Embed Size (px)

Citation preview

BA2 Fundamentals of Management Accounting

Module: 03

Absorption and Marginal Costing

Costing systems I – Absorption and Marginal costing

66

1. Costing systems

So let's set the scene! You are at your friend’s house sitting on the sofa, when

they come back from the kitchen with a can of the latest energy drink. As

they open it and take a sip you look at the price label still stuck to the can

which reads £1.99. You think to yourself 'so they sell it for £1.99 but I bet it

costs them less than a penny to make!'

I'm sure we've all had this thought about a product at some point!

“That's easy!” you might think. “Isn't the cost of something just however much

we paid for it?”

No, not usually!

The actual price paid is not as obvious as you might think.

Imagine you own a business building toy cars and this week you finished

building two new models: Car A and Car B.

The parts for Car A cost £200.

The parts for Car B cost £2,000.

Both have a selling price of £3,000.

On the surface, it appears that Car A is far more profitable than Car B. By

the looks of things you might even consider specialising in producing

Car A and forgetting about Car B altogether.

But what if Car A took five days to build and Car B only took an hour? What if

you needed to hire three different specialists just to assist in the building of

Car A? What if Car A needs £20,000 worth of special machinery to build?

What if you needed to pay rent for a new factory just to manufacture Car A? In

light of this information, what is real cost of Car A and Car B?

As you can see, costing is not always a simple exercise. Accurately costing

products is important because if you don’t know the cost of your product,

there’s no way to know whether it’s profitable.

To overcome this problem, corporations use costing systems. Costing

systems take costs and accurately allocate them to outputs. This allows

corporations to determine the actual costs of producing each product

and give them a better indication of each unit’s profitability. Helping

them make effective decisions.

Costing systems I – Absorption and Marginal costing

67

2. Absorption/Full costing

One of the costing systems used by companies to accurately assess

the cost of a product is absorption costing (also known as full costing.)

Traditional absorption costing is an accounting method used to

determine the full production cost per unit – hence it's other name!

The full production cost includes:

• Direct costs or prime costs such as the cost of materials (e.g. nuts

and bolts) and labour (e.g. the wages of our factory workers).

• Indirect costs known as production overheads (e.g. electricity or new

machinery).

Going back to our toy car example, to calculate the full production cost of a

unit, it's obvious that we need to add the costs of the parts (materials) and the

salary we pay the factory worker to build our product, these are our direct

costs. However, looking at the bigger picture, these are not the only things we

have to pay for to make toy cars. We cannot ignore our indirect costs such

as rent and new machinery. For these indirect costs then, we need a

method to fairly allocate them to the production side.

Our company makes more than one product (like most companies do)

so it would be inaccurate to say that all of the indirect costs are due to

the production of one particular product. This could lead this product's

selling price being set too high and another products selling price too low. It

would also be incorrect to split the costs equally over our production units

(e.g. half for car A, half for car B) because one product may require a much

more intensive and costly process.

The following section on the absorption costing system will show you how to accurately calculate the cost of these overheads and allocate them to

particular cost centres based on relevant information. The definition of a

cost centre is a part of an organisation which can have particular costs

charged to it. For example the salaries of the staff in the admin division can be

charged to the admin cost centre.

As you read through, remember our goal in this process is to end up with an

accurate overhead cost per unit.

Costing systems I – Absorption and Marginal costing

68

Step 1 – Overhead allocation

The first stage of correctly apportioning overhead costs to cost units is to collect together overhead costs into relevant cost centres and categories.

Let's take an example of a pie shop business. The business has four main

cost centres: Preparation, Baking, Purchasing and Admin. Two of these are

production cost centres which are directly related to making the pies. The

other two are service cost centres which are more related to supporting the

production.

The overhead costs directly related to these cost centres are recorded and

grouped together. Let's say they are as follows:

Directly allocated costs:

£

Preparation 60,000

Baking 30,000

Purchasing 50,000

Admin 10,000

We may also have overheads that relate to the business as a whole and

which cannot be specifically allocated to a particular cost centre. For

example, electricity will be used in all areas of the business including

powering the ovens in the baking department or the lighting in the admin

department etc. In this case these general overheads are:

General overheads:

£

Rent 100,000

Machine maintenance 50,000

Water 20,000

Electricity 60,000

Heating 40,000

Step 2 – Apportioning general overheads to cost centres

Remember the aim of absorption costing is to calculate the full cost of a unit of production, so in order to relate an overhead to a cost unit accurately

we want to end up with all overheads in the production cost centres as

these most closely relate to the production of units. It will then be much

easier to relate the costs back to the cost of producing each unit. The process

of sharing overhead costs between production departments is called

apportionment.

Step 2 takes our general overheads and apportions them to cost centres.

To do this, we must decide what is the fairest way to spread our overheads

into cost centres.

Costing systems I – Absorption and Marginal costing

69

Let's start with rent. Rent is most closely related to floor space – the higher

the floor space the higher the rent.

Here's some information that will help us to do this:

Preparation Baking Purchasing Admin

Floor space (m²) 300 200 400 100

Original machine cost £ 50,000 100,000 30,000 20,000

Similarly we can apportion water, electricity and heating by floor space, whereas machine maintenance should be apportioned by the original cost of

the machine as that is a fairer basis of spreading those costs.

We now need to work out exactly how much of each overhead should be

apportioned to each cost centre. We’ll start by calculating the proportion of

floor space used by each cost centre. As you can see our business has a total

of 1000m² worth of space and each cost centre utilises a different amount.

Using the table above we can work out the floor space proportions for each

cost centre by taking the amount used by the department and dividing by our

total of 1000m², then multiplying by 100. For example, the percentage that

the preparation department uses is 300m²/1000m² x 100 = 30%. We've

worked out the rest in the following table:

Preparation Baking Purchasing Admin

Floor space (m²) 300 200 400 100

Percentage of total floor space 30% 20% 40% 10%

Knowing these percentages, we can now calculate the amount of rent, water,

electricity and heating to attribute to each cost centre:

Preparation Baking Purchasing Admin

(30%) (20%) (40%) (10%)

Rent (£100,000) 30,000 20,000 40,000 10,000

Water (£20,000) 6,000 4,000 8,000 2,000

Electricity (£60,000) 18,000 12,000 24,000 6,000

Heating (£40,000) 12,000 8,000 16,000 4,000

Total 66,000 44,000 88,000 22,000

We can now do the same for the cost of the machines. The original cost of

all machines was £200,000, so we can divide the individual machine cost for

each department by this total. We can then create the following table:

Costing systems I – Absorption and Marginal costing

70

Preparation Baking Purchasing Admin

Original machine cost 50,000 100,000 30,000 20,000

Percentage of total

machine cost 25% 50% 15% 10%

Our machine maintenance overhead cost was £50,000. So using the

percentages above, we can find out how much the maintenance costs in each

department. For example, the majority of expensive machinery is found in the

baking department (50%), so 50% of the total machine maintenance can be

apportioned there.

Preparation

(25%)

Bakin

g

(50%

)

Purchasing

(15%)

Admin

(10%)

Machine maintenance

(£50,000) 12,500 25,000 7,500 5,000

With this information we can now find the total apportioned overhead cost of

each cost centre:

Preparation Baking Purchasing Admin

£ £ £ £

Allocated Costs 60,000 30,000 50,000 10,000

Apportioned Costs:

Rent

30,000

20,000

40,000

10,000

Machine Maintenance 12,500 25,000 7,500 5,000

Water 6,000 4,000 8,000 2,000

Electricity 18,000 12,000 24,000 6,000

Heating 12,000 8,000 16,000 4,000

Total

138,500

99,000

145,500

37,000

Step 3 - Re-apportionment of service cost centres into

production costs centres

So, we have attributed our overhead costs to the various cost centres that

make up our business. However, it's difficult to directly absorb service

costs into direct production cost units. After all – how much administration

cost, for example, should relate to each unit – very difficult to say.

The way we overcome this problem is to re-apportion the service costs

Costing systems I – Absorption and Marginal costing

71

proportionately between the two production cost centres.

Costing systems I – Absorption and Marginal costing

72

The following data shows the extent of work carried out by a particular service

cost centre for the production side:

Service cost centre

Preparation Baking Purchasing Admin

Purchasing 45% 35% / 20%

Admin 25% 65% 10% /

We can use these percentages to take the costs out of the purchasing and

administration departments and instead put them into preparation and

baking where they can be directly related to the units produced.

There are three main methods of re-apportioning service cost centres, each

with their own characteristics:

• The Direct Method

• The Step Method

• The Reciprocal Method

The Direct method

This is the simplest and quickest method of apportioning service costs

into production. Here we ignore any services carried out by service cost

centres on behalf of each other (inter-cost centre service).

In our case this would mean disregarding the 20% of work purchasing did for

admin and the 10% of work the admin did for purchasing.

Preparation Baking Purchasing Admin

£ £ £ £

Apportioned costs 138,500 99,000 145,500 37,000

Service cost centre

*Purchasing (45:35:20)

81,844

63,656

(145,500)

/

**Admin 10,278 26,722 / (37,000)

230,622 189,378 / /

In this case the 45, 35, 20 split would instead become a 45:35 ratio for the

purchasing costs, being absorbed exclusively into the production cost

centres.

*The 45 and 35 now form a ratio rather than a percentage so need to be

calculated differently:

Costing systems I – Absorption and Marginal costing

73

45 + 35 = 80

Preparation

45 x 145,500

80

= 81,844

Baking

35 x 145,500

80

= 63,656

** The same goes for the admin costs;

25 + 65 = 90

Preparation

25 x 37,000

90

= 10,278

Baking

65 x 37,000

90

= 26,722

As you can see, these service costs are removed as they are absorbed by

production costs leaving us with grand totals of 0 in each of the service cost

centre columns.

Costing systems I – Absorption and Marginal costing

74

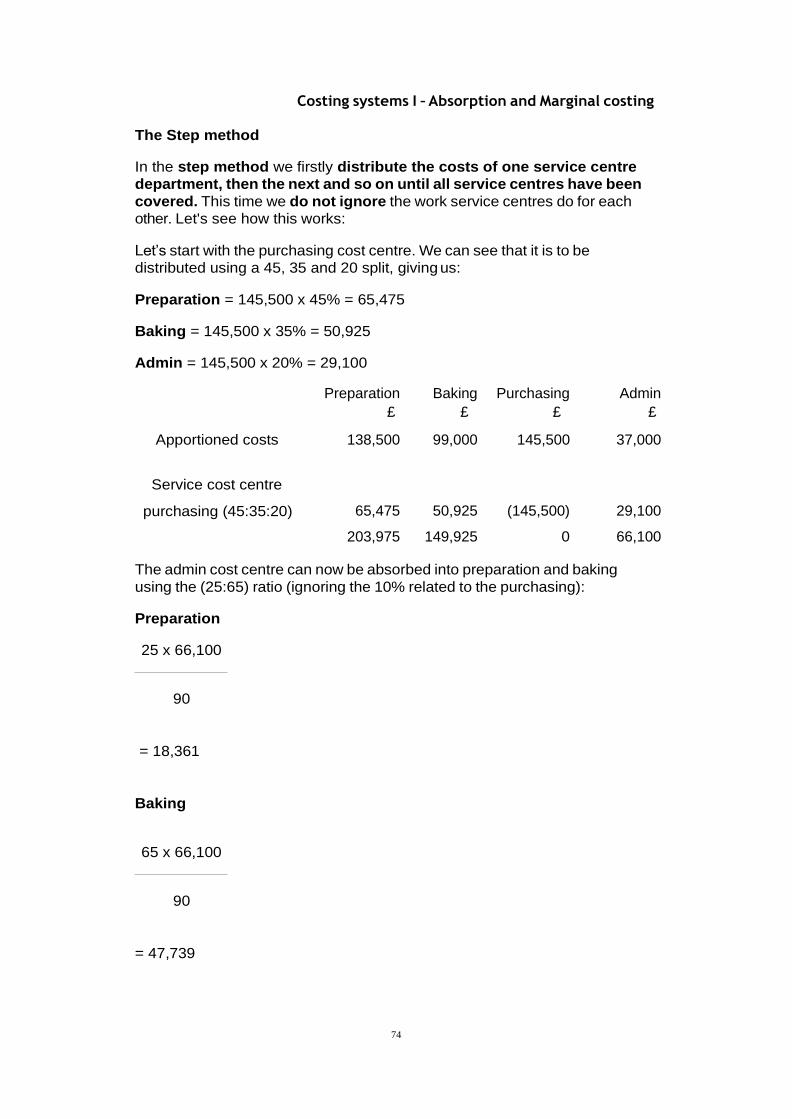

The Step method

In the step method we firstly distribute the costs of one service centre

department, then the next and so on until all service centres have been

covered. This time we do not ignore the work service centres do for each

other. Let's see how this works:

Let’s start with the purchasing cost centre. We can see that it is to be

distributed using a 45, 35 and 20 split, giving us:

Preparation = 145,500 x 45% = 65,475

Baking = 145,500 x 35% = 50,925

Admin = 145,500 x 20% = 29,100

Preparation Baking Purchasing Admin

£ £ £ £

Apportioned costs 138,500 99,000 145,500 37,000

Service cost centre

purchasing (45:35:20)

65,475

50,925

(145,500)

29,100

203,975 149,925 0 66,100

The admin cost centre can now be absorbed into preparation and baking

using the (25:65) ratio (ignoring the 10% related to the purchasing):

Preparation

25 x 66,100

90

= 18,361

Baking

65 x 66,100

90

= 47,739

75

Chapter 4 Costing systems I – Absorption and Marginal costing

Preparation

£

Baking Purchasing Admin

£ £ £

Apportioned costs 203,975 149,925 0 66,100

Admin (25:65) 18,361 47,739 / (66,100)

222,336 197,664 0 0

The weakness of the step method is that in this second step we ignored the

10% of work done by admin for purchasing giving us a good, but not

completely accurate final result. It is however, more straight forward than

our final method; let's have a look at that!

The Reciprocal method

Our last method is the longest and most complicated, but also the most

accurate! The reciprocal method is the best method to use if there are lots of

service cost centres that have all contributed to each other to some extent,

under this method all inter-service work is fully recognised and catered

for.

The reciprocal method works by apportioning costs out as intended to each

cost centre, the next cost centre in turn apportions its costs out as

intended, this carries on until there is nothing left to apportion from any

service cost centre, perhaps this table will demonstrate this more

effectively:

Preparation Baking Purchasing Admin

Apportioned costs

£

138,500

£

99,000

£

145,500

£

37,000

Service cost centre

Purchasing (45:35:20) 65,475 50,925 (145,500) 29,100

66,100

Admin (25:65:10) 16,525 42,965 6,610 (66,100)

As you can see, this time we apportioned the admin costs as intended (25,

65, 10) which made a difference to the amounts that were added onto

preparation and baking.

But there's a problem – it also added cost back to the purchasing column

which had been emptied during the previous step, but it now has a number in

it so we must repeat the apportionment out of purchasing again. We now

continue in this fashion until all service costs have been completely

absorbed and exhausted, like so:

76

Chapter 4 Costing systems I – Absorption and Marginal costing

Preparation

£

Baking Purchasing Admin

£ £ £

Apportioned costs 138,500 99,000 145,500 37,000

Service cost centre

Purchasing (45:35:20)

65,475

50,925

(145,500)

29,100

66,100

Admin (25:65:10) 16,525 42,965 6,610 (66,100)

6,610

Purchasing (45:35:20) 2,975 2,313 (6,610) 1,322

1,322

Admin (25:65:10) 330 860 132 (1,322)

132

Purchasing (45:35:20) 60 46 (132) 26

26

Admin (25:65:10) 6 17 3 (26)

3

Purchasing (45:35:20) 1 1 (3) 1

1

Admin (25:65:10) / 1 / (1)

223,872 196,128 / /

As you can see from the table above, by using the reciprocal method, we have

now apportioned the overhead costs from the service cost centres in full to

production cost centres

Step 4 – Apportioning overheads to cost unit production

We want to calculate the full cost of a unit of production and now that we know our overall overhead costs for each production cost centre we

can absorb it directly into production.

An assumption of absorption costing is that the higher the level

activity/volume produced, the higher the cost of that activity will be. This is

summarised by using what is known as the overhead absorption rate, or

OAR. The OAR is calculated by dividing the production overhead by the

activity level:

77

Costing systems I – Absorption and Marginal costing

Production overhead

Activity level

= Overhead absorption rate

The basis of our activity level should be the one that most fairly reflects the

work in a particular department. For example, our baking department has the

most machines and uses the most machine hours, therefore it would be most

accurate to absorb the units of production by the number of machine hours.

Other suitable figures which we can base our absorption rate on include:

• Per unit produced

• Labour hours

• % of prime cost

Returning to our example, let us assume that the company chose the direct

method of re-apportionment and so has overheads of £230,622 and

£189,378 per our earlier working.

The following data has also been recorded regarding labour and machine

hours in those departments:

Preparation Baking

Overheads £230,622 £189,378

Labour hours 50,000 5,000

Machine hours 3,000 60,000

Units 100,000 100,000

So… how do we calculate the OAR for both the preparation and the

baking department?

We should choose the basis that most fairly reflects the work in a particular

department. We can see from the information that the preparation

department is a manual process with many more labour hours than machine

hours, whereas for the baking department it is machine hours that are the

focus of the work. As such it is fairest to use those as the basis for splitting

our overheads between units. We can now calculate our OAR:

Preparation

78

Costing systems I – Absorption and Marginal costing

230,622

50,000

= £4.61 per labour hour

Overheads for the preparation department are absorbed a rate of £4.61 per

labour hour; for every labour hour worked on a particular pie in that

department we'll include £4.61 of overhead cost.

Baking

189,378

60,000

= £3.16 per machine hour

So, overheads for the baking department are absorbed a rate of £3.16 per

machine hour.

Let’s put this all together!

Our pie company makes a particular pie ‘the big one’ and the following costs

have been identified:

Direct materials (per unit) £6

Direct Labour hours per pie

- Preparation 1.5hrs

- Baking 0.5hrs

Direct machine hours per pie

- Preparation 0.5hrs

- Baking 3hrs

Labour paid at £7 an hour

So, first of all we need to calculate our direct labour costs. We know that

labour is paid at £7 an hour and that a pie takes 1.5 hours of labour time to

prepare and half an hour to bake. So we can work out our direct labour costs

like so:

79

Costing systems I – Absorption and Marginal costing

(1.5 x £7) + (0.5 x £7) = 10.5 + 3.5 = £14

Now, we need to calculate our overheads, we know that baking overheads

for preparation are calculated by machine hours and preparation overheads

are calculated by labour hours:

Preparation overheads (labour hour basis):

1.5 labour hours x £4.61 per labour hour = £6.92

Baking overheads:

3 machine hours x £3.16 per machine hour = £9.48

Now that we have all the individual costs we can now calculate the total:

£

Direct material 6

Direct Labour 14

Preparation overheads 6.92

Baking overheads 9.48

Total: £36.40 per pie – An expensive pie!

Pre-determined overhead rates

The cost per unit is typically calculated at the start of the year for planning

purposes. As such the cost unit is often calculated using budgeted figures

and as such are called the pre-determined or budgeted OAR and is

calculated using the following formula:

Budgeted overhead

Budgeted activity level (e.g. number of units, or labour hours)

Let’s say that a cake shop had budgeted for 102,000 units and overheads of

£450,000 and they are going to use a per unit basis to absorb overheads.

450,000

102,000

= £4.41 per unit

80

Costing systems I – Absorption and Marginal costing

As the year progresses it's that pre-determined OAR that is used in the

accounts throughout the year. We have to use this estimate during the year as

often actual overheads are not known until the year end.

By the end of the year a certain amount of overhead will have been included

in the accounts:

Actual activity (e.g. actual units or labour hours) x budgeted OAR

Let's say our shop actually produced just 100,000 cakes (2000 less than

expected).

100,000 x £4.41 = £441,000

This is the overhead absorbed.

At the end of the year a business will be able to calculate its true overhead

cost but this will be different from that included in the accounts during the

year.

So, if in the cake shop, actual overheads are £420,000 and from the above

calculation £441,000 was included during the year then too much as been

included and we say there is 'over absorption'.

Actual overheads incurred – Overhead absorbed = Under-or Over-

absorption

£420,000 - £440,100 = (£21,100)

£21,100 over absorbed!

At the end of the year the over-absorption is added to the accounts to get the

figure back to the right overhead figure.

81

Costing systems I – Absorption and Marginal costing

Finally, we can sum up the steps in absorption costing in the following

diagram:

3. Marginal costing

Marginal costing is a much more simple costing method compared to

traditional absorption costing. Under marginal costing, fixed production costs

are not included in the cost of each unit of production and are instead treated

as 'period costs' which are written off in full against profit at the end of the

period.

You will recall that in absorption costing, we had “overheads” such as

rent, electricity and water and we found the cost of per unit (overhead

absorption rate) and added to the variable cost per unit to find the total

production cost per unit.

You don't need to worry about overheads when dealing with marginal costing.

Instead, we find what is known as the marginal cost:

82

Costing systems I – Absorption and Marginal costing

Direct materials + direct labour + variable overheads per unit

Using this we can find the contribution per unit:

Selling price per unit – (direct materials + direct labour + variable

overheads per unit)

Under this system, each unit we produce and sell gives us some money

which will help to pay off our fixed costs. After we add up our total

contribution (contribution x total unit sales), we deduct our fixed costs to

find the profit.

We can think of the marginal cost as the extra cost that is incurred as a result

of producing one more unit. Conversely, we can say that it's the cost saved by

producing one less unit.

4. The use of costing information in pricing decisions

Marginal cost pricing

It can be difficult to decide on how much we should mark-up the marginal cost by because we don’t consider the fixed cost. There could be overheads

that are not covered in our cost that may mean we don’t break even or make

profit.

Marginal cost pricing is most useful in situations where the pricing decision is

a one-off. This is for short term decisions and should not be used for

routine production.

Absorption cost (full) pricing

As we have seen, the full cost of the unit can be found once we have allocated the absorbed overhead costs. This makes is a lot easier to decide

how much we must sell our product for to make a certain amount of profit.

If we wish to make £20,000 profit and each product has a full cost of £5, we

know that by selling 4,000 units at £10 we will reach this target. £20,000 of our

£10,000 revenue will cover the cost of producing 4,000 units at £5. The

remaining £20,000 is profit.

5. Selling price methods

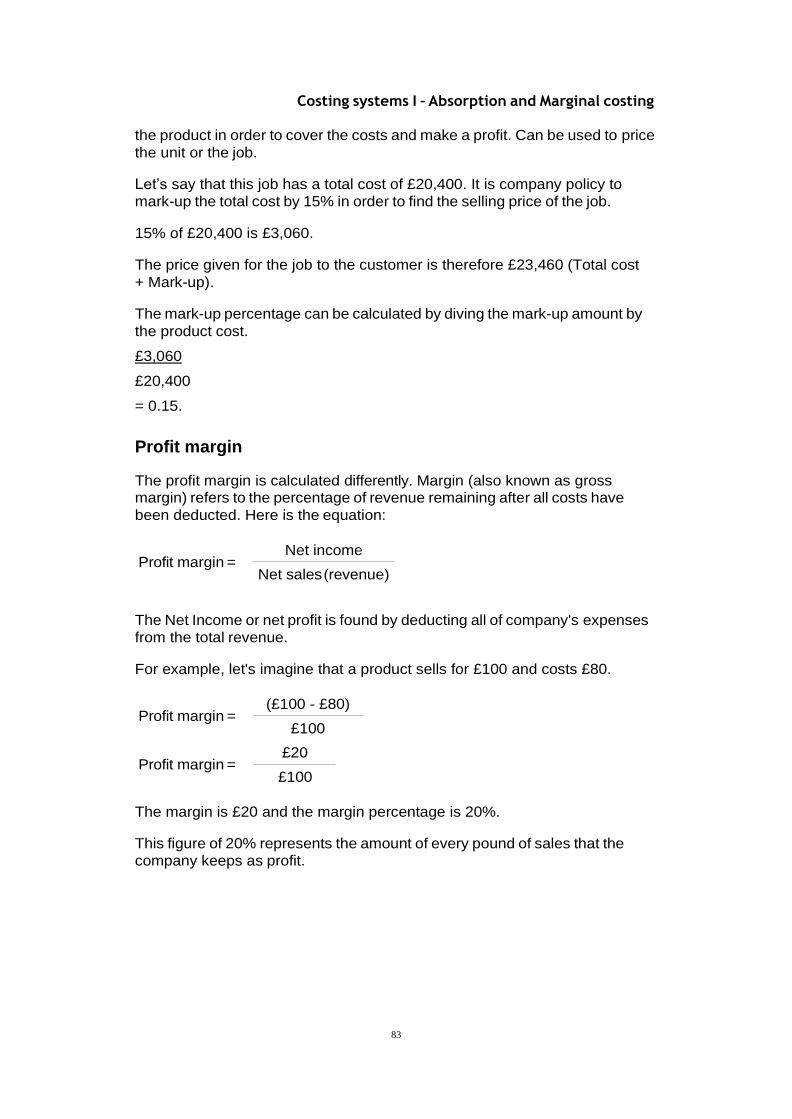

Profit mark-up

There are two methods that can be used to calculate selling prices, mark-up or

margin. Profit mark-up is the selling price of a product that is expressed as a

percentage of its total cost. A mark-up is added onto the total cost of

83

Costing systems I – Absorption and Marginal costing

the product in order to cover the costs and make a profit. Can be used to price

the unit or the job.

Let’s say that this job has a total cost of £20,400. It is company policy to

mark-up the total cost by 15% in order to find the selling price of the job.

15% of £20,400 is £3,060.

The price given for the job to the customer is therefore £23,460 (Total cost

+ Mark-up).

The mark-up percentage can be calculated by diving the mark-up amount by

the product cost.

£3,060

£20,400

= 0.15.

Profit margin

The profit margin is calculated differently. Margin (also known as gross margin) refers to the percentage of revenue remaining after all costs have

been deducted. Here is the equation:

Profit margin =

Net income

Net sales (revenue)

The Net Income or net profit is found by deducting all of company's expenses

from the total revenue.

For example, let's imagine that a product sells for £100 and costs £80.

Profit margin =

Profit margin =

(£100 - £80)

£100

£20

£100

The margin is £20 and the margin percentage is 20%.

This figure of 20% represents the amount of every pound of sales that the

company keeps as profit.

![[PPT]Presentation Outline - Jacksonville State University | … · Web viewChapter 5 Variable Costing Contains Fixed Manufacturing Overhead Presentation Outline Absorption Costing](https://img.dokumen.tips/doc/110x75/5b2897e87f8b9a2a498b4576/pptpresentation-outline-jacksonville-state-university-web-viewchapter.jpg)