Embed Size (px)

Citation preview

Asia Pacific Payments Trends

Global Payments Summit 2013

June 7, 2013

Singapore

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company |

Globally, payments represent close to 1 trillion EUR in revenues,

out of which 33% are generated in APACGlobal banking revenues, %, 2011

100% = EUR 3,100 billion

Retailaccounts

Corporateaccounts

Credit cardissuing

Cardacquiring

E-purse/prepaid

34

35

25

5 1

SOURCE: McKinsey Payments Map

NorthAmerica

Europe

APAC

LatAm

Other

25

25

33

15

2

100% = EUR 930 billion

70

Other bankingrevenues

Payments& accounts

30

Pre-tax profits margin 20-25% (equivalent to EUR 180-230 billion operating result)

McKinsey & Company |

Commercial CA

Latin America

200

1

5

8

15

EMEA

370

11

43

41

41

APAC

14

32

4

49

Consumer credit

card issuing

Consumer CA

Merchant acquiring

Commercial credit

card issuing

26

~04

37

33

North America

320

41

31

Percent of total revenue pool within geography, 2011, USD Billion

Regions have different sources of revenues

Co

ns

um

er

Co

mm

erc

ial

430

SOURCE: McKinsey Payments Map

McKinsey & Company |SOURCE: McKinsey Global Payments Map

898

37%

27%

18%

17%

2010

28%

37%

22%

13%

606

+8% p.a.

Asia-Pacific

North

America

Europe2

LatAm1

2015

15

14

2

CAGR,

2010-15

PercentGrowth 2010-15

USD billions

10%

7%

57%

293

26%

Asia-Pacific will account for 50% of global payments revenue

growth, excluding accounts, over the next 5 years.

1 LatAm – Argentina, Brazil, Chile, Colombia, Mexico

2 Europe – EU27 excluding Luxembourg, Cyprus, Malta, Bulgaria and the 3 Baltics plus Norway, Russia and Switzerland

Global payments revenues

excluding accounts

USD billions

5

3

McKinsey & Company |

Pay later cards account for over 50 percent of the total

revenues in Asia

Payment revenues excluding accounts, 2010

USD billions

45

27

16

12

153

42

Fees

Net interest

income

TotalOthers1

(fees)

Debit

cards

(fees)

10

Cheque

and cash

(fees)

Transfers

(fees)

Pay later

cards

87

1 Includes prepaid, digital, e-money, float

4SOURCE: McKinsey Global Payments Map

McKinsey & Company |

UK

Hong Kong

Singapore

Korea

Australia

Germany

Japan

Portugal

Spain

Brazil

Poland

Italy

Malaysia

South AfricaKSA

Turkey

Russia

Finland

Thailand

China

Kenya

Indonesia

MexicoCanada

US

France

Belgium

India

Ch

eq

ue

Ele

ctr

on

ic

Card transaction per capitaFinland 30,8Canada 45,3US 46,9France 50,2Belgium 52,9UK 53,2Hong Kong 53,7Singapore 55,5Korea 58,9Australia 61,7Germany 68,6Japan 75,0Portugal 77,2Spain 80,4Brazil 85,0Poland 88,4Italy 88,5Malaysia 92,3South Africa 92,4Saudi Arabia 93,4Turkey 93,7Russia 94,7Mexico 96,2Thailand 97,2China 97,8Kenya 98,1Indonesia 99,4India 99,6

Cash’s share of total transactionsPercent

Electronic share of non-cash transactionsPercent, transactions per capita

SOURCE: McKinsey Payments Map

Consumers display very different behavior, with Nordics historically

leading the way in digitalization for payments

Card & cheque

Full electronic

Cash & paper

Cash & electronic

McKinsey & Company |

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

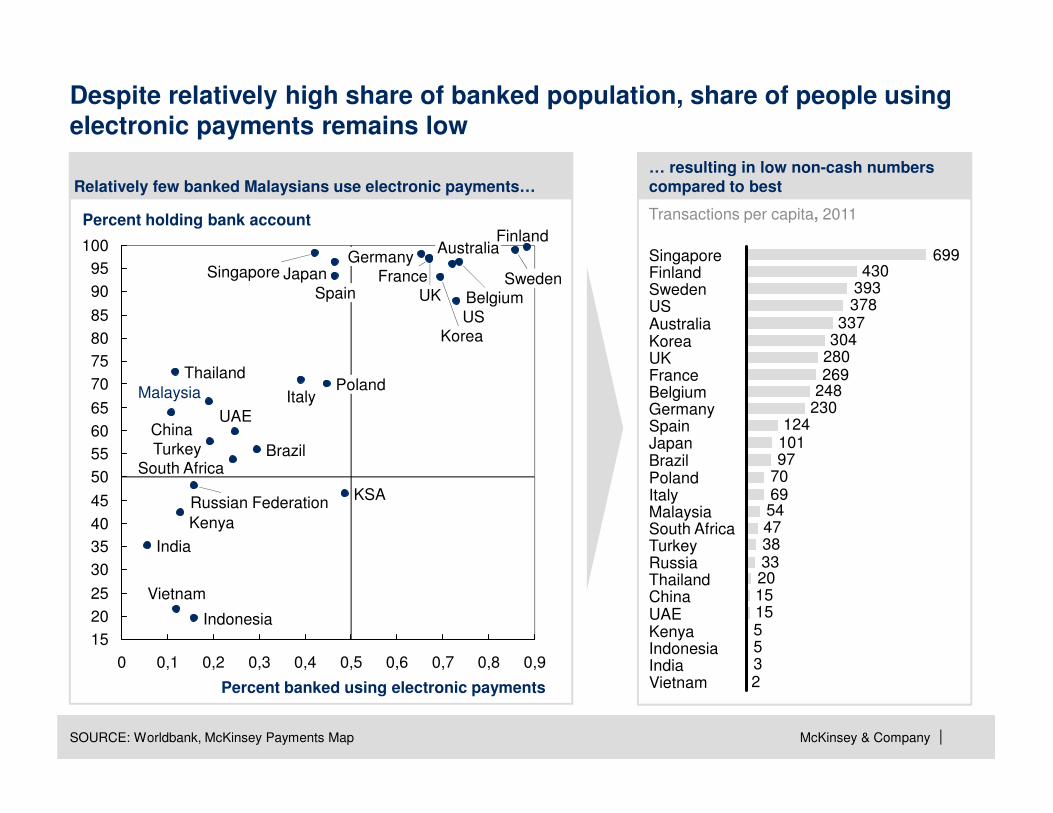

Percent holding bank account

Percent banked using electronic payments

0,90,80,70,60,50,40,30,20,10

Vietnam

India

Indonesia

Kenya

UAE

KSA

China

Thailand

Russian Federation

Turkey

South Africa

PolandMalaysia Italy

Japan

Brazil

Spain

Germany

Belgium

Korea

UK

France

Australia

Sweden

US

Finland

Singapore

Despite relatively high share of banked population, share of people using

electronic payments remains low

SOURCE: Worldbank, McKinsey Payments Map

235515152033384754697097101124

230248269280304337

378393430

699

VietnamIndiaIndonesiaKenyaUAEChinaThailandRussiaTurkeySouth AfricaMalaysiaItalyPolandBrazilJapanSpainGermanyBelgiumFranceUKKoreaAustraliaUSSwedenFinlandSingapore

Transactions per capita, 2011

Relatively few banked Malaysians use electronic payments…… resulting in low non-cash numbers compared to best

McKinsey & Company |

3

Retail payments landscape in Asia is likely to driven by 6 major trends

7

Supplier driven push to drive usage of existing form factors –

credit and debit cards 1

Shift in consumer behavior towards digital transactions and

payments2

Emergence of multiple stored value solutions to electronify low

ticket transactions

Rapid electronification of remittances (especially cross border in

select corridors)4

Enhanced stress on innovation to win5

6Changing player landscape – emergence of non-traditional players

and innovative partnerships

McKinsey & Company | 8

Supplier driven thrust along with regulatory support could accelerate

growth of credit & debit card usage

1. Push on credit and debit cards

▪ Higher credit card penetration

▪ Increased debit usage

▪ Faster terminalization

POS adoption at merchants

▪ Deployment of new technology to meet

merchant needs

▪ Enhanced solutions, reward programs and promotions

EMV Chip + PIN for better security

▪ Industry wide initiative to roll out

EMV Chip + PIN for

debit an credit cards

Enhanced card value propositions▪ Rewards for debit card

with improved features e.g., linked credit,

installment plans

▪ Higher credit card penetration leveraging all data - internal and

third party

Tax incentives to consumers and merchants▪ Tax incentives by

income deduction (e.g. Korea) or VAT refund (e.g., Argentina, Colombia)

McKinsey & Company |

73

339

250

16

166125

42

115

5

2015

162

2010

44

2008

15

Prepaid

Online

Mobile

114%

13%

49%

13%

15% 15%Developed Asia1

Developing Asia2

23% 23%

178%

288%

81%

36%

69% 30%

17% 17%

1 Australia, Japan, S.Korea, Taiwan, Hong Kong and Singapore

2 China, India, Indonesia, Malaysia and Thailand

SOURCE: McKinsey Global Payments Map; IDC New Media market model; Passport Internet retailing report; eMarketer

Asia Pacific B2C ecommerce report

CAGREmerging payment flowsUSD billions 2008-10 2010-15

2. Growth in digital payments

9

Emerging payments, particularly mobile, will experience extremely

strong growth.

McKinsey & Company | 10

Fully functioning “digital wallets” could

leapfrog payments evolution across markets

Payment processing

Travel and More

Payment forms

▪ Credit and debit cards

▪ Prepaid card accounts

▪ Gift cards (closed loop)

▪ Private label credit

▪ Loyalty schemes

▪ Rewards currencies

▪ Unsecured credit

▪ Etc.

Local value storee.g. PayPal account balance

Offers, from▪ Pre-screened sources e.g.

Alliance Data

▪ Offers engines e.g. Groupon

Paid banner advertising

SOURCE: McKinsey Payments Practice

Network Payment Card

“Clipped”

offers

Offers

poolAdvertising

‘Social’ layer

Reviews, shared experiences, etc.

Digital wallet application(accessed through browser or app)

Private Label Card

Loyalty Card

Gift Card

Online and offline purchase tools(i.e. the consumer toolkit at “buy”)

Pre-purchase inputs (i.e. acquired

during “consider” and “evaluate”)

Payments

& banking

Retail

Online

marketing

Telecom

(MNO, handset)

Legend: Industries involved

Primary direction

of data flow

2. Growth in digital payments

Secure connection:

� Internet via MNO

� Internet via Wifi

� NFC

� SMS

Secure connection:

� Internet via MNO

� Internet via Wifi

� NFC

� SMS

Data e.g., aggregated

personal, transactions,

activity

McKinsey & Company | 11

Emergence of multiple solutions in stored value could electronify low

ticket payments

Multiple uses of prepaid cards to replace cash

2010 annual load, USD billions

1

China

89

57

23

5 3

2

India

7

0

3

1

1

Gift

B2B/B2C benefits & payroll

eMoney/transportation

Fuel

Travel

CEPAS example (Singapore) –promoting common standards

▪ Contactless ePurse

Application (CEPAS) is

a nationwide

interoperable

micropayment platform

in Singapore

What is it

▪ In the past, Singapore

had three multi-

propose stored value

cards (MPSVC)

– NETS Flash Pay

card

– EZ link card

– Concession card

CEPAS standard will

allow an interoperable

platform that all

MPSVC issuers will

move to

What are the benefits

3. Stored value instruments

Due to its tax benefits,

prepaid cards for

employee payroll and

benefits has been the

most popular in China

Fuel prepaid card is the

main growth driver in

India as they are used for

expense management by

transport fleet owners

McKinsey & Company | 12

Players will innovate across four dimensions to use in

cross-boarder remittances

Customer segments

Channels

Partnerships Corridors

4. Remittances

US – Ho-Chi-Minh city corridor accounts for 56% of total remittances to Vietnam. DongA and Sacombankhave focused on this corridor to capture disproportionate share

▪ Wells Fargo reports higher PPC for remittance customers

▪ Globe focuses on offshore Filipino workers

▪ Web based remittance product branded ‘AxisRemit’ web based

▪ Transfer moneys from any local bank account to Axis Bank account in India

▪ Even non-Axis Bank customers can avail of this facility▪ Tie-ups with large local

players in key NRI markets (tie-up with Lloyds Bank in UK and Wells Fargo in USA)

▪ Partner banks / agencies initiate remittance via branches (cash) and online (CASA accounts)

▪ Money sent to ICICI Bank account in India

McKinsey & Company |

Six “markers” are essential for successful innovation in payments

Marker Value step change

Walmart: Leading development of U.S. reloadable prepaid sector by leveraging revenue generated from store traffic and increased retail sales to lower and simplify pricing on MoneyCard

M-Pesa: Thoughtfully expanded role of Safaricom agents in Kenya to become largest cash-in / cash-out network in the country

PayPal: Gain traction by being dominant payment mechanism for eBay marketplaces, then expanded into eCommerce payments and merchant acquiring from scale base of users

Cardlytics: Focused on bringing value to merchants through increased customer acquisition and targeted marketing; consumer value in cost savings and “surprise & delight” offers from new stores

Xoom: Tailored disbursement options for online remittances to preferences of receive markets to cover (i) account-to-account and (ii) cash pick-up preferences by country

AliPay: China’s online payments leader solved major issues of trust through “escrow-based” payment process where buyers were guaranteed satisfaction of goods before transaction is settled

Marker Beyond cost

Marker Established infrastructure

Marker Adapt to market context

Marker Adjacent revenues

Marker Niche markets first

1

2

3

4

5

6

5. Innovation

13

McKinsey & Company |

Several non-traditional players are emerging across Asia

� Objective: Churn reduction, increasing ARPU

� Asset: client billing relation, SIM

� Objective: increasing sales and market share

� Asset: smartphone, applications library

� Objective: increasing traffic, payment revenue

� Asset: online content, flexible software solutions

� Objective: increasing traffic, increasing subscribers

� Asset: payment infrastructure, global standards

Innovative partnerships emerging▪ Telcos and Banks specially for financial inclusion - E.g., Vodafonre and HDFC bank, Globe telecom (GX

change) partnership with Philippine savings bank, etc.

Online players

Telcos Handset manufact-urer/platform

Mobile phone

Card systems

6. Competitive landscape

14

McKinsey & Company |

Key questions FOR DISCUSSION

15

▪ What are the key barriers to consumer adoption of electronic

instruments? What changes (regulatory, consumer behavior)

could lead to an inflection point in adoption?

▪ How do you see the future of credit and debit cards across Asia? What will drive electronification

of micro-payments?

▪ Which digital models are likely to succeed

across markets? What is the biggest opportunity and challenge in making the economics of digital

payments work?

▪ Who are the players best positioned to capture

the payments opportunity in Asian markets?

What are the markers of success?

▪ Do you seen greater collaborative eco-systems emerging to deliver end-to-end value to customers?