Embed Size (px)

Citation preview

Asymmetric information and Capital Asymmetric information and Capital StructureStructure

In contrast to the agency costs problem, In contrast to the agency costs problem, here the way of financing does not affect here the way of financing does not affect managerial actions.managerial actions.However, the way of financing affects what However, the way of financing affects what investors think about your firm and how investors think about your firm and how much they will underprice/overprice the much they will underprice/overprice the claims you sellclaims you sell Adverse selection problemAdverse selection problem SignalingSignaling

Adverse Selection ProblemAdverse Selection Problem

Assume there are two equally likely states of nature (1 – Assume there are two equally likely states of nature (1 – good news, 2 – bad news)good news, 2 – bad news)

The firm has liquid assets LThe firm has liquid assets Lii and tangible assets in place and tangible assets in place

AAii

AfterAfter the news has arrived the firm cosniders: (1) do the news has arrived the firm cosniders: (1) do nothing or (2) issue 100 of new equity to new nothing or (2) issue 100 of new equity to new shareholdersshareholders

Do NothingDo Nothing Issue EquityIssue Equity

GoodGood BadBad GoodGood BadBad

LLii 5050 5050 150150 150150

AAii 200200 8080 200200 8080

VVii (firm value) (firm value) 250250 130130 350350 230230

Can it be that the firm issues equity Can it be that the firm issues equity in both states?in both states?

If the market thinks the firm issues 100 of equity in any state, it If the market thinks the firm issues 100 of equity in any state, it values the firm after investment as Vvalues the firm after investment as V = 0.5*350 + 0.5*230 = 290= 0.5*350 + 0.5*230 = 290The existing shareholders in the good state than get: The existing shareholders in the good state than get: ((V-E)/V)*V((V-E)/V)*V11 = (190/290)*350 = 229.31 < 250 = (190/290)*350 = 229.31 < 250Hence, they will choose not to issue equity in the good stateHence, they will choose not to issue equity in the good stateHence, if a firm issues equity it must be in the bad state. Then the Hence, if a firm issues equity it must be in the bad state. Then the market knows V = 230. The existing shareholders than getmarket knows V = 230. The existing shareholders than get((V-E)/V)*V((V-E)/V)*V22 = (130/230)*230 = 130. = (130/230)*230 = 130.

Hence, in the bad state the firm is indifferent between issuing and Hence, in the bad state the firm is indifferent between issuing and doing nothingdoing nothing

We have “lemons problem”. In the good state the firm is underpriced We have “lemons problem”. In the good state the firm is underpriced and does not want to issue equity. Only in a bad state a firm may and does not want to issue equity. Only in a bad state a firm may want to issue and the market forms believes accordingly. want to issue and the market forms believes accordingly.

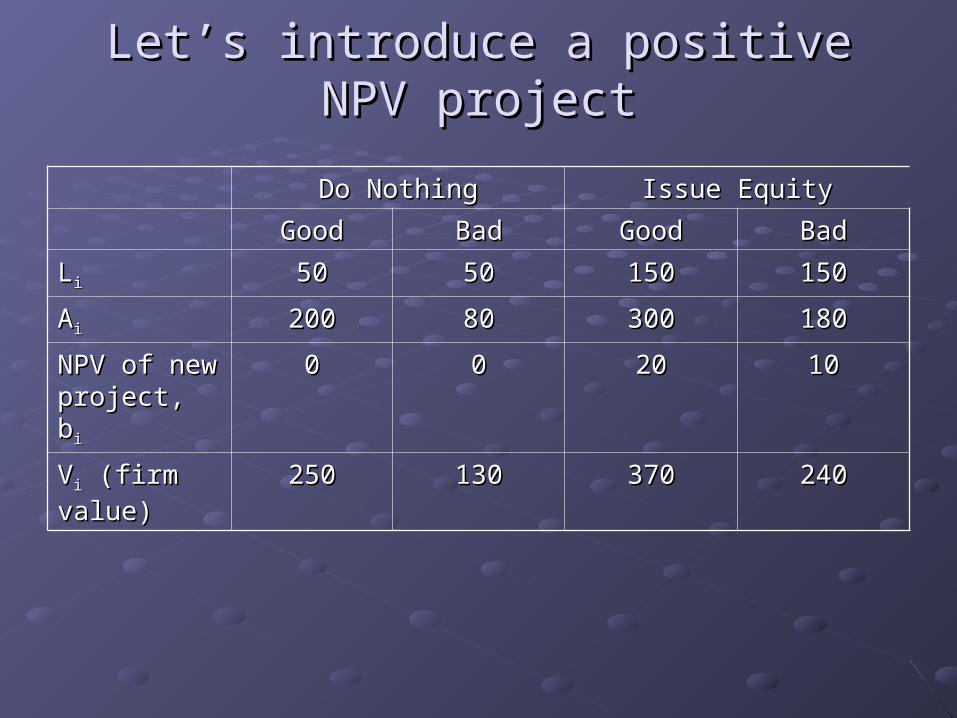

Let’s introduce a positive NPV projectLet’s introduce a positive NPV project

Do NothingDo Nothing Issue EquityIssue Equity

GoodGood BadBad GoodGood BadBad

LLii 5050 5050 150150 150150

AAii 200200 8080 300300 180180

NPV of new NPV of new project, bproject, bii

00 00 2020 1010

VVii (firm value) (firm value) 250250 130130 370370 240240

If the market thinks the firm issues 100 of equity in any If the market thinks the firm issues 100 of equity in any state, it values the firm after investment asstate, it values the firm after investment as

VV = 0.5*370 + 0.5*240 = 305= 0.5*370 + 0.5*240 = 305

The existing shareholders in the good state than get:The existing shareholders in the good state than get:

((V-E)/V)*V((V-E)/V)*V11 = (205/305)*370 = 248.7 < 250 = (205/305)*370 = 248.7 < 250

Hence, they will still not choose not to issue equity in the Hence, they will still not choose not to issue equity in the good stategood stateHence, if a firm issues equity it must be in the bad state. Hence, if a firm issues equity it must be in the bad state. Then the market knows VThen the market knows V = 240. The existing = 240. The existing shareholders than getshareholders than get

((V-E)/V)*V((V-E)/V)*V22 = (140/240)*240 = 140 > 130. = (140/240)*240 = 140 > 130.

Now in the bad state the firm strictly prefers to issue!Now in the bad state the firm strictly prefers to issue!

Can it be now that the firm issues Can it be now that the firm issues equity in both states?equity in both states?

The above result is consistent with the empirical The above result is consistent with the empirical observation: the stock price declines on the observation: the stock price declines on the announcement of an equity issue (for US on announcement of an equity issue (for US on average by 3%)average by 3%)

Two other results that follow from the theory and Two other results that follow from the theory and are observed in practice:are observed in practice: The stock price tends to rise prior to the The stock price tends to rise prior to the

announcement of an equity issue (managers wait until announcement of an equity issue (managers wait until good news become known to the market, but does good news become known to the market, but does not have an incentive to wait when the news is bad)not have an incentive to wait when the news is bad)

Firms tend to issue equity when information Firms tend to issue equity when information asymmetries are minimized, such as immediately asymmetries are minimized, such as immediately after earnings announcementsafter earnings announcements

SourceSource: Deborah Lucas and Robert McDonald, “Equity Issues and Stock Price : Deborah Lucas and Robert McDonald, “Equity Issues and Stock Price Dynamics,” Dynamics,” Journal of FinanceJournal of Finance 45 (1990): 1019–1043. 45 (1990): 1019–1043.

Depending on the model other types of Depending on the model other types of equilibria can existequilibria can exist

Notice: if we make NPV of the project in the Notice: if we make NPV of the project in the good state a bit bigger, the firm will issue equity good state a bit bigger, the firm will issue equity in the good state.in the good state.There are two types of inefficiency that can There are two types of inefficiency that can created by asymmetric infocreated by asymmetric info Positive NPV projects fail to be financed (like in our Positive NPV projects fail to be financed (like in our

model)model) Negative NPV projects may happen to be financed! (It Negative NPV projects may happen to be financed! (It

happens when in the good state the project has NPV happens when in the good state the project has NPV > 0, in the bad state NPV < 0, but on average NPV > > 0, in the bad state NPV < 0, but on average NPV > 0 and there is a pooling equilibrium) 0 and there is a pooling equilibrium)

Implication for capital structureImplication for capital structure

Pecking order theoryPecking order theory: among the methods of : among the methods of financing firms that feel underpriced should start financing firms that feel underpriced should start from the one which is least sensitive to from the one which is least sensitive to information:information: First – retained earnings (liquid assets First – retained earnings (liquid assets LLii)) Second – debtSecond – debt Third – equityThird – equity

Information insensitivity reduces the discount the Information insensitivity reduces the discount the firms incur when they sell their securitiesfirms incur when they sell their securities

Aggregate Sources of Funding for Capital Aggregate Sources of Funding for Capital Expenditures, U.S. CorporationsExpenditures, U.S. Corporations

In aggregate, firms tend to repurchase equity and issue debt. But more than In aggregate, firms tend to repurchase equity and issue debt. But more than 70% of capital expenditures are funded from retained earnings.70% of capital expenditures are funded from retained earnings.SourceSource: Federal Reserve Flow of Funds.: Federal Reserve Flow of Funds.

Capital Structure. Bottom lineCapital Structure. Bottom line

No single theory of capital structureNo single theory of capital structure Too many factors are in playToo many factors are in play

Firms differ a lot in how they choose cap Firms differ a lot in how they choose cap structure but there are some systematic structure but there are some systematic patterns e.g. across industries or ages patterns e.g. across industries or ages

In each case one should understand what In each case one should understand what factors are most importantfactors are most important

Capital budgeting and valuation Capital budgeting and valuation with leveragewith leverage

Three methods:Three methods: WACCWACC Adjusted Present Value (APV)Adjusted Present Value (APV) Flow-to-Equity (FTE)Flow-to-Equity (FTE)

For this lecture we will assume thatFor this lecture we will assume that Risk of the project to evaluate = risk of the firmRisk of the project to evaluate = risk of the firm Debt/Equity remains constantDebt/Equity remains constant

WACC MethodWACC Method

Note: here and below by D we will mean net Note: here and below by D we will mean net debt = debt – cash. I.e. we will value the project debt = debt – cash. I.e. we will value the project net of its cash assets (that earn market interest net of its cash assets (that earn market interest rate)rate)

ExampleExample

Avco is considering introducing new productAvco is considering introducing new product Will become obsolete in 4 yearsWill become obsolete in 4 years Annual sales: $60 mln per yearAnnual sales: $60 mln per year Manufacturing costs and operating expenses: $25 Manufacturing costs and operating expenses: $25

mln per year and $9 mln per yearmln per year and $9 mln per year Upfront R&D and marketing expenses: $6.67 mlnUpfront R&D and marketing expenses: $6.67 mln Upfront equipment expenses: $24 mlnUpfront equipment expenses: $24 mln No NWC requirementsNo NWC requirements Tax rate = 40%Tax rate = 40%

Expected Free Cash Flow from Avco’s Expected Free Cash Flow from Avco’s RFX Project (Spreadsheet)RFX Project (Spreadsheet)

Market risk of the project is expected to be similar to that Market risk of the project is expected to be similar to that of the company’s other lines business.of the company’s other lines business.Debt/equity ratio is supposed to stay the sameDebt/equity ratio is supposed to stay the same

Avco’s Current Market Value Balance Sheet ($ million) Avco’s Current Market Value Balance Sheet ($ million) and Cost of Capital Without the RFX Project:and Cost of Capital Without the RFX Project:

(Remember D = net debt = 300)(Remember D = net debt = 300)

%8.6)1(

cDEwacc rDE

Dr

DE

Er

mln 25.61$068.1

18

068.1

18

068.1

18

068.1

184320 LV

NPV = 61.25 – 28 = $33.25 mlnNPV = 61.25 – 28 = $33.25 mln

Notes:Notes:• we use the same WACC for all periods we use the same WACC for all periods because we assume that D/E remains constantbecause we assume that D/E remains constant• we use the WACC of the firms because we we use the WACC of the firms because we assume the project does not change D/Eassume the project does not change D/E

Implementing a constant Debt-Implementing a constant Debt-Equity ratioEquity ratio

Currently Avco has D/E = 1Currently Avco has D/E = 1By undertaking the new project Avco adds new By undertaking the new project Avco adds new assets to the firm with initial market value Vassets to the firm with initial market value VLL

0 0 = = $61.25 mln.$61.25 mln.Therefore, to maintain D/E constant Avco must Therefore, to maintain D/E constant Avco must add 0.5*61.25 = $30.625 mln in new debt (net add 0.5*61.25 = $30.625 mln in new debt (net debt)debt)For this it can e.g. spend its 20 mln in cash and For this it can e.g. spend its 20 mln in cash and borrow 10.625 mlnborrow 10.625 mlnSince only 28 mln is needed to fund the projects, Since only 28 mln is needed to fund the projects, the rest 30.625 – 28 = 2.625 will be paid to the rest 30.625 – 28 = 2.625 will be paid to shareholders as dividend (or share repurchase)shareholders as dividend (or share repurchase)

Avco’s Current Market Value Balance Avco’s Current Market Value Balance Sheet ($ million) with the RFX ProjectSheet ($ million) with the RFX Project

OK, in this way we can make sure the OK, in this way we can make sure the project doest not change D/E initially. But project doest not change D/E initially. But what happens with time?what happens with time?

We can ensure constant D/E further by properly We can ensure constant D/E further by properly adjusting debt each periodadjusting debt each period

We call the necessary for this amount of debt “debt We call the necessary for this amount of debt “debt capacity”, denote capacity”, denote DDtt

Here Here VVLLt t – the project’s levered continuation value, i.e. – the project’s levered continuation value, i.e.

Continuation Value and Debt Capacity of Continuation Value and Debt Capacity of the RFX Project over Time (Spreadsheet)the RFX Project over Time (Spreadsheet)

Adjusted Present Value MethodAdjusted Present Value Method

We have to compute We have to compute VVUU and and PVPV(Interest (Interest Tax Shield). Let’s ignore other stuff.Tax Shield). Let’s ignore other stuff.

To compute To compute VVUU we need to compute we need to compute rrUU

Why is Why is rrUU like this? From MM II with taxes like this? From MM II with taxes

it seems it should be:it seems it should be:

But MM II was derived (see lecture 8) But MM II was derived (see lecture 8) under the assumption that under the assumption that debt debt is constant is constant in perpetuity, NOT debt-equity ratio!in perpetuity, NOT debt-equity ratio!

What does it change?What does it change?

Dc

cE

cU r

DE

Dr

DE

Er

)1(

)1(

)1(

Similarly to lecture 8:Similarly to lecture 8: VVLL

≡ ≡ E E + + D D = = VVUU + + TSTS

Thus, Thus, DDrrDD + + EErrEE = = VVUUrrUU + + TSrTSrTSTS

But when D/E is kept constant But when D/E is kept constant rrTSTS = r = rU U (interest (interest

tax shield becomes risky and has a similar tax shield becomes risky and has a similar risk to the project’s cash flows)risk to the project’s cash flows)

And, hence,And, hence, we obtainwe obtain

%8 Ur

Now we have to compute the interest tax shieldNow we have to compute the interest tax shield

mln 62.59$08.1

18

08.1

18

08.1

18

08.1

184320 LV

mln 63.1$08.1

20.0

08.1

39.0

08.1

57.0

08.1

73.0Shield)Tax Interest (

432PV

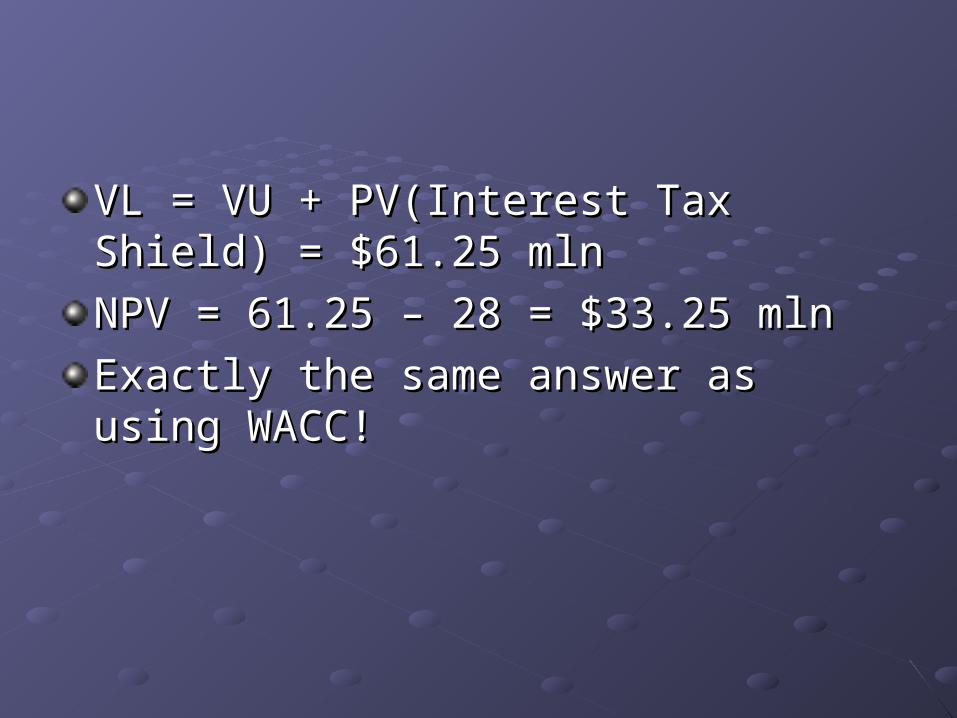

VL = VU + PV(Interest Tax Shield) = VL = VU + PV(Interest Tax Shield) = $61.25 mln$61.25 mln

NPV = 61.25 – 28 = $33.25 mlnNPV = 61.25 – 28 = $33.25 mln

Exactly the same answer as using WACC!Exactly the same answer as using WACC!

![Asymmetric Structure-Preserving Subgraph Queries for Large ...bchoi/fanzheicde15techreport.pdfet al. [9] keep both query and data graphs private. In contrast, as query clients may](https://img.dokumen.tips/doc/110x75/604d53022034390def5c939c/asymmetric-structure-preserving-subgraph-queries-for-large-bchoifa-et-al-9.jpg)