Embed Size (px)

Citation preview

ASIA OFFSHORE ENERGY CONFERENCE30TH SEPT – 2ND OCT 2015

BALI, INDONESIA

The Role and Management of PETRONAS’ Captive Insurance Company

Page 2

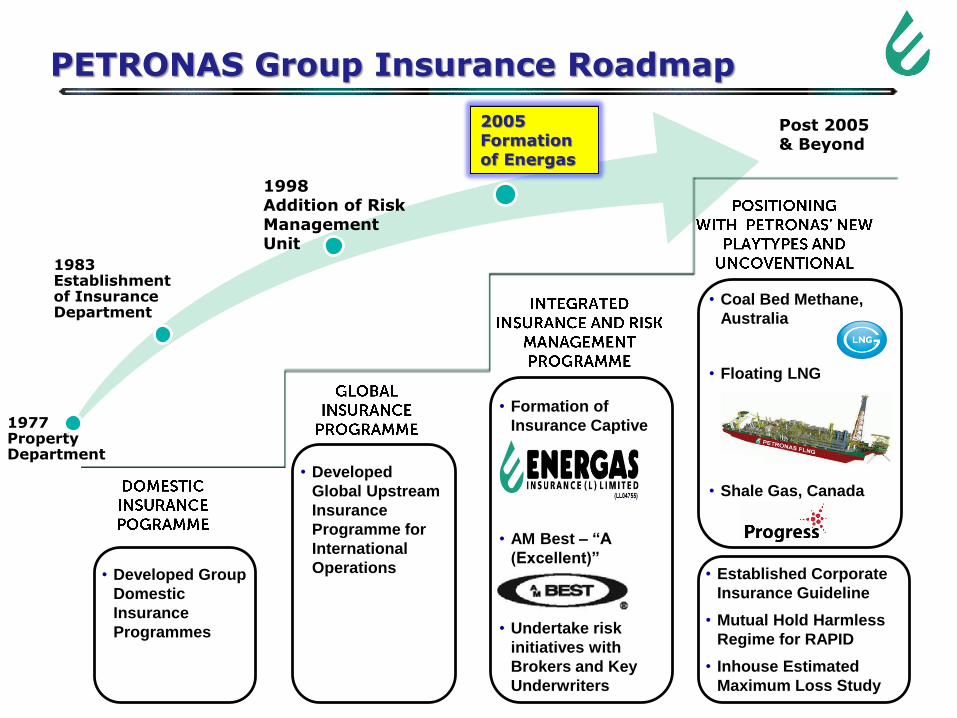

PETRONAS GROUP INSURANCE ROADMAP

BRIEF PROFILE OF ENERGAS

FUNDAMENTALS OF CAPTIVE FORMATION

ORGANIZATION STRUCTURE / CORPORATE

GOVERNANCE

RISK CONTROL FRAMEWORK

UNDERWRITING AND REINSURANCE

CONCLUSION

TABLE OF CONTENTS

• Coal Bed Methane,

Australia

• Floating LNG

• Shale Gas, Canada

PETRONAS Group Insurance Roadmap

• Formation of

Insurance Captive

• AM Best – “A

(Excellent)”

• Undertake risk

initiatives with

Brokers and Key

Underwriters

• Developed Group

Domestic

Insurance

Programmes

• Developed

Global Upstream

Insurance

Programme for

International

Operations

1977Property Department

1983Establishment of Insurance Department

1998Addition of Risk Management Unit

2005Formation of Energas

• Established Corporate

Insurance Guideline

• Mutual Hold Harmless

Regime for RAPID

• Inhouse Estimated

Maximum Loss Study

Post 2005 & Beyond

Page 4

BRIEF PROFILE OF ENERGAS

A wholly owned subsidiary of PETROLIAM NASIONAL

BERHAD (PETRONAS)

Incorporation Date : 24th March 2005

Commenced Operation : 1st April 2005

Commenced Underwriting : 1st April 2006

Authorised Paid-Up Capital : USD 10.5 million

Page 5

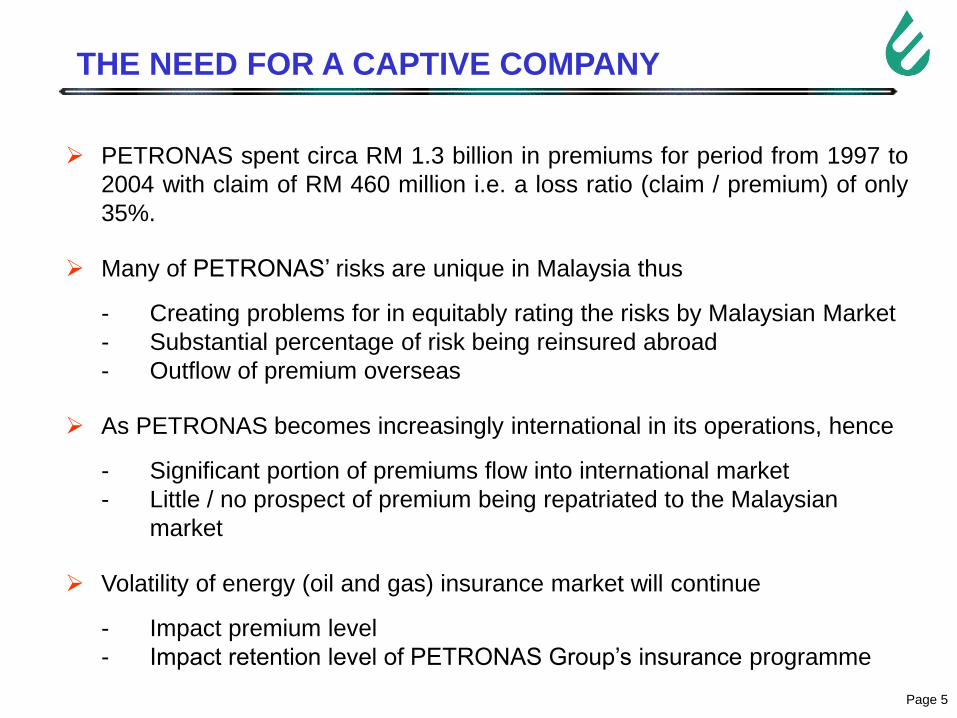

THE NEED FOR A CAPTIVE COMPANY

PETRONAS spent circa RM 1.3 billion in premiums for period from 1997 to

2004 with claim of RM 460 million i.e. a loss ratio (claim / premium) of only

35%.

Many of PETRONAS’ risks are unique in Malaysia thus

- Creating problems for in equitably rating the risks by Malaysian Market

- Substantial percentage of risk being reinsured abroad

- Outflow of premium overseas

As PETRONAS becomes increasingly international in its operations, hence

- Significant portion of premiums flow into international market

- Little / no prospect of premium being repatriated to the Malaysian

market

Volatility of energy (oil and gas) insurance market will continue

- Impact premium level

- Impact retention level of PETRONAS Group’s insurance programme

Page 6

FUNDAMENTAL PURPOSE OF CAPTIVE FORMATION

The fundamental purpose of the captive formation is as follows :

To limit or reduce the overall cost of risk to PETRONAS by

maintaining control over its corporate risk financing programmes

To reduce reliance on conventional insurance market and control

external premium spend to international insurance markets

To build up reserves for the hard market cycle within an internal

vehicle allowing for greater risk retention

Greater control of risk management and insurance processes

Large cost savings in terms of insurance costs to the Group

Page 7

OTHER SUPPLEMENTARY ROLE / BENEFITS

It provides a mechanism for selective retention of risks where it is

financially advisable to do so

It allows alternative or direct access to the international

reinsurance market with the possibility of financial saving

Development of funds allows for the consideration of other risk

transfer mechanisms

Its own retention would reduce foreign exchange outflow

It enables the parent to buy more competitively as overseas

reinsurers recognize the alternative to their direct market

Making available to the local insurance market some of the oil

and gas expertise of PETRONAS to assist the Malaysian market

in the underwriting of energy related risks

Page 8

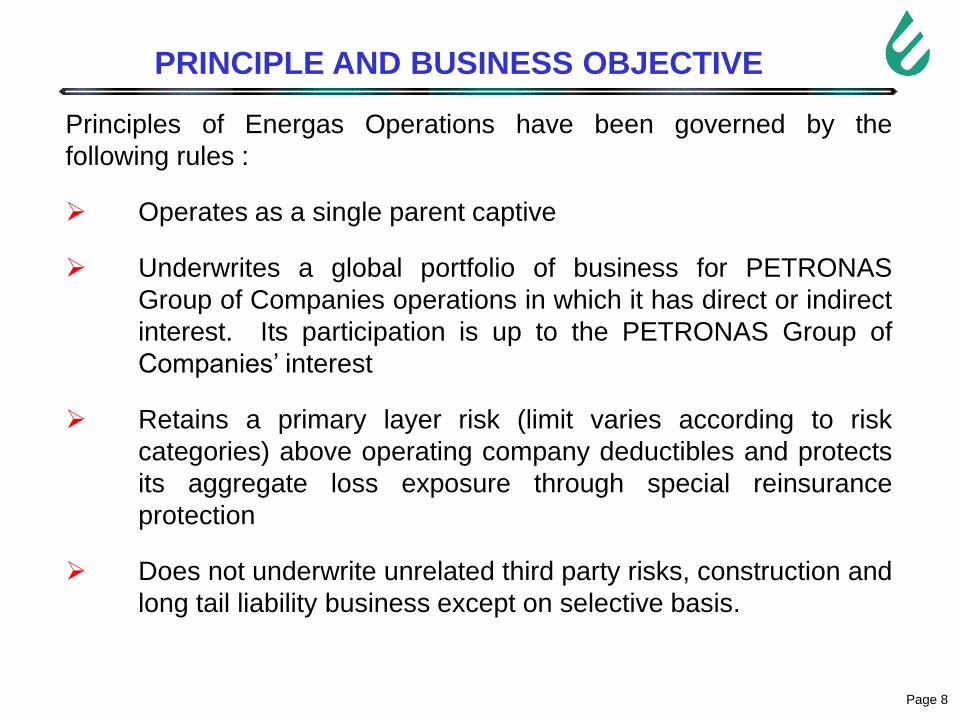

PRINCIPLE AND BUSINESS OBJECTIVE

Principles of Energas Operations have been governed by the

following rules :

Operates as a single parent captive

Underwrites a global portfolio of business for PETRONAS

Group of Companies operations in which it has direct or indirect

interest. Its participation is up to the PETRONAS Group of

Companies’ interest

Retains a primary layer risk (limit varies according to risk

categories) above operating company deductibles and protects

its aggregate loss exposure through special reinsurance

protection

Does not underwrite unrelated third party risks, construction and

long tail liability business except on selective basis.

Page 9

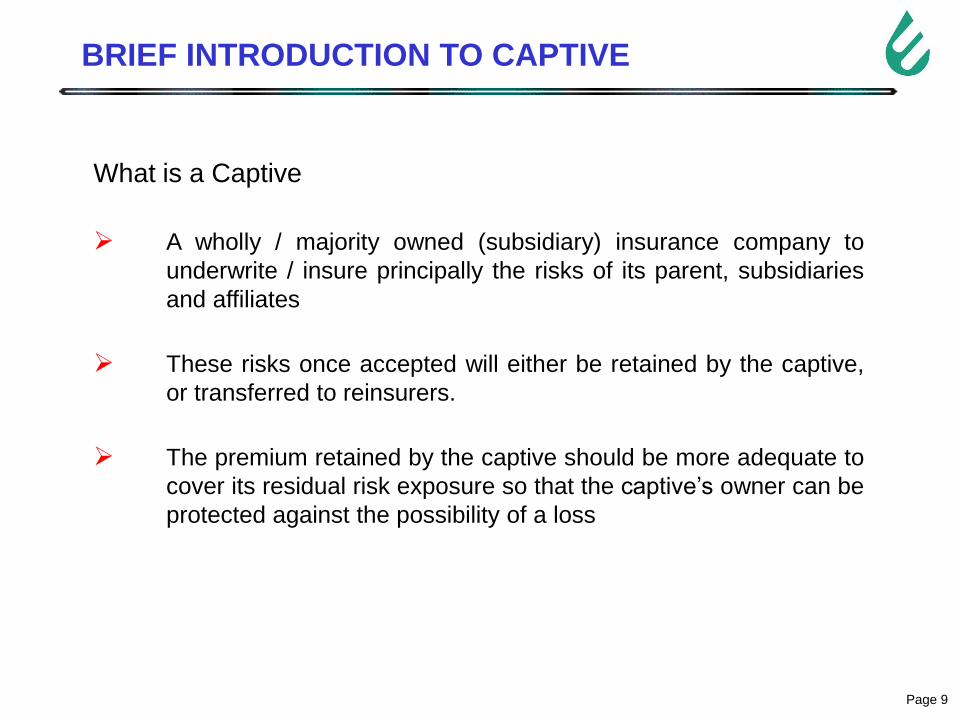

BRIEF INTRODUCTION TO CAPTIVE

What is a Captive

A wholly / majority owned (subsidiary) insurance company to

underwrite / insure principally the risks of its parent, subsidiaries

and affiliates

These risks once accepted will either be retained by the captive,

or transferred to reinsurers.

The premium retained by the captive should be more adequate to

cover its residual risk exposure so that the captive’s owner can be

protected against the possibility of a loss

ORGANIZATION STRUCTURE /

CORPORATE GOVERNANCE

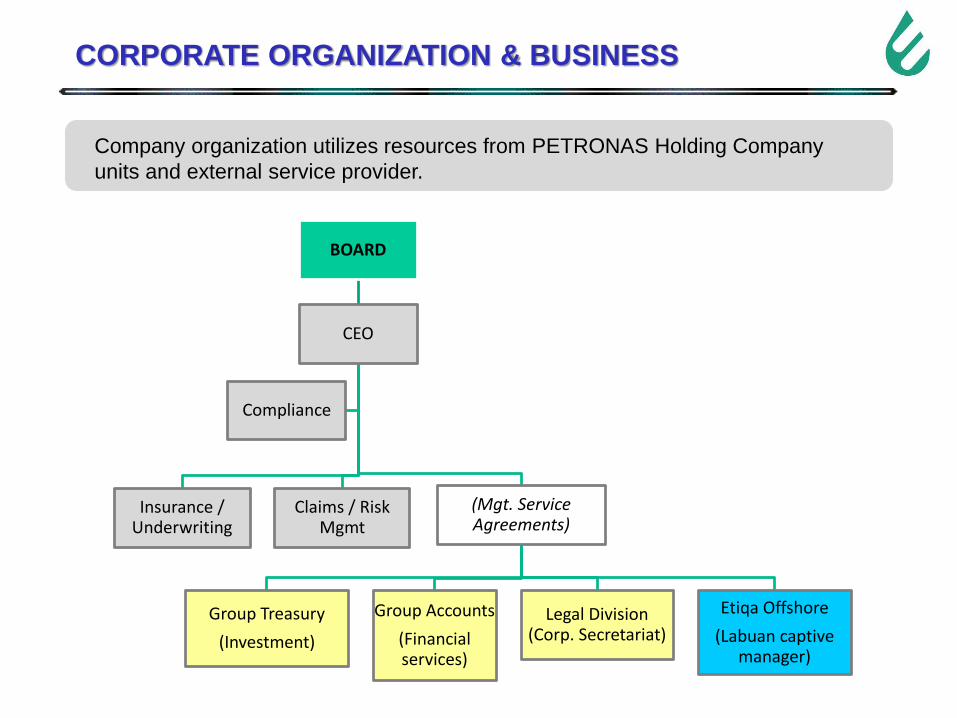

CORPORATE ORGANIZATION & BUSINESS

BOARD

CEO

Insurance / Underwriting

Claims / Risk Mgmt

(Mgt. Service Agreements)

Group Treasury

(Investment)

Group Accounts

(Financial services)

Legal Division(Corp. Secretariat)

Etiqa Offshore

(Labuan captive manager)

Compliance

Company organization utilizes resources from PETRONAS Holding Company

units and external service provider.

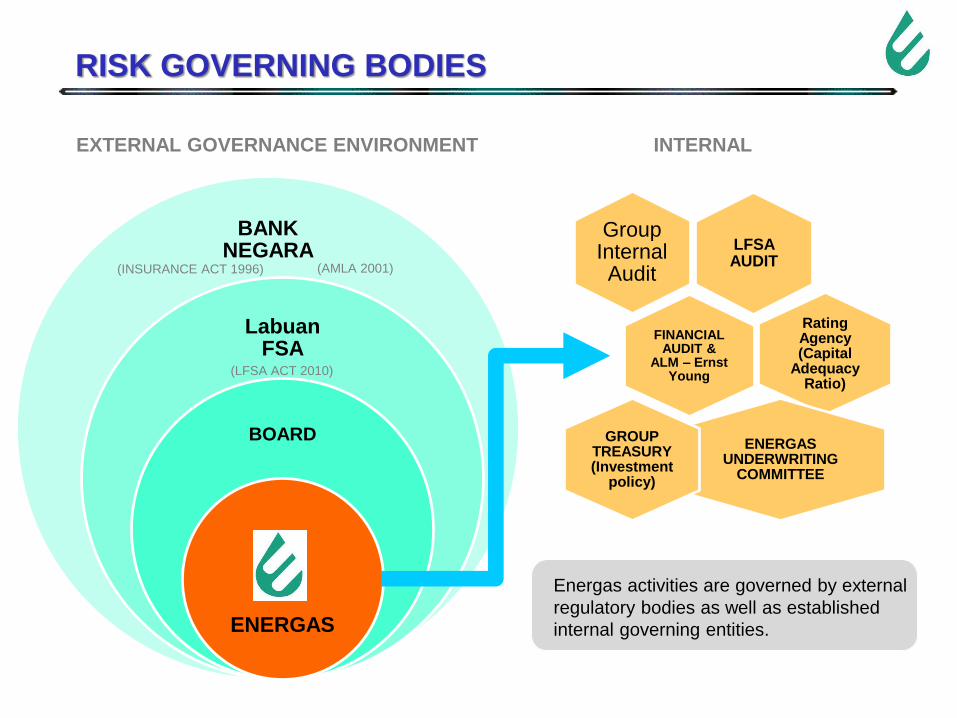

RISK GOVERNING BODIES

BANK NEGARA

Labuan FSA

BOARD

ENERGAS

LFSA AUDIT

Group Internal Audit

FINANCIAL AUDIT &

ALM – Ernst Young

Rating Agency (Capital

Adequacy Ratio)

ENERGAS UNDERWRITING

COMMITTEE

GROUP TREASURY (Investment

policy)

Energas activities are governed by external

regulatory bodies as well as established

internal governing entities.

INTERNALEXTERNAL GOVERNANCE ENVIRONMENT

(INSURANCE ACT 1996) (AMLA 2001)

(LFSA ACT 2010)

Page 13

ENERGAS

BOARD

PETRONASENERGAS

SHAREHOLDERREGULATOR

GROUP

INTERNAL

AUDIT

LABUAN FSA

ENERGAS

CHIEF

EXECUTIVE

OFFICER

INTERNAL AUDIT

MANAGEMENT

COMMITTEE

BOARD AUDIT

COMMITTEE

Audit Report

Business Control

•Compliance

•Operations

•Reporting Audit

Exercise

INTERNAL CONTROL OBJECTIVE• Compliance with applicable

law and requlations• Effectiveness and efficiency

of operations• Reliability of financial

reporting

MONITORING INTERNAL CONTROL SYSTEM

14

BOARD

PETRONASENERGAS

SHAREHOLDERREGULATOR

LABUAN FSA

CHIEF

EXECUTIVE

OFFICER

Business Control

Division of responsibilities

between Chairman and

CEO of Energas

Compliance Operations (Effective and Efficient)

Reporting (Reliability)

• Compliance Officer

• Compliance Checklist

• Audit report and status

• Compliance update every Board sitting

• Audit update quarterly (Chairman) and every Board sitting

• Biannually update on underwriting and operational performance

• Limit of Authority & Summary of Authority

• Underwriting Guidelines,

• Corporate Financial Policy

• Work procedure manual

• Agreement

• Annual Report (Audited)

• Consolidation between Captive Manager and Energas

• Energas Checklist

• Annual Audited Report

• Monthly Management Report (MMR)

• Quarterly Management Report (QMR)

• Relevant Acts

• Policy, Framework and Guideline

• Statutory Reporting

Internal Control Objectives

INTERNAL CONTROL SYSTEM

RISK CONTROL FRAMEWORK

POLICY

GUIDELINES

REPORTING

METHODOLOGY

PROCEDURES

RISK OVERSIGHT STRUCTURE

• Business policies as set by the Board

• No underwriting of risk by Energas which could prejudice the financial

security of PETRONAS

• Underwriting Guideline document as approved by the Board

• LOA and SOA Manual document

• Guidelines for appointing business counterparties

• Quarterly Progress reports to Board

• Monthly financial / claims reporting to LFSA

• Quarterly update report to GIAD

• External / Internal / LFSA audits

• Annual financial stress test on underwriting structure

• Capital Adequacy Ratio analysis by international rating agency

• Asset Liability Management / IBNR studies by third party actuarist

• Developed Work Procedure Manual document for each line function

• Competent and trained manpower

LIQUIDITY

RISK

INVESTMENT

RISK

AGGREGATION

RISK

MARKET /

PRICING

RISK

ENERGAS RISKS

REINSURERS CREDIT

CLAIMS LOSS RECORD

FOREIGN EXCHANGE

GEOPOLITICAL &

REGULATORY

INTERNAL CONTROL FAILURE

INSURANCE CONTRACT

DISPUTE

REINSURANCE COST

ENERGAS RISK PROFILES

Energas monitors a set of specific

risks on a regular basis.

This enables Energas to assess

the overall risk exposure and to

determine which risks and what

level of risk Energas is prepared to

accept and the adequacy of

existing mitigation plans.

ENERGAS RISK PROFILES - Continued

Definition of risks relevant to Energas operations

• A counterparty risk when reinsurers become insolventReinsurers Credit Risk

• Increasing trend of claims impacting net profitHigh Loss record

• Fluctuation in USD vs. RM exchange rates and conversion lossesForeign Exchange

• Significant increase in reinsurances premium expensesReinsurance Cost

• Non compliance to law and regulation in location where Energas operates (Labuan) and underwritesLegislative and Regulatory Risk

• Non compliance to policy, procedures and guidelinesFailure of Internal Business Control

• Lead Reinsurer disputing policy coverage on claim's liability Energas Reinsurers' Dispute Risk

• Accumulation of the underwritten risks under multiple policies at a single location or event

Aggregation of the Insured Risk

• Invested funds bring negative returnsInvestment Risk

• Adequate cash are not available to meet fund / claim obligations at a given time

Liquidity Risk

• Inability to reinsure underwritten risks to appropriate overseas market Market Risk

UNDERWRITING AND

REINSURANCE

Page 20

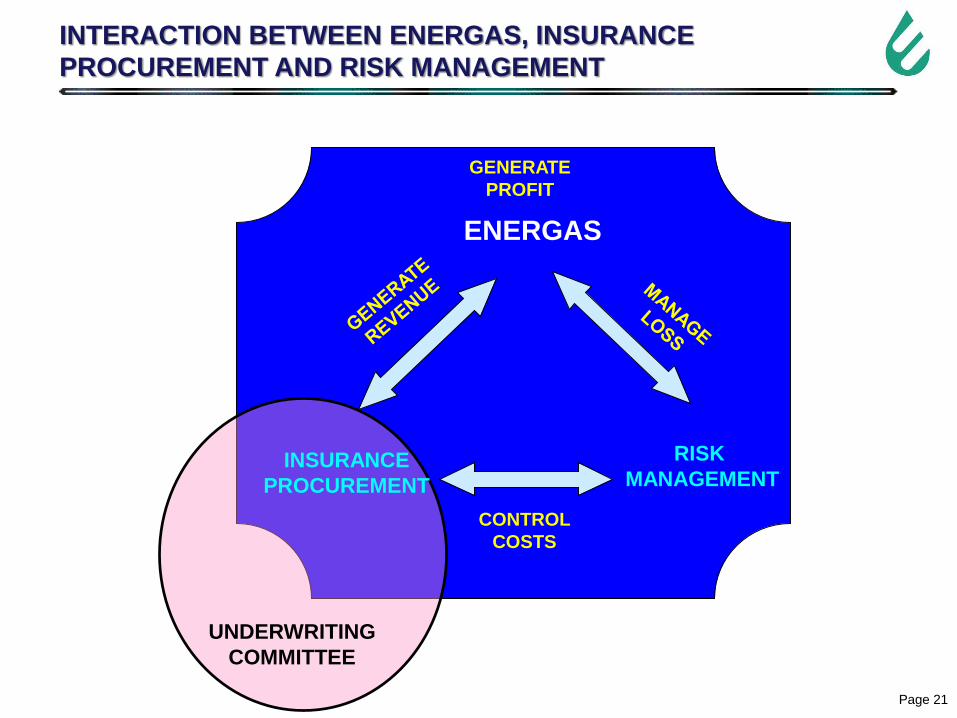

ENERGAS PARTICIPATION PROGRAMME & STRUCTURE

SPECIAL CONSIDERATION IN DETERMINING PROGRAMME STRUCTURE :

Critical to the success of PETRONAS captive is its choice of underwriting

portfolio and reinsurance programme. Captive should therefore elect to

participate in those risks where it can command the optimal balance of

premium income and risk exposure

Programme structure would also take cognizance of the following

requirements :

- Any captive programme must not reduce the role played by the

domestic Malaysian insurance market

- There should be no assumption of risk by the captive which could

prejudice the financial security of PETRONAS

Page 21

ENERGAS

RISK

MANAGEMENT

GENERATE

PROFIT

CONTROL

COSTS

UNDERWRITING

COMMITTEE

INSURANCE

PROCUREMENT

INTERACTION BETWEEN ENERGAS, INSURANCE

PROCUREMENT AND RISK MANAGEMENT

Page 22

CYCLE MANAGEMENT STRATEGY

As a Captive insurance company which does not accept third party

risks Energas’ customer base is defined by its Parent.

Asset values and cost of insurance move in tandem with Group’s

activities and market cycles.

Cycle management is therefore practiced through variation in

reinsurance arrangements particularly favouring Quota Share

reinsurance at times Energas view original rates as being

insufficient for the risks Energas face and then favouring other

structures such as Excess of Loss reinsurance when premium

levels appear to be sufficient to carry the risks Energas face.

Existing risk governance and control within Energas is well

established and appears to be adequate to ensure the risk

exposures are properly mitigated according to our risk

appetite.

Continuous governance and high level risk oversight are

being assured to Energas operations by various external

and internal entities such as Labuan FSA, Group Internal

Audit, financial rating agency, to name a few.

CONCLUSION

THANK YOU