Embed Size (px)

Citation preview

ASX Australian Investor Study2017

Brochure / report title goes here | Section title goes here ASX Australian Investor Study | 2017

ContentsTop 10 findings 01

Executive summary 03

1. Retail investment in Australia 11

1.1 Definitionsusedinthisreport 11

1.2 Thevalueofinvestingtoindividuals 11

1.3 Thevalueofawell-functioningfinancialexchange 12

2. The investment landscape is changing 14

2.1 Lowinterestrateenvironment 14

2.2 Policychange 15

2.3 Digitalinnovation 17

2.4 Demographicshifts 17

3. Who is investing? 20

3.1 ChangesininvestmentownershipinAustralia 21

3.2 TheprofileoftheAustralianinvestor 27

3.3 Understandingpotentialinvestors 40

4. What are Australians investing in and how? 46

4.1 Australianinvestors’portfoliosarenotverydiversified 46

4.2 Useofadvisoryservices 52

4.3 Useoftransactionservices 54

5. Why do Australians invest? 59

5.1 Awareness,knowledgeandattitudes 62

5.2 Australians’attitudestorisk 66

5.3 Diversification 71

6. Seeking a more diversified future 72

References 73

ASX Australian Investor Study | 2017

Top10findings

60%Australian adults or 11.2 million people hold investments outside of their institutional superannuation fund

37%

31% 7% 11%

of Australian adults or 6.9 million people hold investments that are available through a financial exchange

ofAustralian adultsholdshares

ofAustralianadultsholdderivatives

holdotheron-exchangeinvestments

10% to 20%

24% to 39%

More and more young people are investing outside their institutional superannuation funds

Overthelast5 yearstheproportionof18-24 yearoldsinvestinghasdoubledfrom

Theproportion of25-34yearolds hasincreasedfrom

overthe sameperiod

62% 56% 37%

On-exchange investments are a more common investment choice than cash or property

ofinvestors holdon-exchangeinvestments

ofinvestors holdcash

ofinvestorsholdinvestmentproperty

15% 13% 8%

Self-managed superannuation funds (SMSF) use will continue to grow, with 30% of Australian adults that do not currently use an SMSF planning to set one up in the future

ofadultsclaimto haveanSMSF

ofadultswithoutanSMSFareplanningtoestablishonewithinthenextyear

arefurtherplanningtoestablishoneinthenext13-24 months

ASX Australian Investor Study | 2017

1

46% 40% 15%

75%

Diversification is still not well understood

ofinvestorsclaim tobediversifiedand hold2.7investmentproducts

ofinvestorssaytheydonothavediversifiedportfolios. Theyhold1.6 investmentproducts

ofinvestorsdon’tknow ifthey’rediversified

ofshare ownersholdonly Australianshares

65%

40%

42%

of investors holding on-exchange investments transacted in the last 12 months

tradedusingnon-advicebrokersandonlinetradingplatforms

ofshareownershavetradedinthelast12months

71% ofinvestorsthattradedinthelast12monthsmadefewerthan10trades

81% 21%41%ofinvestorsunder35areseekingguaranteedorstableinvestmentreturns

ofthemostriskaverseinvestorsexpectreturns over10%

ofinvestorsover55arecomfortablewithsomevariabilityintheirreturns

Disconnect between investor risk profiles and their return expectations

Younginvestorsaremoreriskaversethanolderinvestors

60% of all investors use some form of professional advice (financial planner, full-service stockbroker, accountant, and/or lawyer) to help them make investment decisions

41%

84%of lapsed investors intend to return to investing

intendtoreturninnext2 years

ASX Australian Investor Study | 2017

2

ASX Australian Investor Study | 2017

3

ExecutivesummaryInvestingisacriticalactivityinanymoderneconomy.It’showbusinessesprepareforservingcustomersinthefuture,howanationgrowsovertime,andhowindividualsandfamiliescanparticipateinfinancialsuccessesofbusinessesandearn anincome.

Investingisasoldaseconomies themselves.Andyet,theearly Twenty-FirstCenturyisalsoatimeofconsiderablechangeintheinvestmentlandscape.Thechangingstructureofourpopulationisreshapingwhoisinvesting andwhy.Newdigitaltechnologieshavebroughtnewwaysforpeopletoinvest,alteredwhattheyinvestin,andhowtheyreceiveadvice.

IntheaftermathoftheglobalfinancialcrisisandtheEuropeansovereigndebtcrisis,therehasbeenaslowingofglobalgrowthandlownominalinterestrates,whichhavecontributedtoloweryieldsandledtoinvestorsreconsideringtheirriskappetite.OverthepastdecadetheAustralianfinancialsectorhasbeensubjecttosignificantpolicychangewhichhasseenatighteningofregulation.Thischangecontinuestounfoldandwillimpactthebehavioursoffinancialintermediaries andinvestors.

In2016,theAustralianequitymarketgenerallyoutperformedotherdevelopedequitymarketsglobally(RBA,2017).Atthetimeofwriting,theS&P/ASX200wasatitshighestlevelsincepriortotheglobalfinancialcrisis.Tradingvolumeshaveincreased23%overthe12monthstoMarch,andcontinuetogrow(ASX,2017a).Thedomesticequitymarketcapitalisationisatahistorichigh,reaching$1.8trillioninMarchthisyear(ASX,2017b).

Atthesametime,significantglobaleventshaveinfluenceddomesticmarketsoverthelastyear.TheannouncementsofdecisionsbyBritishvoterstoleavetheEuropeanUnionandbyUSvoterstoelectPresidentTrumpcoincidedwithincreasedtradingvolumesonASX.Thesetwolargelyunexpecteddevelopmentsarekeyexamplesofaglobalenvironmentcharacterisedbysignificantuncertainty.Geopoliticaldevelopmentsarelikelytocontinuetobeafocusforinvestorsinthenearfuture(InvestmentMagazine,2017).Againstthisbackground,riskmanagementwillbeanimportantconsiderationforallinvestors,increasingtheimportanceofhavinganappropriatelydiversifiedportfolio.

Thisstudydoesnotprovideanassessmentaboutwhetherretailinvestors(hereafterreferredtoas‘investors’)aredoingtherightthing,nordoesitofferadvicefortheseinvestorstofollow.Instead,thisstudyseekstoshedlightoninvestorbehaviourinthiscomplexandchanginginvestmentlandscape,andprovidessome‘foodforthought’fortheinvestmentindustrythatcaterstothem.

This2017editionofthestudyhasbeenpreparedbyDeloitteAccessEconomics, asuccessortodecadesofeffortbyASX, whichhasbienniallypublishedaprofile ofAustralianshareownershipsince1986. Thisstudyisbasedonanonlinesurveyof4,000individuals(arepresentativesample oftheAustralianadultpopulation). ThefocusisonAustralianadultsthat investoutsideoftheirinstitutional superannuationfundarrangements.

Theinvestmentlandscapehasbecomemoresophisticatedovertime,andwhileAustraliahasrankedwellagainstglobalmeasuresoffinancialliteracy,thereisscopetoimprove.Australianinvestors’portfoliosarenotverydiversified,andtheirawarenessoffinancialproductsdeclinesquickly outsideofshares.

Atthesametime,theinvestmentindustrymaynotbeengagingwithinvestorsaswellastheycouldbe.Someofthesurveyfindingsmaychallengeexistingindustryperceptionsofinvestors.Thereisanopportunityfortheindustrytochangeandbecomemoreresponsivetoitscustomers,whichcanhelpdeliverimprovedfinancialoutcomesforAustraliansand theeconomy.

This study also identifies some ‘food for thought’ for the investment industry.

Food for thought for the investment industry

• Do you have a good understanding of how these changes will impact investors?

• Is your business model geared towards supporting investors as the investment environment and their preferences change?

ASX Australian Investor Study | 2017

4

Investment ownership trends Thelevelofownershipof‘on-exchangeinvestments’(whichisdefinedtoincludeinvestmentproductsthatareboughtandsoldthroughafinancialexchange,forexample,sharesandderivatives)hasremainedbroadlyconsistentsincethe 2014study,ataround37%ofthe adultpopulation.

However,investingisbecoming morecommonamongyoungpeople. Theproportionof18-24yearoldsinvestinghasdoubledinthepastfiveyears,from 10%to20%.

Ownershipofinternationalshareshas alsoincreased.Today,nearly8%oftheadultpopulationsaythattheydirectlyholdshareslistedonaninternationalfinancialexchange,upfrom5%in2014.1

Profile of the Australian investor Three-fifths(60%)ofAustralianadultsdirectlyholdinvestmentsofsomesort(includinginvestmentsnotavailable onafinancialexchange)outsideof theirinstitutionalsuperannuationfund (Figurei).ThismeansthatmanyAustralianadultsarecomfortableinvesting, buttheyarenotnecessarilyinvesting inon-exchangeinvestments.

Mostcommonly,Australianinvestors holdtheirinvestmentsinapersonalcapacity.Ofinvestorsholdinginvestmentspersonally,younginvestorsaretheleastprominent.Thismaypartlyreflectthereal orperceivedbarriersthatthisgroupfaces,orthefactthattheyhaveotherpriorities.

Younginvestorsaremoredigitallysavvy, andwhiletheadventofdigitalwealthadvisory(i.e.roboadvice)offersopportunitiesforbothinvestorsandfinancialadviserstotakeadvantageof digitalinnovation,usehasbeenlimited. Thisismostlyduetoalackofknowledgeabouttheseproducts,whichsuggeststhattheinvestmentindustrycoulddomoretoeducateinvestors(andraisesquestionsaboutwhethertheseinnovationstrulymeetinvestors’needs).

Food for thought

• How is your business responding to the growth in numbers of young investors and self-directed investors?

• Do you promote the use of specific investments, like exchange-traded products, to facilitate easy access to international markets?

Figure i: Investment structures used, proportion of adult population

Investments

ShareoftheAustralianadultpopulationholding:

Investmentsinselfmanaged

superannuationfunds*

Investmentsincompanystructures

Investmentsinfamilytrusts

Investmentsinapersonalcapacity

60% 51% 15% 10% 7%

*ThisishigherthantheATO’sSMSFstatisticalreport–December2016,whichindicatesthataround6%ofAustralianadults aremembersofSMSFs

Note: Optionsdonotsumto100%becausemanyinvestorsholdinvestmentsthroughmorethanonestructure;2017(n=4000)

1Itispossiblethatrespondentsmayhavemisinterpretedthequestionandareinpartreportinginternationalsharestheyholdindirectly.

ASX Australian Investor Study | 2017

5

Atthesametime,andcontrarytoconventionalexpectations,younginvestorsalsoappearmoreriskaversethanolderinvestors–with4in5younginvestorspreferringguaranteedorstableinvestmentreturns.Theinvestmentindustrycouldseektobettertailortheirproductsandadvicetomeetthisneed,forexample,byconsideringcapitalprotectedproductsandprovidingeducationonriskmanagement.

On-exchangeinvestmentscollectivelycomprisethemostcommonlyheldinvestments–62%ofallinvestors(thatis, ofthe60%ofAustralianadultsthatinvest insomeway)holdtheminsomeform. Thisisfollowedbycashsavings(56%) andinvestmentproperty(37%).

Irrespectiveofhouseholdincomelevels,cash,shares,andpropertyarethemostcommonlyheldinvestmentsinAustralia,althoughwealthierhouseholdstendtoinvestrelativelymoreinpropertyandshares.

ThereisasignificantdomesticfocusinAustralians’investmentportfolios,with75%ofallshareowners(thatis,thoseinvestorsthatholdsharesofsomekind)onlyholdingdomesticshares,althoughtheymayhaveoverseasequitiesexposurethroughtheirinstitutionalsuperannuationfund.

Overthenext12months,moreinvestorsareplanningtomoveoutofcashthanotherinvestments.Thisislikelyaresultofrecordlowinterestratesandthelowrelativereturnsoncash.However,cashislikelytocontinuetobeoneofthemostpopularinvestmentchoices.

Why Australians invest Australianstypicallyinvestforthelongterm.Retirementandwealthaccumulationarefrontofmindforallagegroups,andindividualsareinvestinginproductsthatreflectthesegoals.

However,investingcanbeapathtoachievingotherlifeoutcomes.Forexample,asreflectedinthesurveyresultsandthecasestudyonWealthEnhancersPtyLtd(seeBoxAonpage34),youngerinvestorsmaybeincreasinglyconsideringinvestingasawaytosavefortheirhomedeposit.Theinvestmentadvisoryindustryisalreadyshiftingawayfrombusinessandproduct-ledoperatingmodelstocustomer-ledones.Byfocusingonbuildinglong-termclientrelationships,financialadviserscanhelptheirclientsinvesttoachieveabroaderrangeofoutcomesthroughoutdifferentlifestages.Thiswillrequirefinancialadviserstohaveabetterunderstandingoftheirclients'individualneeds.Makingbetteruseofcustomerdatawillbeanimportantenablertoachievingthisatscale.

Investors,onthewhole,feelconfidentinvestingincash,shares,andproperty, butquicklyloseconfidencewhenaskedaboutotherinvestments.Lessthan20%ofallinvestorsfeelconfidentinvestinginunlistedmanagedfunds,derivatives,andotheron-exchangeinvestments(suchasbonds,hybridsecurities,andexchange tradedfunds).

Therearelikelyanumberofreasonsforthis,whichmayincludethelingeringinvestorscepticismfromtheglobalfinancialcrisis.Itmayalsobepartlydrivenbyalackofunderstandingoftheseinvestmentproducts.Atthesametimeover30%ofinvestorsarenotawareoftheseproducts.Onewaytoimproveawarenessandunderstandingcouldbethroughimprovingfinancialeducation,includingthroughgreateruseoffinancialadvice.

Food for thought

• Does your business model cater for investors at all life stages?

• Are you developing low cost entry level products to cater for investors just starting out?

• How will you help educate young investors about the pros and cons of investing and of the value of professional financial advice?

Australian investors’ portfolios are not very diversified Diversificationisaboutaninvestor limitingtheirexposuretoanysingleasset(ASIC,2017a).However,Australianshaverelativelyconcentratedinvestmentportfolios,holdingprimarilycashsavings,shares,andinvestmentproperty.Thisonlyreflectsinvestors’holdingsoutsidetheirinstitutionalsuperannuationfund,and couldbebalancedoutdependingonhowtheirsuperannuationisinvested.Typically,superannuationassetsareprimarilyheldinequities(ABS,2017a).

Food for thought

• How can you help investors think about diversification?

• How can you engage investors to improve their awareness of and confidence with different financial products?

ASX Australian Investor Study | 2017

6

Australians’ attitudes to risk Australiansareriskaversebyglobalstandards.Aglobalinvestmentsurveyfoundthatonly29%ofAustralianinvestorsarepreparedtoincreasetheirriskprofilefortheopportunitytoearnmoreincome,comparedto66%ofinvestorsglobally (LeggMason,2015).Thisstudyfindsthatnearly70%ofallAustralianinvestorsareseekingstable,reliableorguaranteedreturnsfromtheirinvestments(Charti).

Thisriskaversionisparticularlystrongamongyounginvestors,challengingthestereotypethatolderpeoplearemoreriskaversethanyoungpeople.Thisisalsoreflectedinyounginvestors’higheraversiontoloss(Chartii).Thismayberelatedtotheeconomicenvironmentthattheyoungercohortshavegrownupin–witnessingtheimpactoftheglobalfinancialcrisisintheirformativeyears.Atthesametime,relativelylowerfinancialknowledgeandfinancialexperiencemayalsobedrivingthishigherdegreeofcautiousness(Kanetal.,2016).

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Chart i: Investors attitudes to risk, proportion of investors

0

Accepthighervariabilitywiththepotentialforhigherreturns

Acceptmoderatevariabilityinreturns

Preferstable,reliablereturns

Preferguaranteedreturns

MaleFemale

Notes: n=2391

Overall

The rise of SMSFs Self-managedsuperannuationfunds(SMSFs)havebecomeincreasinglypopular.Thisstudyfoundthat30%ofinvestorsthatdonotcurrentlyuseanSMSFintendtosetoneupinthefuture,suggestinggrowthinthenumberofusersofthisstructure.

SMSFinvestorsarelong-termfocused– inlinewiththepurposeofsuperannuation.Theirtopinvestmentgoalissavingforretirement.Theyarealsomorelikelytouseprofessionaladvicethantheaverageinvestor,citingtheadvantagesoftailoredadvice,andthecomplexitiesoftaxandadministrativeproceduresastheirmainreasonsfordoingso.

SimilartoAustralianinvestorsmorebroadly,SMSFsareinvestedheavilyincash,shares,andproperty,thoughthecasestudyonClassLimited(seeBoxBonpage36)revealedthatsomeSMSFinvestorsarealsointerestedinalternativessuchascrowd-fundingandpeer-to-peerlending.

Food for thought

• How can you help investors think through whether an SMSF is right for them, including educating them on portfolio construction, administrative and regulatory requirements?

• Given the expected growth of SMSFs, can you afford not to be an SMSF expert?

ASX Australian Investor Study | 2017

7

Notes: n=2391

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Chart ii: Reaction to investment balance dropping 20%, proportion of investors

0

I'dinvestmorefundstotakeadvantageofthelowerunit/sharepricesexpectingfuturegrowth

ThiswasariskIunderstood–I'dleavemyinvestmentsinplaceexpectingperformancetoimprove

I'dbeconcerned,butwouldwaittoseeiftheinvestmentsimprove

I'dcutmylossesandtransfermyfundstomoresecureinvestmentsectors

Losesleep–SecurityofmycapitaliscriticalandIdon'tintendtotakerisks

Overall 35-44 75+45-54 55-6425-3418-24 65-74

Moreriskaverseinvestorsareexpecting (onaverage)lowerreturnsthanlessriskaverseinvestors.However,1in5ofthemoreriskaverseinvestorsareseekingdoubledigitreturns.Giventhatinterestratesarecurrentlyathistoricallows,theseinvestorsmaybeunrealisticallyoptimisticabouttheirreturnexpectations.

Diversificationisoneofthemosteffectivewaystomanageinvestmentrisk(ASIC,2017a),andgiventhelevelofcautiousnessamongstAustralianinvestors,itmaybeexpectedtobewidelyused.However,around40%ofallinvestorsreportthat theydonothaveadiversified investmentportfolio.

Althoughsomeinvestorswillhavemadeaclearchoicetohavemoretargetedportfolios,othersmaybeconstrainedbyalackofaccesstoorknowledgeofcertaininvestmentproducts.

Whiletheinvestmentindustryhastakenstepstoimprovepublicunderstandingofthebenefitsofdiversification,theremaystillbeaninsufficientunderstandingofdiversificationamongstinvestors.Thiscouldmeanthattheinvestmentindustryisstrugglingtoconnectwithinvestors.Theindustryneedstoconsidernewapproachestohelpinvestorsbetterunderstandandnavigatetheirinvestmentjourney.

Food for thought

• How can you help investors understand what returns are reasonable for different asset classes in the current environment?

• How are you helping investors think through the risk and return trade-off?

• How can you help investors to understand the benefits of diversification?

ASX Australian Investor Study | 2017

8

How Australians approach investing Financialadviserscanassistinvestorswithunderstandingandaccessingtheirinvestmentoptions.Newtechnologiesbeingintroducedinthisspacehavethepotentialtosubstantiallychangethefutureoffinancialadviceprovision.

Currently,around60%ofallinvestorsusesomeformofprofessionaladvice(fromafinancialplanner,full-servicestockbroker,accountant,orlawyer)tohelpguidetheirinvestmentdecisions.Financialadvice(fromafinancialplannerorfullservicestockbroker)ismorecommonlysoughtbyhigherincomeinvestors,althoughthedifferencesaremodest(Chartiii).

Ownresearch Financialplanner oradviser

Fullserviceoradvicestockbroker

Accountant LawyerFamilyandfriends

10%

20%

30%

40%

50%

60%

70%

0%

Chart iii: Use of professional advice, by household income

Lessthan$80,000 $80,000-$150,000 Over$150,000

Notes: Investorscouldselectmorethanoneanswer,n=2391

Investorssaidthatthetopreasonsthey useadvicearethattheadvicecanbetailoredtotheirpersonalcircumstances,andthatanadviserhelpsthembettermanageriskintheirportfolio.Forthosenotusingadvice,theirmainreasonsareapreferencetobeincontrol(‘do-it-yourself’investors),andthattheyarenotconvincedthatadviceaddsvalue.

Ofthese‘do-it-yourself’(DIY)investors,theymaynotbeaversetousingfinancialadvice,butitcouldbethatthecurrentformofadvicedoesnotsuittheirpreferences.Innovationssuchasdigitalwealthadvice(i.e.roboadvice),whichoffersadvisoryserviceson-demand,maybemoresuitabletothisgroupofinvestors.Forexample,OwnersAdvisorysuggeststhatmanySMSFusershavetakenupthisservice(seeBoxD onpage56).

However,whenaskedaboutroboadvice, themajorityofinvestorssaidthatthey didnotknowenoughaboutroboadvicetoconsiderusingit.Younginvestorsweremorepositiveaboutusingroboadvice thanolderinvestors.

Providersoffinancialadviceneedto betterdemonstratethevalueoftheirservicestoinvestors.Whiledevelopments intheindustryhavesoughttoincreasetheuseoffinancialadvicebyimprovingitsqualityandaffordability,convincing investorsofthevalueofadvicehasbeen anongoingchallenge.

Developmentsintechnologycanhelpadviserstoengageinvestorsthrough moreefficientandconvenientchannels. Thiswillcontinuetobeanimportantfocusfortheindustry.

Food for thought

• Are you thinking about how you can engage DIY investors?

• How can you demonstrate the value of advice to counter the perceptions of a lack of value and high cost?

• Are you considering the development of your own technology or partnering with other organisations (white labelling) to increase the range of lower cost investment options for investors?

ASX Australian Investor Study | 2017

9

Understanding potential investors Non-investorsarepotentialinvestors.Understandingthebarrierstheyface andtheirattitudestoinvestingwillhelp torealisethatpotential.

Manynon-investorsareyoung,andas suchhavelowerincomes.Of18-34yearoldswhodonotinvest,61%haveanannualhouseholdincomeoflessthan$80,000. Themainreasoncitedbyindividualsthathaveneverinvestedfornotinvestingwasthattheydidnotthinktheyhadenoughmoneytodoso.Threeinfiveindividuals thathaveneverinvestedthinkthattheyneedmorethan$5,000tobegininvesting.2 Astheincomesoftheseindividuals increase,theywillbemorelikelytoinvest.

Individualsthathaveneverpreviouslyinvestedarealsomoreriskaversethaninvestors.Oftheseindividuals,36%wouldwantguaranteedreturnsontheirinvestments,comparedtoaround18% forinvestors.Theseindividualsarealso lessfinanciallysavvythaninvestorsand havelowerawarenessofalternative financialproducts.

Non-investorsthathavepreviouslyinvestedwerenotaversetostartinvestingagainoncetheirpersonalcircumstancesallowed.Around84%oflapsedinvestorssaidthattheyplantostartinvestingagainatsomepoint,with41%ofthisgroupintendingtoinvestagainwithinthenexttwoyears.

Thebarrierstonon-investorsbecominginvestorsaregenerallysurmountable.Improvingfinancialliteracywillencouragemanytostartinvesting.Theinvestmentindustrycouldreviewthetypesof‘entry-level’productsandservicesthatare offeredtoneworreturninginvestors, andhowtocommunicatetheiravailability tothesegroups.

Conclusion InvestingisimportantforAustralians. Asthepopulationages,andpeoplespendmoretimeinretirement,wealthaccumulationisbecomingcriticalto supportstandardsofliving.

Asinglepersonseekinga‘modest’lifestyleinretirementrequiresalumpsumofatleast$370,000(withouttheagepension)investedandreturning7%p.a.(SuperGuide,2017).Forcouples,thislumpsumneedstobeatleast$400,000.Inordertohavea‘comfortable’retirement,householdswillrequiredoubletheseamounts(SuperGuide,2017,andASFA,2016).Compulsorysuperannuationwillnotalwaysbeenoughtomaintainindividuals’lifestyleexpectations inretirement.

Investingearlytoaccumulatewealthwillmakethedifferencebetweenamodestandacomfortableretirementinthefuture–andwhetherornotindividualswillneedtorelyontheagepension.

WhilethemajorityofAustralianadultsholdinvestmentsofsomekind,thereremainsasignificantminoritywhodonotinvest.Thereisabigopportunity–engagingnon-investorswouldsignificantlyincreasethepoolofinvestedfunds,aswellasassistingthosepeopletofurthertheirfinancialgoals.

2Excludesthoseindividualsthatdidnotknoworwereunsure.

Whilemostinvestorsfeelcomfortablewithshares,cash,andproperty,diversificationremainsanissueimpactingoverallrisk.Thismaybeconstraininginvestors’abilitytobestmatchtheirinvestmentbehaviourstotheirfinancialgoals.Furthermore,investorsmaynotbeoptimisingtheirreturnforthelevelofrisktheyaretakingon.

Currently,mostinvestorsinAustraliaareself-directed,andchoosetoconducttheirownresearch.Manyalsoprefertodefertotheirfamilyandfriends.Moreknowledgeableinvestorsmaymakemoreuseofawiderrangeofinvestmentsproducts.However,manyinvestorssimplydonotseethevalueinseekingprofessionalfinancialadvice.Thissuggeststhattheindustryneedstoreconsiderthewayinwhichitinteractswithinvestorstodemonstrateitsrelevanceasapartnerin aninvestor’sjourney.

Thismaybethroughadoptingbusinessmodelsthatarecustomer-ledandfocusingonhowitcanhelpinvestorsachievetheirdesiredoutcomesthroughoutdifferentlifestages.Aswellasadoptingdevelopmentsintechnology.Theimpactofongoingpolicychangealsohasthepotentialtoimprovethevalueandreducethecostoffinancialadvice.Allofthesedevelopmentshavethepotentialtoenhancethevalueoffinancialadvice forinvestors.

Thereisalsoanopportunitytosupportparticipationofnon-investorsbyraisingfinancialliteracythroughfinancialeducationinitiativesandgreateraccesstofinancialadvice,aswellasofferingentrylevelproductstoinvestorsthataretaking theirfirststeps.

Australiahasover11millioninvestors.Butthiscouldbehigher.Thebarrierstoachievingthisarenotinsurmountable.

Food for thought

• How can you engage individuals that have never previously invested or have lapsed?

• Do you offer investment products with low entry costs and appropriate risk profiles for new investors?

ASX Australian Investor Study | 2017

10

ASX Australian Investor Study | 2017

11

TheAustralianShareOwnershipStudyisalongstandingASXinitiative.Firstconductedin1986,thestudyprofilesinvestorstoprovideanunderstandingoftheinvestmentlandscapeinAustralia:perceptions,attitudes,behaviours,anddemographicsofinvestors.

This2017AustralianInvestorStudy isthemostcomprehensiveiterationyet.Thisstudydiscussessomemegatrends andtheirimpactontheinvestmentlandscape,aswellasincludingmorecomprehensivequestionsaboutriskattitudes,familiaritywithalargerrangeofon-exchangeinvestments,useofdiversificationamonginvestors,andviews ofnewtechnologiessuchasroboadvice.

Thisstudyalsoidentifiessome foodforthoughtforthe investmentindustry.

Asurveywasconductedonline,withanationallyrepresentativesampleof4,000Australianresidentsansweringquestionsabouttheirinvestmentactivities.Afullexplanationofthesurveymethodology canbefoundinAppendixA.

Beyondthequantitativesurveyinsights,casestudieshavebeencompiledfromdiscussionswithsixindustryparticipants,whichprovideinsightsintoinvestingfromtheperspectivesofserviceproviders suchasfinancialadvisersand full-servicestockbrokers.

1.1 Definitions used in this report Thisreportfocusesonretailinvestors,specifically,thoseinvestorswhochoosetoinvestoutsideoftheirinstitutionalsuperannuationfund(thatis,superannuationheldinretail,industry,publicsector,andcorporatefunds),andthosewhotakeamoreactiveroleinmanagingtheirsuperannuation,suchasusersofself-managedsuperannuationfunds(SMSFs).

Inthisreport,investmentisdefinedasany'asset acquired for the purpose of producing income and/or capital gains for its owner' (ASX,2017c).Thisincludesinvestmentproperty,cashsavings,andfinancialproductsavailableonafinancialexchangesuchasshares,derivatives,bonds,andexchangetradedfunds.Italsoincludesinvestmentsheldthroughunlisted managedfunds(excludinginstitutional superannuationfunds).

1.2 The value of investing to individuals InvestmentisanimportantsourceofincomeforAustralians.Forthemedianhousehold,approximately20%ofweeklyincomecomesfrominvesting(ABS,2015).3Itprovidesawayforindividualstodiversifytheirsourcesofincome,managefinancialrisk,growtheirwealth,andplantheirretirement.AlmostallAustraliansareinvestorsthroughtheircompulsorysuperannuation,buttheirlevelofparticipationindecisionsaroundtheirinvestmentscandiffersignificantly.

1.2.1 Investment income and wealth creation Wealthcreationisaboutaccumulatingassets.Individualscanbuildtheirwealthmorequicklybysupplementingtheirwageswithreturnsfromtheirinvestments.

3Thisfigureincludeshouseholdsinthedrawdownphaseoftheirinstitutionalsuperannuation.

1.RetailinvestmentinAustralia

Key definitions

Adult population refers to all Australians aged 18 years and older.

Financial advice is advice provided by a financial adviser/planner or full-service/advice stockbroker. This is a subset of Professional Advice.

Lapsed investors are people who have held investments in the past, but do not currently do so.

Never invested are people who have never owned investments.

Non-investors comprise both Lapsed Investors and people that have Never Invested.

On-exchange investments is a term used in this report to refer to listed investments and other financial products available on a financial exchange and held through unlisted managed funds. This includes shares, derivatives, and other products such as bonds and ETFs.

On-exchange investors are people who hold some form of on-exchange investments.

Other investors are people who invest, but not in on-exchange investments. Instead they hold at least one of the following: commercial or residential investment property, cash or term deposits, or other investments that are not on-exchange investments.

Professional advice is advice provided by a financial adviser/planner, full-service/advice stockbroker, lawyer, or accountant.

Share owners are investors who hold shares, either domestically or internationally. This is a subset of on-exchange investors.

ASX Australian Investor Study | 2017

12

Labourincomeisthemainsourceofincomeformostpeople(ABS,2015),butitisrelativelydifficultforpeopletoadjustthisincomequickly.Whilesomeindividualsmayworklongerhoursthisislimitedbythenumberofhoursinaday(andotherphysicallimits).Otherindividualsmay seekouthigherpayingjobs,butcould beconstrainedbytheirqualifications andexperience.

Ontheotherhand,theirmoney(suchassavingsaccruedovertime)maybeeasiertoreallocatetomoreproductiveuses.Individualscanmakeachoicetoallocatetheirmoneyintodifferentassetswithincomegeneratingorcapitalgrowthpotential.Effectively,investingisaboutmakingthemostoftheirmoney,andbydoingsohelpingthembuildwealth morequickly.

Wealthcreationisimportantforsustainingqualityoflife,particularlyinretirement.Afterretiring,individualsrelyontheirsavingsastheirsourceofincome,andhavingaccumulatedmorewealthintheirworkingyearsmeansamorecomfortableretirement.Similarly,wealthaccumulationenablesindividualstoachievefinancialgoalsthroughoutlife,whethertheybehomeownership,payingforchildren’seducation,travelling,orsomethingelseentirely.

1.2.2 Risk management and diversification Withoutinvestmentincome,wages/salarieswouldbetheonlysourceofincomeformany(ABS,2015).Ifpeoplestopworkingorretirewithouthavingaccumulatedsufficientsavings,theymayhavetorelyongovernmentsupport,e.g.agepension.Maintainingtheirdesiredstandardoflivingcouldbechallengingiftheyrelypurelyonwelfarepayments.Investmentallowspeopletodiversifytheirincomestreams,protectagainstlossofasinglesourceofincome,andmaintainahigherstandardoflivinginretirement(ASIC,2017a).

Diversificationisaboutanindividual investormanagingtherisk/rewardtrade-offoftheirinvestmentportfoliotoachievemoreconsistentreturnsovertime,bylimitingtheirexposuretoanysingleasset(ASIC,2017a).Thisconceptofriskmanagementappliestoanindividualwithlabourincomewhoalsoholdsinvestmentpropertyanddividend-payingshares.Thefactthatthisindividualhasmultiplesourcesofincomemeans thattheymaybelessimpactedby aneventsuchasjobloss.

Atthesametime,aninvestorthatspreadstheirfundsacrossawiderangeofassetswilllimittheimpacttotheirportfoliofromthelossofvalueofanyoneasset.Thatis,bydiversifying,individualscanreducethechancethatthevalueoftheirentireinvestmentportfolioisimpactedbya singleevent.

1.3 The value of a well-functioning financial exchange Financialexchangesplayanumberofimportantrolesintheeconomy,includingbeinganinformationsourceandaidingefficientpricediscovery,andaplatformofexchange.Theyprovideindividualswithaccesstocapitalmarkets,assistwithensuringresourcesareallocatedefficiently,givebusinessesacosteffectivewaytoraisecapital,andallowgovernmentstoincreasethedepthofthebondmarket.

Theyalsohaveinstitutionalvalues, providingaframeworkandsetofguidelinesforensuringfinancialtradingisdoneinawaythatmanagesindividuals’riskandstabilityofthesystem.

Australiahaswelldevelopedfinancialmarketswhichofferinvestorsaccessto awiderangeofinvestmentproducts. Thesemarketshavedemonstratedeconomicresilienceandadaptability, makingAustraliaasafe,low-riskenvironmentinwhichtoinvest(Austrade,2017).Morebroadly,theAustralianfinancialservicessectoralsocontributestoeconomicgrowth.In2015,itcontributed$140billiontoGDP(TheTreasury,2016).

Individualscanparticipateinfinancialmarketstodiversifytheirincome,managetheirrisks,andaccumulatewealth.Individualsarealsoabletoaccessinvestmentopportunitiesthattheymayotherwisebeunawareoforunabletoaccess.Forexample,sophisticatedfinancialproductssuchasoptionsandhybridsecuritiesaremadeaccessibleto individualsthroughfinancialmarkets.

Byprovidingtransparencyaroundthespectrumofinvestmentoptionsandthehistoricalreturnandriskofeachoption,exchangesfacilitatedecision-makingbyinvestors.Thiscancontributetoimprovingtheallocationofcapital,asfundsarelikelytobedirectedtotheirmostproductiveuse.Improvingtheproductivityofcapitalcontributestoeconomicgrowth (Musonera,2008).

Exchangesalsocreatesubstantialvalue forbusinesses.Benefitsincludeaccesstoawiderpoolofinvestors,increasedabilitytoraiseequity,andreducedtransactioncostsofcapitalraisingachievedthrough aplatform.

ASX Australian Investor Study | 2017

13

ASX Australian Investor Study | 2017

14

In2016,theAustralianequitymarketgenerallyoutperformedotherdevelopedequitymarketsglobally(RBA,2017a).Atthetimeofwriting,theS&P/ASX200wasatitshighestlevelsincepriortotheglobalfinancialcrisis.Tradingvolumeshaveincreased23%overthe12monthstoMarch,andcontinuetogrow(ASX,2017a).Thedomesticequitymarketcapitalisation isatahistorichigh,reaching$1.8trillion inMarchthisyear(ASX,2017b).

Atthesametime,significantglobaleventshaveinfluenceddomesticmarketsoverthelastyear.TheannouncementsofdecisionsbyBritishvoterstoleavetheEuropeanUnionandbyUSvoterstoelectPresidentTrumpcoincidedwithincreasedtradingvolumesonASX.

Thesetwo,largelyunexpected,developmentsarekeyexamplesofa globalenvironmentcharacterisedbysignificantuncertainty.Geopoliticaldevelopmentsarelikelytocontinueto beafocusforinvestorsinthenear future(InvestmentMagazine,2017).

Theworldofinvestingisfastpacedandrespondstochangequickly.Astheunderlyingenvironmentevolves,sotoo dotheinvestmentspeoplechooseand thewaytheyinvest.

Megatrendssuchasthelowinterestrateenvironment,policychanges,digitalinnovation,anddemographicshiftsareinfluencingthewaythattheAustralianinvestmentmarketoperates.

Thischapteroutlinesthesechangesandhowtheywillinfluenceinvestors’approachtoinvesting.

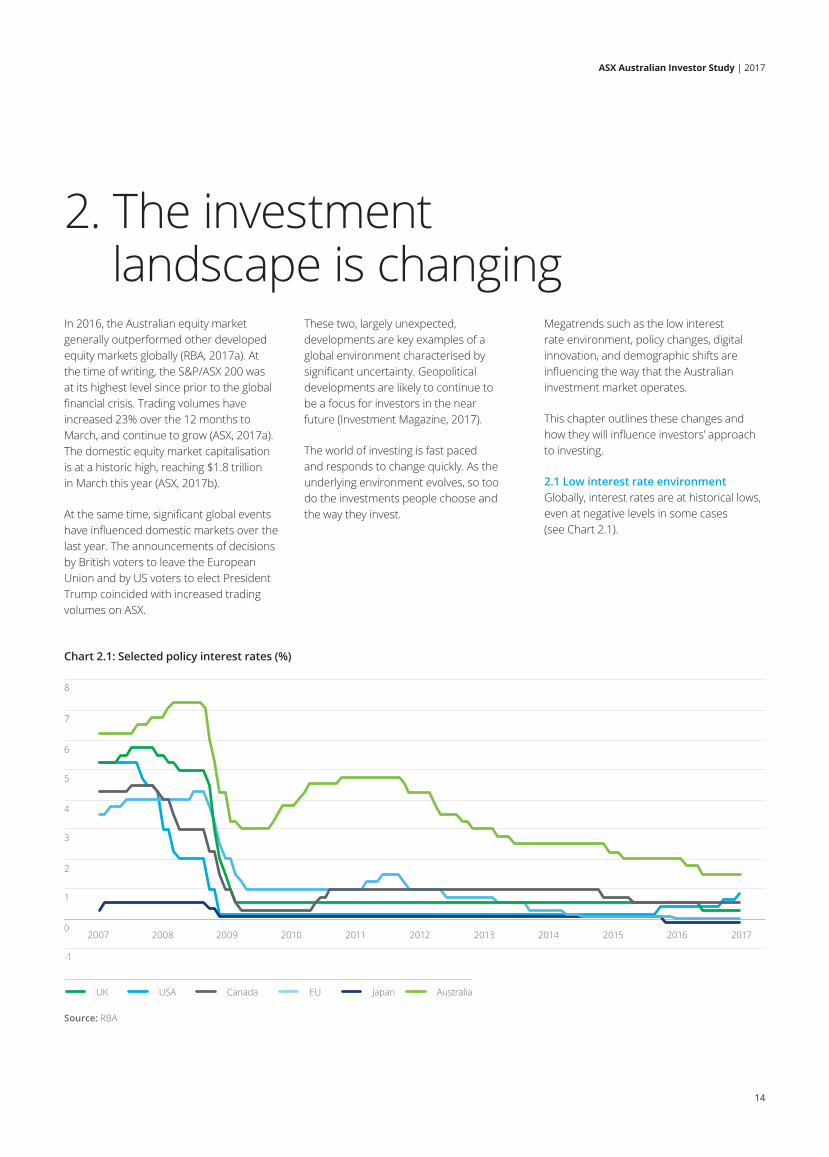

2.1 Low interest rate environment Globally,interestratesareathistoricallows,evenatnegativelevelsinsomecases (seeChart2.1).

2.Theinvestment landscapeischanging

0

1

2

3

4

5

6

7

8

-1

Chart 2.1: Selected policy interest rates (%)

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

UK USA Canada EU Japan Australia

Source: RBA

ASX Australian Investor Study | 2017

15

SincetheGFC,Australianmonetarypolicyhasbeeneasedinanattempttostimulategrowth,leadingtoaperiodofsustainedlowinterestrates.Priortothe2008financialcrisis,Australia’scashrateaveraged6.4%.Since2008thishasdroppedto3.1%,andiscurrentlyatarecordlowof1.5%.Chart2.2showsthatinterestratesonbanktermdepositshavefallensignificantlyoverthelast20years,reducingthereturnoncashinvestments.

Thelowinterestrateenvironment hastwomainimplicationsforinvestors.

Firstly,lowinterestrateshaveanimpactonreturnsacrossarangeofinvestments,notjustcash.CreditSuisseanalysisshowsthatlowinterestratesareassociatedwithlowfutureequityreturns(Buttonwood,2013).Asaresult,investorsmaybeforcedtoseekoutriskierinvestmentsinordertomaintainthereturnstheyareusedtointheirportfolios(Yeates,2016).

Secondly,lowerreturnsmeanthatfeesasaproportionofreturnsarehigher–essentiallyithasbecomemoreexpensivetoinvest.Therefore,investorsmayseekout low-feeinvestmentopportunities,forexampleinexchangetradedinvestments(suchasExchangeTradedProducts)ratherthanunlistedmanagedfunds.Alternatively,someinvestorsmayturntofinancialadvicetohelpthemnavigatethisnewenvironment.

2.2 Policy change TheAustralianfinancialsystemhasbeensubjecttoextensivereviewoverthepastfewyears.Whiletheheadlineshavebeendominatedbybankingsectorregulation,Australianpolicymakershavebeenmorewidelyfocused,withinitiativesthathaveimplicationsforfinancialadvisers,recipientsoffinancialadvice,andinvestors.

Opportunitiesandchallengeshavebeencreatedforbothinvestorsandfinancialadvisersthroughthesereforms.Achangingpolicylandscapecreatesuncertaintyandinvestorsmayturntoprofessionalstohelpthemnavigateit.Conversely,someofthesereformsaimtoempowerinvestorsandimprovefinancialliteracy,andthereforeadvisersmaybeusedlessbyinvestorsorindifferentwaystointhepast.

Akeystreamofreformhasaimedtoimprovethequalityofadviceandfacilitateaccesstofinancialadvice.TheFutureofFinancialAdvice(FoFA)legislationwasintroducedin2012andmandatedin2013,withaspectsofitrefinedin2016.FoFAaimedtoimprovethequalityofadvicewhilebuildingtrustandconfidenceinthefinancialadviceindustrythroughreducingconflictsofinterestandbetteraligningtheinterestsoftheadviserwiththeclient.Atthesametime,thereformsalsoaimedtoincreasetheavailabilityoflow-costsimpleadvicetomakefinancialadvicemoreaccessibletothepublic(Treasury,2010).

0

2

4

6

8

10

12

14

16

18

Chart 2.2: Australian banks' term deposit rates (% per annum)

1982

Source: RBA

Notes:Averagesofthefivelargestbanks'rateson$10,000termdeposits,exceptpriortoApril2001,whentheaveragesareforthefourlargestbanks.

1986 1990 1994 1998 2002 2007 2011 2013

1month 3months 6months 1year 3years

ASX Australian Investor Study | 2017

16

The2014FinancialSystemInquiry(FSI)alsorecommendedfurtherreformstostrengthenconsumeroutcomes,andhadaviewthatthecurrentframeworkwasnotsufficienttodeliverfairtreatmenttoconsumersaroundtheperformanceoffinancialproductsandservices.Inparticular,theFSIidentifiedaneedtoaddressshortcomingsindisclosureand financialadvice.

TheGovernment(2015)respondedto theFSIandcommittedtoanumberofreforms,including:

• Raisingthestandardsoffinancialadvisersbyintroducinglegislationwhichprovidesaprofessionalstandardsframework;

• Improvingthecustomerfocusoffinancialproductdesignandmarketbyintroducinglegislationtomakeissuersanddistributorsoffinancialproductsaccountablefortheirofferings;

• DevelopinganewproductinterventionpowerfortheAustralianSecurities&InvestmentsCommission(ASIC)thatcouldbeusedtomodifyproductsorremoveharmfulproductsfrom themarket;and

• Enablinginnovativedisclosureforfinancialproductsbyintroducinglegislationtofacilitategreater useoftechnologyinfulfilling disclosurerequirements.

Morebroadly,ASIChasfocuseditssupervisoryeffortsonconcernsaroundconductandculture,inthecontextofconsumerandinvestorprotectionandmarketintegrity.Thebehaviourof“gatekeepers”–suchaspromotersofinvestmentproducts–willbepaidparticularattention.Investorresponsibilityremainsa“cornerstone”offinancialmarkets,andimprovingdisclosureforconsumersisa keygoalfortheindustryandregulators.

Suchreformsareaimedatimprovingconsumerprotectioninfinancialmarkets.Theywillimpactthewaythatinvestorsreceivefinancialproductinformationandobtainfinancialadvice,andcouldencourageindividualstoinvest,aswellaschangingwhatproductstheychoosetohold.Theaimofthereformsistoimproveinvestorconfidenceinfinancialmarketsandtoincreasetrustin,andaccessibilityof,financialadviceinAustralia.Someoftheseinitiativesmayhelpaddresssomeofthebarrierstoindividualsseekingfinancialadvice(Section4.2).Ontheotherhand,thestricterrequirementsaroundqualificationsoffinancialadvisersandapproachtoprovidingadvicecouldhaveimplications forthesupplyoffinancialadvisersand thepricetheychargeforadvice.

Otherdevelopmentshavesoughttoimproveinvestoraccesstoinvestmentproducts.Forexample,theAsiaRegionalFundsPassport(ARFP)establishesamultilateralframeworktofacilitatecrossbordermarketingoffundsacrosscountriesinAsia.TheARFPisexpectedtocommencebytheendof2017,andwillmeanthatlicencedmanagedfundmanagersareabletotradeacrossnotjustAustralia,butalsoNewZealand,Singapore,theRepublicofKorea,Japan,Thailand,andthePhilippines(APEC,2017).

ThiswillprovideinvestorswithgreateraccesstoinvestmentoptionsintheAsiaregion,andshouldenablegreaterinvestmentflowsbetweenparticipatingcountries.Theincreasedcompetitionfrominternationalexposurecouldalsomeanthatlocalfundmanagersbecomemorecompetitive,increasingefficiencyacross thefinancialmarket.

TheParliamentrecentlypassedlegislationtoenablesmallandmediumbusinessestoseekcrowd-sourcedequityfunding.Thelegislationwillallowunlistedentitiestoadvertisetheirbusinessplansonlicensedcrowdfundingportals.Thiswillopenthemarketuptoretailinvestors,whereitwaspreviouslyonlyavailableto‘sophisticatedinvestors’,andsetsoutvariousinvestorprotectionprovisionsincludinganinvestorcapof$10,000ayear.

ASX Australian Investor Study | 2017

17

Thisreformwillfurtherexpandtheuniverseofinvestmentproductsavailabletoinvestors,andmayhaveimplicationsforinvestorsallocatingmoreoftheirportfoliooutsideoftraditionalinvestments.Italsobroadensthescopeofinformationandproductsthatadvisersneedtobeacross.

Overallthesepolicychangesarelikelytoofferinvestorsmorechoiceandvariabilityinhowandwhattheychoosetoinvestin.

2.3 Digital innovation Digitalinnovationisoccurringatanincreasinglyrapidpace,facilitatingmoreefficienttrading,fasterandbetteraccesstoinformation,andcheaperandwideraccesstoglobalmarkets.

MobilephonesarebeingusedtotradesharesinAustraliamorethaneverbefore.Infactin2015,6outof10Australianonlineinvestorsusedamobiledevicetotrade(InvestmentTrends,2015).Onlinetradingplatformssuchasnabtrade,CommSec,WestpacOnlineInvesting,andHSBCOnlineShareTradingallowcustomerstousetheirphonestobuyandsellshares,viewtheirportfolios,createwatchlists,andobservemarketmovements.Accordingtothissurvey,onlinetradingplatformsarethemostfrequentlyusedtradingmethodamongstAustralianinvestors(seeSection4.3).

Thesedevelopmentsarechangingthewaythatinvestorsconducttheirtradingactivity,andalsohowtheyaccessadvice.TheefficiencyofthesedigitaltechnologiesandAustralians’propensitytoadoptsuchinnovationsmayleadtoashiftawayfromuseofmoretraditionalmethodsoftradingandadvice.

Australiansarestrongadoptersoftechnology,forexample,86%ofAustralianhouseholdsownsmartphones(DAE,2016a),makingAustraliathesecondmostconcentratedsmartphonemarketintheworld(SMSGlobal,2016).Thisisoftenusedasameasureofopennesstotechnologicaladvance,andmayimplythatdomesticinvestorsaremorewillingtoadoptfinancialtechnology(‘fintech’)innovationssuchasroboadvice.

Roboadviceusescomputingprograms togeneratecustomisedinvestmentadvicebasedoninformationaboutanindividual'sportfolio.Thiscanbeanattractive,lowercostalternativetoinperson professionaladvice.

However,thereisuncertaintyamongstsomeinvestorsastothereliabilityoftheadvicegenerated,andusingfinancialadviserswillremainanimportantpartoftheinvestmentprocess.Furthermore,whileroboadvicemaybeabletomoreefficientingeneratingtransactionaladvice,andrecommendsoundinvestments,itreliesontheinvestorknowingwhatinvestmentsupporttheyneed.RoboadviceisdiscussedinmoredetailinSection4.3.2.

Withdigitalinnovationcomesanewconcern:cybersecurity.Astheeconomybecomesmorereliantoncomputingsystems,theimportanceofprotectingthosesystemsfromattackincreases.Cybercrimeisnowthesecondmostreportedtypeofeconomiccrimeinbusiness(behindassetmisappropriation)andisrising(Layer8Security,2016).Thistrendcouldslowthepaceofadoptionofnewtechnologies.

Overall,digitalinnovationislikelytohavemoreofanimpactonthemethodsoftrading,andthewaysinvestorschoosetoaccessadviceabouttheirinvestmentsthanonthetypesofinvestmentstheyhold.

2.4 Demographic shifts Australia’spopulationisageing.TheproportionoftheAustralianpopulationaged65andoverhasalmostdoubledfrom8%in1964to15%in2016(AIHW,2015&ABS,2017b).Decliningfertilityandfallingmortalityratesmeanthatthistrendisexpectedtocontinue,andthenumberofpeopleagedover65willagaindoubleby2055(Treasury,2015a).

Onaverage,olderAustraliansarewealthierandinvestmorethanyoungerAustralians.4 Thisgroupisbecomingalargershareofthepopulation,andtheyhavedifferentpreferencesaroundhowtheyreceiveadvice,executetheirtrades,andwhat theychoosetoinvestin.

TheageingpopulationhasimportantimplicationsfortheriskprofileofAustralianinvestors.AstheGovernoroftheReserveBankofAustraliaputit,'Older workers tend to become more risk averse when it comes to investment decisions…' (Lowe,asquotedinPickering,2016).RiskattitudesinAustraliawillchangeasthepopulationages,andthiswillhaveabigimpactoninvestmentbehaviour.However,resultsfromthisstudyfindtheopposite,atleastinthecontextofinvesting(Chapter5).Eitherway,theageingpopulationwillchangetheoverallmixofinvestmentsheldbyAustralians.

4Averagehouseholdwealthforthoseaged65andoverwas$900,000in2012,and$710,000forthoseaged35-55(GrattanInstitute,2014)

ASX Australian Investor Study | 2017

18

Intheshortterm,anageingpopulationcouldcounteracttheeffectofdigitalinnovationonthewayinvestorsobtainadvice,asolderpeoplearemorelikelytousein-personfinancialadvicethannewtechnologiessuchasroboadvice.However,thistrendcouldlessenasthecurrentgenerationofyoung,technology-savvyinvestorsage.

TheageingpopulationshouldmeanthequantityofinvestmentandtradinginAustraliawillincrease.OlderAustralianshaveexperiencedthelargestincreaseinwealthofanyagegroupoverthepastdecade.Householdsaged65andoverhaveexperienced2.7%annualgrowthinwealthoverthepastdecade,while55-64yearoldhouseholdshaveexperienced1.9%annualgrowthoverthesameperiod(GrattanInstitute,2014).

Food for thought

• Do you have a good understanding of how these changes will impact investors?

• Is your business model geared towards supporting investors as the investment environment and their preferences change?

DemographicchangesintheAustralianpopulationshouldseethetypesofinvestmentsindividualsholdchange,andalsothewaytheyobtainadvice.Forexample,findingsfromthisstudyshowthatolderpeoplearemorelikelytorelyontheirownresearchregardinginvestmentthanyoungpeople.Thissuggeststhatasthepopulationages,useoffinancialadvicedecreases(astheyoungercohortwhoarenotconfidentenoughtorelyontheirownresearchmatureandgainconfidence).Alternativelyitcouldmeanthatfinancialadvisersadapttheirroletobecomelessprescriptive,morelikeasoundingboard totestideaswithorageneratorofideas oninvestmentoptions.

ASX Australian Investor Study | 2017

19

Investor profiles

Next generation Wealth accumulators Retirees

Top 3 financial goals 1. Accumulatingwealth

2. Savingforahomedeposit

3. Savingfortravel

1.Planningforretirement

2.Accumulatingwealth

3.Supplementingcurrent orfutureincome

1.Planningforretirement

2.Supplementing currentorfutureincome

3.Accumulatingwealth

Risk appetite 81%areseekingguaranteed orstablereturns

67%areseekingguaranteed orstablereturns

60%areseekingguaranteed orstablereturns

Return expectations Expectonaveragea8.2% returnontheirinvestments

Expectonaveragea9.2% returnontheirinvestments

Expectonaveragea8.0% returnontheirinvestments

Mix of investments • 44%holdcash

• 31%holdshares

• 25%holdinvestmentproperty

• 22%holdotheron-exchangeinvestments,includingderivatives

• 53%holdcash

• 51%holdshares

• 42%holdinvestmentproperty

• 25%holdotheron-exchangeinvestments,includingderivatives

• 68%holdcash

• 58%holdshares

• 26%holdinvestmentproperty

• 18%holdotheron-exchangeinvestments,includingderivatives

Use of financial advice 37%usefinancialadvice 44%usefinancialadvice 52%usefinancialadvice

Top 3 reasons for using financial advice

1.Obtainadvicetailoredto theirpersonalcircumstances

2.Getinvestmentideas

3.Helpthemdiversifytheirportfoliosandminimiserisk

1.Obtainadvicetailoredto theirpersonalcircumstances

2.Helpthemdiversifytheirportfoliosandminimiserisk

3.Gainaccesstoinvestments theywouldotherwisenot beawareoforabletoaccess

1.Obtainadvicetailoredto theirpersonalcircumstances

2.Helpthemdiversifytheirportfoliosandminimiserisk

3.Helpthemnavigatetheadministrativeandtaxrequirementsofinvesting

Use of robo advice 15%woulduseroboadvice,28%wouldnot,(therestareunsure)

13%woulduseroboadvice,29%wouldnot(therestareunsure)

4%woulduseroboadvice,41%wouldnot(therestareunsure)

Trading methods of investors that have transacted in the past 12 months

1.42%usedanon-advice brokeroronline tradingplatform

2.36%usedanadvice orfull-servicebroker

3.24%usedafinancialplanner

1.65%usedanon-advice brokeroronline tradingplatform

2.21%usedanadvice orfull-servicebroker

3.18%usedafinancialplanner

1.69%usedanon-advice brokeroronline tradingplatform

2.21%usedanadvice orfull-servicebroker

3.13%usedafinancialplanner

Notes:‘Nextgeneration’isdefinedas18-24yearoldinvestors;‘Wealthaccumulators’isdefinedas25-59yearoldinvestors;and‘Retirees’isdefinedtobeinvestorsaged60andover.

ASX Australian Investor Study | 2017

20

3.Whoisinvesting?

ASX Australian Investor Study | 2017

21

Three-fifths(60%)ofAustralianadultsdirectlyholdinvestmentsofsomesort(includingthosenotavailableonafinancialexchange)outsideoftheirinstitutionalsuperannuationfund.Thischapterexamineswhotheseinvestorsare,aswellasprovidingsomeinsightintowhytheremaining40%ofAustralianadultsdo notinvest.

Beforedivingintothedetail,thischapterbeginsbyreviewingsomeofthehigh-leveltrendsininvestmentownership.

3.1 Changes in investment ownership in Australia Ownershipofon-exchangeinvestmentshasremainedbroadlyconsistentsincethe2014study.Therehasbeenanincreaseinyounginvestorshowever,whohavebeenengagingmorewithon-exchangeinvestments.Theproportionof18-24yearoldswhoholdon-exchangeinvestmentshasdoubledinthepastfiveyears.Therehasalsobeenanincreaseininternationalshareownership inthistime.

Around37%oftheadultpopulation heldon-exchangeinvestmentsasofFebruary2017,upslightlyfrom2014.Ownershipwashigheramongmenthanwomen,with44%and31%holdingon-exchangeproductsrespectively.Therateofon-exchangeinvestmentownershiphasbeenfairlystableoverthepastfiveyears,followingasignificantdeclineafter theearly2000s(Chart3.1).

10%

20%

30%

40%

50%

60%

Chart 3.1: Ownership of on-exchange investments, proportion of adult population

Notes: 1986(n=1304),1988(n=2637),1991(n=3018),1994(n=3253),1997(n=1174),2000(n=1200),2002(n=2401),2004(n=2402),2006(n=2405),2008(n=2400), 2010(n=2400),2012(n=2000),2014(n=4009),2017(n=4000)

01985

9% 9%

16%

21%

34%

52%50%

53%

47%

41% 42%

38%36%

37%

1990 1995 2000 2005 2010 2015 2020

ASX Australian Investor Study | 2017

22

3%

4%4% 4%

5%

8%

6% 6%

7%

Thesignificantincreaseinownershipinthe1990smaybepartlyexplainedbythelargeinitialpublicofferings(IPOs)overtheperiod.Forexample,theCommonwealthBankin1991,Qantasin1993,andTelstrain1997(RBA,1997).TheGlobalFinancialCrisis(GFC)in2007-08shookinvestorconfidenceglobally,andsomeinvestorsmaystillberecovering.Atthesametime,recordlowinterestrateshaveledtoincreasedpropertyinvestmentandhighpropertypricesincapitalcities(ABS,2017c).

ASXdataindicatethat,sincethe laststudy(in2014),thenumberofETFs onissueinAustraliahasincreasedby61%,to203.Overthesameperiod,theproportionoffundsundermanagementallocatedtoglobalequityhasincreased by7.7percentagepointsto39.2%.

Ownershipofinternationalshares,boughtdirectlythroughoverseasexchanges,hasreturnedtoitspre-GFCpeak(Chart3.2).Thismaypartlyreflectimprovedappetiteforoverseaslistedinvestmentsaswellasbetteraccess.However,investingdirectlyininternationalsharescanbeexpensive,andmanyindividualsinsteadinvestthroughmanagedfundsorexchangetradedfunds(ASIC,2016a).5

1%

2%

4%

5%

3%

6%

7%

8%

9%

Chart 3.2: International share ownership, proportion of adult population

Notes: 2017(n=4000)

0%2000 2001 2003 2005 20072002 2004 2006 2008 2009 2010 2011 2012 2013 2015 20172014 20182016

5Againstthisbackground,itispossiblethatsomerespondentsmayhavemisinterpretedthequestionandareinpartreportinginternationalsharestheyholdindirectly,forexample,throughexchangetradedproducts(ETPs).

ASX Australian Investor Study | 2017

23

3.1.2 Change in investor profile YoungAustraliansareinvestingmore.Between2012and2017theproportionofinvestorsagedbetween18and24yearsoldthatholdon-exchangeinvestmentshasdoubledtojustover20%,andtherehasbeena15percentagepointincreaseintheproportionof25-34yearoldsinvestinginon-exchangeinvestmentsoverthesameperiod(Chart3.3).Theagedistributionofinvestorshasbecomeflatter,theproportionofeachagerangeinvestingiseveningout.

Theshareofadultsthatownon-exchangeinvestmentshasbeenbroadlyunchangedformoststatesandterritoriesoverthepastdecade(Chart3.4).On-exchangeinvestmentrateshavehistoricallybeen(andcontinuetobe)highestinNewSouthWales(42%in2017),theAustralianCapitalTerritory(40%),andWesternAustralia(40%),andlowerintheNorthernTerritory(26%),Queensland(32%),and Tasmania(33%).

Notes: 2017(n=4000)

10%

20%

30%

40%

50%

60%

Chart 3.3: Age profile of on-exchange investors, proportion of adult population

02008 2010 2012 2014 2016

18-24 25-34 35-44 45-54 55-64 65-74 75+

ASX Australian Investor Study | 2017

24

*DataareunavailableforACTin2008andNTin2010.

Notes:2017(n=4000)

Notes:2017(n=4000)

10%

20%

30%

40%

50%

60%

Chart 3.4: Incidence of on-exchange investors by location, proportion of adult population

0

2008 2010 2012 2014 2017

WAVICTASSAQLDNT*NSWACT*

In2017justover40%ofadultslivinginmetropolitanareaswereon-exchangeinvestorscomparedto32%ofadultsinregionalareas (seeChart3.5).Theshareofadultsincapitalcitiesthatheldon-exchangeinvestmentshasreturnedtoitsdecadehigh.

25%

30%

35%

40%

45%

Chart 3.5: Incidence of on-exchange investors by metro/regional split, proportion of adult population

20172010 2012 20142008

Capitalcities Regionalareas

ASX Australian Investor Study | 2017

25

Notes:2017(n=605)

Investorsusingthismethod Investorsnotusingthismethod

3.1.3 Changes in investor behaviour Non-advicebrokersandonlinetradingplatformshaveremainedthepreferredtradingmethodforinvestors,andhavebecome morepopularsince2014(Table3.1).

Table 3.1: Changes in method of trading, proportion of on-exchange investors who have traded in the last 12 months

Method 2014 2017

Non-advice broker or online trading platform e.g. nabtrade

An advice or full-service broker e.g. Bell Potter

Through a financial planner/adviser

Purchased directly via a prospectus of a company listed on a stock exchange

Through an employee share scheme

Other

58% 65%

15% 22%

16% 17%

17% 11%

8% 4%

4% 1%

Therehasbeenanincreaseintheshareofinvestorsusingbothnon-advicebrokersandtradingplatforms,andfull-servicebrokers comparedto2014.Therehasbeenadeclineintheshareofinvestorsdirectlypurchasinglistedinvestmentsthroughacompanyprospectusandemployeeshareschemes.Digitalinnovationislikelyinfluencingthistrend.Technologicaladvanceshavemadeiteasierformoreinvestorstodirectlyparticipateintradingthroughonlineplatformssuchasnabtrade.

Whilechangestothesurveymeanthatdirectcomparisonwiththe2014resultsarenotpossible,manyinvestorsinon-exchangeinvestmentscontinuenottouseadvicefromprofessionals(Chart3.6).Otherinvestorsusemorethanoneformofadvice;forexample,13%ofinvestorsselectedboth‘financialplanner/adviser’and ‘ownresearch’.

Food for thought

• How is your business responding to the growth in numbers of young investors and self-directed investors?

• Do you promote the use of specific investments, like exchange-traded products, to facilitate easy access to international markets?

ASX Australian Investor Study | 2017

26

Chart 3.6: Investment advice sought by investors, proportion of on-exchange investors

2017

2014

0%

0%

10%

10%

20%

20%

30%

30%

40%

40%

50%

50%

60%

60%

70%

70%

Ownresearch

Personalnetwork(Friends,Family,Colleague)

Financialplanneroradviser

Reading/Listeningtoexpertcommentators

Familyandfriends

None/Donotseekadviceaboutinvestments

Accountant

Financialplanners/advisers

Lawyer

Stockbrokerswhoprovideadvice

Solicitors/Lawyers

Other

Wealthmanagementadvisers

Other

Fullserviceoradvicestockbroker

Accountants

Notes:2017(n=1494)

ASX Australian Investor Study | 2017

27

3.2 The profile of the Australian investor Three-fifths(60%)ofAustralianadultsdirectlyholdinvestmentsofsomesort(includingthosenotavailableonafinancialexchange)outsideoftheirinstitutionalsuperannuationfund.Thissectionexaminesbothon-exchangeandotherinvestors, whotheyareandhowtheyinvest.

3.2.1 What investment structures do investors use? TherearefourmainstructuresthroughwhichAustraliansholdinvestments:

Figure 3.1: Investment vehicles used, proportion of adult population

Investments

ShareoftheAustralianadultpopulationholding:

Investmentsinselfmanaged

superannuationfunds*

Investmentsincompanystructures

Investmentsinfamilytrusts

Investmentsinapersonalcapacity

60% 51% 15% 10% 7%

*Figureislikelytobeoverstatedduetosamplingerror.TheATO’sSMSFstatisticalreport–December2016indicatethataround 6%ofAustralianadultsaremembersofSMSFs

Note: Optionsdonotsumto100%becausemanyinvestorsholdinvestmentsthroughmorethanonestructure;2017(n=4000)

• Investmentsheldintheirpersonalcapacity,eitheraloneorinjointnames

• Investmentsheldinacompanystructurewheretheyareadirectorofthecompany

• Investmentsheldinafamilytrust

• Investmentsheldinaself-managedsuperannuationfund(SMSF),wheretheyareatrusteeormemberofthefund.

Aroundhalf(51%)ofAustralianadultschoosetoinvestintheirpersonal capacity(Figure3.1).

ASX Australian Investor Study | 2017

28

Notes: n=4000

10%

20%

30%

40%

50%

60%

70%

Chart 3.7: Use of investment structures by age, proportion of adult population

0

18-24 25-34 35-44 45-54 55-64 65-74 75+

Company(7%)SMSF(15%) Familytrust(10%)

3.2.2 Which Australians are investing? TheproportionofAustralianswithpersonalinvestmentsincreaseswithage,whileuse ofotherstructurestypicallyreflectstheir usefortaxplanningandother purposes(Chart3.7).

Ofinvestorsholdinginvestmentspersonally,younginvestorsaretheleastprominent(Chart3.7).However,investingisbecomingmorecommonamongyoungpeople(Section3.1.2).

However,theindustrymaynotbeadaptingtothepreferencesofthisgroupquicklyenough.Younginvestorsaremoredigitallysavvy,andwhiletheadventofdigitalwealthadvice(i.e.roboadvice)offersopportunitiesforbothinvestorsandfinancialadviserstotakeadvantageofdigitalinnovation,take-upgenerallyhasbeenlimited(Section4.3.2).Thisismostlyduetoalackofknowledgeabouttheseproducts,whichsuggeststhattheinvestmentindustrymaynotbedoingenoughtoeducateinvestorsaboutthem(andraisesquestionsaboutwhethertheseinnovationstrulymeetinvestors’needs).

Atthesametime,andcontrarytoconventionalexpectations,younginvestorsalsoappearmoreriskaversethanolderinvestors–with4in5younginvestorspreferringguaranteedorstableinvestmentreturns(Section5.2).Financialproductdevelopersandfinancialadviserscouldseektobettertailortheirproductsandadvicetomeetthisneed,forexample,byconsideringcapital-protectedproducts.

Thecharacteristicsofyounginvestors arediscussedfurtherinSection3.2.3, andinBoxA.

Personal(51%)

ASX Australian Investor Study | 2017

29

Theproportionoffamilytrustinvestorsdeclineswithage:17%of25-34yearoldshaveafamilytrust,butjust4%ofthose65andabovedo.Thissuggeststhatfamilytrustsare,insomecases,beingusedasameansofachievingamoretaxeffectiveoutcomeforthefamilybyredistributingincometofamilymembersthathavelowerincomes,suchasyoungerfamilymembers.

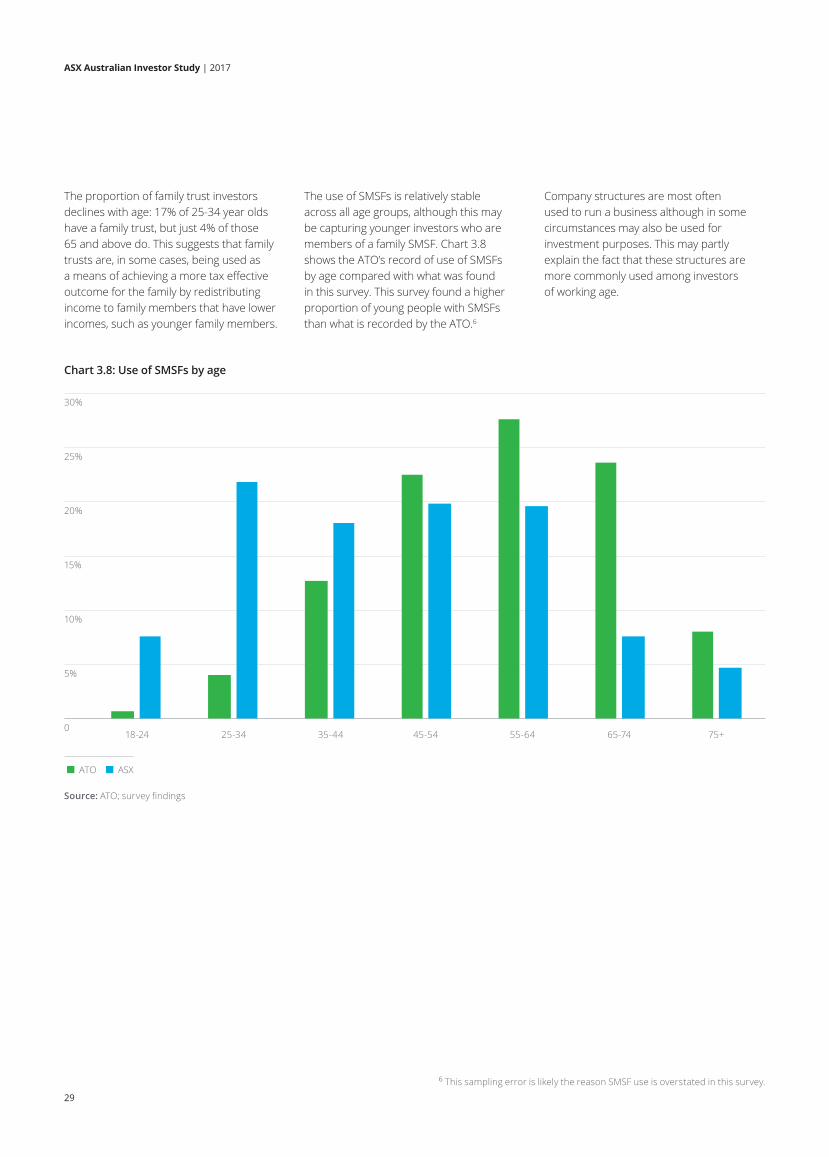

TheuseofSMSFsisrelativelystableacrossallagegroups,althoughthismaybecapturingyoungerinvestorswhoaremembersofafamilySMSF.Chart3.8showstheATO’srecordofuseofSMSFsbyagecomparedwithwhatwasfoundinthissurvey.ThissurveyfoundahigherproportionofyoungpeoplewithSMSFsthanwhatisrecordedbytheATO.6

Source: ATO;surveyfindings

5%

10%

15%

20%

25%

30%

Chart 3.8: Use of SMSFs by age

018-24 25-34 35-44 75+45-54 55-64 65-74

ATO ASX

6ThissamplingerrorislikelythereasonSMSFuseisoverstatedinthissurvey.

Companystructuresaremostoftenusedtorunabusinessalthoughinsomecircumstancesmayalsobeusedforinvestmentpurposes.Thismaypartlyexplainthefactthatthesestructuresaremorecommonlyusedamonginvestors ofworkingage.

ASX Australian Investor Study | 2017

30

3.2.3 Next generation Theproportionof18-24yearoldindividualsinvestinghasdoubledinthepastfiveyears.AnannualsurveyofmillennialattitudesbyDeloitteshowsthatwhilein2015and2016,millennialswerepessimisticaboutthefuture,andgettingmoreso,thistrendhasflippedin2017andmillennialsarenowcautiouslyoptimisticaboutthefuture(Deloitte,2017).7Astheiroverallconfidenceintheeconomycontinuestoimprove,thismayopenthedoortomoreyoungpeoplebeingopentoinvesting.

Nonetheless,despitethisrecentgrowthinparticipationtheyremainunderrepresentedasinvestors;thisagegrouprepresentsaround12%ofthetotalpopulationbutunder9%ofallinvestors.

Againstthisbackground,itisusefultounderstandthecharacteristicsofindividualswithinthisagegroup.Thissectionidentifiessomeofthecharacteristicsofthese younginvestors.

MostyounginvestorsareatleastYear12graduates,withalargesharebeingtertiaryeducated(Chart3.9).

Chart 3.9: Highest education qualification, 18-24 year old investors

Year12/Higherschoolcertificate

Primaryschool

Tradescertificate/Diploma

Year10/Schoolcertificate

UniversityDegree

PostGraduateDegree

Don'tknow/Unsure

0% 5% 10% 15% 20% 25% 35%30% 40%

Notes:n=207

7TheDeloitteMillennialsSurveydefinesamillennialassomeoneborninorafter1982.Thiscapturesawidercohortthanthe18-24year oldsreferredtointhissectionas‘younginvestors’.

ASX Australian Investor Study | 2017

31

Chart 3.11: Top employing industries, 18-24 year old investors

Chart 3.10: Employment status, 18-24 year old investors

Otherservices

Retailtrade

Educationandtraining

Professional,scientific,andtechnicalservices

Administrativeandsupportservices

Artsandrecreationservices

Accommodationandfoodservices

Rental,hiring,andrealestateservices

Healthcareandsocialassistance

Construction

Transport,postal,andwarehousing

0% 2% 4% 6% 8% 12%10%

Notes:n=207

Notes:n=207

Inpaidemployment/self-employed Notinpaidemploymentorself-employed

Ofthoseyounginvestorsthatareinpaidemploymentorself-employed,mostworkinthetradeorprofessional servicesindustries(Chart3.11).

59%

41%

Mostinvestorsinthisagegroupareinsomekindofpaidemploymentorareself-employed(Chart3.10).

ASX Australian Investor Study | 2017

32

5%

10%

15%

20%

25%

Chart 3.12: Gross household income per year, 18-24 year olds

0 Lessthan $20,000

$20,000-$39,999

$40,000-$59,999

$60,000-$79,999

$80,000-$99,999

$100,000-$149,999

$150,000-$199,999

$200,000-$299,999

Over $300,000

Don'tknow /Unsure

Reflectingtheearlystageoftheirworkinglife,individualsinthisagegrouptypicallycompriselowerincomehouseholds. Onaverage,younginvestorshavehigherhouseholdincomescomparedtonon-investors(Chart3.12).

Notes: Totalinvestors(n=207);totalnon-investors(n=485)

Shareoftotalinvestors Shareoftotalnon-investors

ASX Australian Investor Study | 2017

33

10%

20%

30%

40%

50%

60%

Chart 3.13: Value of total household assets, 18-24 year olds*

0

Asindividualsmatureandtheirincome andwealthgrows,theywillbemorelikely toinvest.Nonetheless,thisdoesnotmeanthat18-24yearoldindividualscouldnotinvestmoreatthisstage.Professionaladviserscanplayaroleineducatingyounginvestors.However,only37%ofyounginvestorsusefinancialadvice,compared to45%ofallinvestors(seeSection4.2).

Oftheyounginvestorsthatdonotuse anyprofessionaladvice,thetoptwomost citedreasonsweretheybelievedthat:

1. Advicewastooexpensiveforthem toobtain;and

2. Theirinvestmentwastoosmallto needadvice.

AccordingtoGeorgeLucas,managingdirectorofAcornsGrow,millennialsdo notunderstandtheimportanceofengagingwithfinancialprofessionals(Lucas,2017).Theytendtopreferonlineengagement,andwhiletheyarenotcurrentlylookingforstrictfinancialguidance,theywilllookformoreadviceastheygetolder.Itisimportantforadviserstoadapttodigitalplatformsnow,sothatmillennialswillbemorecomfortableseekingadvisersovertime.

WealthEnhancersPtyLtd,afinancialadvisoryfirmwithafocusonyoungerinvestors,hasfoundthatyounginvestorsarecostconscious–manyfeelthatadviceistooexpensive,particularlythosewithsmallerportfolios.BoxAcontainsfurtherviewsfromWealthEnhancersPtyLtd.

Under $100,000

$100,000- $299,999

$300,000- $499,999

$500,000- $749,999

$750,000- $999,999

$1,000,000- $1,999,999

$2,000,000ormore

Don'tknow /Unsure

*Excludesvalueofthefamilyhome,carandinstitutionalsuperannuationbalance

Notes: Totalinvestors(n=207);totalnon-investors(n=485)

Shareoftotalinvestors Shareoftotalnon-investors

Food for thought

• Does your business model cater for investors at all life stages?

• Are you developing low cost entry level products to cater for investors just starting out?

• How will you help educate young investors about the pros and cons of investing and of the value of professional financial advice?

Inlinewiththedistributionofhouseholdincomesacrossthisagegroup,younginvestorsaretypicallywealthierthan non-investors(Chart3.13).

ASX Australian Investor Study | 2017

34

Box A: Wealth Enhancers Pty Ltd

Wealth Enhancers is a financial advisory firm catering predominantly to younger investors. For their clients, getting value is front of mind and they are conscious of the cost of advice. Many feel that they may not have enough money available to invest to warrant getting advice on how to invest well.

Among those using advice, there are a wide range of financial goals. Some are saving for education, a wedding, starting a business, while others are looking for wealth accumulation or income replacement in order to start a family. However, for almost everyone, investment is about feeling more secure, having a buffer.

Wealth Enhancers considers there to be three main barriers to investing for Gen Y: a lack of confidence, negative prior experiences, and a misunderstanding as to the amount of money required to get started.

• Many young people are not confident in their ability to invest well, and for those who think advice is too expensive, this may not be easy to overcome

• Some young investors may have invested before, but were overly speculative, and subsequently lost money. This experience has been discouraging to them, and made them nervous to invest again

• Many Gen Y investors have a misconception that investment must be done with a large sum of money, and do not understand that they can start building their portfolio with small amounts

Advisers at Wealth Enhancers have also noticed that many Gen Y investors are open to the idea of borrowing to invest. At the same time, some are also using equity investments as a short term tool in order to save for a deposit and enter the housing market.

In Wealth Enhancers’ experience, robo advice has not been something that Gen Y investors have been well aware of. Wealth Enhancers have suggested robo advice as an alternative source of advice to those investors that are likely to value its cost-effectiveness.

ASX Australian Investor Study | 2017

35

3.2.4 The rise of SMSFs SMSFsallowinvestorstohavegreatercontrolovertheirsuperannuation,somethingthatmanyinvestorswant(seeChapter5).ThenumberofSMSFsinAustraliaisgrowingrapidly,andissettocontinuetodosointothefuture.InDecember2012,therewerearound491,000SMSFsinAustraliacomparedtoover585,000today(ATO,2017).MoreinvestorswilluseSMSFsinthefuture. Some30%ofinvestorsthatdonot currentlyuseanSMSFintendtoset oneupinthefuture.

Why do investors use SMSFs? SMSFinvestorshavelongtermgoals broadlyinlinewiththepurposeofsuperannuation–58%ofSMSFinvestorschoosesavingforretirementasagoal, and55%selectedwealthaccumulation.Chart3.14presentsabreakdownofthe topfivegoalsamonginvestorsthatuseSMSFs(respondentswereaskedtorank uptothreegoalsinorderofimportance).

ResearchbyAMPCapitalshowsthat 56%ofSMSFtrusteesestablishedtheirSMSFinanefforttohavemorecontrol overtheirinvestments,and32%establishedthemsothattheycouldchoosespecificsharestoinvestin(AMP,2017).

ThedesireforgreatercontrolovertheirinvestmentportfolioisacommoncharacteristicofinvestorsthatuseSMSFs.Assuch,SMSFinvestorsareengagedinvestors,andusefinancialadviceforguidanceratherthaninstruction.

ClassLimited(BoxB),whosesoftware isusedbyprofessionalstoadviseSMSFs, hasalsofoundthatSMSFinvestorsareusingtheflexibilityofthisstructureto investinalternativeproducts.Thiscouldbearesultofthelowinterestrateenvironment,whereinvestorsaresearchingforwaystoearnhighreturnsoutsideoftraditionalinvestmentoptions.

Notes: n=607

5%

10%

15%

20%

25%

30%

Chart 3.14: Top 5 goals of SMSF investors, proportion of SMSF investors

0

Rank1 Rank2 Rank3

Retirement Wealth accumulation

Supplementing income

Travel Rainyday saving

ASX Australian Investor Study | 2017

36

SMSF investors’ profile Asdiscussedearlierinthischapter,SMSFinvestorsarefairlyevenlysplitfromanageperspective,andaremorelikelytobeestablishedbypeoplewithhigherhouseholdincomeandassets.

TheriskprofileofSMSFinvestorsissimilartothatofinvestorsmorebroadly. MostSMSFinvestorsareseekingstable,reliablereturnsasopposedtovariability.

Chart3.15showsthemake-upofSMSFportfolios.Cashisthemostcommonlyheldasset(51%ofSMSFinvestorsreportholdingcashintheiraccount),followedbysharesandthenotheron-exchangeinvestments.

Box B: Class Limited

Class Limited creates innovative software used by accountants and financial advisers to service SMSFs. Its software is currently used to administer over 120,000 portfolios across Australia.

Class cites the desire for control as the number one reason that investors use SMSFs.

An SMSF opens the door to more flexible uses of an investor’s superannuation balance. For example, Class says that some SMSFs are used by clients to invest in their own business.

Class says that SMSF investors are bold and open to alternative investment opportunities. One example is a recent trend observed by Class that some SMSFs are investing in peer-to-peer (P2P) lending platforms. On average, when SMSFs invest in these platforms, they invest far more than other investors do – in many cases five times as much as a typical investor. This trend has been so strong that Class has begun to partner with P2P platforms (Rate Setter, and SocietyOne–underway) in order to make it easier for SMSFs to invest.

Class notes that SMSF clients typically look for advice rather than instruction, as these are engaged investors. At the same time they are also looking for value. In this context, Class expects that technology such as robo advice will become increasingly popular amongst SMSF investors.

ASX Australian Investor Study | 2017

37

Chart 3.15: Investment products held in SMSFs, proportion of SMSF investors

0% 10% 20% 30% 40% 50% 60%

Cash

Shares

Property

Otheron-exchangeproducts

Unlistedmanagedfunds

Notes: n=607‘Otheron-exchangeproducts’isdefinedinChapter1inthedefinitionsbox,aswellasinAppendixB.

Whilethesurveyfoundthat15%ofAustralianadultshaveanSMSF,thisislikelyanoverestimate.TheAustralianTaxationOffice estimatesthenumberofSMSFsinAustraliaataround585,000,withjustover1.1millionAustraliansmembersofanSMSF(ATO,2017).

Thisnumberislikelytocontinuetogrow.OfthoseinvestorsthatdonotuseanSMSF,whenaskedabouttheirfutureintentions, 30%ofthisgroupplantosetoneupinthefuture.

Who advises SMSF investors? Chart3.16showsthatSMSFinvestorsaremoreinclinedtouseprofessionaladvicethaninvestorsmorebroadly,andwhile doingtheirownresearchisstillthemostpopularoption,fewerSMSFsrelyonthisthaninvestorsmorebroadly.8

Notes: Respondentscouldselectuptothreeanswers,n=2391

5%

10%

15%

20%

25%

30%

35%

40%

Chart 3.16: Advice channels used by SMSF investors, proportion of SMSF investors

0

SMSF Otherinvestors

Fullserviceoradvicestockbroker

Financialplanner oradviser

Accountant Lawyer FamilyandFriends

Idomyownresearch

8Professionaladvicereferstopaidadvicefromafinancialadviser,afullservicestockbroker,alawyer,oranaccountant.

ASX Australian Investor Study | 2017

38

ThegreateruseofadvicemaybeduetothemorecomplexnatureoftheadministrativeandtaxationrequirementsofestablishingandmanaginganSMSF.InvestBluePtyLtd(afinancialadviser)foundthattheirclientsoftenrequireassistancewiththeadministrativesideofinvesting.BoxChasmoredetailonthetypesofSMSFinvestorsthatseekadviceandwhattheytypicallyinvestin.

Whenquestionedonwhytheyusefinancialadvice,SMSFinvestorsnominatedthreemainreasons:9

• 25%said–“Myadviserprovidesmewithadvicetailoredtomypersonalcircumstances”

• 23%said–“Myadviserhelpsmenavigatetheadministrativeandtaxrequirementsofinvesting”

• 22%said–“MyadvisergivesmeaccesstoinvestmentsIotherwisewouldn’tknowaboutorhaveaccessto”

9Financialadvicemeanseitherusingafullserviceoradvicestockbroker,orafinancialplanneroradviser.

Box C: Invest Blue Pty Ltd

Invest Blue is a financial advice practice with 14 offices located in rural and coastal locations across Queensland and NSW. They provide financial advice to people at all stages of life, including SMSF investors.

Among their clients, managing administrative compliance is the main advice sought. Few SMSFs are completely self-run, most use some form of advice, either for navigating compliance or to get investment choice advice.

Invest Blue advisers work with three broad types of SMSF investors: young accumulators, pre-retirees, and retirees. Each of these types of investors have different goals and therefore different investment portfolios.

Young accumulators in their late 30s or early 40s are typically high-income individuals (or couples). Given they have a fair amount of time before they need to access their super balances, they are typically advised to invest in growth assets. Because of their age they are unlikely to have large superannuation balances, so diversification is a challenge. Invest Blue uses a range of on-exchange products to help them diversify within their constraints, such as exchange-traded funds.

Pre-retirees invest more conservatively than young accumulators. This is because they have less time available before they begin to access their super balance, and as such they are advised to invest around 30% of their funds in defensive assets. A common investment among this group is commercial property, particularly among the self-employed. Some choose to purchase the premises from which their business is run.

Retirees are advised to invest for moderate growth – with around half growth assets and half defensive assets. This is to minimise the risk that their balances will drop at the stage of life where they rely, at least to some extent, on their SMSF for income. Fixed income assets such as corporate bonds are commonly used. Given the low interest rate environment, term deposits (which used to make up a large part of their portfolios) are now not recommended.

Invest Blue sees technology playing an important role in advising all three of these groups in the future. It will improve the customer experience, such as by improving real-time reporting, and allowing investors to check their balance at their convenience. At the same time it could lower the cost of advice.

ASX Australian Investor Study | 2017

39

Future SMSF users OfthoseindividualsthatdonotcurrentlyuseanSMSF(investorsandnon-investors),30%areplanningtoestablishan SMSFinthefuture,13%ofthemwithinthenextyear.Itmaybeusefultounderstandwhothesepeopleare.

Most(65%)ofthesepotentialSMSFusersalreadyinvestelsewhere,eitherinon-exchangeproductsorotherinvestmentproducts.

Theyaresplitevenlyalonggenderlines,butdovarybyage.AsChart3.17shows,potentialSMSFinvestorsaregenerallyyounger, 36%ofthemareunder30.GiventhatSMSFsareestablishedbeforeretirementitisnotsurprisingsofewofthesepotentialSMSF investorsareover60,butitisnoteworthythatthereissignificantinterestamongthoseatveryearlystagesoftheircareer.

Notes: n=1017

5%

10%

15%

20%

Chart 3.17: Age of potential SMSF investors, proportion of non-SMSF investors

0 18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-74 75+

ASX Australian Investor Study | 2017

40

5%

10%

15%

20%

25%

Chart 3.18: Income of potential SMSF investors, proportion of total

0 Lessthan $20,000

$20,000-$39,999

$40,000-$59,999

$60,000-$79,999

$80,000-$99,999

$100,000-$149,999

$150,000-$199,999

$200,000-$299,999

Over $300,000

Don'tknow /Unsure

Notes: Totalinvestors(n=207);totalnon-investors(n=485)

PotentialSMSFinvestors Allsurveyrespondents

Food for thought

• How can you help investors think through whether an SMSF is right for them, including educating them on portfolio construction, as well as administrative and regulatory requirements?

• Given the expected growth of SMSF use, can you afford not to be an SMSF expert?

3.3 Understanding potential investors Non-investorsarepotentialinvestors.Understandingthebarrierstheyfaceandtheirattitudestoinvestingwillhelptorealisethatpotential.Themajorityofnon-investors(54%)statethatalackofmoneyisthereasontheyhaveneverinvested.Thisisfollowedby33%ofnon-investorsquotingalackofconfidenceintheirability.Thisindicatesthatlackoffundsandconfidencearekeycharacteristicsoftheseinvestors.