Embed Size (px)

Citation preview

Argentina, the Road to 2011:Economic and Political Outlook

Fernando Straface, Executive Director

Lucio Castro,

Director,

International Economics Program

Av. Callao 25, 1° • C1022AAA Buenos Aires, Argentina - Tel: (54 11) 4384-9009 • Fax: (54 11) 4371-1221 • [email protected] • www.cippec.org

AS/COA

New York, April 28, 2010

The leading Think Tank in Argentina, andtop five in Latin America (Foreign Policy)

We conduct high-quality, independent research in all public policy areas

We analyze current public policy events, but with a long run perspective

High impact and agenda-setting capacity

We understand the politics behind the public policies

Key metrics of CIPPEC

Staff of 90; Budget of USD 2.5 million(2009)

Diversified sources of funding

Strong media presence:

1,416 mentions in national media(2009).

455 articles citing or featuringCIPPEC in national newspapers(2009).

40 articles in international media inthe same year (5 from BBC, 4 fromThe Economist, 2 from the NYT, 2from CNN).

47%

23%

17%

13%

Funding sources in 2009 (in %)

International cooperation Governments

Private companies Individuals

Source: CIPPEC

A Long term perspectiveThe last 20 years have not been lost

80

130

180

230

280

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

PPP-Based GDP Index 1990 - 20091990 = 100

Argentina Brazil Chile Peru Uruguay

Source: CIPPEC based on IMF (2010).

The fiscal front: a problem, not a crisis

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

2005 2006 2007 2008 2009 2010* 2011*

Federal Goverment Primary Expenditures

a share of GDP2009 - 2011

Wages & Salaries Current transfers to the Private sectorCurrent transfers to Provinces Other expenditures

0,50%0,39% 0,92% 1,77%

0,72%3,27%

3,83%2,90%

3,25%4,73%

4,51%5,82%

7,47%8,27%

0,11%0,39%

0,32%0,64% 1,20%

2,80%2,09%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

2005 2006 2007 2008 2009 2010* 2011*

Federal Goverment revenues as a share of GDP

2009 - 2011

Domestic taxes Export Taxes Contrib. to Social Security

Property Income Taxes Other revenue

Source: CIPPEC based on MECON and private sources.

Inflation tax

SSS transfers

6,1%

28,6%

23,2%

13,6%

25,0%

13,9%

3,3%

32,7%

25,9%

22,9%

33,3%

18,9%

0%

5%

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 2010* 2011*

Y.o.y Federal Goverment Real Revenues and Primary

Expenditures Growth Rates2006 - 2011

Revenues Primary Expenditures

Source: CIPPEC based on MECON and private sources.

Fiscal deficit is likely to remain small in 2010-2011

Recent Kirchner’s policies (inflation financing and stock confiscation) are no longer an option

Using FX reserves is also costly politically

BUT domestic financing via a bond to local banks is available

Plus, the debt restructuring might open the way to a limited return to international markets

The fiscal front: a problem, not a crisis (II)

-1,50%

-1,00%

-0,50%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

2007 2008 2009 2010* 2011*

Primary fiscal surplus needed to face the sovereign debt 2010 - 2011

Baseline

Scenario I - successful debt restructuring

Scenario II - GDP growth 5.6% in 2010 and 3.5% and 2011Scenario III - GDP growth 4% in 2010 and 2.8% in 2011Scenario IV - Inflation rate

The fiscal front: a problem, not a crisis (III)

Bye, bye stop and go?The soybean´s dollars rainfall

30

40

50

60

70

80

90

100

110

120

100

200

300

400

500

600

700

20

08

/0

9

20

09

/1

0

20

10

/1

1

20

11

/1

2

20

12

/1

3

20

13

/1

4

20

14

/1

5

20

15

/1

6

20

16

/1

7

20

17

/1

8

20

18

/1

9

20

19

/2

0

Th

ou

sa

nd

m

etr

ic t

on

es

Mil

lio

n m

etr

ic t

on

es

Agricultural production long term projections 2008-2020

Beef Total crops

Source: own calculations based on USDA (2010)

-6.000

-1.000

4.000

9.000

14.000

19.000

24.000

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

*

Tra

de

su

rplu

s

Ex

po

rts a

nd

im

po

rts

Exports, imports and trade surplus (in u$s millions)

Trade Surplus Exports Imports

Source: CIPPEC based on INDEC and private estimatesSource: Own calculations based on USDA 2010

Out of the woodsThe end of the recession

Labor demand index

Source: CIF-UDT (2010)

Accelerating inflationwith unanchored expectations

Source: own calculations based on non-audited provincial statistical offices

Inflation expectations

in the next 12 months (national)

Source: CIF-UTDT (March, 2010)

April 10Media: 30%

Median: 31%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

en

e-0

7

ab

r-0

7

jul-

07

oct-

07

en

e-0

8

ab

r-0

8

jul-

08

oct-

08

en

e-0

9

ab

r-0

9

jul-

09

oct-

09

en

e-1

0

y.o

.y in

fla

tio

n r

ate

m.o

.m i

nfl

ati

on

ra

te (

%)

Monthly and annualized inflation rates (%)

m.o.m y.o.y

Expected nominal depreciation for 2010 is 10%/12%

With a 25% inflation rate, the AR $ will inevitably appreciate in real terms

Inflation differential with and devaluation of main trading partners are the other drivers

Exchange appreciation could be a concern in 2011

Looking for a nominal anchorThe road to FX real appreciation?

Real Multilateral Exchange Rate Index2001=1

Source: Analytica (2010)

Jan-Oct. variation

US BRASIL EU CHINA RMER

An impossible mission? The road to lower inflation in 2011

0,0

5,0

10,0

15,0

20,0

25,0

-3 -2 -1 0 1 2 3 4 5 6

y.o

.y in

fla

tio

n r

ate

Years before and after stabilization

Dinflation. The Emerging Markets Experience

Peg Non-Peg

The region shows that monetary policy works:

Inflation targeting and restoring CB and INDEC credibility are the road to follow.

A drastic fiscal adjustment is no needed.

Slowdown of public expenditure growth rate.

Reduce subsidies along with a social tariff and VAT for “poor-goods”.

Coordinate expectations. Source: CIPPEC based on IMF/WEO (2010)

Disinflation: the Emerging Markets Experience

In the best of the worlds?Favourable TOT and rapid growth in main trade partners

100

150

200

250

300

350

400

18

10

18

20

18

30

18

40

18

50

18

60

18

70

18

80

18

90

19

00

19

10

19

20

19

30

19

40

19

50

19

60

19

70

19

80

19

90

20

00

Terms of Trade 1810 - 2008Long term trend and average

1810 = 100

Long term trend Average

Source: own calculations based on INDEC and Ferreres (2006)

0

50

100

150

200

250

300

350

400

450

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

15

20

20

Commodities prices in constant USD 1990 - 2020

Corn Soybeans Wheat

Source: CIPPEC based on USDA and World Bank projections

A promissing future (if we get to 2011 relatively unharmed)

Relatively low Debt/GDP, mostly in local currency and with a comfortable payments profile

Still manageable fiscal situation

Trading partners growing at high rates in the long term; very favorable terms of trade

Confidence deficit could be relatively easy to reverse with reasonable macro policies.

The beginning of an investment boom?

Now, the politics…

Growing dissatisfaction with the Government

3328

74

49 64

27

4134

27

6265

18

40

23

68 5462

70

-40

-20

0

20

40

60

80

100

M A O N J F M J A O N D J F M A M J J A S O N D JF M A M J J A S O N D J F M

2006 2007 2008 2009 2010

%

Diff. (+) (-) Approve Disapprove

Presidential approval

Source: Poliarquía Consultores

Conflict with theagricultural sector

Lost in mid-termelections

Government has lost popular support since March 08

Mid-term elections reinforced Government’s alienation

Policy challenges are of medium complexity,

but the current political climate is

tense:

0

10

20

30

40

50

60

70

80

90

MAONEFMJAONDEFMAMJ JA SONDEFMAM J JASONDEFM

2006 2007 2008 2009 10

%

M ejoró Se mantuvo igual Empeoró

Source: Poliarquía Consultores

Perceptions on inflation have worsened

Improved Stayed the same Worsened

0

10

20

30

40

50

60

70

80

90

MAONEFM JAONDEFMAM J JA SONDEFMAMJ JA SONDEFM

2006 2007 2008 2009 10

%

M ejoró Se mantuvo igual Empeoró

Source: Poliarquía Consultores

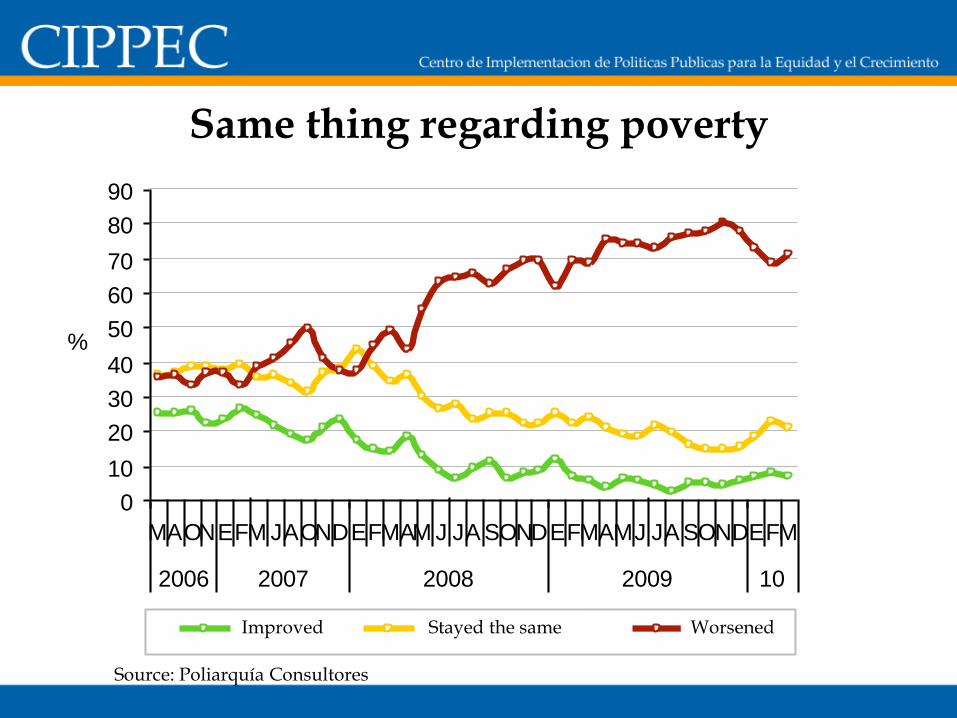

Same thing regarding poverty

Improved Stayed the same Worsened

0

10

20

30

40

50

60

70

80

90

MAONEFM JAONDEFMAM J JASONDEFMAM J JA SONDEFM

2006 2007 2008 2009 10

%

M ejoró Se mantuvo igual Empeoró

Source: Poliarquía Consultores

…and corruption

WorsenedStayed the sameImproved

Politics affect the policy agenda

Stalemate in Congress since December 10th, specially in the Senate

Unstable, minimal coalitions, defined in a bill-by-bill basis

Government is willing to raise the stakes against a renewed but fragmented opposition

No willingness to promote political dialogue: paralysis and legislative deadlock

Political crisis without governability crisis

Low chances of change of direction until the next presidential election

How the presidential election looks today?

0

10

20

30

40

50

60

Positive and negative image of potential candidates

Positive

Negative

Source: Poliarquía Consultores

The candidates’ political compassState-oriented

Market-oriented

Confrontational style

Cooperative style

Néstor

Kirchner

Solanas

Carrió

Alfonsín

de Narváez / Scioli Macri/

Reutemann

CobosDuhalde

Source: Poliarquía Consultores and CIPPEC

Political outlook, 2010-2011

Until next presidential elections, the political arena will focus on:

Inflationary pressures

International isolation

Confrontational dynamics in the domestic front

In short

Argentina continues to enjoy an extremely favorable international economic context

Policy challenges show some complexity, but not as dramatic as those of 1989-1990 or 2001-2002

Politics will be fluid until Presidential elections, but a major crisis is unlikely

Growing negative consensus among opposition forces to avoid the continuation of “bad policies”

Contact Info

Fernando Straface

Executive Director

Lucio Castro

Director,

International Economics Program