Embed Size (px)

Citation preview

ARM 56 Exam Review(CAD009)

Michael Elliott, CPCU, AIAF, The Institutes

Learning Objectives

At the end of this session, you will:

• Dissect the most challenging ARM 56 course topics.

• Practice ARM 56 exam questions.

• Familiarize yourself with the ARM 56 exam format.

What to Expect on the Exam

• Educational Objectives

• Balanced Exam

• Pretest Items

• Get the easy ones

• Don’t get bogged down early

• Use the “mark for later review” feature

• Eliminate the obviously wrong answers

• Use your scratch paper to keep track

Test-Taking Tips

Assignment 1 – Introduction to Risk Financing

Risk Financing Goals

• Pay for negative consequences of an event

• Maintain liquidity

• Manage uncertainty

• Comply with legal and regulatory requirements

• Minimize the cost of risk

Cost of Risk

• Retained losses

• Risk transfer costs

• Loss control expenses

• Risk management administrative costs

The Prouty Approach suggests that losses with low

severity and low frequency should be

A. Transferred

B. Avoided

C. Retained

D. Prevented

Assignment 2 – Estimating Hazard Risk

Estimating Hazard Losses

15

Collect and organize past

data

Limit individual

losses

Apply loss development

and trend factors

Forecast losses

1 2 3 4

One step in forecasting expected losses based on historical

data is to limit individual losses. Which one of the following

occurs as a result of limiting individual losses?

A There is a reduction in the size of the sample that can

be used for forecasting.

B The variability of forecast losses increases.

C The forecaster is better able to match losses to the

layer that is being forecast.

D The organization will be able to reduce or eliminate

losses.

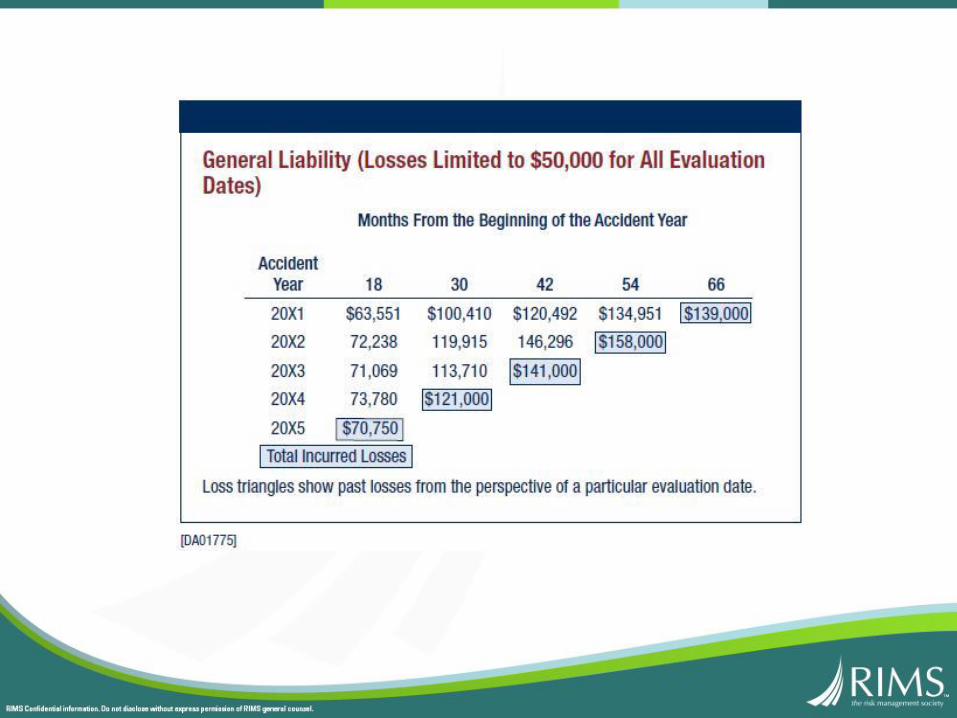

In developing its loss forecast, HCB Company's risk management

professional prepares the following loss triangle:

Months from Beginning of Accident Year

Accident

Year 18 30 42 54 66

20X2 $105,231 $157,003 $176,771 $188,676 $194,678

20X3 $101,137 $165,780 $189,083 $199,440

20X4 $115,781 $178,912 $192,801

20X5 $120,980 $167,413

20X6 $118,605

What is the 30- to 42-month period-to-period loss development factor for

HCB Company for year 20X4?

A: 1.08

B: 1.15

C: 1.43

D: 1.67

Applying Increased Limits Factors

Assume total losses, limited to $100,000 per loss, equal $3,000,000. Based on the factors in the table above, estimated losses limited to $500,000 per loss equal

A. $1,364,000

B. $2,114,000

C. $4,258,000

D. $4,650,000

Probability Interval (of a Total Loss Probability Distribution)

Representation that shows the probability of outcomes falling within certain ranges of a probability distribution. The probability interval is determined by the areas underneath a probability distribution curve.

25

Variation from Expected Losses

26

Assignment 3 – Transferring Hazard Risk Through Insurance

Ideally Insurable Loss Exposure

• Pure risk

• Accidental loss

• Definite in time and measurable

• Large number of similar, independent exposures

• Not simultaneous and not catastrophic

• Economically feasible to insure

Excess Liability Insurance

29

Excess liability insurance is insurance coverage for

losses that exceed the limits of underlying

insurance or a retention amount. It is not an

umbrella and most often takes one of three basic

forms, which are:

• Following form

• Self-contained form

• Combination form

One form of excess liability insurance incorporates

provisions of the underlying policy and then modifies

the provisions with additional conditions or exclusions.

This type of coverage is called

A: A self-contained excess liability policy.

B: An umbrella excess liability policy.

C: A following-form excess liability policy.

D: A combination excess liability policy.

Assignment 5 – Retrospective Rating Plans

32

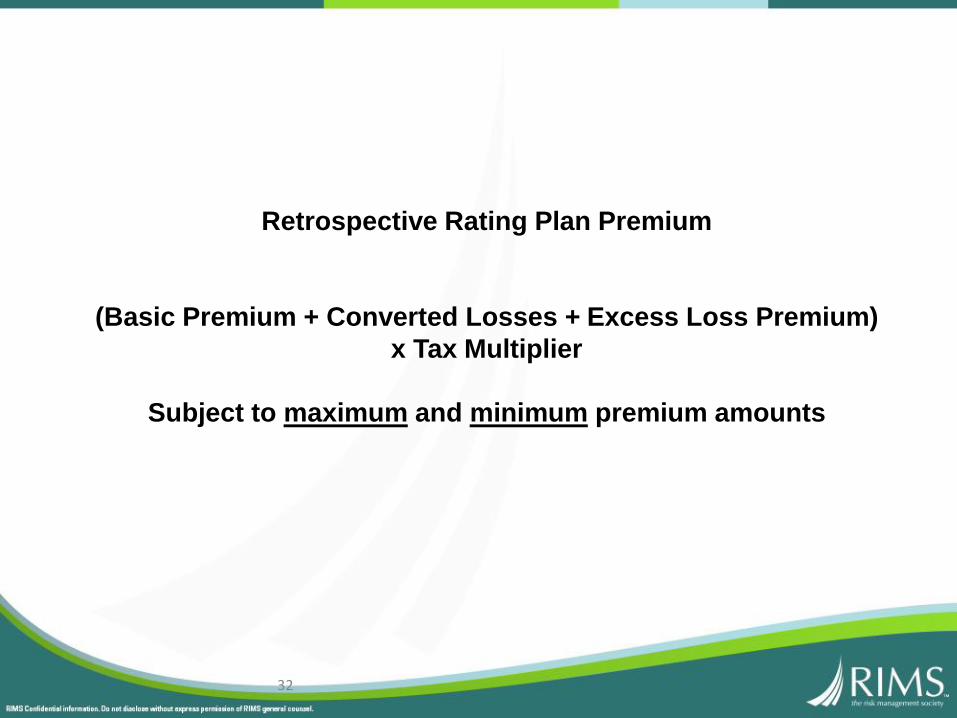

Retrospective Rating Plan Premium

(Basic Premium + Converted Losses + Excess Loss Premium)

x Tax Multiplier

Subject to maximum and minimum premium amounts

Standard premium is calculated by using state rating

classifications and rates, applying them to an insured’s

estimated exposures (for example, sales for a CGL policy or

payroll for workers’ compensation policy) for the policy

period.

1. Basic Premium – covers the insurer acquisition costs, overhead,

and profit. Basic premium is expressed as a percentage of the

standard premium.

33

2. Converted Losses – incurred losses multiplied by a loss

conversion factor, which is a factor used to account for the

unallocated portion of loss adjustment expenses (which

includes, for example, rent for the office space of the claims

department that cannot be allocated to a specific claim.)

3. Excess Loss Premium – compensates the insurer for the risk

that an individual loss will exceed the loss limit, which is the

limit or “cap” on a single loss that the insurer will apply to the

loss when calculating the retrospective premium (that way an

insured is not subject to the maximum premium just because of

a single bad claim when otherwise the loss experience during

the coverage period was good). Excess loss premium is

expressed as a percentage of the standard premium and is

multiplied by the loss conversion factor.

34

4. Tax Multiplier – adds an amount for state premium taxes,

license fees, service bureau charges, and residual market

loadings. It is expressed as a factor that is multiplied by the

other components of the retrospective formula.

5. Maximum Premium – amount that the retrospective rating plan

premium will not exceed. Maximum premium is expressed as a

percentage of the standard premium.

6. Minimum Premium – amount that the retrospective rating plan

premium will not fall below. Minimum premium is expressed as

a percentage of the standard premium.

35

Example of a Retrospective Rating Plan Premium Calculation

Assume that Cranston Manufacturing Company (Cranston) has the following cost factors for its incurred loss retrospective rating plan:

Policy Limit $1,000,000 per occurrenceStandard Premium $700,000Basic Premium 20%Loss Conversion Factor 1.10Loss Limit $500,000 per occurrenceExcess Loss Premium 5%Tax Multiplier 1.04Maximum Premium 150%Minimum Premium 40%

Group 1 - $300,000 incurred losses Group 3 - $700,000 incurred lossesGroup 2 - $400,000 incurred losses Group 4 - $800,000 incurred losses

36

Analysis:

• The basic premium is 20% of the $700,000 standard premium, which is $140,000.

• The excess loss premium is 5% of the $700,000 standard premium, which is $35,000, multiplied by the loss conversion factor of 1.10, for a total of $38,500.

• The maximum premium is 150% of the $700,000 standard premium, which is $1,050,000, and the minimum premium is 40% of the $700,000 standard premium, which is $280,000.

• We now have all we need to determine the retrospective rating plan premium as a function of incurred loss by applying the retrospective rating formula.

[$140,000 + (Level of Incurred Losses x 1.10) + ($35,000 X 1.10)] x 1.04

37

Incurred Losses Premium$ 50,000 $ 280,000 minimum premium applies

100,000 300,040200,000 414,440300,000 528,840400,000 643,240500,000 757,640600,000 872,040700,000 986,440800,000 1,050,000 maximum premium applies

38

39

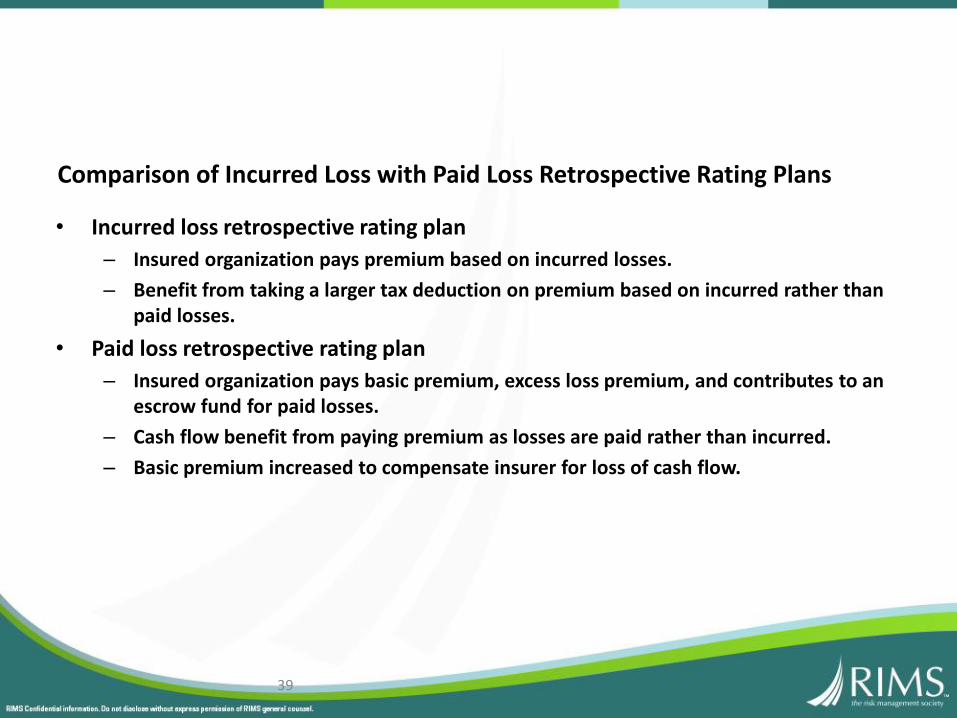

• Incurred loss retrospective rating plan

– Insured organization pays premium based on incurred losses.

– Benefit from taking a larger tax deduction on premium based on incurred rather than paid losses.

• Paid loss retrospective rating plan

– Insured organization pays basic premium, excess loss premium, and contributes to an escrow fund for paid losses.

– Cash flow benefit from paying premium as losses are paid rather than incurred.

– Basic premium increased to compensate insurer for loss of cash flow.

Comparison of Incurred Loss with Paid Loss Retrospective Rating Plans

Assignment 6 – Reinsurance

Reinsurance Functions

41

• Increase large line capacity

• Provide catastrophe protection

• Stabilize loss experience

• Provide surplus relief

• Facilitate withdrawal from a market segment

• Provide underwriting guidance

Surplus Relief• Premium revenue – earned over time

• Acquisition expenses – charged immediately

• For a growing insurance company, mismatch creates a drain on policyholders’ surplus

42

Assets

Liabilities

Surplus+ premium revenue- acquisition expenses (not matched with revenue)

Facilitate Withdrawal From a Market Segment

When withdrawing from a market segment the primary insurer has several options, which include:

43

• Stop selling new policies

• Cancel all policies

• Purchase portfolio reinsurance

Portfolio reinsurance is a reinsurance agreement that reinsures the loss exposures of an entire type of insurance, class of business, or geographic area.

44

Important points to remember:

1. It is an exception to the rule that reinsurers do not accept all the liability for specified loss exposures of a primary insurer.

2. While reinsured, the primary insurer retains direct obligations to insureds (not a novation).

3. Often requires approval from the state insurance department.

Types of Reinsurance

• Facultative

• Treaty

• Pro rata

• Excess of loss

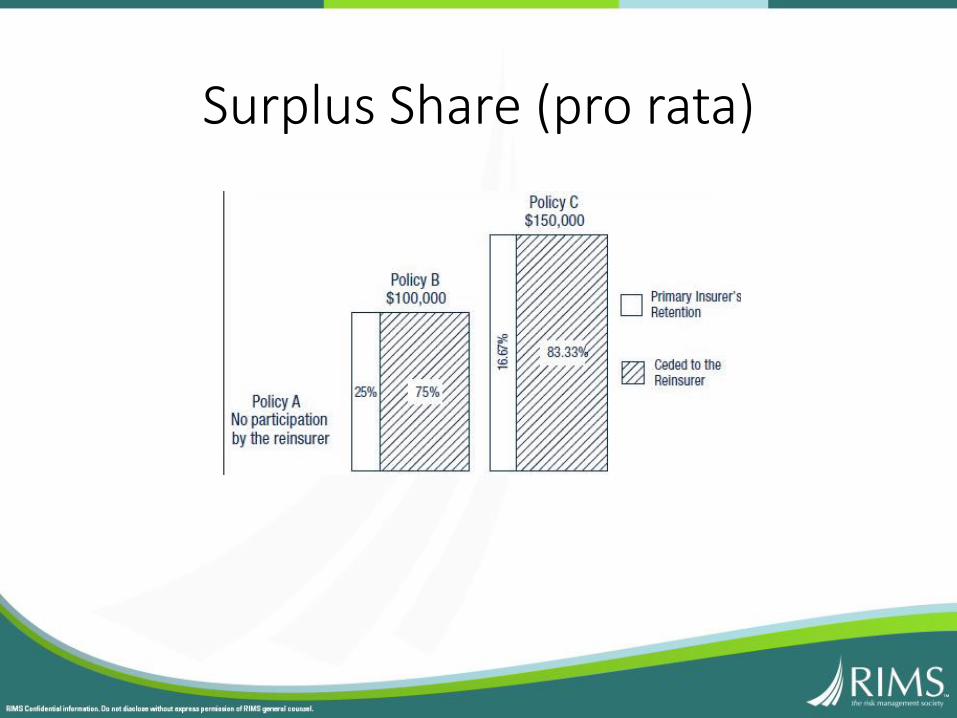

Quota Share (pro rata)

Surplus Share (pro rata)

XYZ Insurance Company has a 9-line surplus share

treaty with a retention $100,000 and a maximum cession

of $900,000. Policy A insures a building for $500,000. If

there is a $50,000 loss under Policy A, how much of it

will XYZ retain?

A: $0

B: $5,000

C: $10,000

D: $50,000

Excess of Loss Reinsurance

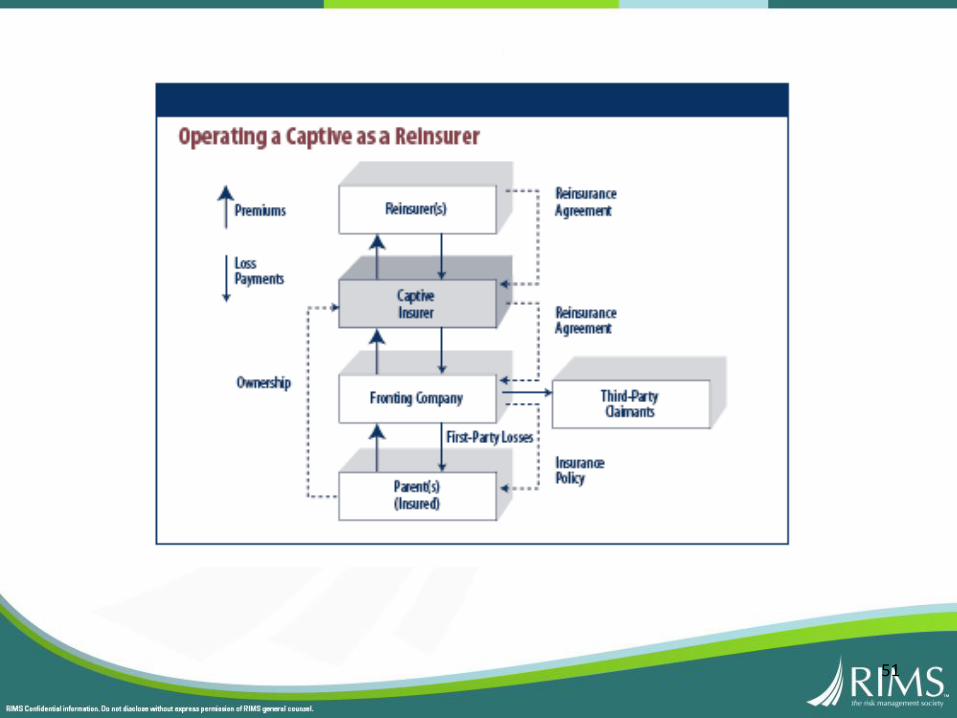

Assignment 7 – Captive Insurance

51

Types of Captives

Single-parent (pure)

• Segregated Cell Captive

Group

• Association captive

• Risk retention group

Rent-a-Captive

Advantages of a Captive

53

1. Reducing the cost of risk

2. Benefiting from cash flow

3. Obtaining insurance not otherwise available

4. Direct access to reinsurers

5. Negotiating with insurers

6. Centralizing loss retention

7. Tax advantages

8. Controlling losses

9. Obtaining rate equity

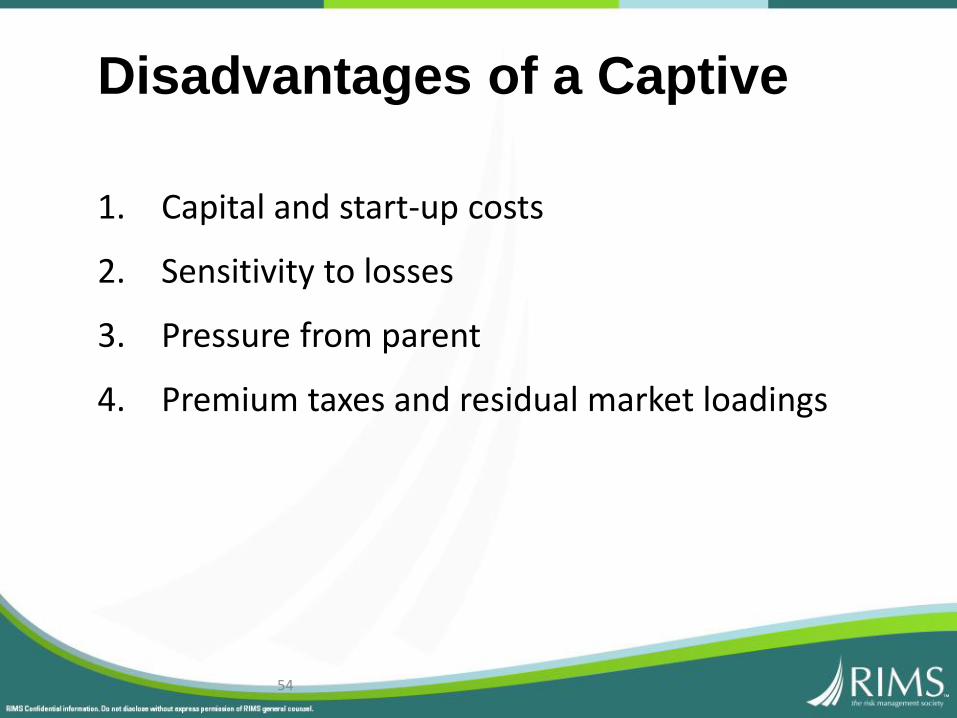

Disadvantages of a Captive

1. Capital and start-up costs

2. Sensitivity to losses

3. Pressure from parent

4. Premium taxes and residual market loadings

54

For which one of the following types of captives must the owners be from the same industry?

A. Group captive

B. Protected cell captive

C. Rent-a-captive

D. Risk Retention Group

Assignment 9 – Transferring Financial Risk

Types of Financial Risk

• Market Risk• Interest rate risk

• Exchange rate risk

• Liquidity risk

• Credit Risk

• Price Risk

Derivatives

• Forward contracts

• Options

• Swaps

Which one of the following gives the holder the right to buy or sell an asset for a specific price?

A. Forward

B. Option

C. Security

D. Swap

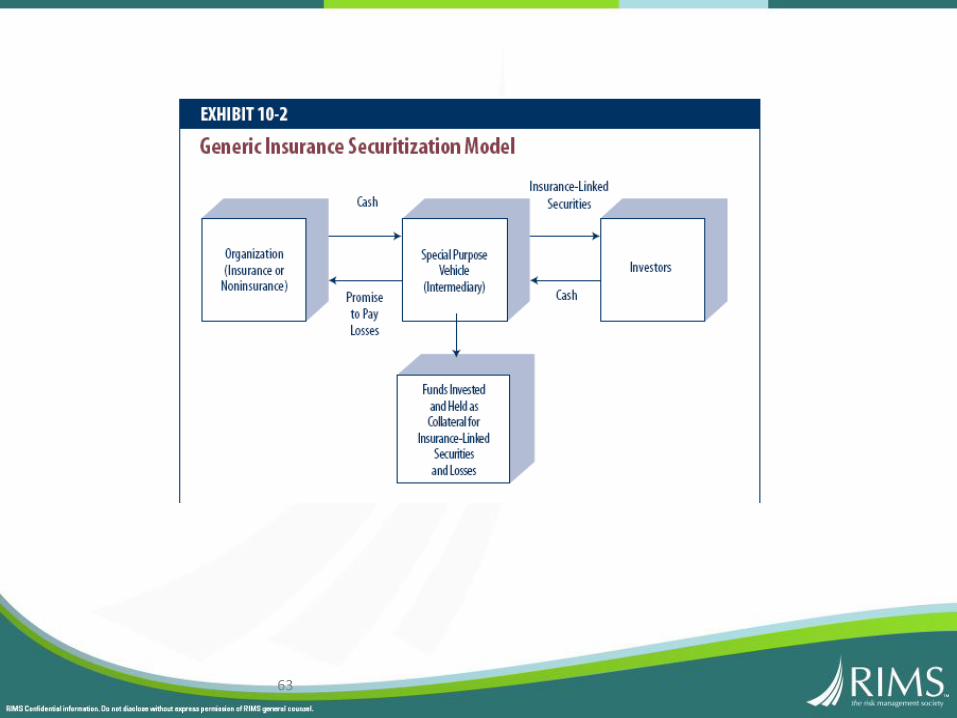

Securitization

With a securitization, income-producing assets, such as mortgage receivables, are transferred to a special purpose vehicle (SPV) in exchange for cash. These assets are

A. Converted into forward contracts.

B. Sold to investors.

C. Traded on an open exchange.

D. Used to collateralize securities sold to investors.

Assignment 10 – Transferring Hazard Risk to the Financial Markets

63

With an insurance securitization, the special purpose vehicle (SPV) is often called a transformer because it tranforms

A. A loss index into indemnity.

B. Cash into securities.

C. Insurable risk into investment risk.

D. Primary insurance into reinsurance.

Standby credit is an arrangement whereby a bank or another financial institution agrees to provide a loan to an organization in the event the organization suffers a loss.

Contingent surplus notes are surplus notes that have been designed so that an insurer, at its option, can immediately obtain funds by issuing surplus notes at a pre-arranged rate of interest.

Catastrophe equity puts are rights to sell equity (stock) at a predetermine price in the event of a catastrophic loss.

65

Contingent Capital

Assignment 11 – Allocating Costs of Managing Hazard Risk

Allocating risk management costs...

67

1. Costs of accidental losses not reimbursed by insurance or

other outside sources

2. Insurance premiums

3. Costs of risk control techniques

4. Costs of administering risk management activities

1. Incurred loss basis – keep track of incurred losses, just as an insurance company would; including IBNR

2. Claims-made basis – keep track of losses for claims made, just as an insurance company would; does not include IBNR

3. Claims-paid basis – keep track of amounts paid on losses during the accounting period, regardless of when the losses occurred

68

69

Prospective cost allocation – cost fixed at beginning of

accounting period

Retrospective cost allocation – cost estimated at beginning of

accounting period an adjusted as loss costs are known

Q & A

73

EO 6.04 – Describe the administration of retrospective rating plans.

74

• Collateral requirements for paid loss retrospective rating plans

• For financial accounting purposes an organization must recognize its

retained losses as they are incurred.

• The additional premium owed (as determined by the retrospective

rating formula) must be recognized as a liability on the organization’s

next balance sheet and as an expense on the organization’s next

income statement.

• With a paid loss retrospective rating plan, premium payments are

based on when losses are paid, not when they are incurred. But for

financial accounting purposes, an organization must recognize

additional premium owed when the losses are incurred, not when they

are paid.

• Incurred but not reported (IBNR) losses must also be recognized if they

can be estimated with reasonable accuracy.

EO 9.02 – Explain how finite risk insurance plans operate, including:

75

• Types of risks covered

• Experience fund terms and calculation guidelines

• Variations in the terms of plans

Common Characteristics of Finite Risk Plans

• The limits of coverage apply on an aggregate basis.

• The term of coverage is usually for five to ten years.

• The premium is usually 50% or more of the policy limits.

• The insurer shares profit with the insured, including investment

income.

• The insured is allowed to commute the policy.

Types of Risk Covered

1. Underwriting risk is the risk that an insurer’s losses and expenses will be greater than the premiums and the investment income it expects to earn under the insurance contract.

2. Investment risk is the risk that an insurer’s investment income will be lower than it expects and includes timing risk and interest rate risk.• Timing risk is the risk, under an insurance contract, that the insured’s

losses will be paid faster or more slowly than expected.

• Interest rate risk is the risk that interest rates will be below the expected rate during the term of the insurance contract.

3. Credit risk is the risk that an insurer will not collect the premiums owed by its insured.

76

Prospective versus Retroactive Plans

Prospective plan is a risk financing plan arranged to cover losses from events that have not yet occurred

Retroactive plan is a risk financing plan arranged to cover losses from events that have already occurred

77

Loss Portfolio Transfers

Loss portfolio transfer is a type of retroactive plan that applies to an entire portfolio of losses. The losses usually have established reserves, but uncertainty exists as to the timing of the loss payments and the potential for further loss development.

78

Important Definitions

EO 10.06 – Analyze the concerns of organizations transferring risk and investors supplying capital.

79

• Financial security of the parties supplying the risk capital (the credit risk).

• Basis risk: the risk that the amount an organization receives to offset its losses might be greater than or less than its actual losses.

EO 13.05 – Describe the practical considerations of selecting a cost allocation basis.

80

An organization’s accounting system can influence allocation.

An organization’s operations may be subject to more than one tax system.

Each department should be charged at least a minimum amount for risk management services regardless of exposure or loss experience.

If an organization is highly decentralized, each department may be purchasing its own insurance.

Cost allocation should penalize or reward each department according to its risk management costs.

Use of computerized risk management information systems (RMIS) has become standard in many industries.

Cost allocation systems should remain as consistent as possible from year to year.

![Rajiv Gandhi Institute of Medical Sciences [RIMS ...rimsadilabad.com/RIMS ADILABAD Foundation_course_ 2019-20 with... · Rajiv Gandhi Institute of Medical Sciences [RIMS], Adilabad,](https://img.dokumen.tips/doc/110x75/602572653bb0fd788643171d/rajiv-gandhi-institute-of-medical-sciences-rims-adilabad-foundationcourse.jpg)