Embed Size (px)

Citation preview

June 2008

Assessing hidden risk in traditional and alternative asset classes

Unigestion at a glance

An independent company, dedicated to investment management since 1971

A highly capitalised and solid structure, aligned with its clients

More than € 100 million equity

A culture of innovation as the pillarfor long term development

First investment in Hedge Funds in 1986*

Early European investor in Private Equity(since 1988)*

A pioneer in the implementationof Minimum Variance (since 1995)

Corporate Profile

Strategies: Minimum Variance EquitiesHedge FundsPrivate Equity

Offices: GenevaLondonParisMunichNew YorkSingapore Guernsey

Employees: 155 total

Data as at 31st March 2008*Investment for own account

Unigestion: 20 years of experience in assessing risk for various asset classes

Minimum Variance Equities

Fundamental risk

Volatility

Correlation

Specific risk

Market risk

Liquidity

At the fund level:Market risk andCredit risk

Operational risk

Systemic risk

At the fund of funds level:Liquidity

At the fund level:Specific risk

Market risk

Credit risk

At the fund of funds level:Liquidity

Hedge Funds Private Equity

Daily, with real-time data Monthly, with weekly/monthly data

Yearly, with quarterly data

Tim

e ho

rizon

Exam

ples

of p

aram

eter

s lo

oked

at

Our speakers

Jean-François HirschelHead of Marketing

Alexei JourovskiHead of Investments - Equities

Christophe de DardelHead of Investments - Private Equity

Gabriele SusinnoHead of Quantitative Research & Risk Control - Hedge Funds

Agenda for today

1. Correlation

Correlation is relevant for linearly-related normal variables, which are not so frequent in the real world

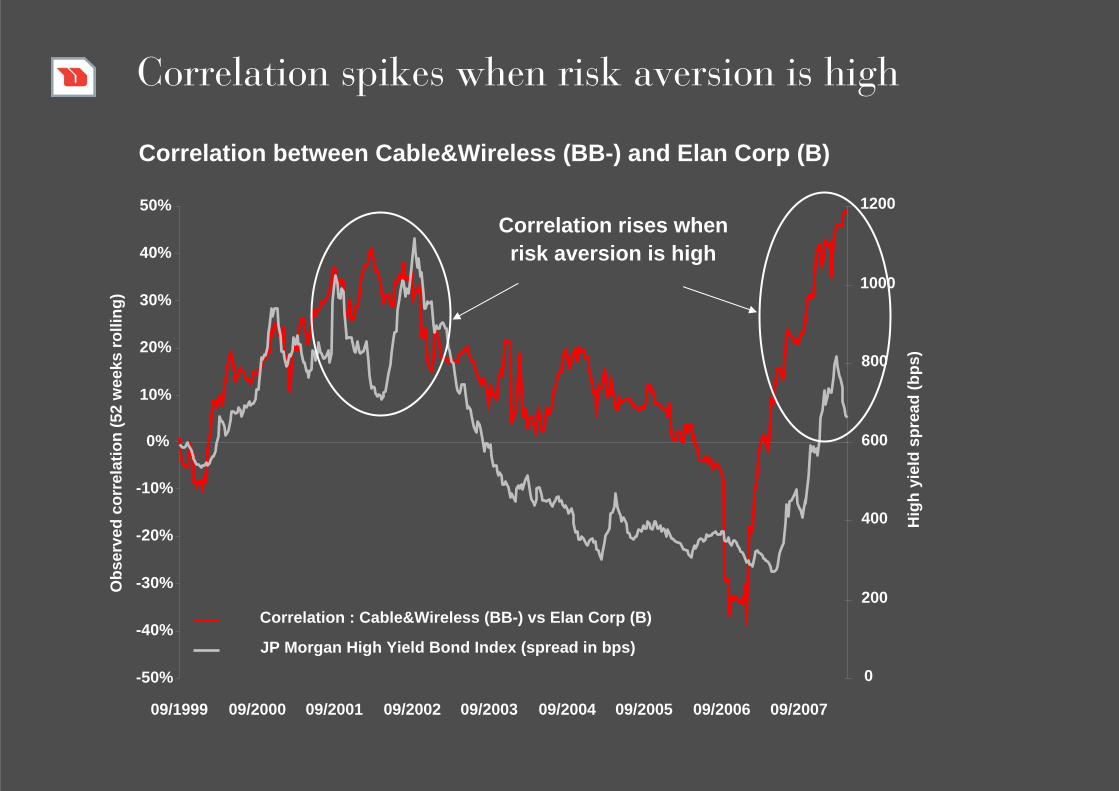

Correlation spikes when risk aversion is high

2. Liquidity

Overcoming the difficulties of estimating liquidity in equities: Liquidity at Risk

The challenge of managing illiquidity in Private Equity: cash flow modeling

3. Leverage

Hedge Funds: adjusting leverage to assets’ volatility

Private Equity: assessing the true impact of leverage

1. Correlation

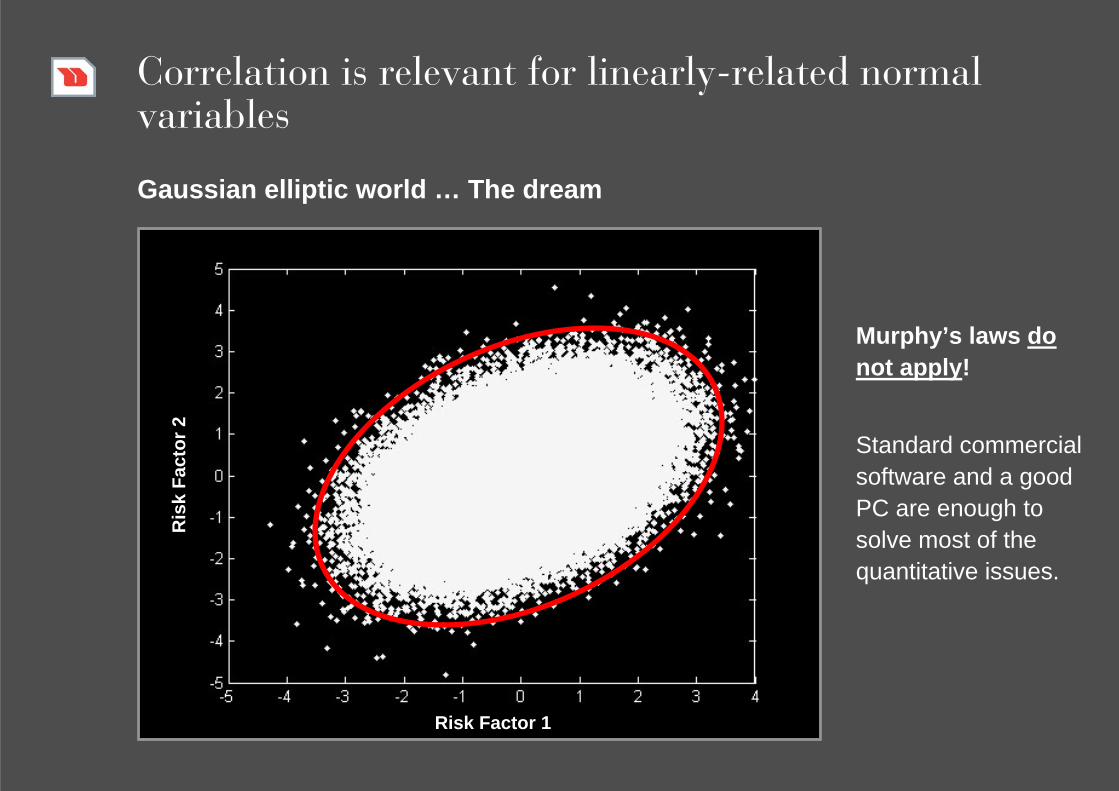

Correlation is relevant for linearly-related normal variables

Risk Factor 1

Ris

k Fa

ctor

2Gaussian elliptic world … The dream

Murphy’s laws do not apply!

Standard commercial software and a good PC are enough to solve most of the quantitative issues.

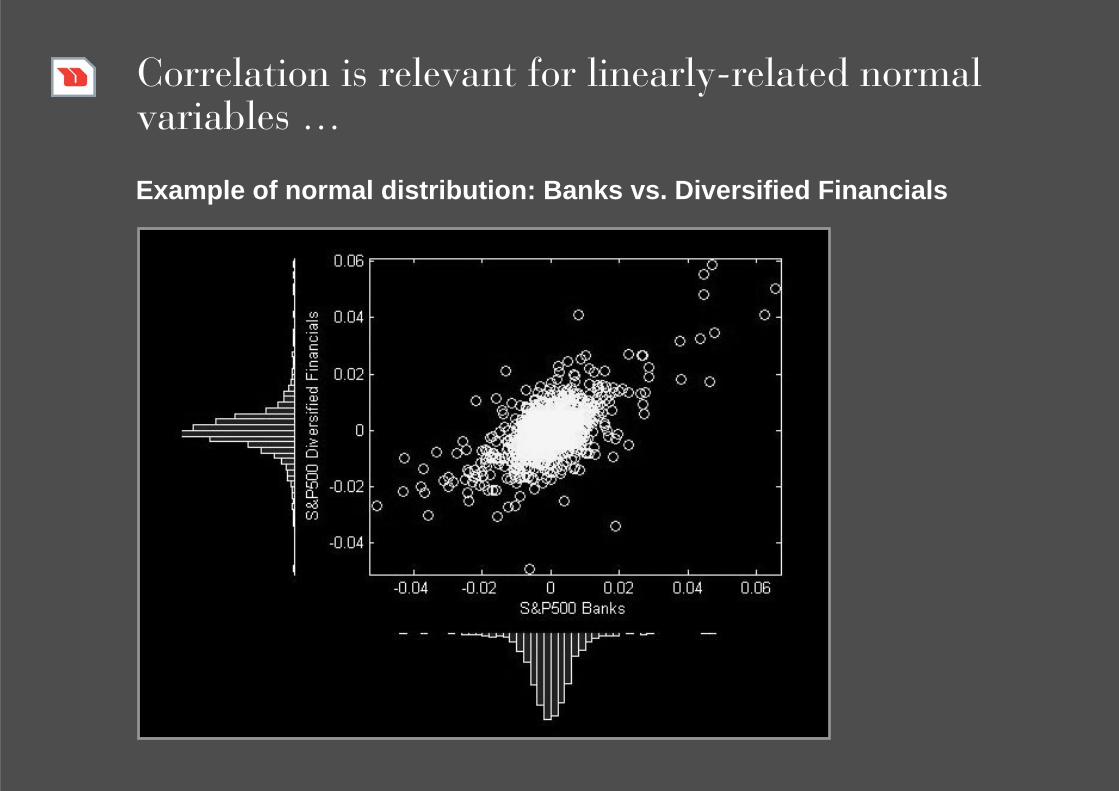

Correlation is relevant for linearly-related normal variables …

Example of normal distribution: Banks vs. Diversified Financials

… which are not so frequent in the real world

Example of fat-tail distribution: Energy vs. Materials

Correlation is misleading in non-normal worldsNon-normal world … The real world … The HF world

Classical Risk Management tools break down! VaR does not work; Standard Deviation is misleadingPortfolio optimization is risk-measure dependentCorrelation based methods are insufficient

Murphy’s laws do apply!

No Universal Recipebut ad hoc approaches.

Risk Factor 1

the “perfect storm”scenario

Ris

k Fa

ctor

2

-0.2 -0.15 -0.1 -0.05 0 0.05 0.1 0.15-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

EDHEC Index: Emerging Markets (Monthly returns)

EDH

EC In

dex:

L/S

Equ

ity(M

onth

lyre

turn

s)

Storm event 31/08/1998

2 sigma event

Correlation spikes when risk aversion is high

Correlation between Cable&Wireless (BB-) and Elan Corp (B)

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

09/1999 09/2000 09/2001 09/2002 09/2003 09/2004 09/2005 09/2006 09/2007

Obs

erve

d co

rrel

atio

n (5

2 w

eeks

rolli

ng)

0

200

400

600

800

1000

1200

Hig

h yi

eld

spre

ad(b

ps)

Correlation : Cable&Wireless (BB-) vs Elan Corp (B)

JP Morgan High Yield Bond Index (spread in bps)

Correlation rises whenrisk aversion is high

2. Liquidity

Liquidity is a very unstable parameterObserved volume of J Sainsbury PLC

Seasonal effect : Liquidity dry up in December

Extreme events :M&A news, earnings announcements

Median daily volume: a realistic liquidity forecast

Liquidity distribution of J Sainsbury PLC

0%

1%

2%

3%

4%

5%

6%

7%

0 40 80 120 160 200 240 280 320 360 400

Daily volume traded (GBP millions)

% O

ccur

renc

e

Median : 65.3 M GBP / dayConfidence : 50%

Average : 99.4 M GBP / dayConfidence : 29%

Overcoming the difficulties of estimating liquidity in equities: Liquidity at RiskLiquidity at Risk estimator for J Sainsbury PLC7%

0%

1%

2%

3%

4%

5%

6%

0 40 80 120 160 200 240 280 320 360 400

Daily volume traded (GBP millions)

% O

ccur

renc

e

Median : 65.3 M GBP / dayConfidence : 50%

Average : 99.4 M GBP / dayConfidence : 29%

Liquidity at Risk : 30 M GBP / dayConfidence : 75%

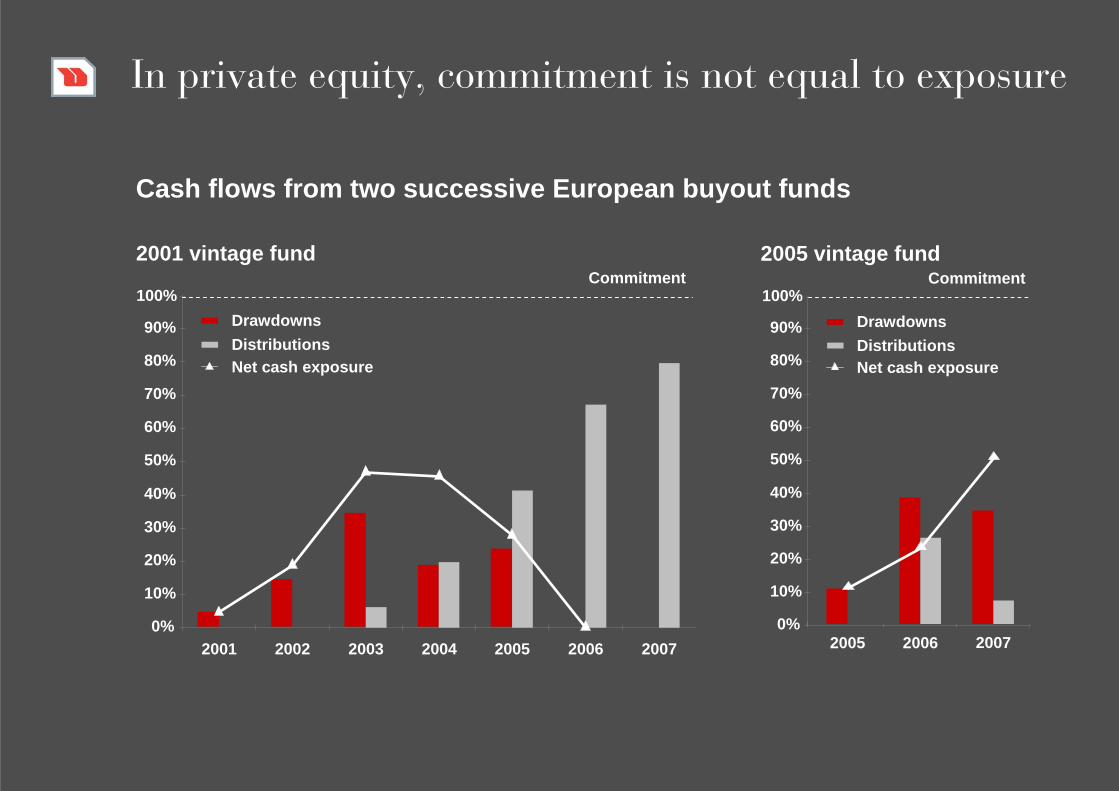

In private equity, commitment is not equal to exposure

Cash flows from two successive European buyout funds

2001 vintage fund

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2001 2002 2003 2004 2005 2006 2007

DrawdownsDistributionsNet cash exposure

Commitment100%

2005 vintage fund

2005 2006 20070%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Commitment100%

DrawdownsDistributionsNet cash exposure

Cash flow forecasting requires sophisticated modeling

Realised portfolio companies

Unrealised portfolio companies

Undrawn commitments

Future commitments

Exit projections

Actual data

Actual data

Assumptions on drawdowns, holding periods, exit multiples, fees, etc…

Assumptions on drawdowns, holding periods, exit multiples, fees, etc…

Portfolio levelassumption (operating expenses, dividends, etc…)

Optimizer: maximiseinvestment level / remain cash positive

Commitment plan

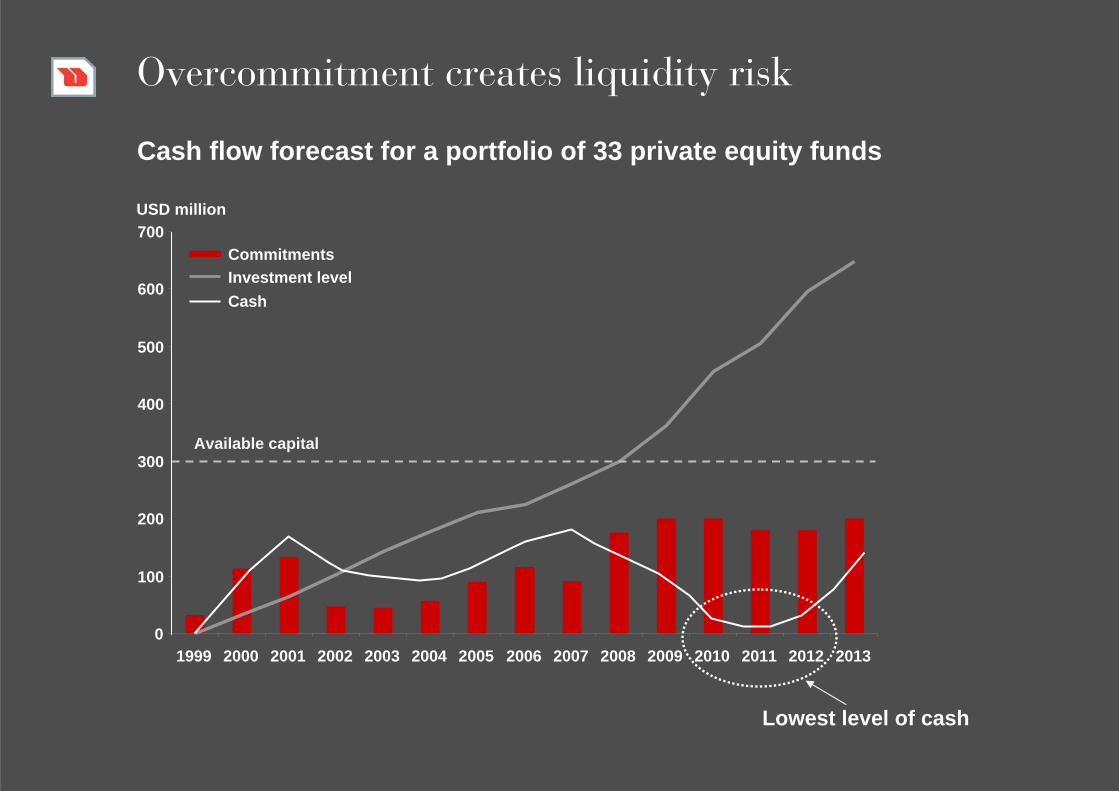

Overcommitment creates liquidity risk

Cash flow forecast for a portfolio of 33 private equity funds

0

100

200

300

400

500

600

700

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

USD million

Available capital

Lowest level of cash

CommitmentsInvestment levelCash

3. Leverage

Adjusting leverage to assets’ volatility

Two ways to the same risk profile:

High Market risk and low leverage

Low Market Risk and high leverage

Leverage: “A creation of exposure greater in magnitude than the initial cash amount posted to an investment.”1

1. cf AIMA Canada Strategy Paper Series October 2006

Financial Risk

Beta

Leverage

Market Risks

Risk Amplifier

Thus leverage is strategy dependent

Examples of typical leverage:2 to 10 X for Arbitrage Strategies2 X for directional strategies such as Equity Hedge.

In Hedge Funds, leverage measure must be adapted to the strategy

The Leverage can be quantified in absolute terms or with respect to the risk profile of a reference index (effective beta equivalent).

Types of Leverage

Financial Leverage or Borrowing Leverage

Strategy Leverage : Impact of portfolio construction rules on the overall portfolio’s risk

Instrument Leverage (Gearing) : intrinsic internal leverage of financial instruments.

In Hedge Funds Leverage measure must be adapted to the strategy:

L/S Strategies: Gross Financial Leverage = (longs + shorts)/Capital

MKT Neutrals: Net Financial Leverage = (longs – shorts)/Capital

Arbitrage and Derivative Strategies: Leverage = Financial Leverage * Gearing

Adjusting leverage to assets’ volatility

Maximum Leverage

There is an optimal level of leverage to maximize the compound rate of growth over the long term, calculated according to what is known as the “Kelly Criterion* ”:

The rule can be used to scale the level of leverage to the strategy’s intrinsic volatility.

CAUTION :

Just considering volatility in Hedge Funds can be risky as FAT TAIL risk is magnified by the leverage.

Neglecting Leverage represents a suboptimal use of capital.

*J. L. Kelly, Jr, A New Interpretation of Information Rate, Bell System Technical Journal, 35, (1956), 917-926

Private Equity: assessing the true impact of leverage

2.5 to 1 leveraged investment in a European white goods company

Value creation before restatement Value creation after restatement

Equity at

entry

700

600

500

400

300

200

100

0

8%14%

60%

18%

2001 2005

Reven

ue incre

ase

Margin im

prove

ment

Multiple

arbitr

age

Levera

geEquity

at ex

it

EUR m

233

64013%

30%

17%

40%

Equity at

entry

Reven

ue incre

ase

Margin im

prove

ment

Multiple

arbitr

age

Debt r

educti

onEquity

at ex

it

2005

700

600

500

400

300

200

100

0

EUR m

233

640

2001

Highly leveraged companies are very sensitive to changes in market conditions

2.5 to 1 leveraged investment in a European white goods company

Investmentin 2001

Exitin 2005

Theoretical exit in down market

Revenue 600 720 620

EBITDA 100 130 100

EV / EBITDA 7.0x 8.5x 6.0x

Enterprise Value (EV) 700 1,105 600

Debt / EBITDA 5.0x

Debt 500 400 415

Equity 200 705 185

Exit multiple 3.5x 0.9x

One size does not fit all

Important information

This presentation has been prepared for your personal use and is for information only. It must not be published, reproduced or disclosed (in whole or in part) by recipients to any other person. All information contained herein is subject to change without notice. This document should be considered current as of the date of publication without regard to the date on which you may access the information.

This presentation is a promotional statement of our investment philosophy and services and does not constitute an offer or a solicitation to subscribe in the strategies or in the investment vehicles described or alluded to herein which may be construed as high risk and not readily realisable investments and may experience substantial and sudden loss including total loss of investment. Such investment is not suitable for all types of investors. All investors must obtain and carefully read the prospectuses which contain additional information needed to evaluate the potential investment and provide important disclosures regarding risks, fees and expenses.

The investment vehicles mentioned herein may not be authorized for public distribution in certain jurisdictions. Most Hedge Funds have only been authorized as a Class B scheme by the Guernsey Financial Services Commission. The Unicapital Investments Funds referred to in this presentation are only registered for public distribution in Luxembourg and are not offered or distributed on a public basis in or from any country where such distribution would be prohibitedby law.

Some figures contained in this document have not been independently verified although they have been obtained from sources believed reliable. As a result, Unigestion SA does not give any warranty or representation as to the accuracy, reliability or completeness of these figures. Data and graphical information as well as some statements contained herein are based on information supplied to Unigestion SA by third parties. No separate verification has been made as to the accuracy or completeness of these data and, as a result, no representations are made by Unigestion in this respect.

Past performance is not indicative of future performance. The value of investments may go down or up. There are no guaranteed returns. The Uni-Benchmark Composites are created by Unigestion SA and are made of single strategy benchmarks composed of the main investable indices.

Unless otherwise mentioned, source of data is Unigestion SA and Bloomberg .

www.unigestion.com

1) Supervised by the Federal Banking Commission.2) Regulated by the Guernsey Financial Services Commission.3) Authorised and regulated by the Financial Services Authority. Registered in England and Wales N°3886428.4) Authorised by BaFin.5) Supervised by “L’Autorité des Marchés Financiers”.

SINGAPORE UNIGESTION ASIA Pte Ltd152 Beach Road Suite #23-05/06The Gateway EastSingapore 189721Singapore

PARIS 5)

UNIGESTION ASSETMANAGEMENT (France) SA12 avenue MatignonF-75008 Paris

MUNICH 4)

UNIGESTION (UK) LtdGerman BranchZweigniederlassung PlaneggBahnhofstrasse 34D-82152 Planegg

NEW YORKUNIGESTION (US) LtdPlaza 10 – HarborsideFinancial CenterSuite 203Jersey City, NJ 07311USA

LONDON 3)

UNIGESTION (UK) Ltd105 PiccadillyUK-London W1J 7NJ

GUERNSEY 2)

UNIGESTION (Guernsey) LtdFarnley HouseLa CharroterieSt. Peter PortGuernsey, GY1 1EJChannel Islands

GENEVA 1)

UNIGESTION SA8C avenue de ChampelCP 387CH-1211 Genève 12

Contacts

Jean-François HirschelManaging Director, Head of MarketingTel. +41 (0)22 704 42 76E-mail : [email protected]

Alexei JourovskiExecutive Director, Head of Investments - EquitiesTel. +41 (0)22 704 43 19E-mail : [email protected]

Christophe de DardelExecutive Director, Head of Investments - Private EquityTel. +41 (0)22 704 42 61E-mail : [email protected]

Gabriele SusinnoExecutive Director, Head of Quantitative Research & Risk Control - Hedge FundsTel. +41 (0)22 704 43 63E-mail : [email protected]