Embed Size (px)

Citation preview

2013 FROST & SULLIVAN AUSTRALIADATA COMMUNICATIONSSERVICE PROVIDER OF THE YEAR

Frost & Sullivan’s Global Research Platform

Frost & Sullivan has more than 50 years of experience

as a global research organisation with 1,800 analysts

and consultants who monitor more than 300

industries and 250,000 companies. The company’s

research philosophy originates with the CEO’s 360

Degree Perspective™, which serves as the foundation

of its TEAM Research™ methodology. This unique

approach enables us to determine how best-in-class

companies worldwide manage growth, innovation and

leadership. Based on the �ndings of this Best Practices

research, Frost & Sullivan is proud to present the

award for 2013 Frost & Sullivan Australia Data

Communications Service Provider of the Year to

Telstra Corporation Limited (known as Telstra).

Australia Data CommunicationService Provider of The Year

02 “We Accelerate Growth”2 0 1 3 F R O S T & S U L L I VA N

2013 FROST & SULLIVAN AUSTRALIADATA COMMUNICATIONSSERVICE PROVIDER OF THE YEAR

2013 Frost & Sullivan 03 “We Accelerate Growth”2 0 1 3 F R O S T & S U L L I VA N

For the Service Provider of the Year Award, the following criteria were used to benchmark Telstra’s performance against its local, regional and global competitors:• Revenue and Revenue Growth• Market Share and Market Share Growth• Innovation and Achievements• Regional and Global Deliver y Capabilities• Customer Feedback

KEYBENCHMARKINGCRITERIAFOR THESERVICE PROVIDEROF THE YEAR AWARD

Australia continues to be one of the prototypes for data communications ser vices markets in the APAC region. Owing to the National Broadband Network (NBN) initiative in the countr y, the wholesale prices of broadband come down signi�cantly, resulting in a price drop for private network services as well. Never theless, a strong domestic revenue growth is expected in the long term, driven by the resources boom and the centralization of infrastructure, as a consequence of vir tualization and cloud computing.

The momentum toward IP/Ethernet ser vices is par ticular ly strong in Australia, with huge decline in revenues of legacy technologies and rapid growth in IP/Ethernet ser vices revenues. There are still concerns over data sovereignty, but many Australian enterprises are actively looking at hybrid clouds that are often located outside the national borders.

Except in the case of public clouds, most often the connectivity is through an MPLS IP VPN. While the growth of MPLS IP VPN has not affected the Ethernet revenues yet, the high-end MPLS circuits that possess speeds in excess of 100 Mbps are often competing with Ethernet ser vices.

Frost & Sullivan estimates the Australia Data Communications market to be valued at US$1.59 billion in 2012 with a healthy YoY growth rate. Among various ver ticals, the BFSI sector continues to lead the adoption.

OVERVIEW OF DATA COMMUNICATIONSMARKET IN AUSTRALIA

SIGNIFICANCE OF THESERVICE PROVIDEROF THE YEAR AWARD

Some key drivers for the increasing demand for data communications ser vices in Australia include:

Continued investment in IP/Ethernet solutions due to migration from legacy technologies, such as ATM, Frame Relay and Leased Circuits, will continue to be an impor tant driver for growth in the forecast period.

Regulatory compliance, growth in multi-media traf�c and the resultant need for quality of ser vice (QoS) have been impor tant enablers of migration toward IP/Ethernet solutions.

The data centre consolidation and growth of third par ty hosted applications and infrastructure requires more bandwidth to maintain performance levels, which also leads to a shift in demand for the type of connectivity.

With the emergence of more satellite of�ces, most large enterprises backhaul the branch traf�c to their headquar ters and thus need high-speed secure connectivity ser vices.

Growing enterprise mobility has made usage of IPSec and SSL VPN more attractive to small and medium businesses. The mobility factor would force many more enterprise users to leverage Internet to connect to corporate networks, which will have an impact on the growth on private network services.

2013 Frost & Sullivan 04 “We Accelerate Growth”2 0 1 3 F R O S T & S U L L I VA N

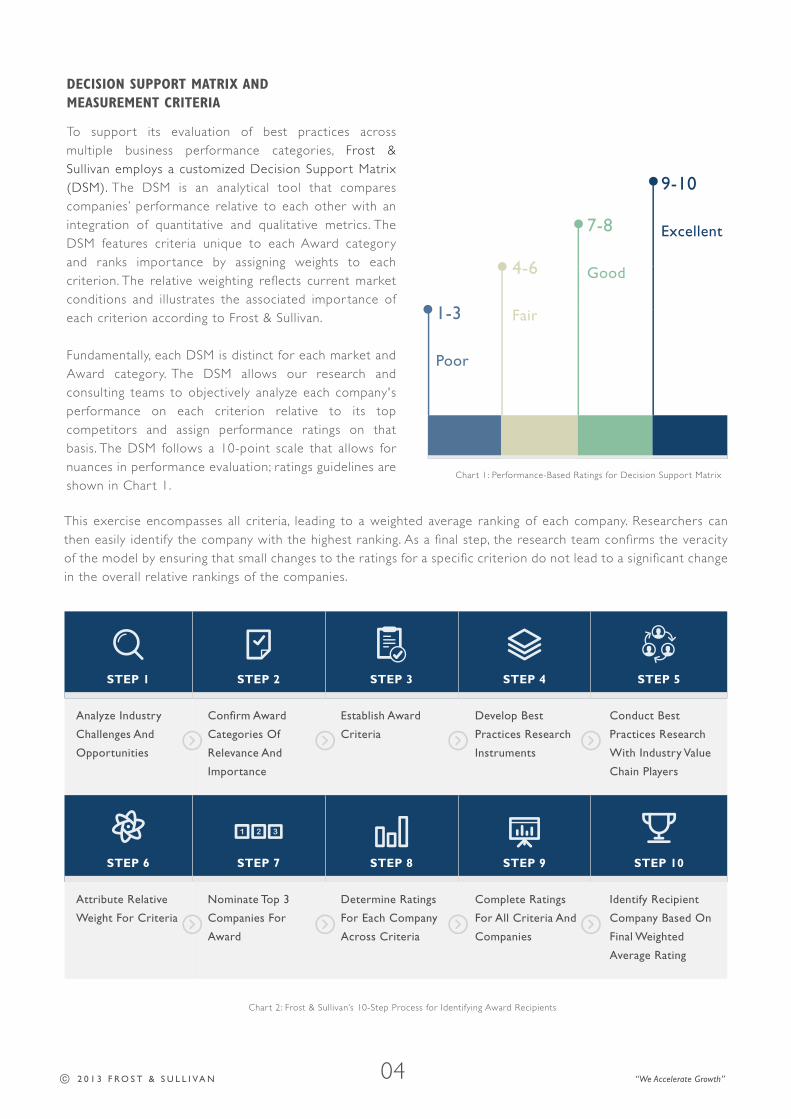

This exercise encompasses all criteria, leading to a weighted average ranking of each company. Researchers can then easily identify the company with the highest ranking. As a �nal step, the research team con�rms the veracity of the model by ensuring that small changes to the ratings for a speci�c criterion do not lead to a signi�cant change in the overall relative rankings of the companies.

Char t 2: Frost & Sullivan’s 10-Step Process for Identifying Award Recipients

To suppor t its evaluation of best practices across multiple business performance categories, Frost & Sullivan employs a customized Decision Suppor t Matrix (DSM). The DSM is an analytical tool that compares companies’ performance relative to each other with an integration of quantitative and qualitative metrics. The DSM features criteria unique to each Award category and ranks impor tance by assigning weights to each criterion. The relative weighting re�ects current market conditions and illustrates the associated impor tance of each criterion according to Frost & Sullivan.

Fundamentally, each DSM is distinct for each market and Award category. The DSM allows our research and consulting teams to objectively analyze each company's performance on each criterion relative to its top competitors and assign performance ratings on that basis. The DSM follows a 10-point scale that allows for nuances in performance evaluation; ratings guidelines are shown in Char t 1.

Char t 1: Performance-Based Ratings for Decision Suppor t Matrix

1-3

Poor

4-6

Fair

7-8

Good

9-10

Excellent

DECISION SUPPORT MATRIX ANDMEASUREMENT CRITERIA

STEP 1 STEP 2 STEP 3 STEP 4 STEP 5

Analyze Industry

Challenges And

Opportunities

Con�rm Award

Categories Of

Relevance And

Importance

Establish Award

Criteria

Develop Best

Practices Research

Instruments

Conduct Best

Practices Research

With Industry Value

Chain Players

STEP 6 STEP 7 STEP 8 STEP 9 STEP 10

Attribute Relative

Weight For Criteria

Nominate Top 3

Companies For

Award

Determine Ratings

For Each Company

Across Criteria

Complete Ratings

For All Criteria And

Companies

Identify Recipient

Company Based On

Final Weighted

Average Rating

MEASUREMENT OF 1–10 (1 = LOWEST; 10 = HIGHEST)

GROWTH STRATEGYAND IMPLEMENTATION

DEGREE OF INNOVATIONINTO BUSINESSPROCESSES

LEADERSHIP INCUSTOMER VALUEAND MARKETPENETRATION

WEIGHTEDRATING

AWARD CRITERIA

33.3%33.3%RELATIVE WEIGHT (%) 33.3% 100%

BEST PRACTICE AWARDANALYSIS FOR TELSTRA

Char t 3: Decision Suppor t Matrix

The Decision Suppor t Matrix, shown in Char t 3, illustrates the relative impor tance of each criterion for the Asia Paci�c Best Practices Award and the ratings for each company under evaluation. To remain unbiased while also protecting the interests of the other organisations reviewed, we have chosen to refer to the other key players as Competitor 1 and Competitor 2.

Australia Data CommunicationService Provider of The Year

Telstra

Competitor 1

Competitor 2

9.0

8.0

8.5

9.0

8.0

8.5

9.5

8.5

7.5

9.2

8.2

8.2

2013 Frost & Sullivan 05 “We Accelerate Growth”2 0 1 3 F R O S T & S U L L I VA N

Criterion 1: Growth Strategy and Implementation

Telstra was the only data communications ser vice provider in Australia that grew its retail business in 2012, despite the signi�cant price erosion in the market. The service provider accounted for more than half of the total market revenue and continues to grow its market share in the year.

Telstra puts a strategic focus on building a global IP VPN network with coverage of the APAC region, as well as developing submarine cables with access to satellite links and to regional data centres. Moreover, to deliver any network application or ser vice to any device in the APAC region is also one strategic goal for Telstra. To implement this, besides continuing the investment into cloud technology over the next few years, Telstra will also be expanding and upgrading its network Point-of-Presence (PoPs) and making fur ther investments in its data centres to ensure their cloud-readiness. In 2012, Telstra managed to maintain a double-digit growth in IP Access and NAS (Network Application Services).

From the product perspective, Telstra’s domestic MPLS IP VPN and Ethernet ser vices post robust growth that more than counterbalanced the loss from legacy technologies. It offers a wide spectrum of Ethernet options including Ethernet ATM, Ethernet Line (E-Line), Ethernet Lite and Ethernet MAN (Metropolitan Area Network), designed to meet various needs of businesses.

Apar t from the strong growth in domestic business, Telstra expands its international business through NNI (Network to Network Interface) with several key service providers in APAC. The service provider’s geographical coverage and scale continue to be key differentiators in the Australia market.

Criterion 2: Degree of Innovation into Business Processes

Telstra invests signi�cantly in its next-generation IP backbone in the countr y, and this leads to the launch of its IP-based offerings which cover 95 percent of Australia businesses. This Next IP network, which is also the core foundation of its hosting and cloud services, has received ISO 27001 Security Management System accreditation for IP MAN, IP WAN and IP Wireless Products and has a 99.999% target core availability.

Since the de�nitive agreement signed with the Commonwealth and NBN Co. in June 2011, Telstra formalised its par ticipation in the rollout of the National Broadband Network in March 2012, and continued to work collaboratively with NBN Co on building its access network. Following several successful trials in the ear ly released sites, Telstra has already launched retail and wholesale ser vices over the NBN.

In addition, Telstra also launched a “One-Stop-Shop” (OSS) Ethernet ser vice option and released Ethernet half circuits which extended the global reach of its Ethernet Private Line (EPL) offering in 2012.

06 “We Accelerate Growth”2 0 1 3 F R O S T & S U L L I VA N

Criterion 3: Leadership in Customer Value and Market Penetration

While its main operations are based out of Australia, Telstra has grown into one of the leading communication and connectivity ser vice provider in the Asia Paci�c region.

To satisfy the increasing connectivity demands between key global markets, Telstra expanded its network coverage by adding nine new PoPs in London, Marseille , Stockholm, Osaka, Tokyo, Sydney (2), Hong Kong and Chicago by the end of 2012. The new offering allows Telstra to ensure that SLAs for various network connectivity options are met end-to-end regardless of the location, which enables Telstra customers in these countries get instant access to key Asia Paci�c markets such as Hong Kong, Singapore and Sydney. This would allow its customers to mitigate risks and scale quickly to meet changing business and bandwidth demands, while tapping in growth oppor tunities in the Asia Paci�c region.

Fur thermore, Telstra committed to invest more on its global infrastructure and technological innova-tion for an enhanced customer experience, and to establish a largest network presence in Asia Paci�c. The service provider currently owns data centres in six countries, respectively Hong Kong, The Philip-pines, Australia, New Zealand, United Kingdom, as well as Singapore with a latest one added in 2012. In overall, it operates approximately 14,000 square metres of data centre space globally. Telstra provides a range of network connectivity options and an extensive backbone network to fully suppor t these data centres and well deliver “con-nected” colocation and hosting services to its customers.

By far, Telstra is facilitating access to over 1,400 PoPs in 230 countries and territories across the globe. Most PoPs are equipped to provide a full suite of bandwidth services, with a growing number able to offer IP Services and enable customers to connect into the major Internet exchanges.

CONCLUSIONFrost & Sullivan concludes that Telstra is the leading service provider in the Australia market that is excellent in offering secure and reliable data communications ser vices, backed by its strong network presence, continuous product excellence, as well as its leadership in customer value. Moving forward, with extended par tnerships and new market expansions, the company is expected to achieve more milestones not only in Australia but also across the Asia Paci�c region.

www.frost-awards.com.au

07 “We Accelerate Growth”2 0 1 3 F R O S T & S U L L I VA N

About Frost & Sullivan

Frost & Sullivan, the Growth Par tnership Company, works in

collaboration with clients to leverage visionary innovation that

addresses the global challenges and related growth

opportunities that will make or break today's market

par ticipants. For more than 50 years, we have been developing

growth strategies for the global 1000, emerging businesses, the

public sector and the investment community. Is your

organization prepared for the next profound wave of industry

convergence, disruptive technologies, increasing competitive

intensity, Mega Trends, breakthrough best practices, changing

customer dynamics and emerging economies?

Contact us: Star t the discussion www.frost.com

BEST PRACTICESAWARD ANALYSIS

2013 FROST & SULLIVAN AUSTRALIADATA COMMUNICATIONSSERVICE PROVIDEROF THE YEAR

![Suprema Presentation 100408.ppt [호환 모드]biometria.pl/files/Suprema_Presentation_100408.pdf9Awarded Frost & Sullivan’s ‘Biometric Company of the Year 2009’ 9RealScan-D](https://img.dokumen.tips/doc/110x75/5aafac7c7f8b9a3a038dad73/suprema-presentation-biometriaplfilessupremapresentation100408pdf9awarded.jpg)