Embed Size (px)

Citation preview

AUDITOR-CLIENT COMPATIBILITY AND AUDIT FIRM SELECTION

Stephen V. Brown *

Arizona State University

W. Robert Knechel

University of Florida

March 12, 2013

* Corresponding Author

Acknowledgements

We are grateful for feedback from Stephen Asare, Ryan Cerf, Praveen Pathak, and Jennifer Wu

Tucker. We would also like to thank workshop participants at Arizona State University, Florida

International University, Southern Methodist University, the University of Florida, the

University of Illinois at Urbana–Champaign, the University of Kentucky, the University of South

Carolina, and the University of Virginia for their feedback on portions of this paper.

AUDITOR-CLIENT COMPATIBILITY AND AUDIT FIRM SELECTION

Abstract

We examine the degree of compatibility between clients and their auditors to test whether

companies systematically prefer specific auditors based on this criterion. Using both financial

statements and narrative disclosures, we introduce two new measures of compatibility based on

how similar a client is to other clients of the same auditor. Our results strongly support the idea

that auditor-client compatibility can predict auditor-client alignment. When compatibility is

lower, clients are more likely to change auditors and are more likely to pick a replacement

auditor with relatively high auditor-client fit. Interquartile changes in compatibility increase the

probability of switching auditors by as much as 19 percent. Further, audit quality, as captured by

discretionary accruals, increases as compatibility increases. Finally, we simulate a mandatory

audit rotation regime in which clients base their choice of auditor on compatibility, finding

changes in market share of as much as 9.7% from a first-best baseline.

Key Words: Audit markets, Auditor switching

1

AUDITOR-CLIENT COMPATIBILITY AND AUDIT FIRM SELECTION

1. Introduction

The process by which a client selects an auditor can be complex and may be influenced

by a number of factors. Some of the factors that might affect the degree of compatibility

between an auditor and a client includes pricing, expertise, location, interpersonal associations

and the extent of agency problems in the client (Chaney et al. [1997], Johnson and Lys [1990],

Knechel et al. [2008]). Some of these attributes are obviously more relevant than others for

determining the overall quality of the resulting audit. A limited amount of research has

examined alignment between clients and types of auditors, based on factors such as the size of

the audit firm (Shu [2000], Landsman et al. [2009]) or degree of specialization. There is even

less research on the compatibility of specific auditors and a specific client. What literature exists

tends to be narrowly focused, such as research on the effects of a client hiring a former audit

partner (e.g., Lennox and Park [2007]). In general, clients may have preferences about the audit

process, its outcomes, and the nature of the relationship with their auditor. In this paper, we

define auditor-client compatibility as the ability of the auditor to satisfy these preferences, given

its own preferences and constraints.1 If client preferences vary from company to company, and

the ability of an auditor to meet a client’s needs varies from firm to firm, the degree of fit

between any two entities will also vary. In this paper, we develop a unique measure of auditor-

client compatibility for Big 4 firms and use it to evaluate the nature of long term client

relationships and changes in auditors.

The degree to which a client and a specific auditor are compatible is not observable.

However, to the extent a company has similar audit preferences as other companies, they would

1 In this paper, we use the term “fit” interchangeably with “compatibility.”

2

presumably choose a similar auditor, subject to various choice constraints (e.g., location). In this

study, we compare the similarity of a company to the current clients of a specific auditor to

generate a proxy for how well that company fits into the auditor’s client base. When a company

appears similar to other clients of the same auditor, ceteris paribus, we presume that the auditor

is likely to have developed expertise and cost advantages related to that “type” of client.

Therefore, we consider clients and auditors compatible when similarity to other clients of the

audit firm is high; and we consider low compatibility to occur when there is very low similarity

between the company and the audit firm’s existing clients.

We introduce two measures of inter-company similarity within an industry, one based on

a client’s financial statements and one based on their narrative disclosures. Each source of

information reveals variation in what managers are disclosing and how they choose to disclose it.

The financial statement similarity proxy relies on the Mahalanobis distance which is used in

cluster analysis to divide objects into groups based on a vector of numeric measures associated

with each object. The vector used in this paper incorporates financial statement components

known to be important in an audit context, i.e., financial proxies for audit complexity, audit risk

and auditor effort. The narrative disclosure similarity measure extends the similarity score

introduced in Brown and Tucker [2011] which was based on year-on-year changes in

Management’s Discussion and Analysis (MD&A). In this paper, we consider narrative

disclosures contained in the annual report including the company’s business description,

footnotes, and MD&A. Using each measure, we calculate the similarity of each client to other

clients of an audit firm in the same industry and year (the “reference group”).

In general, we find that clients tend to hire auditors where compatibility is better.

Depending on the proxy used, up to 59 percent of clients employ one of the two best-fitting

3

auditors among the Big 4. We also observe that the poorer the fit with an existing auditor, the

greater the probability the client will choose to switch to a new auditor. Further, when a client

switches auditors, the successor auditor is generally the one of the three remaining firms that has

the best fit. Extending the analysis of compatibility, we also examine the association between fit

and audit quality. We find that discretionary accruals are lower when the auditor-client

compatibility is better.

The primary contribution of this study is the introduction of two measures of how similar

a company is to a reference group of other companies clustered by audit firm and industry. The

financial statement measure (Mahalanobis distance) has been used in other contexts before, but

not in the accounting literature. While the financial statement similarity score is used in Brown

and Tucker [2011], we extend their pairwise, year-on-year, measure to allow for comparison of

entities within a specified group. Within the audit context, we provide insight into the manner in

which auditors and clients gravitate to each other. We add to the limited literature on auditor-

client fit by considering the suitability of a specific auditor for a specific client. Such insight can

be potentially useful in considering what might happen if mandatory audit firm rotation is

adopted by the PCAOB or European Union since forcing an auditor change could have negative

implications for the engagement if the client is currently served by a highly compatible auditor.

The rest of the paper proceeds as follows. The next section develops the hypotheses and

discusses prior literature. Following that section is the rationale and foundation for the similarity

measures, a demonstration of how they are calculated, and a discussion of observed trends. A

description of the design and results of the empirical tests follows, while the next section

examines these results for their sensitivity to changes in the similarity measures. The final

section contains the conclusion.

4

2. Hypotheses and Prior Literature

2.1. Auditor-Client Compatibility and Selection of Auditor

To make predictions about the choice of an auditor based on auditor-client compatibility

requires two conditions: (1) variation in client preferences regarding the audit and auditor and (2)

variation across auditors in their ability to satisfy those preferences. If auditors are all essentially

equivalent (no auditor variation), clients could randomly choose between them. On the other

hand, if auditors vary but clients all have the same preferences, then all the clients would prefer

the same auditor subject to capacity constraints. The audit literature has documented substantial

evidence of variation in client preferences and auditor capability. For example, a large,

multinational client is more likely to choose a Big N auditor (Chaney et al. [2004]), at least in

part because a smaller auditor does not have the resources and capability of auditing such a

company. Therefore, the US audit market has enough variation to suggest that auditor-client

compatibility is an issue worth examining (Numan and Willekens [2012]).

In a related vein, a large number of studies have also focused on industry specialization

as a differentiator of both demand and supply. Industry specialists are those auditors that have

invested significantly in expertise in auditing a particular industry, typically reflected by larger

market shares in an industry. Specialists are considered to deliver higher quality, e.g., they are

better at detecting errors (Owhoso et al. [2002]), and are associated with clients having higher

earnings response coefficients (Balsam et al. [2003], Gul et al. [2009]) and lower discretionary

accruals (Krishnan [2003]). They are also better at improving audit quality through knowledge

spillovers from non-audit services (Lim and Tan [2008]). Beyond variation in quality, there are

also cost structure differences among specialists. While most studies have found specialists

charge higher audit fees (Gramling and Stone [2001]), there is also the possibility of cost savings

5

through the leveraging of expertise (Cahan et al. [2008], Craswell et al. [1995], Willenborg

[2002]). Further, audits by industry specialists tend to be more efficient (Cairney and Young

[2006]). As a result, client preferences for certain levels of cost and quality will lead them to

choose an auditor with structural characteristics that best meet their needs.2

While most prior literature has focused on broad categories of auditors (e.g., Big 4 or

non-Big 4, specialist or non-specialist), a handful of studies have examined client selection at a

more micro level. For instance, Lennox and Park [2007] find that a company is more likely to

engage a particular auditor when a former employee of that auditor is on the management team

of the client. Research on client-auditor disagreements finds that a client is more likely to switch

auditors in the presence of more conservative accounting treatments, presumably in an effort to

find an auditor who is more amenable to the company’s preferences

(DeFond and Subramanyam [1998]; Krishnan [1994]). Bamber and Iyer [2007] find that auditors

who more strongly identify with the client will be more likely to allow the desired accounting

treatment. While this “opinion shopping” may sound disreputable, Dye [1991] shows that the

firm may simply be trying to better communicate its internal information to the market. The

broad conclusion is that interpersonal relationships and opinion shopping are just two ways a

client can find one auditor to be a more “compatible” than others.

In sum, given sufficient variation among clients and auditors, each is likely to choose a

counterparty that best matches its preferences and needs. While auditors can appear very similar

on the surface, there are likely to be subtle differences that make one auditor a better fit than

2 Investor preference can also play a role in the decision. Switches to larger auditors and specialist auditors are

associated with positive market reactions (Fried and Schiff [1981], Knechel et al. [2007], Nichols and Smith

[1983]).

6

another. Considering all a client’s needs and preferences, one specific auditor will likely provide

a higher net benefit to the client, leading to our first hypothesis:3

H1: The auditor used by a client will tend to be more compatible with the client

than other auditors in the market.

2.2. Auditor-Client Compatibility and Auditor Switching

Under H1, clients will prefer higher compatibility with their auditors. If a client has low

compatibility with their current auditor, it is likely they will eventually consider a change in

auditor to increase the level of fit in the audit. Johnson and Lys [1990] demonstrate companies

are more likely to switch auditors as the client’s operating, investing, and financing activities

change over time. They interpret the increased likelihood of switching as a rational, efficient

response to temporal changes in the company’s audit preferences. In effect, the auditor-client

compatibility that was utility-maximizing in the past has shifted such that another auditor may

now be a better fit. Shu [2000] examines auditor-client fit based on whether the client is with a

Big N auditor when an empirical model would predict a non-Big N auditor, or vice versa, finding

clients are more likely to change auditors when there is a mismatch between the two. We extend

the concept of auditor-client compatibility to examine whether mismatches with a specific

auditor are more likely to lead to auditor switches. Based on the degree of fit between the auditor

and client, we expect that poor compatibility is more likely to lead to an auditor switch, leading

to our second hypothesis:

H2: Clients having relatively poorer compatibility with their current auditor are

more likely to change auditors than those with high compatibility.

3 The decision is also subject to various constraints. For example, Coca-Cola is unlikely to choose the same auditor

as PepsiCo due to competitive concerns. We do not specifically address this issue in this paper, but the effect will

be to shift a client away from its apparent best fit, thus working against our findings. Further, we are unable to

incorporate the effect of specific partners who might service a client due to lack of partner data in the U.S.

7

Once a client has made the decision to change auditors,4 it will need to choose from the

other available auditors. If the company limits itself to Big 4 auditors, a maximum of three

auditors remain, subject to constraints arising from competitor auditor choices and current non-

audit service providers. If compatibility is low with the present auditor who is to be replaced

(H1), it then follows that a company will generally prefer a new auditor that has a better

compatibility from among the remaining options.5 This perspective leads to our third hypothesis:

H3: A client switching auditors will tend to choose a new auditor that has a

relatively higher degree of compatibility among the non-incumbent auditors.

2.3. Effect of Changes in Auditor-Client Compatibility

While it is relatively intuitive to grasp how auditor-client compatibility can influence the

decision to change or retain an auditor, it is less clear how increases in compatibility would

influence audit quality. In experimental studies, Hammersley [2006] shows “matched”

specialists—defined as those operating within their industry of expertise—are more likely to

process experimental cues regarding misstatements than mismatched specialists, while Low

[2004] shows that an industry-based mismatch affects audit planning and risk assessments. These

studies imply that audit quality will be higher when there is a better fit between the auditor and

client. Johnstone, Li, and Luo [2011] find that clients within the same supply chain—a measure

of relatedness, if not similarity—tend to have higher audit quality. On the other hand, a sizable

literature finds decreased audit quality when the auditor closely identifies with the client. In

essence, the possibility exists that auditor-client compatibility could become so good that an

auditor’s independence is compromised. Lennox [2005] shows that companies are more likely to

4 The decision to actually change auditors is complex and would take into considerations beyond that of fit. For

example, the transaction costs of an auditor change can be quite high so the degree of incompatibility would

probably have to be relatively large to justify an auditor change on a cost/benefit basis. 5 We do not predict that the new auditor will necessarily have a better fit than the previous auditor, primarily

because of the endogenous nature of compatibility —a client may appear to become a better fit for an auditor over

time as the auditor’s preferences modify the client’s observable financial statements and related disclosures.

8

receive a clean audit opinion if the auditor becomes affiliated with the client by hiring its former

auditors. Menon and Williams [2004] find clients employing former audit partners in executive

positions tend to report higher levels of discretionary accruals. Taken together, these potentially

offsetting effects lead to our fourth (nondirectional) hypothesis:

H4: Audit quality is associated with auditor-client compatibility.

3. Measurement of Auditor-Client Compatibility

When clients are similar to each other in terms of industry, operations, risks or

transactions, auditors have the opportunity to specialize in those companies for both reputational

and audit production reasons.6 While prior literature typically uses an “all-or-nothing” industry

membership test to organize clients into similar groups, we develop two continuous proxies for

the degree of compatibility between a company and an auditor’s existing client base. The first

proxy is based on cluster analysis and is derived by grouping similar entities together based on a

small set of numeric data (e.g., financial statement accounts). The second proxy is based on

information (text) retrieval which uses narrative-based documents as the underlying data.

The two proxies facilitate the development of measures of client-auditor similarity for

both financial statement and narrative textual disclosures. While the accounting systems and

underlying economics of multiple organizations are not separately observable, their joint effect is

presumed to be reflected in the financial statements and related narrative disclosures. The

narrative disclosures are especially flexible, giving management the opportunity to communicate

firm-specific information or to influence the market’s view of the company. In general, the

numeric proxy and the text-based proxy serve the same purpose, namely, they provide an

indication of how similar a specific client is to all of the other clients audited by a specific

6 Gramling and Stone [2001] summarize the industry specialization literature, which generally finds differences in

both quality and audit fees for industry specialists versus non-specialists.

9

accounting firm on a year and industry basis (i.e., each metric is specific to a firm-year-industry

nexus).

3.1. Financial Statement Similarity

Algorithms used in cluster analysis of numeric data include the Euclidean distance, city-

block distance, Chebychev distance, and Mahalanobis distance (Hair et al. [2006]). Of these, the

Mahalanobis distance-squared (D2) is particularly sophisticated in its ability to weight each

variable according to its individual scale, as well as account for covariances among the various

components. Further, the D2 statistic imposes few restrictions on the underlying variables

(Mahalanobis [1936]). After scaling and accounting for covariance of the variables, an

observation’s distance from the group is larger when the variables for the observation are jointly

more “unusual.” The D2 measure is the generally preferred algorithm in cluster analysis (Hair et

al. [2006])7 but there has been limited use of the D

2 measure in the accounting literature. Rege

[1984] uses it to test the effectiveness of a discriminant function in classifying data into likely

and unlikely takeover targets. If the distance between the two groups is significant then the

discriminant function is considered effective. Iyer [1998] employs the statistic in the context of

distinguishing audit firm alumni that can help the firm market its services. Guilding and

McManus [2002] use the measure to test for potentially influential outlying observations.

However, all these studies use the measure in a statistical context and do not examine the

7 Outside the accounting literature, D

2 has been used in management to compare the distance between countries

along multiple dimensions, including economic, financial, political, cultural, demographic, and geographic location

(Berry et al. [2010]). Climatologists have used the measure to look for boundaries between different regional

climates (Mimmack et al. [2001]). And chemists have used it for multivariate calibration, pattern recognition and

process control (De Maesschalck et al. [2000]).

10

properties of the distance itself.8 We use the D

2 measure in this paper to capture financial

statement similarity.

We use five financial variables that are generally believed to be important in an audit

context (Hay et al. [2006]) to construct our measure of financial similarity: (1) company size

measured as the log of total assets (SIZE) to capture the scope and potential importance of the

client, (2) the combination of inventory and receivables as a proxy for inherent risk (IRISK), (3)

total accruals as an indicator of audit quality (TACC, as calculated by DeFond and Subramanyam

[1998]), (4) cash and equivalents (CASH) as a proxy for liquidity, and (5) return on assets (ROA)

as a measure of profitability. All measures except SIZE are scaled by total assets.9 To calculate

the D2 distance for the sample, these five variables are gathered from Compustat for companies

having assets greater than $1 million and a consistent fiscal year end throughout the sample

period. We exclude utilities or financial services industries due to inherent differences in the

structure of their financial statements. The sample begins in 1997, when EDGAR data is first

widely available and ends in 2009. Former Arthur Andersen clients are included but only after

they have not engaged Andersen for at least one year to limit the potential confounding effect of

changes due to the collapse of Andersen.

A similarity metric can be calculated for a single company by comparing it to some well-

defined group of other companies called the reference group. In this paper, we define the

reference group to be all other clients of an accounting firm in the same industry and same

year.10

We use industries to define our reference groups because of potential systematic

8 The abnormal accrual model could be conceptualized as a distance measure. It empirically models the relationship

between total accruals and various explanatory variables to attempt detection of accrual levels that are unusual-

looking relative to peer companies. 9 Other potential inputs, various permutations of those inputs, and alternative measurement approaches are described

in the robustness section. 10

Hogan and Jeter [1999] document the increasing importance of auditor restructuring along industry lines at the

national level to take better advantage of internal teams of experts. While client compatibility may vary at the office

11

differences and a lack of comparability in the structure of financial statements and narrative

disclosures across different industries. We exclude any reference groups that do not have at least

five observations because the similarity score is unlikely to be reliable in small groups. Further,

possible reference groups are rarely large enough for non-Big 4 auditors so we explicitly limit

the sample to Big 4 clients. Finally, a company is omitted from the reference group in the year

that they switch auditors.

Each observation in the sample consists of a vector of five financial statement variables

(n=5), xT = (x1, x2, …, xn) = (SIZE, IRISK, TACC, CASH, ROA). The mean of these same

financial statements variables for the entire auditor-industry-year is contained in the vector, μT =

(μ1, μ2, …, μn). Finally, the group has a covariance matrix, Σ, for the five inputs. The

Mahalanobis distance-squared is then calculated as:11

( ) ( )

The (x – μ) portion of the measure is calculated by subtracting the mean values of the five

financial variables of the reference group (i.e., auditor-industry-year combination) from the

values for the company-year being analyzed. The Σ covariance matrix is calculated at the

industry-year level to account for different scales and covariances across industries and over time

that are unlikely to vary much across auditors.12

Because D2 is a measure of dissimilarity, it is

converted to a similarity measure by calculating its inverse. Finally, the natural log

level, there are few offices with enough clients to calculate similarity measures within an industry. Calculating the

scores at the office-industry level would lead to a 63% reduction in sample size (and a 30% reduction if calculated at

the office-sector level). 11

The Euclidian distance between observations is a special case of the Mahalanobis distance. If the covariance

matrix (Σ) is the identity matrix, the square root of D2 simplifies to the familiar [(x-μ)

T(x-μ)]

½, which is the

Pythagorean theorem if the vector has length two. 12

Multicollinearity is not problematic as it would be in a regression. However, as the variables approach nearly

perfect multicollinearity, the covariance matrix will not be invertible, which can be a concern when using a small

vector of variables in a small industry. While unusual in the sample, we exclude industry-years that do not have at

least ten company-year observations (twice the number of variables). This restriction is almost always met given the

earlier restriction of at least five observations with an auditor-industry-year.

12

transformation reduces skewness and outliers, yielding our measure of financial statement

similarity:

(

)

3.2. Narrative Disclosure Similarity

The information retrieval literature has developed numerous methods for measuring the

similarity of two documents, often in the context of matching a user’s Internet search query to

the closest applicable web pages (Singhal [2001]).13

A common method for analyzing text

documents is the Vector Space Model (VSM) from the document retrieval literature. The VSM

maps a document into a numeric vector (Salton et al. [1975]). There are numerous ways to

calculate the similarity of document vectors. The most common approach is to calculate the

cosine of the angle between any two vectors (Singhal [2001]), an approach used in the

accounting literature by Brown and Tucker [2011]. They use the VSM cosine statistic to measure

year-on-year dissimilarities in MD&A as a proxy for changes in narrative disclosure. Because

Brown and Tucker [2011] were interested in the differences between just two documents at a

time, they only calculate pairwise similarity scores. In contrast, for this paper, we aggregate these

pairwise scores to get a measure of the similarity between one company’s narrative disclosure

and the disclosures issued by a reference group of clients within the same auditor-industry-year.

13

In theory, the D2 measure can be used in a document context, however, practical considerations limit its

usefulness in such a setting. When mapping a list of words from narrative text into variable vectors, the high

dimensionality makes calculation of the D2 measure impractical. The problem is that the size of the covariance

matrix depends on the unique words used in the documents being analyzed rather than the number of documents.

For example, a covariance matrix using the 98,519 unique words for the MD&A in the sample would contain 9.7

billion elements. This matrix would need to be inverted in the computational process, making the approach

obviously impractical.

13

The VSM-based similarity score for narrative disclosure similarity is calculated based on

three different types of text disclosure in a company’s annual 10-K.14

We select annual report

disclosures that are common to virtually all 10-K’s, reviewed by the auditor, not voluntary, and

considered important by the capital markets and regulators. It is preferable to use more than one

disclosure item because there is considerable variation in the characteristics of different

disclosures in terms of subject matter, time-horizon, and audit requirements. As a result, we

examine the company’s business description,15

management discussion and analysis (MD&A),16

and financial footnotes17

because they are usually the longest disclosure items in the 10-K.

Excluding exhibits, there are an average of 6,338 words in the business description, 7,054 in the

MD&A, and 8,623 in the footnotes (see Table B-1), comprising 17, 18, and 21 percent,

respectively, of the length of the typical 10-K.18

The data for the narrative disclosure score is taken from 10-K’s filed electronically via

the SEC’s EDGAR system for fiscal years 1997 through 2009 for the clients of Big 4 audit firms

14

While it is not feasible to calculate the D2 statistic for documents, it is feasible to calculate the VSM similarity for

financial statements. Using such an approach, Jaffe [1986] uses vectors of different categories of patent applications

to examine the overlap of R&D spending within industries. However, the D2 statistic is superior for numeric data

because VSM does not account for variances and covariances of the variable components, which reduces its

statistical power. 15

Item 101 of Regulation S-K requires the 10-K item 1 contain a detailed narrative description of the business,

including industrial and geographic segments, principal products and services, R&D spending, and competitive

conditions. This is the disclosure that is likely to have the least formal structure but may not change much over

time. 16

Item 303(a) requires that the MD&A contain a discussion of liquidity, capital resources, results of operations, off-

balance sheet arrangements, and contractual obligations. The MD&A is intended to be an interpretation of past and

future operations “through the eyes of management” (SEC [2003]). Given certain conditions, any forward-looking

statements receive Safe Harbor protection (Item 303(c) of Regulation S-K). This is the only disclosure that is

specifically forward-looking to some extent. 17

Although there is some topical overlap with the other two disclosures, footnote content is the only disclosure

specifically determined by GAAP. This is the only disclosure that is formally audited while the other disclosures are

reviewed by the auditor (AU Sections 550; 551) 18

The footnotes and MD&A are particularly important to stakeholders, given the large number of accounting

standards requiring or encouraging specific footnote disclosures and the relatively frequent guidance by the SEC on

MD&A (e.g., SEC [1987], [1989], [2003]). Prior studies have demonstrated the usefulness of footnotes (e.g.,

Shevlin [1991], Amir [1993], Wahlen [1994], Riedl and Srinivasan [2010]). Other research has shown some of the

potential information contained in MD&A (e.g., Feldman et al. [2010], Feng Li [2010], Sun [2010]). Of the three

narrative disclosures, the business description is relatively unexplored except in studies of the full 10-K as a single

document (e.g., Li [2008]).

14

having at least five other observations available for comparison within the same auditor-industry-

year reference group. Appendix A describes the selection and extraction process, which yields

33,355 business description, 31,280 MD&A, and 14,439 footnote observations. Treating the

three narrative disclosure items of the annual report as separate data sets, the similarity score for

each is calculated using an extension of the approach in Brown and Tucker [2011] that allows for

a comparison of a company to its peers (reference group). The process, summarized in Appendix

B, produces three variables—SIMBUS, SIMMD&A, and SIMNOTES—that proxy for the degree of

similarity between one client and all other clients in the same auditor-industry-year. Higher

similarity scores correspond to greater auditor-client compatibility.

3.3. Patterns in Client Similarity

Panel A of Table 1 contains descriptive statistics for the financial statement and narrative

disclosure similarity measures. The sample size is largest for SIMFS (57,035), smallest for

SIMNOTES (14,439), and similar for SIMBUS (33,355) and SIMMDA (31,280). SIMFS is always

negative because of the log transformation. Higher similarity scores indicate greater similarity in

relation to the reference group.19

The narrative disclosure similarities (SIMBUS, SIMMD&A, and

SIMNOTES) are approximately centered around zero.20

Similarity scores are significantly higher

for companies in the top quartile of size than for those in the bottom quartile (untabulated),

indicating that bigger clients tend to be at the “core” of the auditor’s portfolio in terms of their

similarity.

<<<<< Insert Table 1 about here >>>>>

19

The average auditor-industry-year reference group size is 38 clients for financial statements, 23 for the business

description, 22 for MD&A, and 12 for the footnotes. 20

As noted in Appendix B, we maximize the sample size for making the length adjustment by using all available

observations, including non-Big 4 auditors. After restricting the study sample to Big 4 clients, the mean is slightly

above zero.

15

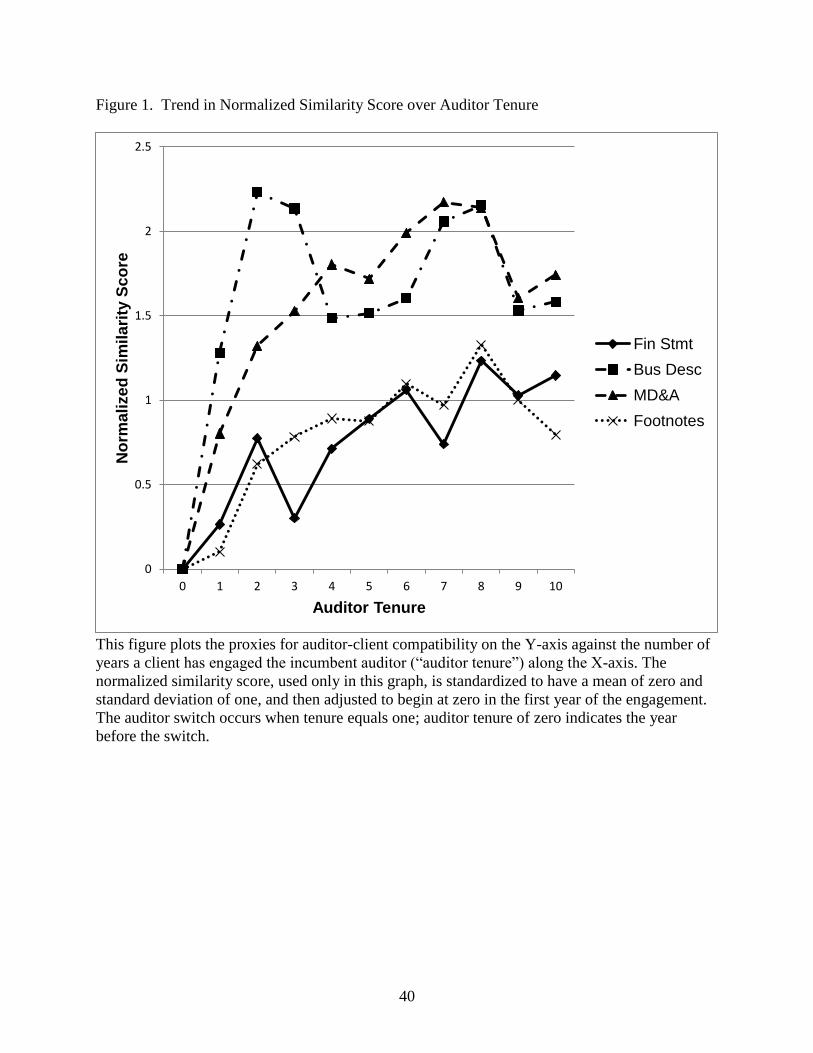

The four similarity scores are not directly comparable to one another because of

variations in how they are calculated (e.g., a score of 0.20 for MD&A is not necessarily larger

than a score of 0.15 for footnotes). To compare across measures, the scores are standardized to

have a mean of zero and standard deviation of one. Figure 1 plots the similarity scores against

auditor tenure—the number of years with the current auditor. A tenure of zero corresponds to the

year prior to the current auditor obtaining the client, while a value of one indicates the first year

of a successor auditor’s tenure (i.e., the first year after an auditor switch). For visual

comparability, all scores are adjusted to begin at zero when auditor tenure is zero. The graph

only presents tenure up to year ten, after which the decreasing number of observations leads to

heightened volatility in the scores. All similarity measures increase over the length of the

auditor-client relationship, indicating that auditor-client compatibility improves over time.

Auditors might find this trend beneficial to the extent that it improves the quality or reduces the

effort involved in the audit engagement. Likewise, clients might benefit from adopting best

practices arising from the auditor’s expertise developed in similar client engagements.

<<<<< Insert Figure 1 about here >>>>>

The business description experiences a rapid increase in similarity during the first two

years of the engagement, after which point the similarity becomes more stable. MD&A similarity

also increases quickly in the first two years and then rises more slowly until approximately year

seven. The trends in financial statement and footnote similarities are highly correlated, which is

not surprising since those disclosures are intended to be closely aligned by regulation. Both of

these measures increase gradually over time with less of a sudden jump in the early years. To

test for the statistical significance of these trends, we compare the similarity scores for short

tenure (less than four years) and long tenure (nine or more years) engagements. In all cases, the

16

similarity scores are significantly higher for longer-tenure clients than for shorter ones. We

perform a related test using year-on-year changes in similarity and find that the annual changes

for long-tenure clients are not as large as the changes seen in newer clients.21

These patterns all

demonstrate that auditor-client compatibility is not a static component of the relationship, but is

partially a function of auditor tenure.

3.4. Validation of Similarity Measures

Table 2 reports the Pearson pairwise correlations among the similarity measures. The

reported correlations are limited to observations with scores available for all four disclosures

(narrative and financial), although the unrestricted correlations are similar. The four similarity

scores are all positively correlated with one another, indicating they measure related constructs.

The correlations are higher among the three narrative disclosures (ranging from 0.61 to 0.72)

than they are with the financial statements (from 0.05 to 0.11).

<<<<< Insert Table 2 about here >>>>>

As a means of validation, the table also contains the correlations between the similarity

measures and various proxies for client differences. For each variable used to produce SIMFS, we

calculate the client’s absolute difference from the mean for the reference group (auditor-client-

year), i.e., |SIZEDIFF|, |IRISKDIFF|, |TACCDIFF|, |CASHDIFF|, and |ROADIFF|.22

We expect

the correlation with the similarity scores to be negative in all cases. The correlations with SIMFS,

range from -0.25 to -0.42 and all are significant. More importantly, the significant correlations

between these difference variables and the narrative disclosure scores are all negative, indicating

the proper functioning of the narrative scores even though they did not explicitly include any

21

The t-statistics for the difference in means between long and short tenure clients of the financial statements,

business description, MD&A, and footnotes are: 24.10, 4.61, 5.13, and 8.72, respectively. The corresponding t-

statistics for the difference in annual changes are: 6.55, 2.94, 2.29, and 1.63. 22

These difference variables should be negatively correlated with SIMFS by design, but these correlations document

the SIMFS measure is working as expected. Performing a series of univariate correlation tests is also substantially

different from the joint difference measure produced using the D2 technique.

17

financial statement variables. Of the difference variables, |ROADIFF| and |TACCDIFF| have the

highest negative correlation with SIMFS, so client profitability and accruals could be important

determinants of financial statement similarity. On the other hand, |IRISKDIFF| has the most

negative correlation with the three narrative scores.23

We also consider the absolute value of unexpected discretionary accruals as a measure of

client differences. Following DeFond and Jiambalvo [1994], accruals are estimated using a

cross-sectional modified Jones model run within SIC 2-digit industries. The residual from this

model is DACC, the unexpected discretionary accruals. As expected, the similarity scores are

negatively correlated with the absolute value of DACC. Finally, we examine the stability of the

similarity scores since it would be expected that auditor-client compatibility will not change

dramatically over short time periods due to the relative stability in financial statements, related

disclosures, and client portfolios from year to year. In untabulated analysis, we find that the

autocorrelation coefficients for SIMFS (0.55), SIMBUS (0.93), SIMMD&A (0.92), and SIMNOTES

(0.92) are high, demonstrating a high degree of time-series stability in all four measures.

4. Analysis of Auditor-Client Alignment

4.1. Sample

For the hypotheses tests, data is collected from Compustat for each observation with at

least one similarity score available. The variables used in our testing are summarized in Table 1

(Panel B). The earliest data come from 1997, corresponding with the earliest availability of the

narrative disclosure data, and end in 2009. Auditor tenure is calculated based on the current

auditor information in Compustat beginning in 1974.

23

This is consistent with the importance of the numerous risk-related disclosures in annual report items (e.g., Kravet

and Muslu [2010], Campbell et al. [2010]).

18

4.2. Auditor-Client Alignment

If clients and auditors randomly choose to enter into an audit engagement without regard

to auditor-client alignment, one would expect a relatively equal distribution of clients across

firms when sorting on the compatibility score (i.e., approximately a 25% market share to each

firm after omitting clients of non-Big 4 firms). According to the first hypothesis, a client is more

likely to use an auditor that also has other clients similar to itself, and are least likely to use an

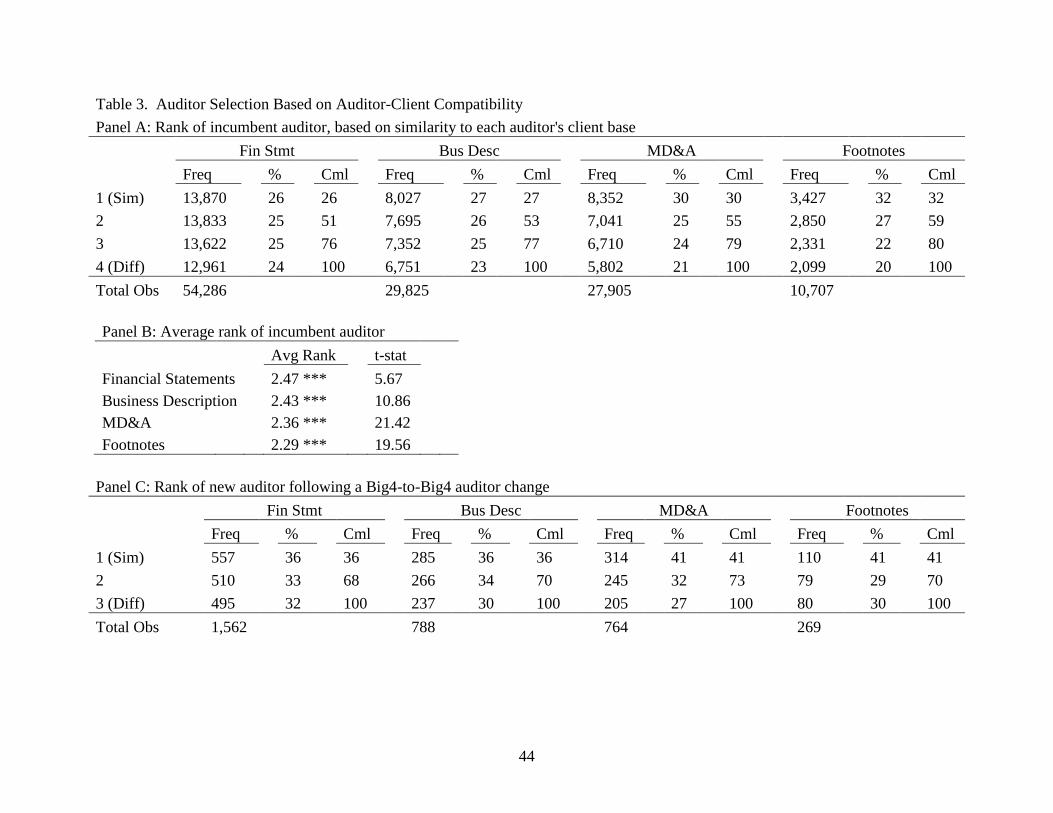

auditor having a less similar set of clients. Table 3, Panel A summarizes auditor-client alignment

using each of the similarity scores.24

In each case, the probability of using a specific auditor

monotonically declines as auditor-client alignment decreases. For financial statements, slightly

more clients use an auditor having the best fit (26%) than with the worst fit (24%). When

examining the business description, 27% of clients use the auditor with which they are best

aligned, while only 23% use the auditor with which they are least aligned. The MD&A pattern is

even stronger, with 30% of clients using the most aligned auditor and just 21% using the least

aligned auditor. The strongest pattern occurs based on similarity within the footnotes, where 32%

of clients use the most similar auditor and only 20% use the least similar auditor. In

combination, these results suggest that clients are indeed associated with highly compatible

auditors.

<<<<< Insert Table 3 about here >>>>>

To evaluate the statistical significance of these patterns, we assign a rank between one

and four, where one corresponds to the most compatible auditor and four to the least compatible.

The average auditor-client alignment rank is then compared to the expected rank under the null

24

We do not expect to see extremely large differences from an equal distribution for existing client-auditor

combinations because of the costs of auditor switching and the duration of auditor tenure in the sample. Many

factors can influence auditor-client alignment when the relationship is stable, i.e., fit as measured by our

compatibility score is just one dimension to alignment. As a result, we feel that the best test of auditor-client

compatibility relates to auditor switches (to be discussed) since that is the point in time when one alignment would

be most salient to a client and we would expect the best match between an auditor and a client.

19

of a random distribution (i.e., the average rank with four options is 2.5). Comparing the average

rank of each score to the null provides a test of the tendency of clients to be associated with a

more closely aligned auditor than with a less aligned one, without requiring that they be with the

most similar auditor. Table 3, Panel B shows the average rank of the incumbent auditor based on

auditor-client alignment. The average ranks are 2.47 (t = 5.67) when using the financial

statements, 2.43 (t = 10.86) for the business description, 2.36 (t = 21.42) for MD&A, and 2.29 (t

= 19.56) for the footnotes, all of which are significantly less than 2.5. Based on the content of

their disclosures, the overall conclusion is that clients are significantly more likely to be

associated with more compatible auditors.

4.3. Likelihood of Auditor Change

In a stable client-auditor relationship, we see that clients are more likely to be aligned

with compatible auditors (H1). However, such alignment at any point in time may reflect legacy

costs and inertia as much as it does a desire for “fit.” Further, the simple descriptive analysis in

the previous section does not address whether this pattern occurs because clients and auditors

jointly choose an engagement that already has a higher alignment, or whether clients merely

become more similar to their auditor over time as a side effect of the audit process. As

previously noted, a client is likely to search out the most compatible auditor when going through

a change in auditors (H2). Therefore, this section presents several analyses surrounding auditor

switches. First, we develop a model of auditor change based on variables from the existing

literature on auditor switching, augmented with the auditor-client similarity measures. We use

the following logit model to analyze auditor switches based on a company’s attributes in the year

prior to the switch (firm and year subscripts are suppressed):

20

(1)

The dependent variable, SWITCH, is an indicator set to one if the client will change

auditors in the subsequent year; all other variables are measured in the current year. Because

larger firms tend to change auditors less frequently, the natural log of total assets (SIZE) in the

year before the switch is included in the model. Following Landsman et al. [2009], the model

includes a variety of controls for audit and financial risk. For audit risk, the model includes

growth, inherent risk, the nature of the audit opinion, and auditor tenure. GROWTH in assets is

associated with greater litigation risk for the auditor. IRISK is defined as receivables plus

inventories, scaled by total assets. MODOPIN is a dummy set to one for anything other than an

unqualified, clean opinion. The audit risk variables are expected to be positively associated with

the probability of an auditor switch. TENURE10 is the number of years the client has engaged its

current auditor, with a maximum value of 10 years, and is expected to be negatively associated

with auditor changes. Financial risk is proxied by return on assets (ROA) and a dummy variable

when a company incurs a loss (LOSS). Both of these variables are expected to be positively

associated with auditor switches. Higher cash and equivalents scaled by total assets (CASH)

proxies for the financial risk for a client. 25

Because M&A activity can lead to an increased

likelihood of changing auditors when the previously separate entities engaged different auditors,

a dummy variable is included to indicate that a company has engaged in acquisition activity that

exceeds ten percent of total assets (ACQUIS). 26

25

All continuous control variables are winsorzed at the 1st and 99

th percentiles and and log-transformed.

26 We omit the leverage variable in Landsman et al. [2009] since it is not significant in either their study or this one.

Absolute discretionary accruals is omitted because it also proxies for the relative “unusualness” of the client relative

to the industry, which is the construct of interest in this paper. Including it does not change the results of the

analyses.

21

The correlations among these variables and the similarity scores are presented in Panel A

of Table 4. The correlations with the similarity scores imply larger (SIZE), more profitable

(ROA), and less risky companies (IRISK) are more likely to have a better fit with their auditor.

This suggests that smaller, less profitable, and more risky companies may be constrained in their

auditor selection (i.e., may not be able to engage their first-best choice) if that auditor declines

the engagement due to concerns about audit or financial risk.

<<<<< Insert Table 4 about here >>>>>

Model (1) is augmented with each of the proxies for auditor-client fit introduced

separately. The results are presented in Table 4, Panel B. The controls are generally consistent

with prior literature. All similarity measures except for SIMBUS are negatively related to auditor

switches. SIMFS (t = 4.72), SIMMD&A (t = 3.40) and SIMNOTES (t = 3.78) have negative

coefficients, supporting H2 that clients having a poorer auditor fit are more likely to switch to a

new auditor.27

Holding all the other variables at their means, an interquartile decrease in

financial statement similarity is associated with a 9.2 percent higher probability of switching.

The increase for MD&A is 11.8 percent and for footnotes is 18.9 percent. This result explains

one of the mechanisms through which the patterns in Table 3 may occur: clients tend to utilize a

better-fitting auditor because they are more likely to change auditors when the fit is poor.

4.4. Auditor Choice Conditional on Decision to Switch Auditors

Hypothesis H3 predicts that a company that hires a new auditor will select the firm that is

most compatible from the set of firms available (i.e., excluding the incumbent that has been

replaced). Since the company has already decided the net benefits of a change outweigh the

27

As an alternative composite test, all similarity scores are converted to quintile rankings and then summed across

the four similarity scores (result ranges from 4 (maximum similarity) to 16 (minimum similarity). We then use this

variable in the auditor switch model. The coefficient is negative as expected (p<.0001).

22

switching costs—possibly due to fee or service considerations rather than compatibility—it is

expected that the new auditor, on average, will be the most compatible of the non-incumbent

firms. Table 3, Panel C, summarizes the average compatibility rank of the new auditor (with 1

being most similar, 3 least similar). Consistent with the earlier results for incumbent auditors, we

see that the likelihood that a firm is selected is a strictly decreasing function of the similarity

scores in all cases. Further, these clients generally choose a new auditor with better auditor-

client fit. To test the statistical significance of this pattern, the average rank of the new auditor is

compared to what the average rank would be if a new auditor was randomly selected from the

remaining 3 firms (i.e., 2.0).28

In Table 3, Panel D, the average rank of the financial statements is

1.96 (t = 1.91; p-value = 0.028), the business description is 1.94 (t = 2.11; p-value = 0.018), the

MD&A is 1.86 (t = 4.85; p-value < 0.001), and the footnotes is 1.89 (t = 2.19; p-value = 0.015).

All four are significantly different from the rank expected for random selection. Thus, all

similarity measures imply clients are significantly more likely to choose a better-fitting auditor

when switching among the Big 4.

Taken together, these tests provide insight into whether the commonly observed pattern is

due to (1) a decision made by clients to choose an auditor with better fit or (2) clients gradually

becoming more aligned with their auditors as the auditors influence the clients’ disclosures over

time. The results in Table 3 support the argument that auditor-client compatibility is partially the

result of the auditor selection process, i.e., when a company decides to change its auditor, it tends

to gravitate to one that is relatively compatible. The pattern in Figure 1 then suggests that the

compatibility continues to grow over the tenure of the auditor. Presumably this evolution

28

A random choice among auditors would imply a rank of (1 + 2 + 3)/3 = 2.

23

continues absent some kind of exogenous shock that would cause companies to change auditors

again.

4.5. Similarity Based on the Entire 10-K

In the primary analysis we use four different similarity scores which are defined in a

rather narrow manner in order to maximize the comparability across different companies within

an industry. Mathematically, it is also possible to run our analysis on the entire 10-K. We do not

include this as our primary analysis because of the likelihood that variations in presentation of so

much different information may disguise the similarity that occurs in specific disclosure items.

The full 10-K narrative yields a similarity score that is highly correlated with the disaggregated

scores, ranging from 0.73 to 0.81. In untabulated analysis, we find results that are fully consistent

with our primary analyses. Specifically, we continue to find companies tend to be associated

with the auditor that is most compatible, with an average rank of 2.34 (t = 25.92, p-value <

0.001). Further, they are significantly more likely to switch auditors when compatibility is low (z

= 3.48, p-value < 0.001). After switching auditors, they also tend to choose a new auditor with

better compatibility (rank = 1.9, t = 3.57, p-value < 0.001).

4.6. Similarity and Discretionary accruals

Higher auditor-client compatibility may be beneficial for a number of reasons including

audit efficiency and auditor-client relationships. However, it is possible that excessive

compatibility could lead to a loss of professional skepticism that might undermine audit quality.

To test whether audit quality is affected by auditor-client fit (H4), we compare the quality of

engagements with better fit to those with poorer fit using discretionary accruals. Signed

discretionary accruals are often used as a proxy for audit quality, with income-decreasing

accruals representing conservatism and income-increasing accruals corresponding to aggressive

accounting practices. The measure of discretionary accruals (DACC) used in this paper follows

24

DeFond and Subramanyam [1998]. Based on univariate correlations (untabulated), SIMFS is the

only similarity score that has a positive correlation with DACC (0.10). The other similarity

scores are uncorrelated. Considering the differences in discretionary accruals between clients

having the best auditor-client fit (i.e., a rank of one in Table 3) and those having the worst fit,

DACC is lower for better-fitting auditors based on the business description (t = 1.50; p-value =

0.067) and MD&A (t = 1.73; p-value = 0.042). Discretionary accruals are also lower for the

financial statement and footnote samples but the results are not statistically significant. Finally,

looking at changes in accruals in the first year after an auditor switch, we observe a significantly

larger decrease in discretionary accruals for better-fitting auditors than for less compatible ones.

However, this pattern only occurs for the financial statement measure; the other measures are

insignificant. On balance, the analysis of accruals provides weak evidence in support of H4 and

suggests that increased compatibility between an auditor and client improves—or does not

harm—audit quality.

5. Supplemental and Robustness Analyses

5.1. Audit Market Equilibrium under Mandatory Audit Firm Rotation

With a few assumptions, we can use the compatibility scores to estimate what would

happen if the PCAOB were to introduce a system of mandatory audit firm rotation for registrants

as it has proposed (PCAOB [2011]). Table 5 provides estimates of market share under such a

system of rotation assuming that clients were forced to change auditors. Panel A indicates the

market share of each audit firm based on the number of clients, assuming that each client would

change to its most compatible auditor with zero switching costs. Panel C does the same thing,

but based on market share of audit revenues. These two panels serve as a first-best baseline as

they represent clients’ choices in a fictionalized world of no switching costs under a non-

mandatory regime in which clients solely consider auditor-client compatibility in their decision.

25

Panel B and D then predict what the respective market shares would be if clients are

forced to move from their current auditor to a new auditor having the highest possible

compatibility out of the remaining three auditors. This prediction simulates a mandatory rotation

regime in which clients make their choices primarily based on auditor-client compatibility. The

“Dev” columns of Panels B and D indicate the deviation in market shares, as a percentage of the

first-best market share, for each firm. The final column provides the market share and deviation

averaged across the four compatibility measures. We see that Deloitte and KPMG would

increase their number of clients by 4.4% and 2.4%, respectively, while E&Y and PwC would

lose 5.6% and 1.2%, respectively. The gains and losses are more extreme when measured by

revenue, although the directional conclusions are identical. Deloitte and KPMG would see a

8.4% and 9.7% increase in audit fees, respectively, but E&Y and PwC would lose 3.6% and

9.6%, respectively. Note, these are the effects of the first time mandatory changes—firms would

have the ability to return to an earlier audit firm in the future.

<<<<< Insert Table 5 about here >>>>>

5.2. Alternative Inputs for Financial Statement Similarity

To test the robustness of the financial statement similarity score used in this paper, we

vary the inputs in the calculation of SIMFS. First, because small- and mid-sized companies are

empirically more frequent than large companies, including SIZE in the analysis could cause the

similarity measure to proxy for client size rather than similarity more generally. To reflect this,

we re-run our analysis leaving SIZE out of the model and leaving the four other inputs in place.

Second, we include return volatility as an additional input in the model to capture risk from a

market perspective. Finally, we include the number of non-missing/non-zero financial statement

variables in Compustat as a measure of audit effort and complexity, since additional financial

26

statement items are likely to increase the scope and intricacy of the audit.29

None of these

independent changes makes a difference in our results.

5.3. Auditor Switching Involving non-Big 4 Firms

Conditional on switching auditors, Hypothesis 3 predicts clients will prefer a better-

fitting auditor. The primary test only examined switches between Big 4 auditors and explicitly

excludes clients switching from or to a non-Big 4 auditor. In a separate analysis, we consider

clients switching from a non-Big N auditor to a Big 4 auditor (i.e., “upward switches”), ignoring

the forced changes by Arthur Andersen clients. Because these clients have four auditors from

which to choose, the null would predict an average rank of 2.5. Only the footnote sample mean

of 2.25 (t = 2.26; p-value = 0.01) implies upward switchers are more likely to choose a better-

fitting auditor. None of the other measures are significant. However, in all cases, the magnitudes

of the average auditor ranks are similar to those observed in Panel C of Table 3. This result

suggests that the decision to move to a Big 4 auditor is driven by factors other than compatibility.

It may also suggest that there are some constraints on an upward-switcher’s ability to identify or

choose the best-fitting auditor.30

5.4. Auditor Switching Involving ex-Andersen Clients

Another form of switching observed during the time period of the sample were former

Arthur Andersen clients switching to new auditors after the firm’s collapse. The patterns in this

subsample seem the most random of the subsets. In this case, none of the similarity scores are

statistically significant at conventional levels for the new auditor (SIMMDA has a p-value of 0.09).

Because the sample sizes are not dramatically smaller than those in Table 3, the former Andersen

29

The number of reporting segments is frequently used to proxy for audit complexity but is unavailable for many

companies in Compustat. Counting the number of variables serves as a broadly available alternative.

30 Alternatively, the similar magnitudes of the ranks between this test and Table 3, Panel C imply the insignificant

result could be driven by the small sample size available for this test.

27

clients appear unlikely to have chosen a new auditor with greater compatibility. This result may

be driven by the capacity constraints induced by the rapid auditor turnover affecting so many

large clients at once. While the sample sizes are small (ranging from 26 to 132 depending on the

similarity score), we also look at ex-Andersen clients that switched a second time in the sample

period. For the second switches, we compare the similarity rank of the new auditor to 2

(reflecting a choice from 3 non-incumbents). We find that the rank of the new auditor is less

than 2 for all four similarity scores but only significant for the business description (p=.017).

The lack of statistical significance for the other three similarity scores may be due to a lack of

power.

5.5. Accounting System Comparability

In a related line of research, De Franco et al. [2011] examine the comparability of

accounting systems between companies. However, their metric is not based on financial

disclosures or narrative text. For each company in their sample, they regress 16 quarters of

earnings (considered to be an accounting system output) on returns (a measure of the net effect

of economic events) to estimate the “accounting function” for that company. To determine the

similarity between any two observations, they use the fitted accounting function to predict

earnings for each observation using actual returns. They interpret the difference between the two

predicted earnings values as a measure of the difference in accounting systems. Aggregating

these differences for all pairs of observations gives a measure of accounting system similarity for

each company within an industry-year (COMPACCT-IND). They construct an alternative

measure using only earnings by regressing 16 quarters of earnings of one company on the

earnings of another. Aggregating the R2 from each regression also gives a proxy for accounting

system similarity (COMPACCT-R2). As a sensitivity test for the D2 metric used in this paper, we

28

calculate these measures as described in more detail in De Franco et al. [2011] as an alternative

to SIMFS.

The COMPACCT-IND variable is uncorrelated with the four primary similarity scores

used in this study, nor is it correlated with most of the alternative proxies for client differences

(|SIZEDIFF|, |IRISKDIFF|, |TACCDIFF|, |CASHDIFF|, and DACC), with the exception of a -

0.06 correlation with |ROADIFF|. In contrast, COMPACCT-R2 has correlations of 0.07, 0.08,

and 0.04 with SIMBUS, SIMMD&A and SIMNOTES, respectively. As an alternative test of auditor

changes, we separately include the two accounting comparability measures in the model for

auditor switches. They are both negative but insignificant.

6. Conclusion

We find strong evidence that auditor-client compatibility helps predict which auditor a

client will choose to engage. When the fit is poorer, clients are more likely to change auditors

and choose a compatible auditor from among their remaining options. An interquartile shift in

similarity with the current auditor’s client base can change the probability of switching auditors

by as much as 19 percent. Descriptively, auditor-client fit is a concave function of auditor tenure;

compatibility with the incumbent auditor increases over time, but at a decreasing rate. Based on

discretionary accruals, overall audit quality increases as auditor-client compatibility increases.

The similarity measures we introduce have additional applications within accounting

research. For example, the measures could serve as an alternative measure of industry

specialization based on the degree of overlap within an auditor’s client base. Beyond auditing,

the measures can be used to isolate firm-specific disclosures from disclosures that are similar

among a set of companies. Econometrically, it is possible to implement a matched-pair design

29

based on having similar narrative disclosures.31

Another possibility is studying how disclosures

propagate throughout an industry by monitoring when a specific disclosure becomes similar to

other existing disclosures of peer firms. The similarity measures have potential usefulness in any

context in which the relationships among a set of companies’ disclosures is of interest.

Our findings have several implications for both regulators and researchers. With the

PCAOB continuing to consider requiring mandatory auditor rotation (PCAOB [2011]), requiring

an auditor change could force auditors and clients into less compatible engagements, which will

potentially lead to changes in audit quality. For researchers, prior literature has directly examined

the effect of auditor type, such as auditor size and specialization, implicitly assuming auditors are

indistinguishable within these groups (i.e., all BigN auditors are essentially the same). Our

findings indicate more heterogeneity among a particular category of auditors than perhaps

previously thought. Therefore, depending on the nature of the research question, it may be

worthwhile to consider the differential effects of specific audit firms rather than examining them

in broad categories.

31

The Mahalanobis measure is already used for this purpose. For example, the psmatch2 Stata library.

30

APPENDIX A

EXTRACTION OF ANNUAL REPORT ITEMS

To gather the business description, MD&A, and footnotes sample, we begin by

downloading all 10-K’s and 10-K405’s available on the SEC’s EDGAR system that meet the

following requirements: (1) fiscal years between 1997 and 2009, (2) assets greater than $1

million, (3) no change in fiscal year-end, (4) not in the utilities or financial services industries,

and (5) engaging a Big4 auditor. As described in Table A1, this initial screen leaves 41,782

annual reports. We next screen out any unusually short annual reports since these typically

belong to holding companies, firms that are winding down, and other atypical observations. We

use a cutoff of 50,000 characters for this purpose (approximately the 4th

percentile of 10-K

length). This filters out most of the unwanted observations without losing a substantial number

of reports. We use characters instead of words because the tables and numbers contained in the

report make it difficult to split the document into “words” at this point in the process. This leaves

40,149 annual reports.

Next, we strip all HTML formatting and data tables as in Li ([2008], [2010]) and split

each annual report into its component items, keeping only the business description, MD&A, and

footnotes (the financial statements are removed when data tables are discarded). We remove any

narrative disclosures that contain language indicating the relevant section has been omitted as

permitted by regulation and skip disclosures that are included by reference, either to an external

document or an attached exhibit, since the variety of alternate locations dramatically increases

the difficulty in obtaining that data. The footnotes, in particular, are frequently included by

reference. We drop any remaining items that do not contain at least 150 characters. Items shorter

31

than this cutoff have typically been omitted or included by reference, but do so using somewhat

unusual wording that the initial string search may not have recognized.

We then split each item into words, keeping disclosures with at least 500 words. Items

shorter than this length are relatively unusual and are unlikely to provide a meaningful

comparison to disclosures by peers in the auditor-industry-year reference group. Finally, we

exclude items exceeding 20,000 words because these frequently indicate problems splitting the

10-K into separate items. For example, the extraction process might erroneously treat the entire

annual report as the business description due to misspellings and other idiosyncratic document

features. Archival studies frequently handle outliers such as these through deletion,

winsorization, or robust techniques during the empirical analysis. However, doing so in the

current study would allow these outliers to be in reference groups and therefore have an

undesirable influence on the calculation of the similarity scores.

The overall sample selection is summarized in Table A-1. There are fewer observations

in the narrative disclosure samples than in the financial statement sample, primarily due to

unavailable reports on EDGAR, items included by reference to other locations, and textual

idiosyncrasies that lead to problems extracting the 10-K items of interest. The substantial drop in

the number of footnote observations, as compared to the business description and MD&A

samples, is because many companies attach financial statements and footnotes as an exhibit to

the report in a variety of unpredictable ways, making their automated extraction difficult.

<<<<< Insert Table A-1 about here >>>>>

32

Table A-1. Narrative Disclosure Sample Selection Process

Reports

10-K available on EDGAR; fiscal years 1997-2009; Compustat assets

> $1M; no FYE change; excl. financials and utilities; Big4 auditor

41,782

Less: Short reports (<50,000 characters)

(1,633)

Total annual reports available

40,149

Bus Desc

MD&A

Footnotes

Less: Item not successfully extracted

(1,918)

(936)

(1,166)

Less: Item specifically omitted

(10)

(41)

(117)

Less: Item included by reference

(23)

(2,840)

(10,516)

Less: Short items (<150 characters)

(1,277)

(1,173)

(3,415)

Less: < 500 or > 20,000 words

(886)

(1,257)

(7,227)

Less: < 5 other clients in auditor-industry-year

(2,680)

(2,622)

(3,269)

Total items available

33,355

31,280

14,439

33

APPENDIX B

CALCULATION OF NARRATIVE DISCLOSURE SIMILARITY SCORE

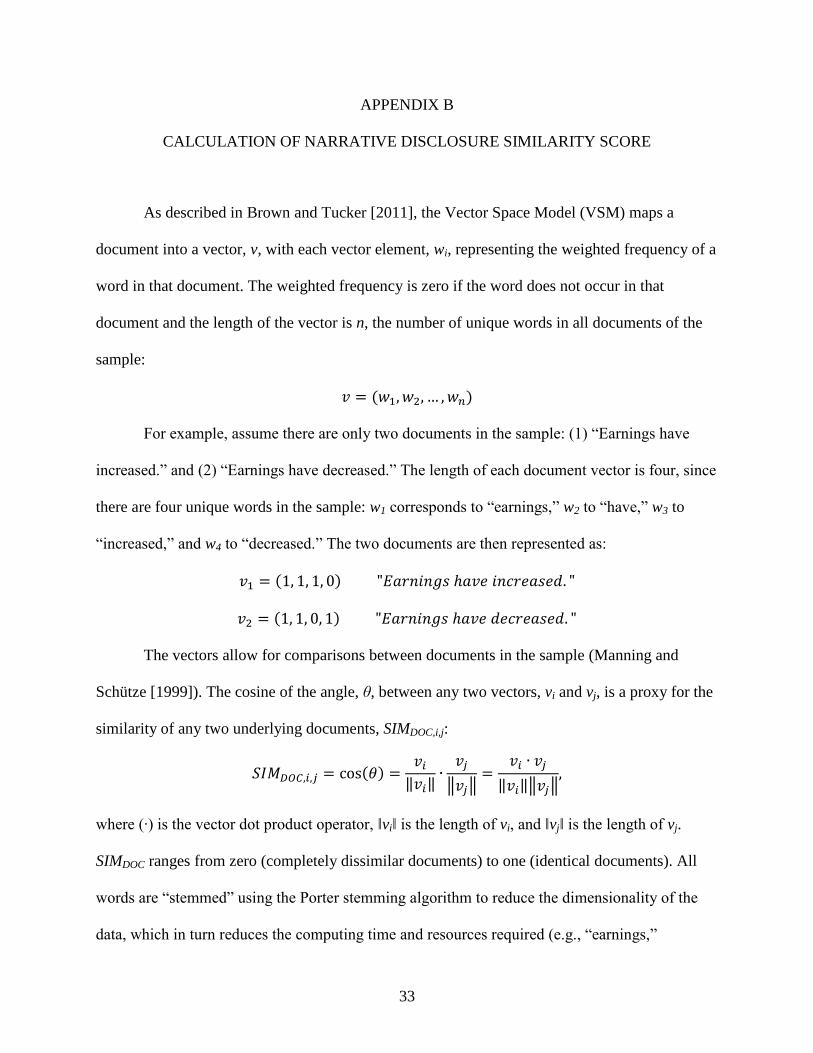

As described in Brown and Tucker [2011], the Vector Space Model (VSM) maps a

document into a vector, v, with each vector element, wi, representing the weighted frequency of a

word in that document. The weighted frequency is zero if the word does not occur in that

document and the length of the vector is n, the number of unique words in all documents of the

sample:

( )

For example, assume there are only two documents in the sample: (1) “Earnings have

increased.” and (2) “Earnings have decreased.” The length of each document vector is four, since

there are four unique words in the sample: w1 corresponds to “earnings,” w2 to “have,” w3 to

“increased,” and w4 to “decreased.” The two documents are then represented as:

( )

( )

The vectors allow for comparisons between documents in the sample (Manning and

Schütze [1999]). The cosine of the angle, θ, between any two vectors, vi and vj, is a proxy for the

similarity of any two underlying documents, SIMDOC,i,j:

( ) ‖ ‖

‖ ‖

‖ ‖‖ ‖

where (∙) is the vector dot product operator, ‖vi‖ is the length of vi, and ‖vj‖ is the length of vj.

SIMDOC ranges from zero (completely dissimilar documents) to one (identical documents). All

words are “stemmed” using the Porter stemming algorithm to reduce the dimensionality of the

data, which in turn reduces the computing time and resources required (e.g., “earnings,”

34

“earned,” and “earn” are all converted to “earn”).32

Consistent with Brown and Tucker [2011],

the term frequency-inverse document frequency (TF-IDF) algorithm is used to decrease the

weight on frequently used words and increase the weight on uncommon words.33

Therefore,

instead of a raw frequency count, each document vector element is the frequency count of the

word multiplied by a weight based on the relative prominence of that word in the entire sample.

Because Brown and Tucker [2011] were interested in differences between just two

documents at a time, they only calculate pairwise similarity scores. In contrast, in this paper the

pairwise scores are aggregated to get a measure of the similarity between one narrative

disclosure and the disclosures issued by the client reference group. As with the financial

statement similarities, the reference group contains other clients of the same auditor, within the

same GICS industry and year. To combine the pairwise SIMDOC,i,j scores between client i and all

other clients j in the same auditor, industry, and year, the pairwise similarities are averaged to get

SIMDOC,i for each observation in the sample.

The SIMDOC,i similarity measure is calculated for each observation in the business

description (RAWSIMBUS), MD&A (RAWSIMMD&A) and footnote (RAWSIMNOTES) samples.

Brown and Tucker [2011] show that these raw scores are positively related to document length

because of the mechanics of the calculation. They control for this relationship by regressing the

raw similarity on the first five powers of the number of words in the observation i document

(LENBUS, LENMD&A, and LENNOTES in the current study). In the current study we use the first

32

Even with the reduced dimensions, the calculations take over one week to run on a 2.66 GHz, quad-core machine,

while occupying most of the 6 gigabytes of working memory. 33

We do not use a “stop word” list to remove extremely common (i.e., unimportant) words, such as “the” and “a,”

from the sample as in Li [2010]. These words will receive a weight of zero, or very close to it, via the TF-IDF

weighting procedure. Brown and Tucker [2011] find no substantial difference in their conclusions between using the

TF-IDF approach and a simple frequency count combined with a stop word list. The TF-IDF weights are generated

independently for each type of narrative disclosure.

35

three powers because the magnitudes of the coefficients rapidly approach zero after this point.34

In order to maximize the sample size for making this adjustment, we use all available

observations, including those from non-Big 4 auditors.

Regressing the raw similarity scores on the first three powers of the document length

yields a residual that represents the variation in the raw similarity scores that cannot be explained

by these factors. These residuals are labelled SIMBUS, SIMMD&A, and SIMNOTES, producing the

similarity scores used in the analysis. Descriptive data for these measure components are in

Table B-1.

<<<<< Insert Table B-1 about here >>>>>

34

Hanley and Hoberg [2012] use the VSM to measure the similarity of an IPO prospectus to all the recent IPO’s

experiencing litigation problems. However, they do not control for document length, making it difficult to ascertain

the validity of their measure.

36

Table B-1. Calculation of Narrative Disclosure Similarity Measures

Variable Mean Std Dev 25% Median 75% Obs

SIMBUS 0.002 0.077 (0.053) (0.017) 0.040 33,355

SIMMD&A 0.002 0.087 (0.057) (0.024) 0.038 31,280

SIMNOTES 0.000 0.048 (0.029) (0.013) 0.011 14,439

RAWSIMBUS 0.108 0.085 0.045 0.087 0.148 36,035

RAWSIMMD&A 0.113 0.095 0.044 0.086 0.155 33,902

RAWSIMNOTES 0.054 0.061 0.021 0.037 0.064 17,708

LENBUS 6,338 3,739 3,602 5,471 8,252 36,253

LENMD&A 7,054 3,870 3,984 6,437 9,401 34,131

LENNOTES 8,623 4,018 5,423 7,934 11,178 18,083 Subscripts: BUS = Business Description, MD&A = Management’s Discussion & Analysis, NOTES = Footnotes to

Financial Statements.