Embed Size (px)

Citation preview

European Power & Renewables DealsQuarterly M&A outlook

As we forecasted in the last edition of our quarterly deal series, deals for gastransportation assets in Europe are proving a major source of M&A flow. Aswe move into the fourth quarter of the year and look ahead to 2013, we see thepotential for an unprecedented flow of deals for onshore wind generationassets. Late summer and autumn 2012 has seen a rush of announcements ofasset sale intentions. A potential total sales value of US$4-5bn from onshorewindpower assets alone is now on the deal table.

www.pwc.com/powerdeals

Autumn 2012

example, the sales of Immingham byConocoPhillips and Sutton Bridge byEDF have been running for some timebut are still to get over the line.

Looking ahead, a summer of dealpreparation looks set to turn into a dealupturn in the fourth quarter and the newyear. The outlook appears strong with anumber of themes at work that willunderpin deal activity. Following theacquisition of 100% of InternationalPower, GDF Suez has set up anadditional divestment programme of 3billion euros. A number of othercompanies have been sizing updivestment options.

The big global utility companies remainfocused on shifts in their globalinternational footprint and balance sheetrestructuring. At the same time there is amajor shift within Europe as companiesmanage the contrasting nuclear outlooksin Germany and the UK. The Horizonsale will have an impact on the UK dealagenda in the coming period and, rightacross Europe, renewable energy dealflow is also likely to be strong (see dealfocus section).

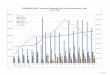

Buyers and sellers were more focused on preparing rather thanexecuting larger deals as a summer lull dampened European power andrenewables big deal flow. After a Q2 upturn fuelled by three multi-billion dollar deals, total European deal value fell sharply in Q3. A fallin value was also evident globally. But the value downturn was notuniformly reflected in deal volume. While deal numbers fell by 25% forpower and renewables targets outside Europe, deal volume insideEurope increased by 28%.

By number

Q4 2011

Q3 2011

Q2 2011

Q2 2012

Europe Global

95

115

109

92

68

294

350

268

265

227

Q1 2011

Figure 1: Quarterly power and renewable energy deal trends – Europe (by target) and global

By value (US$bn)

Q4Q3Q2 Q12011

10

20

30

40

50

60

70

Europe Global

Electricity Gas Renewables

18.3

11.58.1

14.4

5.7

62.5

54.7

16.7

66.6

27.3

Source: European Power & Renewables Deals, Autumn 2012

Q1 Q2 Q3 Q4Q12012 2011

Q12012

Q4 2011

Q3 2011

Q2 2011

Q2 2012

Q1 2011

Q1 2012 89 255Q1 2012

23

50.3

Q2 Q2

6

Q3 Q3

24.7

Q3 2012 87 207Q3 2012

Deal flow: a pause for preparation

The deal volume upturn wasattributable to a surge in gas deals. Gasdeal numbers were at a two year high,trebling from the volume in theprevious quarter which, in turn, wasalready up on most earlier recentperiods. The largest deal was theUS$3bn sale of Wales & West Utilities inthe UK, accounting for much of theUS$4.3bn Q3 gas transaction value. Welook at this and other leading gas dealsin the ‘dealmakers’ section. Lookingahead, the outlook for gas deals will bepartly shaped by regulatory changesthat lie ahead next year in a number ofmajor European territories. A greaterfocus on incentive arrangements toimprove quality of supply has thepotential to reward owners who candraw on strong operating experience todrive out performance.

In a quiet period for big dealmaking, it’sthe deals that are not getting done asmuch as the ones that are goingthrough which provide the interest. Inparticular, sales of thermal generationportfolios are proving especiallydifficult to get off the ground as buyersand sellers weigh up the uncertaineconomics of gas-fired power stationsin a changing market. In the UK, for

2 European Power & Renewables Deals: Quarterly M&A outlook

No. Value of Date Target name Target nation Acquirer name Acquirer nationtransaction announced(US$m)

Figure 2: Top five deals for European power targets

3,036.2

749.6

296

281.6

203.2

25 July 12

17 July 12

20 July 12

10 Aug 12

30 July 12

Wales & West Utilities Ltd

SNAM SpA (5%)

Naturgas Energia Transporte SAU

Polish Energy Partners SA

A2A Coriance SAS

United Kingdom

Italy

Spain

Poland

France

Cheung Kong (Holdings) Ltd;Cheung Kong Infrastructure Holdings Ltd;Power Assets Holdings Ltd;Li Ka Shing Foundation Ltd

Market purchase

Enagas SA; Ente Vasco de la Energia

Kulczyk Investment SA

KKR & Co LP

Hong Kong

Italy

Spain

Luxembourg

France

1

2

3

4

5

Source: European Power & Renewables Deals, Autumn 2012

Deal makers: gas and grids take the spotlight

No. Value of Date Target name Target nation Acquirer name Acquirer nationtransaction announced(US$m)

Figure 3: Top five deals for European renewable energy targets

227.4

193.3

39.3

31.3

11.9

18 July 12

14 Aug 12

18 July 12

28 Aug 12

18 July 12

Aerowatt SA

PNE Wind AG (Offshore wind park projects Gode Wind I, II and III )

Aion Renewables photovoltaic power plants

AEG Power Solutions (six solar plants)

Muehlhausen solar power stations

France

Germany

Italy

Italy

Germany

JMB Energie

DONG Energy A/S

Avelar Energy Ltd

Clear Financial

Greenfoot Solar BV

France

Denmark

Switzerland

Ireland

Netherlands

1

2

3

4

5

Austria – Verbund rumoured to be considering sales of its transmission systemoperator APG and a minority stake in Steweag Steg.

France – Total assessing options for the sale of its south-west France gastransport and storage assets, TIGF.

Ireland – Bord Gais Eireann retail energy privatisation.

Germany – Energie Baden-Württemberg (EnBW) reportedly seeking advisersfor the sale of its electricity and gas transmission networks.

Greece – privatisation of Greece’s gas company DEPA and natural gas gridoperator DESFA.

Italy – ENI’s continuing sale of its stake in gas distribution network operator,Snam.

Netherlands – The Dutch Government has proposed the part privatisation ofTenneT and Gasunie. But, following recent elections, it remains uncertainwhether and when this will happen.

Pan-Europe – GDF Suez is expected to divest around 3bn euros of assets indifferent European countries.

Poland – both Iberdrola and DONG Energy rumoured to be selling their Polishwindpower businesses.

Spain – sale of Eolia, one of the leading independent European renewablepower producers, and further divestments of ACS renewable assets (wind andconcentrating solar power). Iberdrola has decided to sell its wind energyoperations in France, Poland and potentialy wind assets in Germany.

UK – It’s widely reported that Iberdrola will be selling a stake in Scottish Power,the electrical transmission and distribution network operator. Proposed sale ofHorizon nuclear joint venture by E.ON and RWE. The UK and Dutchgovernments, RWE and E.ON, the shareholders in uranium enrichmentcompany, Urenco, are considering their options for a possible exit.

In the pipeline – highlights

Three deals for gas network and pipelineassets head the list of Q3 deals and togetheraccount for US$4.1bn of the US$6bn totalEuropean power and renewables deal valuein the quarter. Top of the list is the US$3bnpurchase of gas transportation,distribution and meter services companyWales and West Utilities by Hong Kong’sCheung Kong Holdings which already ownsanother of the eight UK gas distributionnetworks, Northern Gas Networks. Theseller was a consortium of investors led bythe Macquarie European InfrastructureFund. In part, the sale’s timing arises fromthe fund’s maturity horizon.

Negotiations on the Wales and West deal wereconducted bilaterally. Bilateral arrangements,where investors are keen on a particular assetor asset class and approach sellers or assetowners directly rather than wait for an auctionprocess to get underway, are becoming morecommon in the power and utilities sector. Thisis the case particularly where there are alreadygood price reference points in the market fromprevious deals for similar assets. Thedivestment by ENI of a further 5% of Italiangas transmission operator Snam is the latestinstalment of its eventual full divestmentwhich arises from a government decree.

The third in the trio of Q3 big gas deals sawSpanish gas grid operator Enagas buy 90% ofNaturgas Energia Transporte from Portuguesepower utility company EDP. The grid part of thesector is proving a lively deal space. Elsewhere inEurope, the German market is seeing a lot ofmunicipal deals as the large utility companiesseek to dispose shares in regional distributionnetwork companies to local municipalities, inpart to retain the concessions within thesecompanies. Iberdrola is reported to be planning apartial sale of a minority stake in its UKelectricity grid, owned by its Scottish Powersubsidiary1.

In a notable deal announced just after the quarterend, Danish pension fund PensionDanmarkacquired a 50% stake in three US wind farms fromE.ON. The deal further highlights the interest ofinsurance and pension funds in the windpowersector (see next section). E.ON will remainresponsible for the day-to-day operation of thewind farms. Ninety per cent of the powergenerated will be sold under fixed-price powerpurchase agreements. Describing the investment,PensionDanmark observed that the assets providean attractive return at a level very similar to whatyou can expect from equities, but with significantless risk and exposure to the business cycle.2

3 European Power & Renewables Deals: Quarterly M&A outlook

1 Reuters, 27 September 2012.2 E.ON press release, 8 October 2012.

Deal focus: a rush of sales set to boost onshore wind deals

4 European Power & Renewables Deals: Quarterly M&A outlook

The coming months could see an unprecedented flow of deals for onshore windgeneration assets in Europe. Late summer and autumn 2012 has seen a rush ofannouncements of asset sale intentions. The result is US$4-5bn lying on the deal table inOctober 2012. We are aware of eleven hoped-for sales (see figure 4) with around 3GWtotal generation capability. Most of this is already in operation with the rest underdevelopment or ready for construction.

Not all of these sales will necessarily reachcompletion. But even if some fail, it willstill represent a major step up in onshorewind deal flow. In the third quarter of2012, the total value of deals for all formsof renewable power generation assets inEurope was just US$US0.5bn, down fromUS$1.1bn and US$1.7bn in the first andsecond quarters. The US$4-5bn of newdeal intentions for onshore wind thus hasthe potential to far exceed recent totalrenewables deal value.

An enlarged deal flow for onshore windassets could become a feature of powersector dealmaking. Unlike many otherpower assets, sellers are more able toparcel up wind generation projects tomake a sale easier. A large power station,network or customer base is generally notdivisible and a full stake divestment is anall or nothing move. But onshore windassets can be drip fed onto the market inportfolio sizes more closely tied tofinancial requirements.

Seller motivation for these deals stemsfrom the need to free up capital for futureinvestment and a reappraisal of portfoliosor specific territories. In France, a secondround of tender for offshore windfarms,totalling 1305MW, is expected before theend of 2012. Elsewhere, both DONGEnergy and Iberdrola are seeking buyersfor wind farms in Poland. These movescome at a time when proposed Polishenergy reforms appears to favour solarpower and offshore wind over onshorewind and biomass.

The proposed sales mainly involveoperational assets. Once operational, windfarm returns are relatively steady andreasonably predictable but potential value-add, for example in the form of synergiesor greater efficiency, is minimal. Buyerappetite among infrastructure funds,pension funds, insurance companies andsovereign wealth funds, as well as theattractiveness of particular territoriallocations, will be factors in decidingwhether this sudden flow of potentialdeals becomes a more permanent part ofthe power and renewables deal landscape.

Institutional investors have the advantageof a lower cost of capital and other buyersare likely to find it hard to compete. In arecent completed deal, insurance companyMunich Re, represented by its assetmanagement arm MEAG, bought HGCapital’s operating UK onshore windportfolio, comprising three operating windfarms with a combined capacity of102MW. The move brings Munich Re astep closer to its target of up to 2.5bn eurosinvestment in renewable energies.

Munich Re is far from alone in itsacquisition of wind farms. Fellow Germaninsurer Allianz’s investment strategy hasincluded renewables since 2005 but itspurchases have accelerated recently.

Vendor Location Capacity

Figure 4: Selection of onshore wind assets for sale – October 2012

Alpiq

DONG Energy

Edison

Element Power

Eolfi Asset Management

Iberdrola

Iberdrola

Platina

SSE

Italy

Poland

Italy

Poland

France

Poland

France

UK

Portugal

60 wind farms

111.5MW operational, 40MW ready for constructionand 690MW under development

462MW

700MW under development

70MW

185MW

Onshore wind

69MW operational

900MW under development

Source: European Power & Renewables Deals, Autumn 2012

In March 2012 it added two completedwind parks in France to its portfolio. Thesedeals and others in the preceding 12month period boosted the value of theinsurer’s renewables investment portfolioby 25%. It has indicated that it may makeindividual investments of up to 1bn eurosin offshore wind parks. As at March 2012,Allianz had a total of over 1.3bn eurosinvested in renewable energies, including34 wind farms with a total capacity of658MW.

ContactsGlobal contacts

Norbert SchwietersGlobal Power & Utilities Leader Telephone: +49 211 981 2153 Email: [email protected]

Andrew McCrossonTelephone: +44 20 7213 5334 Email: [email protected]

Paul NillesenTelephone: +31 88 792 7237 Email: [email protected]

Territory contacts

AustriaMichael SponringTelephone: +43 1 501 88 2935 Email: [email protected]

Central and Eastern EuropeDirk Buchta Telephone: +420 251 151 807 Email: [email protected]

DenmarkPer TimmermannTelephone: +45 3945 3945Email: [email protected]

Søren Skov LarsenTelephone: +45 3945 9151 Email: soren.skov.larsendk.pwc.com

FinlandMauri HätönenTelephone: +358 9 2280 1946 Email: [email protected]

FrancePhilippe GiraultTelephone: +33 1 5657 8897Email: [email protected]

GermanyNorbert Schwieters Telephone: +49 211 981 2153 Email: [email protected]

Jan-Philipp SauthoffTelephone: +49 211 981 2135Email: [email protected]

GreeceSocrates Leptos-BourgiTelephone: +30 210 687 4693Email: [email protected]

IrelandAnn O’ConnellTelephone: +353 1 792 8512Email: [email protected]

IsraelEitan GlazerTelephone: +972 3 795 4 664Email: [email protected]

ItalyGiovanni PoggioTelephone: +39 06 570252588Email: [email protected]

NetherlandsJeroen van HoofTelephone: +31 88 792 1328Email: [email protected]

NorwayStåle Johansen Telephone: +47 9526 0476Email: [email protected]

PolandPiotr Luba Telephone: +48 22 523 4679 Email: [email protected]

Portugal Joao Ramos Telephone: +351 213 599 405 Email: [email protected]

Russia Tatiana Sirotinskaya Telephone: +7 495 967 6318 Email: [email protected]

SpainCarlos Fernández Landa Telephone: +34 91 568 4839 Email: [email protected]

SwedenMartin GaveliusTelephone: +46 8 5553 3529Email: [email protected]

SwitzerlandMarc Schmidli Telephone: +41 58 792 1564 Email: [email protected]

TurkeyFaruk Sabuncu Telephone: +90 212 326 6082 Email: [email protected]

United KingdomSteve JenningsTelephone: +44 20 7802 1449Email: [email protected]

Jason Morris Telephone: +44 131 524 2265 Email: [email protected]

Darren Bloomfield Telephone: +44 20 7213 3402 Email: [email protected]

MethodologyEuropean Power & Renewables Deals includes analysis of all globalpower utilities, renewable energy and clean technology dealactivity. This version focuses on the European market. We includedeals involving power generation, transmission and distribution;natural gas transmission, distribution and storage; energy retail;and nuclear power assets. Deals involving operations upstream ofthese activities, including upstream gas exploration andproduction, are also excluded. Renewable energy deals are definedas those relating to the following sectors: biofuels, biomass,geothermal, hydro, marine, solar and wind. Renewable energydeals relate to the acquisition of (i) operating and construction-stage projects involved in the production of renewable energy and(ii) companies manufacturing equipment for the renewables sector.We define clean technology deals as those relating to theacquisition of companies developing energy efficient products forrenewable energy infrastructure.

The analysis is based on published transactions from the Dealogic ‘M&A Global database’ for all electricity, gas utility and renewables deals. It encompasses announced deals, including those pending financial and legal closure, and those which are completed.Deal values are the consideration value announced or reported including any assumption of debt and liabilities. Comparative data for prior years and quarters may differ to that appearing inprevious editions of our analysis or other current year dealspublications. This can arise in the case of updated information ormethodological refinements and consequent restatement of theinput database.

© October 2012 PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as thecontext requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients.PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for theacts or omissions of any other member firm nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.