Embed Size (px)

Citation preview

ASIAN DEVELOPMENT BANK RRP: PNG 32472

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

BOARD OF DIRECTORS

ON A

PROPOSED LOAN

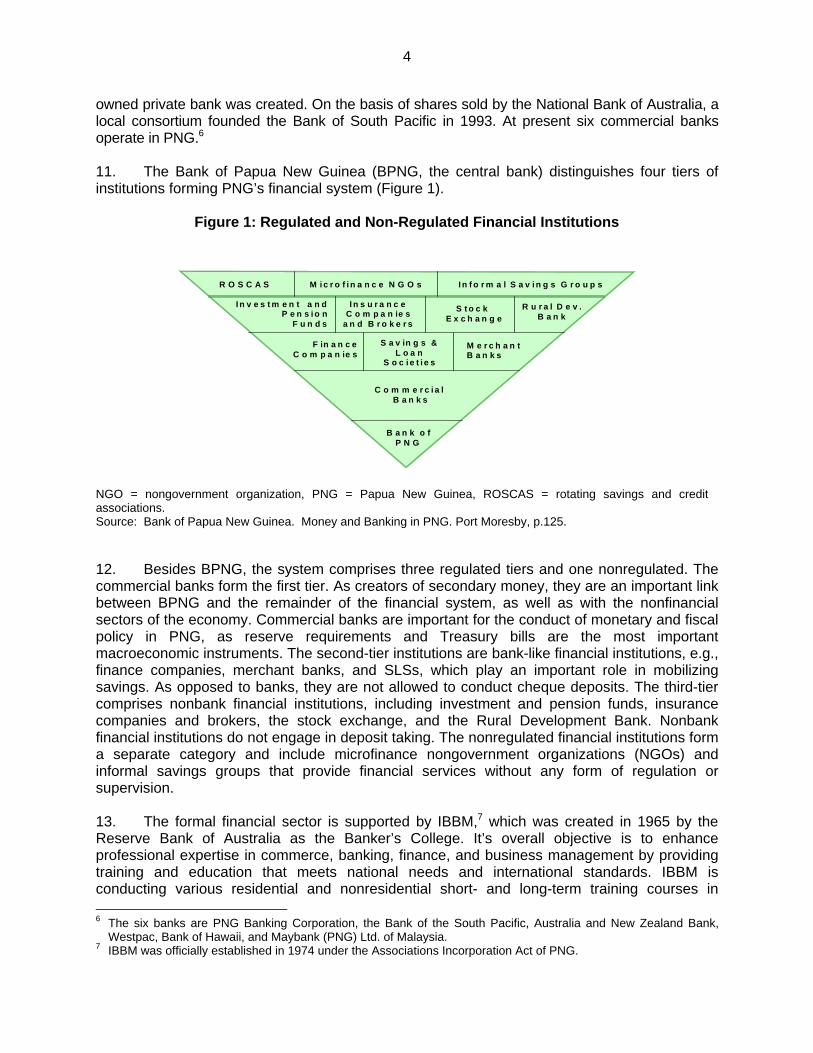

TO THE

INDEPENDENT STATE OF PAPUA NEW GUINEA

FOR THE

MICROFINANCE AND EMPLOYMENT PROJECT

September 2000

CURRENCY EQUIVALENTS(as of 15 September 2000)

Currency Unit – Kina (K)K1.00 = $0.370$1.00 = K2.703

The kina floats freely. For calculations in this report, an exchange rate of K2.5 to $1.00 hasbeen used, which was the rate prevailing at the time of appraisal.

ABBREVIATIONS

ADB – Asian Development BankAusAID – Australian Agency for International DevelopmentBPNG – Bank of Papua New GuineaEU – European UnionIBBM – Institute of Banking and Business ManagementLLDAT – Lik Lik Dinau Abitore TrustMCC – microfinance competence centerMFI – microfinance institutionMSC – microfinance steering committeeNCD – National Capital DistrictNGO – nongovernment organizationNWCP – National Women’s Credit ProjectPNGBC – Papua New Guinea Banking CorporationPIU – project implementation unitPNG – Papua New GuineaRDB – Rural Development BankRFF – revolving finance facilityROSCAS– rotating savings and credit associationsSLS – saving and loan societySOE – statement of expendituresTA – technical assistanceVFL – Village Finance LimitedUNDP – United Nations Development ProgrammeZOPP – Ziel-Orientierte Projekt Planung

NOTES

(i) The fiscal year of the Government and its agencies ends on 31 December.(ii) In this report, "$" refers to US dollars.

CONTENTS

Page

LOAN AND PROJECT SUMMARY ii

MAP vi

I. THE PROPOSAL 1

II. INTRODUCTION 1

III. BACKGROUND 1

A. Poverty Conditions 1B. Sector Description 3C. Government Policies and Plans 11D. External Assistance to the Sector 11E. Lessons Learned 12F. ADB’s Sector Strategy 13G. Policy Dialogue 14

IV. THE PROPOSED PROJECT 14

A. Rationale 14B. Objective and Scope 16C. Cost Estimates 20D. Financing Plan 20E. The Executing Agency 21F. Implementation Arrangements 21G. Environmental and Social Measures 25

V. PROJECT JUSTIFICATION 26

A. Financial and Economic Analyses 26B. Impact on Poverty 27C. Risks 28

VI. ASSURANCES 28

A. Specific Assurances 28B. Conditions for Loan Disbursement 29

VII. RECOMMENDATION 29

APPENDIXES 31

LOAN AND PROJECT SUMMARY

Borrower Papua New Guinea (PNG)

Project Description The Project will assist the Government enhance privatesector-led economic growth and employment creation. Thiswill be achieved through the provision of sustainablemicrofinance services to viable enterprises as well assavings facilities to the population at large. The Project willstrengthen the institutional capacity of at least 40potentially sustainable existing and new microfinanceinstitutions (MFIs). It will establish a microfinancecompetence center to provide training and on-sitecounseling to MFIs; develop, test, and implement newclient-oriented saving services and loan products; andestablish a revolving finance facility to provide neededcapital to MFIs for onlending. Reduction of poverty byintegrating the poor into the mainstream developmentprocess is the goal.

Classification Primary: poverty reductionSecondary: economic growth

EnvironmentalAssessment

Category CEnvironmental implications were reviewed, and no adverseenvironmental impacts were identified.

Rationale Poverty is of increasing concern to the Government.Approximately 31 percent of the population live below thepoverty line of $1 per day. To a large extent this can beattributed to the incomplete transition from a purelysubsistence economy to a modern cash-based economy.Poverty in PNG is directly linked to the inability to earnsufficient cash income to pay for school fees, health care,and other nonfood items, and to save for futurerequirements and times of hardship.

The formal sector can only provide a small number of jobs.Income-earning opportunities for the majority of thepopulation will need to come from smallholder agriculture,and micro and small enterprises in agroprocessing andtrading. The growth of the micro and small enterprisesector is currently inhibited by (i) lack of vocational skills,(ii) deterioration of the law and order situation, (iii) poorinfrastructure, and (iv) limited provision and restrictedaccess to financial services. Efforts are under way toovercome the first three of these impediments. Sustainablemicrofinance services are still needed.

iii

PNG’s financial system displays a significant institutionalgap, which leaves micro and small enterprises,semisubsistence farmers, and poor households without anyfinancial services. MFIs are scattered across PNG, andoperate in isolation and without clear perspectives. Theknowledge of microfinance best practice is limited. Theability to design appropriate savings and loan products tosuit clients’ needs is nonexistent. None of the existingservice providers have the institutional capacity to achievesustainability in the near to medium-term.

Microfinance initiatives require support measures toenhance their institutional capacity to ensure thesustainable delivery of microfinance services to a largenumber of micro and small enterprises, and to providesavings facilities to the poor and currently unservedpopulation. The Project is designed to address these needsthrough the establishment of a microfinance competencecenter and a revolving finance facility for MFIs.

Objective and Scope The objective of the Project is to provide sustainablemicrofinance services to viable enterprises and savingsservices to the population at large. The project strategy toachieve this objective is based on building the institutionalcapacity of potentially sustainable MFIs. The Projectcomprises three components: component A, establishmentof a microfinance competence center; component B,development, testing, and implementation of new savingsand loan products; and component C, establishment of arevolving finance facility. The Project will provide thenecessary expertise, training, counseling, and someequipment to enhance the MFIs’ institutional capacity. Studytours and visits to successfully operating MFIs in Asia, andin-country conferences and workshops will provideexposure to best practices in microfinance. Resources willbe made available to fund a pilot microbanking schemeand the revolving finance facility.

Cost Estimates The total cost of the Project is estimated at $20.5 millionequivalent, comprising $9.1 million in foreign exchangecosts and $11.4 million equivalent in local currency costs.

Financing Plan Proposed ADB financing is estimated at $9.6 millionequivalent (47 percent of total cost). Government financingwill amount to $4.7 million equivalent (23 percent of totalcost). Counterpart funding of $1.2 million will be provided bythe Institute of Banking and Business Management and $0.5million by the Bank of PNG. The MFIs’ contribution isestimated at $3.7 million equivalent. Grant cofinancing willbe provided by the Australian Agency for InternationalDevelopment ($0.9 million).

iv

Loan Amount andTerms

Based on the present allocation of funding, the loan wouldamount to $9.6 million from the ADB’s Special Fundsresources. The loan would bear a 32-year maturity, includingan 8-year grace period, with 1 percent interest charge duringthe grace period and 1.5 percent during the remainingperiod.

Period of Utilization Until 31 December 2006

Executing Agency Bank of Papua New Guinea (BPNG, the central bank)

ImplementationArrangements

The Institute of Banking and Business Management will bethe Implementing Agency for components A and B, andBPNG will directly implement component C. BPNG will setup a project steering committee to guide and coordinateimplementation. A project implementation unit will beestablished for day-to-day administrative andimplementation matters.

Procurement Procurement of goods and services financed under theProject will be in accordance with ADB’s Guidelines forProcurement. Procurement of vehicles, computers, andother office equipment will be subject to internationalshopping procedures. Furniture, training materials, andrelated service contracts, each below $100,000 equivalent,will be awarded on the basis of direct purchaseprocedures.

Consulting Services The Project will require an estimated 144 person-months ofinternational consulting services to assist in (i) building MFIinstitutional capacity, (ii) developing curriculum and trainingfor MFIs, (iii) developing microfinance products, and (iv)establishing a revolving finance facility. In addition,domestic consultants to support project implementation, andtraining and on-site counseling of MFI staff will render 240person-months of services. All consultants to be financed byADB will be selected and engaged in accordance with ADB’sGuidelines on the Use of Consultants and otherarrangements satisfactory to ADB on the engagement ofdomestic consultants. The international consultants will beengaged as a team from a firm.

Estimated ProjectCompletion Date

30 June 2006

Project Benefits andBeneficiaries

More than 45,000 people will directly benefit from theProject. These beneficiaries comprise poor households,micro and small enterprises, and semisubsistence farmers.At least 40 potentially sustainable, existing, and new MFIs

v

will benefit from the Project. The MFIs will provide reliablesavings facilities and access to tailor-made loan productsto the people.

vi

I. THE PROPOSAL

1. I submit for your approval the following Report and Recommendation on (i) a proposedloan to the Independent State of Papua New Guinea (PNG) for the Microfinance andEmployment Project (Project); and (ii) proposed administration by the Asian Development Bank(ADB) of a grant for the Project to be provided by the Australian Agency for InternationalDevelopment (AusAID).

II. INTRODUCTION

2. At the request of the Government, ADB provided technical assistance (TA)1 to preparethe Microfinance and Employment Project for possible ADB financing in 2000. The TA startedwith the Microfinance Best Practice conference in February 2000 in Lae with broad participationfrom a wide range of stakeholders and practitioners. Field surveys covering three of the fourregions of PNG were carried out to assess the credit needs of micro and small enterprises, thedemand for saving facilities, and the capacity and weaknesses of current microfinanceproviders. The resulting report was discussed during a participatory project planning workshopin March 2000, during which the goal-oriented project planning (ZOPP)2 method was appliedand resulted in the project framework given in Appendix 1. Participants included representativesfrom national and provincial government agencies, microfinance institutions (MFI), savingsgroups, savings and loan societies (SLSs), the central bank, commercial banks, the Institute ofBanking and Business Management (IBBM), private sector, and bilateral and multilateralassistance agencies. The ADB Loan Fact-Finding Mission was fielded 19–30 March 2000. Thiswas followed by the Appraisal Mission from 19 June – 7 July 2000.3 In addition, the Missionvisited Bulolo and Wau in the Momase region, and in Wau, discussed in detail the possibility ofpilot testing a microbanking scheme. The national and district governments expressed stronginterest in and support for the proposed Project.

III. BACKGROUNDA. Poverty Conditions

3. After 25 years of political independence and some economic and social progress, a largepercentage of the people of PNG remain poor. The human poverty index for PNG is at the level ofBurundi and Mali, which are among the most poverty afflicted nations in the world. The 1996household survey indicated that 31.0 percent of PNG’s population live below the poverty line of $1per capita per day.4 The incidence of poverty is high compared with countries with similar percapita income levels. Approximately 17 percent of the population cannot meet the basicrequirement of 2,200 calories per day per adult equivalent, even if they spend all their income onfood.

4. The poverty coexists with wealth. The richest 10 percent of the population account for 36percent of consumption, whereas the poorest 50 percent account for just 20 percent. The Gini 1 TA 3315-PNG: Microfinance and Employment, for $150,000, approved on 29 November 1999.2 ZOPP, from the German term “Zielorientierte Projekt Planung” is a project planning and management method that

is based on two techniques — matrix building and stakeholder workshops. The main output of a ZOPP session is aproject planning matrix equivalent to a project logical framework, to provide in-depth analysis of project objectives,outputs, activities, and performance indicators and risks. It encourages brainstorming, strategizing, informationgathering, and consensus building among stakeholders.

3 The mission comprised A. Iffland, Project Economist and Mission Leader; and O. Tiwana, Counsel. The Missionwas assisted by T. Schiller, staff consultant.

4 World Bank. 1999 Papua New Guinea: Poverty and Access to Public Services, Report No. 19584-PNG. The $1 aday is at 1985 prices converted to the national currency at a purchasing power parity exchange rate.

2

coefficient of 0.461 is high by comparison with countries of similar income levels. This is in largepart a reflection of the dualistic pattern of growth during the postindependence period. Growth hasbeen led by a capital-intensive minerals sector generating state revenues used in part to support alarge public service. The semisubsistence sector on which the vast majority of the populationdepends has shown little growth. Per capita real gross domestic product in the nonminingeconomy grew at the average rate of just 0.2 percent per annum during 1978–1998.

5. Poverty in PNG has an important regional dimension with the vast majority of the poor(93.3 percent) living in rural areas. The incidence and extent of poverty vary significantly acrossthe five major regions (Table 1). The Momase and North Coast region exhibits the highestincidence of poverty, with 45.8 percent of the population living below the poverty line. Povertyrates in the regions of Papua and South Coast, the Highlands, and the New Guinea Islands areclustered slightly below the national average, ranging from 33.2 to 35.8 percent. The urbanizedNational Capital District (NCD) accounts for only 3.8 percent of the poor; only a quarter of theNCD’s population lives below the poverty line. The depth of poverty, measured by the povertyseverity index,5 is twice as high in the poorest Momase and North Coast region as in the NCD.

Table 1: Poverty Measures by RegionRegion Headcount Index Poverty Severity % of total

PopulationIndex Contribution to

total (%)Index Contribution

in total (%)

NCD 25.8 3.8 3.3 3.3 5.5Papua and South Coast 33.2 13.2 5.5 14.7 14.9Highlands 35.8 38.3 5.3 38.0 40.1Momase and NorthCoast

45.8 35.5 6.6 34.2 29.2

New Guinea Islands 33.6 9.2 5.3 9.8 10.3PNG Total 37.5 100.0 5.6 100.0 100.0Urban 16.1 6.5 1.6 4.2 15.1Rural 41.3 93.5 6.3 95.8 84.9

NCD = National Capital District, PNG = Papua New Guinea.Source: Papua New Guinea. 1996. Household Survey. Port Moresby.

6. The distribution of poverty can also be viewed in terms of the regional distribution ofnational poverty. The Momase region accounts for almost 36 percent of the poor in PNG, but hasonly 29 percent of the population. The Highlands, with about 40 percent of the population,accounts for 38 percent of the poor. Hence, over three quarters of the poor population of PNG livein these two regions. Measuring poverty with the distributionally sensitive poverty severity indexindicates the same two regions account for over 70 percent of PNG’s poverty.

7. The incidence of poverty in PNG is linked to the ability to earn cash income to pay fornonfood items, to vary and improve diets, and to permit savings for times of economic difficulty(e.g., drought). Almost 17 percent of the poor population live in households where the householdhead earns no cash income, relying entirely on subsistence production (and perhaps gifts ofcash). The poverty rate for these households is 47 percent. Almost 8 percent of the poor live in

5 The poverty severity index is a distributionally sensitive poverty measure that takes into account the distribution of

consumption of those falling below the poverty line. This index shows that poverty is significantly deeper in ruralareas of PNG than in urban areas.

3

households, whose main source of cash income is hunting, gathering, and fishing. The povertyrate for these households is 57 percent. Poverty rates are also above the national average forhouseholds that earn cash income from tree crops (44 percent) and commercial agriculture (42.7percent). These households account for 42.5 percent and 19.0 percent of the poor population,respectively. Where household heads earn cash income from running a business or wageemployment, poverty rates are much lower (at 25 percent and 17 percent, respectively). Althoughthe latter households collectively account for 29 percent of PNG’s total population, they accountfor only 14 percent of the poor population. In general, increased provision of opportunities forearning secure cash incomes is needed to reduce the incidence and severity of poverty.

8. Both the extent of income-earning opportunities and the ability to respond to suchopportunities are determined to a significant degree by access to the basic public services oftransport, utilities, health, education, and financial services. The PNG population as a wholeexpressed considerable dissatisfaction with access to services in 1996, and it is highly likely thatthe degree of dissatisfaction increased during the late 1990s as a result of a widely acknowledgeddeterioration in service provision. Poverty reduction requires improved service delivery to ruralareas. This was the intention of provincial and local government reforms introduced under theOrganic Law of 1995, but effective implementation of devolution has been limited by capacity andfunding constraints.

9. The fundamental and long-recognized development challenge for PNG is to achievesustained economic growth with equity. The poorest 40 percent of the population must participatein, and benefit from, the growth process if poverty is to be reduced. Hence, poverty interventionshave to be primarily targeted at rural areas where the vast majority of the poor live. There aresevere development constraints, including the rugged terrain of PNG’s 462,000 square kilometers,the complexity of land tenure systems, the dispersal of 4.5 million people collectively speakingwell over 700 languages, limited and deteriorating physical infrastructure, a major law and orderproblem, and the low level of human resource development. Nonetheless, some key developmentconstraints can be eased over time through appropriate government action, notably for investmentin human capital, better service delivery including access to finance by the rural areas, andinfrastructure improvement. The Government is committed to addressing these issues to reducepoverty and socioeconomic inequalities through private sector-led growth and employmentcreation (para. 33).

B. Sector Description

1. The Financial System

10. Banking history in PNG dates back to 1916, when the Bank of New South Wales opened abranch in Port Moresby. It was set up mainly to carry out payment transactions, and to meet thecredit needs of the modern business sector, the working capital needs of plantations, and theforeign trade sector. Until after the Second World War, no other bank established branches in thecountry. Up to 1974 the system was essentially a small extension of the Australian system withpolicies decided by management outside the country. With independence, the PNG branch of theCommonwealth Banking Corporation was transferred to the Government and started to work asthe first PNG-owned bank under the name of Papua New Guinea Banking Corporation (PNGBC).Although, there was little utilization of trade or credit facilities by the local population, considerableuse was made of savings account facilities. In 1970, Papua New Guineans held nine tenths of thetotal number of 400,000 savings accounts, which accounted for one third of the total value. From1973 to 1986, PNGBC systematically extended the banking network to all provinces. While allforeign-owned banks were incorporated locally by 1976, it took 20 years until the first nationally

4

owned private bank was created. On the basis of shares sold by the National Bank of Australia, alocal consortium founded the Bank of South Pacific in 1993. At present six commercial banksoperate in PNG.6

11. The Bank of Papua New Guinea (BPNG, the central bank) distinguishes four tiers ofinstitutions forming PNG’s financial system (Figure 1).

Figure 1: Regulated and Non-Regulated Financial Institutions

B a n k o fP N G

C o m m e r c i a l B a n k s

F in a n c eC o m p a n ie s

M e r c h a n tB a n k s

S a v in g s &L o a n

S o c i e t i e s

I n v e s t m e n t a n dP e n s i o n

F u n d s

I n s u r a n c eC o m p a n ie s

a n d B r o k e r s

S t o c k E x c h a n g e

R u r a l D e v .B a n k

R O S C A S M i c r o f i n a n c e N G O s I n f o r m a l S a v i n g s G r o u p s

12. Besides BPNG, the system comprises three regulated tiers and one nonregulated. Thecommercial banks form the first tier. As creators of secondary money, they are an important linkbetween BPNG and the remainder of the financial system, as well as with the nonfinancialsectors of the economy. Commercial banks are important for the conduct of monetary and fiscalpolicy in PNG, as reserve requirements and Treasury bills are the most importantmacroeconomic instruments. The second-tier institutions are bank-like financial institutions, e.g.,finance companies, merchant banks, and SLSs, which play an important role in mobilizingsavings. As opposed to banks, they are not allowed to conduct cheque deposits. The third-tiercomprises nonbank financial institutions, including investment and pension funds, insurancecompanies and brokers, the stock exchange, and the Rural Development Bank. Nonbankfinancial institutions do not engage in deposit taking. The nonregulated financial institutions forma separate category and include microfinance nongovernment organizations (NGOs) andinformal savings groups that provide financial services without any form of regulation orsupervision.

13. The formal financial sector is supported by IBBM,7 which was created in 1965 by theReserve Bank of Australia as the Banker’s College. It’s overall objective is to enhanceprofessional expertise in commerce, banking, finance, and business management by providingtraining and education that meets national needs and international standards. IBBM isconducting various residential and nonresidential short- and long-term training courses in 6 The six banks are PNG Banking Corporation, the Bank of the South Pacific, Australia and New Zealand Bank,

Westpac, Bank of Hawaii, and Maybank (PNG) Ltd. of Malaysia.7 IBBM was officially established in 1974 under the Associations Incorporation Act of PNG.

NGO = nongovernment organization, PNG = Papua New Guinea, ROSCAS = rotating savings and creditassociations.Source: Bank of Papua New Guinea. Money and Banking in PNG. Port Moresby, p.125.

5

banking, finance, and business management for staff of commercial banks in PNG and thePacific region, and private sector enterprises. All commercial banks in PNG, the central bank, aswell as the Teachers Savings and Loan Society, the largest SLS in PNG, are members of IBBM.

14. The structure of this potential market for microfinance services is shown in Figure 2.

Figure 2: Toward Mainstream Financial Services

15. The upper end of the market, the peak of the pyramid, comprises people that haveaccess to financial services, and the lower end of the market, the base of the pyramid, consistsof people engaged in nonremunerated subsistence activities. The potential market formicrofinance services is between those two market segments with an estimated number of851,000 potential customers. Taking a conservative stand, it can be assumed that at least onethird of this market has actual demand for credit.8 This amounts to 255,000 potential borrowers.Based on an average loan size of $240 the total demand for credit would amount to $61 million.Using a loan size of $800, more appropriate for microenterpises and small farmers, the amountincreases to $200 million. Appendix 2 provides details on the micro and small enterprise sector.

16. With regard to savings, existing regulated and nonregulated financial institutions areoffering deposit-taking facilities to some extent. PNGBC plays the dominant role in savingsmobilization with a total of 465,765 passbooks and transaction accounts, and an averageaccount balance of $141. PNGBC expanded its network of branches in urban centers andagencies in remote areas until the mid-1980s. The worsening security situation increased thecost of operations to an unsustainable level and subsequently forced PNGBC to reduce itsnetwork substantially. From 407 agencies in 1984, only 87 remained in operation in 1997. Thewithdrawal of this financial service, particularly from the rural and more remote areas, hascreated a vacuum and at the same time a niche for informal savings groups to be established.

2. Providers of Microfinance Services

17. Microfinance providers can be found in each of the different tiers that comprise thefinancial system. Among the first tier institutions, there are currently two commercial banks 8 Results of the sample survey of micro and small enterprises and their perceived credit needs, part of the TA

(footnote 1), as well as information provided by commercial banks on the requests received for personal loanssuggest that the demand for credit is in the range of 300,000 potential borrowers.

Banks and Financial Institutions

MicrofinanceInstitutions

Credit Savings Insurance

Upgrading

Downscaling

High-End Market

Low-End Market

16.800 (1%)

851.000 (55%)

691.000 (44%)

6

offering financial services suitable for the microfinance market, PNGBC and to a lesser extent,the Bank of the South Pacific. Both banks offer deposit services, with PNGBC playing the keyrole in mobilizing savings in PNG. From a total of $415 million of PNGBC’s demand and termdeposits, $127 million correspond to a total of 465,765 passbook and transaction accounts, withan average account balance of $141. Compared with the strong involvement in mobilizing smallsavings, PNGBC is not significantly active in the field of microcredit. Of a total loan portfolio of$257 million, only an outstanding balance of approximately $1.2 million (0.18 percent) belongsto nearly 800 credits disbursed to the microfinance sector. According to PNGBC’s estimates,about 40 percent of the corresponding portfolio is at risk. Based on this performance and theGovernment’s plan to privatize PNGBC, its engagement in microcredit will decrease in thefuture.

18. The bank-like financial institutions, the second tier, the SLSs, and Village FinanceLimited (VFL) provide microfinance services. While the commercial banks were always orientedto the modern economy, the SLSs were originally conceived in the 1960s by the Reserve Bankof Australia to promote financial education and development in rural areas, encourage savings,provide credit, and support small capital formation. After independence the system of SLSscame under the supervision of BPNG. Most SLSs are affiliated with the PNG Federation ofSavings and Loan Societies. Notwithstanding the original rural orientation of the SLSs, urban-based societies became increasingly important during the 1980s. Generally, urban societies arecentered on common employment, and often secure contributions through payroll deductionschemes. During the 1980s many SLSs ran into problems with high loan delinquencies due tomismanagement and inexperienced staff. As a consequence, today most SLSs are eitherdormant or were liquidated by BPNG. As of December 1998, there were 21 SLSs in the countrywith a total membership of 64,025 and a savings balance of $47 million equivalent to anaverage savings balance of $737 per member. Since 1998, BPNG has carried out arevitalization program and introduced five new regional SLSs. To avoid the problems of thepast, almost all SLSs have established a maximum loan amount equivalent to the amount ofindividual savings held with the institution. A considerable amount of savings deposits ischanneled either as deposits to the commercial banks or is invested in Government bonds.While SLSs are important service providers, particularly to the urban middle class, the size ofthe system, in terms of assets and loans, is insignificant when compared with the commercialbanks.

19. VFL was founded in 1998 as a wholly owned subsidiary of PNGBC with initial capital of$400,000. It is a special purpose financial institution established to deliver microfinance servicesthroughout PNG. In 1999, VFL obtained a financial institutions license, which requires targetingthe underprivileged and returning all profits for investing in microfinance. VFL started fieldoperations in 1999. With a group lending methodology, the company targets poor women inrural and urban areas. By December 1999, there were 156 outstanding loans with an averagesize of $144 and a portfolio at risk of less than 5 percent. On the savings side, 376 compulsoryand voluntary savings accounts exist, with an average balance of $19. As of March 2000, VFL isauthorized to extend individual loans of up to $12,000.

20. As part of the third tier comprising nonbank financial institutions, the Rural DevelopmentBank (RDB), founded in 1967, is one of the Government’s financial instruments to promotedevelopment in urban and rural areas. RDB maintains a small network with seven branches and11 representative offices. It has always been a credit supply institution with no deposit facilitiesfinanced by the national Government budget. Unlike other development banks, it was neverused as a conduit for foreign investment, although during the 1980s the World Bank and ADBestablished credit lines for onlending for approved agricultural development projects. Like many

7

other development banks, RDB has a bad loan portfolio with large credits targeted to priorityprojects and granted on subsidized interest rates. Because of its poor repayment rates in 1998,RDB had to write off $8 million of a total loan portfolio of $24 million. To save RDB, theGovernment provided capitalization with a one-off transaction of $12 million. In the future RDBwill concentrate on priority banking for the most profitable clients of the existing loan portfolio. Atthe end of 1998, RDB’s total assets were valued at $35 million, with $12 million in loans andadvances and an even higher amount invested in profitable Government T-bills ($13.5 million).The portfolio at risk lies in the range of over 70 percent. Approximately 12 percent of theoutstanding loans, or 2,400 credits with an average loan size of $1,225 correspond to themicrofinance market. These loans form part of a small loan program established to financesmall capital investments like outboard motors, basic capital equipment, and farming supplies.

21. The nonregulated financial institutions form the fourth tier of the financial system andcomprise various microfinance and microcredit schemes. The Papua New Guinea NationalWomen’s Credit Project (NWCP), a project initiative of the Department of Home Affairs and theNational Council of Women, was established in response to the 1987 National Women’s Policyto deliver credit to underprivileged poor women. While several pilot phases had rather poorperformance, with the exception of the program in the Western Highlands, in 1996 the NWCPwas implemented nationwide with total funding of $1 million. The NWCP seeks to strengthenwomen’s associations at the district level to serve as conduits for servicing credit needs of groupbased, noncollateralized, rural and urban women borrowers. To date, the NWCP is operationalin approximately 41 districts. By December 1999, the estimated value of the loan portfolio wasabout $120,000, with 1,250 loans outstanding and an average loan size of $112. The portfolio atrisk is in the range of above 50 percent. Approximately 8,200 women are affiliated with thewomen’s district credit associations for the purpose of credit.

22. Lik Lik Dinau Abitore Trust (LLDAT), the best-known and most-documented NGOengaged in microfinance in PNG, emerged from the collaboration of seven parties, includinggovernment departments: PNGBC; United Nations Development Programmme (UNDP);National Council of Women; and the Foundation of Law, Order, and Justice. The LLDAT beganoperation in 1994 with the objective to provide savings and credit facilities to very poor mainlyrural women. It was founded explicitly to replicate the Grameen Bank model. After a promisingbeginning, LLDAT’s performance was severely affected by the lack of institutional capacity andliquidity problems. To date, there are 2,704 group members affiliated with the trust. ByDecember 1998, LLDAT had an outstanding loan balance of $85,000, with 1,493 groupmembers and an average loan size of $195.9 According to recent estimations, the portfolio atrisk is above 50 percent.

23. The North Simbu Rural Development Project established a microcredit scheme with thesupport of the provincial government, the provincial council of women, and the AustrianVolunteers Service. The scheme targets women and applies a group approach, with loans givento individual members of the group. During the 16 months since inception, the project processeda total of 630 loans, with 36 currently outstanding. The overall repayment rate is 94 percent, theaverage loan size $200.

24. In response to the lack of adequate rural finance facilities, in 1995 the LutheranDevelopment Service initiated the Putim na Kisim Project. It aims to establish savings cells atthe village level as the basis for the development of rural saving and loan societies. The project

9 According to the last audited financial statements from December 1999.

8

is seen as a pure bottom-up approach, and thus as an alternative to the governmentrevitalization program for SLSs. A vital role in the project concept is played by the integratedYangpela Didiman Program, run by the Lutheran Development Service for more than 25 years.Village people are trained to serve at the village level as volunteer development workers. In theirrole of multipliers, their aim is to improve agricultural and basic livelihood skills and to fosterspiritual development throughout their community. To date, there are more than 3,000volunteers in hundreds of villages. The Putim na Kisim Project relies on this existing structure toadd village banking to the multipurpose program portfolio of the Yangpela Didiman Program.Currently, there are 20 saving cells operating in the framework of the pilot phase. The savingcells have 817 members, with total savings of $29,000. The average individual savings balanceis $31. Lending is to start in 2000, and the methodology will be similar to that applied by theSLS: the loan amount will be determined by the individual savings balance, interest rates will bein the range of 10 percent per annum.

25. The VVN Saving Society in East New Britain Province is an example of the informalsavings schemes that exist throughout PNG. The society was established in 1997 through theinitiative of a member of the village community. The 700 members save voluntarily, with acurrent savings balance of $40,000. Funds are held in a group savings account with PNGBC.There are no minimum balance requirements, and withdrawals can be made without limitationsthree days per week.

26. All MFIs and budding microfinance initiatives have a number of characteristics incommon. They are scattered all over PNG, mainly in rural areas, and operate in isolation andwithout clear perspectives. The knowledge of microfinance best practice is rather limited, whichis reflected by a microfinance landscape dominated by Grameen Bank replications irrespectiveof their appropriateness and suitability for PNG. The ability to design appropriate savings andloan products to suit the needs of the clients is generally very weak. The majority of MFIs sufferfrom lack of well-defined and transparent governance and management structures, and theabsence of an effective management information system. The managers and the loan officerslack even basic training to adequately carry out their jobs. MFIs are undercapitalized and haveno mechanism to raise additional funds for onlending through deposits or from formal financialinstitutions. Taking all these factors into account, it is not surprising that none of the MFIs haveachieved financial viability and have no vision on how to achieve it. Details are in Appendix 3.

3. Demand for Microfinance Services

27. The size and structure of the potential market for microfinance services is based on thestructure of the economically active population. Figure 3 distinguishes between wage income,nonwage earning, and income in-kind.

9

AssetsAssets LiabilitiesLiabilities

MoneyClaims from WantokTools and EquipmentAnimalsUsing rights of LandCoffee/Palm treesGardensHouse

• Claims of Wantok

• Credit of supplier

• Credit from MFI

• Equity

Figure 3: Regional Distribution of Income per Capita (1996 in Kina)

NCD = National Capital DistrictSource: Papua New Guinea. 1996. Household Survey.

In 1996, the average per capita income in the provinces, excluding the NCD, amounted to about$400 (K1.000). The importance of monetary wage income as compared with monetary nonwageincome is decreasing in the more remote areas where income in-kind is the predominantsource. In more than twothirds of the provinces, the average monetary income is clusteredaround the poverty line of K46110 per adult equivalent per year. While wage earners in theprovinces are potential clients for savings products, their ability to use credit for nonconsumptivepurposes is limited. The nonwage earners receive their income from agricultural production andother business activities, and have an articulated demand for credit to be used for workingcapital and investments in their businesses.

28. A closer look at the assets and liabilities of a potential client will provide a betterunderstanding of the demand for microfinance services. This is done in a generic way and resultsin the balance sheet structure given in Figure 4.

Figure 4: Generic Balance Sheet of MFI-Clients

10 This poverty line of K461 is based on the cost of a food consumption basket that meets a minimum energy

requirement of 2,200 calories per adult equivalent per day and reflects the dietary pattern of the lower incomegroups (food poverty line).

- 200.0 400.0 600.0 800.0 1,000.0 1,200.0 1,400.0 1,600.0 1,800.0 2,000.0

Gulf

E/Sepik

New Ireland

Madang

W/Sepik

Manus

E/Highlands

Enga

Morobe

NCD

Wage Nonwage In Kind

10

29. Most striking is the important role of claims and liabilities that are related to the extendedfamily network of the wantok. These relationships are only partly valued in money and follow morethe logic of social reciprocity. Within the framework of PNG’s traditional culture, claims of thewantok are of higher priority than legal obligations outside the wantok system. This has to beunderstood as part of the social safety net of the traditional culture that is still predominant inalmost all parts of PNG society. From an economic point of view this allows a smallholder tohandle external shocks such as a draught by attending obligations within the wantok in a flexibleway. A wantok works as a form of extended equity that assumes part of the risk as well asparticipates in the return of an investment. For the purpose of demand targeting, this has to betaken into account. It would not be wise to try to compete or even to substitute the relationshipswithin the wantok with those of formal or semiformal financial institutions. As in the moderneconomy, the majority of funding for a small business would be related to equity, in the traditionaleconomy of PNG—with good reason—this most likely relates to the wantok. In both cases afinancial institution would always try to avoid the risk related to equity financing, and rather wouldinsist that existing equity covers the risk of a bank loan. The same is true when it comes to thewantok system, where an assessment is needed as to whether the wantoks stand ready to takesome of the credit risk or whether there is only a potential claim that actually increases the risk ofthe borrower.

30. With regard to savings products, the wantok system leads to the need for highly liquidproducts, and also for less liquid term deposits. As obligations toward wantok members may haveto be attended to on short notice, some liquidity is important, but at the same time, less liquid termdeposits can protect individual savings from being siphoned off by the wantok system.

31. The following figures on the structure of the economically active population in PNG givesome indication of the demand and the potential market for microfinance services. Table 2distinguishes between remunerated and nonremunerated economic activities.

Table 2: Economically Active Population

Persons Target

Monetary 1990 1996 % % Persons %

Wage Job 240,763 277,418 24 9

Business 14,580 1 6,800 1 1 16,800 1

Self-Employed 67,082 77,295 7 3 77,295 5

Professional Farm/Fish 671,954 774,256 68 27 774,256 50

Total 994,379 1,145,769 100Nonmonetary

Subsistence Farm/Fish 600,342 691,742 39 24 691,742 44

Student 347,469 400,370 23 14

Housework 275,567 317,521 18 11

Retired 63,965 73,703 4 3

Handicapped/Disabled 11,859 13,664 1 0

Unemployed 133,612 153,954 9 5

Others 107,840 124,258 7 4

T o t a l 1,540,654 1,775,213 100 100Population over 10 years 2,535,033 2,920,982 1,560,093 100

11

32. Within the remunerated part of the economically active population, 24 percent areclassified as employees receiving a wage income, 1 percent as entrepreneurs, 3 percent asself-employed, and 68 percent as engaged professionally in farming or fishing. Within thenonremunerated part of the total economically active population, 39 percent are in the categoryof subsistence farm or fishing activities. On the basis of the poverty assessment it can beassumed that at least the two last-mentioned categories comprise the poor. According to thisclassification, the target market for microfinance loan products (nonconsumption loans) willcomprise businesspersons, self-employed, and professional and subsistence farmers andfisherfolk. Based on the 1990 census, an estimated 1,5 million people will be in this group. Withregard to savings products, an additional 0.3 million people or 30 percent of the remainingeconomically active population, considered to not be integrated in the cash economy, can beadded.11

C. Government Policies and Plans

33. In the Medium-Term Development Strategy, 1997-2002, which was reconfirmed by thenew Government in 1999 and is reviewed annually, the Government emphasizes theimportance of private sector development for the future of PNG. This development priority wasreconfirmed during the National Dialogue in 2000. The development of a vibrant micro, small,and medium-size enterprise sector to spearhead economic growth is of specific importance tothe Government. This is reflected in the Small and Medium Enterprise Policy, approved in 1998.To improve the business environment, the policy identifies and addresses key issues andconstraints hindering business development. The Government aims to focus on the weaknessesof the financial system to improve the provision of financial services for private sectordevelopment. The Government perceives access to financial services as a key to enhancing theeconomic integration of micro and small enterprises and those who want to save money forfuture financial needs. Hence, the regulatory framework for banks and other financial institutionshas been revised, and new Central Bank and Banks and Financials Institutions acts weregazetted this year. A microfinance workgroup involving major stakeholders was established toprepare a microfinance policy to be submitted for Government approval by the end of 2000. Thedraft Microfinance Policy Paper is given in Appendix 4.

D. External Assistance to the Sector

34. The financial sector is receiving support at the macro level under the overall structuraladjustment program. This comprises advisory services by the Reserve Bank of Australia toreview PNG’s monetary policy. The World Bank is assisting BPNG with banking supervision,including nonbanks and SLSs. The International Monetary Fund has assisted with thedevelopment and introduction of the new Central Bank Act, and Banks and Financial InstitutionsAct.

35. In comparison with the support provided to BPNG, external assistance for microfinanceis rather fragmented. It ranges from setting up revolving credit funds as a part of largecomprehensive rural development projects and sector programs, to the provision of seed moneyto village communities and women’s groups. Most initiatives aim at reducing poverty anduplifting underprivileged groups of society, particularly women. International NGOs andvolunteer organizations, church-based institutions, private companies, and individuals are

11 Since the last census in 1990, the cash-based economy has strongly advanced. It can therefore be safely assumed

that a much larger percentage of the economically active population is partially or fully integrated.

12

involved. Neither the Government nor any other institution has an overview of the various actorsand the assistance provided.

36. LLDAT, the best-known and most-documented microfinance provider in PNG, was setup with TA and seed capital from UNDP. Insufficient funding and managerial and institutionalcapacity constraints led AusAID to provide rescue assistance. This includes capital and short-term advisory assistance. AusAID also provided support for a nine-month pilot project inBouganville, the Bouganville Haus Moni. The support focused on creating awareness forsavings, training community leaders, and establishing savings cells in selected districts.AusAID is considering providing assistance to the urban-based ItaKara development project todeliver financial and business development services in an integrated approach.

37. The European Union (EU) provided seed capital to the Bougainville Provincial Council ofWomen to set up a microcredit scheme. Implementation is rather slow and a recent progressevaluation suggested the redesign of the scheme, which will be implemented shortly. The EU isalso supporting the design and planning of a rural credit scheme for smallholder cocoa andcopra farmers in Bougainville.

E. Lessons Learned

38. During 1988-1998, ADB approved 15 microfinance projects, 6 projects with microfinancecomponents, and 34 TAs to support microfinance operations in the Asian and Pacific Region.ADB recently completed a review of its microfinance operations during this period.12 While TAhas been an important element in ADB’s microfinance activities, TAs suffered from a number ofdrawbacks: (i) lack of adequate sector analysis, (ii) insufficient institutional analysis and lack of acoherent long-term approach to institutional development, (iii) limited involvement ofstakeholders in the design of TA leading to problems of ownership, and (iv) lack of measurableand monitorable indicators to assess performance. The project preparatory TA for this Projectaddressed these shortcomings and emphasized the building of local ownership for the Project.

39. ADB’s microfinance project loans have improved over time. The early projects, the firstgeneration projects, in general (i) focused on microcredit delivery; (ii) allowed subsidizedinterest rates; (iii) paid little attention to financial viability; and (iv) were very poorly targeted. Inrecent years, the projects support a wider array of institutions, go beyond credit services toprovide voluntary savings on a limited scale, emphasize market-oriented interest rates, and paymore attention to financial viability.

40. Although it is difficult to reliably measure the development impact of finance services,assessments of the operations of already completed microfinance projects and review reportson the ongoing projects offer some important insights on the development impact of ADB’smicrofinance assistance. These projects provide a wealth of information and experiences. Themain lessons learned form the key areas of ADB’s Microfinance Development Strategy13:

(i) A financial systems development approach14 is the key to achieving sustainableresults and to maximizing development impact.

12 Asian Development Bank. 1999. Review of Asian Development Banks’ Microfinance Portfolio. Manila.13 Asian Development Bank. 2000. Finance for the Poor: Microfinance Development Strategy. Manila14 This approach emphasizes an enabling policy environment, financial infrastructure, and the development of

financial intermediaries that are committed to achieving financial viability and sustainability within a reasonableperiod and that can provide a variety of financial services.

13

(ii) Microfinance clients are more concerned about access to adequate services thanthe cost of the services.

(iii) A broad range of microfinance service providers is required to respondadequately to the diversity of demand for financial services and to expand theoutreach.

(iv) Considerable TA for capacity building is needed to build strong retail institutionswith a commitment to outreach and sustainability.

(v) The demand for savings services by poor households and microenterpises is asstrong, if not stronger, than the demand for credit. Expansion of the outreach ofsavings services can have a significant impact on both institutional sustainabilityof MFIs and poverty reduction.

41. An analysis of the microfinance projects supported by AusAID and the EU in PNGprovide insights on operational issues and requirements for microfinance services. Lessonslearned identify the following as important requirements for a successful microfinance project inPNG:

(i) transparent governance and management structure outside the influence ofGovernment,

(ii) business plan and a management information system to monitor keyperformance indicators,

(iii) training of management and loan officers,(iv) flexible savings and loan products based on the requirements of the clientele,(v) adequate equity to allow expansion.

42. The lessons learned and the insights gained from AusAID and EU-assisted microfinanceschemes, ADB’s completed and ongoing microfinance projects, as well as international bestpractice in microfinance as disseminated by the Consultative Group to Assist the Poor have hada strong influence on the design of all project components, which aim to provide microfinanceservices to the poor while achieving financial viability of MFIs.

F. ADB’s Sector Strategy

43. The ADB’s current country operational strategy for PNG was discussed by the Board inOctober 1998. It is in line with the Government’s Medium-Term Development Strategy andADB’s Medium-Term Strategic Framework and Strategy for the Pacific.

44. The strategy emphasizes the importance of financial services for economic and socialdevelopment in PNG. It recognizes the need to improve access to financial services particularlyin rural areas and for the poorer strata of the population. On the deposit side, limited access tomodern savings and transaction mechanisms, force the poor to hold cash and have an adverseeffect on the already serious law and order problem. On the funding side, very limited access tocredit continues to be a serious impediment to private sector development and sustainablegrowth. Better access to financial services will assist the poor to create microenterpises andgenerate broad-based income. This will lead to new employment opportunities, a keydevelopment objective of PNG. In the context of PNG and the rather limited success of variousmicrocredit schemes, institutional strengthening and capacity building of existing serviceproviders is crucial for the provision of sustainable microfinance services. The Project reflectsthese features, which are key elements of ADB’s microfinance strategy, and is designed toassist the Government in addressing identified shortcomings.

14

G. Policy Dialogue

45. Policy dialogue with the Government in this area was initiated in 1998 in conjunction withADB’s microfinance strategy. It was followed by a detailed sector analysis and studies coveringvarious aspects of microfinance, which provided the Government with valuable backgroundinformation and formed the basis for a continued dialogue with ADB microfinance specialists.With the mushrooming of microcredit schemes and revolving loan funds and their rather limitedsuccess, the Government is aware of the need to develop a common understanding ofmicrofinance issues and to provide general guidelines. The conference, Microfinance BestPractice in February 2000 (para. 2), supported this view and initiated the drafting of amicrofinance policy paper, that was discussed at the stakeholder workshop in March 2000. Thedraft policy paper is in Appendix 4.

46. At present MFIs are operating in an unregulated environment and without supervision.Recent experiences with money pyramid schemes has forced the Government to tighten theregulatory framework for financial institutions. While this is an important step toward a soundfinancial sector, the increased capital requirements of $600,000 equivalent restrict thepossibilities of microfinance providers acquiring a banking license and, thus, take deposits. Anagreement was reached by the stakeholders at the two workshops (para.2) that a regulatoryand supervisory framework for MFIs needs to be drawn up to facilitate service delivery and tosafeguard clients’ deposits. The Project will assist in drafting appropriate legislation for aregulatory and supervisory framework for MFIs to facilitate sustainable growth of microfinanceservices while proceeding with the much needed institutional capacity building of MFIs.

IV. THE PROPOSED PROJECT

A. Rationale

47. Poverty in PNG is an increasing concern of the Government. In 1996, 31 percent of thepopulation lived below the international poverty line of $1 per capita per day and evidencesuggests the situation is worsening. To a large extent this has to be attributed to the incompletetransition from a purely subsistence economy to a modern cash-based economy. The incidenceof poverty is directly linked to the inability of families to earn cash income to pay for school fees,health care, and other nonfood items, and to save for future requirements and times of hardship.

48. The formal private sector can only provide for a small number of jobs. Income-earningopportunities for the majority of the population will be in the agriculture sector, and inestablishing micro and small enterprises in manufacturing and trading. However, the growth ofthe private sector as a whole, and the micro and small enterprise subsector in particular, isinhibited by key factors; (i) lack of vocational and entrepreneurial skills; (ii) deteriorating law andorder situation; (iii) poor infrastructure, particularly rural roads; and (iv) limited provision andrestricted access to financial services.

49. The lack of vocational and entrepreneurial skills is a serious constraint to theestablishment of micro, small, and medium-size enterprises. Most enterprises are not in aposition to satisfy required quality standards, reliable delivery, or to offer competitive prices fortheir products. Apart from assistance provided by the EU and the AusAID, ADB is providingassistance through the Employment-Oriented Skills Development Project.15 Regarding

15 Loan 1706-PNG(SF), Employment-Oriented Skills Development, for SDR14,591,000, approved on 28 October

1999.

15

agricultural production and the need to improve the farming systems of small semisubsistenceand cash crop farmers, ADB is assisting through the Smallholder Support Services PilotProject.16

50. The deteriorating law and order situation has been cited as a significant deterrent tolocal as well as foreign investment, and adds to the high cost of doing business. As a result,commercial banks have closed many of their branches in the rural and more remote areas.

51. Poor infrastructure, particularly rural access roads, seriously restricts market access forboth agricultural and manufacturing products. Many provinces have no road links to neighboringprovinces. Others provinces experience frequent traffic interruptions due to poor maintenance ofexisting road links. This increases the isolation of rural communities and leads to significantlosses in export earnings and business income. Infrastructure improvements feature high on theGovernment’s development agenda and receive substantial support from all major bilateral andmultilateral assistance agencies. ADB is providing assistance through the Road Upgrading andMaintenance Project.17

52. Limited access to financial services for micro and small enterprises is another majorimpediment to private sector development (Appendix 2). PNG’s financial system displays aninstitutional gap that leaves micro and small enterprises, semisubsistence farmers, and poorhouseholds with barely any financial services. Commercial banks cater to the credit needs ofmedium and large enterprises, and with the exception of PNGBC, offer deposit facilities only toformally employed people with a regular salary. Various microfinance schemes have emergedover the past 10 years, the majority almost exclusively target poor women in the subsistencesector. By December 1999, there were less than 10,000 loans outstanding that can be classifiedas micro loans, in comparison with a potential demand for credit by approximately 255,00018

potential borrowers (para.15).

53. In principle there are two institutional strategies to introduce new financial services toPNG: (i) downscaling commercial bank operations and their products, and (ii) upgradingmicrofinance institutions. Both strategies have been discussed with the Government and aresupported by the microfinance policy framework currently being prepared. The Project followsthis approach and combines both institutional strategies.

54. To reduce the institutional gap and to expand and strengthen the microfinanceinstitutional landscape, the existing MFIs have to fulfill a dual mission: they have to achievefinancial self-sustainability, as well as increase outreach, both in scale (number of clients) and indepth (service delivery to the lowest income population possible). This will ultimately determinethe MFI’s contribution to the economic and social development of PNG. The challenge of anMFI consists thus in striking a balance between those two, at first glance opposing, objectiveskeeping in mind that the level of financial self-sustainability of an MFI will determine the scale ofits outreach. To be financially viable and to achieve considerable outreach with its services,MFIs must possess an adequate institutional capacity. Appendix 3 gives details on the strengthand weaknesses of MFIs in PNG.

16 Loan 1652-PNG, Smallholder Support Services, for $7.6 million, approved 10 December 1998.17 Loan 1709-PNG, Road Upgrading and Maintenance, $63 million, approved on 16 November 1999.18 These make up one third of the economically active population, which is classified as integrated in the cash

economy, self-employed, or engaged in professional farm/fishing.

16

55. None of the existing MFIs have the necessary institutional capacity to achievesustainability in the near future. All depend on seed money from either Government orassistance agencies for their lending operations. Without a banking license, MFIs are notpermitted to mobilize savings for onlending and other sources of funds are not available. Thisseverely restricts their operations in increasing outreach and achieving financial self-sustainability.

56. MFIs are scattered across PNG, and operate in isolation and without a clear perspective.In comparison with Asian countries, PNG’s microfinance sector is at an early stage ofdevelopment. The knowledge of microfinance best practice is rather limited and the ability todesign appropriate savings and loan products to suit the needs of the clients in PNG isnonexistent. Hence, Grameen Bank replications dominate the microfinance landscape. Whilethere are some promising features in a number of MFIs, none of the existing service providershas emerged as a market leader. All MFIs and microfinance initiatives in PNG require varioussupport measures to enhance their institutional capacity to ensure sustainable delivery ofmicrofinance services to a large number of micro and small enterprises, and to provide savingsfacilities to the poor and currently unserved population segment. The Government is aware ofthe shortcomings, is proceeding with the finalization of the microfinance policy, and has askedthat the Project foster the development of the microfinance sector.

B. Objective and Scope

57. The overall objective is to contribute to economic growth through private sectordevelopment, employment creation, and development of the financial system. The goal is toreduce poverty and integrate the majority of the poor19 into the mainstream developmentprocess. The Project’s specific objective is to provide sustainable microfinance services toviable formal and informal enterprises, and savings services to the population at large.

58. The Project comprises three main components: component A, capacity building of MFIsthrough a microfinance competence center; component B, development, testing, andimplementation of new savings and loan products and delivery methods; C, establishment of arevolving finance facility (RFF) for MFIs. In addition, the Project will establish a projectimplementation unit (PIU) to support the implementation of the three components.

59. The Project, through these three components, will build the institutional capacity ofvarious providers of microfinance services, who are the Project’s institutional target group. Inturn these MFIs, enabled to deliver sustainable services, will provide small business loans20 forworking capital and investment purposes to micro and small enterprises, particularly in ruralareas, where the vast majority of MFIs are operating. Savings services will be available tohouseholds in rural areas, where the majority of the poor live.

1. Microfinance Competence Center (Component A)

60. The Project will assist the Government to establish a microfinance competence center(MCC) within IBBM to enhance the institutional capacity of potentially sustainable MFIs. Theseinclude banklike institutions, e.g., SLSs and VFL, and nonregulated financial institutions, e.g.,NGO and government-run microfinance and microcredit schemes, ROSCAS, and informal

19 The Project targets poor households that earn cash income from horticultural and agricultural production, and from running a small business. These account for 75.5 percent of the poor population. 20 The average loan amount of each MFI portfolio will not exceed $2,000.

17

community savings groups. The MCC will set up a network of existing microfinance serviceproviders and thereby create a forum for policy implementation. By establishing the MCC theProject will institutionalize local capacity building needed to provide the required expertise andtechnical skills to expand financial services. The MCC will provide the following services:

(i) Public awareness and public relations activities will be developed for allmicrofinance service providers and their potential clients. Emphasis will beplaced on developing internal communication mechanisms between existingservice providers, through the formation of an MFI network. Through schools andother existing community channels, the network will publicize the basic conceptsof banking and the benefits of savings, and advertise the availability ofmicrofinance services. The MCC will assist MFIs in conceptualizing publicrelations strategies.

(ii) In-house training courses will broaden the understanding of microfinance andimprove the technical and organization skills of MFI staff involved in providingmicrofinance services. Study tours and in-country conferences and workshopswill facilitate upgrading of MFIs.

(iii) On-site TA and training will be designed to suit the specific requirements of anMFI, ranging from start-up assistance for newly formed MFIs, support programsto achieve sustainability of operations, specific assistance geared to expandservices, to guidance in the formalization process to acquire the status of aformal financial institution.

(iv) A consultative process between the network of MFIs and BPNG will be initiatedand facilitated to establish a regulatory and supervisory framework for MFIs.

(v) A rating system for microfinance service providers will be designed on the basisof internationally accepted best practices. MCC staff will be trained to carry outthe MFI assessments. The rating determines if an MFI will have access to theRFF (component C of the Project).

61. The Project will (i) provide international and domestic expertise, computer equipment,training materials, and upgrading of trainers to establish the MCC; and (ii) finance in-housetraining and on-site consultancies for MFIs, as well as study tours, workshops, and conferences;and support MCC management to develop a business plan and a strategy to achieve financialviability by the end of project implementation.

2. New Savings and Loan Products (Component B)

62. This component will develop and test new savings and loan products and deliverymethods for financial services, and will support MFIs in implementing them. Specific attentionwill be given to linking community savings groups with financial institutions. A pilot test willinvolve downscaling commercial banks. Microfinance products oriented to target groups will bedesigned, and MFIs will be advised on appropriate delivery mechanisms. One pilotmicrobanking scheme will be designed, and established and operated in Wau, a remote town inMomase, PNG’s poorest region. The Project will provide international expertise, equipment, andtraining to develop, test, and implement new savings and loan products, and equity for the pilotmicrobanking scheme. Specifically, the Project will

(i) establish dialogue between commercial banks and informal savings groups, anddesign detailed linkage modalities;

(ii) advise MFIs on appropriate microfinance products;

18

(iii) identify commercial banks interested in providing microfinance services, andprovide support in downscaling products and delivery methodologies;

(iv) design tailor-made savings and loan products for MFIs, and provide support andbackstopping to MFIs during initial implementation;

(v) design delivery mechanisms and marketing concepts for microfinance productsaddressing specific target groups;

(vi) monitor the performance of the delivery methods and disseminated information tothe MFI network; and

(vii) establish, operate, and document one pilot microbanking scheme.

63. Downscaling of commercial banks requires a variety of institution-building measures to(i) overcome the significant cultural gap between the formal financial sector and the boundariesof economic life of the rural population, and (ii) link business practices of the traditional economywith the principles of modern banking. Communities and community leaders must be activelyinvolved to provide information on borrowers, which is otherwise not available to formal banks.This underscores the need to develop a lending technology that takes into account a client’swhole socioeconomic environment. The creation of VFL by PNGBC is one example ofdownscaling. Latin American countries are at the forefront of successfully downscalingcommercial banks; some examples can also be found in Asia.

64. The pilot microbanking scheme will demonstrate the application of new savings and loanproducts and delivery mechanisms, based on international best practice and modified to PNG’sspecific requirements. All stages of the development process of the pilot scheme will bedocumented in detail to be used as a guide for new MFIs.

3. Revolving Finance Facility (Component C)

65. This component will establish the RFF, which will provide the necessary funding for MFIsto achieve sustainability and expand their loan portfolios. Credit lines and equipment loans willbe made available to eligible MFIs for onlending to micro and small enterprises. The projectinputs comprise short-term international expertise to finalize the details of these financialinstruments during the first eight months of project implementation, subject to approval by ADB,and prior to disbursement of loan proceeds to the RFF. The RFF will be set up withcontributions from the Government (60 percent) and ADB loan proceeds (40 percent).

66. To access the RFF, MFIs must meet the following eligibility criteria: (i) registration withthe MCC and satisfactory rating (not older than six months) issued by the MCC; (ii) satisfactoryloan repayments, as established by an on-time repayment rate of at least 85 percent; (iii) adetailed plan for operational and financial self-sufficiency with a strategy for improvements overthe next year and agreed performance targets; (iv) adequate management information andaccounting systems in place to ensure successful expansion, efficiency improvements, andsatisfactory performance of the loan portfolio; and (v) average loan amount of the MFI portfolioto be funded does not exceed K5,000 ($2,000). The maximum exposure of the RFF to onesingle MFI will not exceed 40 percent.

67. The conditions of credit lines are (i) credit lines to MFIs are made available in kina or indollars provided the MFI is able—on the discretion of the management agent—to hedge therelated foreign exchange risk; (ii) for credit lines extended in dollars the interest rate will be theapplicable 3-month LIBOR21 plus a reasonable margin to cover costs, and for credit lines

21 LIBOR = London interbank offered rate.

19

contracted in kina the interest rate will be the most recent kina auction rate 22 plus a reasonablemargin to cover costs; (iii) interest rates are payable on a monthly basis over the outstandingbalance; (iv) a penalty fee is charged in the event of late interest payments (arrears of more than30 days) of an additional 3 percent per annum; (v) a commitment fee of 0.25 percent per month ispayable by the respective MFI to the RFF for contracted but not yet disbursed balances of thecredit line; (vi) maximum maturity of the credit lines is 5 years; and (vii) maximum credit lineamounts are determined by the management agent on the basis of MFIs’ stage of development.The conditions of the credit lines are subject to periodic review by the management agent.Modifications of the conditions and the change of the interest rate are subject to approval by themicrofinance steering committee (MSC).

68. The MFIs will apply the following conditions for onlending to micro and small enterprises:(i) only business loans will be extended; (ii) the maximum maturity for loans to be used for workingcapital is up to 12 months and for fixed assets, equipment, or livestock (investment loans) up tothree years; (ii) loans are only granted in kina; (iii) the interest rate will be the kina auction rate ofthe BPNG plus a margin to be defined by the MFI on the basis of market rates ensuring thefinancial sustainability of the respective MFI.

69. BPNG, the Implementing Agency, will hold the funds of the RFF in a separate account,similar to previous arrangements with the World Bank and the EU. It will outsource the day-to-day management of the RFF to a private sector management agent, e.g., a private financeinstitution or other relevant private entity based in PNG. The selection of the management agentwill be in accordance with competitive procedures acceptable to ADB. This guarantees thenecessary independence, as well as efficient management of the funds. It also underscores theintended private sector orientation of microfinance in general and of this Project in particular.The management agent will be paid on a fixed fee basis and will carry out the following tasks: (i)financial management of the funds; (ii) administration of the RFF’s financial instruments; (iii)monitoring of MFI performance ensuring that performance targets are met; and (iv) quarterlyreporting to BPNG on performance of the RFF and the participating MFIs. The detailed terms ofreference for the management contract will be finalized during the first six months of projectimplementation. Detailed procedures for reporting and auditing will be put in place to ensuretransparency of operations.

70. ADB will disburse the first installment of $280,00023 direct to a special account managedby the management agent under the supervision of BPNG, provided the following conditions arefulfilled: (i) a management contract (approved by ADB) has been signed and is legally effectivebetween PBNG and the management agency, and (ii) a model agreement for onlendingbetween the management agent and MFIs has been approved by BPNG and ADB. Appendix 5provides details on the implementation arrangements.

4. Project Management

71. In support of the Executing and Implementing Agencies and to facilitate successfulimplementation of the three components, the Project will (i) build the capacity of the PIU by

22 The kina auction facility is a monetary management instrument introduced on 1 May 1995 in which BPNG can

accept deposits (buy kina) from commercial banks or lend (sell kina) to the commercial banks. BPNG announcesthe auction volume and the rate (kina auction rate) is determined by the market through competitive bidding. Therate is a weighted average of the successful bids received and allocated.

23 The first installment is 10 percent of ADB’s total contribution of $2.8 million and is the initial contemplated level ofdisbursement to MFIs within the first three months of operation of the RFF. The total amount of the RFF is $7million. ADB loan proceeds contribute 40 percent and the Government 60 percent to the RFF.

20

engaging domestic consultants, and (ii) establish a project monitoring and evaluation systemand a management information system for components A and B. Office furniture, computer, andother office equipment and transport will be provided to ensure that the PIU is able to carry outthese activities.

C. Cost Estimates

72. The total cost of the Project, including taxes and duties and interest during projectimplementation, is estimated at $20.5 million equivalent. The cost estimates are summarized inTable 3 and details are given in Appendix 6.

Table 3: Project Cost Summary($’000)

ComponentsForeign

ExchangeLocal

CurrencyTotal Cost

A. Microfinance Competence Center 3,217 2,669 5,886B. New Savings and Loan Products 1,879 1,666 3,454 B.1 Development and Testing (891) (1,604) (2,495) B.2 Pilot Microbanking (988) ( 62) (1,050)C. Revolving Finance Facility 3,050 4,535 7,585D. Project Implementation Unit 234 581 815

Subtotal (Base Cost) 8,380 9,451 17,831

E. Physical Contingencies 266 263 529F. Price Contingencies 247 1,665 1,912G. Interest during Project Implementation 240 - 240

Total 9,133 11,379 20,512Base costs as of 30 March 2000. Physical contingencies calculated at 5 percent of base costs, excluding revolvingfinance facility. Price contingencies calculated using estimated annual escalation of 2.4 percent for international pricesand 5 percent for local cost components. In preparation of these estimates an exchange rate of 1$ = K2.6 was assumed.Figures may not add up to total due to rounding.Source: Staff estimates.

D. Financing Plan

73. The Government has asked ADB to provide a loan of $9.6 million equivalent, or about 47percent of the total project cost, from its Special Funds resources. The loan would bear a 32-yearmaturity, including a grace period of 8 years, and 1 percent interest charge during the graceperiod and 1.5 percent thereafter.

74. AusAID will provide grant cofinancing to be administered by ADB, specifically for the pilotmicrobanking in Wau and training under the MCC. In the event that AusAID grant financing is notforthcoming, the Government will make arrangements to obtain the additional funding from othersources.

21

Table 4: Financing Plan($’000)

Source ForeignExchange

LocalCurrency

Total Cost

Amount % Amount % Amount %Government - - 4,669 41.0 4,669 22.8Bank of PNG 11 0.1 423 3.7 434 2.1Institute of Banking 78 0.9 1,147 10.1 1,225 6.0MFIsa 396 4.3 3,284 28.9 3,680 17.9AusAID 594 6.5 315 2.8 909 4.4ADBb 8,054 88.2 1,541 13.5 9,595 46.8

Total Project Cost 9,133 44.5 11,379 55.5 20,512 100.0ADB = Asian Development Bank, AusAID = Australian Agency for International Development, MFIs = microfinanceinstitutions, PNG = Papua New Guinea.a The contributions from the MFIs refer to their recurrent costs in expanding their operations and staffing levels as a result of capacity building under the Project.b Including interest during project implementation. Figures may not add up to total due to rounding.

E. The Executing Agency

75. BPNG will be the Executing Agency for the Project. It will be responsible for the overallcoordination and implementation of the Project. Although BPNG has been involved in variousexternally funded projects and has the knowledge and skills to oversee implementation, itsresource capacity is limited. To enhance the effectiveness and efficiency in project coordinationand management, the Project will support two domestic consultants to work as the projectmanager and project assistant. The project organizational structure is in Appendix 7.

F. Implementation Arrangements

1. Microfinance Steering Committee