Embed Size (px)

Citation preview

Auditing: The Art and Science of Assurance Engagements

Chapter 16: Audit of Cash Balances

Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Chapter 16 Learning Objectives

1. Identify the different types of cash accounts. Explain the relationship between cash and the other transaction cycles.

2. Describe the steps in auditing the general cash account.

3. Identify the additional procedures conducted when there is suspicion of fraud.

4. Explain how an audit of the payroll cash account differs from the audit of the general cash account.

16-2Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Types of Cash Accounts

• General cash account• Imprest payroll account • Branch bank account• Imprest petty cash fund• Cash equivalents

16-3Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Relationship between Cash and Transaction Cycles

• General cash is considered significant in almost all audits, even when the ending balance is immaterial.

• The amount of cash flowing into and out of the cash account is frequently larger than for any other account in the financial statements (e.g. cash for sales, cash for purchase, cash for payroll).

16-4Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

General Cash Internal Controls

• Controls over the transaction cycles:– Appropriate controls over the receiving of cash (sales and

other receipts) and controls over disbursements (payments to suppliers, employees and others)

• Independent bank reconciliations:– Should be completed on a timely basis– Bank statements should be received unopened by an

independent reconciler

16-5Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Cash Errors discovered in Audits of other Transaction Cycles

• Examples of such errors include:– Failure to bill a customer– Billing customer at an incorrect price– Duplicate payment of a vendor’s invoice– Payment for raw materials not received– Payment to an employee for hours not worked– Payment to a related party at an inflated interest rate

16-6Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

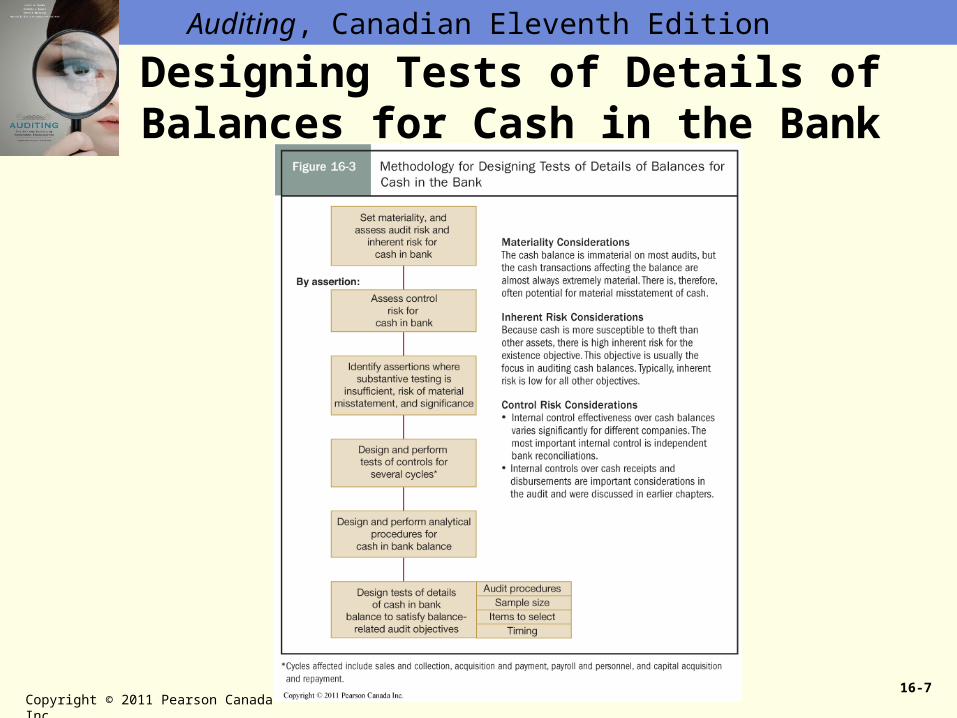

Designing Tests of Details of Balances for Cash in the Bank

16-7Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Materiality Considerations

• The cash balance is immaterial on most audits.• Cash transactions affecting the balance are almost

always material.• Potential for material misstatement of cash exists.

16-8Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Cash – Inherent Risks

• Cash is more susceptible to theft than other assets.• This results in high inherent risk for the existence

objective.• Inherent risk is typically low for other audit objectives.

16-9Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Cash – Control Risk

• Control risk for cash needs to be addressed on a cycle by cycle basis (particularly controls over cash receipts and disbursements).

• Control risk varies from organization to organization.• Most important internal control is independent bank

reconciliations.

16-10Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Audit of the General Cash Account

1. Assess controls over the transaction cycles affecting the recording of cash receipts and disbursements.

2. Assess controls over the preparation of independent bank reconciliations.

3. Test key controls to be relied upon.

4. Analytical procedures may be limited if the year end bank reconciliation is audited 100%.

5. Design and conduct audit procedures of year end cash balances.

16-11Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Year-end Audit Procedures for Cash

• Detail tie-in: Tests of deposits in transit, full bank reconciliation, trace reconciled balance to general ledger.

• Existence, completeness, accuracy: Send and test bank confirmation, obtain and test cut-off bank statement, extended tests of bank reconciliation, or proof of cash.

(Continued)

16-12Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Year-end Audit Procedures for Cash (Continued)

• Cut-off: Count cash on hand and trace to subsequent deposit, tests of deposits in transit, record last cheque number and follow-up use in subsequent year, trace outstanding cheques to subsequent reconciliation.

• Presentation and disclosure: Examine minutes, loan agreements, confirmations; review of financial statements.

16-13Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Review Question 16-15, p. 560

• In auditing the bank reconciliation, discuss the differences in emphasis with respect to deposits in transit and outstanding cheques.

16-14Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

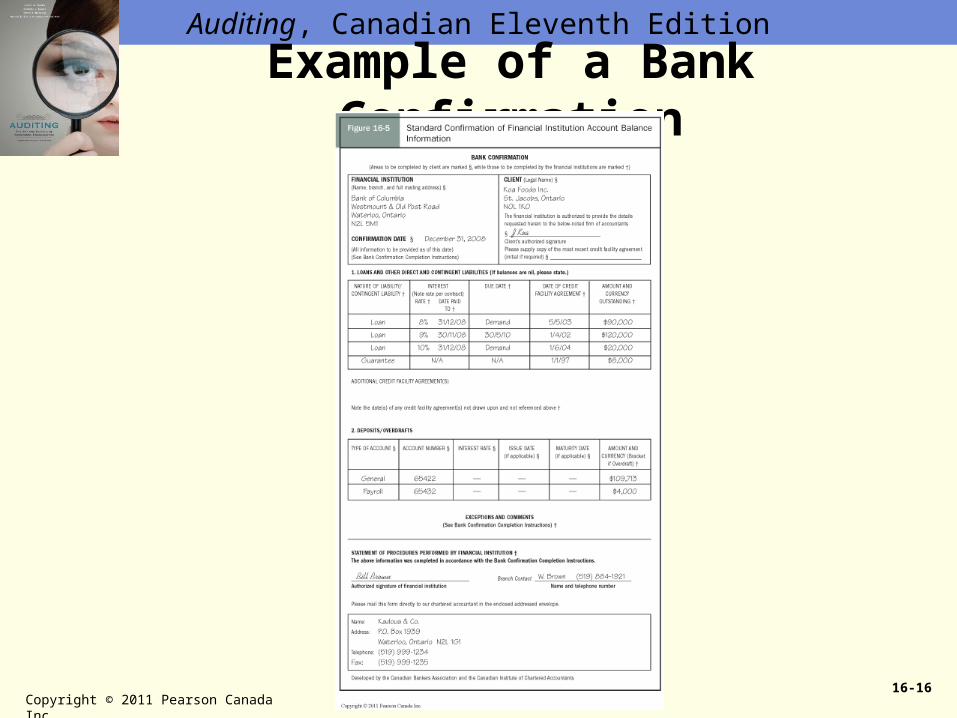

Bank Confirmation

• A standard form approved by the CICA and Canadian Bankers Association is used.

• Auditor controls the sending of the bank confirmation and has it returned to the auditor’s office.

• Provides information about cash accounts, loans, guarantees or other holdings.

16-15Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Example of a Bank Confirmation

16-16Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Review Question 16-5, p. 560

• Discuss the difference between positive confirmations of accounts receivable and bank confirmations.

16-17Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Cutoff Bank Statement

• Is a partial bank statement from the month after the client’s year end.

• The client is requested to authorize the bank to either send the bank statement to the auditor’s offices or authorize the auditor to pick it up directly from the bank.

16-18Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Fraud-Oriented Procedures

• Extended tests of bank reconciliation: transactions are traced to source journals or source documents.

• Proof of cash: transactions are both traced and reconciled to supporting journals or source documents.

• Tests for kiting: detailed bank transfer schedule

16-19Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Discussion Problem 16-17, p. 560

• Identify motivations for theft of cash• Identify preventive controls• List audit procedures for detection

16-20Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Audit of Payroll Cash Account

• Requires a short period of time if an imprest account is used and the bank reconciliation is current.

• Reconciling items tend to be outstanding cheques only.

16-21Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Audit of Electronic Cash Transactions

• Examples of electronic cash:– Automated deposit of payroll to employees– Electronic cash management (e.g. transfer from

general account to payroll account)– Electronic data interchange (e.g. payment to

suppliers or payment from customers)– Electronic funds transfer (e.g. transfer of cash to

other branches)– Receipt of debit card payments from customers

16-22Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Control Over Debit Card Cash Receipts

• Cash reconciliation processes should continue as part of the cash receipts function.

• Debit card totals should be agreed on a daily basis to amounts deposited in the bank (reconciliation independent of point of sale data entry).

16-23Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Control Over and Audit of Electronic Payments

• Automatic pre-authorized monthly payments: – Controls should be in place to ensure that only authorized

amounts are set up for payment– Controls should exist to ensure that all automatic

withdrawals are recorded in the accounts in the period made

• Payments tested as part of purchases, payments cycle.

(Continued)

16-24Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition Control Over and Audit of Electronic

Payments (Continued)

• Payroll payments:– Should be paid using an imprest bank account– Master file changes (e.g. new employee set up and wage rate

changes) should be properly authorized and independently verified

– Independent approval of amounts paid and bank accounts established should occur

• Tested as part of the personnel and payroll cycle

(Continued)

16-25Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Control Over and Audit of Electronic Payments (Continued)

• Audit of electronic receipts and payments– Extent of work depends upon assessed quality of

internal controls– Usually fewer outstanding bank transactions for

electronic transactions than for paper-based transactions

(Continued)

16-26Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Control Over and Audit of Electronic Payments (Continued)

– Automatic transactions should be agreed to an authorized schedule

– For imprest payroll, review documentation and agree to the reconciliation

16-27Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Petty Cash

• Balance is frequently immaterial, however usually audited because of– Susceptibility to defalcation– Client expectations

16-28Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Internal Controls Over Petty Cash

• Most important control is that the fund is the responsibility of one individual.

• Should not be mingled with other receipts.• Funds should be kept separate from other activities.• Disbursements and reimbursements should be

properly documented and authorized.

16-29Copyright © 2011 Pearson Canada Inc.

Auditing, Canadian Eleventh Edition

Audit Tests for Petty Cash

• Focus is on transactions rather than ending balance.• As with other cycles, the auditor documents and

evaluates internal controls prior to the actual conduct of tests, which are tailored to the quality of the internal controls.

16-30Copyright © 2011 Pearson Canada Inc.

![audit-uii.yolasite.comaudit-uii.yolasite.com/resources/AUDITING/5 Investments and Cash... · CHAPTER 18 / AUDITING INVESTMENTS AND CASH BALANCES [867] the audit risk model might indicate](https://img.dokumen.tips/doc/110x75/5aa79cf97f8b9a294b8c56c1/audit-uii-investments-and-cashchapter-18-auditing-investments-and-cash-balances.jpg)