Embed Size (px)

Citation preview

Please refer to the important disclosures and analyst certification on inside back cover of this document, or on our website www.macquarie.com/disclosures.

Australia & NZ

Macquarie Marquee Ideas (MMIs) represent our best alpha-generating ideas. MMIs represent a collection of Macquarie Research's best ideas derived from our coverage universe. The time frame for each idea is typically three months, with the list reviewed every two weeks. Stocks may be removed from the list earlier than the three month typical duration if the particular MMI has played out and expected outperformance of the idea has materialised. Similarly MMIs may remain on the list for longer than three months if significant alpha is still to be generated. Selection criteria reflect high levels of analyst conviction and near term catalysts The MMI list is selected by a group of Macquarie Research Senior Analysts, Strategists, the Quant Team and by Heads of Research. MMI's are typically in line with the analysts' fundamental view. However emphasis is on level of conviction and the existence of catalysts over the next quarter. In order for institutional investors to realistically invest in MMIs, minimum stock turnover requirements have also been considered. Overleaf are Macquarie’s valuations on all the stocks we cover.

13 July 2012 Macquarie Securities (Australia) Limited

Macquarie Marquee Ideas Still signs of a pulse… What a month for our Macquarie Marquee Ideas. We engaged Dr Craig Collie

to check the pulse of our MMI list yesterday and he assures us that there are

signs of life. Our MMI list isn't a portfolio, but a list of stocks we believe will

both outperform and benefit from a short to medium term catalyst. Clearly the

market is currently separated into two camps - 1) Telcos, REITs, banks,

consumer staples and 2) The rest. Stock selection has been rendered

challenging by the current macro environment. Most stocks/sectors in any

way associated with Resources / Materials have been punished.

We add a counter-consensus gaming sector pairs trade – Long TAH / Short

TTS (TAH, $2.91, Outperform, TP: $3.20, TSR: 16.7%, TTS, $2.64,

Underperform, TP: $2.40, TSR: -3.9%). We add a Sell idea in Primary

Healthcare (PRY, $3.16, Underperform, TP: $2.60, TSR: -12.9%).

Origin - APLNG has taken FID on train two. As such our catalyst has passed.

While we continue to be positive on ORG, we remove it from our MMI list after

an excess return of -5.2% since its inception on 20 February 2012. We have

also removed Wotif after recent outperformance and no immediate catalyst; it

has produced an excess return of 3.7% since its addition to the MMI list on 14

May 2012.

We have removed Whitehaven Coal, which has produced an excess return of

-14.3% since its inception on 20 June 2012. Thermal coal dynamics have

deteriorated significantly such that incremental demand from China is

currently extremely weak. We believe in the short term this has changed

potential M&A dynamics for the stock. Financing for any bid has become

incrementally more difficult. Similarly any bidder may also be looking for a

bottom that is not evident at this point.

Macquarie Marquee Ideas

Rec Code/Stock Start Date

Last price

FY12 PER TP TSR % Analyst

LEADERS

O/P AMC – Amcor 05/07/12 7.22 13.8 7.70 12.7 John Purtell

O/P DJS – David Jones 23/03/12 2.35 11.1 3.12 41.7 Rob Blythe

O/P IPL – Incitec Pivot 01/06/12 2.93 11.0 3.45 21.9 John Purtell

O/P NCM – Newcrest 03/02/12 22.49 16.0 32.00 44.1 Mitch Ryan

U/P PRY – Primary Healthcare 13/07/12 3.16 13.7 2.60 -12.9 Craig Collie

O/P QRN – QR National 05/06/12 3.30 21.8 4.30 34.1 Ian Myles

O/P RIO – Rio Tinto 01/04/11 55.65 9.3 88.00 60.7 Adrian Wood

EMERGING LEADERS

O/P AQG – Alacer Gold 22/05/12 4.98 8.8 10.00 100.8 Mitch Ryan

O/P MRM – Mermaid Marine 22/05/12 2.64 11.5 3.47 35.4 Andrew Wackett

O/P RCR – RCR Tomlinson 23/03/12 1.75 8.4 2.62 54.9 Andrew Wackett

O/P SVW – Seven Group 09/09/11 7.05 8.4 11.78 72.2 Andrew Wackett

PAIR TRADE

O/P GPT – GPT Group (Long) 29/06/12 3.31 14.0 3.50 11.5 Rob Freeman

U/P SGP – Stockland (Short) 29/06/12 3.16 10.6 3.22 9.6 Paul Checchin

O/P NAB – NAB (Long) 05/07/12 23.59 9.4 27.66 25.3 Michael Wiblin

U/P CBA – CBA (Short) 05/07/12 53.60 12.7 48.52 -3.2 Michael Wiblin

O/P TAH – TAB Holdings (Long) 13/07/12 2.91 6.1 3.20 16.7 Lachlan Fitt

U/P TTS – Tatts Group (Short) 13/07/12 2.64 11.4 2.40 -3.9 Lachlan Fitt

Source: Macquarie Research, FactSet pricing, July 2012

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 2

Macquarie Marquee Ideas

PRY AU – Primary Healthcare

We have added Primary Healthcare to our MMI list

Date became MMI: 12/07/2012 PRY AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Underperform

Last Price: AUD 3.16

Price Target: AUD 2.60

TSR %: - 12.9

Catalyst:

Full year results in August

We believe if a more conventional accounting policy were applied to PRY, its profit would be 50%

lower this year, and as such view the stock as materially over-valued. However, perhaps more

concerning for shareholders is that the current treatment of upfront GP payments seemingly

results in the forfeiting of a $17m tax shield, suggesting ~20% of shareholder cash is

unnecessarily being paid to the tax office each year.

By choosing not to expense upfront GP payments, PRY is essentially electing to divert cash away

from shareholders to the tax office. Although this creates a potential value-play if management do

decide to change the policy, we see it as unlikely due to: (i) the detrimental effect on key valuation

metrics (ie PER, EV/EBIT, dividend payout ratio); and (ii) the hesitancy normally exhibited by

management to restate historical accounts.

PAIR TRADE – TAH AU – TABCorp Holdings (LONG) / TTS AU – Tatts Group (SHORT)

We have added a pair trade to our MMI list.

Date became MMI: 12/07/12 TAH AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform (Long)

Last Price: AUD 2.91

Price Target: AUD 3.20

TSR %: 16.7

Catalyst:

FY12 Result. Commencement of

legal action vs Vic Govt. Final

report from DBCDE re the review

of the Interactive Gambling act.

Agreement between TVN and

Tabcorp re media rights.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 3

Date became MMI: 12/07/12 TTS AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Underperform (Short)

Last Price: AUD 2.64

Price Target: AUD 2.40

TSR %: - 3.9

Catalyst:

FY12 result

Fig 1 Tatts trades at a 44% premium to TAH based on FY14 FCF yield

Fig 2 Tatts dividend yield is 120bps+ lower than Tabcorp

Source: Company data, Macquarie Research, February 2012 Source: Company data, Macquarie Research, February 2012

Long TAH:

Despite the weak economic environment, Tabcorp's 3Q trading update was positive. Strong

momentum in the core Wagering business offset softness in Pokies and Keno. Channel feedback

suggests the strong 3Q momentum has continued into 4Q, with Tabcorp benefitting from a refocus

on the Victorian retail network and the removal of Tote Tasmania from the premium rebate market.

In addition, the Euro 2012 soccer tournament in June will have helped boost 4Q growth rates in

the wagering business relative to 3Q. We expect these trends will flow through to a robust FY12

result, and anticipate consensus upgrades heading into Tabcorp's result on 9 August (MRE are

currently ~1% ahead of consensus NPAT forecasts for FY12).

As well as a robust FY12 result, we see a number of other positive catalysts for Tabcorp in coming

months. We expect these catalysts will remove investor concerns around a number of risks that

have lingered over previous years. The catalysts include:

Increased comfort on Tabcorp's ability to cover its minimum performance obligation

(MPO) under the new Victorian wagering licence. We note this has been a concern of the

market since Tabcorp was awarded the new Vic wagering licence last July; however, based

on our estimates, we believe Tabcorp has 8-10% headroom under their MPOs in both FY13

and FY14. We expect strong trends from Tabcorp's Victorian business to be evident at the

FY12 result, which should allay these concerns and remove the current overhang we believe

exists from this issue.

8.7%

9.5%

11.3%

8.3%

6.6%7.0%

0%

2%

4%

6%

8%

10%

12%

FY13e FY14e FY15e

FCF Yield (%)

Tabcorp Tatts

6.9%6.5%

7.2%

5.3% 5.3%5.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

FY13e FY14e FY15e

Div Yield (%)

Tabcorp Tatts

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 4

Final report from the DBCDE in coming weeks on the Interactive Gambling Act and

proposed removal of restrictions on in-play betting online. The draft report recommended

that in-play betting could be liberalised if approved by the relevant state/territory regulatory

authority and the relevant sports controlling body (where one exists), but also recommended a

blanket ban of "micro-betting" (ie. next ball in cricket, next point in tennis). We have previously

estimated that full liberalisation of online live betting could generate an additional $180m in

annual wagering industry revenues by FY16, of which Tabcorp's share could be $45m. This

would increase NPAT by ~7% and valuation by 20cps. Excluding "micro-betting", we estimate

the benefits reduce by ~25%. We continue to incorporate 10cps in our target price for in-play

betting, which is consistent with the outcomes of the draft report.

Completion of agreement between Tabcorp and TVN regarding media rights, where we

believe the market has become overly negative on the potential increase in rights fees

Tabcorp will be required to make. Our current expectation is that Tabcorp will need to pay

an additional $10m per annum to extend the rebroadcast agreement for NSW and Victorian

racing with TVN. This would see annual rights fees of $37.5m paid by Tabcorp to the racing

industry-owned broadcaster. Following the recent proposal by TVN to aggregate NSW

regional and provincial rights into the existing vehicle, we would anticipate a final agreement

will be struck with Tabcorp in coming months.

Compensation claim can commence against the Victorian Government from mid-

August. While we acknowledge any challenge is likely to be lengthy and could potentially

involve several court appeal processes, we see further newsflow on the matter as an

incremental positive for the stock price. Tabcorp believes it is entitled to up to $687m (~93cps)

in compensation for the change in licence structure for Victorian gaming operators. On a post-

tax basis, we see compensation in the range of $481-549m, which equates to 63-72cps on a

discounted basis. We currently allocate a 30% risk-weighted amount (23cps) in our $3.20/sh

valuation.

These catalysts would follow a string of newsflow that has increased certainty for investors.

Previous announcements include the renewal of its Victorian wagering licence, and the

positive resolution for the racing industry of the Race Field Fee dispute via a High Court ruling.

Short TTS:

Our short TTS call is a valuation argument and not based on an expectation that earnings will

disappoint at the FY12 result in late August. Tatts‟ portfolio of businesses continues to trade well,

with the jackpot run in lotteries over the past few months no doubt boosting growth rates during

2H12; however, this will make growth rates tougher to achieve through FY13. In addition, Tatts‟

wagering business is likely to have continued to receive a margin boost as the shift from tote

betting to fixed odds continues. While this is positive for short-term earnings, we remain

concerned that this may reverse over the medium/long term (the same concern is applicable to

Tabcorp).

Over the next 2-3 months, several of the positive catalysts that exist for Tabcorp are less relevant

for Tatts. Firstly, Tatts exposure to online sports betting is relatively low, and therefore we see

limited upside to the TattsBet business from a liberalisation of online in-play betting. Secondly,

while Tatts are also likely to commence legal proceedings against the Victorian government for

compensation from the loss of their gaming licence, we note the upside leverage from a positive

outcome is less significant for Tatts than it is for Tabcorp (Tatts 41cps or ~15% of current price,

Tabcorp 93cps or ~30% of current price).

In saying this, Tatts is likely to receive a valuation boost should it acquire SA Lotteries when the

sale process is completed later this year or early next year. We estimate Tatts will pay no more

than $300m for the licence, which would be value-accretive; however, we see the majority of this

upside already being priced in at current levels.

On a longer-term view, we see some risks to the high margin revenue that Tatts generates from its

NSW monitoring licence that expires in 2016. We don't currently factor in any requirement for Tatts

to make an upfront payment to extend this licence and note there may be competitive tension that

could reduce the margins Tatts are able to renew the contract at, or it could lose the monitoring

contract altogether.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 5

ORG AU – Origin Energy

We have removed Origin Energy from our MMI list.

Origin Energy has produced an excess return of -5.2% since its addition to the MMI list on 20

February 2012.

While the second train has been sanctioned, ORG is yet to resolve funding concerns. We had

expected that a second train FID would also come with a sell-down in APLNG equity. While ORG

has committed to reducing its exposure from 37.5% to 30%, we expect that this process will take

several months, particularly given a dataroom is yet to be open. Nonetheless, given the favourable

market for Australian LNG assets highlighted by recent transactions, we remain confident that

APLNG can secure a partner in the fullness of time which will drive a re-rating.

WTF AU – Wotif.com

We have removed Wotif.com from our MMI list.

Wotif.com has produced an excess return of 3.7% since its addition to the MMI list on 14 May

2012.

We retain our Outperform recommendation, which is not based on a return to previous rates of

growth or rerating but rather on the stock offering a circa 6.5% yield, delivering modest earnings

growth in the current environment with potential for acceleration if market conditions improve

WHC AU – Whitehaven Coal

We have removed Whitehaven Coal from our MMI list.

Whitehaven has produced an excess return of -14.3% since its addition to the MMI list on 20 June

2012.

We remain positive on Whitehaven from a fundamental point of view in the medium and long term;

however note the current weakness in the thermal coal market is likely to drag on the stock in the

near term, and as such we are removing it from the MMI.

IPL AU – Incitec Pivot

Date became MMI: 01/06/12 IPL AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 2.93

Price Target: AUD 3.45

TSR %: 21.9

Catalyst:

Expected DAP price strength over

coming weeks, Moranbah start-

up in July

IPL is hosting an Investor day on 7 August. Key focus will be on IPL‟s Australian business,

including presentations on Moranbah, IPF and Dyno Asia Pacific. We expect these to provide

greater confidence that 1) Moranbah start-up is on track following first AN this month and 2) IPL

has made changes within its IPF business that should prevent a recurrence of the extent of

inventory losses that saw disappointing IPF 1H EBIT of $2m.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 6

Soft commodity prices (corn, wheat) are +30% over the last three months. Given the correlation

with fertiliser prices, this should be positive but is yet to play out. Global urea prices have fallen

over the last month to US$435/t (FOB, Middle East), which is negative directionally for IPL.

However, US urea prices have started to rally, with NOLA back up at US$460/t. We currently

assume US$500/t 2H urea – if we assumed US$450/t 2H urea (similar to current local prices), this

would have a -3% impact on our FY12eps.

We estimate fair value DAP based on historic corn and wheat price relationships is currently

US$720t (+27% on spot US$565/t) and fair value urea US$568/t (+23% vs US spot US$460/t).

This is positive for the affordability equation. Of course, other demand/supply drivers are also

important. At present, the Indian monsoon is not as favourable, which may impact Q3 Indian DAP

imports whilst additional Middle East urea supply is expected in 2H. Higher wheat prices are

positive for sentiment for Australian broadacre farmers, which should in turn encourage urea

demand for top-dress application. Recent rainfall in NSW and Victoria has come at a good time to

boost the moisture profile and should stimulate top-dress urea demand in 2H.

US coal not as bad as feared so far. The other issue is US coal demand weakness and impact on

Dyno Americas. We understand that Dyno has had a reasonable May / June and demand into

coal, as yet, has not fallen by the -10% plus predicted in May (this is consistent with US coal

production, which is down 6% YTD vs down 8% YTD back in May). Dyno is also less exposed to

Appalachian (30% of US coal volume) than other regions (PRB, Illinois) and AN pricing has held

up well, in part due to EDC plant closure (1-3 months before start-up). There are also some

tentative signs of Q&C improvement, as housing has bottomed and infrastructure spend is starting

to filter through.

AQG AU – Alacer Gold

Date became MMI: 22/05/12 AQG AU vs Small Ordinaries, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 4.98

Price Target: AUD 10.00

TSR %: 100.8

Catalyst:

Updated Çöpler resource due in

September.

In light of the current market conditions where investors are pulling away from commodities in

general and risk appetite has dwindled, there has been indiscriminate selling of the gold sector.

While this has created a lot of value in the market, theoretical upside needs to be tempered

against the risks inherent in the stock. As such we think those stocks with a higher degree of risk,

the explorers and unfunded developers, will be on the sideline for at least six months and that the

strongest medium term returns will be provided by low-cost producers, with tier one assets. Alacer

fits our target profile and has been oversold on poor communication to the market and the recent

management change.

With cash costs of ~US$600/oz, we forecast Alacer to generate US$200m of cash flow this year

(after capex and exploration of US$210m). For the cash flow to be eroded to zero, the gold price

would have to fall to US$950/oz. As such, we believe that Alacer is a stand-out gold stock for its

ability to generate strong cash flow, which when coupled with the ever-growing resource at Çöpler

provides a fully funded growth.

The feasibility study for the Çöpler sulphide project was initiated in January 2012 and is expected

to be complete by the end of 2012. We have recently revised up our capex estimate for the project

to US$550m (from US$425m). We value the Çöpler sulphide project at US$852m. Our production

forecast remains unchanged at 155koz attributable gold, with production to commence in late

2014.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 7

MRM AU – Mermaid Marine

Date became MMI: 22/05/12 MRM AU vs Small Ordinaries, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 2.64

Price Target: AUD 3.47

TSR %: 35.4

Catalyst:

Contract wins on Gorgon,

Wheatstone and Inpex.

Mermaid has been unfairly sold off in the mining services sector from $3.44 in February to current

levels of $2.64. This is despite the company having no exposure to coal or base metals. We

continue to believe that all committed Western Australian based LNG projects will be built. We

see WA/NT LNG plants going from two in number in 2011 to seven by 2015/2016, with obvious

ramifications for the size of MRM's core market. MRM remains in a strong competitive position to

benefit from this growth.

In our view, Mermaid is a strong play on the high levels of oil and gas activity in Western Australia

over the medium term. We believe Mermaid‟s strong market position is likely to lead to further

earnings upgrades.

DJS AU – David Jones

Date became MMI: 23/03/2012 DJS AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 2.35

Price Target: AUD 3.12

TSR %: 41.7

Catalyst:

FY12 result and update on online

Please refer to Essentials article 23 March 2012, “Zebra loses its $tripe$”.

We have upgraded our recommendation on DJS to Outperform. Why not? We have had the

massive downgrade - while guidance for FY12 NPAT is for a 35-40% fall, DJS expect growth in

FY13 & 14. Further the financial services earnings have been exposed, and DJS are spending a

fortune to acquire/develop an online business model which will allow the social customer to

engage with the brand at all levels. DJS is fast tracking the development of its brand as a social

object, not to lead the market but merely to catch-up. While it might be late, it has engaged

credible business partners (IBM) to build out a capability, and, if the brand is relevant and the

online piece well executed, DJS may just manage to accelerate sales growth.

The share price has not been this low since 2006, and while earnings expectations have tumbled,

so has the price. We are looking for a relief rally and a “what-if” proposition regarding sales. This

isn‟t a macro call or even an interest rate cut call: DJS is undervalued and its transformation

initiatives could improve perception and ability to compete with the various pure-play online and

established Omni Channel Retailers.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 8

NCM AU – Newcrest

Date became MMI: 03/02/2012 NCM AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 22.49

Price Target: AUD 32.00

TSR %: 44.1

Catalyst:

Wafi-Golpu PFS due September

2012.

Precious metals prices are curiously weak at the moment, particularly given that real interest rates

continue to drift lower and lower. Part of the sluggish performance seems related to confusion in

FX markets, with the Euro being strangely stable despite expectations it would shift lower. This

uncertainty has weighed on gold stocks over the first quarter of the year, but has been further

compounded by the current environment affecting gold producers where the majority of stocks

have missed production guidance and experienced increasing operating costs and capital

expenditure.

Newcrest has not been immune to these pressures, clearly struggling to deliver on operational

guidance throughout the course of 2012. That said, we believe the market has temporarily lost

focus on the quality of Newcrest's asset base relative to its global peers and the longer-term value

inherent in the projects. By way of example we note CVO's 0.8moz per annum production for a

+30 year mine life and Lihir's 1.2moz per annum production for a +25 year mine life both at sub

$500/oz cash costs.

Although it is important to acknowledge that the operational underperformance has created

downside sentiment towards the stock which will not be abated easily, we believe over the coming

six months the production outlook is positive. With near-term growth projects (Lihir MOPU and

Cadia East) providing upward momentum to the production profile, we believe the risk is to the

upside from current levels.

Newcrest has historically traded at an average P/NPV (Macquarie price deck) multiple of 1.6x

since 2008. It is currently trading at ~1.0x a level not seen since 2002. As such, we believe that

the low risk of further operational disappointment is significantly offset by the long-term upside

represented by tier one, long-life assets trading at the cheapest level in 10 years.

RIO AU – Rio Tinto

Date became MMI: 01/04/11 RIO AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 55.65

Price Target: AUD 88.00

TSR %: 60.7

Catalyst:

Easing in Chinese inflation data

and/or material loosening of policy.

The equity sell-off of the past few months has meant that, other than briefly in the height of the

global turmoil of 2008, long-term valuation metrics (DCF and mid-cycle earnings) in the last ten

years have never been more supportive for Rio Tinto than right now.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 9

Rio Tinto is trading almost 15% below what we term our "zero option" valuation. What that means

is that if we utilise our long run price estimates from today in perpetuity and a 95c A$/US$, we

arrive at a ~A$65ps DCF valuation for Rio Tinto. Note that this includes no change to our

aggressive operating and capital cost inflation assumptions over coming years.

Even taking a particularly conservative (prudent) view on the timing and cost of Rio Tinto's flagship

Pilbara expansions, Rio Tinto appears comfortably inexpensive on almost all valuation metrics,

given our view on a potential multi-year shelf in iron ore prices. Outperform.

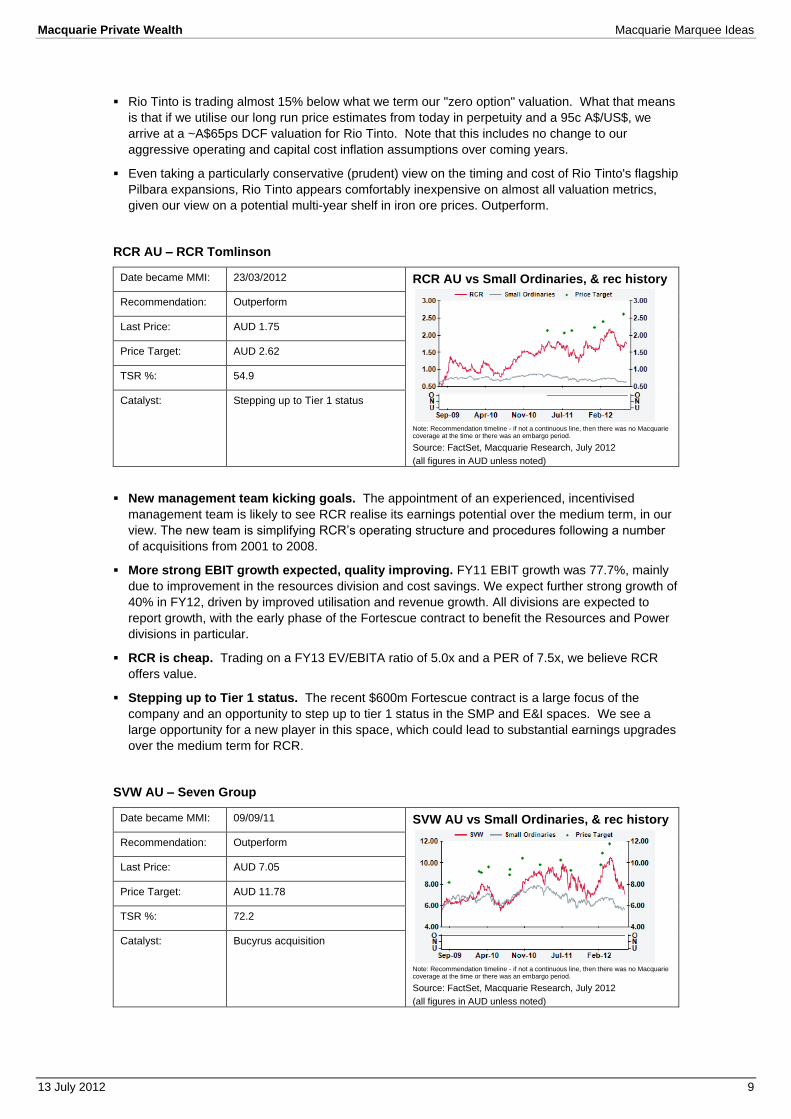

RCR AU – RCR Tomlinson

Date became MMI: 23/03/2012 RCR AU vs Small Ordinaries, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 1.75

Price Target: AUD 2.62

TSR %: 54.9

Catalyst:

Stepping up to Tier 1 status

New management team kicking goals. The appointment of an experienced, incentivised

management team is likely to see RCR realise its earnings potential over the medium term, in our

view. The new team is simplifying RCR‟s operating structure and procedures following a number

of acquisitions from 2001 to 2008.

More strong EBIT growth expected, quality improving. FY11 EBIT growth was 77.7%, mainly

due to improvement in the resources division and cost savings. We expect further strong growth of

40% in FY12, driven by improved utilisation and revenue growth. All divisions are expected to

report growth, with the early phase of the Fortescue contract to benefit the Resources and Power

divisions in particular.

RCR is cheap. Trading on a FY13 EV/EBITA ratio of 5.0x and a PER of 7.5x, we believe RCR

offers value.

Stepping up to Tier 1 status. The recent $600m Fortescue contract is a large focus of the

company and an opportunity to step up to tier 1 status in the SMP and E&I spaces. We see a

large opportunity for a new player in this space, which could lead to substantial earnings upgrades

over the medium term for RCR.

SVW AU – Seven Group

Date became MMI: 09/09/11 SVW AU vs Small Ordinaries, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 7.05

Price Target: AUD 11.78

TSR %: 72.2

Catalyst:

Bucyrus acquisition

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 10

While our SVW call hasn‟t worked of late, we are maintaining our faith in the name. SVW is not

materially impacted by recent thermal coal weakness. WesTrac is performing strongly, with key

customer Fortescue spending $1.6bn on equipment. Revenue growth for both WesTrac Australia

and China was over 20% in H1. EBIT of $181.2m was well ahead of our $148.5m expectation and

up 67% on pcp. While gearing is high, it should reduce significantly post up to $1bn of planned

asset sales.

Outperform. We believe WesTrac is a quality business with substantial growth opportunities that

is being undervalued by the market.

QRN AU – QR National

Date became MMI: 05/06/12 QRN AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 3.30

Price Target: AUD 4.30

TSR %: 34.1

Catalyst:

QRN‟s share price performance

has been flat since the late March

profit warning, yet more than 50%

of its business is a regulated

asset.

QRN is semi defensive. 50% of the business is regulated, but importantly the income from the

asset is revenue-protected and thus offers a higher level of certainty versus peers. Moreover it

offers ~12%pa RAB growth over the next four years, nearly 50% above its closest rival. The

inherent value in the RAB is under appreciated. A RAB multiple of 1.20-1.25 is already being

reflected in comparable assets in this space. On this basis, 2/3rds of QRN‟s EV is supported by

the below rail business, irrespective of flooding or coal outlook.

QRN leverage remains too low. The regulated business can support debt of $2.9-3.5bn and

should still be able to maintain its BBB+ credit rating. This is before any consideration of

leveraging the above rail (AIO is ~2.7x ND: EBITDA in FY13). QRN FY13 debt is forecast at

$1.5bn; thus QRN we believe has at least $1.4-2.0bn of spare debt capacity, which would only

optimise the regulated assets. This is necessary to minimise the impact from any unfavourable

bond movements. Fear over QRN ability is unfounded, as growth in the RAB will support

additional leverage. A step change in debt adds 6-7% to eps, and 5% to the valuation.

PAIR TRADE – GPT AU – GPT Group (LONG) / SGP AU – Stockland (SHORT)

Date became MMI: 29/06/12 GPT AU vs ASX 200 Prop, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform (Long)

Last Price: AUD 3.31

Price Target: AUD 3.50

TSR %: 11.5

Catalyst:

We believe GPT may provide a

positive refinement to guidance at

their 1H12 result in August.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 11

Date became MMI: 29/06/12 SGP AU vs ASX 200 Prop, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Underperform (Short)

Last Price: AUD 3.16

Price Target: AUD 3.22

TSR %: 9.6

Catalyst:

Below-market FY13 guidance at

the result in August and continued

dilutive non-core asset sales.

Long GPT:

Current FY12 guidance appears conservative. We are of the view that GPT is able to achieve

FY12 EPS growth of 5.6%. This comprises operating income growth of 1.0%, supplemented by a

4.5% reduction in the share count due to the current on-market share buyback. This estimate

compares favourably to current operating EPS growth guidance of „at least CPI + 1%‟. We

therefore believe a positive mid-year earnings refinement could be delivered by the group. This

will be an attractive outcome for such a low risk proposition.

Key delta remains retail landscape but immediate impact low. GPT experienced a difficult

1Q12 on the retail leasing front, reporting an overall leasing spread of -6.0% (FY11: +2.0%). This

comprised flat on renewal deals (~50% of activity) and -10% on new deals (~50% of activity). As

highlighted in prior research, we continue to anticipate re-leasing spreads to remain negative and

incorporate this in our earnings estimates. Despite this, we note that the nearer-term impact on

earnings is more modest, as only 13.6% of specialties expire this year. Assuming a negative 10%

spread on these deals would still equate to +2.5% specialty rental growth overall.

Valuation metrics remain attractive. With the stock currently offering a TSR of ~11% on our

estimates, including a 6% dividend yield with earnings risk to the upside, we note GPT remains an

attractive investment proposition, particularly in light of its defensive, low risk nature.

Short SGP:

Risk to FY13 guidance with downside to market forecasts. In contrast to GPT, we believe

market earnings forecasts are too high and reflect an operating profit margin assumption that is

too optimistic. While we suspect many analysts have assumed the midpoint of SGP's operating

profit margin guidance (22.5%), we expect actual near-term margins will be ~20.0% at best due to

the drag from the roll-off of ~$580m of impaired inventory. We are ~3% below consensus in FY13

and ~5% below in FY14.

Retirement - the other negative delta. SGP own a 14.3% stake in FKP, who may look to

demerge its retirement assets from the main business. Should this demerger come to fruition, it is

likely to trigger a capital raising to both repay $125m in convertible bonds and de-gear the

respective balance sheets. Not only would this place further capital demands on SGP, but the

market is likely to view negatively either decision by SGP to participate or not.

Looking fairly valued and buyback running out of steam. With the stock hovering close to our

$3.22ps price target, SGP appears to be relatively fairly valued. The stock price has been

supported by the group's on-market buyback, which is now ~75% complete. We anticipate

downward pressure on the stock price as the buyback runs out of steam.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 12

AMC AU – Amcor

Date became MMI: 05/07/12 AMC AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period. Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform

Last Price: AUD 7.22

Price Target: AUD 7.70

TSR %: 12.7

Catalyst:

Result 21 Aug. We believe

earnings guidance for growth next

year will be a positive given the

current environment.

Refresh of views post the recent North American analyst tour. The trip highlighted the clear

potential for organic and acquisitive growth in a number of categories, including Diversified

Products (DPs), tobacco in LatAm and Medical Flexibles.

We expect a solid FY12 result of $634m on August 21 and forecast 8% earnings growth in FY13

driven by Alcan and Ball synergies, Aperio and Botany start-up coupled with defensive end-

markets. This is in the context of a tough broader earnings environment. Attributes of relative

earnings certainty, a management team which is delivering and a solid dividend yield are highly

desirable at present.

PAIR TRADE – NAB AU – National Australia Bank (LONG) / CBA AU – Commonwealth Bank (SHORT)

Date became MMI: 05/07/12 NAB AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Outperform (Long)

Last Price: AUD 23.59

Price Target: AUD 27.66

TSR %: 25.3

Catalyst:

3Q update in August

Date became MMI: 05/07/12 CBA AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, July 2012

(all figures in AUD unless noted)

Recommendation: Underperform (Short)

Last Price: AUD 53.60

Price Target: AUD 48.52

TSR %: - 3.2

Catalyst:

Full year results in August

Long NAB:

NAB appear to have come clean on their exposure to the UK region – Whilst there is downside

risk, we have captured this in our valuation, with effective write-downs on UK CRE book of 15%,

being higher than local banks.

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 13

Margins – NAB has been the most aggressive on repricing and will have more levers heading in to

an election year – NAB has been the most aggressive in repricing to date across both mortgages

(31bp since March) and business lending (18bp liquidity margin) offsetting rising funding costs.

Credit growth – Business looking better than housing; APRA data showed business lending

outperforming mortgage credit, benefiting NAB being the dominant banker to businesses.

Provisioning – Cumulative write-off analysis shows NAB is covered at similar levels to the other

majors except WBC.

On P/E basis, NAB is the cheapest across the majors at ~9x

Short CBA:

RoE likely to be under pressure from competitive intensity, regulatory changes, balance sheet

quality drive and incremental investment. We see the retail business coming under pressure as

growth slows, pro-cyclicality increasing capital intensity, wealth flows continuing to weaken and

regulatory changes all putting downward pressure on RoE

Questions over capital generation – 3Q update showed Tier 1 capital generation for the sector

was +1 to 27bp on a Basel 2.5 basis, compared to CBA‟s 15bp decline in 3Q (-12bp, move to

Basel 2.5; -10bp IRRB; and hence 7bp underlying capital generation). Normalising out previous

paper losses could suggest that capital generation for the quarter may have been negative.

Domestic asset quality outlook not as good as 18bp BDD charge suggests – The 3Q12 BDD

charge of $232m (18bp) is exceptionally low given the macro environment in our view. Specific

provision coverage was flat at (47%), whilst housing NPLs increased 5% QoQ. Non-housing NPLs

declined 5% QoQ. While CBA has the cleanest book of the majors, we continue to believe that the

bad debt charge is unsustainably low at this point.

Limited PPoP growth raises questions about revenue trajectory – The 3Q pre-provision profit

(c$2.73b) is similar to 1Q12 ($2.76b) and 2Q12 ($2.75b), indicating limited PPoP momentum. We

have questions over near-term revenue momentum, particularly given CBA appears to be losing

market share based on recent APRA data.

On a valuation basis, CBA is above our 12-month target price and estimated to return a -3.2%

TSR over the year. While CBA is a quality bank and has always traded at a premium to the

sector, it is now trading on a record PE+PBV premium to peers. Decomposition of CBA‟s two-year

sector outperformance shows performance has been driven exclusively by PE expansion. Without

better-than-peer earnings delivery soon, a de-rating is a distinct possibility. (see Dividend

expectations too high, 6/7/12)

Macquarie Marquee Ideas – Performance

Code/Stock Type Start Date

Excess return since

inception %* Excess return over last

week %*

RIO – Rio Tinto Buy 01/04/11 -22.3 -2.2

SVW – Seven Group Buy 09/09/11 -16.6 -4.7

NCM – Newcrest Buy 03/02/12 -32.7 -5.3

DJS – David Jones Buy 22/03/12 5.7 -3.0

RCR – RCR Tomlinson Buy 23/03/12 -13.5 -0.5

MRM – Mermaid Marine Buy 22/05/12 -9.8 -2.9

AQG – Alacer Gold Buy 22/05/12 -21.2 -7.8

IPL – Incitec Pivot Buy 01/06/12 4.4 -0.5

QRN – QR National Buy 05/06/12 -6.4 0.6

Long GPT/Short SGP Pairs 29/06/12 -2.1

Long NAB/Short CBA Pairs 05/07/12 1.0

AMC – Amcor Buy 05/07/12 3.9 -0.8

Source: Macquarie Research, FactSet pricing, July 2012 *Not annualised

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 14

Macquarie Research earnings revisions

The table below highlights all earnings revisions during the past week. Earnings revisions are classified as either upwards or

downwards according to their overall % change in EPS for FY1, FY2 and FY3. Earnings forecasts are adjusted earnings.

Note: All figures are in the currency in which the company reports.

Adjusted Profit EPS

Ccy From To % Chg. From To % Chg. Reason

Upward Revisions

Austal AUD 06/12 5.40 10.65 97.2% 2.87 5.66 97.2% Updated for revised Australian assumptions. See Essentials 5

(ASB.AU)

06/13 44.09 44.17 0.2% 23.44 23.49 0.2% July.

06/14 70.59 70.21 -0.5% 37.54 37.33 -0.5%

Ausdrill AUD 06/12 114.64 114.64 0.0% 37.38 37.38 0.0% Updated FY13 assumptions. See Essentials 3 July.

(ASL.AU)

06/13 121.26 129.55 6.8% 39.21 41.86 6.7%

06/14 148.13 149.79 1.1% 47.42 47.85 0.9%

BT Investment Management AUD 09/12 43.40 44.15 1.7% 15.18 15.44 1.7% Minor revisions following release of June FUM balances and

(BTT.AU)

09/13 48.73 46.28 -5.0% 17.04 16.19 -5.0% performance fees. FY12 Performance fee of $8.1m slightly ahead

09/14 53.74 51.98 -3.3% 18.79 18.18 -3.3% of our $7m forecast. See Essentials 2 July.

Caltex Australia AUD 12/12 342.61 369.64 7.9% 126.89 136.90 7.9% Adjusted forecasts for 1H12 interim guidance. See Essentials 29

(CTX.AU)

12/13 364.39 363.69 -0.2% 134.96 134.70 -0.2% June

12/14 288.63 287.74 -0.3% 106.90 106.57 -0.3%

Crown AUD 06/12 409.27 434.65 6.2% 55.60 59.09 6.3% We have reviewed our earnings forecasts for Crown to reflect

(CWN.AU)

06/13 497.39 479.05 -3.7% 68.29 65.77 -3.7% softness in the consumer environment, as well as incorporating

06/14 601.17 559.72 -6.9% 82.53 76.84 -6.9% See Essentials 27 June.

Domino's Pizza Enterprises AUD 06/12 25.57 26.35 3.0% 35.81 36.83 2.9% Earnings revisions prior to FY12 result announcement. See

(DMP.AU)

06/13 29.90 31.39 5.0% 41.69 43.74 4.9% Essentials 12 July.

06/14 33.57 35.36 5.4% 46.81 49.20 5.1%

Rialto Energy AUD 06/12 -8.77 -8.77 0.0% -1.95 -1.95 0.0% Adjusted production profile. See Essentials 27 June

(RIA.AU)

06/13 -19.57 -18.54 5.3% -1.67 -1.59 5.2%

06/14 81.00 44.44 -45.1% 5.51 2.79 -49.4%

Reckon AUD 12/12 19.19 19.59 2.1% 14.43 14.81 2.6% Upgraded FY12 and FY13 EPS to take into account Linden House

(RKN.AU)

12/13 20.53 21.26 3.5% 15.44 16.32 5.8% acquisition and further price rises in the Business Division.

12/14 20.68 22.19 7.3% 15.54 17.04 9.6% See Essentials 11 July.

UGL AUD 06/12 169.16 169.86 0.4% 102.34 102.76 0.4% We reduce our FY13 and 14 eps by 5% and 7% respectively to

(UGL.AU)

06/13 195.42 185.61 -5.0% 118.22 112.29 -5.0% reflect a flatter outlook for UGL's Resources and Infrastructure

06/14 217.34 202.43 -6.9% 131.49 122.47 -6.9% divisions. See Essentials 11 July.

Whitehaven Coal AUD 06/12 72.29 76.33 5.6% 7.44 7.53 1.3% Rebuilt model following merger with Aston and acquisition of

(WHC.AU)

06/13 70.02 114.57 63.6% 7.21 11.31 56.9% Boardwalk. See Essentials 20 June.

06/14 145.06 228.27 57.4% 14.93 22.53 50.9%

Downward Revisions

Automotive Holdings Group AUD 06/12 63.50 62.47 -1.6% 24.41 24.01 -1.6% Updated for acquisitions. See Essentials 6 July.

(AHE.AU)

06/13 69.51 72.77 4.7% 26.72 27.97 4.7%

06/14 76.65 80.70 5.3% 29.47 31.02 5.3%

Auckland International Airport NZD 06/12 138.60 138.60 0.0% 10.52 10.48 -0.3% Revised following latest price reset on aeronautical charges.

(AIA.NZ)

06/13 148.96 153.51 3.1% 11.30 11.61 2.7% See Essentials 22 June.

06/14 156.34 169.71 8.6% 11.86 12.83 8.2%

Aust Infrastructure Fund AUD 06/12 27.01 22.48 -16.8% 4.35 3.62 -16.8% Updated for internalisation. See Essentials 2 July.

(AIX.AU)

06/13 44.28 15.06 -66.0% 7.13 2.43 -66.0%

06/14 51.96 79.45 52.9% 8.37 12.80 52.9%

Aristocrat Leisure AUD 12/12 105.69 88.04 -16.7% 19.16 15.97 -16.7% Update re 1H12 profit expectations. See Essentials 3 July.

(ALL.AU)

12/13 132.74 115.17 -13.2% 23.54 20.54 -12.7%

12/14 141.07 134.87 -4.4% 24.65 23.74 -3.7%

Ansell USD 06/12 134.81 134.81 0.0% 102.70 102.70 0.0% Revised forecasts for Industrial and New Verticals divisions,

(ANN.AU)

06/13 154.64 145.02 -6.2% 118.35 110.99 -6.2% post US ISM and EU PMI monthly data showing decline. See

06/14 168.14 159.59 -5.1% 128.69 122.14 -5.1% Essentials 4 July.

APN News & Media AUD 12/12 86.40 73.58 -14.8% 13.35 11.39 -14.7% Updated for Brands Exclusive transaction, outdoor JV transaction

(APN.AU)

12/13 88.87 76.36 -14.1% 13.16 11.43 -13.2% and difficult trading conditions. See Essentials 22 June.

12/14 94.30 82.82 -12.2% 13.38 11.98 -10.5%

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 15

Adjusted Profit EPS

Ccy From To % Chg. From To % Chg. Reason

Bradken AUD 06/12 99.34 95.37 -4.0% 59.72 57.33 -4.0% Revision to earnings reflects a softening in the outlook for OEM

(BKN.AU)

06/13 132.09 118.06 -10.6% 76.32 68.94 -9.7% demand. See Essentials 11 July.

06/14 146.04 134.19 -8.1% 81.96 76.54 -6.6%

Boral AUD 06/12 132.86 97.76 -26.4% 17.93 13.14 -26.7% Boral downgrade to FY12 guidance. See Essentials 28 June.

(BLD.AU)

06/13 213.32 148.53 -30.4% 28.64 19.58 -31.6%

06/14 302.14 218.57 -27.7% 40.57 28.81 -29.0%

Bank of Queensland AUD 08/12 45.00 45.00 0.0% 7.70 7.70 0.0% Earnings downgrade - see following note on no sale of loan

(BOQ.AU)

08/13 236.79 221.66 -6.4% 75.25 70.44 -6.4% portfolio. See Essentials 28 June.

08/14 242.40 242.40 0.0% 74.20 74.20 0.0%

Energy Resources of Australia AUD 12/12 -67.53 -138.08

-104.5% -13.04 -26.67 -104.5% Q2 Production report. See Essentials 12 July.

(ERA.AU)

12/13 -118.54 -178.59 -50.7% -22.90 -34.49 -50.7%

12/14 -76.52 -139.92 -82.8% -14.78 -27.03 -82.8%

Iluka Resources AUD 12/12 725.36 342.94 -52.7% 173.22 81.90 -52.7% 1H12 sales reported. Material downgrades. FY12EPPs downgraded

(ILU.AU)

12/13 1184.54 468.80 -60.4% 282.88 111.95 -60.4% 53%, FY13EPS down 60%, FY14EPS down 59%. See Essentials 11 July.

12/14 1246.61 514.98 -58.7% 297.70 122.98 -58.7%

Oakton AUD 06/12 10.66 9.99 -6.3% 11.45 10.75 -6.1% We have reduced FY12/FY13 EPS by -6.1% and -15.4% due to a

(OKN.AU)

06/13 12.63 10.65 -15.7% 13.53 11.44 -15.4% weaker macro and hence lower revenue assumptions. See Essentials

06/14 14.20 12.05 -15.1% 15.18 12.92 -14.9% 9 July.

Perpetual AUD 06/12 65.00 63.84 -1.8% 147.58 144.94 -1.8% Update for strategy update. Changes to earnings following sale of

(PPT.AU)

06/13 61.33 57.28 -6.6% 138.78 129.30 -6.8% mortgage servicing business and cost outs across the business. See

06/14 75.36 80.09 6.3% 170.54 180.81 6.0% Essentials 26 June.

Restaurant Brands NZD 02/13 21.69 19.62 -9.5% 22.17 20.06 -9.5% FY13 EPS lowered due primarily to higher depreciation and G&A

(RBD.NZ)

02/14 25.28 23.56 -6.8% 25.84 24.09 -6.8% costs. See Essentials 12 July.

02/15 28.06 28.29 0.8% 28.69 28.92 0.8%

SAI Global AUD 06/12 52.72 52.72 0.0% 26.07 26.07 0.0% Reduced FY13 EPS by 6% due to softer assumptions for Compliance

(SAI.AU)

06/13 65.24 61.33 -6.0% 32.27 30.33 -6.0% Services. See Essentials 6 July.

06/14 72.07 67.75 -6.0% 35.64 33.51 -6.0%

Skilled Group AUD 06/12 49.48 49.00 -1.0% 21.20 21.00 -1.0% Reduced FY13 EPS by 2% to reflect softer OMS expectations. See

(SKE.AU)

06/13 55.05 54.22 -1.5% 23.57 23.22 -1.5% Essentials 6 July.

06/14 57.83 61.51 6.4% 24.76 26.34 6.4%

Source: Macquarie Research, Factset pricing, July 2012

Macquarie Private Wealth Macquarie Marquee Ideas

13 July 2012 16

Macquarie Research recommendation changes

Note: All figures are in the currency in which the company reports.

Recommendation

Company From To Comment

Upward Revisions

Aristocrat Leisure UNDERPERFORM NEUTRAL Upgrade to Neutral following the recent stock price correction and the 1H12 profit outlook. See

(ALL.AU)

Essentials 3 July.

National Australia Bank NEUTRAL OUTPERFORM Move to Outperform. We adjust our margin forecasts up slightly to reflect recent repricing.

(NAB.AU)

Earnings move up 1-2%. See Essentials 4 July.

Downward Revisions

Aust Infrastructure Fund OUTPERFORM NEUTRAL AIX is trading similar to SYD in terms of discount to NAV. AIX multiple has expanded and the

(AIX.AU)

internalisation has been factored in. See Essentials 2 July.

Ansell OUTPERFORM NEUTRAL Downgrade to Neutral. With a market-leading position in each product area, we remain positive

(ANN.AU)

on ANN for the longer-term. In the near-term however we do see risk to the stock given the challenges each Division faces in FY13. See Essentials 4 July.

Boral NEUTRAL UNDERPERFORM We moved to an Underperform recommendation from Neutral. Weather impacts, a tough

(BLD.AU)

domestic housing outlook in CY12 together with a slow recovery in the non-residential market is likely to see trading conditions remain challenging for BLD. See Essentials 28 June.

Cochlear OUTPERFORM NEUTRAL Downgrade to Neutral. With COH outperforming the market by 16% over the past 6 months and

(COH.AU)

now trading in line with our valuation, we believe the stock is currently fairly valued. See Essentials 27 June.

Domino's Pizza Enterprises OUTPERFORM NEUTRAL DMP is a high quality business with strong and growing free cashflow, an undergeared balance

(DMP.AU)

sheet and a strong medium term growth outlook. However, current multiples are demanding. Recommendation reduced to Neutral. See Essentials 12 July.

UGL OUTPERFORM NEUTRAL UGL's share price has held up well in recent months. We have pulled back our recommendation

(UGL.AU)

to Neutral from Outperform on valuation grounds. See Essentials 11 July.

Source: Macquarie Research, Factset pricing, July 2012

Ma

cq

ua

rie P

rivate

Wealth

M

acqu

arie

Marq

ue

e Id

eas

13 J

uly

20

12

17

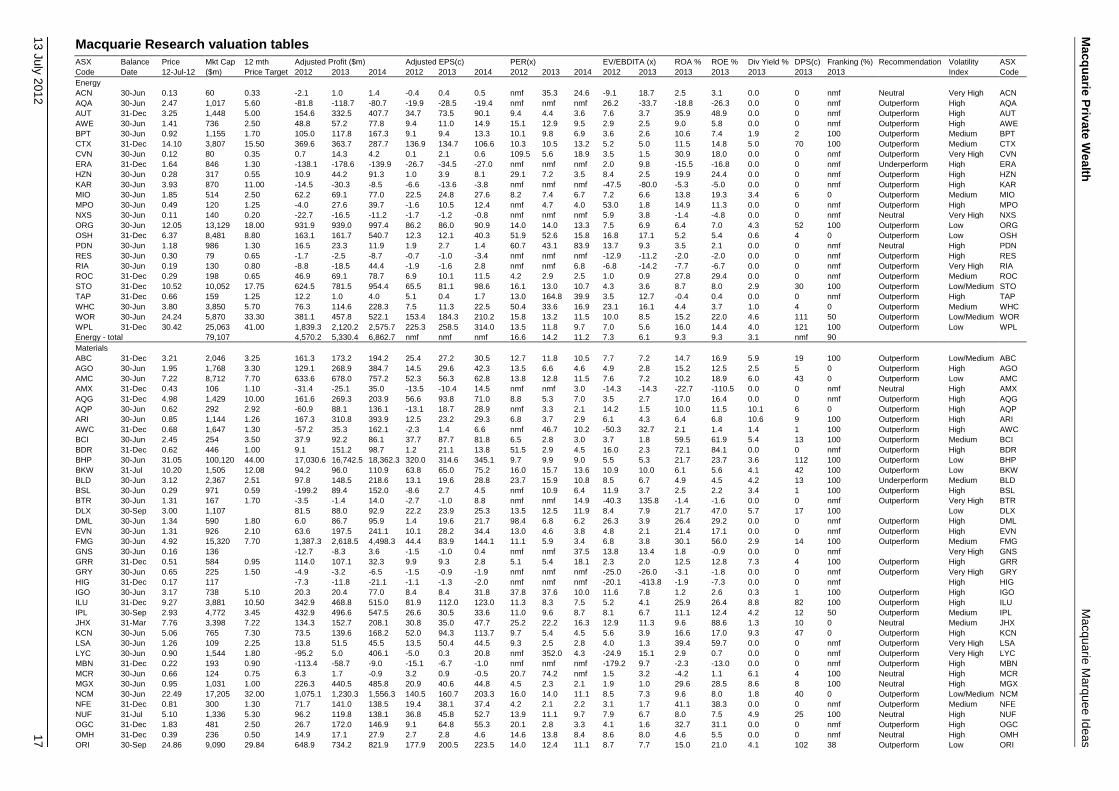

Macquarie Research valuation tables

ASX Balance Price Mkt Cap 12 mth Adjusted Profit ($m) Adjusted EPS(c) PER(x) EV/EBDITA (x) ROA % ROE % Div Yield % DPS(c) Franking (%) Recommendation Volatility ASX

Code Date 12-Jul-12 ($m) Price Target 2012 2013 2014 2012 2013 2014 2012 2013 2014 2012 2013 2013 2013 2013 2013 2013 Index Code

Energy ACN 30-Jun 0.13 60 0.33 -2.1 1.0 1.4 -0.4 0.4 0.5 nmf 35.3 24.6 -9.1 18.7 2.5 3.1 0.0 0 nmf Neutral Very High ACN

AQA 30-Jun 2.47 1,017 5.60 -81.8 -118.7 -80.7 -19.9 -28.5 -19.4 nmf nmf nmf 26.2 -33.7 -18.8 -26.3 0.0 0 nmf Outperform High AQA

AUT 31-Dec 3.25 1,448 5.00 154.6 332.5 407.7 34.7 73.5 90.1 9.4 4.4 3.6 7.6 3.7 35.9 48.9 0.0 0 nmf Outperform High AUT

AWE 30-Jun 1.41 736 2.50 48.8 57.2 77.8 9.4 11.0 14.9 15.1 12.9 9.5 2.9 2.5 9.0 5.8 0.0 0 nmf Outperform High AWE

BPT 30-Jun 0.92 1,155 1.70 105.0 117.8 167.3 9.1 9.4 13.3 10.1 9.8 6.9 3.6 2.6 10.6 7.4 1.9 2 100 Outperform Medium BPT

CTX 31-Dec 14.10 3,807 15.50 369.6 363.7 287.7 136.9 134.7 106.6 10.3 10.5 13.2 5.2 5.0 11.5 14.8 5.0 70 100 Outperform Medium CTX

CVN 30-Jun 0.12 80 0.35 0.7 14.3 4.2 0.1 2.1 0.6 109.5 5.6 18.9 3.5 1.5 30.9 18.0 0.0 0 nmf Outperform Very High CVN

ERA 31-Dec 1.64 846 1.30 -138.1 -178.6 -139.9 -26.7 -34.5 -27.0 nmf nmf nmf 2.0 9.8 -15.5 -16.8 0.0 0 nmf Underperform High ERA

HZN 30-Jun 0.28 317 0.55 10.9 44.2 91.3 1.0 3.9 8.1 29.1 7.2 3.5 8.4 2.5 19.9 24.4 0.0 0 nmf Outperform High HZN

KAR 30-Jun 3.93 870 11.00 -14.5 -30.3 -8.5 -6.6 -13.6 -3.8 nmf nmf nmf -47.5 -80.0 -5.3 -5.0 0.0 0 nmf Outperform High KAR

MIO 30-Jun 1.85 514 2.50 62.2 69.1 77.0 22.5 24.8 27.6 8.2 7.4 6.7 7.2 6.6 13.8 19.3 3.4 6 0 Outperform Medium MIO

MPO 30-Jun 0.49 120 1.25 -4.0 27.6 39.7 -1.6 10.5 12.4 nmf 4.7 4.0 53.0 1.8 14.9 11.3 0.0 0 nmf Outperform High MPO

NXS 30-Jun 0.11 140 0.20 -22.7 -16.5 -11.2 -1.7 -1.2 -0.8 nmf nmf nmf 5.9 3.8 -1.4 -4.8 0.0 0 nmf Neutral Very High NXS

ORG 30-Jun 12.05 13,129 18.00 931.9 939.0 997.4 86.2 86.0 90.9 14.0 14.0 13.3 7.5 6.9 6.4 7.0 4.3 52 100 Outperform Low ORG

OSH 31-Dec 6.37 8,481 8.80 163.1 161.7 540.7 12.3 12.1 40.3 51.9 52.6 15.8 16.8 17.1 5.2 5.4 0.6 4 0 Outperform Low OSH

PDN 30-Jun 1.18 986 1.30 16.5 23.3 11.9 1.9 2.7 1.4 60.7 43.1 83.9 13.7 9.3 3.5 2.1 0.0 0 nmf Neutral High PDN

RES 30-Jun 0.30 79 0.65 -1.7 -2.5 -8.7 -0.7 -1.0 -3.4 nmf nmf nmf -12.9 -11.2 -2.0 -2.0 0.0 0 nmf Outperform High RES

RIA 30-Jun 0.19 130 0.80 -8.8 -18.5 44.4 -1.9 -1.6 2.8 nmf nmf 6.8 -6.8 -14.2 -7.7 -6.7 0.0 0 nmf Outperform Very High RIA

ROC 31-Dec 0.29 198 0.65 46.9 69.1 78.7 6.9 10.1 11.5 4.2 2.9 2.5 1.0 0.9 27.8 29.4 0.0 0 nmf Outperform Medium ROC

STO 31-Dec 10.52 10,052 17.75 624.5 781.5 954.4 65.5 81.1 98.6 16.1 13.0 10.7 4.3 3.6 8.7 8.0 2.9 30 100 Outperform Low/Medium STO

TAP 31-Dec 0.66 159 1.25 12.2 1.0 4.0 5.1 0.4 1.7 13.0 164.8 39.9 3.5 12.7 -0.4 0.4 0.0 0 nmf Outperform High TAP

WHC 30-Jun 3.80 3,850 5.70 76.3 114.6 228.3 7.5 11.3 22.5 50.4 33.6 16.9 23.1 16.1 4.4 3.7 1.0 4 0 Outperform Medium WHC

WOR 30-Jun 24.24 5,870 33.30 381.1 457.8 522.1 153.4 184.3 210.2 15.8 13.2 11.5 10.0 8.5 15.2 22.0 4.6 111 50 Outperform Low/Medium WOR

WPL 31-Dec 30.42 25,063 41.00 1,839.3 2,120.2 2,575.7 225.3 258.5 314.0 13.5 11.8 9.7 7.0 5.6 16.0 14.4 4.0 121 100 Outperform Low WPL

Energy - total 79,107 4,570.2 5,330.4 6,862.7 nmf nmf nmf 16.6 14.2 11.2 7.3 6.1 9.3 9.3 3.1 nmf 90

Materials ABC 31-Dec 3.21 2,046 3.25 161.3 173.2 194.2 25.4 27.2 30.5 12.7 11.8 10.5 7.7 7.2 14.7 16.9 5.9 19 100 Outperform Low/Medium ABC

AGO 30-Jun 1.95 1,768 3.30 129.1 268.9 384.7 14.5 29.6 42.3 13.5 6.6 4.6 4.9 2.8 15.2 12.5 2.5 5 0 Outperform High AGO

AMC 30-Jun 7.22 8,712 7.70 633.6 678.0 757.2 52.3 56.3 62.8 13.8 12.8 11.5 7.6 7.2 10.2 18.9 6.0 43 0 Outperform Low AMC

AMX 31-Dec 0.43 106 1.10 -31.4 -25.1 35.0 -13.5 -10.4 14.5 nmf nmf 3.0 -14.3 -14.3 -22.7 -110.5 0.0 0 nmf Neutral High AMX

AQG 31-Dec 4.98 1,429 10.00 161.6 269.3 203.9 56.6 93.8 71.0 8.8 5.3 7.0 3.5 2.7 17.0 16.4 0.0 0 nmf Outperform High AQG

AQP 30-Jun 0.62 292 2.92 -60.9 88.1 136.1 -13.1 18.7 28.9 nmf 3.3 2.1 14.2 1.5 10.0 11.5 10.1 6 0 Outperform High AQP

ARI 30-Jun 0.85 1,144 1.26 167.3 310.8 393.9 12.5 23.2 29.3 6.8 3.7 2.9 6.1 4.3 6.4 6.8 10.6 9 100 Outperform High ARI

AWC 31-Dec 0.68 1,647 1.30 -57.2 35.3 162.1 -2.3 1.4 6.6 nmf 46.7 10.2 -50.3 32.7 2.1 1.4 1.4 1 100 Outperform High AWC

BCI 30-Jun 2.45 254 3.50 37.9 92.2 86.1 37.7 87.7 81.8 6.5 2.8 3.0 3.7 1.8 59.5 61.9 5.4 13 100 Outperform Medium BCI

BDR 31-Dec 0.62 446 1.00 9.1 151.2 98.7 1.2 21.1 13.8 51.5 2.9 4.5 16.0 2.3 72.1 84.1 0.0 0 nmf Outperform High BDR

BHP 30-Jun 31.05 100,120 44.00 17,030.6 16,742.5 18,362.3 320.0 314.6 345.1 9.7 9.9 9.0 5.5 5.3 21.7 23.7 3.6 112 100 Outperform Low BHP

BKW 31-Jul 10.20 1,505 12.08 94.2 96.0 110.9 63.8 65.0 75.2 16.0 15.7 13.6 10.9 10.0 6.1 5.6 4.1 42 100 Outperform Low BKW

BLD 30-Jun 3.12 2,367 2.51 97.8 148.5 218.6 13.1 19.6 28.8 23.7 15.9 10.8 8.5 6.7 4.9 4.5 4.2 13 100 Underperform Medium BLD

BSL 30-Jun 0.29 971 0.59 -199.2 89.4 152.0 -8.6 2.7 4.5 nmf 10.9 6.4 11.9 3.7 2.5 2.2 3.4 1 100 Outperform High BSL

BTR 30-Jun 1.31 167 1.70 -3.5 -1.4 14.0 -2.7 -1.0 8.8 nmf nmf 14.9 -40.3 135.8 -1.4 -1.6 0.0 0 nmf Outperform Very High BTR

DLX 30-Sep 3.00 1,107

81.5 88.0 92.9 22.2 23.9 25.3 13.5 12.5 11.9 8.4 7.9 21.7 47.0 5.7 17 100

Low DLX

DML 30-Jun 1.34 590 1.80 6.0 86.7 95.9 1.4 19.6 21.7 98.4 6.8 6.2 26.3 3.9 26.4 29.2 0.0 0 nmf Outperform High DML

EVN 30-Jun 1.31 926 2.10 63.6 197.5 241.1 10.1 28.2 34.4 13.0 4.6 3.8 4.8 2.1 21.4 17.1 0.0 0 nmf Outperform High EVN

FMG 30-Jun 4.92 15,320 7.70 1,387.3 2,618.5 4,498.3 44.4 83.9 144.1 11.1 5.9 3.4 6.8 3.8 30.1 56.0 2.9 14 100 Outperform Medium FMG

GNS 30-Jun 0.16 136

-12.7 -8.3 3.6 -1.5 -1.0 0.4 nmf nmf 37.5 13.8 13.4 1.8 -0.9 0.0 0 nmf

Very High GNS

GRR 31-Dec 0.51 584 0.95 114.0 107.1 32.3 9.9 9.3 2.8 5.1 5.4 18.1 2.3 2.0 12.5 12.8 7.3 4 100 Outperform High GRR

GRY 30-Jun 0.65 225 1.50 -4.9 -3.2 -6.5 -1.5 -0.9 -1.9 nmf nmf nmf -25.0 -26.0 -3.1 -1.8 0.0 0 nmf Outperform Very High GRY

HIG 31-Dec 0.17 117

-7.3 -11.8 -21.1 -1.1 -1.3 -2.0 nmf nmf nmf -20.1 -413.8 -1.9 -7.3 0.0 0 nmf

High HIG

IGO 30-Jun 3.17 738 5.10 20.3 20.4 77.0 8.4 8.4 31.8 37.8 37.6 10.0 11.6 7.8 1.2 2.6 0.3 1 100 Outperform High IGO

ILU 31-Dec 9.27 3,881 10.50 342.9 468.8 515.0 81.9 112.0 123.0 11.3 8.3 7.5 5.2 4.1 25.9 26.4 8.8 82 100 Outperform High ILU

IPL 30-Sep 2.93 4,772 3.45 432.9 496.6 547.5 26.6 30.5 33.6 11.0 9.6 8.7 8.1 6.7 11.1 12.4 4.2 12 50 Outperform Medium IPL

JHX 31-Mar 7.76 3,398 7.22 134.3 152.7 208.1 30.8 35.0 47.7 25.2 22.2 16.3 12.9 11.3 9.6 88.6 1.3 10 0 Neutral Medium JHX

KCN 30-Jun 5.06 765 7.30 73.5 139.6 168.2 52.0 94.3 113.7 9.7 5.4 4.5 5.6 3.9 16.6 17.0 9.3 47 0 Outperform High KCN

LSA 30-Jun 1.26 109 2.25 13.8 51.5 45.5 13.5 50.4 44.5 9.3 2.5 2.8 4.0 1.3 39.4 59.7 0.0 0 nmf Outperform Very High LSA

LYC 30-Jun 0.90 1,544 1.80 -95.2 5.0 406.1 -5.0 0.3 20.8 nmf 352.0 4.3 -24.9 15.1 2.9 0.7 0.0 0 nmf Outperform Very High LYC

MBN 31-Dec 0.22 193 0.90 -113.4 -58.7 -9.0 -15.1 -6.7 -1.0 nmf nmf nmf -179.2 9.7 -2.3 -13.0 0.0 0 nmf Outperform High MBN

MCR 30-Jun 0.66 124 0.75 6.3 1.7 -0.9 3.2 0.9 -0.5 20.7 74.2 nmf 1.5 3.2 -4.2 1.1 6.1 4 100 Neutral High MCR

MGX 30-Jun 0.95 1,031 1.00 226.3 440.5 485.8 20.9 40.6 44.8 4.5 2.3 2.1 1.9 1.0 29.6 28.5 8.6 8 100 Neutral High MGX

NCM 30-Jun 22.49 17,205 32.00 1,075.1 1,230.3 1,556.3 140.5 160.7 203.3 16.0 14.0 11.1 8.5 7.3 9.6 8.0 1.8 40 0 Outperform Low/Medium NCM

NFE 31-Dec 0.81 300 1.30 71.7 141.0 138.5 19.4 38.1 37.4 4.2 2.1 2.2 3.1 1.7 41.1 38.3 0.0 0 nmf Outperform Medium NFE

NUF 31-Jul 5.10 1,336 5.30 96.2 119.8 138.1 36.8 45.8 52.7 13.9 11.1 9.7 7.9 6.7 8.0 7.5 4.9 25 100 Neutral High NUF

OGC 31-Dec 1.83 481 2.50 26.7 172.0 146.9 9.1 64.8 55.3 20.1 2.8 3.3 4.1 1.6 32.7 31.1 0.0 0 nmf Outperform High OGC

OMH 31-Dec 0.39 236 0.50 14.9 17.1 27.9 2.7 2.8 4.6 14.6 13.8 8.4 8.6 8.0 4.6 5.5 0.0 0 nmf Neutral High OMH

ORI 30-Sep 24.86 9,090 29.84 648.9 734.2 821.9 177.9 200.5 223.5 14.0 12.4 11.1 8.7 7.7 15.0 21.0 4.1 102 38 Outperform Low ORI

Ma

cq

ua

rie P

rivate

Wealth

M

acqu

arie

Marq

ue

e Id

eas

13 J

uly

20

12

18

ASX Balance Price Mkt Cap 12 mth Adjusted Profit ($m) Adjusted EPS(c) PER(x) EV/EBDITA (x) ROA % ROE % Div Yield % DPS(c) Franking (%) Recommendation Volatility ASX

Code Date 12-Jul-12 ($m) Price Target 2012 2013 2014 2012 2013 2014 2012 2013 2014 2012 2013 2013 2013 2013 2013 2013 Index Code

OZL 31-Dec 7.55 2,293 12.33 172.2 211.8 177.9 55.9 69.4 58.3 13.5 10.9 13.0 2.9 3.1 8.3 7.6 4.6 35 50 Outperform Medium OZL

PAN 30-Jun 0.62 149

8.8 8.0 5.1 4.2 3.8 2.4 14.7 16.3 25.5 1.2 1.4 0.2 2.6 2.5 2 100

High PAN

PEM 31-Dec 0.27 208 0.50 40.5 66.1 73.5 5.1 8.3 9.3 5.3 3.2 2.9 3.2 2.3 14.1 15.4 0.0 0 nmf Outperform High PEM

PNA 31-Dec 2.53 1,530 3.70 197.7 300.9 242.9 33.3 50.7 40.9 7.6 5.0 6.2 4.1 2.9 29.1 28.6 0.0 0 nmf Outperform High PNA

PRU 30-Jun 2.45 1,122 3.30 47.7 125.4 193.6 11.3 29.7 45.8 21.7 8.3 5.3 22.6 5.2 30.9 30.2 0.0 0 nmf Outperform High PRU

RIO 31-Dec 55.65 24,250 88.00 11,357.2 13,276.8 12,641.9 596.1 698.7 665.3 9.3 8.0 8.4 5.2 4.6 17.8 21.9 2.7 148 100 Outperform Low/Medium RIO

SBM 30-Jun 1.44 466 2.30 116.9 162.7 104.6 39.9 55.5 35.7 3.6 2.6 4.0 1.7 1.5 21.8 26.1 0.0 0 nmf Neutral High SBM

SFR 30-Jun 6.96 1,055 7.00 -41.1 326.0 284.6 -27.3 215.7 188.3 nmf 3.2 3.7 -23.7 2.4 66.5 124.9 0.0 0 nmf Neutral High SFR

SGM 30-Jun 8.95 1,833 11.21 90.2 149.3 237.5 43.8 72.5 115.4 20.4 12.3 7.8 7.6 5.8 6.3 6.1 6.6 59 43 Underperform Medium SGM

TRY 30-Jun 3.95 353 6.50 59.7 122.5 101.5 67.1 137.6 114.1 5.9 2.9 3.5 2.6 1.4 75.0 54.2 0.8 3 0 Outperform Medium TRY

WSA 30-Jun 3.90 701 5.90 55.7 58.4 78.4 31.0 32.5 43.6 12.6 12.0 8.9 6.9 5.8 14.5 18.0 4.4 17 0 Outperform Medium WSA

YAL 30-Jun 1.02 1,009 1.80 86.1 60.0 215.8 16.0 6.0 21.7 6.3 16.9 4.7 18.3 8.2 5.4 2.4 0.0 0 nmf Neutral Very High YAL

Materials - total 222,149 34,964.7 41,191.7 45,876.6 nmf nmf nmf 11.3 9.5 8.3 5.9 5.1 16.6 19.1 3.4 nmf 80

Industrials AAX 31-Dec 3.42 424 4.12 39.9 48.5 53.1 32.0 38.7 42.3 10.7 8.8 8.1 6.4 5.5 14.2 17.2 5.6 19 35 Outperform High AAX

AIO 30-Jun 4.26 4,155 6.55 239.7 373.8 416.3 24.6 38.3 42.7 17.3 11.1 10.0 7.8 6.4 10.1 10.7 2.7 12 100 Outperform Low AIO

AIX 30-Jun 2.40 1,490 2.42 22.5 15.1 79.5 3.6 2.4 12.8 66.3 98.9 18.8 -15.4 -6.2 12.7 0.8 4.4 11 47 Neutral Low AIX

ALS 31-May 1.96 185

14.1 20.4 23.1 15.0 21.6 24.5 13.1 9.1 8.0 7.2 5.9 6.1 5.1 6.6 13 100

High ALS

ASB 30-Jun 1.62 305 1.63 10.6 44.2 70.2 5.7 23.5 37.3 28.6 6.9 4.3 13.2 5.4 7.9 15.5 7.4 12 100 Neutral Low/Medium ASB

ASL 30-Jun 3.35 1,020 4.55 114.6 129.5 149.8 37.4 41.9 47.8 9.0 8.0 7.0 4.3 3.8 14.4 16.7 4.9 17 100 Outperform Medium ASL

BKN 30-Jun 5.14 867 6.21 95.4 118.1 134.2 57.3 68.9 76.5 9.0 7.5 6.7 6.3 5.3 12.4 15.6 8.4 43 100 Neutral Low/Medium BKN

BLY 31-Dec 2.81 1,296 4.87 218.7 238.0 265.4 48.0 52.2 58.2 5.9 5.4 4.8 3.3 2.9 16.7 18.6 5.6 16 15 Outperform High BLY

BXB 30-Jun 6.05 9,409 6.95 603.8 663.6 734.5 40.2 42.7 47.3 15.1 14.2 12.8 8.1 7.6 14.1 22.9 5.1 31 20 Neutral Low BXB

CAB 30-Jun 5.05 608 4.90 67.6 71.3 75.5 56.2 59.2 62.7 9.0 8.5 8.1 8.3 7.9 20.5 23.5 7.8 39 100 Underperform Low/Medium CAB

CDD 30-Jun 7.86 1,089 7.91 76.8 95.7 100.7 63.5 68.0 71.2 12.4 11.6 11.0 9.1 7.6 14.7 18.0 5.3 42 70 Outperform Low CDD

CLO 30-Jun 0.72 558 0.91 54.2 63.1 66.8 7.0 8.1 8.6 10.3 8.9 8.4 7.0 5.8 12.9 17.3 4.2 3 100 Outperform Medium CLO

CPB 31-Mar 52.74 3,592 62.70 222.4 256.7 279.3 329.4 380.2 413.5 16.0 13.9 12.8 10.5 9.2 22.9 26.5 4.8 255 50 Neutral Low CPB

CSR 31-Mar 1.23 622 1.98 90.3 79.7 111.2 17.8 15.7 22.0 6.9 7.8 5.6 2.3 2.3 6.6 6.4 11.4 14 0 Neutral Low CSR

DOW 30-Jun 3.07 1,317 4.20 168.1 179.8 192.6 39.2 41.9 44.7 7.8 7.3 6.9 3.2 3.0 8.8 10.7 3.3 10 75 Outperform Medium DOW

EHL 30-Jun 0.84 527 0.94 68.2 77.8 83.9 10.8 12.3 13.3 7.7 6.8 6.3 3.3 2.9 12.1 11.8 6.6 6 100 Neutral Low/Medium EHL

GNG 30-Jun 0.97 146 1.44 13.8 21.0 23.1 9.2 13.9 15.3 10.6 7.0 6.3 5.0 3.2 36.3 44.6 8.2 8 100 Neutral High GNG

GWA 30-Jun 2.05 619 2.07 41.3 48.3 52.6 13.7 16.0 17.4 15.0 12.8 11.8 8.7 7.9 10.9 11.6 8.8 18 100 Neutral Low/Medium GWA

KSC 30-Jun 1.30 116 1.46 14.8 15.9 18.3 16.9 17.9 20.3 7.7 7.2 6.4 3.4 3.2 7.5 7.0 8.5 11 100 Outperform Low/Medium KSC

LEI 31-Dec 15.39 5,188 19.50 413.8 661.9 777.2 123.0 196.7 230.9 12.5 7.8 6.7 3.1 2.6 11.2 22.2 7.7 118 50 Underperform Medium LEI

LYL 30-Jun 7.06 273 8.25 22.3 25.6 28.3 57.6 66.2 73.2 12.3 10.7 9.6 7.5 6.6 33.1 41.5 6.1 43 100 Outperform Low/Medium LYL

MAH 30-Jun 0.53 391 1.01 56.9 65.3 72.6 7.5 8.5 9.3 7.0 6.2 5.7 1.9 1.6 12.2 16.6 6.6 4 100 Outperform High MAH

MIN 30-Jun 8.72 1,612 12.12 169.4 206.7 259.3 91.8 111.2 139.5 9.5 7.8 6.3 5.2 4.2 21.9 25.6 6.3 55 100 Outperform Low/Medium MIN

MND 30-Jun 21.64 1,919 24.97 120.3 140.1 156.3 132.2 153.1 170.5 16.4 14.1 12.7 9.3 7.9 27.6 59.8 5.8 125 100 Outperform Low/Medium MND

MQA 31-Dec 1.39 665 1.82 150.0 169.4 210.4 31.8 35.0 43.0 4.4 4.0 3.2 13.5 12.5 5.4 -96.5 8.3 12 0 Neutral Medium MQA

MRM 30-Jun 2.64 579 3.47 51.8 57.0 62.6 23.0 24.8 26.8 11.5 10.6 9.8 6.3 5.9 16.2 17.2 4.0 11 100 Outperform Low/Medium MRM

NWH 30-Jun 3.15 878 4.78 93.2 107.0 118.3 33.4 38.4 42.4 9.4 8.2 7.4 4.5 3.9 21.0 46.7 6.3 20 100 Outperform High NWH

PPX 30-Jun 0.05 33 0.17 -37.7 -56.8 -53.1 -6.2 -9.3 -8.7 nmf nmf nmf 33.9 -303.8 -1.3 -9.6 0.0 0 nmf Neutral Very High PPX

PRG 31-Mar 2.24 265 2.60 30.2 33.9 35.4 25.4 28.4 29.7 8.8 7.9 7.5 5.3 5.0 7.7 8.9 5.8 13 100 Outperform High PRG

QAN 30-Jun 1.05 2,367 1.21 61.0 327.4 313.0 2.7 14.5 13.8 38.8 7.2 7.6 3.3 2.7 3.4 5.3 0.0 0 nmf Neutral High QAN

QRN 30-Jun 3.30 8,052 4.30 369.3 556.0 562.2 15.1 22.8 23.0 21.8 14.5 14.3 9.0 6.7 8.3 7.6 3.8 13 63 Outperform Low QRN

QUB 30-Jun 1.50 1,382 1.65 62.5 65.3 74.1 7.8 7.2 8.1 19.3 20.8 18.5 24.8 9.3 8.3 6.1 2.9 4 100 Neutral Medium QUB

RCR 30-Jun 1.75 230 2.62 27.9 36.9 41.2 20.9 27.6 30.9 8.4 6.3 5.7 4.3 3.4 12.6 15.8 5.1 9 100 Outperform Medium RCR

RQL 30-Jun 0.37 91 0.54 11.7 12.0 13.0 4.7 4.8 5.2 7.9 7.7 7.1 4.6 3.7 14.4 12.0 2.7 1 100 Outperform High RQL

RWH 30-Jun 2.13 214 2.30 16.3 19.9 22.0 16.2 19.9 21.9 13.2 10.7 9.7 7.6 6.5 11.4 14.1 3.7 8 100 Outperform Low RWH

SAI 30-Jun 4.61 942 5.02 52.7 61.3 67.8 26.1 30.3 33.5 17.7 15.2 13.8 10.9 9.5 11.4 17.5 3.5 16 100 Outperform Low SAI

SEK 30-Jun 6.00 2,023 6.77 128.4 153.3 170.7 38.1 45.5 50.7 15.7 13.2 11.8 11.8 9.5 23.6 35.8 3.8 23 100 Neutral Low/Medium SEK

SKE 30-Jun 2.28 532 2.66 49.0 54.2 61.5 21.0 23.2 26.3 10.9 9.8 8.7 6.7 6.3 12.0 11.9 4.8 11 100 Outperform Medium SKE

SLM 30-Jun 2.22 355

38.9 38.5 41.8 24.4 24.1 26.2 9.1 9.2 8.5 6.2 6.2 8.8 14.1 8.8 20 100

Low/Medium SLM

SPT 30-Jun 2.61 694 1.68 40.8 42.4 46.9 15.4 16.0 17.7 17.0 16.4 14.8 5.8 5.6 6.9 9.2 4.0 11 100 Neutral Medium SPT

SVW 30-Jun 7.05 2,167 11.78 259.7 321.6 343.5 83.9 103.7 110.7 8.4 6.8 6.4 7.6 6.2 9.4 13.6 5.1 36 100 Outperform Medium SVW

SYD 31-Dec 2.90 5,398 2.96 66.6 103.2 122.5 3.6 5.5 6.6 81.1 52.3 44.1 13.5 12.6 5.0 5.7 7.9 23 0 Neutral Low SYD

TCL 30-Jun 5.68 8,283 6.80 68.1 137.3 163.8 4.7 9.4 11.1 120.5 60.6 51.2 24.9 18.2 3.7 4.4 5.7 33 22 Outperform Low TCL

TOL 30-Jun 3.87 2,775 5.12 253.4 287.1 328.3 35.4 40.0 45.8 10.9 9.7 8.5 5.8 5.5 7.4 10.3 6.5 25 100 Outperform Medium TOL

TPI 30-Jun 0.74 1,168 0.88 67.1 96.5 122.8 5.2 6.1 7.8 14.3 12.1 9.5 5.4 5.1 7.5 4.5 0.0 0 nmf Outperform Medium TPI

TSE 30-Jun 1.74 909 2.45 121.0 134.2 150.3 22.1 24.6 27.5 7.8 7.1 6.3 5.5 4.9 7.6 12.0 8.9 16 50 Neutral Medium TSE

UGL 30-Jun 12.39 2,061 13.50 169.9 185.6 202.4 102.8 112.3 122.5 12.1 11.0 10.1 8.0 7.2 9.5 15.5 6.1 76 100 Neutral Low UGL

VAH 30-Jun 0.39 851 0.50 63.0 156.8 218.0 2.9 7.2 10.0 13.4 5.4 3.9 4.5 3.3 6.4 15.1 0.0 0 nmf Outperform High VAH

WDS 30-Jun 0.42 61 0.70 9.0 12.8 13.9 6.1 8.6 9.2 6.9 4.9 4.6 2.0 1.7 8.3 7.2 9.5 4 100 Neutral High WDS

WHG 30-Jun 0.86 228 0.90 23.8 26.6 28.6 8.9 9.9 10.7 9.7 8.6 8.0 6.0 5.5 9.9 9.6 9.3 8 100 Neutral Low WHG

Industrials - total 80,929 5,206.9 6,799.2 7,705.7 nmf nmf nmf 15.6 12.3 10.9 7.2 6.2 8.4 11.8 5.2 nmf 55

Consumer Discretionary AAD 30-Jun 1.27 423 1.10 33.1 36.2 40.3 10.2 11.0 11.9 12.4 11.5 10.6 7.9 7.6 7.4 8.4 10.3 13 0 Neutral Medium AAD

AHE 30-Jun 2.60 678 2.58 62.5 72.8 80.7 24.0 28.0 31.0 10.8 9.3 8.4 7.5 6.7 11.1 15.4 7.7 20 100 Neutral Low/Medium AHE

Ma

cq

ua

rie P

rivate

Wealth

M

acqu

arie

Marq

ue

e Id

eas

13 J

uly

20

12

19

ASX Balance Price Mkt Cap 12 mth Adjusted Profit ($m) Adjusted EPS(c) PER(x) EV/EBDITA (x) ROA % ROE % Div Yield % DPS(c) Franking (%) Recommendation Volatility ASX

Code Date 12-Jul-12 ($m) Price Target 2012 2013 2014 2012 2013 2014 2012 2013 2014 2012 2013 2013 2013 2013 2013 2013 Index Code

ALL 31-Dec 2.56 1,409 2.60 88.0 115.2 134.9 16.0 20.5 23.7 16.0 12.5 10.8 9.7 8.1 21.5 30.3 4.8 12 0 Neutral Medium ALL

APN 31-Dec 0.61 393 0.70 73.6 76.4 82.8 11.4 11.4 12.0 5.3 5.3 5.0 5.6 5.9 7.6 8.0 11.6 7 100 Underperform Medium APN

ARP 30-Jun 9.02 654 9.50 38.1 43.3 48.5 52.6 59.7 67.0 17.1 15.1 13.5 10.8 9.7 26.4 27.0 3.3 30 100 Outperform Low ARP

BBG 30-Jun 1.05 432

39.4 60.6 66.2 12.2 16.5 13.9 8.6 6.4 7.6 5.7 2.1 4.0 4.5 0.0 0 nmf

Very High BBG

BRG 30-Jun 4.46 580 4.80 45.1 49.9 54.3 34.2 37.8 41.1 13.0 11.8 10.8 8.0 7.5 23.0 27.3 4.9 22 100 Outperform Medium BRG

CMJ 30-Jun 3.38 1,899 3.27 92.5 96.1 111.3 16.5 17.1 19.8 20.5 19.8 17.1 -226.6 -314.5 15.6 27.1 4.9 17 0 Neutral Low CMJ

CTD 30-Jun 2.08 156 2.30 11.8 13.3 14.2 16.3 17.7 19.0 12.7 11.7 10.9 8.6 7.6 21.6 25.0 4.3 9 100 Outperform Medium CTD

CWN 30-Jun 8.56 6,235 10.00 434.6 479.1 559.7 59.1 65.8 76.8 14.5 13.0 11.1 10.3 9.5 12.2 14.7 4.3 37 50 Outperform Low CWN

DJS 31-Jul 2.35 1,242 3.12 111.2 124.9 124.6 21.2 23.8 23.7 11.1 9.9 9.9 6.0 5.5 15.3 16.1 8.9 21 100 Outperform Medium DJS

DMP 30-Jun 10.30 720 10.14 26.3 31.4 35.4 36.8 43.7 49.2 28.0 23.5 20.9 15.0 12.9 23.9 26.5 3.1 32 100 Neutral Low DMP

EGG 30-Jun 0.61 52 0.50 -1.2 1.1 2.8 -1.4 1.3 3.3 nmf 48.3 18.4 1.1 1.7 2.8 0.7 0.0 0 nmf Underperform Very High EGG

EGP 30-Jun 4.25 3,509

119.8 179.2 222.3 16.9 21.7 26.7 25.1 19.6 15.9 11.4 9.9 7.8 6.3 2.6 11 100

Low/Medium EGP

FAN 30-Jun 2.25 231 2.60 23.9 26.8 28.9 23.3 26.1 28.2 9.7 8.6 8.0 5.9 5.3 20.5 22.9 6.7 15 100 Outperform Low/Medium FAN

FLT 30-Jun 20.63 2,064 22.97 200.4 213.7 229.0 198.9 211.8 226.6 10.4 9.7 9.1 5.9 5.6 13.4 23.9 5.1 106 100 Neutral Medium FLT

FWD 30-Jun 12.20 722 14.11 53.2 60.2 66.0 88.0 97.9 105.8 13.9 12.5 11.5 7.6 7.0 26.9 25.1 6.6 81 100 Outperform Low FWD

FXJ 30-Jun 0.57 1,329 0.60 200.0 157.5 149.6 8.5 6.7 6.4 6.6 8.4 8.9 4.6 5.0 5.1 3.4 4.1 2 100 Underperform Medium FXJ

GUD 30-Jun 8.82 624 8.30 44.3 47.0 51.1 63.7 67.4 73.3 13.8 13.1 12.0 8.7 8.3 15.2 15.4 10.2 90 100 Neutral Low GUD

HVN 30-Jun 1.92 2,034 1.90 181.0 199.0 184.5 17.1 18.8 17.4 11.2 10.2 11.0 7.1 6.7 7.4 8.0 4.7 9 100 Underperform Low/Medium HVN

IVC 31-Dec 8.02 882 8.40 44.5 48.7 51.6 40.8 44.6 47.3 19.7 18.0 17.0 11.4 10.8 10.3 31.5 4.5 36 100 Outperform Low IVC

JBH 30-Jun 8.82 872 15.04 105.8 109.3 118.2 104.3 106.8 115.4 8.5 8.3 7.6 4.7 4.6 20.1 52.8 7.4 65 100 Outperform Medium JBH

KMD 31-Jul 1.13 226 1.45 26.2 31.4 37.3 13.1 15.7 18.6 8.6 7.2 6.1 5.9 4.9 17.4 14.1 8.4 10 100 Outperform High KMD

MYR 31-Jul 1.68 977 2.17 136.6 141.9 144.0 22.7 23.6 23.9 7.4 7.1 7.0 4.2 4.2 11.4 16.2 11.4 19 100 Neutral Medium MYR

NVT 30-Jun 4.28 1,606 4.05 73.9 85.6 96.2 19.7 22.8 25.6 21.7 18.8 16.7 13.9 12.2 18.8 35.0 5.1 22 100 Neutral Low/Medium NVT

NWS 30-Jun 21.62 17,264 21.95 3,336.1 3,315.0 3,644.3 133.6 149.1 178.0 16.2 14.5 12.1 8.6 7.7 10.9 13.4 0.7 16 0 Neutral Low NWS

PBG 30-Jun 0.48 438 0.75 72.5 82.1 89.4 7.5 9.8 10.6 6.4 4.9 4.5 4.3 4.0 10.8 10.7 10.6 5 100 Neutral Medium PBG

PMV 31-Jul 4.73 734 5.70 57.3 66.2 71.2 36.6 42.2 45.4 12.9 11.2 10.4 5.8 5.1 6.1 5.5 7.6 36 100 Neutral Low PMV

PRT 30-Jun 0.67 244 0.81 27.7 29.5 31.3 7.5 8.0 8.5 8.9 8.3 7.8 6.2 6.0 14.0 18.0 9.0 6 100 Outperform Low/Medium PRT

REA 30-Jun 13.45 1,772 14.68 84.3 96.9 109.2 64.3 73.6 82.9 20.9 18.3 16.2 12.9 11.0 40.2 37.0 2.7 37 100 Outperform Low REA

SFH 30-Jun 0.52 100 0.40 3.0 9.8 12.4 1.6 5.1 6.4 32.9 10.1 8.1 3.5 2.8 9.6 17.4 3.8 2 100 Underperform High SFH

SGH 30-Jun 1.92 324 1.83 30.0 39.3 42.1 19.2 22.4 23.6 10.0 8.6 8.1 7.6 5.9 11.0 17.8 3.5 7 100 Neutral Low/Medium SGH

SGN 31-Dec 0.94 339 1.05 43.4 45.7 46.8 11.9 12.6 12.9 7.8 7.4 7.2 4.9 4.7 10.6 12.0 9.4 9 100 Neutral Medium SGN

SUL 30-Jun 7.27 1,426 7.70 92.0 122.4 137.2 53.7 62.2 69.8 13.5 11.7 10.4 7.8 7.4 14.7 19.2 4.8 35 100 Outperform Low/Medium SUL

SWM 30-Jun 1.60 1,062 3.54 235.0 248.9 253.7 33.4 35.1 34.6 4.8 4.5 4.6 5.7 5.9 9.2 9.2 12.4 20 100 Outperform High SWM

SXL 30-Jun 1.14 800 1.48 106.0 115.8 128.0 15.0 16.4 18.2 7.5 6.9 6.2 6.1 5.9 8.7 7.0 8.7 10 100 Outperform Medium SXL

TAH 30-Jun 2.91 2,125 3.20 343.9 181.4 183.0 48.0 24.5 24.3 6.1 11.9 12.0 4.0 5.6 11.4 12.5 6.9 20 100 Outperform Low TAH

TEN 31-Aug 0.48 646 0.52 13.6 26.2 42.8 1.2 1.9 3.0 38.6 25.7 15.9 7.8 9.9 4.7 3.0 0.0 0 nmf Neutral Medium TEN

TGA 31-Mar 1.54 225 1.51 29.1 29.9 30.3 20.7 20.4 20.7 7.4 7.5 7.4 5.3 5.3 21.6 20.3 6.3 10 100 Neutral Low/Medium TGA

TRS 30-Jun 9.13 238 13.00 20.9 23.1 26.7 79.5 87.9 101.7 11.5 10.4 9.0 5.5 5.1 21.9 32.2 6.0 55 100 Outperform Low/Medium TRS

TTS 30-Jun 2.64 3,598 2.40 308.9 224.7 223.6 23.1 16.4 16.0 11.4 16.1 16.5 7.1 9.1 8.6 8.4 5.3 14 100 Underperform Low TTS

WTF 30-Jun 4.18 885 4.70 57.1 61.3 66.4 26.7 28.5 30.9 15.7 14.6 13.5 8.4 7.9 31.0 63.9 6.5 27 100 Outperform Medium WTF

Consumer Discretionary - total 62,170 7,125.3 7,218.4 7,873.2 nmf nmf nmf 12.1 12.0 11.0 7.9 7.3 10.5 12.0 4.2 nmf 82

Consumer Staples CCL 31-Dec 13.35 10,164 13.84 570.2 618.0 668.9 75.3 81.2 87.5 17.7 16.4 15.3 10.3 9.7 16.1 27.2 4.8 64 100 Neutral Low CCL

ELD 30-Sep 0.22 99 0.23 14.2 24.9 27.8 3.2 5.5 6.2 6.9 4.0 3.6 9.0 8.9 3.1 4.9 0.0 0 nmf Neutral High ELD

GFF 30-Jun 0.53 1,036 0.62 108.9 131.1 141.0 6.2 5.8 7.2 8.6 9.1 7.4 5.9 5.5 9.6 8.6 10.4 6 38 Outperform High GFF

MTS 30-Apr 3.19 2,757 3.94 252.8 265.1 283.8 32.9 31.2 32.8 9.7 10.2 9.7 10.7 7.0 11.6 18.3 8.2 26 100 Neutral Low MTS

TGR 30-Jun 1.30 190 1.32 23.9 26.2 27.8 16.3 17.9 19.0 8.0 7.3 6.8 5.1 4.7 9.0 8.9 6.9 9 50 Neutral Low/Medium TGR

TWE 30-Jun 4.45 2,880 3.11 109.7 117.3 123.5 16.9 18.1 19.0 26.3 24.6 23.4 11.7 11.4 4.8 4.0 2.4 11 50 Underperform Low TWE

WES 30-Jun 30.28 30,477 30.53 2,153.0 2,238.9 2,426.9 185.8 191.6 206.3 16.3 15.8 14.7 8.9 8.6 8.4 8.6 5.8 175 100 Neutral Low WES

WOW 30-Jun 27.00 33,262 30.67 2,207.9 2,400.8 2,577.2 180.5 197.1 211.6 15.0 13.7 12.8 9.0 7.8 16.4 28.0 5.1 139 100 Outperform Low WOW

Consumer Staples - total 80,865 5,440.5 5,822.2 6,277.0 nmf nmf nmf 15.5 14.6 13.6 9.1 8.3 11.0 13.3 5.4 nmf 98

Health Care ACR 30-Jun 4.14 689 4.74 5.7 26.8 53.9 3.4 16.0 32.2 120.9 25.9 12.9 407.6 17.4 56.3 45.5 7.2 30 0 Outperform Medium ACR

ANN 30-Jun 13.18 1,722 14.46 130.8 135.0 149.1 99.6 103.3 114.2 13.2 12.8 11.5 10.5 10.1 12.0 19.6 2.9 38 0 Neutral Low ANN

API 31-Aug 0.34 166 0.43 21.8 22.7 24.0 4.5 4.6 4.9 7.6 7.3 6.9 4.1 4.0 4.2 3.9 6.5 2 100 Outperform High API

COH 30-Jun 64.74 3,686 68.50 161.1 168.4 180.3 283.5 296.0 316.8 22.8 21.9 20.4 15.2 14.5 30.1 40.3 4.2 270 60 Neutral Medium COH

CSL 30-Jun 38.50 19,505 39.00 989.5 1,121.1 1,212.0 190.1 225.3 244.8 20.3 17.1 15.7 13.8 11.9 23.4 30.3 2.7 105 3 Outperform Low CSL