Embed Size (px)

Citation preview

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

NO. 3JULY 2010

PAAMCO recognizes the importance of continuous research

into the markets and securities that create opportunity for

hedge fund managers. This series of papers addresses the

implications of emerging securities, trading strategies or

asset classes for the hedge fund industry.

This paper is for informational purposes only. PAAMCO

does not necessarily endorse or engage in these strategies.

The views in this piece are those of the author alone and do

not necessarily express the views of PAAMCO.

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIESby Putri Pascualy, Associate Director [email protected]

EXECUTIVE SUMMARY

A bank loan is a confi dential, private offering made by a company to qualifi ed banks and to accredited

investors. Bank loans are fl oating-rate instruments with seniority in a company’s capital structure,

are secured by a lien on the borrower’s assets and typically have more restrictive covenants than

bonds. As a result of these factors, bank loans have historically exhibited lower default rates and

higher recovery rates relative to bonds. Even so, there are a number of key risks to investing in bank

loans, including credit risk, liquidity risk, and settlement risk.

Bank loans have become an increasingly important instrument in the toolkit of a credit hedge fund

manager. The bank loan market enjoyed tremendous growth over the past two decades thanks to

increased loan supply from issuers as well as increased demand from institutional investors. The

formation of the Loan Syndication and Trading Association (LSTA) in 1995 led to the creation of

standardized market practices, which in turn led to a viable secondary market for bank loans and

contributed to the substantial growth of the loan market.

Putri Pascualy, MBA, CQF is an Associate Director at PAAMCO specializing in long/short credit strategy. Ms. Pascualy analyzes investment opportunities in credit markets and has expertise in bank loan and direct lending strategies.

T A B L E O F C O N T E N T S

I. Bank Loans Primer

A. Characteristics of Bank Loans

B. Investors in the Bank Loan Market

C. Key Developments in the Leveraged Bank Loan Market

D. Trading in the Secondary Market

E. Risks of Investing in Bank Loans

F. Loan Origination and Syndication Process

II. Investment Strategies in Bank Loans

A. Relative Value Trade

B. New Issue Trade

C. Balance Sheet Arbitrage

D. Stressed and Distressed Loan Trade

E. Debtor-in-Possession (DIP) Trade

Conclusion

Appendix

Bibliography

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

I. BANK LOANS PRIMER

A. Characteristics of Bank LoansGiven investors’ broad familiarity with bond markets, it is perhaps most straight-forward to explain bank loans by highlighting key differences relative to bonds:

• Bank loans are not securities. A bank loan is a confi dential, private offering made by a company (the “issuer”) only to qualifi ed banks and accredited investors (usually a syndicate of lenders). Unlike a public bond issuance, terms are often negotiated between the issuer and the syndicate.1

1 Prior to 2004, bank loans had no CUSIPs, i.e., they have no common identifi ers. In January 2004, the Loan Syndication and Trading Association (LSTA) and Standard and Poor’s, operator of the CUSIP Service Bureau, launched a service that provides CUSIP numbers for bank loans. Although the industry has yet to consistently adopt the usage of one set of common identifi ers across the board, the process of standardization of identifi ers for loans helped with secondary loan market trading.

Bank Loans are referred to by a myriad of other names in the market, including senior secured loans and syndicated loans.

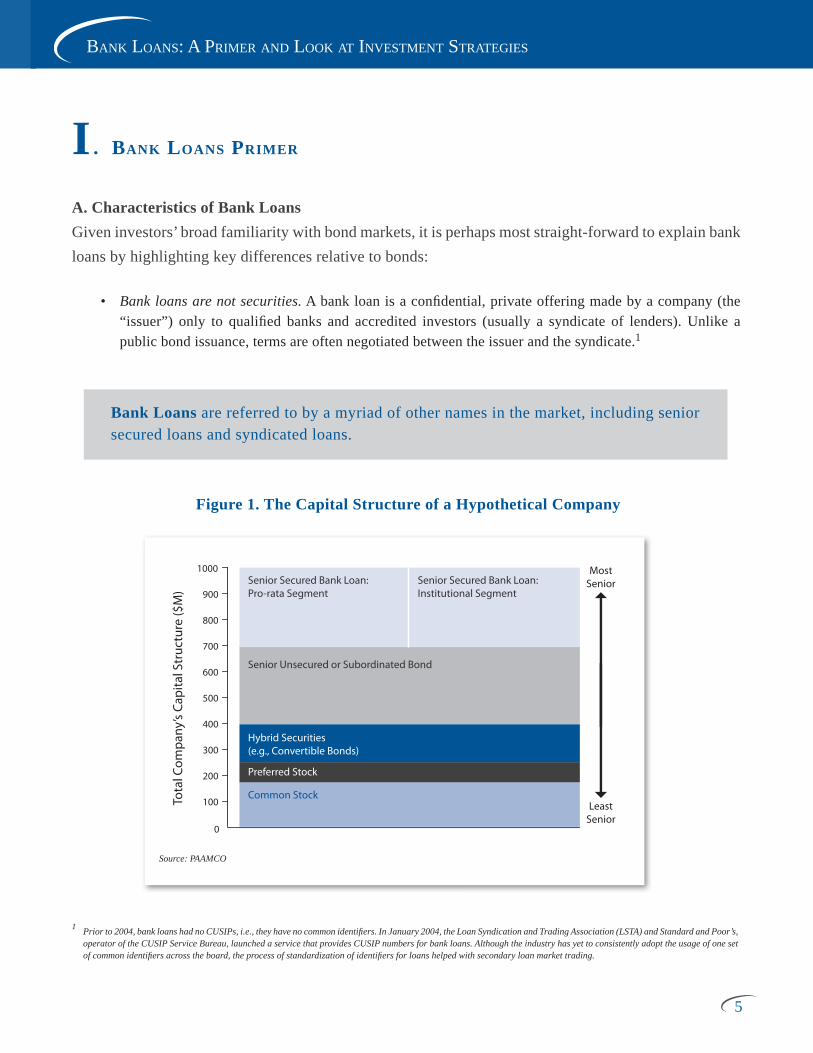

Figure 1. The Capital Structure of a Hypothetical Company

100

0

200

300

400

500

600

700

800

900

1000Senior Secured Bank Loan:Pro-rata Segment

Tota

l Com

pany

’s Ca

pita

l Str

uctu

re ($

M)

MostSenior

LeastSenior

Senior Unsecured or Subordinated Bond

Hybrid Securities(e.g., Convertible Bonds)

Preferred Stock

Common Stock

Senior Secured Bank Loan:Institutional Segment

Source: PAAMCO

5

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

• Bank loans are senior to bonds and most other securities. Bank loans sit at the top of a company’s capital structure (Figure 1). In the event of bankruptcy, loan obligations are secured by a lien on the borrower’s assets and are therefore senior to unsecured and subordinated bonds, to hybrid instruments as well as to preferred and common stock.2

• Bank loans are fl oating rate instruments. Coupons are typically quoted as a spread above a fl oating rate (e.g., 3 month LIBOR). In contrast, bonds have fi xed coupons. As a result, bank loans typically have lower interest rate duration than bonds. The interest rate component on bank loans is typically adjusted on a quarterly basis as LIBOR changes. Some loans include a LIBOR fl oor, which makes them attractive when LIBOR remains low for a prolonged period.

• Bank loans typically have stronger covenants than bonds.

-- Loans typically have more covenants. Fitch compared loan covenants against bond indentures for sub investment grade credits and found that a loan typically had 20 covenants versus 6 for bonds.3 Covenants provide loan investors with the ability to monitor performance of the borrower and/or limit the ability of the borrower to undertake certain actions that may impair the value of the loan investors’ claim. As such, more numerous covenants provide better protection for creditors.

-- Loan covenants typically are more restrictive than bond indentures. For example, loan covenants often include restrictions or requirements on mergers while bond indentures rarely contain similar language.

-- Loan covenants typically have a higher degree of enforceability. Loans are collateralized by a lien on the borrowers’ assets.

• Bank loans generally trade at a lower yield than the corresponding company’s bonds because of their relative seniority and lower risk.

• Bank loans’ market practices for trading, clearance and settlement differ from bonds. Loans and some bonds trade on the over-the-counter (OTC) market.4 However, unlike bonds, bank loans are privately negotiated contracts. It is common industry practice for secondary trading of a loan to be done through the agent bank, usually the bank most familiar with the unique details of that particular loan. There is currently no one industry-wide central depository that acts as a public database of loan information.5

2 Bankruptcy would include corporate reorganization (Chapter 11) or liquidation (Chapter 7) in the US. In this paper we focus on the legal system in the United States to illustrate our point. The concept of seniority applies across the globe, however the details and application of bankruptcy laws differ across the various legal jurisdictions within the European and Asian loan markets. Investors are advised to consult legal counsel with relevant expertise.

3 Mariarosa Verde, “Loan Preserver: The Value of Covenants”, Fitch, March 4, 1999.

4 Select bonds are traded on an exchange.

5 There are currently a few data providers (Reuters Loan Pricing Corporation and Markit) that provide database services for paying subscribers.

6

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

6 Industry convention defi nes par value of a bank loan at 100.

7 Historically, loans trading below 80 were considered distressed. However, the LSTA no longer uses price as an indicator for distressed loans because under that defi nition, almost the entire universe of large leveraged loans would have been considered distressed at one point in 2008 regardless of the health of the underlying borrower. Currently, whether a loan trades on par or distressed documents depends on several factors including potential for restructuring bankruptcy, likelihood of impending default, downgrade, and balance sheet trends.

One of the most signifi cant accomplishments of the LSTA was the establishment of a standard settlement process for loans trading near face value (“par”6 or “near par” loans). Industry convention is for par/near par loans to settle in T+7 (settlement date = trade date + 7 business days). Common industry practice is for distressed7 loans to settle in T+20. Distressed loans trade on a more complex set of documents than par loans. However, settlement time for both par and distressed loans can take substantially longer during times of heightened market volatility.

• The bank loan market does not have an established repo market to enable short-selling of bank loans. Unlike with cash bonds, there is currently no method to enable the short selling of cash loans.

The bank loan market can be categorized into two rating segments: investment grade and sub-investment grade/high yield loans. Sub-investment grade/high yield loans are defi ned as loans rated lower than BBB-/Baa3. Figure 2 compares the two segments. In the high yield segment, issuers carry higher levels of debt on their balance sheets. Leveraged loans refer to bank loans issued by issuers who carry higher levels of debt on their balance sheets relative to investment grade issuers (Figure 2). The focus of this paper is sub-investment grade/high yield loans, as hedge funds are typically focused on this segment of the loan market.

Figure 2. The Bank Loan Market by Rating

Source: Loan Pricing Corporation

7

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

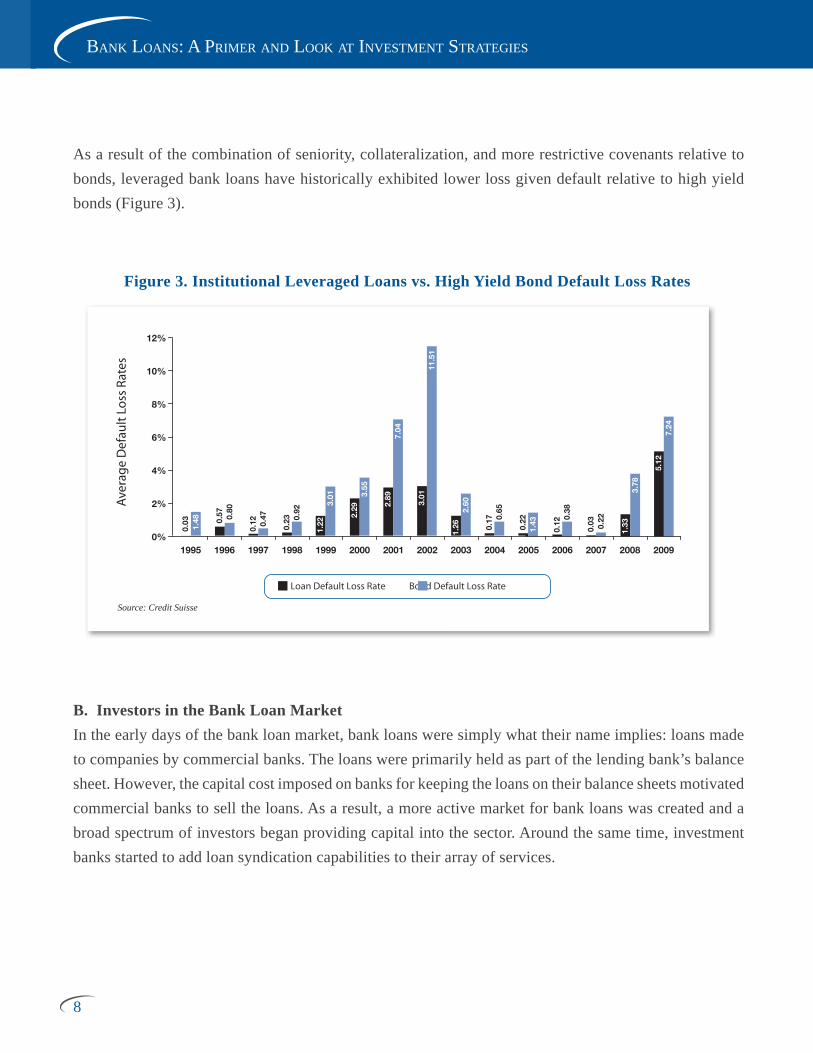

Figure 3. Institutional Leveraged Loans vs. High Yield Bond Default Loss Rates

As a result of the combination of seniority, collateralization, and more restrictive covenants relative to bonds, leveraged bank loans have historically exhibited lower loss given default relative to high yield bonds (Figure 3).

Loan Default Loss Rate Bond Default Loss Rate

Aver

age

Def

ault

Loss

Rat

es

Source: Credit Suisse

B. Investors in the Bank Loan MarketIn the early days of the bank loan market, bank loans were simply what their name implies: loans made to companies by commercial banks. The loans were primarily held as part of the lending bank’s balance sheet. However, the capital cost imposed on banks for keeping the loans on their balance sheets motivated commercial banks to sell the loans. As a result, a more active market for bank loans was created and a broad spectrum of investors began providing capital into the sector. Around the same time, investment banks started to add loan syndication capabilities to their array of services.

8

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

The sub-investment grade8 bank loan market can be broken into two main segments by investor types (Figure 4):

• The Non-Institutional or Pro-Rata segment refers to the piece of the loan facility that is held by bank investors.

• The Institutional segment refers to the piece of the loan facility held by non-bank investors (e.g., hedge funds, insurance companies, specialty fi nance companies and prime rate funds).

Compared to the pro-rata segment, the institutional segment of loans issued by sub-investment grade companies offers more attractive yield for institutional investors.

Figure 4. Pro-Rata and Institutional Segments of Bank Loans Market

Source: “Bank Loans: Secondary Market and Portfolio Management”, Edited by Frank Fabozzi, 1998

8 Loans issued by investment grade companies are in the form of revolvers as a backstop for their commercial paper facilities. A revolver or a revolving line of credit is a type of loan where the borrower can take out full or partial withdrawals up to a maximum predetermined amount. The amount available for borrowing is the difference between the size of the revolver and the current amount currently drawn. Once a payment has been made against the drawn amount, that amount will again be available for future borrowing. An example of a consumer-based revolving line of credit is credit cards. Corporations typically use revolvers to fund their short-term funding needs (e.g., backstop against commercial paper or to use as working capital).

9

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

Many institutional investors obtain their exposure to the loan asset class via Collateralized Loan Obligations (CLOs), which are structured vehicles investing primarily in loans. The CLO structure enables institutional investors to obtain exposure to a diversifi ed portfolio of bank loans under a specifi c set of risk characteristics.9 The rapid growth of the CLO market between 2003 and 2006 translated into increased demand for loans and the creation of more new loans. At the end of 2006, CLOs constituted more than 50% of the demand in the sub-investment grade loan market.

There are two types of CLOs with fundamentally different structures: market value and cash fl ow CLOs. Market value CLOs have liquidation triggers that depend on the market value of the underlying investments. As a result, the deterioration in the price of bank loans in early 2008 triggered the liquidation of most market value CLOs. This was structured to protect the senior CLO noteholders from signifi cant impairment.

Cash fl ow CLOs are less affected by the deterioration in the market value of the loans because unlike market value CLOs, a decline in market value of the loans alone will not trigger an event of default. Although the structure of a cash fl ow CLO is less sensitive to mark-to-market volatility in loan prices, during the peak of the credit crisis, cash fl ow CLOs saw their limits tested. Still, most of the cash fl ow structures managed to avoid triggering the event of default clause. This is because cash fl ow from the underlying loans, the allowable amount for lower rated and defaulted assets, as well as the degree of portfolio diversifi cation all collectively play roles in determining the overcollateralization test for the structure. Multiple breaches have to take place before an event of default10 is triggered. As of mid-2010, the majority of CLOs still in existence are cash fl ow CLOs.

9 In a Collateralized Loan Obligation structure, investors can gain exposures with different risk and return characteristics to one diversifi ed portfolio of bank loans. For example, imagine a portfolio of loans and two investors. Investor A requires an investment grade rated investment with positive cash fl ow and wants any early prepayment of principal to go to him. Investor B has a longer term perspective, higher risk tolerance and is willing to trade positive cash fl ow for a higher return expectation. The portfolio of loans would be put into a vehicle and two different claims would be issued using the loans in the vehicle as collateral. Investor A receives an investment grade note that pays periodic coupons and has priority claim on all the prepayments from the underlying bank loans until the note is paid off in full. Investor B does not expect a periodic coupon payment, but benefi ts from any excess cash fl ow from the underlying loans after investor A has been paid. The tranching of cashfl ows (i.e., Investor A is ahead of Investor B in the line for cash from the underlying bank loans) is often referred to as a payment waterfall. Investor B benefi ts from increased value of the underlying bank loans, however Investor B absorbs any loan losses until his claims are exhausted before the losses start to impair the claims of Investor A. Investor A benefi ts from the structure, which was created to provide some protection against signifi cant impairment while Investor B benefi ts from potential upside in exchange for taking additional risk.

10 Generally an event of default in a CLO structure means that the “Controlling Class” (typically the most senior outstanding notes) has the right to demand accelerated repayment of their principal and direct the liquidation of the underlying assets.

10

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

C. Key Developments in the Leveraged Bank Loan Market

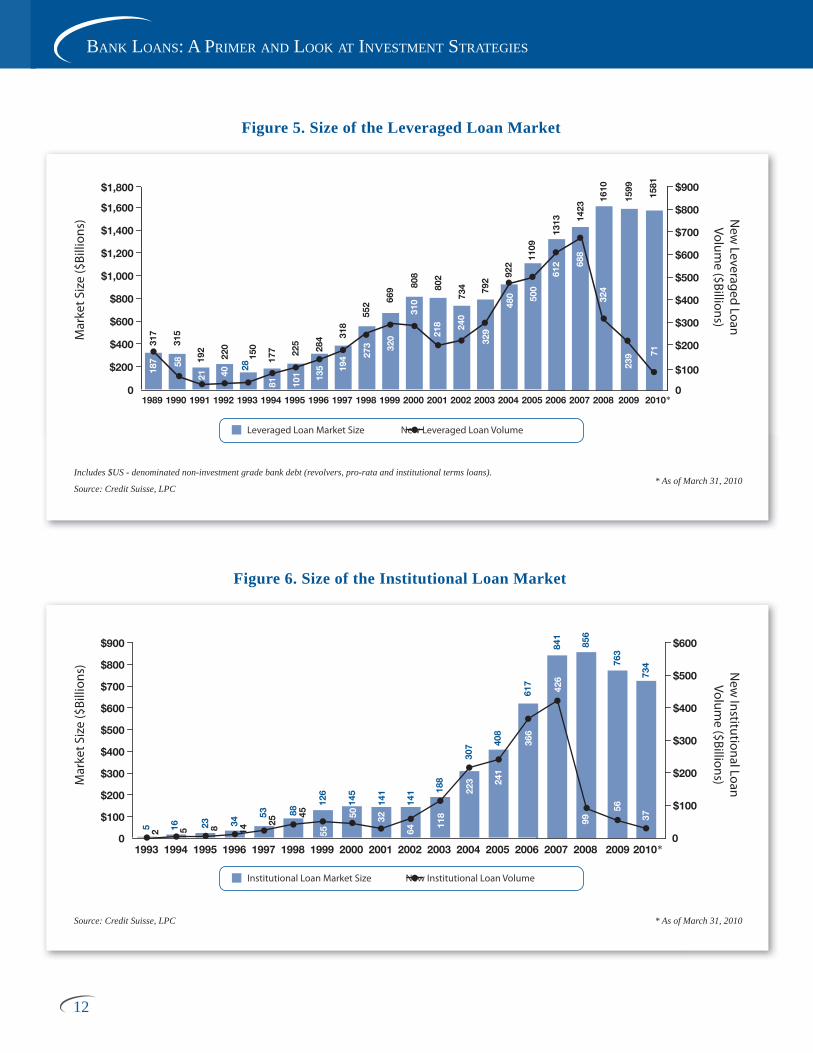

The leveraged loan market grew from $317 billion in 1989 to $1.6 trillion11 in 2009, a 400% increase

(Figure 5). Demand for the institutional segment increased from virtual non-existence in 1993 to $763

billion in 2009 (Figure 6), or nearly half of the total leveraged loan market.

Several factors drove this substantial growth:

• The supply of leveraged bank loans increased because leveraged companies found it preferable to issue loans rather than bonds due to the lower fi nancing cost. In addition, banks sold part of their loan portfolios in order to manage their capital and regulatory requirements. Banks also found capturing the fee associated with the syndication process of arranging, packaging and selling loans, to be a more effi cient use of capital and an attractive alternative to investing in the loans.

• The development of a viable secondary market for loans was a key factor and was aided by the creation of the Loan Syndication and Trading Association (LSTA)12 in 1995. The creation of the secondary market gave lending banks access to investors. Lending was no longer limited to the size of the banks’ balance sheets. According to the LSTA, the secondary trading volume of loans grew from $50 billion in 1Q05 to $110 billion in 1Q10.13 The opening of an active secondary trading market was a welcome development to an asset class that had been long perceived as illiquid.

• Demand for leveraged loans increased because ratings-sensitive investors (e.g., insurance companies) wanted to invest in the highly-rated tranches of CLOs.14

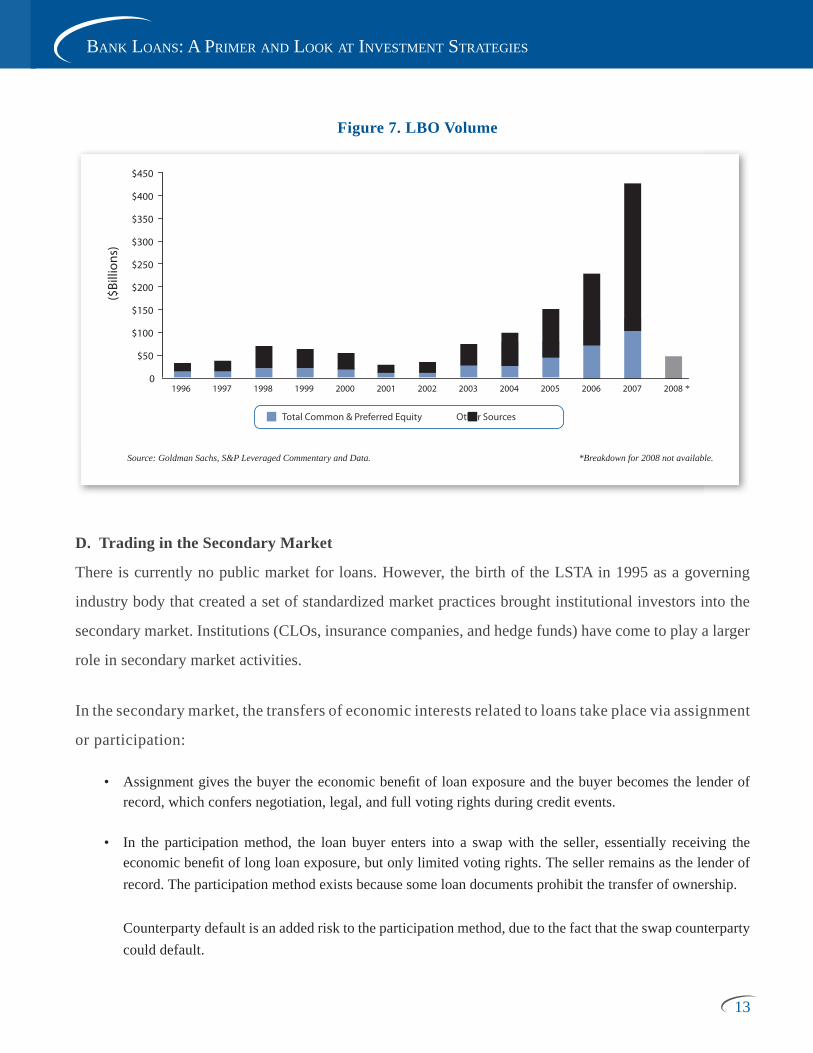

• The presence of CLOs as a robust source of demand for loans compressed the cost of borrowing in the loan market. Leveraged buyout (LBO) investors15 came into the market to take advantage of the widely available and attractively priced fi nancing. In 2004 the volume of LBO deals increased and peaked in 2007. Much of the fi nancing came from bank loans, which contributed to further growth in the bank loan market. Figure 7 shows past annual LBO volume broken down into equity vs. non-equity sources.

• As secondary market trading developed, institutional investors came to the bank loan market. Their motivations varied as some sought to diversify their existing portfolios, others aimed to take advantage of select periods of price displacement in the loan market, while others sought to benefi t from the balance sheet arbitrage trade.16

11 Includes $US-denominated non-investment grade bank debt.

12“The Loan Syndication and Trading Association promotes a fair, orderly, and effi cient corporate loan market and provides leadership in advancing the interests of all market participants.” Source: www.lsta.org

13 Source: www.lsta.org

14 The remaining equity tranches are often retained by the CLO manager.

15 A leveraged buyout is a transaction when investors acquire a company using borrowed money to fi nance the acquisition. Investors can be private equity fi rms or management of the acquired fi rm.

16 See section II “Trading Strategies in Bank Loans” for more information.

11

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

Figure 6. Size of the Institutional Loan Market

Institutional Loan Market Size New Institutional Loan Volume

Source: Credit Suisse, LPC * As of March 31, 2010

Source: Credit Suisse, LPC

Includes $US - denominated non-investment grade bank debt (revolvers, pro-rata and institutional terms loans).* As of March 31, 2010

Figure 5. Size of the Leveraged Loan Market

New

Leveraged LoanVolum

e ($Billions)M

arke

t Siz

e ($

Billi

ons)

Leveraged Loan Market Size New Leveraged Loan Volume

Mar

ket S

ize

($Bi

llion

s) New

Institutional LoanVolum

e ($Billions)

12

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

D. Trading in the Secondary Market

There is currently no public market for loans. However, the birth of the LSTA in 1995 as a governing

industry body that created a set of standardized market practices brought institutional investors into the

secondary market. Institutions (CLOs, insurance companies, and hedge funds) have come to play a larger

role in secondary market activities.

In the secondary market, the transfers of economic interests related to loans take place via assignment

or participation:

• Assignment gives the buyer the economic benefi t of loan exposure and the buyer becomes the lender of record, which confers negotiation, legal, and full voting rights during credit events.

• In the participation method, the loan buyer enters into a swap with the seller, essentially receiving the economic benefi t of long loan exposure, but only limited voting rights. The seller remains as the lender of record. The participation method exists because some loan documents prohibit the transfer of ownership.

Counterparty default is an added risk to the participation method, due to the fact that the swap counterparty

could default.

13

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

($Bi

llion

s)

Source: Goldman Sachs, S&P Leveraged Commentary and Data. *Breakdown for 2008 not available.

Figure 7. LBO Volume

Total Common & Preferred Equity Other Sources

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

$50

$100

$150

$200

$250

$300

$350

$400

$450

0

101

*

E. Risks of Investing in Bank Loans

As with all investments, bank loans involve a number of key risks:

• Credit Risk: This involves default risk and uncertainty in loss given default. As usual, this is a particularly salient risk for below investment grade issuers.17

• Liquidity Risk: Loans are not “securities” and there is no public market for loans. Therefore, certain segments of the loan market are subject to substantial liquidity risk, over and above the usual liquidity risk of high-yield bonds from the same issuer.

This risk is more signifi cant for smaller loans. The larger, more liquid bank loans (“fl ow names”) usually have deep liquidity. For example, the size of the institutional segment of Hospital Corporation of America (HCA)’s November 2006 loan issuance was $8.8 billion. In comparison, the average equity capitalization of a name in the Russell 100018 equity index (which is considered to be liquid) is approximately $10 billion. HCA is one of the more liquid names in the bank loan market, but is certainly not alone in terms of the liquidity it enjoys. Examples of other bank loans with high liquidity include EFH (previously TXU), Charter Communications, Wrigley’s, and Ford.

• Settlement Risk: Because of the more complex nature of bank loan documents relative to other securities, bank loans take substantially longer to settle than bonds and equities. Distressed loan trades, which are still largely paper-based, involve a more complex set of documents and take longer to settle than par loans. Longer settlement time increases counterparty risk. The additional operational complexities related to bank loans necessitates a knowledgeable and experienced back offi ce for timely completion of the trade. Firms often outsource the back offi ce work for distressed loans to specialists.

Unlike bonds, a bank loan trade (i.e., the loan assignment process) requires consent from the agent banks and possibly from the borrower. Further delays to the settlement time can result from an unresponsive agent bank, a possible retraction of previously given consent, an absence of a standard assignment agreement and the need to obtain physical signatures. Furthermore, internal procedures for the assignment process vary across various agent banks.

• Mark-to-Market Risk: This occurs when the secondary market prices drop, refl ecting increasing concerns about default. Such risk is not inherent in bank loans themselves, but is particularly relevant for loan investors who use leverage through Total Return Swaps (TRS) or through participation swaps and for market value CLOs.

17 Default risk is simply the risk that the borrower fails to pay interest and/or principal as promised. Credit analysis on a company’s current and future revenue, market share cost structure, quality of management, cash fl ow generation and profi tability form a key part of evaluating default risk. A company’s size and access to fi nancing also play an important part in assessing default risk. If an issuer is unable to issue new debt or equity to replace a loan that is due, default is likely unless the issuer has enough cash to repay the principal outright. Upon default, loss given default measures how much impairment is suffered by the lender. Valuation of collateral backing the loan (if any) and the amount of debt junior to the loan are important in determining loss given default (or consequently, recovery amount). Source: Standard and Poors

18 “The Russell 1000 Index measures the performance of the large-cap segment of the U.S. equity universe. It includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000 represents approximately 90% of the U.S. market.” Russell 1000 Index Fact Sheet, www.russell.com

14

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

Due to the historical low yield and low volatility of loans, many loan investors leverage up their loan exposure. The most popular of these leverage mechanisms are Total Return Swaps (TRS) and CLOs, some of which have market value triggers. During the height of volatility in the loan market in 2008, many of these market value triggers were hit, prompting a vicious cycle of selling and price decline.

• Swap Counterparty Risk: Investors who obtain their loan exposure through the participation method can suffer losses if the counterparty fails to meet its swap obligations, even if the underlying asset on the swap is performing.

• Legal and Taxation Risk: This is relevant for non-taxable investors investing in loans via the origination process (as part of a syndicate), participation, or exposure to a revolver since they could subject the investor to Effectively Connected Income (ECI).19 As with all tax related matters, investors are advised to seek advice from tax counsel.

F. Loan Origination and Syndication Process

A company interested in entering the bank loan market interviews commercial and investment banks

to serve as arrangers. The arrangers present their proposed terms and pricing as well as strategy. A lead

arranger (“book runner”) is selected to carry out the deal.

The lead arranger puts together an information memo (IM) for potential investors. Key information in

the IM includes proposed terms and pricing of various parts of the loan package and the borrower’s

fi nancial information. Potential investors must select whether to have access to the borrower’s private

fi nancial information including internal projections. If they choose to have such access, the investors

are considered to be “over the wall” (i.e., in possession of material non-public information) and are

restricted from trading in the borrower’s public securities. For large issuers with multiple prior issuances

of publicly traded securities and broad availability of publicly available information, investors often

choose to forgo access to private information in order to remain unrestricted.

Since the late 1990s, most of the deals in the United States have been done on a “best efforts” basis.

This method means that the arrangers are not committed to sell the entire loan package, unlike in the

19 Cleary, Gottlieb, Stein & Hamilton, “IRS Chief Counsel Memo on Loan Origination by Foreign Entities,” Alert Memo, September 23, 2009. Kaye Scholer LLP, “IRS Issues Guidance On U.S. Lending Activities By Non-U.S. Investor”, Tax Department, October 2009.

15

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

underwriting method where the underwriter is committed to sell a pre-determined amount of the loan

package. In an underwritten deal, the “market fl ex” language, which saw an increase in popularity in

the late 1990s, effectively reduces the underwriters’ commitment risk. The “fl ex” language allows the

arrangers some fl exibility (within a pre-determined limit) to modify terms and pricing of the loan in

order to better refl ect investors’ risk return appetites. For example, in a market where investors are

more risk averse, the “fl ex” language allows banks to offer either a higher interest rate or lower pricing

on the loan, effectively increasing investor yield. Reverse “fl ex” language is used to reduce yield in

an oversubscribed offering.

Another type of deal is the “club deal”. Popular in Europe and with smaller deals in the United States

($100 million and under), the loan is pre-marketed to a small group of lenders.

Figure 8. Top 10 US Leveraged Loan Underwriters - 2009

Source: Bloomberg

16

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

II. INVESTMENT STRATEGIES IN BANK LOANS

The examples below illustrate some of the motivations for hedge funds to add bank loan exposure

to their portfolios.

A. Relative Value Trade

A popular Relative Value Trade is a capital structure arbitrage trade that involves going long a bank

loan and shorting a more junior part of the capital structure (of the same or different issuer) such as

the subordinated bond or equity. In the event of credit spread widening, the trade profi ts from the short

bond and equity position while the long loan exposure is expected to hold its value due to seniority,

collateralization and covenants.

Another variation of the relative value trade is to go long and short bank loans of different issuers, which

relies on the hedge fund manager’s credit research skills. Short exposure to individual bank loans can now

be obtained through Loan Credit Default Swaps (LCDS)20. However, this market was launched immediately

prior to the 2008 credit crisis21 and as a result the liquidity of single name LCDS has been limited.

Profi table execution of the relative value loan trade hinges upon a fund manager’s fundamental credit

research. This would include a strong understanding of company valuation, fi nancial analysis, market

comparables and capital structure (which is getting increasingly complex, particularly in an environment

where companies have created various off-balance sheet vehicles) and parent/subsidiary relationships.

This trade typically works best in periods of economic recovery and expansion where if the market

value of an instrument is trading far from the fundamental value, pricing and valuation will converge

in a reasonable amount of time. Similarly, the trade does not work when the market is largely driven by

technical and other non-fundamental factors.

20 Loan Credit Default Swaps have similar structure to regular (Corporate) Credit Default Swaps. The fi rst meaningful difference between them is that the underlying reference obligation is a bank loan as opposed to a bond. The second key difference is that a Loan Credit Default Swap contract is cancelled if the underlying loan is called by the issuer.

21 ISDA published standardized documents for LCDS on June 8, 2006.

17

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

B. New Issue Trade

A New Issue Trade results in a profi t when an investor purchases a newly issued bank loan at a discount

to par value and receives upfront fees, then resells the loan into the secondary market at par a few days

after. The discount is referred to as Original Issue Discount (OID) and it is part of the “market fl ex”

language that arrangers can use to make a new issue bank loan more attractive to investors. In select

deals, investors also receive upfront fees from the issuer at the close of the syndication process. Larger

commitments tend to receive larger upfront fees, which are typically expressed as a percentage of

commitment size. Having established relationships with loan syndicate desks plays an important part in

a hedge fund manager’s ability to access the new issue loan market. Access to major underwriter banks

is particularly important in Europe, where club deals are more popular than in the US.

This trade works best in periods where the loan market enjoys a healthy balance of new issue supply

and demand. During periods of economic contraction, low investor appetite for bank loans may result

in select new loan issues offering higher OID and upfront fees. However, the initial investor may not be

able to turn around and realize the gain to par if the demand in the secondary market is weak. In 2009,

the loan market was effectively closed. In contrast, the high yield bond market was wide open due to

strong investor appetite and better investor familiarity with high yield bonds relative to bank loans.

Issuers turned to the high yield bond market and the resulting reduction in the volume of new issue loan

market gave rise to lower than expected upfront fees and OID.

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

18

C. Balance Sheet Arbitrage

A basic Balance Sheet Arbitrage trade profi ts by using lower cost fi nancing to invest in higher yielding

assets. Loan investors can obtain leveraged exposure to the asset class through a Total Return Swap

(TRS). A TRS is a bilateral agreement that allows counterparties to swap the total return of a single

asset or a basket of assets22 in exchange for a fl oating rate (typically LIBOR) plus a swap spread. A TRS

is similar to a plain vanilla swap, except in a TRS the total return of the asset (i.e., cash fl ows and price

appreciation and depreciation) is swapped as opposed to just the cash fl ows.

Another form of the Balance Sheet Arbitrage is the LIBOR arbitrage. This opportunity arises when a

LIBOR-based TRS line is used to fi nance a loan with a LIBOR base set at a minimum that is higher than

current LIBOR. The investor profi ts when LIBOR is lower than the minimum LIBOR on the asset.23

D. Stressed and Distressed Loan Trade

Stressed and Distressed Loan Trades appeal to distressed debt investors who typically look to invest

in the fulcrum security within a company’s capital structure. A fulcrum security is the security that is

most likely to convert to equity in the reorganization process. The 2003-2006 LBO boom has placed

an unprecedented amount of leverage on companies’ balance sheets. Much of the added leverage was

in the form of bank loans, which has the impact of pushing the fulcrum security further up the capital

structure. This means that in certain situations the bank loan can be the fulcrum security.

22 These assets are referred to as reference asset(s). In addition to bank loans, a TRS can be structured on various types of reference assets including single equities and bonds, equity and bond indices, leases, real estate, ABS, etc. For a detailed illustration of this trade please see the appendix.

23 Arbitrage profi t from the LIBOR arbitrage can be calculated by Max((LIBOR fl oor of asset – LIBOR),0) * (Leverage - 1)

19

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

An example of this trade involves a company that is currently undergoing restructuring under the

Chapter 11 process. Assume that the company’s book liabilities are $100M in bank loans and $100M in

unsecured bonds. Around the announcement of the Chapter 11 fi ling, a distressed investor may be able

to purchase the loan at depressed prices, which refl ects the heightened market risk premium from the

uncertainties surrounding the bankruptcy process.

Let us consider two basic scenarios:24 a short term profi t opportunity and a loan-to-own opportunity. In

the fi rst scenario, assume the fi rm is valued at $150M. In this scenario, the claim of the loan investors are

fully covered at par, pre-Chapter 11 equity holders see their claims extinguished and $50M remains for

unsecured bondholders. This trade profi ts when the loan price appreciates to par. In the second scenario,

the fi rm is valued at $90M. The loan holders receive $90M and all of the company’s equity for their

$100M claim, while the claims of the bondholders and equity holders are extinguished. If the company

emerges from the bankruptcy process as a viable entity, this trade profi ts as loan holders become the sole

owners of the post-bankruptcy entity. Furthermore, during the restructuring process, the loan holders can

expect to receive default interest, which can add 1-2% above the non-default spread level.

The main risk of this trade clearly lies in the navigation of the bankruptcy and restructuring processes.

Determining the valuation of a company in bankruptcy is challenging. Various interest groups

(shareholders, company management and creditors) with competing interests will advance valuations

that maximize their expected economic outcome. Cross-class litigation is a real possibility and timing

risk can be signifi cant, as some companies have gone through long, drawn-out restructuring processes

that can take years. The trade requires strong legal and negotiation capabilities in addition to valuation

and investing skills. Distressed investing may include involvement in creditors and other committees,

which are time and labor intensive. Members in the creditors committee are also subject to certain

trading restrictions.

24 Assumptions (for simplicity’s sake): adherence to seniority and no expenses (fi ling cost, legal cost, trustee and other administrative fees) and no outstanding obligations that are senior to the bank loan holders (e.g., outstanding contributions to employee benefi t plans, tax liens, etc.) associated with the bankruptcy process.

20

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

E. Debtor-In-Possession (DIP) Trade

During the Chapter 11 process, a Debtor-in-Possession (DIP) loan provides the company the working

capital it needs in order to operate as a going concern. A DIP lender receives “super priority” status

via a lien that receives priority relative to the pre-bankruptcy bank loan lenders (a “priming lien”). DIP

loans typically carry larger coupons than the pre-bankruptcy bank loans and will also include other

sweeteners including commitment and closing fees.

A priming lien can only be granted with the consent of the primed pre-bankruptcy bank loan holders

(pre-petition lenders in bankruptcy jargon) or if the court decides that the claims of the pre-petition

lenders are suffi ciently protected by the value of the company’s assets despite the priming lien. The

pre-petition lenders would consent to being primed because the company (and thus the assets that

collateralize their claim) is worth more as a going concern than if the company were forced to liquidate

due to a lack of funds to maintain day-to-day operations.

To prevent priming, pre-petition lenders can provide DIP fi nancing, which is referred to as a “defensive

DIP” in bankruptcy jargon. If a new set of lenders provide DIP fi nancing, this is referred to as “new

money DIP” or “offensive DIP”. Coupon and fees tend to be lower for a defensive DIP and higher

for an offensive DIP.

A DIP lender faces extension and exit risk. The increasingly complex capital structures of issuers

combined with a wide range of interests in the creditor groups can lead to a protracted and contentious

restructuring process. Valuation battles may be particularly diffi cult in an environment where companies

face an uncertain economic outlook. Lastly, a DIP lender needs an open and functioning capital market

to ensure availability of exit fi nancing.

21

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

CONCLUSION

The bank loan market has undergone signifi cant changes since its early days. Standardized market

practices, particularly in regards to trading, settlement and documentation, have gone a long way towards

creating an actively functioning secondary market, improving liquidity and expanding the number and

type of market participants.

During the credit crisis of 2007-2008, the loan market saw unprecedented volatility. Much of the

volatility was exacerbated by excessive leverage in many of the vehicles through which investors

obtained exposure to bank loans. Many of the excessively leveraged bank loan vehicles have left the

market. The low supply of new loans met relatively high demand in 2009, creating a highly favorable

technical tailwind for bank loans. The loan market continues to heal as banks are slowly offering

new fi nancing for bank loans, although this time around the banks are more conservative about size,

terms, and pricing of fi nancing facilities. Existing CLOs continue to provide a level of support to the

secondary bank loan market. There is potential for newly issued CLO vehicles, albeit with lower levels

of leverage and simpler structures. Outside the CLO market, investors with favorable rates of funding

can still benefi t from the arbitrage opportunities while stressed and distressed credit hedge funds look

to generate attractive returns on an unlevered basis.

Bank loans and the loan market will continue to provide leveraged issuers with an attractive fi nancing

method while presenting opportunities for institutional investors. Nonetheless, institutional loan

investors face unique risks due to the specifi c characteristics of the instrument and the loan market.

22

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

APPENDIX:

Figure 9 shows an example of a TRS on $10M of a bank loan trading at par that pays LIBOR + 350bps.

The Total Return Payer is the party who owns the loan and passes on the economic benefi ts of owning

this asset to the Total Return Receiver in exchange for the fl oating payment. The payer receives the

swap spread of LIBOR + 100bps, for example, on a notional of $10M and pays the total return on the

loan. This total return consists of coupon payments, fees, amortization payments, price appreciation

and depreciation. Total return can be negative if the loan price falls.

Figure 9. Total Return Swap

23

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

25 The number of days required as notice period can be found in the ISDA agreement.

26 Leverage measured as Market Value of Asset/Equity.

27 Economically, the Total Return Swap is similar to the reverse repo transaction. However, under tax and accounting rules, ownership of asset is not transferred in a Total Return Swap (unlike in a reverse repo transvaction), which makes a TRS faster and easier to set up. This is important for loan investors, where the sale/transfer of the loan may have to be approved by the issuer and potentially the lead agent.

28 Between 1992 – 2007, the highest annual volatility of the Credit Suisse Leveraged Loan Total Return Index was 4.4% (2007) and the second highest annual volatility was 4.01% (2002).

The Receiver also puts forth $2.5M cash (25% margin rate) as collateral, which is invested in Treasuries.

This lowers the counterparty credit risk in situations where the loan drops in value and the Payer

should receive a large payment. The collateral requirement changes as the market price of the loan

fl uctuates and the Total Return Payer usually has the right to change the margin rate with reasonable

notice to the Receiver.25

In the scenario described above, the receiver borrows at LIBOR + 100bps to obtain an asset that yields

LIBOR + 350bps. The receiver only had to come up with $2.5M worth of capital to obtain $10m exposure

to the bank loan (i.e., 4x leverage).26 This use of TRS as a funding mechanism renders it similar to a

synthetic reverse repo.27 The swap receiver’s ability to use the TRS as a way to obtain leverage vehicle

for bank loans is a reason why the swap has been popular with hedge funds and other parties with

high fi nancing cost. Banks and other low cost borrowers are natural payers in this swap. The main risk

assumed by the investor (the receiver in the TRS) is the credit risk of the bank loans (the reference

assets). To a lesser extent, the receiver is also exposed to the credit risk of the swap payer. The higher the

credit risk of the swap payer, the lower the swap spread and/or margin charged to the swap receiver. The

leverage embedded in the use of the TRS magnifi es the risk and return of the investor’s loan exposure.

Historically, given very low volatility on bank loans,28 moderate leverage on bank loans provided an

attractive risk/reward profi le for institutional investors.

24

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

29 In many Total Return Swap agreements, a drop of NAV or performance beyond a pre-set threshold constitutes a termination event. This means the Total Return Swap Payer has the right to terminate the TRS agreement after notifying the TRS receiver. The fi nancing provided by the TRS payer to purchase the reference assets becomes due in full. The TRS Receiver has two options: repay the TRS Payer in cash or the Payer will sell the underlying assets in order to generate the cash.

30 In a loan BWIC, a list of bank loans will be offered for sale for a limited amount of time via a loan broker/dealer, who will collect the bids from interested parties.

31 Assume the case of a TRS with an AUM liquidity trigger with a hedge fund as the swap receiver. If the hedge fund loses more than a certain amount of AUM within a certain period of time as a result of negative performance and/or investor redemptions, the liquidity trigger is breached. The fi nancing provided by the swap payer is immediately due in full. The swap receiver either has to provide the cash or the swap payer has the right to seize and sell the underlying collateral.

However, the credit events of 2008 have demonstrated the effect of mark-to-market triggers on leverage

facilities.29 When bank loan prices declined, many of the liquidation triggers were hit and widespread

forced selling took place as Total Return Swap lines were unwound and the assets liquidated via the “Bids

Wanted In Competition” Process (BWIC)30. The crisis highlights the importance of understanding the

terms of a leverage facility, particularly when leverage providers have the right to terminate the facility.

Some key terms include liquidity triggers (a drop in assets under management and/or performance

triggers31 are the most common), recourse features, length of cure periods and notice periods. In the

event of a trigger breach, cure and notice periods provide investors with valuable time and an option that

can possibly delay or deter forced liquidation from happening.

25

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

BIBLIOGRAPHY:

Acciavatti, Peter, Tony Linares and Nelson Jantzen, “2009 High-Yield and Leveraged Loan Outlook and Strategy,” JP Morgan, December 11, 2008.

Antczak, Stephen, Douglas Lucas, George Bory, Chris Hazelton and Jung Lee, “A Look at Liquidations,” UBS Investment Research, October 10, 2008.

Antczak, Stephen, Douglas Lucas, George Bory, Chris Hazelton and Jung Lee, “A Primer on the Leveraged Loan Market,” UBS Investment Research, October 14, 2008.

Blau, Jonathan, Miranda Chen, Daniel Sweeney and Janet Yung, “Leveraged Finance Strategy Update,”Credit Suisse, October 1, 2009 and April 9, 2009.

Cleary, Gottlieb, Stein & Hamilton, “IRS Chief Counsel Memo on Loan Origination by Foreign Entities,” Alert Memo, September 23, 2009.

Fabozzi, Frank, “Bank Loans: Secondary Market and Portfolio Management,” Frank J. Fabozzi Associates, 1998.

Kaye Scholer LLP, “IRS Issues Guidance on U.S. Lending Activities by Non-U.S. Investor,” Tax Department, October 2009.

Loan Syndications and Trading Association, “User’s Guide for LSTA Distressed Trading Documentation,” www.lsta.org.

Markit, “Index Methodology for the CDX Indices (“Index Methodology”),” August 31, 2007.

Markit, “LCDX: The New North American Loan-Only Credit Default Swap Index,” May 21, 2007

Markit, “Markit Credit Indices: A Primer,” July 2009.

Markit, “Markit LCDX Primer.”

Rogoff, Brad, “Loan Market Opportunities,” Lehman Brothers, February 2008.

Standard and Poors, “A Guide to the Loan Market,” October 2008.

Thomson Reuters Loan Pricing Corporation (LPC).

26

BANK LOANS: A PRIMER AND LOOK AT INVESTMENT STRATEGIES

Pacifi c Alternative Asset Management Company®, LLC (“PAAMCO®”) is an institutional fund of hedge funds investment fi rm dedicated to offering strategic alternative investment solutions to the world’s preeminent sophisticated investors. PAAMCO’s clients include large public and private pension plans, foundations, endowments, and fi nancial institutions. Located in Irvine, California, with a European offi ce in London, Pacifi c Alternative Asset Management Company Europe®, LLP (“PAAMCO Europe®”), and an Asian offi ce in Singapore, Pacifi c Alternative Asset Management Company Asia®, Pte. Ltd. (“PAAMCO Asia®”), the fi rm is committed to meeting the needs and demands of its global institutional client base both now and in the future. PAAMCO is registered with the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission, and is a member of the National Futures Association. PAAMCO Europe is authorized and regulated by the Financial Services Authority. PAAMCO Asia is an Exempt Fund Manager and Exempt Financial Advisor under the Monetary Authority of Singapore.

Pacifi c Alternative Asset Management Company, LLC19540 Jamboree Road, Suite 400Irvine, CA 92612 United StatesTel: +1 949 261 4900Fax: +1 949 261 4901

Pacifi c Alternative Asset Management Company Europe, LLP25 Victoria StreetLondon SW1H 0EX United KingdomTel: +44 20 7593 5360Fax: +44 20 7593 5361

Pacifi c Alternative Asset Management Company Asia, Pte. Ltd.167/169C Telok Ayer StreetSingapore 068620Tel: +65 6594 2400Fax: +65 6594 2401