Embed Size (px)

Citation preview

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Accounting Issues:

Dr. Wallace R. Leese, Ph.D.

1. At what value should the asset received be recorded?

2. Should a gain or loss be recognized on the exchange of the assets?

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #1

Dr. Wallace R. Leese, Ph.D.

Adams Mining Co. traded a rare, 1913 antique truck (specially equipped for mining during that era), for an patent with Gemstone Industries. Adams had $150,000 invested in the truck, with accumulated depreciation of $90,000. Gemstone had $20,000 in capitalized costs for the patent, along with $2,000 in amortization. Neither Adams nor Gemstone were able to reasonably determine the FMV of either of these two items.

Required:

Record the transaction for both Adams and Gemstone.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #1

Dr. Wallace R. Leese, Ph.D.

Adams: Gemstone:

Truck: 150,000$ Patent: 20,000$ Acc. Dep: (90,000) Amort: (2,000)BV: 60,000$ BV: 18,000$

Adams:Patent 60,000Accumulated Depreciation 90,000 Old Equipment 150,000

Gemstone:

Investment--antiques 18,000 Patent 18,000

Debit Credit

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

FMVof either asset determinable?

Yes

NoRecord asset

received at BV of asset given-up

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

1

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #2

Bain Media Services traded a printing press for a parcel of land held by Pitt Development. The land was appraised at $150,000. Pitt had the land recorded at $90,000 on their books. Bain paid $240,000 for the press 5-years ago, and has accumulated depreciation in the amount of $80,000.

Required:

Record the transaction for both Bain and Pitt.

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

General Procedures

1. Remove old asset from books2. Record new asset at FMV3. Record any cash paid or received4. Record any gain or loss

Debit CreditAccumulated Depreciation 1New Aset (at FMV) 2Cash 3Loss on Exchange 4 Old Asset 1 Cash 3 Gain on Exchange 4

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Determining Gain or Loss

What you Get $aaaLess: What you Give Up (bbb)Gain/(Loss) $ccc

Example:You trade a car with a BV of $15,000 for another car with a FMV of $25,000.

FMV of Assets Received: 25,000$ Less: BV of Old Assets: (15,000)Realized Gain: 10,000$

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #2

Dr. Wallace R. Leese, Ph.D.

Bain: Pitt:

Press: 240,000$ Land: 90,000$ Acc. Dep: (80,000) Acc. Dep:BV: 160,000$ BV: 90,000$ FMV: ? FMV: 150,000

Bain:Land 150,000Accumulated Depreciation 80,000Loss on Exchange of Assets 10,000 Equipment 240,000

Pitt:

Equipment 150,000 Land 90,000 Gain on Exchange of Assets 60,000

Debit Credit

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

FMVof either asset determinable?

Assets similar in nature?

Record transaction using General

Procedure.

Yes

No

No

Yes

Record asset received at BV of

asset given-up

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

2

1

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #3

Stone Transportation arranged to trade a delivery pickup for a newer custom pickup with ABC Tire Company. The CEO of Stone Transportation plans to use the pickup for personal use (as a company perquisite). Stone paid $25,000 for their pickup 3-years ago, and has accumulated depreciation in the amount of $8,000. Stone paid ABC an additional $5,000 for the newer pickup. The Newer pickup had a bluebook value of $29,000.

Required:

Record the transaction for Stone transportation.

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #3

Dr. Wallace R. Leese, Ph.D.

Stone:

Truck: 25,000$ Acc. Dep: (8,000)BV: 17,000$ FMV: 29,000

Stone:Automobiles 29,000Accumulated Depreciation 8,000 Cash 5,000 Automobiles 25,000 Gain on Exchange of Assets 7,000

Debit Credit

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

FMVof either asset determinable?

Assets similar in nature?

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Record transaction using General

Procedure.

Yes

No

No

No No

Yes

Yes Yes

Record transaction using General

Procedure.

Record asset received at BV of

asset given-up

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

3

2

1

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #4

Trader Jim is an outdoor store—primarily clothing. Trader Jim arranged to swap some of its outdoor clothing inventory for some uniforms with Scott’s Uniform Supply Company. The uniforms will be issued to employees as standard company attire. The clothing inventory exchanged cost $1,800, has a replacement value of $2,500 and could have been sold for $3,000. Scott’s Uniforms intended to use the outdoor clothing in another line of business. Scott’s cost for the uniforms was $2,000.

Required:

Record the transaction for Trader Jim and Scott’s Uniforms.

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #4

Dr. Wallace R. Leese, Ph.D.

Trader Jim: Scott's Uniforms

Inventory: 1,800 Inventory: 2,000$ FMV: 2,500

Trader Jim:Uniforms 2,500 Inventory 1,800 Gain on Exchange of Assets 700

Scott's Uniforms

Inventory (Clothes) 2,500 Inventory (uniforms) 2,000 Gain on Exchange of Assets 500

Debit Credit

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

FMVof either asset determinable?

Assets similar in nature?

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Record transaction using General

Procedure.

Yes

No

No

No No

No

Yes

Yes Yes

YesIs asset

received to be sold?

2

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record asset received at BV of

asset given-up

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

The asset received must be held for sale in the same line of business.

2

3

2

4

1

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #5

Webber Electric sells industrial electrical components to local industrial manufacturers. Webber arranged to exchange a gasoline powered forklift for an electric-powered forklift with Jensen Electric. Webber’s gas-powered forklift had a book value of $13,000 (originally, Webber paid $25,000). Likewise, Jensen’s forklift had a book value of $12,000 and accumulated depreciation of $20,000. The electric-powered forklift has a FMV of $10,000.

Required:

Record the transaction for both Webber and Jensen.

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #5

Dr. Wallace R. Leese, Ph.D.

Webber: Jensen:

Gas Forklift 25,000$ Elect Forklift 32,000$ Acc. Dep: (12,000) Acc. Dep: (20,000)BV: 13,000$ BV: 12,000$ FMV: ? FMV: 10,000

Webber:Equipment 10,000Accumulated Depreciation 12,000Loss on Exchange of Assets 3,000 Equipment 25,000

Jensen:

Equipment 10,000Accumulated Depreciation 20,000Loss on Exchange of Assets 2,000 Equipment 32,000

Debit Credit

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

FMVof either asset determinable?

Assets similar in nature?

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Record transaction using General

Procedure.

Doestransaction

create again?

Yes

No

No

No No

No No

Yes

Yes Yes

Yes

Yes

Is asset received to

be sold?

2

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record asset received at BV of

asset given-up

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

The asset received must be held for sale in the same line of business.

2

5

3

2

4

1

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #6

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Webber Electric sells industrial electrical components to local industrial manufacturers. Webber arranged to exchange a gasoline powered forklift for an electric-powered forklift with Jensen Electric. Webber’s gas-powered forklift had a book value of $9,000 (originally, Webber paid $25,000). Likewise, Jensen’s forklift had a book value of $12,000 and accumulated depreciation of $20,000. The electric-powered forklift has a FMV of $10,000.

Required:

Record the transaction for both Webber and Jensen.

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #6

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Webber: Jensen:

Gas Forklift 25,000$ Elect Forklift 32,000$ Acc. Dep: (16,000) Acc. Dep: (20,000)BV: 9,000$ BV: 12,000$ FMV: ? FMV: 10,000

Webber:Equipment 9,000Accumulated Depreciation 16,000 Equipment 25,000

Jensen:

Equipment 10,000Accumulated Depreciation 20,000Loss on Exchange of Assets 2,000 Equipment 32,000

Debit Credit

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Assets similar in nature?

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Record transaction using General

Procedure.

Doestransaction

create again?

Is cash received?

No

No No

No No

No

Yes

Yes Yes

Yes

Yes

Yes

Is asset received to

be sold?

2

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Defer all gains

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

5

3

2

4

6

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #7

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Trader Jim is an outdoor store—primarily clothing. Trader Jim arranged to swap some of its outdoor clothing inventory for similar clothes with Scott’s Outdoor & More. The clothing received by Trader Jim will be held for resale in the same line of business. Trader Jim’s inventory cost $18,000, has a replacement value of $25,000 and could have been sold for $30,000. Scott’s inventory cost was $19,000. In addition, Scott had to pay an additional $6,500 cash to complete the transaction.

Required:

Record the transactions for Trader Jim and Scott’s Outdoor & More.

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #7

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Trader Jim: Scott's Outdoor

Inventory: 18,000 Inventory: 19,000$ FMV: 25,000 Cash paid: 6,500

Trader Jim:Cash 6,500Inventory (new) 18,500 Inventory (old) 18,000 Gain on Exchange of Assets 7,000

Scott's Outdoor

Inventory (new) 25,000Loss on Exchange of Assets 500 Inventory (old) 19,000 Cash 6,500

Debit Credit%26

000,25

500,6

Recognize all gain

Recognize all losses

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Doestransaction

create again?

Is cash received?

Is cash³ 25% of total transaction's

FMV?

No No

No No

No

No

Yes Yes

Yes

Yes

Yes

Yes

Is asset received to

be sold?

2

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Defer all gains

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

5

3

4

6

7

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Sample Problem #8

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Trader Jim is an outdoor store—primarily clothing. Trader Jim arranged to swap some of its outdoor clothing inventory for similar clothes with Scott’s Outdoor & More. The clothing received by Trader Jim will be held for resale in the same line of business. Trader Jim’s inventory cost $18,000, has a replacement value of $25,000 and could have been sold for $30,000. Scott’s inventory cost was $19,000. In addition, Scott had to pay an additional $3,500 cash to complete the transaction.

Required:

Record the transactions for Trader Jim and Scott’s Outdoor & More.

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Partial Answer to Problem #8

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Trader Jim: Scott's Outdoor

Inventory: 18,000 Inventory: 19,000$ FMV: 25,000 Cash paid: 3,500

Trader Jim:Cash 3,500Inventory (new) ? Inventory (old) 18,000 Gain on Exchange of Assets ?

Scott's Outdoor

Inventory (new) 22,500 Inventory (old) 19,000 Cash 3,500

Debit Credit%14

000,25

500,3

Recognizepartial gain

Cash Paid,Defer all gains

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

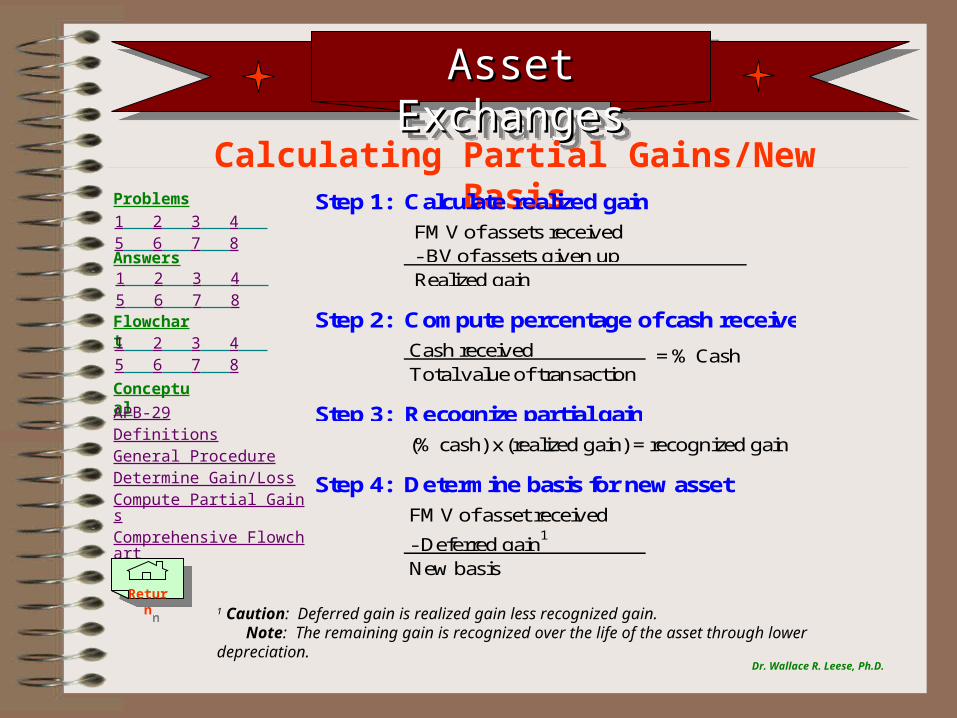

Calculating Partial Gains/New BasisStep 1: Calculate realized gain

Step 2: Compute percentage of cash received

Cash receivedTotal value of transaction

Step 3: Recognize partial gain

(% cash) x (realized gain) = recognized gain

Step 4: Determine basis for new asset

FMV of asset received

- Deferred gain1

New basis

- BV of assets given up FMV of assets received

Realized gain

= % Cash

1 Caution: Deferred gain is realized gain less recognized gain. Note: The remaining gain is recognized over the life of the asset through lower depreciation.

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Answer to Problem #8

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Trader Jim: Scott's Outdoor

Inventory: 18,000 Inventory: 19,000$ FMV: 25,000 Cash paid: 3,500

Trader Jim:Cash 3,500

Inventory (new)1

15,480 Inventory (old) 18,000 Gain on Exchange of Assets 980

Scott's Outdoor

Inventory (new) 22,500 Inventory (old) 19,000 Cash 3,500

Debit Credit

Trader Jim:Realized Gain:

25,000 FMV received

(18,000) BV given up7,000

% Cash Received:3,500

25,000

Recognized Gain:14% x 7,000 = 980

Deferred Gain:7,000 Realized(980) Recognized

6,020

= 14%

1New Basis21,500 FMV Received(6,020) Deferred Gain15,480

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Doestransaction

create again?

Is cash received?

Is cash³ 25% of total transaction's

FMV?

No No

No No

No

No

Yes Yes

Yes

Yes

Yes

Yes

Is asset received to

be sold?

2

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Defer all gains

Defer a portionof the gains

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

5

3

4

6

78

Dr. Wallace R. Leese, Ph.D.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

FMVof either asset determinable?

Assets similar in nature?

Assetgiven-up

normally held for sale?

Are bothassets Productive

assets?

1

Record transaction using General

Procedure.

Doestransaction

create again?

Is cash received?

Is cash³ 25% of total transaction's

FMV?

Yes

No

No

No No

No No

No

No

Yes

Yes Yes

Yes

Yes

Yes

Yes

Is asset received to

be sold?

2

Asset Exchanges

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Record transaction using General

Procedure.

Defer all gains

Defer a portionof the gains

Record transaction using BV of

surrendered asset1

2

3

54

6

8 7

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

APB Opinion No. 29

Dr. Wallace R. Leese, Ph.D.

Normal Procedure• FMV is recognized on reciprocal nonmonetary

transactions (gains/losses recognized)

Exceptions to Normal ProcedureGenerally:• Transactions recorded at BV• Some monetary consideration allowed

Where exceptions are applicable:1) Held for sale products/property in exchange for

products/property to be sold in the same line of business.

2) Productive assets for similar productive assets

(NOTE: Exchange cannot be made for the purpose of facilitating a sale to a customer)

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

Asset ExchangesAsset ExchangesAsset ExchangesAsset Exchanges

Definitions

Dr. Wallace R. Leese, Ph.D.

Monetary items: Cash, claims to cash, obligations to pay cash, and other balance-sheet items that are fixed in dollar amounts.

(Examples: Cash, A/R, A/P, Bonds)

Nonmonetary transactions: Exchanges that involve few or no monetary items.

Similar Productive Assets: Assets that are of the same general type, that perform the same function, or that are employed in the same line of business.

Problems

Answers

Conceptual

APB-29DefinitionsGeneral ProcedureDetermine Gain/LossCompute Partial GainsComprehensive Flowchart

Flowchart

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

ReturnReturn

![[Arnold S. Leese] Freemasonry](https://img.dokumen.tips/doc/110x75/543f825fafaf9ffb098b4795/arnold-s-leese-freemasonry.jpg)