quickly than expected from the

Political agitation willincrease

—as the oppositionincreases pressure on

the government

The economy will recover—

Bangladesh 7

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

floods, thanks to generous donor support in the form of food andrehabilitation assistance, and the government’s moderately effective macro-economic measures. The government expects GDP growth to reach 6.4% in1999/2000, with the agricultural sector growing by 8.7% and manufacturing by10%. The EIU also expects a recovery in 1999/2000, but we estimate slightlylower GDP growth, of 6.2%. We are less optimistic about the prospects formanufacturing and agriculture, anticipating growth of 7.8% and 5.8%respectively. As the urgency of flood relief subsides, the effective macro-economic management that followed the floods is likely to revert to its usualcourse, burdened by corruption and excessive bureaucracy. Poor infrastructureand inefficient resource allocation will continue to act as major obstacles tosustained growth.

Inflation has been contained by a number of factors, including a recovery infood supplies; tight monetary and fiscal policies; the collapse of the capitalmarket; the crowding out of credit to the private sector; and slower growth ingovernment credit. Despite some recent relaxation in monetary and fiscalpolicies (to stimulate growth), these forces are expected to continue throughthe forecast period. As a consequence, we expect the annual average inflationrate to fall to 7.6% in 1999 and 7% in 2000, from 9.5% in 1998. With abumper harvest of the boro rice crop and about 1m tonnes of food aid in theaftermath of the floods, the inflation rate fell to 7.7% year on year in April1999, compared with 8.7% year on year in March.

According to fiscal estimates, Bangladesh’s export income has fallen drastically,owing to flood damage, which has disrupted transport and communicationsand lowered industrial output and distribution. The export growth rate fell tobelow 6% in 1998/99, compared with double-digit growth rates experiencedsince the early 1990s. The trade deficit has been exacerbated by a 8.5% rise inthe import bill, as foodstuffs and capital goods and machinery lost in thefloods have had to be imported. The trade deficit rose to $313.8m in February1999, compared with $225m in February 1998—a 39% rise year on year. Thedeficit narrowed slightly in 1999/2000, but Bangladesh's export com-petitiveness is still suffering, as, despite the most recent 2% devaluation, thetaka remains overvalued vis-à-vis the currencies of the South-east Asiancountries affected by the regional economic crisis.

An increase in interest payments on the country’s external debt will cause adeterioration in the income balance over the forecast period and put pressureon the current account. We expect inward workers’ remittances to rise in 1999-2000, assuming a sustained recovery in oil prices and in the South-east Asianeconomies. However, the country will still need bilateral and multilateral loansto meet its financing requirement. This will be exacerbated by a deteriorationin the capital account in the current fiscal year, and the poor exportperformance indicated by preliminary data for 1998/99. Export growth ishighly unlikely to be above trend over the forecast period, as the current powercrisis and the unstable political environment have further dampened prospectsin an area in which Bangladesh is already vulnerable, owing to its narrowexport base.

—and inflation will fall—

—but pressures on thecurrent account will persist

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

-5

-4

-3

-2

-1

0

1

2

1991 92 93 94 95 96 97 98 99 2000

$ bn; left scale

% of GDP; right scale

Current-account balance

(a) Estimates. (b) Forecasts. Source: EIU.

98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)98(a) 99(b) 2000(b)

8 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

However, a larger current transfers surplus, including workers’ remittances, isexpected partly to offset the deterioration in the trade balance and the declinein earnings from services and investment income. We expect the current-account deficit to rise to 2% of GDP in 1999, before falling to 1% in 2000, asthe export sector begins to recover and the current transfers balance improves.

The foreign-exchange reserves position will remain stable, thanks to theforeign aid provided for post-flood rehabilitation and $138m received from theIMF for balance-of-payments support. According to IMF data, Bangladesh’sforeign-exchange reserves (excluding gold) stood at $1.5bn at end-March 1999,compared with $1.7bn at end-March 1998. As import pressures subside andexport earnings begin to recover during the remainder of 1999, reserves arelikely to stabilise. The continued strengthening of foreign direct investment(FDI) has so far failed to improve the reserves position. FDI is concentrated inthe gas sector, and the government is committed to buying a certain amountof gas from the gas companies, priced in dollars. Import cover will average just2.2 months in 1999, compared with 2.8 months in 1998, and rise onlymarginally in 2000, to 2.3 months.

Faced with dwindling export earnings, and pressed by the leading exportbodies of the country—in addition to recommendations from the World Bankand the IMF—Bangladesh devalued its currency by 2.06% on July 18th. Thiswas the third major devaluation of the taka in the last 13 months and the firstin the current fiscal year. The taka has now been devalued by more than 18%against the dollar since June 1996, when the AL assumed power. However, thetaka will remain under pressure, as higher import payments and other outwardremittances, together with the Asian crisis and a loss of export competitiveness,increase the need for further devaluations in late 1999 and early 2000. Weforecast a 7.6% depreciation in 1999, from Tk48.5:$1 at end-1998 to Tk52.5:$1at end-1999. A further easing of inflation and an improvement in exportperformance will reduce pressure on the taka in 2000. We forecast an annualaverage exchange rate of Tk54:$1 in 2000, compared with Tk50.5:$1 in 1999.

Forecast summary(% change year on year unless otherwise indicated)

1997a 1998b 1999c 2000c

Real GDPd 5.9 5.6a 5.2 6.2 of which: agriculture 6.4 3.1a 5.0 5.8 industry 3.8 7.3a 4.8 8.2

Consumer prices (av) 5.6 9.5a 7.6 7.0

Merchandise exports fob ($ m) 4,840 5,144 5,665 5,937

Merchandise imports fob ($ m) 6,588 6,749 8,001 7,990

Trade balance ($ m) –1,748 –1,604 –2,236 –2,052

Current-account balance ($ m) –327.3 –230.4 –719.0 –363 % of GDP –1.0 –0.7 –2.0 –1.0

Exchange rate (av; Tk:$) 43.89 46.98a 50.50 54.00

Exchange rate (end-period; Tk:$) 45.45 48.50a 52.50 55.50

a Actual. b EIU estimates. c EIU forecasts. d Fiscal years ending June 30th of year stated.

Foreign-exchange reserveswill remain stable

Devaluations of the takawill continue

Bangladesh 9

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

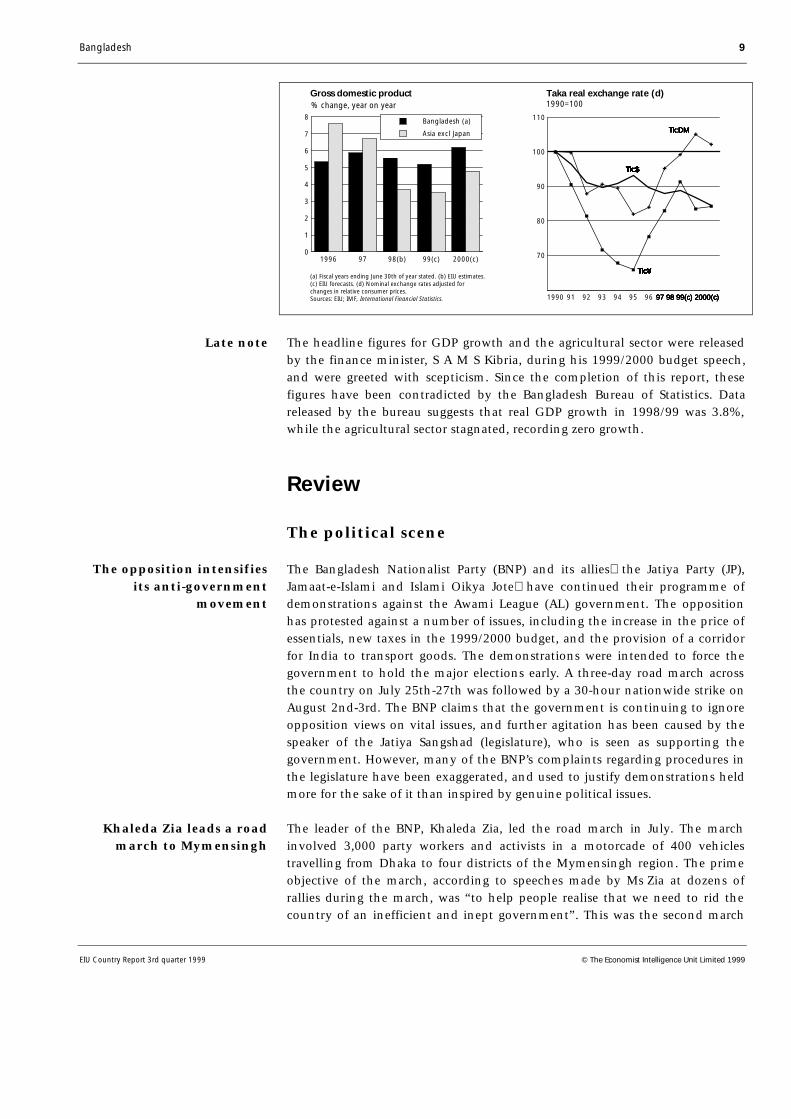

The headline figures for GDP growth and the agricultural sector were releasedby the finance minister, S A M S Kibria, during his 1999/2000 budget speech,and were greeted with scepticism. Since the completion of this report, thesefigures have been contradicted by the Bangladesh Bureau of Statistics. Datareleased by the bureau suggests that real GDP growth in 1998/99 was 3.8%,while the agricultural sector stagnated, recording zero growth.

Review

The political scene

The Bangladesh Nationalist Party (BNP) and its alliesthe Jatiya Party (JP),Jamaat-e-Islami and Islami Oikya Jotehave continued their programme ofdemonstrations against the Awami League (AL) government. The oppositionhas protested against a number of issues, including the increase in the price ofessentials, new taxes in the 1999/2000 budget, and the provision of a corridorfor India to transport goods. The demonstrations were intended to force thegovernment to hold the major elections early. A three-day road march acrossthe country on July 25th-27th was followed by a 30-hour nationwide strike onAugust 2nd-3rd. The BNP claims that the government is continuing to ignoreopposition views on vital issues, and further agitation has been caused by thespeaker of the Jatiya Sangshad (legislature), who is seen as supporting thegovernment. However, many of the BNP’s complaints regarding procedures inthe legislature have been exaggerated, and used to justify demonstrations heldmore for the sake of it than inspired by genuine political issues.

The leader of the BNP, Khaleda Zia, led the road march in July. The marchinvolved 3,000 party workers and activists in a motorcade of 400 vehiclestravelling from Dhaka to four districts of the Mymensingh region. The primeobjective of the march, according to speeches made by Ms Zia at dozens ofrallies during the march, was “to help people realise that we need to rid thecountry of an inefficient and inept government”. This was the second march

The opposition intensifiesits anti-government

movement

Khaleda Zia leads a roadmarch to Mymensingh

0

1

2

3

4

5

6

7

8

1996 97 98(b) 99(c) 2000(c)

Bangladesh (a)

Asia excl Japan

Gross domestic product% change, year on year

(a) Fiscal years ending June 30th of year stated. (b) EIU estimates.(c) EIU forecasts. (d) Nominal exchange rates adjusted forchanges in relative consumer prices.Sources: EIU; IMF, International Financial Statistics.

70

80

90

100

110

1990 91 92 93 94 95 96 97 98 99 2000

Taka real exchange rate (d)1990=100

Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$Tk:$

Tk:¥

Tk:$

Tk:¥Tk:¥

Tk:DMTk:DMTk:DM

Tk:$

Tk:¥

Tk:$

Tk:¥Tk:¥

Tk:DMTk:DMTk:DM

97 98 99(c) 2000(c)

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:$

Tk:¥

Tk:DM

97 98 99(c) 2000(c)97 98 99(c) 2000(c)97 98 99(c) 2000(c)97 98 99(c) 2000(c)

Late note

10 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

by the BNP-led opposition in three months. The first was from Dhaka to thenorthern town of Panchagarh on May 16th-18th, when Ms Zia reached herhometown of Dinajpur in a similar convoy.

A strike was held in July to protest against an increase in value-added tax (VAT)in the 1999/2000 budget, which was seen as regressive and thus directedagainst the poor. The strike was marred by large-scale violence, including thedeath of a police officer in a bomb explosion, which the government allegedwas caused by BNP supporters. The BNP responded to the allegations bysuggesting that the AL was responsible for the explosion and that the killingwas actually a deep-rooted government conspiracy to create confrontationbetween the opposition and the security forces. The BNP warned of furtherprotests if charges against its leaders and activists were not withdrawn.

On May 12th Bangladesh’s High Court ruled that strikes were illegal. JudgeMohammad Golam Rabbani said that strikes had the potential to threaten ordisturb public tranquillity and that “an assembly of five or more persons takinga decision for hartal (strike) or trying to plan one is unlawful”. The judgementfollowed an unprecedented request by the High Court to the main oppositionand government parties in February to show why strikes and anti-strikeactivities should not be declared an offence. Despite a petition filed by thesecretary-general of the BNP, Abdul Mannan Bhuiyan, the Supreme Courtupheld the High Court ruling.

Bangladesh faces growing public debate over the frequent strike calls byopposition political parties (the BNP has organised around 30 days of nation-wide strikes since the AL took office in June 1996). The prime minister, SheikhHasina Wajed, has recently disavowed the tactic, but as she called strikesfrequently while in opposition between 1991 and 1996, the BNP is refusing toaccept her word on the issue. Nevertheless, the BNP’s decision to stage roadmarches represents a noticeable change of tactics. The change reflects internaltensions within the BNP, as members who were opposed to strikes have giventheir support to marches, which are seen as less disruptive to the country.

The next general election is not due until 2001 and the prime minister, SheikhHasina Wajed, has ruled out the possibility of holding it early. At publicmeetings Ms Hasina confirmed that she would not hold the election early,criticising the opposition parties for trying to create anarchy and disruptdemocracy in the country. She suggested that the opposition should engage inconstructive dialogue, instead of staging strikes and road marches, and deniedthat there was any substance to the issues they had raised.

Earlier, parliament passed four separate pieces of legislation extending thedeadlines for upazila and city corporation polls. The extension allows thegovernment to stall the city corporation elections for a further 90 days: theywere originally due by April 4th. This date was itself an extension; the pollswere previously scheduled to take place on March 15th. The date for upazilapolls, which were due by July 30th, was extended for an additional 150 days.The opposition parties walked out of the parliament, demanding that both setsof polls be held simultaneously, under a non-partisan caretaker government.

The prime ministerconfirms that polls will

be on schedule

The BNP stages a strikeagainst the 1999/2000

budget

The deadlines for upazilaand city corporation polls

are extended again

The High Court declaresstrikes unlawful

Bangladesh 11

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The BNP and its allies plan to organise more road marches over the nexttwo months, from Dhaka to the divisional cities of Sylhet, Khulna and Barisaland to some district towns. The BNP leadership used the march in July toencourage supporters to besiege Dhaka on November 7th. This coincides withthe day commemorating the national revolution and solidarity, when thealliance is likely to reaffirm plans to oust the AL from power. Recent pressreports have indicated that even those among the BNP who are opposed tostrike action appear to be supporting the programme. This is owing to theirbelief that, despite their attempts to follow parliamentary procedure, the ALhas failed to respect their right to speak. However, it is also likely that thechange in attitude reflects growing pressure from within the BNP, as these soft-line MPs have faced strong accusations of supporting the government againsttheir own party.

At the end of July the AL government agreed in principle to a proposal for thetransshipment of Indian goods via Bangladesh’s land routes. Under theproposal, goods in sealed containers will be transferred from Indian toBangladeshi trucks at a border point. The Bangladeshi trucks will transport thecontainers to another border point, where they will be returned to Indianlorries. A joint committee comprising experts from both countries has beenestablished to work out the transshipment charges, schedules and other details.

The move evoked protests from opposition parties, who called for a 30-hournationwide strike on August 2nd-3rd. Ms Zia claimed that the proposal toprovide transit ran counter to the independence, sovereignty and territorialintegrity of Bangladesh. The BNP-led coalition sees the decision as furtherevidence that Ms Hasina is co-operating with India, against the wishes of theBangladeshi people.

However, leaders of at least two top business chambers gave their instantapproval to the deal. Mr. Abdul Awal Mintoo, the president of the Federationof Bangladesh Chambers of Commerce and Industry (FBCCI), the country’smain business body, hailed it as a positive decision, which would not onlyincrease foreign-exchange earnings for Bangladesh, but would develop thecountry’s transport sector. The chief of the Dhaka Chamber of Commerce andIndustry (DCCI), M H Rahman, said the question of transit should not be sucha large issue. Both leaders said that the opposition’s calls for strikes were agreater cause for concern, claiming that strikes were far more damaging to thedomestic economy, and hence to the people.

The prime minister, for her part, defended her decision, saying that it was theBNP government of Ziaur Rahman that had originally approved the transitfacility agreement with India in the 1980s. Moreover, Ms Zia had agreed to it in1993, when she signed the South Asian preferential trade agreement (SAPTA)and the government was thus fulfilling obligations agreed to in an inter-national treaty. Ms Hasina also claimed that Bangladesh would earn royalties ofTk20bn ($396m) annually.

More road marchesare planned

Bangladesh allows thetransshipment of

Indian goods

but the oppositionparties oppose the move

despite approval by somebusiness bodies

The prime minister defendsthe cabinet decision

12 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

The government has launched a countrywide crackdown on crime, althoughthe primary focus is on the southern districts, following the killing of theleader of the Jatiya Samajtantrik (JSD) party, Kazi Aref Ahmed, and five othersin January, and the killing of seven people in two powerful bomb explosions ata cultural function in Jessore on March 7th. In April, as part of the strategy, anamnesty was offered to political extremists and fugitives from the law. Thisoffer has led to 1,600 outlaws surrendering to the authorities with their armsand ammunition. The government promised to rehabilitate those who sur-rendered, by withdrawing cases against them, and finding them employment.

Despite the crackdown, all forms of crime are rising. According to policesources, at least 1,571 people were murdered in January-May 1999, comparedwith 1,304 murders in January-May last year. There were 1,264 incidents ofrape in the same period, compared with 974 last year. In Dhaka city alone, thenumber of crimes reported increased to 8,401, compared with 7,235 in 1998.National statistics indicate that the number of crimes reported rose to 50,242,from 44,928 in 1998. There is a significant difference between the actual levelof crime and the number of crimes reported, as the incompetence of the policeforce, in addition to social issues, dissuade Bangladeshis from reportingoffences. The government’s failure to improve the security of the country,while at the same time politicising the police force, has worsened foreigninvestor sentiment, as reports are rising of the harassment of foreign com-panies and the theft of their goods by politically connected groups.

Al least 25 people died in police stations, prisons and court custody in the firsthalf of 1999, according to Odhikar, a human rights coalition in Bangladesh. Atotal of 531 girls and women were raped in custody during the period, with atleast four of these rapes allegedly by police personnel.

Bangladesh has been ranked 150th out of 174 countries in the UNDevelopment Programme’s human development index for 1999 (the countrywas ranked 146th in 1998). The index, which mainly focuses on life expect-ancy, educational attainment and adjusted real income, noted as a positivedevelopment the increased participation of women in the workforcerisingfrom 5% in 1965 to 42% in 1995mainly owing to growth in the readymadegarments industry. The report, however, pointed out that the time spent inunpaid work remains high. On average, according to the latest data available,women in both formal and informal urban manufacturing sectors worked31 unpaid hours a week in 1995, compared with 14 hours a week for men.

A senior AL politician, Kader Siddiqui, was expelled from the party onJuly 23rd for anti-AL speeches and activities. Mr Siddiqui, a highly respectedleader during the war with Pakistan and a close confidant of SheikhMujibBangladesh’s founding leader and father of Ms Hasinahas openlycriticised the prime minister and the AL leadership on issues such as corruptionin recent months. On July 26th Mr Siddiqui threatened to convene a meetingof the councillors of the party within 90 days, claiming that the governmenthad no legal authority to expel him without consulting council members.However, he has repeatedly ruled out joining any of the opposition parties.

The crackdown oncriminals pays dividends

but crime is still rising

Human rights conditionsdeteriorate

An Awami Leaguepolitician is expelled

from the party

Bangladesh 13

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Jyotirindriyo Bodhipriyo Larma, alias Shantu Larma, who led the insurgentmovement in the Chittagong Hill Tracts (CHT), took over the chairmanship ofthe 22-member interim CHT regional council on May 25th. At a function heldto celebrate the occasion Mr Larma called for all the parties concerned to forgetthe past and enter a period of constructive assistance and sympathy, to allowthe CHT agreement to succeed. He requested that those involved work togetherin the interests of the region and the country as a whole, with an obliquereference to Bengali settlers and to army personnel, as well as to the rebel triballeaders who are still demanding full autonomy for the region.

During a visit to Dhaka in mid-July the foreign minister of Myanmar, U WinAung, agreed to the speedy repatriation of 7,000 Myanmar refugees, known asRohingyas. (More than 250,000 Rohingyas fled to Bangladesh in early 1992,fearing persecution at home.) Although Bangladesh has called for the return ofall 21,000 registered Rohingya refugees—who are still residing in two camps inthe Cox's Bazar district (which borders Myanmar's western Moslem-majorityArakan province)—the full number are unlikely to return home until at leastend-2000. Most of the Rohingyas are Muslims and economic refugees, andsome are political activists who drew the wrath of Myanmar's military bysupporting both the pro-democracy leader Aung San Suu Kyi and the militantsfighting for a Muslim homeland in Arakan. Although repatriation began inSeptember 1992 under the supervision of the UN High Commissioner forRefugees (UNHCR), the process suddenly came to a halt in July 1997, withsome 21,000 refugees still left in Bangladesh. Although repatriation resumed inOctober 1998, it has moved extremely slowly. A representative of the UNHCRin Cox's Bazar recently expressed dismay over the slow pace of the return.

Bangladesh signed a contract with Russia in June to buy eight MIG-29 combataircraft for $115m, to augment its air-force capability. The decision provokedsharp criticism from Ms Zia, who claimed in a statement on July 1st that thepurchase had involved corruption, as the fighters could have been bought forless than the stated amount. In addition, she condemned the government’sdecision to buy army trucks from the Indian company, Ashok Leyland, sayingthat India itself did not use these allegedly substandard vehicles for its army.The US and foreign-aid donors have also criticised the aircraft purchases, owingto the increased pressure on the country’s already weak foreign-exchangereserves position. However, the AL government has defended its purchases,stating that they are vital to the country’s national security interests.

Economic policy

On June 30th parliament approved a budget envisaging revenue of Tk342.9bn($7.6bn) for fiscal year 1999/2000. The most important tax changes were aprojected increase in revenue through value-added tax (VAT), and a cut inimport duties on raw materials to encourage industrial growth. According tothe government, the budget would register a surplus of Tk63.5bn. Projectedrevenue income was 22.5% higher than in the 1998/99 budget, while expend-iture was expected to rise by 6.2%. About Tk83.6bn was expected to come from

Shantu Larma becomeschairman of the CHT

regional council

Myanmar refugees areto return

There is controversy overthe purchase of eightMIG-29s from Russia

A new budget is launched

14 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

foreign donors. The proposed budget also includes a withdrawal of the 5%duty on paper pulp, reducing duty on edible oil from 25% to 15%, and waivingimport duties on raw materials for pharmaceuticals. A supplementary tax onlocally produced ceramic and porcelain items has also been withdrawn. Otherproposals and data outlined in the budget were as follows.

• GDP growth in 1998/99 was estimated to be 5.2%, despite the floods whichdevastated large areas in July-September 1998. The finance minister, S A M SKibria, claimed that effective macroeconomic measures and a remarkable rateof growth in the agricultural sector were behind the economy’s rapid recovery.

• The outlay for the annual development programme (ADP), has been raisedby 13.9% compared with 1998/99, to Tk155bn, with 50.5% financed throughdomestic sources. The transport sector has been given priority, with theconstruction of the Dhaka eastern bypass and bridges on the rivers Dharla,Rupsa, and Paksi seen as essential.

• New taxes have been imposed on bonus shares, saving certificates, featurefilms, brick manufacturing, and doctors’ services at private clinics andhospitals. However, a five-year tax holiday has been announced for new privatehospitals, under certain conditions.

• Tax exemption limits have been raised. Earnings below Tk75,000 ($1,546) ayear will be non-taxable (the previous limit was Tk60,000). Income tax on thenext Tk50,000 will be at 10%, and for the next Tk125,000 at 18%, with incomeabove these levels subject to a 25% tax rate.

• The VAT regime has been expanded to comprise a further 31 items,including spectacle lenses, frames and mountings, goggles and sunglasses,view-, invitation- and greetings-cards and vehicle tyres and tubes.

• The 2.5% infrastructure development surcharge (IDS) and the 3% advancedincome tax on cotton (imports) have been withdrawn, along with charges of15% (VAT) and 2.5% (IDS) on synthetic staple fibre yarn and fabrics.

• A 5% tax on the purchase of luxury cars with an engine capacity over2,000cc and jeeps with a capacity of over 3,000cc has been imposed. A fixedtax for certificates indicating roadworthiness, following a test, has been intro-duced for selected vehicles.

• Special export incentives for the garment and jute sectors have beenextended, and new export incentives have been provided for the leather sectorand small sectors such as quilts and fresh and artificial flower exports. Theadvance income tax of 0.25% charged at source on exports has been abolished.

• Pre-shipment inspection (PSI) has been made mandatory for the majority ofimports, to reduce corruption.

• Real-estate companies have been made liable for advanced income tax as afinal discharge of tax liability, prior to building plans being submitted forapproval.

• Tk30bn, or 17% of the budget, has been allocated to defence expenditureand Tk32bn (18%) has been allocated to education.

Bangladesh 15

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

The main opposition political parties rejected the budget as favouring the richby raising the tax burden for ordinary people, and staged nationwide dawn todusk strikes both before and after the budget presentation. On June 25th theBangladesh Economic Association criticised the budget for failing to allocateresources efficiently and for overemphasising revenue collection, rather thanindustrialisation or investment generation. The Federation of BangladeshChambers of Commerce and Industry (FBCCI), the Dhaka Chamber ofCommerce and Industry (DCCI) and the Metropolitan Chamber of Commerceand Industry (MCCI) gave mixed reactions, commending the lowering oftariffs on industrial inputs and the rationalisation of tax rates and exportincentives, but criticising the extensions of VAT. The textile associations of thecountry hailed the budget as textile-friendly, pragmatic and export-oriented.

Government revenue earnings for 1998/99 fell short of their targets. Revenuecollection reached Tk148.37bn, compared with a target of Tk157bn—ashortfall of Tk8.62bn, or 5%. However, this was still 7.5% higher than revenuein 1997/98. The shortfall was largely attributed to the flood damage, a fall innon-foodgrain imports, congestion at the Chittagong port, and large-scalesmuggling. Revenue collection from imports was Tk85.39bn, compared withthe target of Tk90.5bn. Two sources represented the bulk of the shortfall: theindustrial sector contributed Tk37.32bn, compared with a target of Tk39.25bn,and income tax revenue was Tk23.65bn, compared with a target of Tk24.7bn.

According to government figures, the overall budget deficit increased from4.2% of GDP in 1997/98 to 5.3% in 1998/99, the highest level since 1994/95.The increase in the deficit reflects a decline in the revenue/GDP ratio, whichfell from 9.7% in 1997/98 to 9% in 1998/99, and an increase in theexpenditure/GDP ratio from 13.9% to 14.3%. The World Bank’s June 1999economic update on Bangladesh highlighted the vulnerability of the country’sexternal account. Despite a larger surplus on the current transfers account, dueto strong remittances growth and stagnant non-food imports in the first eightmonths of 1998/99, foreign reserves have stayed at around $1.7bn sinceNovember 1998, barely equivalent to 2 months of import cover (and only$1.5bn on an IMF basis).

Fiscal trends, 1995-2000(% of GDP)

1995/96 1996/97 1997/98 1998/99 1999/2000a

Revenue 9.1 9.5 9.7 9.0 10.0

Expenditure 13.5 13.9 13.9 14.3 14.2

Balance –4.5 –4.5 –4.2 –5.3 –4.2

Financing: Net domestic 1.7 1.5 1.6 2.1 1.5 Net foreign 2.8 2.9 2.5 3.3 2.7

a Budget projection.Source: World Bank, Periodic Economic Update, June 1999.

but evokes mixedreactions

Revenue collection fallsshort of targets

and the budget andcurrent-account deficits

widen

16 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

The economy

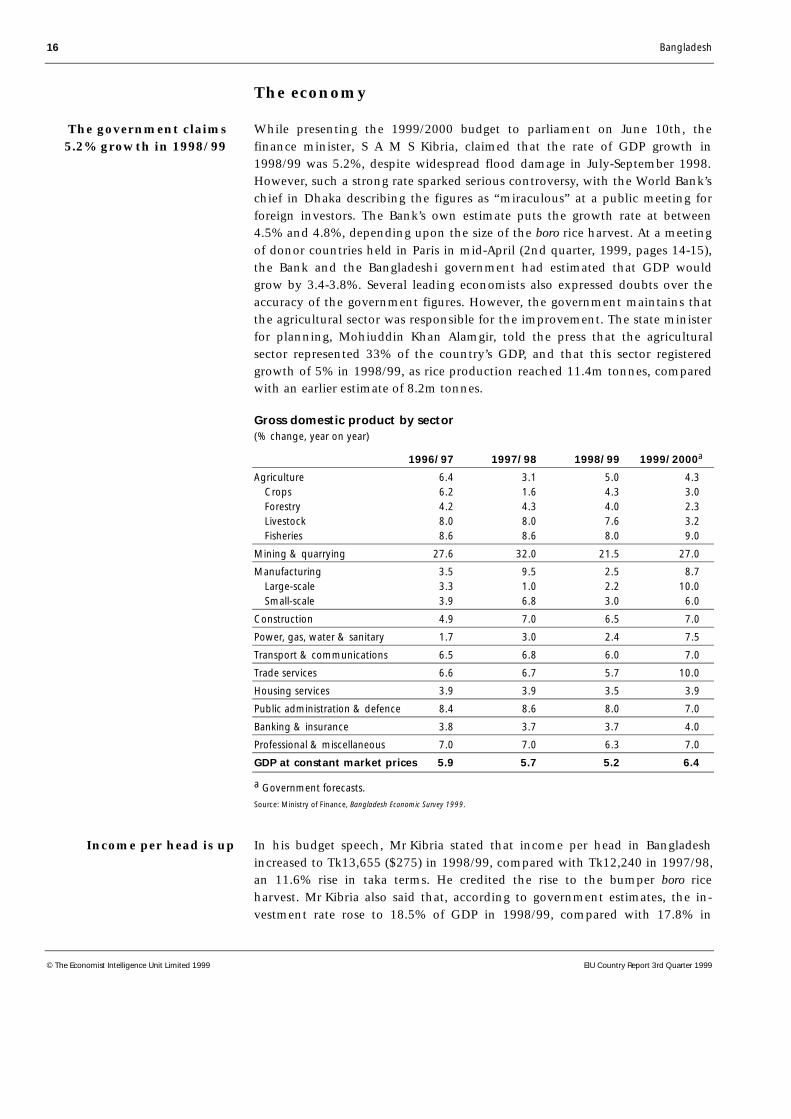

While presenting the 1999/2000 budget to parliament on June 10th, thefinance minister, S A M S Kibria, claimed that the rate of GDP growth in1998/99 was 5.2%, despite widespread flood damage in July-September 1998.However, such a strong rate sparked serious controversy, with the World Bank’schief in Dhaka describing the figures as “miraculous” at a public meeting forforeign investors. The Bank’s own estimate puts the growth rate at between4.5% and 4.8%, depending upon the size of the boro rice harvest. At a meetingof donor countries held in Paris in mid-April (2nd quarter, 1999, pages 14-15),the Bank and the Bangladeshi government had estimated that GDP wouldgrow by 3.4-3.8%. Several leading economists also expressed doubts over theaccuracy of the government figures. However, the government maintains thatthe agricultural sector was responsible for the improvement. The state ministerfor planning, Mohiuddin Khan Alamgir, told the press that the agriculturalsector represented 33% of the country’s GDP, and that this sector registeredgrowth of 5% in 1998/99, as rice production reached 11.4m tonnes, comparedwith an earlier estimate of 8.2m tonnes.

Gross domestic product by sector(% change, year on year)

1996/97 1997/98 1998/99 1999/2000a

Agriculture 6.4 3.1 5.0 4.3 Crops 6.2 1.6 4.3 3.0 Forestry 4.2 4.3 4.0 2.3 Livestock 8.0 8.0 7.6 3.2 Fisheries 8.6 8.6 8.0 9.0

Mining & quarrying 27.6 32.0 21.5 27.0

Manufacturing 3.5 9.5 2.5 8.7 Large-scale 3.3 1.0 2.2 10.0 Small-scale 3.9 6.8 3.0 6.0

Construction 4.9 7.0 6.5 7.0

Power, gas, water & sanitary 1.7 3.0 2.4 7.5

Transport & communications 6.5 6.8 6.0 7.0

Trade services 6.6 6.7 5.7 10.0

Housing services 3.9 3.9 3.5 3.9

Public administration & defence 8.4 8.6 8.0 7.0

Banking & insurance 3.8 3.7 3.7 4.0

Professional & miscellaneous 7.0 7.0 6.3 7.0

GDP at constant market prices 5.9 5.7 5.2 6.4

a Government forecasts.Source: Ministry of Finance, Bangladesh Economic Survey 1999.

In his budget speech, Mr Kibria stated that income per head in Bangladeshincreased to Tk13,655 ($275) in 1998/99, compared with Tk12,240 in 1997/98,an 11.6% rise in taka terms. He credited the rise to the bumper boro riceharvest. Mr Kibria also said that, according to government estimates, the in-vestment rate rose to 18.5% of GDP in 1998/99, compared with 17.8% in

Income per head is up

The government claims5.2% growth in 1998/99

Bangladesh 17

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

1997/98, although this may partly have reflected the need for infrastructureand rehabilitation expenditure following the floods. Nevertheless, investmenthas followed an upward trend throughout the 1990s, with the share of private-sector investment in the total rising continuously. If this trend continues inthe longer term, the economy and the use of resources may become moreproductive. However, it is estimated that the domestic savings/GDP ratio fell to8.4% of GDP in 1998/99, compared with 8.6% in the previous year. If the risein income per head is a realistic estimate, this is worrying, although the fallcould be attributable to greater flood-related expenditure. (The savings/GDPratio in Bangladesh remains one of the lowest in Asia.)

Investment/GDP ratios(%)

1990/91 1991/92 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99

Total 11.5 11.1 14.3 15.4 16.7 17.0 17.3 17.8 18.5

Private sector 5.8 6.6 7.8 7.8 9.4 10.7 10.8 11.2 11.5

Source: Ministry of Finance, Bangladesh Economic Survey 1999.

More than 150,000 workers of the state-owned jute and textile industriesstaged a 48-hour strike on June 29th-30th, demanding higher wages, pro-ductivity commission awards and a halt to the privatisation process. The strikewas sponsored by the leading trade-union body of the Bangladesh Jute MillsCorporation (BJMC), the Bangladesh Textile Mills Corporation (BTMC) and theBangladesh Sugar and Food Industries Corporation (BSFIC). Road and railwaycommunications in the port city of Chittagong came to a complete halt, owingto barricades erected by the workers.

The rate of inflation has declined gradually since December 1998, when theconsumer price index (CPI) rose by 8.8% year on year, pushed up by a 10.5%rise in food prices as the floods disrupted supplies. By April 1999 the year-on-year rate had fallen to 7.7%, largely reflecting a decline in food-price inflationfrom 17.6% at end-1998 to 9.8% in April 1999.

Agriculture

According to government estimates, the agricultural sector grew by 5% year onyear in 1998/99, due to a 10m-tonne boro rice harvest. After a contraction of1% in 1994/95, the sector saw growth of 3.7% in 1995/96, 6.4% in 1996/97and 3.1% in 1997/98. The reasons given by the government for the bumperboro crop included the provision of timely credit and policy support (includingagricultural loans without collateral), imports of high-quality seeds and anincreased supply of fertiliser. The government claimed that the large harvestraised the overall GDP growth rate to 5.2%, from an earlier estimate of below4%. However, while many independent analysts agree that the governmenthandled the impact of the floods well, many have expressed scepticism at theofficial GDP figures (see The economy). A further indication that the size of thecrop has been exaggerated is that the selling price on local markets has not

Workers of state-ownedenterprises stage a

48-hour strike

Inflation is falling

A bumper boro harvestpropels agricultural

growth to 5%

18 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

falllen significantly; although the government has raised its procurement level,this is not sufficient to maintain the prices currently witnessed.

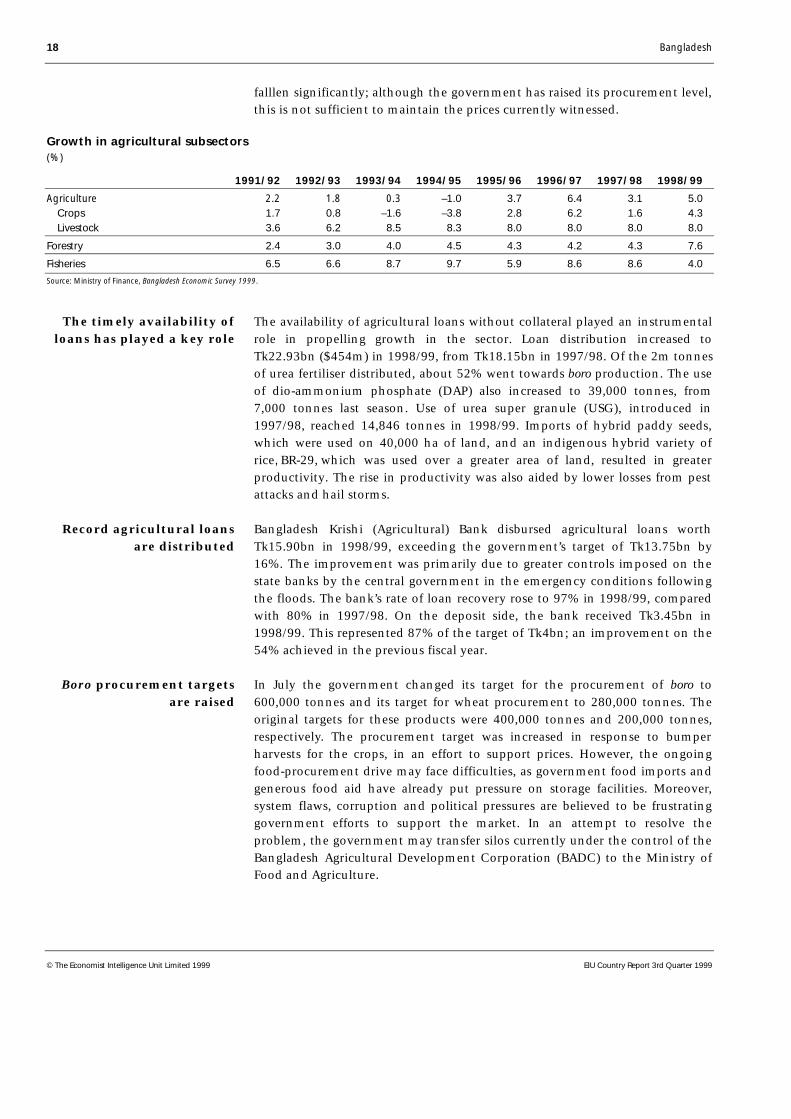

Growth in agricultural subsectors(%)

1991/92 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99

Agriculture 2.2 1.8 0.3 –1.0 3.7 6.4 3.1 5.0 Crops 1.7 0.8 –1.6 –3.8 2.8 6.2 1.6 4.3 Livestock 3.6 6.2 8.5 8.3 8.0 8.0 8.0 8.0

Forestry 2.4 3.0 4.0 4.5 4.3 4.2 4.3 7.6

Fisheries 6.5 6.6 8.7 9.7 5.9 8.6 8.6 4.0

Source: Ministry of Finance, Bangladesh Economic Survey 1999.

The availability of agricultural loans without collateral played an instrumentalrole in propelling growth in the sector. Loan distribution increased toTk22.93bn ($454m) in 1998/99, from Tk18.15bn in 1997/98. Of the 2m tonnesof urea fertiliser distributed, about 52% went towards boro production. The useof dio-ammonium phosphate (DAP) also increased to 39,000 tonnes, from7,000 tonnes last season. Use of urea super granule (USG), introduced in1997/98, reached 14,846 tonnes in 1998/99. Imports of hybrid paddy seeds,which were used on 40,000 ha of land, and an indigenous hybrid variety ofrice, BR-29, which was used over a greater area of land, resulted in greaterproductivity. The rise in productivity was also aided by lower losses from pestattacks and hail storms.

Bangladesh Krishi (Agricultural) Bank disbursed agricultural loans worthTk15.90bn in 1998/99, exceeding the government’s target of Tk13.75bn by16%. The improvement was primarily due to greater controls imposed on thestate banks by the central government in the emergency conditions followingthe floods. The bank’s rate of loan recovery rose to 97% in 1998/99, comparedwith 80% in 1997/98. On the deposit side, the bank received Tk3.45bn in1998/99. This represented 87% of the target of Tk4bn; an improvement on the54% achieved in the previous fiscal year.

In July the government changed its target for the procurement of boro to600,000 tonnes and its target for wheat procurement to 280,000 tonnes. Theoriginal targets for these products were 400,000 tonnes and 200,000 tonnes,respectively. The procurement target was increased in response to bumperharvests for the crops, in an effort to support prices. However, the ongoingfood-procurement drive may face difficulties, as government food imports andgenerous food aid have already put pressure on storage facilities. Moreover,system flaws, corruption and political pressures are believed to be frustratinggovernment efforts to support the market. In an attempt to resolve theproblem, the government may transfer silos currently under the control of theBangladesh Agricultural Development Corporation (BADC) to the Ministry ofFood and Agriculture.

The timely availability ofloans has played a key role

Record agricultural loansare distributed

Boro procurement targetsare raised

Bangladesh 19

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Energy and power

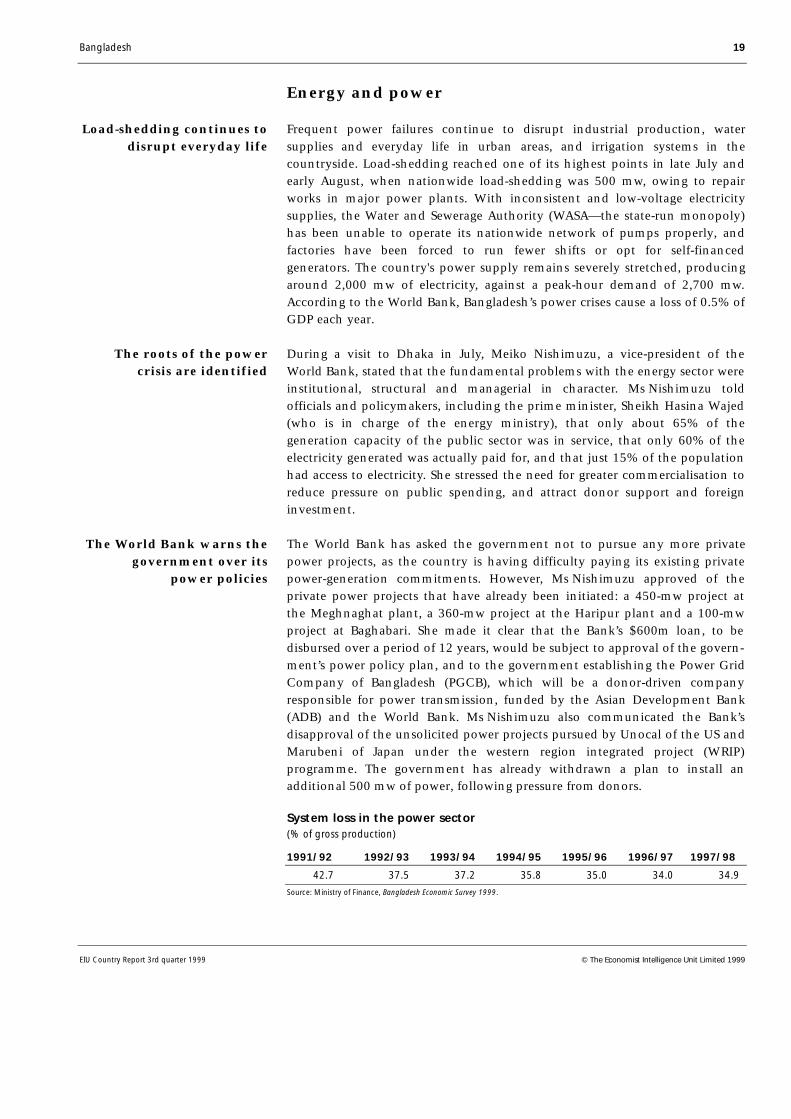

Frequent power failures continue to disrupt industrial production, watersupplies and everyday life in urban areas, and irrigation systems in thecountryside. Load-shedding reached one of its highest points in late July andearly August, when nationwide load-shedding was 500 mw, owing to repairworks in major power plants. With inconsistent and low-voltage electricitysupplies, the Water and Sewerage Authority (WASA—the state-run monopoly)has been unable to operate its nationwide network of pumps properly, andfactories have been forced to run fewer shifts or opt for self-financedgenerators. The country's power supply remains severely stretched, producingaround 2,000 mw of electricity, against a peak-hour demand of 2,700 mw.According to the World Bank, Bangladesh’s power crises cause a loss of 0.5% ofGDP each year.

During a visit to Dhaka in July, Meiko Nishimuzu, a vice-president of theWorld Bank, stated that the fundamental problems with the energy sector wereinstitutional, structural and managerial in character. Ms Nishimuzu toldofficials and policymakers, including the prime minister, Sheikh Hasina Wajed(who is in charge of the energy ministry), that only about 65% of thegeneration capacity of the public sector was in service, that only 60% of theelectricity generated was actually paid for, and that just 15% of the populationhad access to electricity. She stressed the need for greater commercialisation toreduce pressure on public spending, and attract donor support and foreigninvestment.

The World Bank has asked the government not to pursue any more privatepower projects, as the country is having difficulty paying its existing privatepower-generation commitments. However, Ms Nishimuzu approved of theprivate power projects that have already been initiated: a 450-mw project atthe Meghnaghat plant, a 360-mw project at the Haripur plant and a 100-mwproject at Baghabari. She made it clear that the Bank’s $600m loan, to bedisbursed over a period of 12 years, would be subject to approval of the govern-ment’s power policy plan, and to the government establishing the Power GridCompany of Bangladesh (PGCB), which will be a donor-driven companyresponsible for power transmission, funded by the Asian Development Bank(ADB) and the World Bank. Ms Nishimuzu also communicated the Bank’sdisapproval of the unsolicited power projects pursued by Unocal of the US andMarubeni of Japan under the western region integrated project (WRIP)programme. The government has already withdrawn a plan to install anadditional 500 mw of power, following pressure from donors.

System loss in the power sector(% of gross production)

1991/92 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98

42.7 37.5 37.2 35.8 35.0 34.0 34.9

Source: Ministry of Finance, Bangladesh Economic Survey 1999.

Load-shedding continues todisrupt everyday life

The roots of the powercrisis are identified

The World Bank warns thegovernment over its

power policies

20 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

The World Bank’s recommendation for unbundling the power sector through avertical separation of functions (power generation, transmission anddistribution) sparked protests by several groups. At a workshop organised bythe Institute of Engineers in Dhaka on July 9th concern was expressed that thevertical separation of the electricity management would better serve thepurposes of the donors than improve the performance of the troubled sector.Some believe that separation will result in foreign companies generating powerto sell to local distributors at huge margins, as Bangladesh is obliged to signagreements with independent power providers (IPPs) permitting suchconditions to attract foreign companies in the first place. The workshop wasattended by engineers from the Power Development Board (PDB), the DhakaElectricity Supply Authority (DESA), the Rural Electrification Board (REB), theDhaka Electricity Supply Company (DESCO), and the Bangladesh atomicenergy commission. The group admitted that reforms were needed in thepower sector to increase efficiency and ensure transparency and accountability,but declared that they would not let the country be exploited by foreigners.

The new head of the troubled PDB, Quamrul Islam Siddique, criticised donorsfor suggesting the privatisation of the power sector. Mr Siddique claimed thatseparation was intended to protect the interests of foreign companies in thelong run, but would cause serious problems with co-ordination. He believesthat the PBD is facing difficulties because it is not run by technicalprofessionals; the solution, in his opinion, lies in controlling trade unions,reducing the level of power theft, and maximising revenue collection, ratherthan in wholesale privatisation.

In July the Bangladesh energy ministry and the World Bank signed a partialrisk guarantee (PRG) on the 350-mw Haripur power plant, which is being builtby AES Corporation of the US on a build-operate-own (BOO) basis. The PRGwill enable AES to mobilise $65m in commercial lending for the project.According to the agreement, the World Bank will pay for the electricity, shouldthe government fail to do so. With the approval of the World Bank, thegovernment has also signed an agreement with AES for developing theMeghnaghat project, with 800 mw of generation capacity, including theinstallation of a 450-mw Meghnaghat combined cycle power plant (MCCPP).The agreement is the largest signed for private power generation in Bangladesh,with AES due to complete the project in 37 months at a cost of $300m.Bangladesh will buy power from the AES at a 22-year levelled tariff of2.79 cents/kw.

Petrobangla, the state-owned oil and gas company, approved the transfer ofownership of gas Blocks 15 and 16, popularly known as the Sangu gasfield,from UK-based Cairn Energy to the UK-Dutch company Shell on June 30th.Cairn Energy, together with the Holland Sea Search, an Anglo-Dutch jointventure, had signed production-sharing agreements with the government in1993-94 for the exploration and development of gas. In early 1996 thecompanies discovered gas in Block 15, but lacked the funds to develop the fieldand invest in a gas-transmission system (as falling prices for gas and oil since1997 made the project too expensive). Shell and a US company, Halliburton,

Experts oppose the“vertical separation” of

power management

as the new PBD chief alsocriticises donors

A partial risk guaranteeagreement is signed

Shell takes overthe Sangu gasfield

Bangladesh 21

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

purchased a 17.5% stake in Holland Sea Search in both of the blocks. Cairn andShell struck a deal in 1998, under which Cairn surrendered its stakes, includingthe right to operate in the block, to Shell. With Petrobangla’s approval of thetransfer deal, the rights to operate the Sangu field went to Shell with effectfrom July 1st.

In July Unocal and Occidental Petroleum, two US oil giants, traded each other'sassets and liabilities in Bangladesh through a barter deal. Under the share-purchase agreement signed on May 27th, Unocal took over Occidental’s 50%working interests in the three gas blocks in north-eastern Bangladesh, inexchange for Unocal’s 29% stakes in the three oil-producing fields in Yemen.The transferred assets of Occidental in Bangladesh include two production-sharing contracts covering blocks 12, 13 and 14. The Jalalabad gasfield inBlock 13 currently produces 60m-100m cu ft of gas per day.

The PGCB and RPG Transmissions of India signed an agreement in Dhaka inJune, under which RPG will supply transmission-line towers and erect 230-kwtransmission lines, under the Meghnaghat power station associated trans-mission lines project, financed by the ADB. The Tk373.3m ($7.4m) agreementwill allow transmission of the power generated by the Meghnaghat powerstation to Dhaka and other areas of the country.

Petrobangla expects to produce nearly 250m cu ft/day of gas from new wellscurrently under development in the north-eastern Habiganj and Rashidpurgasfields, with a $200m grant from the World Bank and the ADB. The drillingshould be finished by December. The additional output will add to the195m cu ft/day produced in the Habiganj fields and the 85m cu ft/day fromthe Rashidpur fields. Reserves are estimated at 3trn-4trn cu ft. Petrobangla alsorecently began production of 40m cu ft/day from its Bianibazar gasfield, whichwas discovered in 1981. The company is also drilling a development well atSalda river in the eastern Comilla district, bordering India's Tripura state, wherea gasfield with 2bn cu ft of reserves was discovered. Bangladesh produces morethan 900m cu ft/day of gas at present, including 105m cu ft now produced byShell at the offshore Sangu field, and 100m cu ft/day produced by Occidentalin north-eastern Jalalabad.

The large gas reserves and the potential for export have attracted the interest ofmultinational companies, the US government, international donor agenciesand the country’s own business community. Shell and Unocal, who areengaged in production-sharing contracts to drill more wells, have already toldthe government that they must be assured of a market before they invest infurther exploration. Some of Bangladesh’s top business leaders, including thechiefs of the country’s top trade body, the Federation of Bangladesh Chambersand Commerce (FBCCI), and the Foreign Investors’ Chamber of Commerceand Industry (FICCI), have recommended that Bangladesh should exportnatural gas in order to boost fledging foreign-exchange reserves and spurdevelopment. However, the export of gas remains politically controversial, asboth the prime minister and the leader of the main opposition party, KhaledaZia, are committed to restricting supplies to domestic use.

Unocal takes overOccidental’s business

A deal on powertransmission is signed

250m cu ft of gas from newfields will be added

Pressure mounts to allowgas exports

22 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

Gas reserves, July 1999(trn cu ft)

Known discovered reserves 21.0 Proven recoverable reserves 12.6 Reserves already used 3.0 Newly discovered reserves (not announced) 5.5

Total recoverable reservesa (as of Jul 1999) 15.1

a Total of proven recoverable reserves and newly discovered reserves less reserves already used.Source: John C. Holzman, Prospects for the Bangladesh Gas Industry, in The Holiday, July 23rd 1999.

Infrastructure and communications

Bangladesh and India signed an agreement on June 17th to introduce a directbus service between Dhaka and Calcutta, the first since partition in 1947. Thefirst commercial service between the two cities began in July. Initially, twobuses from Dhaka and two from Calcutta will operate on the Dhaka-Benapol-Calcutta route every day except Sundays. An earlier journey was made onJune 20th to inaugurate the service, and Atal Behari Vajpayee and SheikhHasina Wajed, the prime ministers of India and Bangladesh, together with thechief minister of West Bengal, Joyti Basu, were present to greet the first arrivals.The bus service is seen as an important step towards the eventual aim ofopening up the countries’ borders to allow multimodal transport connections.

A meeting of transport experts from ten countries was held in Dhaka in lateMay, where it was agreed to set up a trans-Asian railway (TAR). This wouldcomprise a 11,705-km route connecting Yunnan Province of China withTurkey—and passing through Bangladesh and India—by means of interlockingnational tracks. The proposed route would enter Bangladesh from Keranigonjin India, run through Shahbazpur in Sylhet, and re-enter India throughDarshana. The government, which sponsored the four-day conference, wel-comed the development, but the main opposition party, the BangladeshNational Party (BNP), opposed the proposal, as it was seen as a conspiracy bythe government to allow India to use Bangladesh as a corridor.

Bangladesh is set to privatise its national airline, Biman Bangladesh Airlines, byJune next year. According to the civil aviation minister, Mosharraf Hossain, thestate will off-load 49% of its shares through a strategic partnership. Thegovernment is likely to move ahead under a project aided by the World Bank,as this is expected to face less resistance from Biman employees—who havebeen included in all consultations on the privatisation process—than was thecase with earlier proposals. The company has long suffered from various irreg-ularities, with its losses exacerbated by the unauthorised payment of incentivecommissions, unplanned expenditure for sales promotions, and the transportof Bangladeshis deported from abroad. It is felt that the operating conditions ofthe airline must be rationalised before a successful privatisation can proceed.

The Dhaka-Calcuttacommercial bus service

begins

A trans-Asian railwayis proposed

The privatisation ofBangladesh Airlines is

indicated

Bangladesh 23

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Biman Bangladesh Airlines: income and losses(Tk m)

1992/93 1993/94 1994/95 1995/96 1996/97 1997/98

Income 8,805 9,680 10,681 10,764 11,444 12,408

Expenditure –8,126 –9,040 –10,070 –10,541 –12,423 –12,565

Balance 679 639 611 223 –979 –156

Source: Ministry of Finance, Bangladesh Economic Survey 1999.

A Bangladeshi-Malaysian joint-venture company, Sheba Telecom, signed a dealon July 22nd with a Canadian equipment supplier, Telos Engineering, toimprove its rural telecommunications network under the Sheba access project.Sheba Telecom plans to expand its services by a further 42 thanas (villages) insouthern and eastern parts of the country, in addition to the 62 thanas inwhich it already operates, by using wireless local loop technology (WLLT).

GrameenPhone, a subsidiary of Grameen Bank, has signed a deal with adelivery service company, DHL Worldwide Express Bangladesh, under its newcorporate sales package initiative. Under the agreement, DHL couriers will begiven GrameenPhone mobile phones with a short messaging service (SMS) anda voice-mail service (VMS). The company hopes to expand on this initiativeand provide customised packages suiting the needs of larger organisations,including multinational banking and financial institutions.

Money and finance

The government, facing dwindling exports earnings, devalued the taka by2.06% on July 18th. This was the third major downward adjustment of thetaka in the last 13 months and the first in the current fiscal year, which beganon July 1st. Since the current government took over in June 1996, the taka hasbeen devalued by more than 18% against the dollar. The Bangladesh ready-made garments manufacturers and exporters association (BGMEA), whichrepresents the country’s main export-earning sector, had been pressuring for alarge-scale devaluation of the taka for some time, and welcomed the move.Growth in readymade garments exports fell to 12% in 1998/99, from 23% inthe previous year. The appreciation of the taka against its competitors in Asiancountries was the main reason for the slowdown in growth.

However, as the government will buy power from private power companies indollars, the price of power will rise, thereby increasing the cost of productionof manufactured goods. The devaluation was thus seen as a negative step byother manufacturers, who rely on domestic markets for sales. They worry thatthe government has already agreed with donors to increase electricity tariffsand that a rise in tariffs will affect their cost base. The price of electricity wasincreased by Tk0.05/kw in early July and the manufacturers contended that itmight increase again as a result of the devaluation. A rise in utility pricesfollowing the devaluation will also increase inflationary pressures, which willcause problems for many sectors of the economy.

Sheba Telcom strikes a dealwith a Canadian firm

GrameenPhone signs adeal with DHL

The taka has beendevalued again

despite some criticismfrom domestic sectors

24 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

The share price indices of both the Dhaka Stock Exchange (DSE) and theChittagong Stock Exchange (CSE) have moved upwards, reflecting somewhatstronger domestic investor sentiment. On August 2nd the DSE all-share priceindex rose to 529.04 points, from a 63-month low of 462.58 points onMay 3rd. The market capitalisation of the DSE increased to Tk48.28bn ($9.6bn)on August 2nd, compared with Tk42.12bn on May 3rd. The all-share priceindex of the CSE also rose, to 218.25 points on August 2nd, from 201.71 at thebeginning of May. Investor confidence—and hence trading volumes—havebeen subdued since 1996, when the DSE was trading at 3,642 points and themarket crashed.

The recent rise in the stockmarket has been greatly influenced by the increasedrole of the state-owned Investment Corporation of Bangladesh (ICB). Thecompany, which has a large stake in the stockmarket, has been a reluctantplayer since the 1996 crash. However, the government recently ordered thecompany to buy shares from the capital market.

Average stockmarket capitalisation(Tk m)

1991/92 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99a

10,048 12,816 21,700 34,965 48,894 116,590 67,116 48,912

a Up to December 1998.Source: Bangladesh Bank, Economic Trends, May 1999.

The DSE, the largest bourse in the country, banned trading in allotment letterswith effect from August 1st, to combat the menace of fake allotment letterswhich has recently threatened the settlement of share transactions. The banwill apply to all listed companies, but not to new companies, which will enjoythe facility for 100 days, under current Company Law.

The country’s stockmarket watchdogthe Securities and ExchangeCommission (SEC)has been caught in a series of financial and administrativeirregularities. A government audit, released in mid-July, detected gross irreg-ularities in the appointment of several staff, as well as in payments to foreignand local consultants working for the SEC. These are estimated to have resultedin a loss of Tk53m to the government in 1997-98.

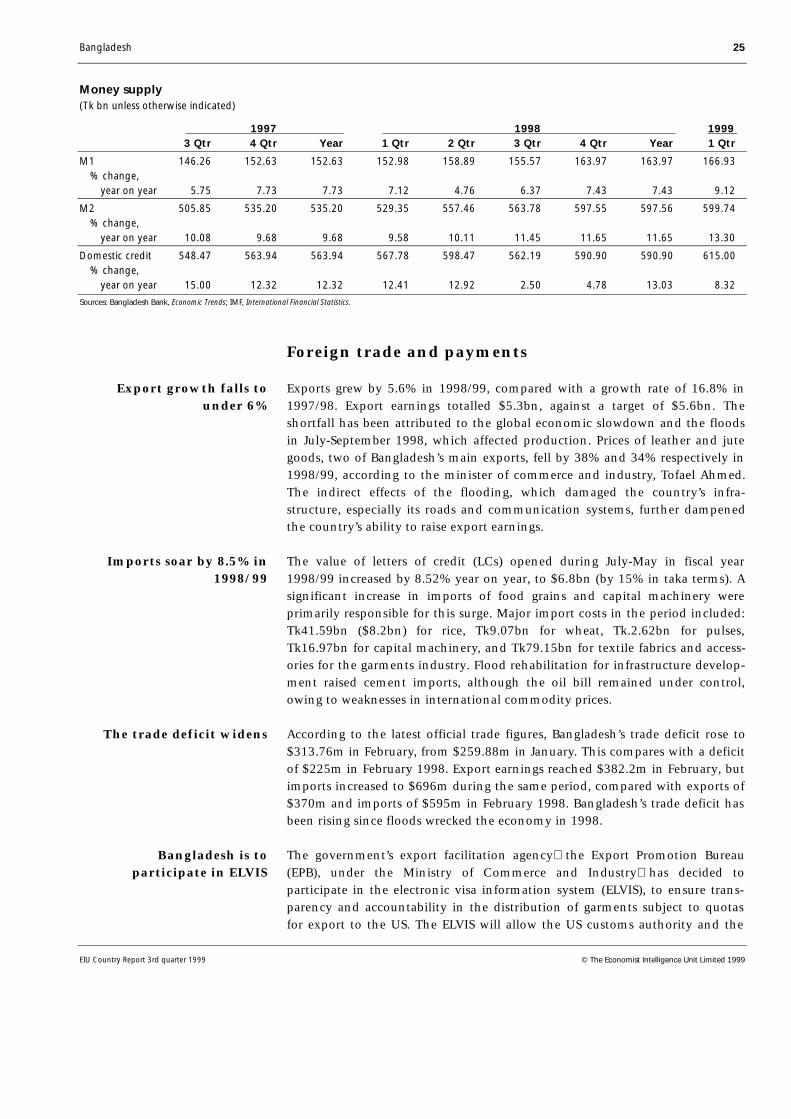

Money supply (M2) rose by 1.05% to Tk599.74bn in March, from Tk593.50 inFebruary. The year-on-year rise was 13%. The supply of M1 increased fromTk164.10bn in February to Tk166.93bn in March, a year-on-year increase of9%. The M2 growth rate has seen a rising trend, in contrast to domestic credit,which has remained below trend since the third quarter of 1998, when thefloods dampened confidence in the economy.

The stockmarket rises

The DSE bans allotment-letter trading

The stockmarket watchdogis in trouble

The money supply has risen

Bangladesh 25

EIU Country Report 3rd quarter 1999 © The Economist Intelligence Unit Limited 1999

Money supply(Tk bn unless otherwise indicated)

1997 1998 1999 3 Qtr 4 Qtr Year 1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr

M1 146.26 152.63 152.63 152.98 158.89 155.57 163.97 163.97 166.93 % change, year on year 5.75 7.73 7.73 7.12 4.76 6.37 7.43 7.43 9.12

M2 505.85 535.20 535.20 529.35 557.46 563.78 597.55 597.56 599.74 % change, year on year 10.08 9.68 9.68 9.58 10.11 11.45 11.65 11.65 13.30

Domestic credit 548.47 563.94 563.94 567.78 598.47 562.19 590.90 590.90 615.00 % change, year on year 15.00 12.32 12.32 12.41 12.92 2.50 4.78 13.03 8.32

Sources: Bangladesh Bank, Economic Trends; IMF, International Financial Statistics.

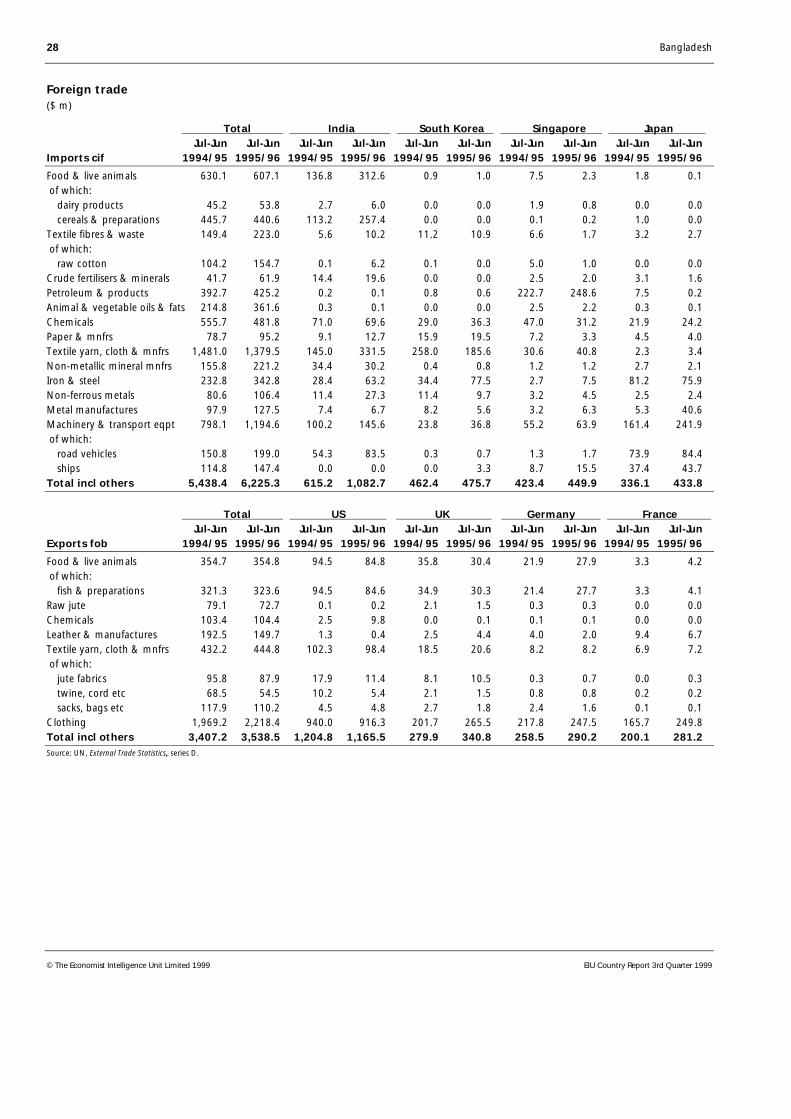

Foreign trade and payments

Exports grew by 5.6% in 1998/99, compared with a growth rate of 16.8% in1997/98. Export earnings totalled $5.3bn, against a target of $5.6bn. Theshortfall has been attributed to the global economic slowdown and the floodsin July-September 1998, which affected production. Prices of leather and jutegoods, two of Bangladesh’s main exports, fell by 38% and 34% respectively in1998/99, according to the minister of commerce and industry, Tofael Ahmed.The indirect effects of the flooding, which damaged the country’s infra-structure, especially its roads and communication systems, further dampenedthe country’s ability to raise export earnings.

The value of letters of credit (LCs) opened during July-May in fiscal year1998/99 increased by 8.52% year on year, to $6.8bn (by 15% in taka terms). Asignificant increase in imports of food grains and capital machinery wereprimarily responsible for this surge. Major import costs in the period included:Tk41.59bn ($8.2bn) for rice, Tk9.07bn for wheat, Tk.2.62bn for pulses,Tk16.97bn for capital machinery, and Tk79.15bn for textile fabrics and access-ories for the garments industry. Flood rehabilitation for infrastructure develop-ment raised cement imports, although the oil bill remained under control,owing to weaknesses in international commodity prices.

According to the latest official trade figures, Bangladesh’s trade deficit rose to$313.76m in February, from $259.88m in January. This compares with a deficitof $225m in February 1998. Export earnings reached $382.2m in February, butimports increased to $696m during the same period, compared with exports of$370m and imports of $595m in February 1998. Bangladesh’s trade deficit hasbeen rising since floods wrecked the economy in 1998.

The government’s export facilitation agencythe Export Promotion Bureau(EPB), under the Ministry of Commerce and Industryhas decided toparticipate in the electronic visa information system (ELVIS), to ensure trans-parency and accountability in the distribution of garments subject to quotasfor export to the US. The ELVIS will allow the US customs authority and the

Export growth falls tounder 6%

Imports soar by 8.5% in1998/99

The trade deficit widens

Bangladesh is toparticipate in ELVIS

26 Bangladesh

© The Economist Intelligence Unit Limited 1999 EIU Country Report 3rd Quarter 1999

Bangladesh authorities to monitor the garments exports quota on a day-to-daybasis. Meanwhile, the EPB has opened a web page to raise publicity forBangladesh exports around the world. The web page also includes detailedinformation on government investment and trade policies, and details offinancial and trade organisations in Bangladesh.

Tourism indicators

1993 1994 1995 1996 1997 1998

Number of tourists 126,785 140,122 156,231 165,887 182,420 171,691

Forex earnings (m taka) 594.4 759.4 955.2 1,401.2 2,741.4 1,993.8a

a January-October.Source: Bangladesh Bureau of Statistics, Monthly Statistical Bulletin, February 1999.

Tourism figures for 1998 indicate that export earnings fell year on year, as thenumber of visitors declined. Both the number of visitors and revenue had beenrising in previous years, and the fall is probably largely the result of a decline invisitors from other parts of Asia, owing to the Asian financial crisis. However,the unstable domestic environment is also dampening the industry; tourismfigures in other countries within the region have begun to recover, suggestingthat the Asian crisis is not Bangladesh’s only problem.

Aid and development

Japan’s Overseas Economic Co-operation Fund (OECF) will provide $47m for abalancing, modernising and renovating (BMRE) programme for the Ghorashalurea fertiliser plant. The BMRE programme aims to save energy, improve thenumber of days the plant is operational from 300 to 330 a year, improveenvironmental controls, replace a 16-mw turbine generator and increase theoperational life of the plant. The OECF will also provide about $3m to con-struct a cooling tower at the Fenchugonj 90-mw combined-cycle power station.