Embed Size (px)

Citation preview

Chateau the Bali (Ungasan) Resort Development Project

Feasibility Review Report

2009.8.17

Strictly Private and Confidential

Stric

tlyPr

iva

tea

nd

Co

nfid

en

tial

Samil PricewaterhouseCoopers is the Korean member firm of PricewaterhouseCoopers. “PricewaterhouseCoopers” refers to the

network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legalentity.

www.samil.comLS Yongsan Tower191 Hangangno 2-ga, Yongsan-guSeoul 140-702, KOREA(Yongsan P.O. Box 266, 140-600)

A member firm of

SAMIL : FG0-09-

TO : PT. Chateau The Bali

Re: Feasibility Review Report August 17, 2009

In accordance with our engagement letter dated June 2009, Samil PricewaterhouseCoopers

have attached our report on the feasibility review of Chateau The Bali project. For this feasibility

study, we have reviewed profitability of the cash flow for the project.

Future cash flows are estimated based on the company’s business plan. We do not provide any

assurance on the results of this estimation. Our work was performed in limited time and based

primarily on information provided by the Company. We accept no responsibility for accuracy of

the information we used. Actual results can be different from shown in this report as

circumstances do not occur as expected.

We make no representation regarding the sufficiency of our work either for purposes for which

this report has been requested or for any other purpose. The sufficiency of the work we

performed is solely the responsibility of the Company. Had we been requested to perform

additional work, additional matters might have come to our attention that would have been

reported to you.

This report is solely for your use in connection with internal decision making with the Chateau

The Bali Pool Villa Resort Development Project, and it is not to be used for any other purpose or

to be copied or distributed or otherwise made available or referred to, in whole or in part, to any

other party without our prior written consent. We do not accept any liability or responsibility to

any third party to whom our report is shown or into whose hands it may come (Except for the

related third party, set out in our engagement).

[DC2]

Should you require clarification of any of the matters contained in our report, please contact

CPA & Partner Seo, Jun-sub (TEL: 02- 709-0758).

Sincerely yours,

Samil PricewaterhouseCoopers

Strictly Private and Confidential

1

[DC2]

Table of Content

Page

Ⅰ. Work Scope & Limitation···················································································2

Ⅱ. Project Status·····································································································3

1. Project Overview ···················································································································3

2. Project Site ··························································································································12

3. SWOT Analysis····················································································································13

4. Developer of the Project ······································································································15

5. Appraised Value of the Related Land/Building of the Project··············································16

6. Presale Plan ························································································································17

Ⅲ. Market Status and Outlook ··············································································26

1. Indonesia’s Economy ··········································································································26

2. Tourism Status of Bali ··········································································································28

3. Analysis of Similar Resorts ··································································································31

Ⅳ. Income & Cash Flow Analysis·········································································35

1. Presale Estimation···············································································································35

2. Estimation of Revenue from Room Sales ···········································································37

3. Estimation of Operating Expense························································································40

4. Operating Cash Flow Estimation·························································································45

5. Cumulative Cash Flow Projection ·······················································································49

Ⅴ. Risk Factors and Solutions for the Project ····················································52

Strictly Private and Confidential

2

[DC2]

Ⅰ. Work Scope & Limitation

This review was performed based primarily on information provided by the Company and the

disclosed data from international and local research institutions, including securities

companies. We were not engaged to test the accuracy or reasonableness of the data we used,

and we do not accept responsibility for such information. Moreover, we do not accept any

responsibility of inaccurate valuation results caused from inaccurate data.

We performed this review based on the agreed upon procedures with the disclosed information

from international and local research institutions, including securities companies, governments,

and the historical data of the Company. Please note that the estimation performed in this report

is based on the assumptions. Because events and circumstances frequently do not occur as

expected, there might be differences between predicted and actual results, and those

differences may be material. Also, please note that our report is dependent on the continuing

validity of the assumptions on which it is based.

Valuation is solely performed based on the information of the Company, the target company

information from the Company, and disclosed information from the local and international

financial and research institutions. Moreover, as of the date that the review was performed, the

hotel and pool villa resort development project has NOT been executed, and this review was

performed based on the assumption that the project will take place as it has been planned.

Please note that if there are any changes in the business plan, the estimated values can be

materially different from the ones in this report.

This report is solely for your use in connection with internal decision making, and it is not to be

used for any other purpose or to be copied or distributed or otherwise made available or

referred to, in whole or in part, to any other party without our prior written consent. We do not

accept any liability or responsibility to any third party to whom our report is shown or into whose

hands it may come (Except for the related third party, set out in our engagement).

Strictly Private and Confidential

3

[DC2]

Ⅱ. Project Status

1. Project Overview

The resort will be constructed and presold with the goal of becoming the most luxurious pool

villa resort in Bali with Therapy-oriented Spa and 96 units of high-end private pool villas.

The resort will be comprised of various facilities, including Therapy Spa, Business Centers,

Restaurants, a Putting Ground, and an Aqua Gym. The resort will be the first therapy spa-

oriented resort in Indonesia

General overview of the project is as follows.

[Table] Project Overview

Type Content

Location Jl. Pura Masuka Tunjung Br. Kertha Lestari Kuta Selatan Badung, Bali, 80363

Indonesia(20 minutes from Denpasar airport, 30 minites from Kuta

downtown)

Total Area 78,540㎡

Rooms - 96 Units of Therapy Spa-oriented Private Pool Villa

Type Room Type Number of Units

1 BED 45 Units

2 BED 7 Units

3 BED 42 UnitsPOOL VILLA

4 BED 2 Units

Total 96 Units

Other

Facilities

Business Center, Restaurant, Therapy Spa, Mega size Pool, Kids Pool,

Promenade, Putting Ground, Medical facilities, Aqua Gym, Private Beach,

Tennis Court, Wine Cave, Bar, Private Pool, and Private Sauna

Note - Grand Opening in Oct. 2009

- Pre-opening(Preparation of Grand Opening) in Aug. 2009

[Source] The Company’s Business Plan

Strictly Private and Confidential

4

[DC2]

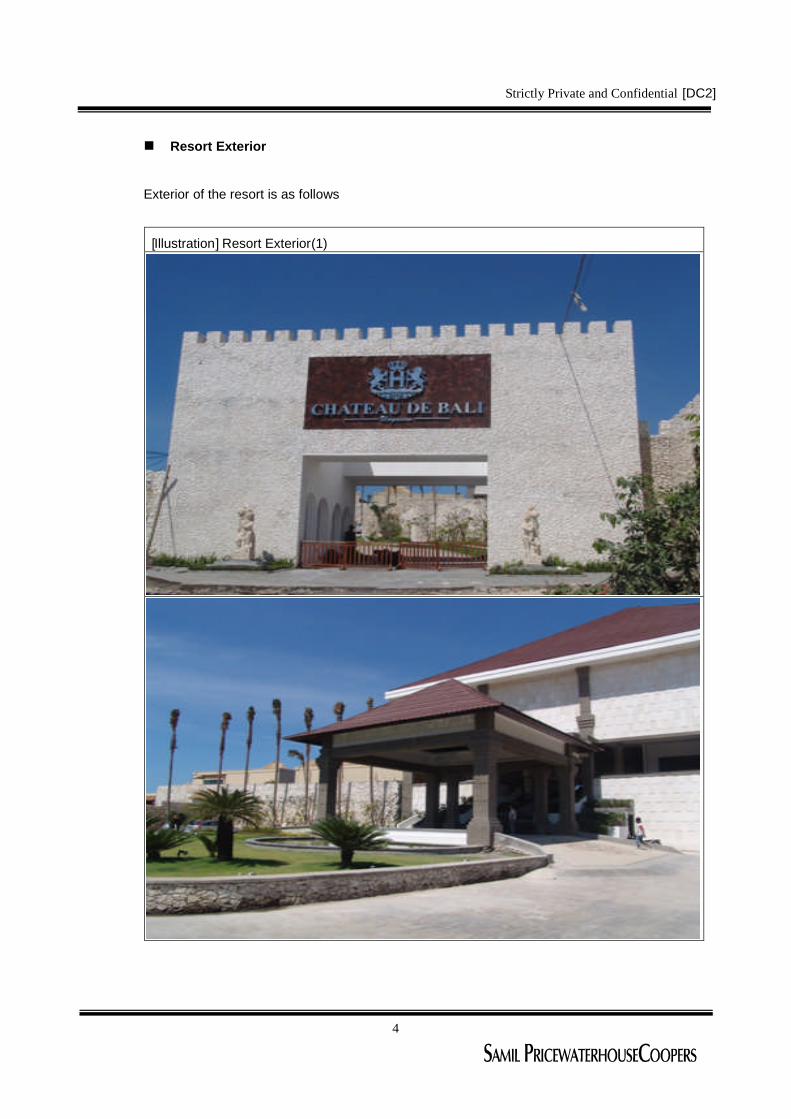

Resort Exterior

Exterior of the resort is as follows

[Illustration] Resort Exterior(1)

Strictly Private and Confidential

5

[DC2]

[Illustration] Resort Exterior(2)

Strictly Private and Confidential

6

[DC2]

[Illustration] Resort Exterior(3)

Strictly Private and Confidential

7

[DC2]

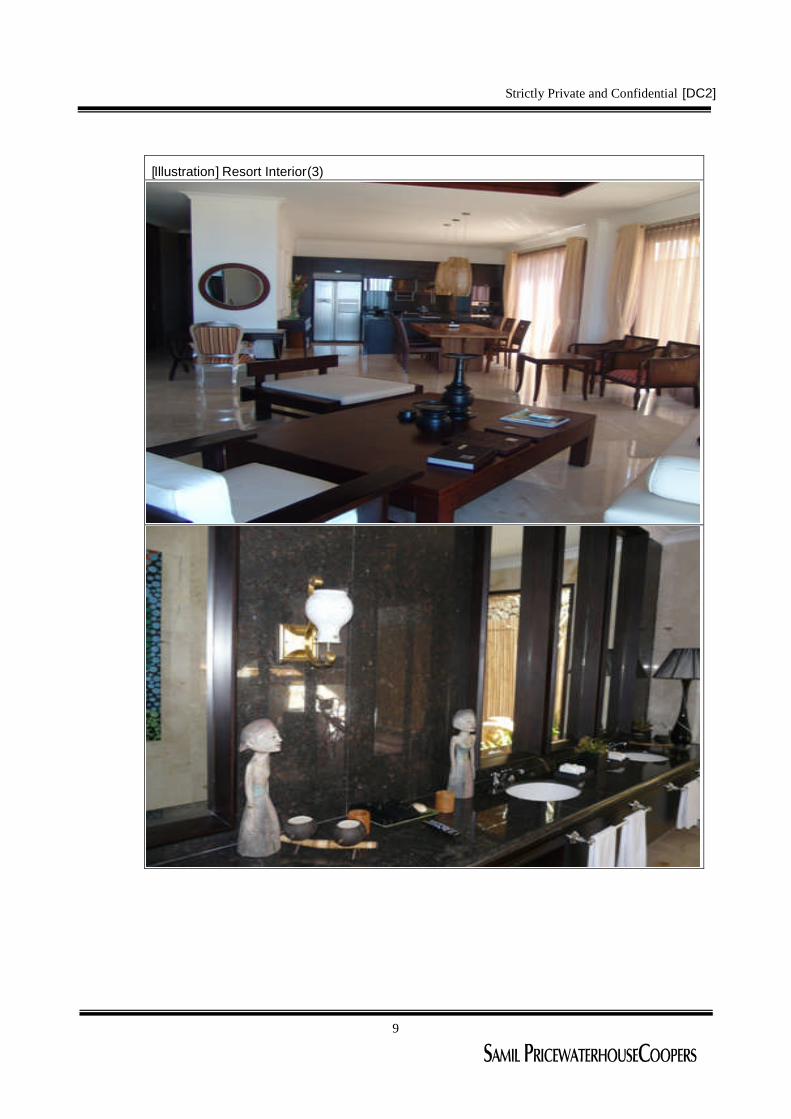

Resort Interior

Interior of the resort is as follows

[Illustration] Resort Interior(1)

Strictly Private and Confidential

8

[DC2]

[Illustration] Resort Interior(2)

Strictly Private and Confidential

9

[DC2]

[Illustration] Resort Interior(3)

Strictly Private and Confidential

10

[DC2]

Unit Exterior

Exterior of the unit is as follows.

[Illustration] Unit Exterior(1)

Strictly Private and Confidential

11

[DC2]

[Illustration] Unit Exterior(2)

Strictly Private and Confidential

12

[DC2]

2. Project Site

Bali, where the project site is located, is called as ‘The Last World of God’(aka. The Paradise

of Earth) as it possesses intact nature, and it is located south of Java Sea, north of Indian

Ocean, and is on the boarder of Lombok.

The area of Bali is 563,286km, and the population of 3.15 million resides (mostly working in

tourism and farming industry) in the island. Bali has the best weather for young people who

enjoy marine sports and old generation who prefer relaxation as it has both dry and raining

seasons and has relatively small amount of annual rainfall. Indonesian government developed

and is still developing the whole island as the tourists’site, and recently various types of villas

are developed. Moreover, almost all airlines from the world travel to Bali island, providing easy

accessibility for all generation from everywhere.

Site Analysis

The project site (Ungasan) is located in the southern Bali and is about 20 minutes away from

Denpasar Airport, and has easy accessibility (20 minutes) from Kuta downtown.

As Ungasan possesses beautiful sceneries, world-class resorts, such as Karma and Banyan

Tree, are developing their resorts in this region. Moreover, Bali is constructing a circular road

and the value of the real estate in the area continues to increase, making this area as the best

investment option.

Furthermore, as all villa units are constructed at the sea level of 70m and 1.26 km away from

the Indian Ocean in a staircase form, beautiful sea and sceneries can be experienced.

Strictly Private and Confidential

13

[DC2]

Geographical location for the project is as follows.

[Illustration] Project Site

3. SWOT Analysis

SWOT Analysis of the Project Site is as follows.

Strengths

The Biggest in Size + The Most Luxurious Facility + The Best Service

As the resort is managed by Korean, it can satisfy the needs of Korean Customers

Possesses the Know-How of managing Pool Villa as Dreamland Pool Villa resort was and

still is managing by the same management

The region is famous for new luxurious pool villa complex (Chateau the Bali, Karma,

Banyan Tree, etc)

Weaknesses

Low Brand Recognition as it is relative new

Too many hotels in Bali

Instability of the real estate market in Indonesia

Opportunities

Strictly Private and Confidential

14

[DC2]

Bali is considered as one of the Best Resting Place

Increased demand of high-end pool villas

Rapidly increasing pool villa demands from Korean tourists

Continuous interests from Japanese and Australia tourists

Increased number of Korean flights to Bali

Stricter restriction of Hotels in Bali (Higher Barrier of Entry in Hotel Industry)

Threats

Lack of Pool Villa awareness in Korea

Low Hotel rate from old and less luxurious hotels

Reduced number of tourists due to the economy

The Company plans to take following actions to minimize the effects from its Weaknesses and

Threats from the SWOT analysis.

Action Plan for Weaknesses

Introduce well-known brands

Appoint global marketing & presale agencies

Contract Long term lease with the condition of transferring the land ownership when it is

allowed to foreigner

Action Plan for Threats

Plans to expand the target market from Korea to worldwide

Plans to target high-end market

Develop luxurious facilities and its operating programs

Strictly Private and Confidential

15

[DC2]

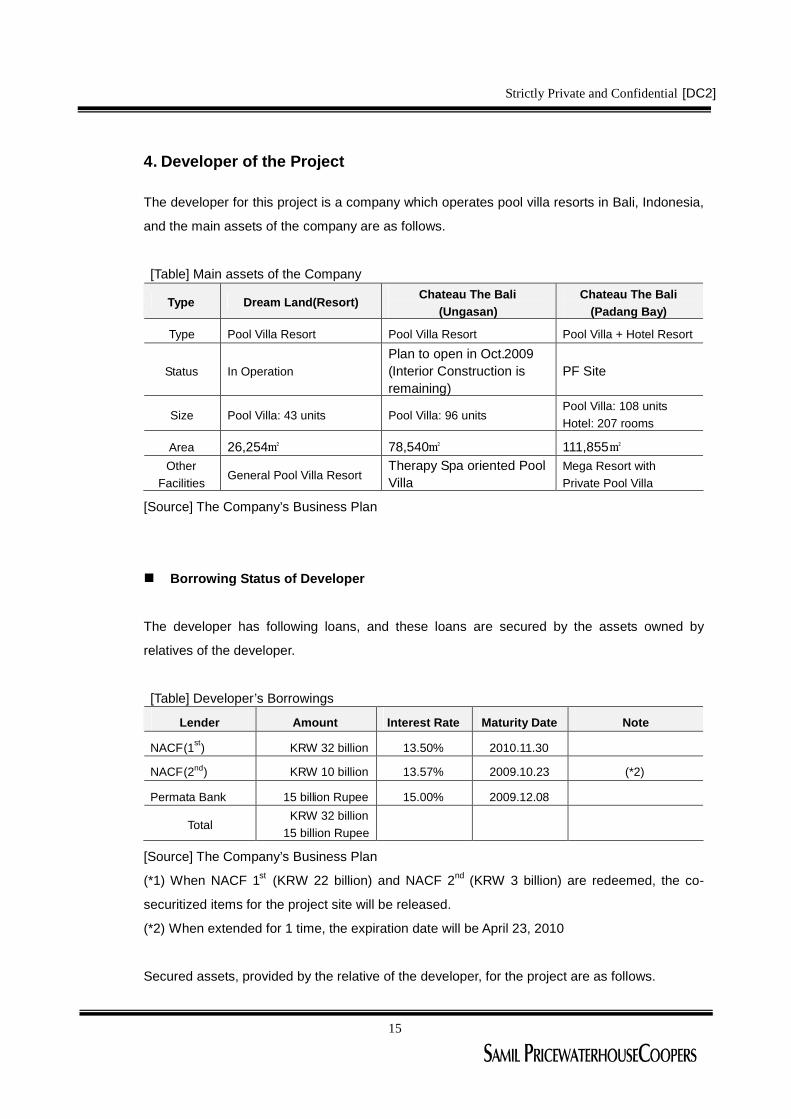

4. Developer of the Project

The developer for this project is a company which operates pool villa resorts in Bali, Indonesia,

and the main assets of the company are as follows.

[Table] Main assets of the Company

Type Dream Land(Resort)Chateau The Bali

(Ungasan)Chateau The Bali

(Padang Bay)

Type Pool Villa Resort Pool Villa Resort Pool Villa + Hotel Resort

Status In OperationPlan to open in Oct.2009(Interior Construction isremaining)

PF Site

Size Pool Villa: 43 units Pool Villa: 96 unitsPool Villa: 108 unitsHotel: 207 rooms

Area 26,254㎡ 78,540㎡ 111,855㎡Other

FacilitiesGeneral Pool Villa Resort

Therapy Spa oriented PoolVilla

Mega Resort withPrivate Pool Villa

[Source] The Company’s Business Plan

Borrowing Status of Developer

The developer has following loans, and these loans are secured by the assets owned by

relatives of the developer.

[Table] Developer’s Borrowings

Lender Amount Interest Rate Maturity Date Note

NACF(1st) KRW 32 billion 13.50% 2010.11.30

NACF(2nd) KRW 10 billion 13.57% 2009.10.23 (*2)

Permata Bank 15 billion Rupee 15.00% 2009.12.08

TotalKRW 32 billion

15 billion Rupee

[Source] The Company’s Business Plan

(*1) When NACF 1st (KRW 22 billion) and NACF 2nd (KRW 3 billion) are redeemed, the co-

securitized items for the project site will be released.

(*2) When extended for 1 time, the expiration date will be April 23, 2010

Secured assets, provided by the relative of the developer, for the project are as follows.

Strictly Private and Confidential

16

[DC2]

[Table] Secured AssetsSecured Assets Provider(*1) Borrowing

AmountLender Note

Project Site(Padang Bay)

Nyoman Sedana 6 lots

Furniture Factory 1 PT. SEAWON CorpRelated Party with

Developer

Furniture Factory 2 PT. Korin Istana CorpRelated Party with

Developer

Other Land(Ungasan)

Nyoman Sedana

KRW 32 billion NACF

7 lots

Dreamland (Resort)Kadek Eraniti and 2others KRW 10 billion NACF

Land (Nusa Dua) Kadek Eraniti 4 lots

Land (Dreamland) Nyoman Sedana 1 lots

Land (Ungasan) Nyoman Sedana

15 billion RupeePermata

Bank2 lots

[Source] The Company’s Business Plan

(*) All secured assets are owned by the developer’s wife and relatives.

5. Appraised Value of the Related Land/Building of the Project

The appraised values of the assets of the Company for this project are as follows.

[Table] Appraised Value (in thousands of USD, except otherwise noted)

Secured Asset AppraisalDate

AppraisedValue

Appraiser Note

2008-09-10 24,000 hari utomo & rekanLoan from Bank for

IPODreamlandResort

2009-04-07KRW 25

billionKaram DongkukAppraiser

When fundingNACF1st fund 10 bil(Request Financial

Lender)

2009-04-16 74,568 CBRE/KJPP YUHALWhen Sold to

Geecoinc(Request to Buyer)

2009-05-00 70,000Mirae & SaehanAppraiser

"Chateau The Bali(Ungasan)

2008-09-10 82,000 hari utomo & rekanLoan from Bank for

IPO

Project Site(Padang Bay)

2009-06-26 39,203(*1) hari utomo & rekan "

Strictly Private and Confidential

17

[DC2]

(Source) Appraisal Report from Appraiser

(*1) The median value of the exchange rate of 2009.5.31 by the central bank of Indonesia was

applied (Selling Rate: 10,392 rupee/USD, Buying Rate: 10,288 rupee/USD, Median Rate:

10,340 rupee/USD).

.

6. Presale Plan

1) Presale Plan

Except for the hotel, all rooms, including Pool Villa, will be presold to Koreans and foreign

investors, and the detail presale plan is as follows.

Presale Plan: Koreans

Presale agency contract will be signed with Geecoinc, a foreign-oriented real estate agency in

Korea, and it will perform marketing activities, including advertisings, presentations, and

conferences, targeting VVIP in Korea.

Presale Plan: Foreign Investors

The presale plan will be prepared based on the nations.

Indonesia: Plans to collaborate with Exotiq, an Indonesian agency, targeting wealthy

Indonesians and foreigners who reside in Indonesia

Japan: Plans to proceed the presale by collaborating with local travel and real estate

agencies in Osaka and Nagoya

Russia & Kazakhstan, etc: Plans to proceed the presale by allocating units to Absolte, a

Kazakhstan agency, and Bali Villa Bella, a Russian agency

Singapore & Hong Kong, etc: Plans to proceed the presale by signing sales contract with

Savills, a Singapore agency, and Midland, a Hong Kong agency, targeting wealthy

individuals in Southeast Asia and Europe

Strictly Private and Confidential

18

[DC2]

[Table] Presale County & Agency

Country Presale Agency

Korea Geecoinc

Indonesia Exotiq

Japan Travel & Real Estate Agencies in Osaka &Nagoya

CIS – Kazakhstan, etc Absolute

Russia Bali Villa Bella

Singapore Savills

Foreign

Hong Kong Midland

(Source) The Company’s Business Plan

2) Presale Value

The Pool Villa will be presold at the following rates.

[Table] Expected Presale Value of Pool Villa by Room type (in USD)Size

Room TypeLand Building(*1)

# of UnitPresaleValue

PresaleAmount

4 Bedroom 1,400.00㎡ 865.76㎡ 1 3,420,000 3,420,000

1,050.00㎡ 678.21㎡ 1 2,680,000 2,680,000

4 Bedroom - Subtotal 2 6,100,000

3 Bedroom 810.00㎡ 522.61㎡ 8 1,980,000 15,840,000

690.00㎡ 522.61㎡ 6 1,830,000 10,980,000

600.00㎡ 473.66㎡ 22 1,580,000 34,760,000

440.00㎡ 323.94㎡ 2 1,180,000 2,360,000

420.00㎡ 322.38㎡ 3 1,080,000 3,240,000

400.00㎡ 307.53㎡ 1 1,030,000 1,030,000

3 Bedroom – Subtotal 42 68,210,000

2 Bedroom 400.00㎡ 307.53㎡ 7 990,000 6,930,000

2 Bedroom – Subtotal 7 6,930,000

1 Bedroom 280.00㎡ 183.12㎡ 34 550,000 18,700,000

266.00㎡ 183.12㎡ 11 530,000 5,830,000

1 Bedroom – Subtotal 45 24,530,000

Total 96 105,770,000

Strictly Private and Confidential

19

[DC2]

(Source) The Company’s Business Plan

(*1) Areas of other facilities are included in the building size in accordance with Indonesian

regulation.

The presale values for Chateau The Bali (Ungasan) are little lower than the similar resorts in

the market. However, as the location and facilities of the Chateau The Bali (Ungasan) is more

advanced and better than the ones nearby, it is reasonable to believe that the units can be

presold at the value that the Company provided.

Above presale value can be compared with competitors’ in near site as follows. C151 3

Bedroom was sold at USD 550,000 in 2006, and it was traded at USD 700,000 in 2008.

Moreover, two units of One Bedroom and one unit of Two Bedroom in Chateau The Bali

(Ungasan) were presold at USD 550,000 and USD 750,000 in 2008, respectively. Presale of

these units to Korean investors was suspended as exchange rate fluctuation was extreme in

the 2H of 2008.

3) Presale Value Comparison with Similar Facilities

Banyan Tree

The presale value per land area of Banyan Tree is 35%~98% higher than the Chateau the Bali,

and the presale value per constructed area (㎡) is 74%~124% higher than the Chateau the Bali.

[Table] Banyan Tree Presale Value

Area(㎡) Presale Valueper ㎡ (US$)

PresalePeriod Type

Land Building

PresaleValue(US$) Land Building

1 Bed 403㎡ 239㎡ 1,236,568 3,068 5,174

2 Bed 565㎡ 315㎡ 1,886,909 3,340 5,9902007.02

3 Bed 1,200㎡ 680㎡ 4,333,333 3,611 6,373

1 Bed 403㎡ 239㎡ 1,593,500 3,954 6,667

2 Bed 565㎡ 315㎡ 2,121,000 3,754 6,7332009.08

3 Bed 1,200㎡ 680㎡ 4,600,000 3,833 6,765

Strictly Private and Confidential

20

[DC2]

Karma Kandara

Karma Kandara is partially operating (still in construction phase), and they do not have 1 Bed

and 2 Bed units. Also, Karma Kandara does not disclose presale information on 4 Bed

(Construction area: 358㎡) and 5 Bed(Construction area 822㎡) units.

[Table] Karma Kandara Presale Value

Area(㎡) Presale Valueper ㎡ (US$)

PresalePeriod Type

Land Building

PresaleValue(US$) Land Building

2007.02 3 Bed - 328㎡ 907,000 - 2,765

2009.08 3 Bed - 328㎡ 1,200,000 - 3,659

LivBali

The presale value per land area of LivBali is 35%~41% lower than the Chateau the Bali, and

the presale value per constructed area (㎡) is 24%~54% lower than the Chateau the Bali.

[Table] LivBali Presale Value

Area(㎡)Presale Valueper ㎡ (US$)Presale

PeriodType

Land Building

PresaleValue(US$) Land Building

1 Bed 270㎡ 257㎡ 350,000 1,296 1,362

2 Bed 353㎡ 218㎡ 530,000 1,501 2,4312009.09

3 Bed 435㎡ 305㎡ 670,000 1,540 2,197

Rama Chandra Villa

The presale value per land area of Rama Chandra Villa is 14%~138% higher than the Chateau

the Bali, and the presale value per constructed area (㎡) is 97% higher than the Chateau the

Bali.

Strictly Private and Confidential

21

[DC2]

[Table] Rama Chandra Villa Value

Area(㎡) Presale Valueper ㎡ (US$)

PresalePeriod Type

Land Building

PresaleValue(US$) Land Building

2 Bed 390㎡ 368㎡ 1,100,000 2,821 2,989

3 Bed 566㎡ 419㎡ 2,850,000 5,035 6,802NA

4 Bed 591㎡ 527㎡ 3,500,000 5,922 6,641

4) Presale Condition

Presale Condition for the Pool Villa is as follows.

[Table] Presale Condition

Type Presale Condition

Location Ungasan, Bali

Opening Date Oct. 2009

Construction 92% Completed

Payment Schedule for

Presale

Signing : USD 5,000

Contract date: 30% / Within one month from signing date

1st installment : 30% / Within one month from contract date

2nd installment : 30% / Within one month from 1st installment

Remaining : 10% / Within one month from 2nd installment

Operating Profit

Distribution Condition

8% of designated profit for 2 years

Distributes 40% of profits from Room Sales

21 days free accommodation for a year (Apply to Dreamland

and Padang Bay Resort)

Owner Ship Type One of below three options

HGM(PMA)

SHM(nominee)

Long term lease(Maximum period: 80 years)

* Ownership will be transferred when owning the land by foreigners

is allowed.

Maintenance Fee $25 x Villa unit ㎡ (Year) -> Water & Electricity included

Note 96unit are planed to be presold / Presale Completed: 3unit (3%)

(Source) The Company’s Business Plan

Strictly Private and Confidential

22

[DC2]

Presale condition comparison with similar facilities in near site is as follows.

Banyan Tree

[Table] Banyan Tree Presale Condition

Type Presale Condition

Location Ungasan, Bali

Opening Date Nov. 2009

Construction 90% Completed, Pavement and Interior remaining

Started construction in Feb. 2007

Payment Schedule for

Presale

Signing : USD 10,000

Contract : 30% / Within one month from signing date

1st Installment : 30% / Within one month from contract date

2nd Installment : 30% / Within one month from 1st installment

Remaining : 10% / Within one month from 2nd installment

* If paid in full when contracting, the signing will be returned

Operating Profit

Distribution Condition

8% of designated profit for 2 years

Distributes 40% of profits from Room Sales

21 days free accommodation for a year (Apply to all Banyan

Tree resort)

Ownership Type One of below three options

HGB(PMA)

SHM(nominee)

Long term lease(50yrs)

Maintenance Fee Maintenance fee : X

sink fund: $2 x Villa Building Area(Monthly)

Note 50units out of 73 units are planned to be presold / Presale

completed: 30unit (60%)

(Source) Presale Catalog of Banyan Tree

Strictly Private and Confidential

23

[DC2]

Karma Kandara

[Table] Karma Kandara Presale Condition

Type Presale Condition

Location Ungasan, Bali

Opening Date March 2008

Construction In Operation (20units are in construction: 85% completed)

Payment Schedule for

Presale

Signing : USD 10,000

Contract : 30% / Within one month from signing date

1st Installment : 30% / Within one month from contract date

2nd Installment : 30% / Within one month from 1st installment

Remaining : 10% / Within one month from 2nd installment

Operating Profit

Distribution Condition

5% of designated profit for 2 years

Distributes 40% of profits from Room Sales

28 days free accommodation for a year (Apply to all Karma

resorts)

Ownership Type One of below three options

HGB(PMA)

SHM(nominee)

Long term lease(50yrs)

Maintenance Fee Maintenance fee : USD 7,600 (Year)

Note 45 out of 46 units are presold 45unit (97%)

(Source) Presale Catalog of Karma Kandara

Strictly Private and Confidential

24

[DC2]

LivBali

[Table] LivBali Presale Condition

Type Presale Condition

Location Jimbaran, Bali

Opening Date Dec 2009

Construction 80% completed

Payment Schedule for

Presale

Signing : USD 6,000

Contract : 30% / Within one month from signing date

1st Installment : 30% / When construction is 30% completed

2nd Installment : 30% / When construction is 60% completed

Remaining : 10% / When construction is completed

Operating Profit

Distribution Condition

Distributes 40% of profits from Room Sales

21 days free accommodation for a year

Ownership Type One of below three options

HGB(PMA)

SHM(nominee)

Long term lease(50yrs)

Maintenance Fee Maintenance fee : USD 4,000 (Year)

Note 23 out of 28 units are presold (82%)

(Source) Presale Catalog of LivBali

Strictly Private and Confidential

25

[DC2]

Rama Chandra Villa

[Table] Rama Chandra Villa Presale Condition

Type Presale Condition

Location Ungasan, Bali

Opening Date TBD

Construction -

Payment Schedule for

Presale

Signing: USD 10,000

Contract : 30% / When Contracted

1st Installment : 20% / 2 month from the contract date and when

30% construction is completed

2nd Installment : 20% / Within 2 month from the 1st installment

and when 50% construction is completed

3rd Installment: 20% / Within 2 month from the 2nd installment

and when 70% construction is completed

4th Installment : 7% / When Construction is completed and when

move in

Remaining : 3% / Within 12 months from move in date

Operating Profit

Distribution Condition

Distributes 40% of profits from Room Sales

Ownership Type One of below three options

HGB(PMA)

SHM(nominee)

Long term lease(50yrs)

Maintenance Fee -

Note 23 out of 40 units are presold (58%)

(Source) Presale Catalog of Rama Chandra Villa

Strictly Private and Confidential

26

[DC2]

Ⅲ. Market Status and Outlook

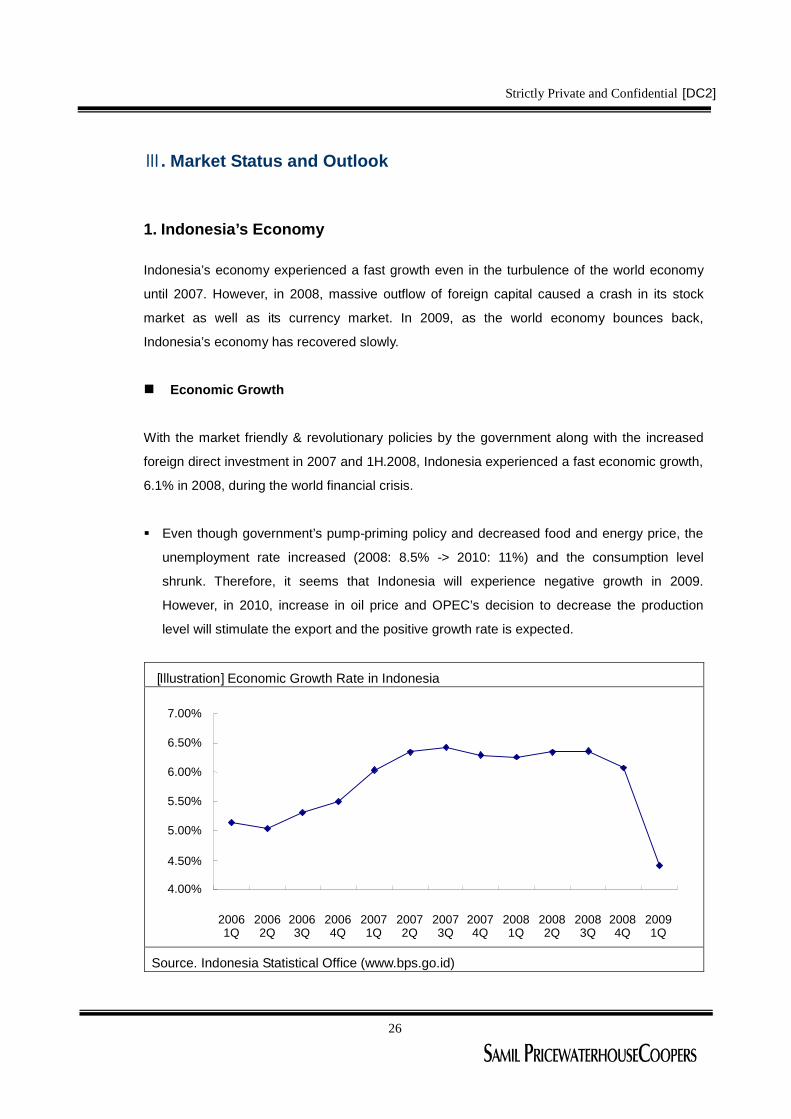

1. Indonesia’s Economy

Indonesia’s economy experienced a fast growth even in the turbulence of the world economy

until 2007. However, in 2008, massive outflow of foreign capital caused a crash in its stock

market as well as its currency market. In 2009, as the world economy bounces back,

Indonesia’s economy has recovered slowly.

Economic Growth

With the market friendly & revolutionary policies by the government along with the increased

foreign direct investment in 2007 and 1H.2008, Indonesia experienced a fast economic growth,

6.1% in 2008, during the world financial crisis.

Even though government’s pump-priming policy and decreased food and energy price, the

unemployment rate increased (2008: 8.5% -> 2010: 11%) and the consumption level

shrunk. Therefore, it seems that Indonesia will experience negative growth in 2009.

However, in 2010, increase in oil price and OPEC’s decision to decrease the production

level will stimulate the export and the positive growth rate is expected.

[Illustration] Economic Growth Rate in Indonesia

Source. Indonesia Statistical Office (www.bps.go.id)

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

7.00%

20061Q

20062Q

20063Q

20064Q

20071Q

20072Q

20073Q

20074Q

20081Q

20082Q

20083Q

20084Q

20091Q

Strictly Private and Confidential

27

[DC2]

Interest

BI(Bank Indonesia), the central bank of Indonesia, lowered its interest rate since November,

2008 from 9.5% to 7.25% in May, 2009. This indicates BI’s confidence in reaching the inflation

goal of 5~7% and its intention to improve liquidity.

Indonesia focuses on the economic growth rather than controlling inflation. Therefore, further

decrease in interest rate is expected.

[Illustration] Changes in Interest rate in Indonesia

Source. Central Bank of Indonesia (www.bi.go.id)

Inflation

As price of raw materials, such as grocery, oil, and mineral, skyrocketed, the consumer price

level rose to 10.1, 60% increase from the prior year. The consumer price level is expected to

decrease as the international raw material prices and domestic consumption rates are

decreasing.

As international oil price decreases, government decreased the support for oil related

goods. In April, the annual average CPI was 6%, the lowest for the past 16 months.

As Rupee is appreciated since mid 2008, the increased price of imported goods is

expected, which will lead to the inflation.

6.00%

7.00%

8.00%

9.00%

10.00%

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6

2008 2009

Strictly Private and Confidential

28

[DC2]

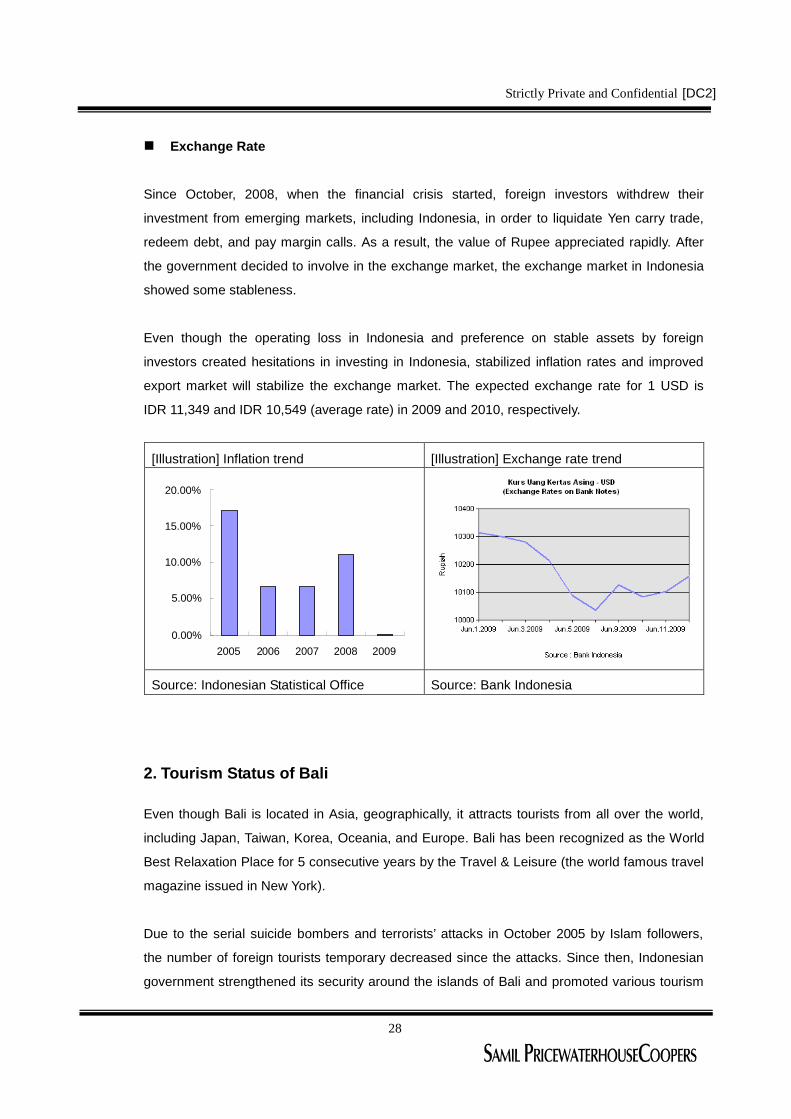

Exchange Rate

Since October, 2008, when the financial crisis started, foreign investors withdrew their

investment from emerging markets, including Indonesia, in order to liquidate Yen carry trade,

redeem debt, and pay margin calls. As a result, the value of Rupee appreciated rapidly. After

the government decided to involve in the exchange market, the exchange market in Indonesia

showed some stableness.

Even though the operating loss in Indonesia and preference on stable assets by foreign

investors created hesitations in investing in Indonesia, stabilized inflation rates and improved

export market will stabilize the exchange market. The expected exchange rate for 1 USD is

IDR 11,349 and IDR 10,549 (average rate) in 2009 and 2010, respectively.

[Illustration] Inflation trend [Illustration] Exchange rate trend

Source: Indonesian Statistical Office Source: Bank Indonesia

2. Tourism Status of Bali

Even though Bali is located in Asia, geographically, it attracts tourists from all over the world,

including Japan, Taiwan, Korea, Oceania, and Europe. Bali has been recognized as the World

Best Relaxation Place for 5 consecutive years by the Travel & Leisure (the world famous travel

magazine issued in New York).

Due to the serial suicide bombers and terrorists’attacks in October 2005 by Islam followers,

the number of foreign tourists temporary decreased since the attacks. Since then, Indonesian

government strengthened its security around the islands of Bali and promoted various tourism

0.00%

5.00%

10.00%

15.00%

20.00%

2005 2006 2007 2008 2009

Strictly Private and Confidential

29

[DC2]

programs, and these efforts led to continuous increase in number of tourists.

In April, 2009, Bali hosted the most foreign tourists in its history with 178,879 visitors, 21.94%

increased number compare to April, 2008 (147,515 individuals). Cumulated foreign visitors until

April, 2009, is 645,061, increasing 8.15% from prior period (596,469).

[Illustration] Foreign Tourist Arrivals to Bali

Source: www.balidiscovery.com

Analyzing visitors by nations, tourists from Australia ranked 1st in 2009, followed by Japan.

During the first four months of 2009, total 102,179 visitors from Australia toured Bali, increasing

30.08% compare to 2008. On the other side, for Japanese tourists, the increased rate compare

to prior year was only 7.45%, giving up the number one ranking to Australia.

For Korea, it was maintaining its ranking, 3rd, for a long period, however, the number of tourists

in 2009 decreased by 5.62% compared to prior period, and the ranking fell to 5th. Also, for

Taiwan, the ranking fell to 7th in 2009, after maintaining its ranking at 4th for a long period.

Tourists Increased Nations

The nations that sent more tourists to Bali than the past during the first four months of 2009 are

as follows: Australia (+30.08%), China (+54.03), Malaysia (+37.70%). Russia (+4.75%),

Netherlands (+0.42%), France (+25.32%).

-

50,000

100,000

150,000

200,000

Jan Feb Mar Apr

2009

2008

Strictly Private and Confidential

30

[DC2]

Tourists Decreased Nations

The nations that sent less tourists to Bali than the past during the first four months of 2009 are

as follows: Japan (-7.45%), Thailand (-23.24%), Korea (-5.62%), USA (-1.80%), Germany(-

11.66%), England (-6.50%).

[ Illustration] Top Bali Markets Jan-Apr 2008 vs 2009

Source. www.balidiscovery.com

Average stay length for foreign visitors who travel Bali is about 3.75 days. Statistically,

domestic tourists travel longer than foreign visitors as tourists from Indonesia stay at Bali for

around 4.29 days.

Visitors from Indonesia usually stay longer period at Badung, Gianyar and Denpasar regions,

and foreign tourists stay longer period at Tabanan, Karangasem and Buleleng regions than

domestic travelers.

Stay length of the tourists is directly related to the hotel occupancy rates. In March, 2009, the

hotel occupancy rate was 57.72%, which has been increased from the prior month (50.99%).

The hotels in Denpasar region has the better occupancy rates than the average with 62.49%,

whereas, the occupancy rate for the hotels in Karangasem region was only 34.35%.

As per balidiscovery.com, the number of foreign tourists in March, 2009, was 161,169,

increased by 4.7% from prior period. In April 2009, the number of foreign tourists increased by

21.94% with 178,879 individuals, indicating the increasing trend of the foreign visitors.

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

JapanAustralia

ThailandKorea

ChinaMalaysia

RussiaNetherlands

FranceUSA

GermanyEngland

2008

2009

Strictly Private and Confidential

31

[DC2]

3. Analysis of Similar Resorts

The resort will be developed on the land of 78,540㎡ with therapy-oriented Spa and 96 units of

private pool villa. This development is considered as the mega project in Bali..

This resort is expected to compete with mega brand villas, such as Banyan Tree and Karma,

as well as smaller villas. As per the company’s official, this resort has relative lower brand

recognition and costumer loyalty, but its easy accesilibility (30 minutes from airport, near

central tourism area, near golf course), will attract tourists. Also, Banyan Tree Pool Villa and

Karma Pool Villa are located near site and it possesses beautiful scenery as it is located on the

cliff side. Furthermore, the rate of this resort, which is relatively lower than famous branded

resorts and its know-how in managing Dreamland and Blue Ocean Bali Resort will help

obtaining competitiveness.

Following is the information of the Pool Villa & Hotel located in near the project site.

Karma Kandara

Karma Pool Villa is a famous brand pool villa, and its chain villas are located throughout

Southeast Asia. It is especially popular and famous to European countries, but with its

outstanding and unique facilities, it will soon gain interests from Korean. Karma Kandara is as

good as the most luxurious villas in Bali, such as Bvlgari, Ritz Carton and Four Seasons. As it

has the private beaches and pools for kids along with many unique facilities, it is considered as

the best place for family trip and honeymoon.

[Table] Karma Kandara Room Rate (in USD)

Room Type Size Rate(*1) Note

One-Bedroom Pool Residence - 605

Two-Bedroom Pool Residence - 776

Three-Bedroom Pool Residence - 984

Four-Bedroom Pool Residence - 1,390

Cliff Front Residence - 3,852

Grand Cliff Front Residence - 7,000

[Source] The Company’s Business Plan

Strictly Private and Confidential

32

[DC2]

(*1) Rate: Low Season Rate (Taxes and service fees are excluded)

Bvlgari

The resort, located 20 minutes from the airport, is comprised of 59 villas and other supporting

facilities. This resort is famous for its modernized and Baliness architect design, along with its

luxurious Bvlgari antique materials.

[Table] Bvlgari Room Rate (in USD)

Room Type Size Rate(*1) Note

Ocean-View One-Bedroom 250-300㎡ 1,300

Ocean-Cliff One-Bedroom 250-300㎡ 1,550

Two_Bedroom - 1,950

Bvlgari Villa(Three-Bedroom) 1,300㎡ 8,000

Premier Ocean-View One-Bedroom 250-300㎡ 1,450

[Source] The Company’s Business Plan

(*1) Rate: Regular Season Rate (Taxes and service fees are excluded)

Amankila

This Aman branded resort is famous for 3 step sea-faced swimming pool, and it is considered

as the one of the most beautiful resort in the world. This resort is comprised of 35 pool villa

units. The wide windows along with unique room design provide romantic atmosphere for

couples and families.

[Table] Amankila Room Rate (in USD)

Room Type Size Rate(*1) Note

Garden Suite(One-Bedroom) - 850

Ocean Suite - -

Pool Suite(One-Bedroom) - 1,350

Kilasari Suite(One-Bedroom) - 1,800

Indrakila Suite(One-Bedroom) - 2,100

Amankila Suite(Two-Bedroom) - 3,100

[Source] The Company’s Business Plan

Strictly Private and Confidential

33

[DC2]

(*1) Rate: Regular Season Rate (Taxes and service fees are excluded)

The Beverly Hills Bali

This luxurious resort, opened in September 2006 with 25 pool villa units and co-operated by

Bvlgari and Marriot, is famous for its Bvlgari materials in its design. Its famous spa is built with

lumbers, which is over 200 years old from Java islands.

[Table] The Beverly Hills Bali Room Rate (in USD)

Room Type Size Rate(*1) Note

One-Bedroom Villa 400㎡ 499

Two-Bedroom Villa 600㎡ 700

[Source] The Company’s Business Plan

(*1) Rate: Regular Season Rate (Taxes and service fees are excluded)

Ocean Blue Hotel Bali

The constructor of this project constructed this pool villa resort, and it is now operated by

Korean management. It is located 10 minutes from the airport and comprised of 141 pool villa

units.

[Table] Ocean Blue Hotel Bali Room Rate (in USD)

Room Type Size Rate(*1) Note

Grand Deluxe One-Bedroom - 600

Imperial Two-Bedroom - 900

[Source] The Company’s Business Plan

(*1) Rate: Regular Season Rate (Taxes and service fees are excluded)

The Dreamland Luxury Villas & Spa

Dreamland is co-established by Korean developer, who pursued in lumber processing industry

in Indonesia since 2000 (Developer of this project), and Guno & Company from Japan. Each of

the 40 villas, which was built in the forest of 40,000 pyeong (~12,000㎡), possesses unique

Strictly Private and Confidential

34

[DC2]

characteristics and attributes, combined with traditional Bali style with modernized design.

[Table] Dreamland Room Rate (in USD)

Room Type Size Rate(*1) Note

One-Bedroom Suite 210㎡ 460

Two-Bedroom Ocean Suite 270㎡ 700

Three-Bedroom Family Mansion 1,000㎡ 900

[Source] The Company’s Business Plan

(*1) Rate: Low Season Rate (Taxes and service fees are excluded)

(*2) This villa is operated by the developer of this project.

Strictly Private and Confidential

35

[DC2]

.Ⅳ Income & Cash Flow Analysis

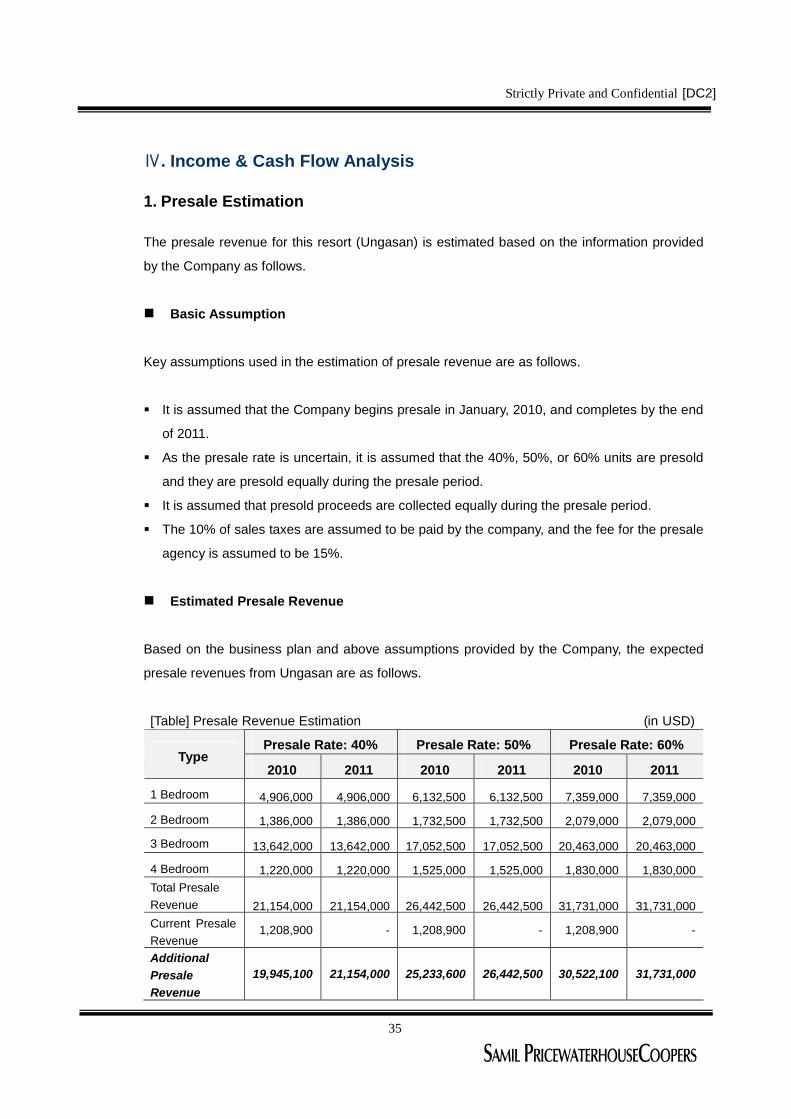

1. Presale Estimation

The presale revenue for this resort (Ungasan) is estimated based on the information provided

by the Company as follows.

Basic Assumption

Key assumptions used in the estimation of presale revenue are as follows.

It is assumed that the Company begins presale in January, 2010, and completes by the end

of 2011.

As the presale rate is uncertain, it is assumed that the 40%, 50%, or 60% units are presold

and they are presold equally during the presale period.

It is assumed that presold proceeds are collected equally during the presale period.

The 10% of sales taxes are assumed to be paid by the company, and the fee for the presale

agency is assumed to be 15%.

Estimated Presale Revenue

Based on the business plan and above assumptions provided by the Company, the expected

presale revenues from Ungasan are as follows.

[Table] Presale Revenue Estimation (in USD)

Presale Rate: 40% Presale Rate: 50% Presale Rate: 60%Type

2010 2011 2010 2011 2010 2011

1 Bedroom 4,906,000 4,906,000 6,132,500 6,132,500 7,359,000 7,359,000

2 Bedroom 1,386,000 1,386,000 1,732,500 1,732,500 2,079,000 2,079,000

3 Bedroom 13,642,000 13,642,000 17,052,500 17,052,500 20,463,000 20,463,000

4 Bedroom 1,220,000 1,220,000 1,525,000 1,525,000 1,830,000 1,830,000Total PresaleRevenue 21,154,000 21,154,000 26,442,500 26,442,500 31,731,000 31,731,000Current PresaleRevenue

1,208,900 - 1,208,900 - 1,208,900 -

AdditionalPresaleRevenue

19,945,100 21,154,000 25,233,600 26,442,500 30,522,100 31,731,000

Strictly Private and Confidential

36

[DC2]

Sales Taxes 1,994,510 2,115,400 2,523,360 2,644,250 3,052,210 3,173,100

Agency Fee 2,991,765 3,173,100 3,785,040 3,966,375 4,578,315 4,759,650Net PresaleRevenue

14,958,825 15,865,500 18,925,200 19,831,875 22,891,575 23,798,250

Review on Presale Value

The presale unit price provided by the Company is as follows.

[Table] Pool Villa Presale Value by Room Type (in USD)

SizeType Room Type # of Units

Land Building(*1)

Presale

Value

1 1,400.00㎡ 865.76㎡ 3,420,0004 Bedroom

1 1,050.00㎡ 678.21㎡ 2,680,000

8 810.00㎡ 522.61㎡ 1,980,000

6 690.00㎡ 522.61㎡ 1,830,000

22 600.00㎡ 473.66㎡ 1,580,000

2 440.00㎡ 323.94㎡ 1,180,000

3 420.00㎡ 322.38㎡ 1,080,000

3 Bedroom

1 400.00㎡ 307.53㎡ 1,030,000

2 Bedroom 7 400.00㎡ 307.53㎡ 990,000

34 280.00㎡ 183.12㎡ 550,000

Pool Villa

1 Bedroom11 266.00㎡ 183.12㎡ 530,000

(Source) The Company’s Business Plan

(*1) Areas of other facilities are included in the building size in accordance with Indonesian

regulation.

The presale values for Chateau The Bali (Ungasan) are little lower than the similar resorts in

the market. However, as the location and facilities of the Chateau The Bali (Ungasan) is more

advanced and better than the ones nearby, it is reasonable to believe that the units can be

presold at the value that the Company provided. Therefore, the unit presale value provided by

the Company was used in the estimation of the presale revenue.

Strictly Private and Confidential

37

[DC2]

Review on Presale Rate

When the global financial market recovers, the presale rate is expected to return to the

historical rates. However, as presale rate is highly sensitive to the presale price, quality of

facilities, and external economical factors, we concluded that it is difficult to estimate the

presale rate. Therefore, we estimated the presale revenue by applying the presale rates of

40%, 50%, and 60%. This estimation does not provide any assurance that the presale rate will

be higher than the ones that are used in the estimation.

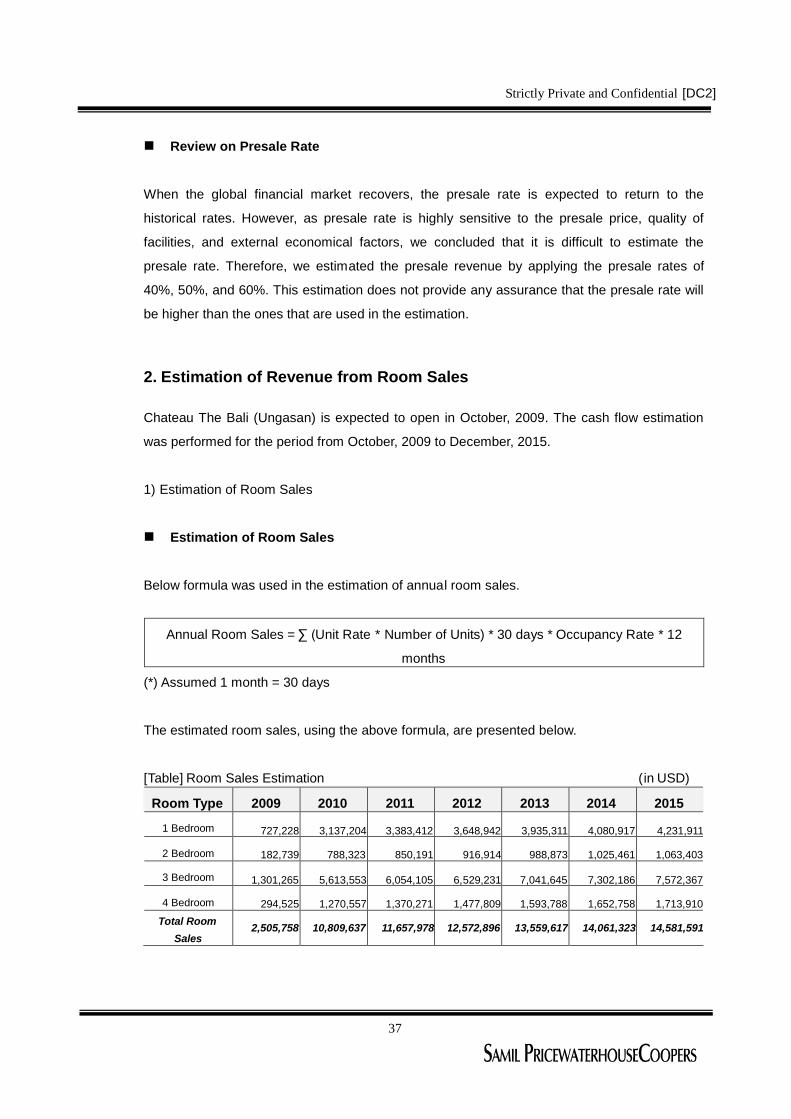

2. Estimation of Revenue from Room Sales

Chateau The Bali (Ungasan) is expected to open in October, 2009. The cash flow estimation

was performed for the period from October, 2009 to December, 2015.

1) Estimation of Room Sales

Estimation of Room Sales

Below formula was used in the estimation of annual room sales.

Annual Room Sales = ∑ (Unit Rate * Number of Units) * 30 days * Occupancy Rate * 12

months

(*) Assumed 1 month = 30 days

The estimated room sales, using the above formula, are presented below.

[Table] Room Sales Estimation (in USD)

Room Type 2009 2010 2011 2012 2013 2014 2015

1 Bedroom 727,228 3,137,204 3,383,412 3,648,942 3,935,311 4,080,917 4,231,911

2 Bedroom 182,739 788,323 850,191 916,914 988,873 1,025,461 1,063,403

3 Bedroom 1,301,265 5,613,553 6,054,105 6,529,231 7,041,645 7,302,186 7,572,367

4 Bedroom 294,525 1,270,557 1,370,271 1,477,809 1,593,788 1,652,758 1,713,910

Total Room

Sales2,505,758 10,809,637 11,657,978 12,572,896 13,559,617 14,061,323 14,581,591

Strictly Private and Confidential

38

[DC2]

Number of Units & Room Rates by Room Type

The data provided by the Company was used in this feasibility study, and the provided number

of units and room rates are as follows.

[Table] Number of Unit & Price by Room Type (in USD)

Type Room Type Size # of Unit Room Rate(*1)

1 Bedroom 183㎡ 45 650

2 Bedroom 308㎡ 7 1,050

3 Bedroom 308 ~ 523㎡ 42 1,800Pool Villa

4 Bedroom 678 ~ 866㎡ 2 11,000

(Source) The Company’s Business Plan

(*1) Published Rate

Direct comparison of room rate to the competitors is not reasonable as the room rate is highly

dependent on occupancy rate and geographical conditions, such as location and natural

environment of the resort. Considering many factors, such as the published rate and the lack of

brand recognition, only 50% of the room rate provided by the company was applied in the

estimation of room sales.

Occupancy Rate

The data provided by the Company was used to perform the feasibility study of the Chateau

The Bali (Ungasan), and the provided room occupancy rates are as follows. Room occupancy

rates provided by the company are relative lower than similar resorts in the market, including

Dreamland.

[Table] Expected Occupancy rate for the project

Type Room Type Size # of Unit OccupancyRate

1 Bedroom 183㎡ 45 65%

2 Bedroom 308㎡ 7 65%

3 Bedroom 308 ~ 523㎡ 42 45%Pool Villa

4 Bedroom 678 ~ 866㎡ 2 35%

(Source) The Company’s Business Plan

Strictly Private and Confidential

39

[DC2]

Even though the expected occupancy rates provided by the company are lower than the similar

resorts’occupancy rates, the rates were adjusted in this feasibility study, considering the lack of

brand recognition and other factors. We assumed the provided occupancy rate will be reached

in 5 years, and the growth rate was calculated based on the average growth rates of similar

resorts in 2002~2007 period (4%).

Changes in the Revenue after 1st year

In the estimation of revenue after 1st year, different room occupancy rates and room rates are

used. Other than these factors, we assumed there are no other changes.

For room occupancy rate, we used 51%, which was provided by the company at the first time,

and applied the average growth rate of 4%, which is the growth rate of similar resorts in 2002-

2007 period. Other than these changes, we assumed there are no other changes. As a result,

the occupancy rate of 2015 for this project is expected to be lower than the similar resorts’

occupancy rates in 2007.

[Table] Expected Room Occupancy Trend

Room Type 2009 2010 2011 2012 2013 2014 2015

1 Bedroom 55.3% 57.5% 59.8% 62.1% 64.6% 64.6% 64.6%

2 Bedroom 55.3% 57.5% 59.8% 62.1% 64.6% 64.6% 64.6%

3 Bedroom 38.3% 39.8% 41.4% 43.0% 44.7% 44.7% 44.7%

4 Bedroom 29.8% 30.9% 32.2% 33.5% 34.8% 34.8% 34.8%

(Source) The Company’s Business Plan

We assumed that the inflation rate in 2010 will remain the same for the estimated period. 3.7%

of inflation rate in 2010 was applied in the estimation of the room rate. It was noted that similar

resorts in Bali adjust their room rates annually.

[Table] Expected Room Rate Trend

Room Type 2009 2010 2011 2012 2013 2014 2015

1 Bedroom 325 337 349 362 376 390 404

2 Bedroom 525 544 565 585 607 630 653

3 Bedroom 900 933 968 1,004 1,041 1,079 1,119

4 Bedroom 5,500 5,704 5,915 6,133 6,360 6,596 6,840

Strictly Private and Confidential

40

[DC2]

(Source) The Company’s Business Plan

2) Estimation of Revenues from Food & Beverage (F&B) and Others

Revenues from F&B and Others are estimated based on the proportion of these revenues at

Dreamland resort for the last 2 years.

[Table] Dreamland Revenue Composition

Type Revenue fromRoom

Revenue from F&B Revenue fromOthers

Revenue 63.5% 26.0% 10.5%

(Source) The Company’s Business Plan

(*) Revenue from Others includes revenue from telephone, business center, spa, and health

related fees.

Estimated Revenues from F&B and Others

Estimated revenues from F&B and Others based on the proportion of Dreamland revenue are

as follows.

[Table] Estimated Revenues from F&B and Others (in USD)

Type 2009 2010 2011 2012 2013 2014 2015Revenue from

Room 2,505,758 10,809,637 11,657,978 12,572,896 13,559,617 14,061,323 14,581,591

Revenue fromF&B 651,497 2,810,506 3,031,074 3,268,953 3,525,500 3,655,944 3,791,214

Revenue fromOthers 263,105 1,135,012 1,224,088 1,320,154 1,423,760 1,476,439 1,531,067

Total 3,420,359 14,755,155 15,913,140 17,162,003 18,508,877 19,193,705 19,903,872

3. Estimation of Operating Expense

Operating expenses are estimated based on the operating expense of Dreamland resort.

Expenses unrelated to F&B and Others revenues are included in the cost of room sales.

1) Estimation of Cost of Room Sales

Strictly Private and Confidential

41

[DC2]

Cost of Room Sales at Dreamland

Average room sales costs at Dreamland for the last 2 years are as follows.

[Table] Cost of Room Sales at Dreamland

Type Rate NoteLabor & Labor-related Expense 6.00%

General Admin Expense 9.45%

Marketing Expense 5.51%

Maintenance Expense 7.87%

Utility Expense 17.32%

Other Selling Expense 10.00%

Fixed Cost 9.92%

(Source) The Company’s Business Plan

Estimated Cost of Room Sales

Estimated costs of room sales based on the Dreamland cost of room sales are as follows.

[Table] Estimated Cost of Room Sales (in USD)

Type 2009 2010 2011 2012 2013 2014 2015Room SalesRevenue 2,505,758 10,809,637 11,657,978 12,572,896 13,559,617 14,061,323 14,581,591

Labor & Labor-related Expense 150,345 648,578 699,479 754,374 813,577 843,679 874,895

General AdminExpense 236,765 1,021,384 1,101,542 1,187,991 1,281,224 1,328,630 1,377,789

MarketingExpense 138,113 595,807 642,566 692,995 747,381 775,034 803,710

MaintenanceExpense 197,304 851,153 917,952 989,992 1,067,687 1,107,191 1,148,158

Utility Expense 434,068 1,872,537 2,019,493 2,177,983 2,348,911 2,435,821 2,525,947

Other SellingExpense 250,576 1,080,964 1,165,798 1,257,290 1,355,962 1,406,132 1,458,159

Fixed Cost 248,603 248,603 248,603 248,603 248,603 248,603 248,603

Total Cost ofRoom Sales 1,655,774 6,319,026 6,795,432 7,309,227 7,863,345 8,145,091 8,437,261

Cost rate ofRoom Sales 66.08% 58.46% 58.29% 58.13% 57.99% 57.93% 57.86%

Strictly Private and Confidential

42

[DC2]

2) Estimation of Cost of F&B

Cost of F&B at Dreamland

Average F&B costs at Dreamland for the last 2 years are as follows.

[Table] Cost of F&B at Dreamland

Type Rate Note

Ingredient expense 30.00%

Labor & Labor-related expense 12.00%

Other expense 10.00%

Cost rate of F&B revenue 52.00%

(Source) The Company’s Business Plan

Estimated Cost of F&B

Estimated costs of F&B based on the Dreamland cost of F&B are as follows.

[Table] Estimated Cost of F&B (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

F&B revenue 651,497 2,810,506 3,031,074 3,268,953 3,525,500 3,655,944 3,791,214

Ingredientexpense 195,449 843,152 909,322 980,686 1,057,650 1,096,783 1,137,364

Labor & Labor-related expense 78,180 337,261 363,729 392,274 423,060 438,713 454,946

Other expense 65,150 281,051 303,107 326,895 352,550 365,594 379,121

Total Cost ofF&B 338,778 1,461,463 1,576,159 1,699,856 1,833,260 1,901,091 1,971,431

Cost rate ofF&B revenue 52.00% 52.00% 52.00% 52.00% 52.00% 52.00% 52.00%

3) Estimation of Cost of Other Revenue

Cost of Other Revenue at Dreamland

Average Other Revenue costs at Dreamland for the last 2 years are as follows.

Strictly Private and Confidential

43

[DC2]

[Table] Cost of Other Revenue at Dreamland

Type Rate Note

Raw Material Expense 17.62%

Labor & Labor-related Expense 17.71%

Other Expense 13.33%

Cost rate of Other revenue 48.67%

(Source) The Company’s Business Plan

Estimated Cost of Other Revenue

Estimated costs of Other revenue based on the Dreamland cost of Other revenue are as

follows.

[Table] Estimated Cost of Other Revenue (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

Other revenue 263,105 1,135,012 1,224,088 1,320,154 1,423,760 1,476,439 1,531,067

Raw MaterialExpense 46,357 199,979 215,673 232,599 250,853 260,135 269,760

Labor & Labor-related Expense 46,607 201,059 216,838 233,856 252,209 261,541 271,218

Other Expense 35,081 151,336 163,213 176,021 189,836 196,860 204,143

Total Cost ofOther revenue 128,044 552,373 595,724 642,476 692,898 718,535 745,121

Cost rate ofOther revenue 48.67% 48.67% 48.67% 48.67% 48.67% 48.67% 48.67%

Strictly Private and Confidential

44

[DC2]

4) Estimated Operating Expense

[Table] Estimated Operating Expense (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

Total Revenue 3,420,359 14,755,155 15,913,140 17,162,003 18,508,877 19,193,705 19,903,872

Cost of Roomsales 1,655,774 6,319,026 6,795,432 7,309,227 7,863,345 8,145,091 8,437,261

Cost of F&Brevenue 338,778 1,461,463 1,576,159 1,699,856 1,833,260 1,901,091 1,971,431

Cost of Otherrevenue 128,044 552,373 595,724 642,476 692,898 718,535 745,121

Total COGS 2,122,597 8,332,862 8,967,315 9,651,559 10,389,503 10,764,716 11,153,813

Cost Rate 62.06% 56.47% 56.35% 56.24% 56.13% 56.08% 56.04%

Strictly Private and Confidential

45

[DC2]

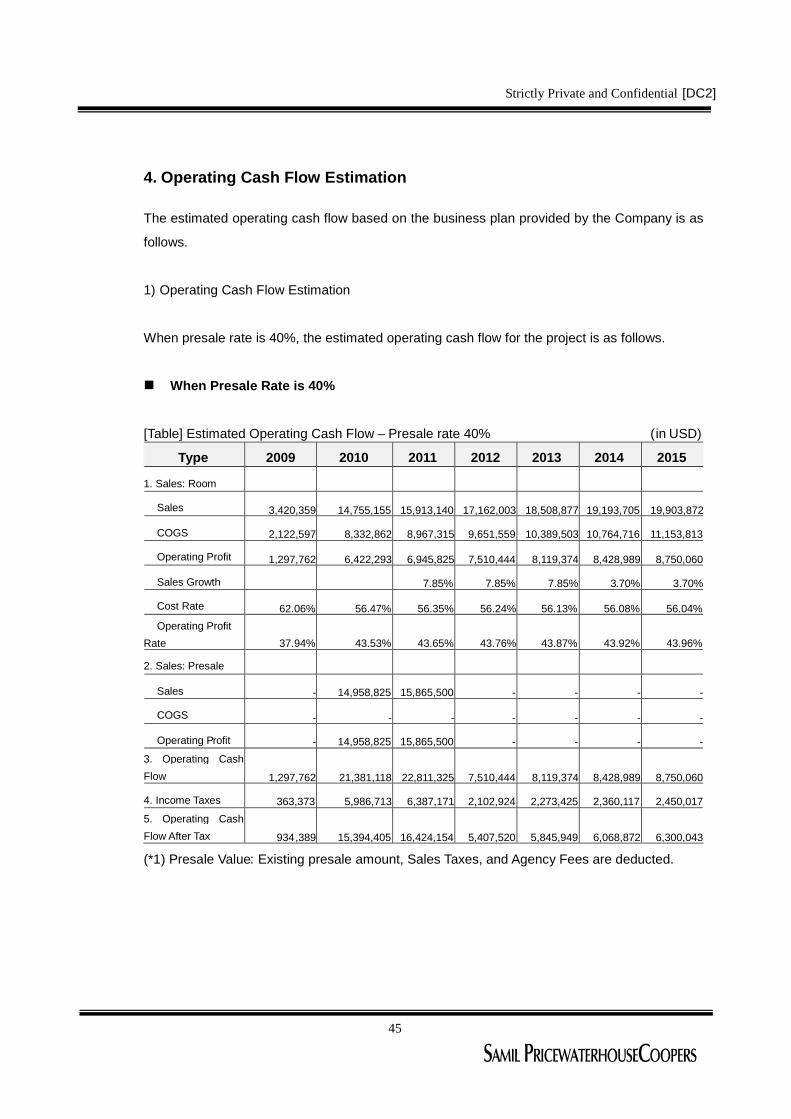

4. Operating Cash Flow Estimation

The estimated operating cash flow based on the business plan provided by the Company is as

follows.

1) Operating Cash Flow Estimation

When presale rate is 40%, the estimated operating cash flow for the project is as follows.

When Presale Rate is 40%

[Table] Estimated Operating Cash Flow – Presale rate 40% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

1. Sales: Room

Sales 3,420,359 14,755,155 15,913,140 17,162,003 18,508,877 19,193,705 19,903,872

COGS 2,122,597 8,332,862 8,967,315 9,651,559 10,389,503 10,764,716 11,153,813

Operating Profit 1,297,762 6,422,293 6,945,825 7,510,444 8,119,374 8,428,989 8,750,060

Sales Growth 7.85% 7.85% 7.85% 3.70% 3.70%

Cost Rate 62.06% 56.47% 56.35% 56.24% 56.13% 56.08% 56.04%

Operating Profit

Rate 37.94% 43.53% 43.65% 43.76% 43.87% 43.92% 43.96%

2. Sales: Presale

Sales - 14,958,825 15,865,500 - - - -

COGS - - - - - - -

Operating Profit - 14,958,825 15,865,500 - - - -

3. Operating Cash

Flow 1,297,762 21,381,118 22,811,325 7,510,444 8,119,374 8,428,989 8,750,060

4. Income Taxes 363,373 5,986,713 6,387,171 2,102,924 2,273,425 2,360,117 2,450,017

5. Operating Cash

Flow After Tax 934,389 15,394,405 16,424,154 5,407,520 5,845,949 6,068,872 6,300,043

(*1) Presale Value: Existing presale amount, Sales Taxes, and Agency Fees are deducted.

Strictly Private and Confidential

46

[DC2]

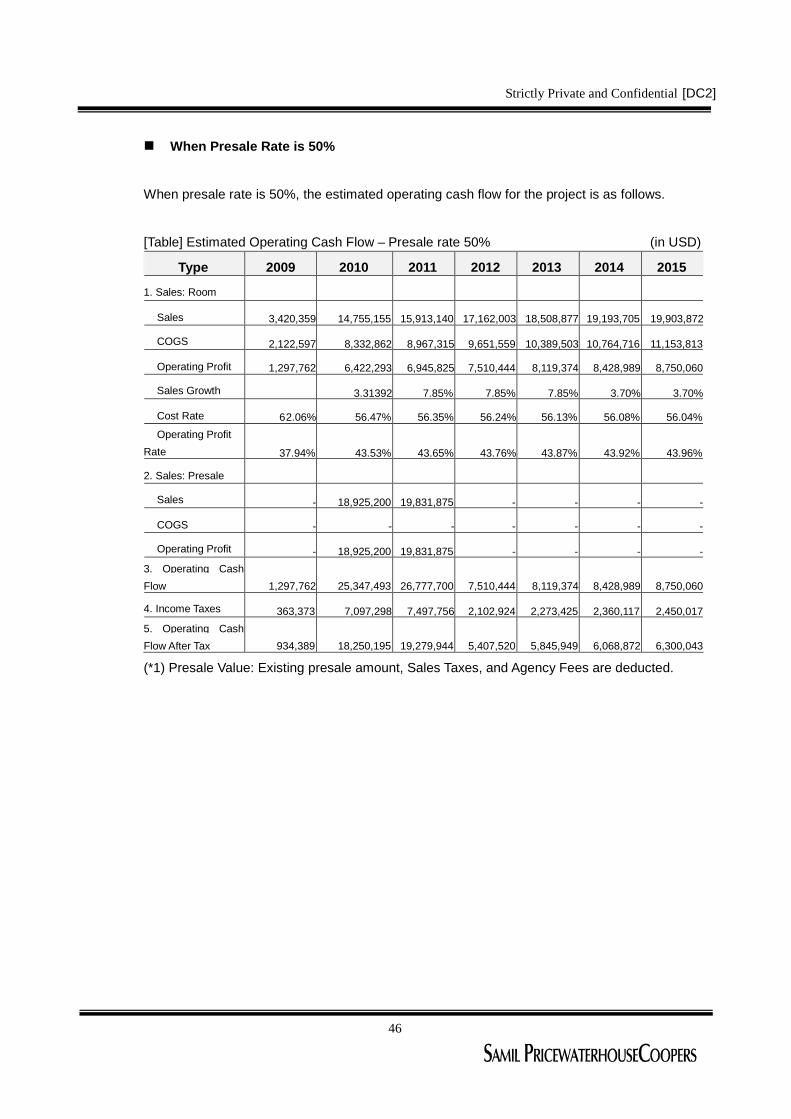

When Presale Rate is 50%

When presale rate is 50%, the estimated operating cash flow for the project is as follows.

[Table] Estimated Operating Cash Flow – Presale rate 50% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

1. Sales: Room

Sales 3,420,359 14,755,155 15,913,140 17,162,003 18,508,877 19,193,705 19,903,872

COGS 2,122,597 8,332,862 8,967,315 9,651,559 10,389,503 10,764,716 11,153,813

Operating Profit 1,297,762 6,422,293 6,945,825 7,510,444 8,119,374 8,428,989 8,750,060

Sales Growth 3.31392 7.85% 7.85% 7.85% 3.70% 3.70%

Cost Rate 62.06% 56.47% 56.35% 56.24% 56.13% 56.08% 56.04%

Operating Profit

Rate 37.94% 43.53% 43.65% 43.76% 43.87% 43.92% 43.96%

2. Sales: Presale

Sales - 18,925,200 19,831,875 - - - -

COGS - - - - - - -

Operating Profit - 18,925,200 19,831,875 - - - -

3. Operating Cash

Flow 1,297,762 25,347,493 26,777,700 7,510,444 8,119,374 8,428,989 8,750,060

4. Income Taxes 363,373 7,097,298 7,497,756 2,102,924 2,273,425 2,360,117 2,450,017

5. Operating Cash

Flow After Tax 934,389 18,250,195 19,279,944 5,407,520 5,845,949 6,068,872 6,300,043

(*1) Presale Value: Existing presale amount, Sales Taxes, and Agency Fees are deducted.

Strictly Private and Confidential

47

[DC2]

When Presale Rate is 60%

When presale rate is 60%, the estimated operating cash flow for the project is as follows.

[Table] Estimated Operating Cash Flow – Presale rate 60% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

1. Sales: Room

Sales 3,420,359 14,755,155 15,913,140 17,162,003 18,508,877 19,193,705 19,903,872

COGS 2,122,597 8,332,862 8,967,315 9,651,559 10,389,503 10,764,716 11,153,813

Operating Profit 1,297,762 6,422,293 6,945,825 7,510,444 8,119,374 8,428,989 8,750,060

Sales Growth 3.31392 7.85% 7.85% 7.85% 3.70% 3.70%

Cost Rate 62.06% 56.47% 56.35% 56.24% 56.13% 56.08% 56.04%

Operating Profit

Rate 37.94% 43.53% 43.65% 43.76% 43.87% 43.92% 43.96%

2. Sales: Presale

Sales - 22,891,575 23,798,250 - - - -

COGS - - - - - - -

Operating Profit - 22,891,575 23,798,250 - - - -

3. Operating Cash

Flow 1,297,762 29,313,868 30,744,075 7,510,444 8,119,374 8,428,989 8,750,060

4. Income Taxes 363,373 8,207,883 8,608,341 2,102,924 2,273,425 2,360,117 2,450,017

5. Operating Cash

Flow After Tax 934,389 21,105,985 22,135,734 5,407,520 5,845,949 6,068,872 6,300,043

(*1) Presale Value: Existing presale amount, Sales Taxes, and Agency Fees are deducted.

Strictly Private and Confidential

48

[DC2]

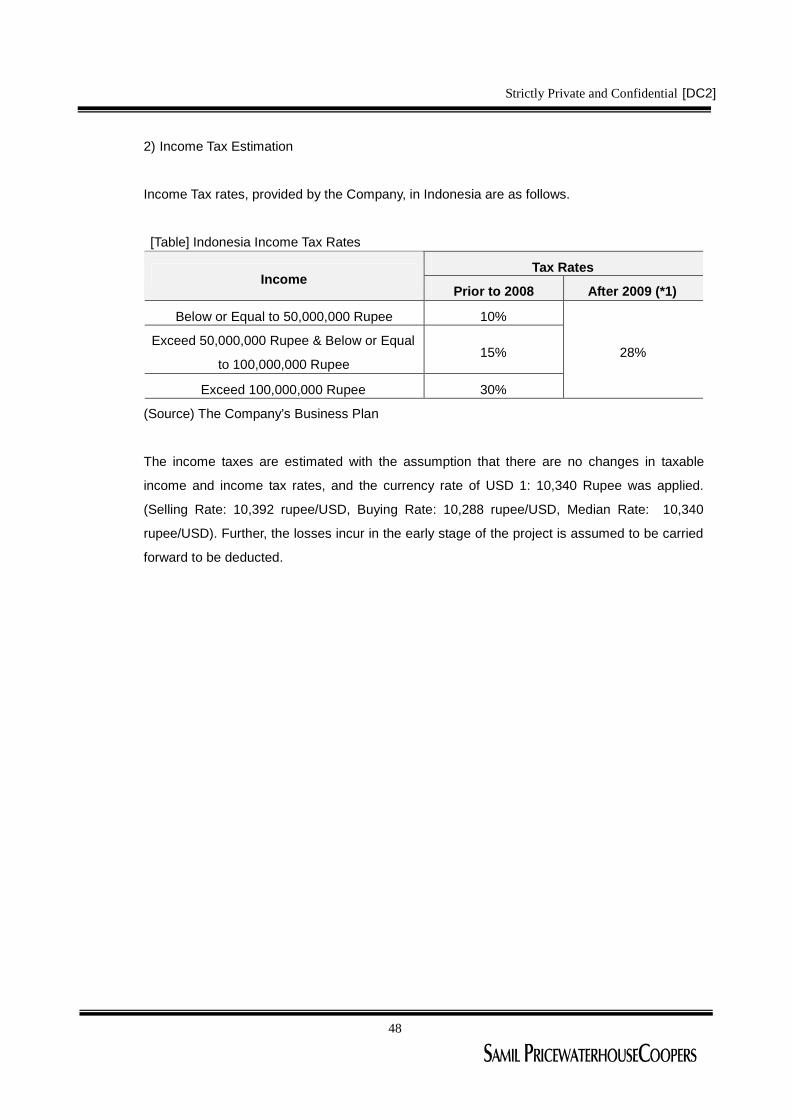

2) Income Tax Estimation

Income Tax rates, provided by the Company, in Indonesia are as follows.

[Table] Indonesia Income Tax Rates

Tax RatesIncome

Prior to 2008 After 2009 (*1)

Below or Equal to 50,000,000 Rupee 10%

Exceed 50,000,000 Rupee & Below or Equal

to 100,000,000 Rupee15%

Exceed 100,000,000 Rupee 30%

28%

(Source) The Company’s Business Plan

The income taxes are estimated with the assumption that there are no changes in taxable

income and income tax rates, and the currency rate of USD 1: 10,340 Rupee was applied.

(Selling Rate: 10,392 rupee/USD, Buying Rate: 10,288 rupee/USD, Median Rate: 10,340

rupee/USD). Further, the losses incur in the early stage of the project is assumed to be carried

forward to be deducted.

Strictly Private and Confidential

49

[DC2]

5. Cumulative Cash Flow Projection

The cumulative cash flow projection based on the estimated operating cash flow is as follows.

When the presale rate is 40%

The Company plans to distribute 8% of the presale amount for the first 2 years, and then plans

to distribute 40% of net operating profit. The estimated distributable dividends are estimated as

below.

[Table] Dividend Estimation – Presale Rate: 40% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

Presale Revenue - 21,154,000 21,154,000

Operating Profit, Net

of Tax 934,389 21,105,985 22,135,734 5,407,520 5,845,949 6,068,872 6,300,043

Dividend Rate(*) 8% 8% 40% 40% 40% 40%

Dividend Amount 846,160 2,538,480 865,203 935,352 971,020 1,008,007

Available cumulative cash flow based on the operating cash flow of Chateau the Bali

(Ungasan) is estimated as below.

[Table] Cumulative Cash Flow Estimation – Presale Rate: 40% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015Operating Cash

Flow, Net of Tax 934,389 15,394,405 16,424,154 5,407,520 5,845,949 6,068,872 6,300,043

Dividends - 846,160 2,538,480 865,203 935,352 971,020 1,008,007

Net Cash Flow (*) 934,389 14,548,245 13,885,674 4,542,316 4,910,597 5,097,852 5,292,036

Cumulative Cash

Flow 934,389 15,482,634 29,368,308 33,910,624 38,821,222 43,919,074 49,211,110

(*) As funding method is not confirmed, financing cost and reserve capital for operating are not

considered in the estimation.

Strictly Private and Confidential

50

[DC2]

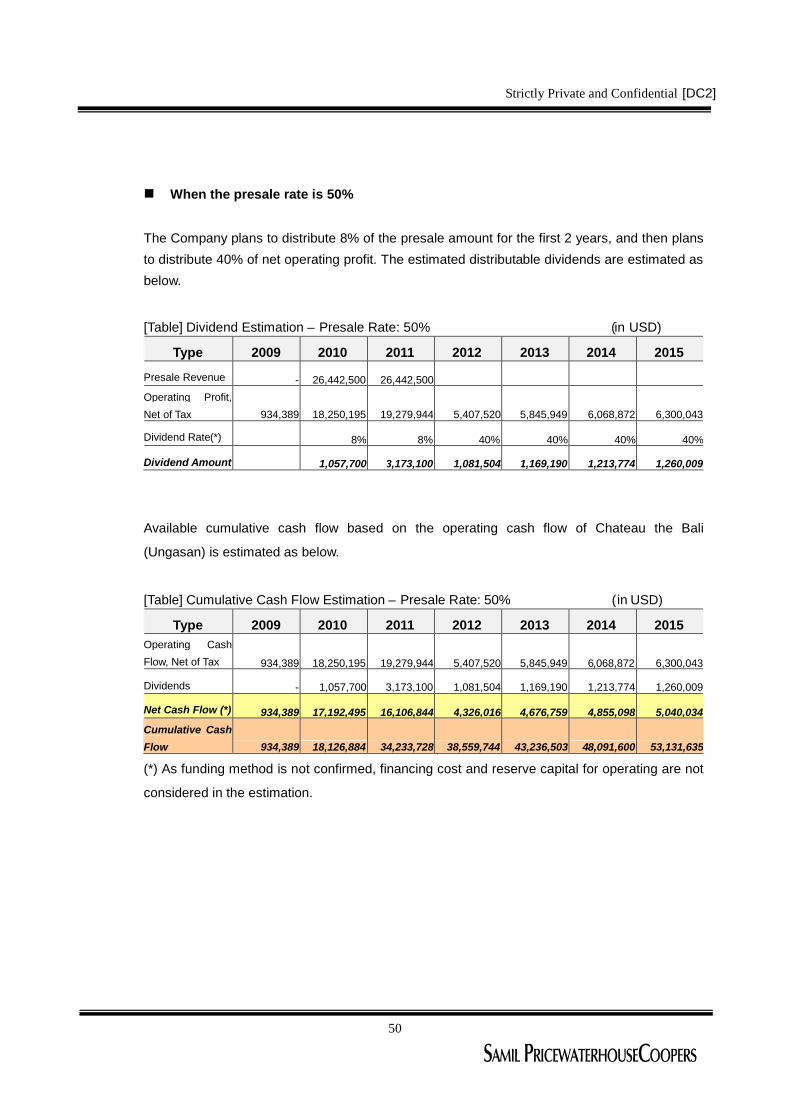

When the presale rate is 50%

The Company plans to distribute 8% of the presale amount for the first 2 years, and then plans

to distribute 40% of net operating profit. The estimated distributable dividends are estimated as

below.

[Table] Dividend Estimation – Presale Rate: 50% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

Presale Revenue - 26,442,500 26,442,500

Operating Profit,

Net of Tax 934,389 18,250,195 19,279,944 5,407,520 5,845,949 6,068,872 6,300,043

Dividend Rate(*) 8% 8% 40% 40% 40% 40%

Dividend Amount 1,057,700 3,173,100 1,081,504 1,169,190 1,213,774 1,260,009

Available cumulative cash flow based on the operating cash flow of Chateau the Bali

(Ungasan) is estimated as below.

[Table] Cumulative Cash Flow Estimation – Presale Rate: 50% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015Operating Cash

Flow, Net of Tax 934,389 18,250,195 19,279,944 5,407,520 5,845,949 6,068,872 6,300,043

Dividends - 1,057,700 3,173,100 1,081,504 1,169,190 1,213,774 1,260,009

Net Cash Flow (*) 934,389 17,192,495 16,106,844 4,326,016 4,676,759 4,855,098 5,040,034

Cumulative Cash

Flow 934,389 18,126,884 34,233,728 38,559,744 43,236,503 48,091,600 53,131,635

(*) As funding method is not confirmed, financing cost and reserve capital for operating are not

considered in the estimation.

Strictly Private and Confidential

51

[DC2]

When the presale rate is 60%

The Company plans to distribute 8% of the presale amount for the first 2 years, and then plans

to distribute 40% of net operating profit. The estimated distributable dividends are estimated as

below.

[Table] Dividend Estimation – Presale Rate: 60% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015

Presale Revenue - 31,731,000 31,731,000

Operating Profit,

Net of Tax 934,389 18,250,195 19,279,944 5,407,520 5,845,949 6,068,872 6,300,043

Dividend Rate(*) 8% 8% 40% 40% 40% 40%

Dividend Amount 1,269,240 3,807,720 1,297,805 1,403,028 1,456,529 1,512,010

Available cumulative cash flow based on the operating cash flow of Chateau the Bali

(Ungasan) is estimated as below.

Table] Cumulative Cash Flow Estimation – Presale Rate: 60% (in USD)

Type 2009 2010 2011 2012 2013 2014 2015Operating Cash

Flow, Net of Tax 934,389 21,105,985 22,135,734 5,407,520 5,845,949 6,068,872 6,300,043

Dividends - 1,269,240 3,807,720 1,297,805 1,403,028 1,456,529 1,512,010

Net Cash Flow (*) 934,389 19,836,745 18,328,014 4,109,715 4,442,921 4,612,343 4,788,033

Cumulative Cash

Flow 934,389 20,771,134 39,099,148 43,208,863 47,651,784 52,264,127 57,052,160

(*) As funding method is not confirmed, financing cost and reserve capital for operating are not

considered in the estimation.

Strictly Private and Confidential

52

[DC2]

Ⅴ. Risk Factors and Solutions for the Project

Risk factors and solutions for the risks are as follows.

Laws and Regulation Risk

< Risk > In accordance with Indonesia regulation, foreigners cannot own land in Indonesia

< Solution>

As the CEO of the developer transferred the ownership of the land to his relatives, no risk

regarding land acquisition exists.

Managing Risk

< Risk > Low brand recognition might lead to unfavorable operating results

< Solution >

The developer has 5 years of experience in operating pool villa resort in Bali. Moreover, by

recruiting the general manager who has experience in working for five star hotels for more

than 20 years, the operating risk is minimized.

Presale Risk

< Risk > Risk of not selling (pre-sale) enough villas

< Solution >

The Company plans to construct and presale the most luxurious resorts.

The Company plans to contract with global presale agencies in the world to enhance the

presale rates by utilizing the Global Network.

Exchange Rate Risk

< Risk > Fluctuation risk in Indonesian currency

< Solution >

As Rupee continues to depreciate, gains on currency translation is expected when the

Strictly Private and Confidential

53

[DC2]

borrowed fund is redeemed.

Country Risk

< Risk > Possible Terrorist’s Attacks in Bali

< Solution >

As Indonesian government provides more secured policies after the terrorist’s attack in

October, 2005, another terrorist’s attack seems unlikely.

![Hotel & Branded Residences BALI - [Primary] …country-clone.htl-web.com/files/2017/02/Bali-Hotel... · E-commerce providers including Traveloka, Pegipegi and Blibli report ... Hotel](https://img.dokumen.tips/doc/110x75/5aebc7e87f8b9ae5318e22a2/hotel-branded-residences-bali-primary-country-clonehtl-webcomfiles201702bali-hotele-commerce.jpg)