Embed Size (px)

Citation preview

Auto Component Industry in India: Growing Capabilities & Strengths

• India: A Vibrant Economy

• Automotive Industry in India

• Auto Component Industry in India

• Policy Environment

• Capabilities & Challenges

• The Way Forward

• About ACMA

Agenda

2

India: A Vibrant Economy

3

4

1. Largest Democracy – 1.2 billion people, Growing Middle Class

2. 4th largest GDP (PPP) and 10th largest GDP (Nominal, USD 1.8 trillion)

3. One of the fastest growing economies• India’s average GDP growth rate: 8.4% over past 5 years

• Expected to outpace China in the next decade

4. 3rd Largest Investor base in the World

5. Robust Legal and Banking Infrastructure

6. Demographics Advantage – Youth driven economy

7. Suburbanization & Rural to Urban Migration – 140 million by 2020; 700 million by 2050

8. 2nd largest pool of Certified Professionals and highest number of Qualified Engineers in the world

9. Investment in Infrastructure

India: A Vibrant Economy

Automotive Industry in India

5

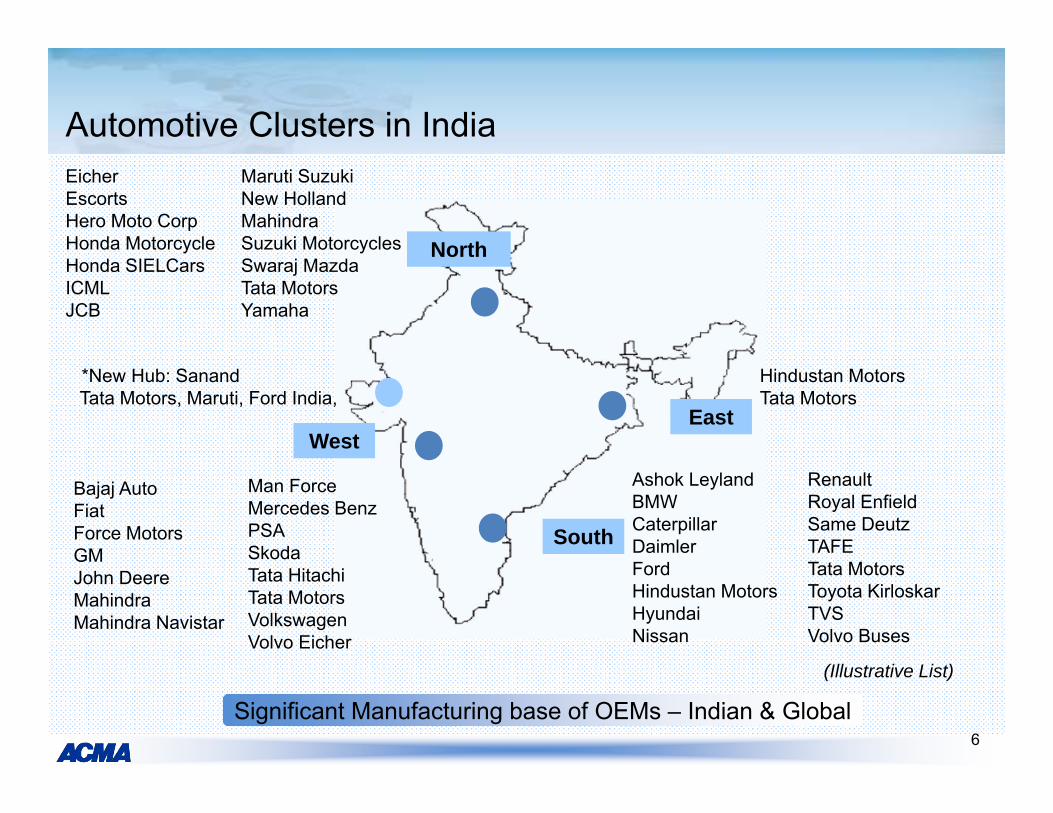

Automotive Clusters in India

West

Hindustan MotorsTata Motors

North

Significant Manufacturing base of OEMs – Indian & Global

Ashok Leyland BMWCaterpillarDaimlerFordHindustan MotorsHyundaiNissan

RenaultRoyal EnfieldSame DeutzTAFETata MotorsToyota KirloskarTVS Volvo Buses

East

South

EicherEscortsHero Moto CorpHonda MotorcycleHonda SIELCars ICMLJCB

Maruti SuzukiNew HollandMahindraSuzuki MotorcyclesSwaraj MazdaTata MotorsYamaha

Bajaj AutoFiatForce MotorsGMJohn DeereMahindraMahindra Navistar

Man ForceMercedes BenzPSASkodaTata HitachiTata MotorsVolkswagenVolvo Eicher

(Illustrative List)

6

*New Hub: SanandTata Motors, Maruti, Ford India,

7

Rapidly growing presence of Global OEMs

Passenger Vehicle market share by OEM parent country2007 2011

MahindraHindustan MotorsPremier

Maruti SuzukiTata MotorsMahindraHindustan MotorsPremier

Mercedes BenzFordToyotaHondaGMFiat HyundaiMaruti SuzukiTata MotorsMahindraHindustan Motors

BMWVWSkodaRenault NissanMercedes BenzFordToyotaHondaGMFiatHyundaiMaruti SuzukiTata MotorsMahindraForce Motors Hindustan Motors

Loca

lFo

reig

n

1980 1990 2000 2011

(Illustrative List)

1,838 2,357

2,987 3,146 3234

5100

10,000

-

2,500

5,000

7,500

10,000

2008-09 2009-10 2010-11 2011-12 2012-13 2015-16 2020-21

(’000 units)

CAGR 2008-12: 14%

CAGR 2012-21: 13%* *

Passenger Vehicles Production

*

(* Estimates)Figures for financial year – April to March

8

Figures for financial year – April to March

( ’000 units)Commercial Vehicles

(* Estimates)

9

Tractors( ’000 units)

CAGR 2011-21: 5%*

Two & Three Wheelers

(In ’000 units)

Commercial Vehicles include:• Small Commercial Vehicles (SCV) < 1 ton• Light Commercial Vehicles (LCV) > 1 ton but < 7.5 tons

• Medium Commercial Vehicles (MCV) > 7.5 tons but <16 tons• Heavy Commercial Vehicles (HCV) > 16 tons

Construction Vehicles( ’000 units)

CAGR 2011-21: 14%*

CAGR 2008-12: 22%CAGR 2012-21: 11%*

CAGR 2008-12: 16%CAGR 2012-21: 7%*

Other Vehicles Production

9

Auto Component Industry in India

10

Auto Component Industry Profile - Turnover

Engine Parts31%

Drive Transmission & Steering Parts

19%Body & Chassis12%

Suspension & Braking Parts

12%

Equipments10%

Electrical Parts9%

Others7%

Comprehensive Product Range

USD

billi

on

(* Estimates)

*

11

CAGR 2008-12: 12%

CAGR 2013-21: 14%*

Figures for financial year – April to March

*

Auto Component Industry Profile - ExportsU

SD b

illion

Export Destinations

OEM/Tier 1 account for 80%; Aftermarket for 20%

3.8 4 3.4 5.28.5 9.3

12

30

0

10

20

30

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2015-16 2020-21

(* Estimates)

*

*

12

CAGR 2008-12: 22%

CAGR 2013-21: 16%*

Figures for financial year – April to March

Australia, 1% Africa, 9%

Europe, 35%

North America,

26%

Asia, 25%

South America, 4%

Increased Component Outsourcing

Tier 1 Component Manufacturers• Bosch• Continental• Cummins• DANA• Delphi• Denso• Eaton• Getrag• Kolbenschmidt• Magna• Meritor• TRW• Valeo

OEMs• BMW• Caterpillar• Ford• FIAT• GM• MAN• Mercedes-Benz• Nissan• Peugeot• Renault• Toyota• Volkswagen

Over 30 IPOs of Global OEMs & Tier 1 Procuring from India

Indian components already driving on international roads

(Illustrative List)

13

Auto Component Industry Profile - Imports

Sources of Imports

(* Estimates)

6.2 6.8 6.5 8.513.2 13.1

19

35

0

10

20

30

40

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2015-16 2020-21

USD

billi

on

*

*

14

CAGR 2008-12: 11%

CAGR 2013-21: 13%*

Figures for financial year – April to MarchNorth

America, 8%

South America,

1%

Asia, 59%

Europe, 32%

33.954

858.5

12

30

13.2

19

35

0

50

100

150

2011-12* 2015-16 (E) 2020-21 (E)

Production for domestic consumption Exports Imports

15Total Industry Potential: USD 150 billion by 2020

Vision 2020: Indian Auto Component Industry

85

150

USD

Bill

ion

56

E-Estimated

Source: ACMA - EY Vision 2020

Policy Environment & Trade

16

Favorable Policy Regime

Auto Policy 2002 and Auto Mission Plan 2006-16 – framework for Automotive Manufacturing in India

• Manufacturing and Imports Free from Licensing and Approvals

• WTO compliant policies (no import restrictions and reduced tariff levels)

• Robust Legal system and stable Foreign Exchange regime

• Joined UN-ECE WP 29 for Global Standard in Technology

• Increased budgets for R&D activities

• 100% FDI permitted without prior Govt. approval

Robust Indian Automotive

Industry

17

Major International Auto Component Companies with India Manufacturing footprint

(Illustrative List)

18

• Aisin Seiki Co.• BorgWarner• Continental• Delphi• Denso Corporation• Eaton• FAG• Faurecia• GKN• Honda Foundry Co. Ltd.• Honeywell• Knorr Bremse• Koyo• Magna

• Magneti Marelli• Mando Corporation• Meritor• Mitsuba Corporation• NHK Spring• Robert Bosch• Showa Corporation• Sumitomo Wiring Systems• Toyoda Gosei• USHIN• Valeo• Visteon• Yazaki• ZF

Capabilities & Challenges of Indian Component Suppliers

19

Indian Suppliers’ Focus – Global Best Practices

Industry fast embracing modernshop-floor practices:

5-S; 7-WKaizenTQMTPM6 SigmaLean Manufacturing

Deming Award - 12

Japan Quality Medal - 2 JIPM - 3Shingo Silver

Medallion - 1TPM Award

- 15

Largest no. of Deming Award winning companies outside Japan

Focus on Quality

20

Increasing focus on Innovation and Research

• AMD

• Boeing

• Bosch

• Caterpillar

• Continental

• Cummins

• Ford

• GM

• GE

• Honda

• Honeywell

• Hyundai

• Intel

• Magna

• Motorola

• Mercedes Benz

• Microsoft

• Renault Nissan

• Suzuki

• Valeo

Design & Research Centers of leading Global companies in India

(Illustrative List)

21

Challenges – Typical of a high Growth Emerging Market

• Raising Capital & Scaling Capacities

• Infrastructure Challenges

− Roads

− Ports

− Power

• Inflation

• Availability of Skilled Manpower

• Managerial Depth across Tiers

• R&D Competence

22

Conclusion

• Vibrant Indian Economy

• Automotive Industry - Double Digit Growth in all segments

• India fast emerging as hub for Global Vehicle Programs

• 2020: USD 113 billion Auto Component Industry

• Growing Engineering and IT capability for Designing & Manufacturing

• Respect for IPR

• Opportunity to Partner in Product & Process Innovation

• Opportunity to Outsource for OEMs/T1s and Aftermarket

India: The Gateway of Growth

23

About ACMA

24

About ACMA

• Established in 1959

• Apex body of Auto Component Industry in India

• 650+ members from the Organized sector

• Represents 85% of the Industry by turnover

• Represented on all Government and Industry bodies –

Strategic to the Auto Sector

• Offices across all Regions in the Country

• An ISO 9001-2008 Institution

ACMA – Excellence in Service Delivery

25

Collection &Dissemination of

Information

QualityEnhancement

TechnologyUp-gradation

Promotes IndianAutomotive Component Industry

Vital Catalyst for Industrial Development

Trade Promotion

ACMA Services

26

ACMAThe Capital Court, 6th Floor, Olof Palme Marg, Munirka, New Delhi – 110 067

Tel: 011-26160315, Fax: 011-26160317E-mail: [email protected], Website: www.acma.in

Thank You

for any assistance contact

27

![[Insert Exercise Name] - CTEP AAR-IP... · [Insert aligned core capabilities from situation manual] Strengths . The following strengths related to this objective were observed in](https://img.dokumen.tips/doc/110x75/5f040ce77e708231d40c1297/insert-exercise-name-ctep-aar-ip-insert-aligned-core-capabilities-from.jpg)