Embed Size (px)

Citation preview

For institutional investors only/not for public viewing or distribution

Asset Backed Securities

September 2017

For institutional investors only/not for public viewing or distribution

ABS AUM growth, £ bn

2

Source: TwentyFour31st August 2017

0.1 0.3

0.9 0.8

1.0

1.6

2.8 3.0

4.3

5.8

12.2008 12.2009 12.2010 12.2011 12.2012 12.2013 12.2014 12.2015 12.2016 08.2017

ABS

For institutional investors only/not for public viewing or distribution

TwentyFour’s ABS fund range

3

OEIC

Investment Co.

Direct Lending (Inv.Co.)

Bank

Pension Fund

Insurance Co

Mandated Fund

Fiduciary Manager

Segregated MandatesAsset Backed SecuritiesEuropean

TwentyFour Income Fund

UK Mortgages Ltd.

Monument Bond Fund

Senior

Liquid Investment

Grade

Less Liquid/High

Yield

UK CoveredBonds

Senior UK RMBS

IG ABS

Senior UK RMBS

IG ABS

High Yield ABS

Local Authority

High Yield ABS

High Yield ABS

Monument European

ABS

For institutional investors only/not for public viewing or distribution

2

UKML – Current Investments

*IRR estimates based on modelled scenarios and calculated from trade inception. There can be no guarantee or assurance that they will be achieved.Source: TwentyFour,14th September 2017

Malt Hill No.1(Coventry Building Society)

Loans originated and purchased in 2015

c. £265m Buy-to-Let loans

Zero loans in arrears

Estimated IRR* 6.48%

Oat Hill No.1(Capital Home Loans)

c. £574m legacy Buy-to-Let loans originated before the crisis

Excellent performance – just 0.8% arrears

Estimated IRR 10.22%

TML(The Mortgage Lender)

Portfolio in ramp-up

New originator began lending in July 2016

Owner-occupied loans

Current completions & pipeline c. £108m

Estimated IRR 9.22%

Available Investment Capital

C. £40m released following Oat Hill securitisation

Currently looking at further investments

4

Risk appetite is similar to a lower-risk mortgage lender (e.g. a building society)

For institutional investors only/not for public viewing or distribution

0

100

200

300

400

500

600

700

800

900

AAA AA A BBB BB B

Cre

dit

Sp

read

(b

ps)

ABS/Corporate Spreads

5

Source: TwentyFour, Barclays6th September 2017

AAA AA A BBB BB B

Prime RMBS 50 100 155 200 320

Buy To Let RMBS 75 130 175 215

Near Prime RMBS 60 135 180 230

CMBS 105 140 185 250

CLOs 115 175 230 315 565 765

Euro Corps 27 38 76 116 220 394

£ Corps 30 56 104 151 279 473

$ Corps 68 57 84 139 239 394

For institutional investors only/not for public viewing or distribution

Portfolio Highlights

6

Portfolio highlights Monument Bond Fund TwentyFour Income Fund

Assets Under Management £368.5m £458.2m

Gross yield (%)* 2.80 6.92

Interest rate duration (years) 0.12 0.12

Credit spread duration (years) 3.30 3.63

Average rating A+ BB+

YTD Performance 3.83% 9.67%

1 year Performance 5.76% 12.67%

3 year Performance 7.13% 13.79%

Past performance is not an indication of future performance. *The gross yield is the yield on an investment before the deduction of taxes and expenses. It is calculated as the annual return on an investment prior to taxes and expenses divided by the current price of the investment. TFIF performance figures are based on NAV per share.Source: TwentyFour 31st August 2017

For institutional investors only/not for public viewing or distribution

Current Market Trends

7

H2 2016 saw continued spread tightening and consistent performance with none of the volatility seen in fixed rate credit

markets, driven by central bank policy support and ongoing relative value

H1 2017 exhibited strong technically driven performance

Trend expected to continue, driven by low supply outlook and increasing demand

- Strongest sector performance UK Non Conforming RMBS and CLOs

- Excellent fundamental performance of the asset class

A number of potential threats to sentiment and spread stability exist

Current positioning is cautious

– Should external events overpower the strong technical, then we would expect short windows of excellent investment

opportunities

European ABS expected to be a top performing asset class in 2017

Source: TwentyFour

For institutional investors only/not for public viewing or distribution

Monument Bond Fund Positioning

8

Rating breakdown Sector breakdown Geographic breakdown

Non-Conforming Residential mortgage backed securities (NC RMBS), Commercial mortgage backed securities (CMBS), Residential mortgage backed securities (RMBS), Collateralised loan obligations (CLOs), Buy-to-let Residential mortgage backed securities (BTL RMBS) , Prime Residential mortgage backed securities (Prime RMBS).Source: TwentyFour31st August 2017

UK, 54.92%

Mixed, 21.48%

Italy, 5.97%

Netherlands, 4.46%

Portugal, 3.73%

Spain, 3.37%

Germany, 1.20% Cash & Equiv,

4.87%

2.92%

4.87%

5.34%

8.47%

15.25%

21.48%

41.67%

CMBS

Cash & Equiv

Consumer ABS

BTL RMBS

Prime RMBS

CLO

NC RMBS

0% 20% 40% 60%

21

.8%

19

.1%

31

.4%

27

.6%

0%

5%

10%

15%

20%

25%

30%

35%

AAA/Cash& Equiv

AA A BBB

For institutional investors only/not for public viewing or distribution

TFIF Positioning

9

Non-Conforming Residential mortgage backed securities (NC RMBS), Commercial mortgage backed securities (CMBS), Residential mortgage backed securities (RMBS), Collateralised loan obligations (CLOs), Buy-to-let Residential mortgage backed securities (BTL RMBS) , Prime Residential mortgage backed securities (Prime RMBS). Mixed Jurisdiction Exposure (look-through basis) looks through to underlying assets e.g. CLOs. Source: TwentyFour. 31st August 2017

Geographical breakdownRating breakdown Sector breakdown

0.2%

1.3%

1.8%

8.9%

10.4%

17.3%

24.8%

35.3%

0% 10% 20% 30% 40%

Student Loans

CMBS

Cash & Equiv

Consumer ABS

BTL RMBS

Prime RMBS

NC RMBS

CLO

8.3

%

6.8

%

11

.4%

15

.8%

21

.5%

23

.6%

1.5

%

11

.1%

0%

5%

10%

15%

20%

25%

AA

A/C

ash

& E

qu

iv AA A

BB

B

BB B

CC

C

NR

39

.5%

6.6

% 1.8

%

6.1

%

3.6

%

6.6

%

13

.6%

4.82%

4.15%

1.19% 0.87%

0.07%

5.58%

5.59%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

UK

Ne

the

rlan

ds

Spai

n

Ital

y

Po

rtu

gal

Ge

rman

y

Fran

ce

Mix

ed

Mixed Jurisdiction Exposure (look-through basis)

Single Jurisdiction Exposure

For institutional investors only/not for public viewing or distribution

European ABS Performance Fundamentals

10

In 2016 European ABS credit performance was more positive than the previous year. The upgrade rate reached an all

time high of 19.8% from 14.6% in 2015. The downgrade rate declined to 5.2% from 16.5%

The European ABS sector includes a diverse array of subsectors. CMBS was the worst performing subsector in 2016, but

it is also small, constituting only about 7% of S&P European structured finance ratings outstanding. Most defaults in

2016 were largely CMBS, structured shortly pre-crisis which were most affected by the lower lending standards and

declines in real estate values

CLOs are now one of the largest European subsectors by ratings outstanding and generally performed well in 2016 with

a downgrade rate of only 1.7% and an upgrade rate of 34.9% as many legacy transactions are now amortizing and de-

risking

European structured finance downgrades in 2016 were concentrated in 2006 & 2007 vintages, with generally higher

downgrade rates at the lower rating levels. The investment grade downgrade rate was 2.9% compared with speculative

grade downgrade rate of 10.1%

Source: S&P 2016 Annual Global Structured Rating transitions

For institutional investors only/not for public viewing or distribution

Primary Market Issuance & Rating Distribution

11

Primary Market Issuance YTD 2017 is €51.4Bn vs. total issuance €83.4Bn in 2016. However, there is a reasonable primarysupply building in the market and ABS issuance can fluctuate quarter on quarter

Predominantly AAA issuance with mezzanine bonds in the majority of transactions being retained by the issuer in thenon CLO sector. For example, the UKAR sale of Bradford & Bingley’s legacy portfolio totalled £11bn which accounted fora large proportion of UK RMBS issuance YTD

Expect the supply demand imbalance to continue for the foreseeable future which will provide support to strongperformance seen over the last six months

Source: IFR, Bloomberg, Morgan Stanley Research31st August 2017

2017 YTD Issuance Summary by Sector and Country Issuance – Ratings Distribution

Source: IFR, Bloomberg, Morgan Stanley Research Source: IFR, Bloomberg, Morgan Stanley Research

For institutional investors only/not for public viewing or distribution

TwentyFour Asset Management LLP8th FloorThe Monument Building11 Monument StreetLondonEC3R 8AFT: +44 (0)20 7015 8900twentyfouram.com

12

For institutional investors only/not for public viewing or distribution

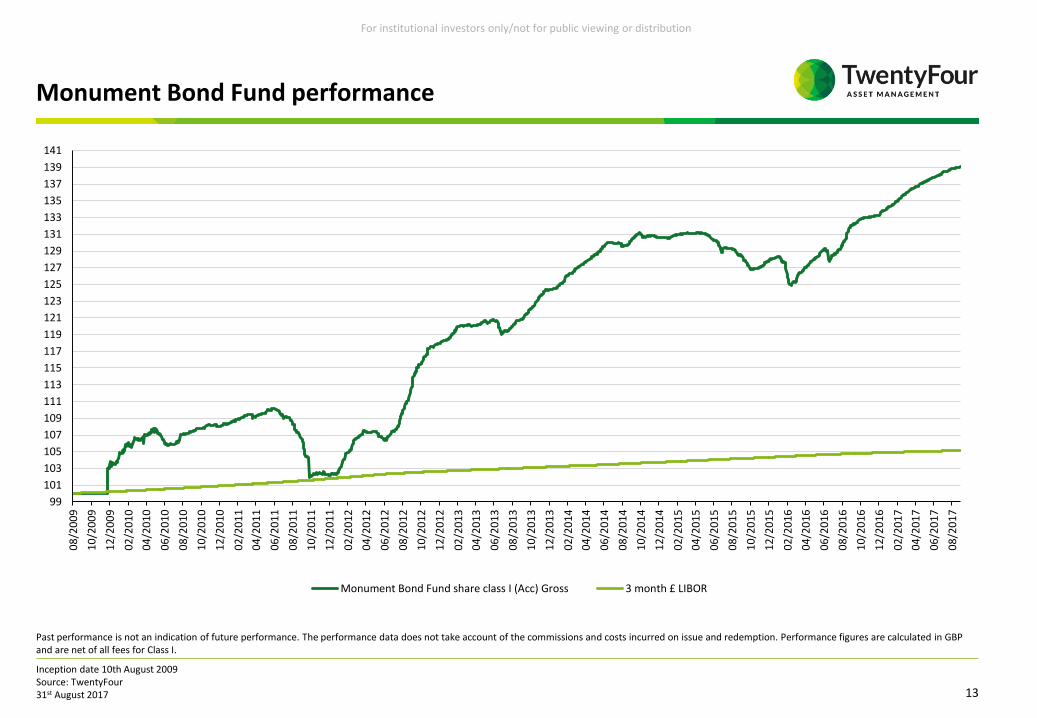

Monument Bond Fund performance

13

Past performance is not an indication of future performance. The performance data does not take account of the commissions and costs incurred on issue and redemption. Performance figures are calculated in GBP and are net of all fees for Class I.

Inception date 10th August 2009Source: TwentyFour31st August 2017

99

101

103

105

107

109

111

113

115

117

119

121

123

125

127

129

131

133

135

137

139

141

08

/20

09

10

/20

09

12

/20

09

02

/20

10

04

/20

10

06

/20

10

08

/20

10

10

/20

10

12

/20

10

02

/20

11

04

/20

11

06

/20

11

08

/20

11

10

/20

11

12

/20

11

02

/20

12

04

/20

12

06

/20

12

08

/20

12

10

/20

12

12

/20

12

02

/20

13

04

/20

13

06

/20

13

08

/20

13

10

/20

13

12

/20

13

02

/20

14

04

/20

14

06

/20

14

08

/20

14

10

/20

14

12

/20

14

02

/20

15

04

/20

15

06

/20

15

08

/20

15

10

/20

15

12

/20

15

02

/20

16

04

/20

16

06

/20

16

08

/20

16

10

/20

16

12

/20

16

02

/20

17

04

/20

17

06

/20

17

08

/20

17

Monument Bond Fund share class I (Acc) Gross 3 month £ LIBOR

For institutional investors only/not for public viewing or distribution

TFIF NAV performance

14

Past performance is not an indication of future performance. Source: TwentyFour31st August 2017

Past performance is not an indication of future performance. The performance data does not take account of the commissions and costs incurred on issue and redemption. Performance figures are calculated in GBP and are net of all fees.

95

105

115

125

135

145

155

03

/20

13

04

/20

13

05

/20

13

06

/20

13

07

/20

13

08

/20

13

09

/20

13

10

/20

13

11

/20

13

12

/20

13

01

/20

14

02

/20

14

03

/20

14

04

/20

14

05

/20

14

06

/20

14

07

/20

14

08

/20

14

09

/20

14

10

/20

14

11

/20

14

12

/20

14

01

/20

15

02

/20

15

03

/20

15

04

/20

15

05

/20

15

06

/20

15

07

/20

15

08

/20

15

09

/20

15

10

/20

15

11

/20

15

12

/20

15

01

/20

16

02

/20

16

03

/20

16

04

/20

16

05

/20

16

06

/20

16

07

/20

16

08

/20

16

09

/20

16

10

/20

16

11

/20

16

12

/20

16

01

/20

17

02

/20

17

03

/20

17

04

/20

17

05

/20

17

06

/20

17

07

/20

17

08

/20

17

NAV per Share NAV per Share including coupons Share Price Share Price including coupons

For institutional investors only/not for public viewing or distribution

Disclaimer

This document has been prepared by TwentyFour Asset Management LLP ("TwentyFour"), portfolio manager of the Funds, for information purposes only. This document is an indicative summary of the terms andconditions of the securities described herein and may be amended, superseded or replaced by subsequent summaries. The final terms and conditions of the securities will be set out in full in the applicable offeringdocument(s).

This document shall not constitute an offer to sell or the solicitation of an offer to buy any securities described herein. TwentyFour is not acting as advisor or fiduciary. Accordingly you must independently determine,with your own advisors, the appropriateness for you of the securities before investing. TwentyFour accepts no liability whatsoever for any consequential losses arising from the use of this document or reliance on theinformation contained herein.

No offers, sales, resales or delivery of the securities described herein or distribution of any offering material relating to such securities may be made in or from any jurisdiction except in circumstances which will resultin compliance with any applicable laws and regulations and which will not impose any obligation on TwentyFour or any of its affiliates.

TwentyFour does not guarantee the accuracy or completeness of information which is contained in this document and which is stated to have been obtained from or is based upon trade and statistical services or otherthird party sources. Any data on past performance, modelling or back-testing contained herein is no indication as to future performance and there can be no assurance that targeted or projected returns will beachieved, that the Company will achieve comparable results or that the Company will be able to implement its investment strategy or achieve its investment objectives. No representation is made as to thereasonableness of the assumptions made within or the accuracy or completeness of any modelling or back-testing. All opinions and estimates are given as of the date hereof and are subject to change. The value ofany investment may fluctuate as a result of market changes. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.

TwentyFour, its affiliates and the individuals associated therewith may (in various capacities) have positions or deal in securities (or related derivatives) identical or similar to those described herein.

This document is being made available in the UK to persons who are investment professionals as defined in Article 19 of the FSMA 2000 (Financial Promotion Order) 2005. Outside of the UK, it is directed at personswho have professional experience in matters relating to investments. Any investments to which this document relates will be entered into only with such persons. This document is not for distribution to retailcustomers.

No action has been made or will be taken that would permit a public offering of the securities described herein in any jurisdiction in which action for that purpose is required.

This document does not disclose all the risks and other significant issues related to an investment in the securities. Prior to transacting, potential investors should ensure that they fully understand the terms of thesecurities and any applicable risks. This document is not a prospectus for any securities described herein. Investors should only subscribe for any securities described herein on the basis of information in the relevantprospectus (which has been or will be published and may be obtained from TwentyFour by visiting it’s website www.Twentyfouram.Com), and not on the basis of any information provided herein.

TwentyFour Asset Management LLP is registered in England No. OC335015, and is authorised and regulated in the UK by the Financial Conduct Authority, FRN No. 481888. Registered Office: 8th Floor, The Monument Building, 11 Monument Street, London, EC3R 8AF.Copyright TwentyFour Asset Management LLP, 2017 (all rights reserved). This document is confidential, and no part of it may be reproduced, distributed or transmitted without the prior written permission of TwentyFour.

15