Embed Size (px)

DESCRIPTION

it gives the awareness on microfinance

Citation preview

Awareness of Microfinance in Urban India 2013

DECLARATION

I, Disha Tiwari, student of Master of Management Studies

(Finance), Jankidevi Bajaj Institute of Management Studies

(JDBIMS), S.N.D.T Women’s University, Mumbai, declare that

the work done, and the project report titled ‘Awareness of

Microfinance in urban India, is original work carried out by me.

All references, made to any published material in this report,

have been duly acknowledged.

This report has not been submitted to any University / Academic

Institution for the award of any degree or diploma.

I solemnly declare that I am singularly responsible for any

infringement on the Intellectual Property of anybody else in this

report.

Place: Mumbai

Date: 22nd April, 2013

Disha Tiwari

1

Awareness of Microfinance in Urban India 2013

ACKNOWLEDGEMENT

This research project is made possible through the help and support from everyone,

including: teachers, family, friends, and in essence, all sentient beings.

Especially, please allow me to dedicate my acknowledgment of gratitude toward the

following significant advisors and contributors:

First and foremost, I would like to thank my project guide Dr. Nitin Wani for his support

and encouragement. He gives me timely guidelines and offered invaluable detailed

advices on grammar, on subject of the project and logical way to proceed further in the

project.

Second, I would like to thank Mr.Narayan Bhaskar, administrative head of the Svasti

Microfinance Pvt ltd who allowed me to visit their institution and on field to meet

microfinance users and Mr.Vishnukant with whom I visited the microfinance users

residing in Mankhurd & Chembur. And also to Mrs.Anjali Jadhav from Hindustan

Microfinance Pvt Ltd who gave me relevant information regarding the working pattern

of their institution.

2

Awareness of Microfinance in Urban India 2013

CHAPTER 1

1. Introduction

A microfinance institution (MFI) is an organization that provides microfinance services.

MFIs range from small non-profit organizations to large commercial banks.

Microcredit is already a flourishing business working mostly through Self-Help Groups

(SHGs). These, supported by banks, notably by the government’s National Bank for

Agriculture and Rural Development (NABARD), typically brought together about 15

women, who pooled their savings for a few months, allocated them to members who

needed small amounts temporarily, and were then also eligible for a bank loan (short- to

medium-term). Government agencies such as NABARD envisioned the role of

Microfinance Institutions (MFIs) in this model as that of someone who will link SHGs

primarily with banks. The number of borrowers through SHGs was expanding rapidly

especially after 2005 central government budget support to this sector.

Microfinance programs have generally targeted poor women. By providing access to

financial services only through women-making women responsible for loans, ensuring

repayment through women, maintaining savings accounts for women, providing

insurance coverage through women-microfinance programs send a strong message to

households as well as to communities.

The economic empowerment of women has a positive impact as it helps in enhancing

the wellbeing of women. The well-being of women includes many things including their

health, autonomy to take decisions, earning income, and above all, her mental, physical

and emotional stability. Because of the prevalence of patriarchy in India, women are

usually dominated by the male members in the family, be it by their husbands, fathers,

brothers, and later on, their sons. Women thus have to mould themselves according to

the wishes of their male family members.

According to CGAP-(Consultative group to assist the poor works)

Microfinance helps very poor households meet basic needs and protect against

risks.

The use of financial services by low-income households is associated with

improvements in household economic welfare and enterprise stability or growth.

By supporting women's economic participation, microfinance helps to empower

women, thus promoting gender-equity and improving household well-being.

3

Awareness of Microfinance in Urban India 2013

For almost all significant impacts, the magnitude of impact is positively related

to the length of time that clients have been in the program.

1.1 A brief history of Microfinance

Microfinance is most common in the developing world; it started in Bangladesh in

the year 1970. Microfinance credits are usually either interest free or carry interest

that does not compound. Microfinance is a financial system that gives very small

loans to working poor in developing countries to allow them to improve their

business without having to pay unmanageable interest rates. People who receive the

loan use the money to establish or expand businesses that create income for their

families to feed, house, educate and provide health care for their children. They can

also put aside money for a better future. Microfinance is the provision of financial

services to low income clients; solidarity lending groups and self-employed who

traditionally lack access to banking and related services.

1.2 The Current State of the Indian Microfinance Industry

It is interesting to note that there is extreme concentration in the Indian microfinance

industry – approximately one-third of all outstanding microloans and borrowers are

from the state of Andhra Pradesh. It is also interesting to note that despite the recent

growth of the industry, around 90% of the Indian population remains without access

to financial services.

Microfinance in India is funded by private and public capital. Private capital comes

in the form of private equity investments and funds from the capital markets. Loans

from private equity firms and the recent initial public offering of SKS microfinance

are examples of private capital. Public capital is known in India as priority sector

lending. The Indian government mandates all banks in India to lend to the priority

sector. The priority sector includes agriculture, small enterprise, retail trade,

education, and housing finance. The intent behind this policy was to make sure that

under-served markets are not ignored by commercial banks. Microfinance falls into

this definition of the priority sector, and this capital has been the primary driver of

the recent growth in microfinance. From 2003 to 2009, the number of microloans

extended to the poor in India grew from 1.0 million to 26.7 million.

4

Awareness of Microfinance in Urban India 2013

MFI’s differ from one another in terms of:

Lending model

Loan repayment structure

Mode of interest rate calculation

Product offerings

Legal structure

1.3 Key players of Microfinance system

National Bank for Agricultural and Rural Development (NABARD)

Reserve Bank of India(RBI)

Self-help Groups(SHG’s)

Micro Finance Institutions(MFI’s)

Non-Government organisations(NGO’s)

Credit Rating Information Services of India Ltd(CRISIL)

1.4 Objectives

The broad objectives of the study can be stated as

follows:

To find the awareness on microfinance among

low income group people.

To analyse the accessibility of microfinance to

the poor people in urban India.

To study the credit rating of microfinance by

CRISIL.

1.5 Significance of study

Microfinance is most common in the developing world; it started in Bangladesh in

the year 1970. Microfinance credits are usually either interest free or carry interest

that does not compound. Microfinance is a financial system that gives very small

loans to working poor in developing countries to allow them to improve their

business without having to pay unmanageable interest rates. People who receive the

loan use the money to establish or expand businesses that create income for their

families to feed, house, educate and provide health care for their children. They can

5

Awareness of Microfinance in Urban India 2013

also put aside money for a better future. Microfinance is the provision of financial

services to low income clients, especially women who traditionally lack access to

banking and related services. This study helps MFI the outreach of their financial

services in the urban India (Mumbai).

1.6 Limitations of the study

As mentioned above, this study is carried out in one particular area (Mumbai) of

urban India to know the awareness level of Microfinance Institutions among people

having very less income.

Usually Microfinance users are located in the area where Microfinance institutions

have their place of operation. And they are still aloof from the suburban part (Navi

Mumbai) due to which it is difficult to reach the users of microfinance.

1.7 Chapter scheme

The first chapter is about the introduction of microfinance, its brief history, and

current status of microfinance. The objective of the study and its significance and

limitations are also mentioned in the first chapter. However second chapter talks

about theoretical background and the literature review of the past papers. It also

deals with role of CRISIL in microfinance industry.

Third chapter of this study deals with the research methodology used to carry out

this project in which the source of data and collection method is described.

Fourth chapter is divided into two parts. First part shows the analyses of primary

data and its interpretation which is based on awareness of microfinance while second

part deals with the study of credit rating of microfinance based on secondary data.

Fifth chapter is all about the findings made from the analyses of data. Conclusion

and recommendations are made in the sixth chapter of this study.

CHAPTER-2

6

Awareness of Microfinance in Urban India 2013

2. Theoretical Background

There is growing interest in microfinance as one of the avenues to enable low

income population to access financial services. India with a population of around

300 million poor people has emerged as a large potential opportunity for the

microfinance sector. With only 48% of the population accessing financial

services, expanding the microfinance sector is also important from the

perspective of financial inclusion (World Bank, 2008). Since 2004, the Reserve

Bank of India (RBI) has emphasized financial inclusion as an important goal.

The recent global financial crisis also underlines the desirability of financial

sector growth by broadening access to financial products rather than by

facilitating excessive leverage to a subset of the population or by increasing the

complexity of financial products.

While there have been various initiatives to promote microfinance in India since

the 1970s, the sector witnessed rapid growth only in the 1990s. The RBI has

since the mid-1990s helped in attracting funding for the sector by including

microfinance in the “priority sector”, to which banks are mandated to allocate a

percentage of their lending. However, no specific regulation was imposed on the

sector as a whole primarily because it was felt that regulation may hamper the

sector’s key strengths of informality and flexibility.

With the growth of the sector both in terms of size, scope and number of

participants, there is however now a need for developing a more formal

regulatory structure.

First, regulation is needed to enable a number of large microfinance institutions

(MFIs) to offer savings services, so as to address a major shortcoming of the

sector. The largest MFIs in the country, which cumulatively account for 80% of

the sector in terms of portfolio outstanding are non-banking finance companies

(NBFCs), who are unable to accept savings deposits

Second, microfinance sector institutions are no longer solely socially motivated.

Due to the growing perception that it is possible to earn high returns through

microfinance lending, commercially driven entities are also being attracted to the

sector. This further underlines the need for supervision and consumer protection.

7

Awareness of Microfinance in Urban India 2013

Third, some MFIs have started offering products such as insurance, remittances

and pensions by tying up with mainstream providers. While this helps in

broadening the scope of microfinance services, it also calls for coordinated

regulation of the sector particularly in view of the limited financial literacy of its

participants. Such increasing overlap between various financial institutions is

expected to continue.

Finally, while the diversity of legal forms in the sector has arisen due to its

unplanned, entrepreneurial growth, a uniform regulatory framework would

enable a level playing field and prevent regulatory arbitrage.

While regulation is essential, avoiding over regulation that hampers innovation

and unduly increases transaction costs is also equally important.

Microfinance Institutions-

A range of public sector as well as private sector offers the micro finance

services in India. Based on asset sizes, MFI can be divided into three categories:

5-6 institution which have attracted commercial capital and scaled up

dramatically within last five years. The MFIs which include SKS, SHSRE

and grameen style program but after 2000, converted into for profit regulated

entities mostly Non-Banking Finance Companies (NBFC’s).

Around 10-15 institutions with high growth rate, including both news and

recently form for profit MFI’s. Some of MFI’s are Grameen koota, Bandhan

and ESAF.

The bulk of India’s 1000 MFI’s are NGO’s struggling to achieve significant

growth. Most continues to offer multiple development activities in addition

to microfinance and have difficultly accessing growth trends.

(microfinancedata.pdf)

LITERATURE REVIEW

8

Awareness of Microfinance in Urban India 2013

Savita Shankar (2011) defines financial inclusion as ongoing access to a range of

financial services in an affordable and convenient manner. As low income groups

are often among those lacking such access, microfinance programmes providing

financial services to them have emerged as a public policy instrument to promote

financial inclusion. This thesis evaluates the contribution of microfinance

programs in promotion of financial inclusion in India. To sustain financial

inclusion, group microfinance members should graduate to individual financial

services. The thesis therefore also explores the environment in which such

graduation could take place.

The thesis analysed appropriate regulatory framework for the microfinance

sector. The study has implications for policymakers at the national and state

level, microfinance providers, members and funding agencies. The thesis

findings also suggest that there is considerable scope for policy relevant

empirical research on microfinance in India.

Anand (2011) has criticised industry for their oppressive style of functioning

which allegedly has caused hardships to credit seekers in some districts of

Andhra Pradesh, where in some cases some of the clients even committed

suicide. These resulted in speculations from various quarters, suggesting curbing

of Microfinance Institutions’ (MFIs’) operational freedom which, MFIs

contested, would force them out of the business. The main reason for such

incidences was said to be the high rates of interest and the marketing (especially

collection) tactics adopted by MFIs. In turn, MFIs argued that they themselves

get funds at a very high rate of interest, and when one adds the operating

expenses of MFIs the final credit rate would come up to what MFIs are generally

charging. And if they do not ensure repayment of their loans by their clients, the

cost of funds will go even higher. With this backdrop, this study has been carried

out to find the actual reasons behind the hardships of MFIs’ clients, reasons for

the high cost of capital, causes of inefficiency in operations which have increased

the cost of credit further, and problems with the current marketing strategy and

other related areas. This study encompasses all aspects of microfinance as

present in Andhra Pradesh (India) and suggests possible solutions.

9

Awareness of Microfinance in Urban India 2013

Basu and Srivastava (2005) suggests that despite substantial efforts and

a vast network of rural banks, the rural poor still have very little access to

formal finance. In this scenario, new microfinance approaches designed to

deliver finance to the poor have emerged. The paper assesses the potential

and possibilities of microfinance in enriching rural access. The authors

evaluate the growth of SHG-Bank linkage model of microfinance. The

number of SHGs linked to banks has increased from 500 in 1990s to 8lac in

2004. But with an outreach of only 12 million, the SHG- Bank linkage has a

long way to go. It is further mentioned that less than 5% of poor rural

households have access to microfinance. In this too, the regional imbalance

is also a concern. SHG-Bank linkage capitalises on country’s vast resources

of rural bank branches. To encourage banks to lend to SHGs, NABARD

provides refinance options. Moreover, SHG lending is calculated as “priority

sector lending” which acts as an added incentive for banks.

Sriram (2010) traces the different stages of progress of microfinance

institutions over the last two decades. Three distinct waves of growth of

microfinance institutions have been stated. The first wave was when the

development sector discovered the methodology of reaching loans to the poor

through a callable model, which was mastered by the Grameen bank. The

second wave was when these microfinance institutions reached scale and sought

methods to morph into commercial organisations. The third wave was when

mainstream institutions like L&T finance and Equities took to microfinance as

a business. Other than SHG model, the other model followed by microfinance

institutions is the Grameen model wherein customers are identified using a

poverty index and are organised into small groups. With MFIs operating

more than acceptable levels of commercial activities in a non-profit format, it

was difficult for them to explain their form to the commercial world. The

option was to either set up a local area bank or form a non- banking

financial company (NBFC). Bank license being difficult to obtain, the latter

was the available alternative. The author highlights the loopholes in legislation

and regulation in this context.

According to Karmakar (2009), microfinance covers the delivery of banking

and other financial services at affordable costs to the vast sections of

10

Awareness of Microfinance in Urban India 2013

disadvantaged and low- income groups. Easy access to public goods and

services is essential for an open, inclusive and efficient society.

Microfinance provides savings and credit facilities under three models – a)

the banks providing “no frills” deposit and loan facilities, b) SHG-bank

linkage model, c) microfinance institutions model and d) the post offices. The

role of NABARD in policy formulation, financial innovations,

technological interventions and institutional strengthening has been

highlighted. The author also criticizes the lack of any regulatory framework

foe microfinance institutions other than NBFCs.

Nair (2001) opines that the SHG model of microfinance depends on

social intermediation through self-help or solidarity groups so that financing is

cost effective and peer pressure and monitoring act as collateral. Group

lending avoids high cost intermediation between banks and clients and

reduces individual borrowing transaction cost. The author classifies the

microfinance sector into two broad categories – Financial and non-financial.

Financial sector includes commercial banks, rural banks etc. Non-financial

sector comprises of not for profit microfinance institutions (NGOs,

trusts), mutual benefit microfinance institutions (state credit cooperatives)

and for profit microfinance institutions (non-banking financial

companies). The logical foundation of promoting non-financial microfinance

institutions rests on the apparent failure of the financial sector institutions

and the disappointing performance of government programmes. There

has been a 40% reduction in transaction cost due to SHG intermediation and

consequent reduction in time spent by the bank staff. Similarly, borrower’s

transaction cost has been found to have declined by 85% with the elimination

of complex documentation and procedures and reduction in time and costs

incurred in repeated visits to bank

11

Awareness of Microfinance in Urban India 2013

.Krishnamurthy and Varalaxmi (2011) suggested that the awareness programs should

be conducted in each educational institution to explain the benefits of microfinance. It

is crucial that more microfinance institutions should be set up to provide loans all over

the country. Microfinance should be made easy for the microfinance seekers to go for

it and flourish the business environment. The study concluded that microfinance

institutions are not only contributing significantly to the development of finance

sector in their respective countries, but also they play an important role to eradicate

poverty by providing much needed capital to low income people which are able to

generate tremendous return on the investment.

K.S.Ranjani (2012) points out at absence of regulation as one of the important factor

contributed to the recent turmoil in the microfinance industry. This paper looks into

the need for regulation of Microfinance Institutions (MFI) aspects of regulation and

international experiences in regulation that could guide the industry in India. This

paper also attempts to build a conceptual framework for regulation of MFI in India.

Like every other financial intermediary, microfinance institutions will benefit the

customer as well as the industry at large when they subject themselves to both self and

statutory regulation.

Khavul (2002) states that Microfinance is an emerging phenomenon that opens access

to capital for individuals previously shut out from financial services. In its direct

engagement with the poor, microfinance represents a new way for financial capital to

potentially stimulate economic growth in developing countries. However,

microfinance is poorly understood, and it remains unclear whether it delivers on its

promises. The goal of this paper is to introduce the topic of microfinance to a wider

audience of management researchers and to identify opportunities for future research

in this new and growing area.

12

Awareness of Microfinance in Urban India 2013

CHAPTER-3

RESEARCH METHODOLOGY

The methodology adopted to accomplish the objectives of the study has been

elaborated in this chapter.

3.1Data source-

This study is basically based on primary data collected from microfinance users

of Svasti Microfinance Pvt ltd and other non-users of microfinance. However,

secondary data also supports this study. The secondary data has been collected

from newspaper articles and other websites providing information on

microfinance.

3.2Year of the study - The 10 months are divided according to the following

manner in order to be an effective project.

July to September(2012): Focusing on the study as a whole and

identifying the problems and framing the title, collecting information as well

as details raring industry and also framing objectives.

October to December (2012): Literature review. Framing of

questionnaire for data collection, information collected through questionnaire

for data collection and interpretation.

January to April(2013): From the interpretation the researcher list out

certain findings, suggestion, conclusion & rough copy submission for

correction, after the correction fair copy was prepared and submitted.

3.3 Sample-

The sample of 140 data has been collected from the group of women who

themselves or their spouse earning less than INR 10000 per month. The group of

women include vegetable vendor, garland maker, peon, house worker, hospital

receptionist and housewife located in the different parts of Mumbai. And the

remaining data is collected from nearby resident place from the same group of

people.

13

Awareness of Microfinance in Urban India 2013

3.4Type of data-

The type of data is primary for the research purpose based on non-probability

convenience. Along with primary data, secondary data is also supporting this

study. Primarily the part-2 of the analysis is based on secondary data.

14

Awareness of Microfinance in Urban India 2013

CHAPTER 4

DATA COLLECTION AND ANALYSIS

Fig.1.1

Interpretation- Out of the 140 respondents 61% (85) access to the banks for

finance while 39% (55) access to the microfinance institution for the finance.

Fig.1.2

Interpretation- out of 140 respondents, 61% are not aware of microfinance while

39% are aware of it and therefore using the microfinance services according to their

benefits from various MFI’s such as Hindustan Microfinance Pvt ltd, Svasti

Microfinance Pvt ltd and other similar institution located in various parts of

Mumbai.

15

Awareness of Microfinance in Urban India 2013

Fig.1.3

Interpretation- From the above graph, it can be interpreted that microfinance users

are only having one type of account with MFI’s i.e. loan account. Other types of

accounts are not maintained by the MFI.

Fig.1.4

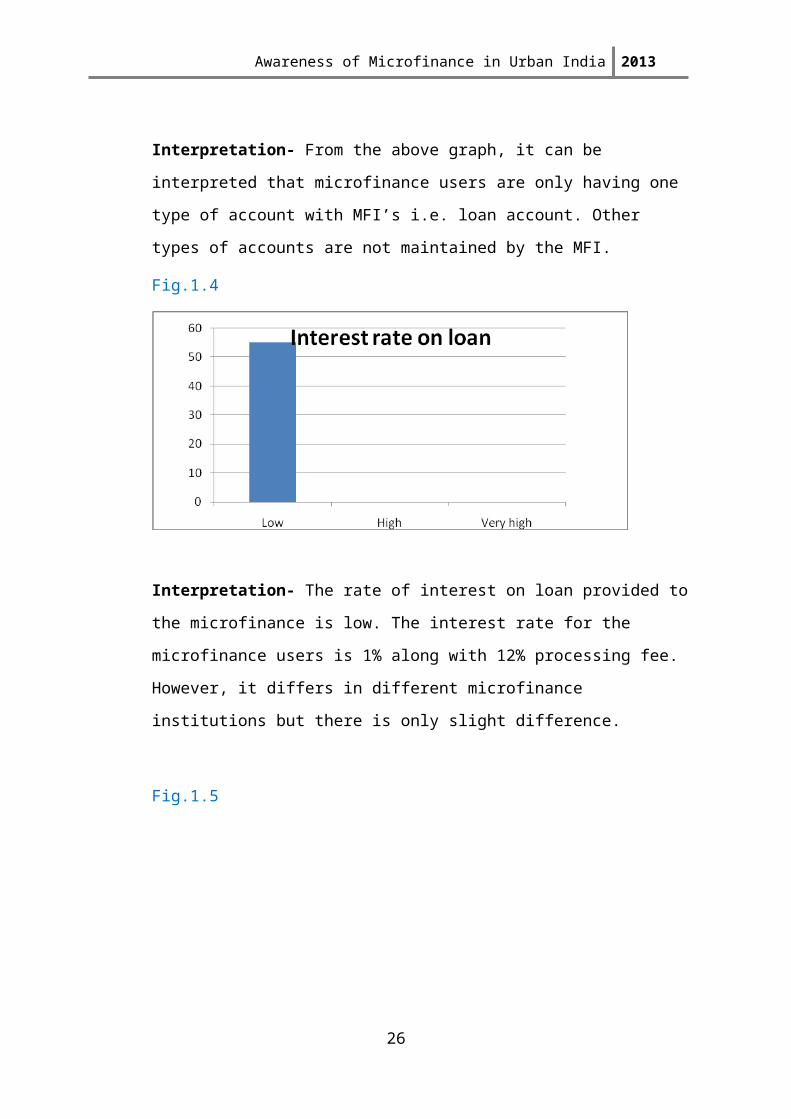

Interpretation- The rate of interest on loan provided to the microfinance is low.

The interest rate for the microfinance users is 1% along with 12% processing fee.

However, it differs in different microfinance institutions but there is only slight

difference.

16

Awareness of Microfinance in Urban India 2013

Fig.1.5

Interpretation- The purpose of taking loan from MFI’s is different. From the

research it is found that majority of people (44%) take loan for job creation i.e.

using funds for establishing small business like small groceries, 25% people use the

funds for health purpose like medical expenses of the family members, 18% people

use the funds for housing as it is again a critical factor to bear expenses of housing

in the urban area especially in Mumbai and 13% people need funds for the

education of their children.

Fig.1.6

Interpretation- The research shows that 73% of the microfinance users are highly

satisfied while 27% are only satisfied and there are 0% users who are unsatisfied

with the services provided by various MFI’s in urban India.

17

Awareness of Microfinance in Urban India 2013

Fig.1.7

Interpretation- There are several reasons for change in economic condition of

microfinance users. 44% of users believes that their economic condition has been

improved as the loan taken from MFI’s facilitate income earning while 18%

believes that funds from microfinance facilitate stress and disaster management and

9% have both the reason for change in their economic condition. Whereas 29% have

different reason such as financial reliability for women has reduced.

Fig.1.8

18

Awareness of Microfinance in Urban India 2013

Interpretation- The most critical factor for availing microfinance from the MFI is

the availability as still there is lack of marketing of microfinance products among

the urban poor people and there is no other critical factor except instalment for the

very few who have very less income and more expenses.

Fig.1.9

Interpretation- The most influencing factor for opting microfinance is the

collateral free loan. Therefore, 40 out of 55 respondents believe that they are

motivated to take loan from MFI’s because of no collaterals while 9 people believes

that they are influenced to take microfinance as it helps to establish small business

and the remaining 7 are using microfinance because it gives them long term

financial independence.

Fig.1.10

19

Awareness of Microfinance in Urban India 2013

Interpretation- For all microfinance users i.e. 100% people have convenience in

repayment of instalment of the loan taken as the instalment amount is taken on

weekly basis within the range of Rs100-250

Fig.1.11

Interpretation- Out of the total microfinance users, 9% suggest to reduce the

interest rate further and 9% suggest to broad the range of financial services while

82% give different suggestions such as reducing the instalment period from weekly

to monthly and providing education to establish small business.

Fig.1.12

Interpretation- This figure illustrates that the services provided by the MFI’s apart

from the loan are general insurance and financial education where 30 people are

20

Awareness of Microfinance in Urban India 2013

accessing to general insurance and 10 out of 55 are taking only financial education

while the remaining 15 are not accessing any other service from MFI except loan.

Small entrepreneur training and life insurance services are not provided by these

MFI’s.

Fig.1.13

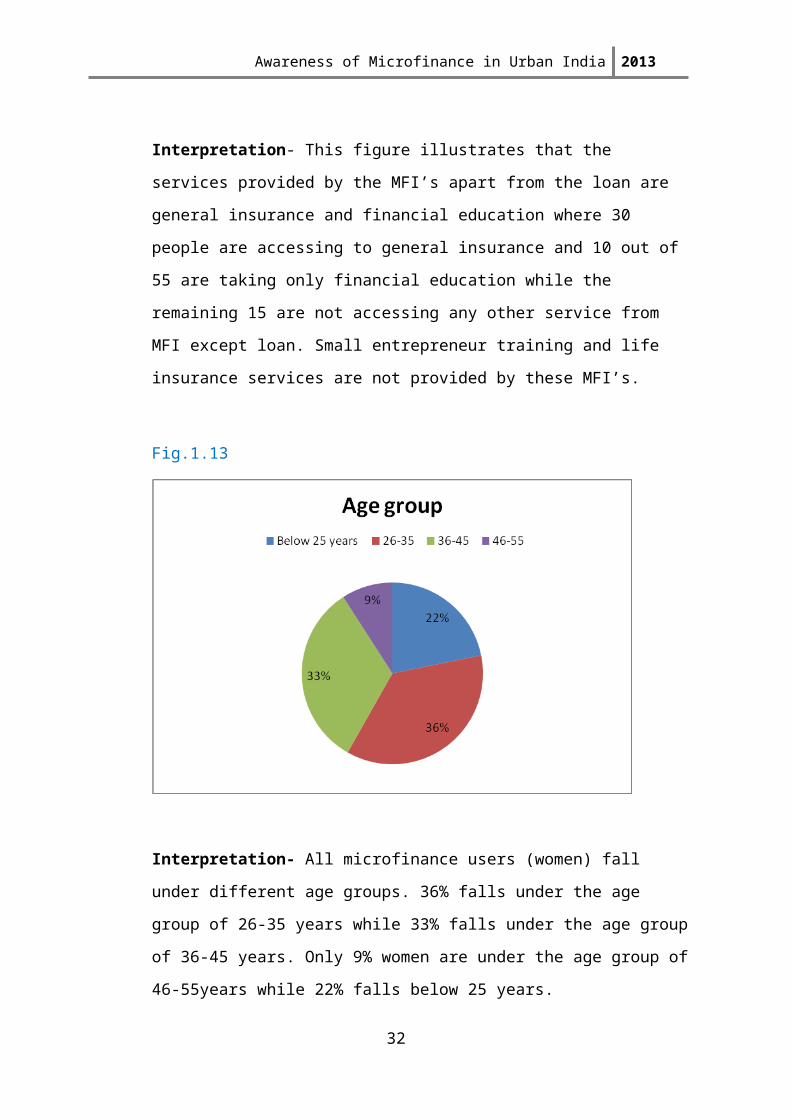

Interpretation- All microfinance users (women) fall under different age groups.

36% falls under the age group of 26-35 years while 33% falls under the age group

of 36-45 years. Only 9% women are under the age group of 46-55years while 22%

falls below 25 years.

21

Awareness of Microfinance in Urban India 2013

Fig.1.14

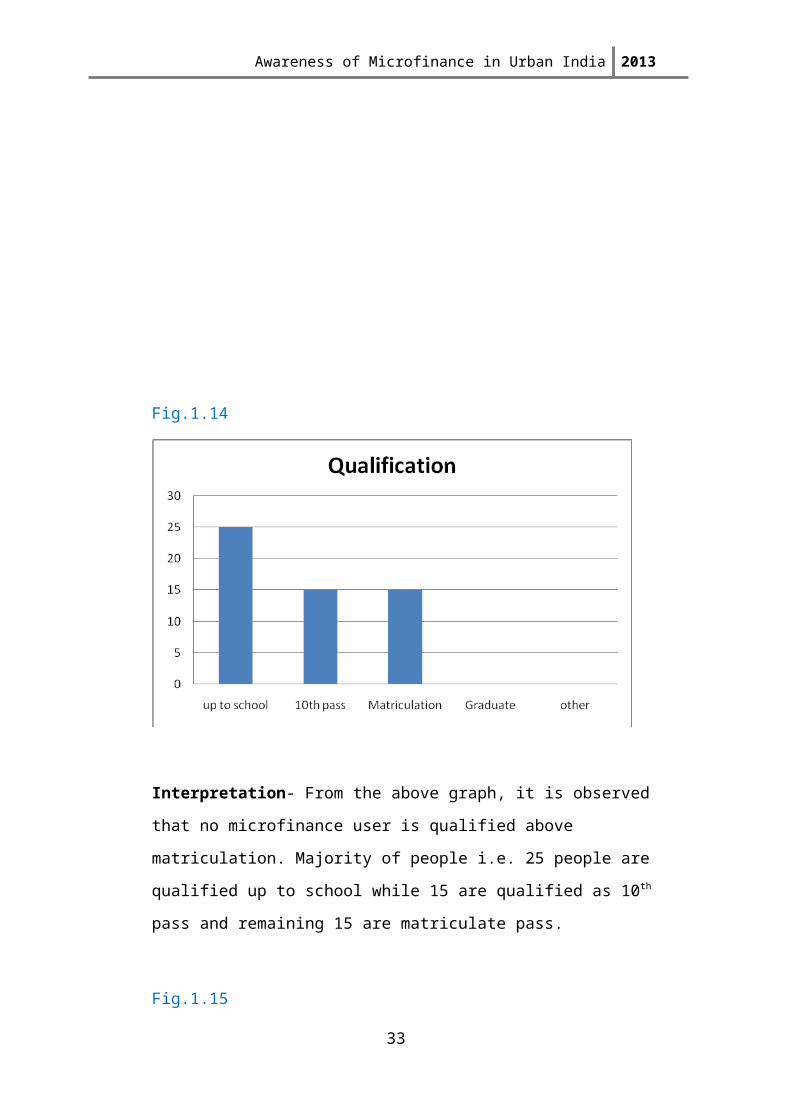

Interpretation- From the above graph, it is observed that no microfinance user is

qualified above matriculation. Majority of people i.e. 25 people are qualified up to

school while 15 are qualified as 10th pass and remaining 15 are matriculate pass.

Fig.1.15

Interpretation- 54% of microfinance users are having some small kinds of business

of selling of vegetable, fruits, snacks, artificial accessories etc., 9% are having small

22

Awareness of Microfinance in Urban India 2013

retail shops, 13% are doing service as school peon, household worker, hospital

receptionist etc. while 24% are either housewife or helping in the work of their

spouse.

Fig.16

Interpretation- From the above graph it can be observed no microfinance user has

income above Rs10000 per month. In fact majority people i.e. 30 out of 55 are

having income less than Rs 3000 while only 15 people are having income between

Rs3000 to Rs5000 and remaining 10 are having income more than Rs5000 per

month.

Fig.1.17

23

Awareness of Microfinance in Urban India 2013

Interpretation- From the above graph it can be interpreted that people having one

child and people having no child are equal i.e. 5 respondents in each category. The

majority of people are having three children i.e. 28 out of all users and 15 people

are having two children while only 2 are having more than 3 children.

24

Awareness of Microfinance in Urban India 2013

PART-II

Role of CRISIL in credit rating of Microfinance

CRISIL (Credit Rating Information Services of India) is India’s leading ratings

agency. CRISIL provides grading and risk assessments of microfinance institutions,

and rates MFI’s bank facilities and securitisation transactions.

CRISIL offers customized diagnostic services that cater to the requirements of donors

and social investors proposing to invest in, or provide grants to, MFIs, or

microfinance programs of non-government organizations (NGOs).

These studies, apart from carrying out a strengths, weaknesses, opportunities, and

threats (SWOT) analysis, may be customized to indicate actions that the MFIs can

explore to scale up and sustain their microfinance operations, while minimizing risks.

CRISIL also offers customized services, such as a review of the business plan and

periodic monitoring of microfinance programs, with an option of an MFI Grading

under this service.

CRISIL’s microfinance institution (MFI) grading is a current opinion on the ability of

an MFI to conduct its operations in a scalable and sustainable manner. The grading is

assigned on an eight point scale, with ‘mfR1’ being the highest and ‘mfR8’ the lowest.

The MFI grading is a measure of the overall performance of an MFI on a broad range

of parameters under CRISIL’s MACRO framework. It includes a traditional

creditworthiness analysis using the CRAMEL approach, modified to be applicable to

the microfinance sector. The acronym MICROS stands for Management, Institutional

arrangement, Capital adequacy and asset quality, Resources and asset-liability

management, operational effectiveness, and scalability and sustainability.

MFI grading scale: mfR1-highest, mfR8-lowest (www.crisil.com)

25

Awareness of Microfinance in Urban India 2013

According to the study done by Micro-credit ratings International Limited in 2006:-

The purpose of this study is to estimate the investment required to enable the microfinance

sector. SHGs and MFIs had to meet the overall demand for micro-credit by 2010 in a

financially sound and sustainable manner. MFIs are expected to meet about 25% of the

micro-credit demand by 2010, while the other 75% of the demand is expected to be met by

the bank-SHG linkage programme. This paper estimates the equity investment required by

MFIs to grow while maintaining a sound capital adequacy position. It also estimates the

promotional and operational expenses likely to be incurred in enabling the bank-SHG linkage

programme to meet the overall demand from poor families. (www.m-cril.com)

26

Awareness of Microfinance in Urban India 2013

CHAPTER-5

INTERPRETATION AND FINDINGS

From the above analysis the findings are:-

1. The awareness about microfinance services among urban poor people

is still very low. More than half population is still unaware of

microfinance.

2. There is only loan account maintained by MFI’s for their customers.

3. The greatest advantage to the microfinance users are the low interest

rate on loan, no collaterals and the small amount of instalments.

4. The users of microfinance have income less than Rs.10000 per month,

generally ranging between Rs.2000 to Rs.6000 having their own small

business.

5. The age group of respondents (women) falls between 26-45 years

having qualification up to school.

6. The other service provided by the MFI’s is general insurance. Financial

education is provided but it is still not up to the mark. And there is no

small entrepreneur training for them to establish their own business.

7. CRISIL plays a significant role in rating the microcredit given by MFI.

27

Awareness of Microfinance in Urban India 2013

CHAPTER-6

CONCLUSION AND RECOMMENDATION

Conclusion-

This study shows the awareness of microfinance among urban poor people. The

earlier studies were carried out on the regulatory framework of microfinance,

contribution of microfinance to the economy of a country, style of functioning of

MFI, the role of NBFC’s and other key players in the microfinance. This study is

carried out in the Mumbai region. Collection of sample data and its analysis shows

that there is still lack of marketing of microfinance service among urban poor

population but the services of existing MFI’s are more or less satisfactory to the users

of microfinance.

Recommendation-

From this study, it is suggested that there should be proper marketing of

microfinance among poor people in the urban areas.

The range of services provided by the microfinance should be

increased up to significant level including financial education, small

entrepreneur training programs.

The maximum loan amount of Rs25000 should be extend as the

growing prices of basic commodities, housing and education will not suffice

the needs of microfinance users.

The weekly payment of instalment should be extend to at least 15 days

as sometimes it is not possible for the poor people to pay the instalment within

a week time if some calamity occurs or source of income stops.

APPENDIX

28

Awareness of Microfinance in Urban India 2013

QUESTIONNAIRE

I am a student of MMS-II from Jankidevi Bajaj Institute of Management Studies,

SNDT University. I am doing a research project on “Awareness of microfinance in

urban India” which is done for the academic purpose. Please tick on the appropriate

option for the below questions.

1. What is the other source of finance do you access?

Banks

Microfinance Institution

Other(specify)

2. Are you aware of microfinance?

Yes

No

If yes then answer the following-

1. Nature of account do you have with MFI?

Savings a/c

Current a/c

Deposit a/c

Loan a/c

2. How is the interest rate on the given loan?

Low

High

Very high

3. For what purpose you generally use the availed funds from MFI?

Housing

Job creation

Health

Education of children

Other(specify)

4. To what extent you are satisfied with the services by microfinance

institution?

Highly satisfied

29

Awareness of Microfinance in Urban India 2013

Satisfied

Unsatisfied

5. What do you think about the changes in your economic condition after

becoming member of MFI?

Credit received from MFI facilitated income earning

Advice/training from MFI facilitated income earning

Savings in MFI facilitated stress and disaster management

All of the above

Other (specify)

6. What is the critical factor for availing service from the MFI?

Interest rate

Processing

Instalment factor

Availability

Other(specify)

7. What are the factors influencing for opting microfinance?

No collaterals

Help to establish small businesses.

Long term financial independence

Other(specify)

8. Are you able to repay instalments of the loans comfortably?

Yes

No

9. What are your suggestions for the MFI?

Broadening the range of financial services.

Reduce the interest rates

Flexible repayment option

Other(specify)

10. What are the other services you are getting from MFI?

Micro insurance

Life insurance

Financial education

30

Awareness of Microfinance in Urban India 2013

Small entrepreneur training

All of the above

None of the above

PERSONAL DETAILS

1. Name:

Native Place:

Gender:

Male

Female

2. Age:

Below 25 years

26-35 years

36-45 years

46-55 years

3. Qualification:

Up to school

10th pass

Matriculate

Graduate

Other(specify)

4. Occupation:

Service

Business(specify)

Retailer

Other(specify)

5. Monthly income: (per month)

Below 3000

3000-5000

5000-10000

10000 above

6. Number of children :

One

31

Awareness of Microfinance in Urban India 2013

Two

Three

More than three.

None

7. Number of children going to school:

All

Specify

BIBLIOGRAPHY

1. Anand. “High cost of finance in microcredit business in Andhra

Pradesh(India): Problems and possible solutions” The Icfaian Journal of

Management Research, Vol. VII, No. 4, 2008.

32

Awareness of Microfinance in Urban India 2013

2. Savita Shankar, “An analysis of the role of microfinance programs in

promoting financial inclusion in India” submitted to LEW KYUAN YEW

SCHOOL OF PUBLIC POLICY, National university of Singapore,2011.

3. Susanna Khavul, “Creating opportunities for the poor” Academy of

Management Perspectives, pg-58, August 2010.

4. DR.M.Krishnamurthy; S.Varalakshmi, “Microfinance perception- A study

with special reference to Salalah, Sultanate of Oman” ZENITH

International Journal of Multidisciplinary Research Vol.1 Issue 3, July

2011.

5. K.S.Ranjani, “Regulating Microfinance in India- A conceptual framework”

Synergy (January, 2012), Vol. X No. I.

6. Sriram, M.S., 2010, “Commercialisation of Microfinance in India:A

Discussion of the Emperor’s Apparel”, Economic and Political Weekly,

June 12, 2010 vol xlv no 24.

7. Nair, Tara, 2001, “Institutionalising Microfinance in India: An Overview

of Strategic Issues”, Economic and Political Weekly, Vol. 36, No. 4,

Money, Banking & Finance (Jan 2001), pg. 399-404.

8. Karmakar, K.G., 2009, “Emerging Trends in Microfinance”, Economic

and Political Weekly, March 28, 2009 vol xliv no 13.

9. Basu Priya and Srivastava Pradeep, 2005, “Exploring Possibilities:

Microfinance and Rural Credit Access for the Poor in India”, Economic

and Political Weekly, Vol. 40, No. 17 (Apr.2005), pg. 1747+1749-1756.

Web References-

1. CGAP, 2006. “Comparative Database on Microfinance Regulation”

www.microfinancegateway.org

2. http://crisil.com

3. http://fusionmicrofinance.com

4. http://www.inm.org.bd

33

Awareness of Microfinance in Urban India 2013

5. http://www.nabard.org

6. http://www.iitk.ac.in

7. http://www.microfinancegateway.org

8. http://www.centre-for-microfinance.org

9. http://www.mcril.com

10. http://www.smeworld.org

34